Abstract

Maritime insurance developed in medieval Europe is the ancestor of all forms of insurance that appeared subsequently. We address the question of why modern insurance was first invented in medieval Europe, and neither earlier nor elsewhere. Drawing from insights from the literature on uncertainty aversion, we show that medieval merchants had to bear more frequently natural risks (they traveled longer distances) and new human risks with unknown probabilities (they faced unpredictable attacks by corsairs due to increased political fragmentation and commercial competition in Europe). The increased demand for protection in medieval seaborne trade met the supply of protection by a small group of wealthy merchants with a broad information network who could pool risks and profit from selling protection through a novel business device: the insurance contract. A new market—the market for insurance—was then born. Next, analyzing more than 7,000 insurance contracts redacted by notaries and about 100 court proceedings housed in the archives of Barcelona, Florence, Genoa, Palermo, Prato, and Venice, we study the main features of medieval trade, the type of risks faced by merchants, and the characteristics of insurance contracts and markets from 1340 to 1500.The empirical analysis delivers two main findings. First, risks related to human activities (e.g., attacks by corsairs) seem to have had a relatively greater impact on insurance premia compared to natural risks (proxied by seasonal risks). Second, distance mattered but the route seems to have had a greater impact on insurance premia. Specific routes (e.g., in the Tyrrhenian and the western Mediterranean) were more plagued by human risks, which were harder to avoid for the majority of merchants who did not have a broad information network compared to the few wealthy merchants, who became the key players in selling insurance in the early stages of the development of insurance markets.

A set of Teaching Slides to accompany this article is available online as Supplementary Data.

1. Introduction

Nowadays, insurance contracts are pervasive and represent one of the pillars for coping with myriad economic, financial, environmental, health, and technological risks including the ones brought by the fast-growing high-tech sector. In 2022, insurance premia worldwide amounted to more than the combined GDPs of France, Italy, and Spain.

Yet, centuries ago societies lived without any insurance. When, where, and why was insurance invented? Well before the concept of probability became formalized in the 16th and 17th centuries, medieval merchants in Europe understood how to pool risks in addressing new and unknown risks through the invention of insurance. The origins of insurance contracts and markets can be traced back to the mid-14th century when Italian merchants introduced these contracts to protect their short- and long-distance maritime trading activities spanning from the North Sea all the way to the Middle East.

We address the question of why modern insurance was first invented in medieval Europe, and neither earlier nor elsewhere. Drawing from the theoretical insights from the literature on risk and uncertainty aversion, we show that medieval merchants had to bear more frequently natural risks (they traveled longer distances and all year round) and new human risks with unknown probabilities (they faced unpredictable attacks by corsairs due to increased political fragmentation and commercial competition in Europe). The increased demand for protection in medieval seaborne trade met the supply of protection by a small group of wealthy merchants with a broad information network, who could pool risks and profit from selling protection through a novel business device: the insurance contract. A new market—the market for insurance—was then born in the mid-14th century.

Next, we study the main features of medieval trade, the types of risks faced by merchants, and the characteristics of insurance contracts and markets from 1340 to 1500 through the analysis of more than seven thousand insurance contracts redacted by notaries and about one hundred court proceedings housed in the archives of Barcelona, Florence, Genoa, Palermo, Prato, and Venice. The empirical analysis delivers two main findings that are consistent with the predictions of our conceptual framework. First, risks related to human activities (e.g., attacks by corsairs, warfare) seem to have had a relatively greater impact on insurance premia compared to natural risks (proxied by seasonal risks). Second, distance mattered but the route seems to have had a greater impact on insurance premia. Longer routes potentially increased the probability of losses from natural risks; however, these risks were mostly avoidable by choosing longer but safer routes. In contrast, regardless of distance, specific routes (e.g., in the Tyrrhenian and the western Mediterranean) were more plagued by human risks (e.g., attacks by corsairs) which were harder to avoid for the majority of sedentary merchants; these merchants did not have a broad information network compared to the few wealthy merchants, who became the key players in pooling risks and selling insurance in the early stages of the development of insurance markets.

The main contribution of the article lies in the approach we take to study the rise of insurance in medieval times. To the best of our knowledge, we are the first to develop a conceptual framework with uncertainty aversion to explain the rise and development of insurance in medieval Europe, and to empirically analyze the characteristics of maritime insurance markets as well as the determinants of risk premia in medieval times. The empirical analysis enables us to disentangle the correlation between the different types of risks faced by medieval merchants and the insurance premia. Finally, we exploit geographical network representations to visualize the extension of medieval seaborne trade and of insurance markets.

Our work contributes to the theoretical and empirical literature on insurance and on the theoretical literature on uncertainty aversion.1,2 We then bring insights for the literature that analyzes the interactions between institutions and long-run economic development.3 Finally, our article contributes to the historical literature that studies the Commercial Revolution and the growth of trade in medieval Europe.4

The article is organized as follows. Section 2 presents the historical context in which insurance contracts and markets emerged in medieval Italy. The Commercial Revolution witnessed major progresses in nautical technologies and techniques and the introduction of freight rates differentiated by type of good. These innovations contributed to the decline of ground transportation and the blossoming of maritime shipping, even for goods with low value. Insurance contracts appeared first in Genoa and Florence around the mid-14th century. In Genoa, insurance contracts were first disguised as a way to avoid charges of usury. Initially, an insurance contract was drawn up as mutuum, a fictitious sea loan resembling the foenus nauticum used in ancient times—a loan to be repaid only in the case of safe arrival of the shipment. Then, during the 14th century, the insurance contract took the form of a fictitious sale contract, and only in the 15th century became openly written as an insurance contract. Meanwhile, insurance contracts developed in Florence during the mid-14th century without the need of disguising them under fictitious sale contracts. From Florence and Genoa, insurance contracts spread to other commercial centers in the Mediterranean, such as Palermo, Barcelona, and later Venice.

Two key historical facts must be kept in mind to understand the context in which maritime insurance contracts and markets developed. First, thanks to major progresses in nautical technologies and techniques that punctuated the Commercial Revolution, maritime commerce took place over longer distances and all year round, whereas trade in the Mediterranean during ancient times typically occurred along the coasts and during the safer summer season. Traveling longer distances and all year round entailed having to cope more frequently with natural risks (e.g., thunderstorms). Second, starting from the late 13th and early 14th centuries, corsairs began disrupting trade routes in the Mediterranean, especially the ones along the Italian and Spanish coasts. Unlike pirates who disrupted seaborne trade since antiquity, corsairs were private citizens hired by governments and states to damage commercial competitors. Their presence and the way they conducted their business created previously unknown and much unpredictable risks to merchants who had to cope with a new type of uncertainty.

In Section 3, we describe a conceptual framework that shows under which conditions uncertainty averse and risk averse merchants invent and employ insurance contracts to cope with previously unknown risks. The main predictions are as follows. First, new risks with unknown probabilities (e.g., human risks like attacks from corsairs) make the uncertainty averse merchant willing to buy more protection to reduce these risks. The information asymmetry with the insurer knowing the “true” probability of human risks (e.g., attacks by corsairs) thanks to his broad information network makes the newly invented insurance contract profitable for the supply side who can pool risks. Hence, insurance contracts and markets arise. Second, human risks (with unknown probabilities) should have a relatively larger effect on insurance premia compared to natural risks (with known probabilities). Third, ceteris paribus, the higher the human risks (e.g., attacks by corsairs and warfare), the higher the insurance premium. Any mechanisms that mitigate human risks (e.g., shipping the merchandise on an armed galley), reduce the insurance premium.

Section 4 presents our novel dataset consisting of insurance contracts and court records from previously unexplored archival sources. We analyze about 7,000 insurance contracts we found in notarial deeds housed at the archives of Barcelona, Florence, Genoa, Palermo, Prato, and Venice and 104 court records from the merchants’ court at the State Archives of Florence. The contracts and court records date between 1343 and 1506. Most contracts report information about the goods shipped, the vessels used and the routes of the shipments, which we can use to compute the distance traveled and to build the network representation of the shipments. All contracts list the parties involved and the total amount insured. A subset of these contracts report the insurance premium percentages, which range from 0.75% to 22%.

Section 5 presents the main findings of the empirical analysis. First, we document and discuss the extent of maritime commerce in the Middle Ages showing that our dataset well represents the patterns of medieval trade that historians have described. Thanks to the details contained in each contract, we can investigate the routes of commerce and its seasonality, as well as the goods shipped on such routes, and the vessels used. Second, we describe the structure of the insurance market in the first century and a half following its rise. The main finding is that in the early stages of the development of insurance markets, a small group of wealthy merchants supplied most of the insurance contracts and were the key players in these markets. Once it was clear that insurance could be a profitable business, more and more merchants began participating not only on the demand side as they had done earlier, but also on the supply side.

Lastly, we analyze and identify the main variables correlated to the insurance premium that was the pivotal feature connected with the rise of insurance. We find that risks related to human activities (e.g., attacks by corsairs, warfare) seem to have had a relatively greater impact on insurance premia compared to natural risks (proxied by seasonal risks). Second, distance mattered but the route seems to have had a greater impact on insurance premia. Longer routes potentially increased the probability of losses from natural risks, but these risks were mostly avoidable by choosing longer but safer routes. In contrast, regardless of distance, specific routes (e.g., in the Tyrrhenian and the western Mediterranean) were more plagued by human risks (e.g., attacks by corsairs), which were harder to avoid for the majority of merchants who did not have a broad information network compared to the few wealthy merchants, who became the key players in pooling risks and selling insurance in the early stages of the development of insurance markets. These findings are consistent with the predictions of the conceptual framework we develop to study the invention of insurance in medieval times.

2. Historical Context

2.1. Trade in Antiquity

2.1.1. Natural Risks

Long-distance trade played a major role in the economic exchanges that took place between the major centers of civilization in Europe and Asia during antiquity.5 Merchants transferred raw materials, foodstuffs, and luxury goods through trade routes that connected locations over vast distances. A lot of goods and merchandise were transported across locations by pack animals overland. While natural phenomena (e.g., a thunderstorm, a fire) could damage the merchandise carried overland, ground transportation created relatively modest natural risks, that is, risks generated by natural phenomena.

The other way of transporting commodities across locations was seaborne trade employing seagoing ships. While transporting merchandise using seagoing ships would make possible to ship larger quantities and in shorter times with respect to overland transportation, seaborne transportation posed several challenges. The lack of instrumentation for measuring position accurately would increase the risk of getting lost offshore or ending up in a destination different from the one intended. Winds varying along the same route and according to the season affected traveling times and generated the risk of a shipwreck. A thunderstorm hitting a vessel in the middle of the Mediterranean or the North Sea was a potentially more damaging natural phenomenon than a thunderstorm overland. To minimize risks coming from natural phenomena, seaborne trade typically occurred along the coasts (making the journey longer but safer), and avoiding winter navigation (reducing business and earning opportunities but, again, making the voyage safer). A clear trade-off emerged between the duration and the riskiness of journeys oversea, as shown in the example in Table 1. Merchants could choose a direct and shorter route when traveling from Alexandria in Egypt to the island of Rhodes (route no. 1,350 nautical miles), which would take only 5 days of navigation but facing dangerous North–West winds, or they could take a longer route (route no. 4,800 nautical miles) by navigating along the coasts from Egypt, the Land of Israel, Syria, Turkey, Greece, and finally the island of Rhodes, which was not plagued by dangerous winds but clearly took twice the number of days with respect to route no. 1.

Travel times from Alexandria to Rhodes.

| Route (summer) | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Distance (n.m.) | 350 | 500 | 750 | 800 |

| Dangerous winds | yes | partly | no | no |

| Time in days | 5 | 6 | 9 | 10 |

| Route (summer) | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Distance (n.m.) | 350 | 500 | 750 | 800 |

| Dangerous winds | yes | partly | no | no |

| Time in days | 5 | 6 | 9 | 10 |

Source: De Graauw (2022).

Travel times from Alexandria to Rhodes.

| Route (summer) | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Distance (n.m.) | 350 | 500 | 750 | 800 |

| Dangerous winds | yes | partly | no | no |

| Time in days | 5 | 6 | 9 | 10 |

| Route (summer) | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Distance (n.m.) | 350 | 500 | 750 | 800 |

| Dangerous winds | yes | partly | no | no |

| Time in days | 5 | 6 | 9 | 10 |

Source: De Graauw (2022).

Hence, ancient merchants traveling on seagoing ships had ways to minimize the probability of shipwrecks due to natural phenomena (i.e., the probability of natural risks) by traveling along the coasts and/or avoiding winter navigation.

2.1.2. Human Risks

In ancient economies, risks related to local or long-distance trade were not just the outcome of natural phenomena. Risks while transporting commodities overland or oversea could emerge as the outcome of human activities such as theft, carelessness in handling commodities during the loading and unloading operations, and commercial wars or political conflicts among cities, states, or empires.

Yet, with property rights on land being clearly defined and with any given location being under a political ruling power, merchants could “purchase” protection for their merchandise (and for themselves) through military protection provided by their own rulers, and/or paying tolls or taxes to their own rulers or the rulers of the foreign territories through which they traveled. Either mechanism for buying protection would reduce or minimize the risks generated by human activities.

In the case of seaborne trade, however, merchants could not “purchase” the same protection from local or foreign rulers because there were no enforceable property rights over the seas—no state or empire owned, say, the North Sea or the Mediterranean. In antiquity, attacks by pirates were the main sources of human risks for seaborne trade. Although pirates posed a potential threat to trade and increased the probability of human risks that could damage trading activities, their attacks were not so frequent. When their attacks occasionally became frequent and posed a major threat, for example, in the Mediterranean in classical antiquity, the Roman fleet took care of “cleaning” the Mediterranean from the attacks of pirates.

2.2 Medieval Trade

2.2.1 Natural Risks

During the 11th–13th centuries, the so-called Commercial Revolution brought a number of major demographic, economic, and institutional changes that profoundly shaped European economies and societies in the subsequent centuries (Lopez 1976). Many business practices and tools that we commonly use today, like the cheque, or modern double-entry bookkeeping, were developed in medieval times in the commercial centers that emerged with the re-birth of towns and the revival of long-distance trade after the so-called Dark Ages that had followed the collapse of the Roman Empire.

Gradually, (less risky) ground transportation over long distances declined as the need of transporting larger and larger quantities of commodities to the growing populations in the newly established urban centers made overland trade less feasible and more costly. More and more commodities required to be shipped on seagoing ships, increasing the demand for seaborne transportation. Simultaneously, major nautical progress (e.g., pivoted compass, portolan sailing charts, and triremes galleys) made seaborne trade potentially more profitable because these advancements made possible to travel longer distances and during the whole year including the winter, unlike in the past. However, longer routes and all-year-round journeys exposed merchants to higher probabilities of having their merchandise damaged by natural risks. For example, making a longer journey increased the probability of encountering dangerous winds or threatening thunderstorms. Yet, after shipping merchandise using the same route (even if a longer and potentially more dangerous route), merchants could assess the riskiness of a journey along that route due to natural phenomena (e.g., they would learn where the marine currents were more dangerous or in which directions winds were blowing when going, say, eastward or coming back, say, southward).

2.2.2 Human Risks

During the 13th–15th centuries, in a politically fragmented Europe, cities and states (e.g., Catalonia against Genoa, France against England) competed for the control of maritime commercial routes. The novelty with respect to the past is that cities and states that were also commercial powers, began employing corsairs (privateers) to commercially and economically damage their competitors. Corsairs were private citizens, who organized a military expedition oversea and engaged in an undeclared war (the so-called guerra di corsa) on behalf of one of the commercial powers. Unlike pirates who attacked any vessels and were considered thieves to be prosecuted, corsairs were formally authorized by states or cities to assault shipments of their competitors. Corsairs pursued two goals: (i) economically damage the commercial competitors of the state that had hired the corsairs, and (ii) personally profit from the military enterprise by confiscating (and then selling) the merchandise on the vessels that they had attacked.

The threat posed by corsairs to seaborne trade grew particularly during the 14th and 15th centuries and became the major human risk, that is, the major risk related to human activities, as the following three quotes (among the many available) document:

“Tutto il mare è pieno di chorsali.”

(The entire [Mediterranean] sea is full of corsairs).

wrote a Florentine merchant in Genoa on the 2nd of June 1385 in a letter to a fellow merchant.

“Chatalani e Genoessi rubano l’un a l’altro in mare.”

(Catalans and Genoese steal from each other in seaborne trade).

wrote in the late 14th century Gaspare Bechalla from Genoa, who was one of the managers in Barcelona of the richest Tuscan merchant Francesco Datini.

“Great robberies occurred over the seas between the Catalans and the citizens of Genoa. [...] The practice [of stealing from each other] had become so widespread among the said nations that it resembled a war.” 6

wrote a merchant from Barcelona at the end of the 14th century.

2.2.3 The Invention of Insurance Contracts in Medieval Italy

In the medieval economy described above, the demand for “protection” from merchants against both natural and human risks that could damage the blossoming seaborne trade, greatly increased. The invention of insurance contracts occurred in this historical context.

It is not easy to precisely pin down the origins of the new contract. As De Roover (1945) noted, “the problem of the origins of marine insurance is one of the most complicated and controversial questions in the history of business institutions.” In fact, there is no agreement among historians and jurists on the relationship elapsing between the foenus nauticum of Greek and Roman derivation, and the development of marine insurance in the Middle Ages.7

In ancient times, proto-insurance contracts emerged as extensions of sea loans, such as the foenus nauticum (Hoover 1926; De Lara 2008). These contracts provided an amount of money to be lent to a merchant, who would repay this sum, plus an interest payment, conditionally on the safe arrival and success of the expedition. Already in 12th century Genoa, the portion of the sea loan contract dealing with insurance had become the main feature, and eventually the loan became marginal. Interest rates on sea loans were very high, ranging from 25% up to 50%, because merchants were paying both the cost of the loan and the insurance part of the contract. By the 14th century, however, many Italian merchants had become very rich and had liquidity to fund their shipments and businesses, so the loan part of the contract became fictitious in the mutuum, which was used in Genoa in the 14th century.8

Although maritime insurance contracts developed at the same time in Florence and Genoa, from Genoa comes the document considered as the first modern insurance contract, redacted by the notary Tomaso Casanova on the 18th of March 1343 (Melis 1975). Yet, our discovery of an insurance contract drafted in the same year in Palermo with the insurer and the insured being a Genoese merchant and a Pisan merchant makes it plausible to hypothesize that Genoese and Tuscan merchants had begun using insurance contracts a bit earlier than previously thought.

Insurance contracts had different characteristics in Genoa and Florence. Insurance contracts drafted in Genoa, at least until the first half of the 15th century, followed a very rigid set of rules and were always in a disguised form, with insurance premia rarely reported. Genoese contracts were very precise in reporting what risks were covered, and under which conditions the contract could have been invalidated. Only notarial deeds were considered to be valid and were typically redacted in Latin. Much different and more informal rules regulated insurance contracts and markets in Florence (Ceccarelli 2012). Already during the mid- and late-14th century, insurance contracts were explicitly mentioned and never disguised under other contractual forms. These contracts were private agreements between the two parties, redacted in Italian, without the services of notaries. Key to the development of the Florentine insurance market were the brokers (sensali) who matched the demand and supply sides of the market for protection and drafted the formal deeds.9

With Italian merchants expanding their trading and business activities abroad during the 14th and 15th centuries, insurance contracts and markets soon began developing in other commercial centers in Europe, such as Barcelona and Palermo, likely brought by many Genoese and Florentine merchants who had commercial partners and subsidiaries there.10 Meanwhile, insurance contracts developed in Venice only during the second half of the 15th century, likely transplanted by Florentine merchants who had their business headquarters there (Nehlsen-von Stryk 1988).

3 Conceptual Framework: The Market for Protection

The first question we address is why insurance contracts and markets were developed in medieval Europe, neither earlier nor elsewhere. This section describes the conceptual framework we develop to model the rise of insurance contracts and markets (a formal model is being developed in a companion paper). We make assumptions that capture the key features of seaborne commerce in medieval Europe and derive a set of predictions. Narrative evidence presented in Section 3.4 and evidence from the empirical analysis on the historical dataset of insurance contracts we collected (Section 5) will then be compared to the predictions of the conceptual framework.

3.1 Demand Side

Suppose that a merchant intends to ship his merchandise. He can bear risks, or he can purchase protection against risks—from the state, and/or from fellow merchants. We assume that the merchant is uncertainty averse and faces:

a known probability of loosing the cargo due to natural risks (e.g., thunderstorms);

an unknown probability of loosing the cargo due to risks generated by human activities (e.g., corsairs hired by states to damage their commercial competitors).

The rationale behind these two assumptions is as follows. During the medieval period, progress in nautical technology enables merchants to travel longer distances and during the winter. While both improvements may potentially expand business and trade opportunities, they might also increase the riskiness of the journey, and, hence, the probability of a negative event leading to the loss of the cargo. Yet, after a few trips along the same route, merchants can assess the probability of natural risks and learn if this probability has increased because they now travel longer distances and also during the winter.

In contrast, human risks (i.e., risks generated by human activities), such as attacks by corsairs, are unpredictable because the knowledge of the dynamics of these attacks would require merchants to have a broad information network all over the routes, which sedentary merchants living and doing business in their place of residence, typically lack. Hence, merchants face an unknown probability of loosing the cargo due to human risks.

The merchant can reduce the expected loss:

investing in self-protection (e.g., choose a longer route with no dangerous winds, ship the merchandise on an armed galley, etc.);

purchasing protection from third parties.

3.2 Supply Side

Political institutions can supply protection to merchants shipping their merchandise in a variety of ways. States might, for example, provide protection to their merchants by making ships transporting merchandise travel in convoys escorted by an armed fleet. In addition or alternatively, merchants might be requested to pay a special tax in exchange for a safe journey when they travel across and to locations.

We do not formally model the public supply of protection and we focus on the private supply of protection, with private agents (e.g., merchants) becoming the main suppliers of protection against risks to fellow merchants through the invention of insurance contracts. In particular, we assume that a wealthy merchant (i.e. the insurer) has (i) capital (liquidity) and (ii) a broad information network thanks to his extensive business activities. We make three main assumptions regarding the insurer. He observes the investment (self-protection) made by the fellow merchant who seeks protection for his shipments to reduce the probability of loss. Unlike the merchant who seeks protection and is uncertainty averse because he does not know the probabilities of human risks, the insurer is risk averse as he knows the “true” probability of loss deriving from human risks (e.g., corsairs) given his broad information network. Finally, there is no moral hazard because on each vessel a public clerk is required to travel and to annotate any details of the journey, including any opportunistic behavior (such as, theft of the merchandise).

Thanks to his wealth deriving from a diversified set of businesses and his comparative advantage in information on risks related to seaborne trade, the wealthy merchant (i.e., the insurer) can pool risks, choose how much risk he wants to undertake at the given price, and benefit from “selling protection” through the insurance contract.

3.3 Predictions and Insights

The theoretical framework delivers the following predictions.

First, new risks with unknown probabilities (e.g., human risks like attacks from corsairs) make the uncertainty averse merchant willing to buy more protection to reduce these risks. The information asymmetry with the insurer knowing the “true” probability of human risks (e.g., attacks by corsairs) thanks to his broad information network makes the newly invented insurance contract profitable for the supply side who can pool risks. Hence, insurance contracts and markets arise.

Second, human risks (with unknown probabilities) have a relatively larger effect on insurance premia compared to natural risks (with known probabilities).

Third, ceteris paribus, the higher the human risks (e.g., attacks by corsairs and warfare), the higher the insurance premium. Any mechanisms that mitigate human risks (e.g., shipping the merchandise on an armed galley), reduce the insurance premium.

3.4 Theory Meets History

3.4.1 State Protection from Risks in Ancient Trade

As mentioned in Section 2, in ancient economies most trade was carried on overland. Natural risks were relatively modest when carrying merchandise overland. At the same time, as property rights on land were easily defined and enforced, merchants could buy protection against human risks (e.g., attacks by thieves or during warfare) by obtaining military protection by their own rulers or paying taxes/tolls to their own rulers or foreign rulers in return for safety for their merchandise and for themselves. Therefore, trade overland did not generate a significant demand for protection, and when needed, rulers could easily supply it.

Similarly, in antiquity, there was not a lot of demand for protection when merchants shipped their merchandise overseas. Natural risks (e.g., thunderstorms) clearly existed but after a few trips along the same route, merchants and vessels’ crews learned the frequencies of natural risks along a specific route and could avoid or minimize them by choosing a longer but safer route. As property rights over the sea did not exist and could not be easily enforced, nobody owned the seas so that merchants could not easily purchase protection by paying taxes or tolls to their own or foreign rulers in exchange for protection. When human risks emerged (e.g., pirates) and became a major issue for the economies and populations of a given political entity, the states (e.g., the Roman Empire) took care of eliminating these risks.

These two features of trade in antiquity implied that there was no profitability for private citizens or merchants from selling protection through the insurance business as nobody would buy it. Therefore, in ancient economies, the need for insurance contracts and markets did not arise and protection from natural and human risks was extended when necessary by the states themselves.

3.4.2 More Demand for Protection in Medieval Trade

Medieval Europe saw a major growth in seaborne trade (Section 2). Medieval seaborne trade presented two main novelties with respect to commerce in antiquity. First, technological advances in nautical progress enabled merchants to travel longer distances and also during the winter—enlarging their business opportunities but also exposing merchants to higher probabilities of natural risks. Yet, after a few trips, natural risks even if more likely, would become predictable, and hence, merchants still knew the (higher) probabilities of these natural risks.

Second, the political fragmentation of Europe during the medieval period, with states greatly competing over commercial routes, generated totally new human risks that for most merchants were unpredictable (i.e., they could not assess the probability of these novel risks): attacks by corsairs. Corsairs (privateers) were private citizens hired by the states themselves to attack the vessels of competitors and stole the merchandise in order to damage the economies of competing states.

Merchants with small or medium businesses, who were often sedentary merchants in their hometowns without a broad trade and information network, lacked information on the frequency (and, hence) probability of attacks by corsairs. Corsairs could suddenly attack at any times, on any routes, often changing their strategies of attacks. Unlike the riskiness of natural phenomena, such as strong winds on a given route in a given season, which could be assessed after making a few journeys on the same route in the same season, the unpredictability of attacks and confiscations of merchandise by corsairs generated new risks with unknown probabilities for the majority of medieval merchants all over Europe, and especially in the Mediterranean Sea.

To sum up, both the increased riskiness coming from natural phenomena due to longer journeys, but most important, the emergence of new human risks (attacks by corsairs and warfare) with much higher unpredictability for most merchants who lacked a broad information network, generated a huge demand for protection in medieval commercial centers in Europe. Venice chose to meet this increased demand through state protection, whereas Florence and Genoa resorted to a private solution: the invention of insurance contracts and markets.

The Venetian Way: State Protection of Seaborne Trade. Since early times, the Venetian Republic had made major investments in its armed fleet to expand commercial routes (Lane and Mueller 1985; Lane 1987; Mueller 1997). This investment made it profitable to use the Venetian fleet to protect Venetian merchants against human risks. These merchants traveled in convoys (mude) under the protection of the Venetian fleet. Because Venice provided state protection to its merchants, insurance contracts and markets did not develop in Venice until the late 15th century. When these markets developed, they were likely transplanted by Florentine merchants residing and conducting their businesses in Venice. It is also interesting to note that even when Venetian merchants began adopting insurance contracts, the insurance premia were lower than the ones prevailing in other locations such as Barcelona, Florence, Genoa, or Palermo (probably because the Venetian fleet was still making the journeys of Venetian merchants relatively safer).

The Florentine and Genoese Way: Insurance Was Invented. During the 13th and early 14th centuries, Florence and Genoa witnessed a major urban and commercial growth. A small group of very rich merchants emerged in both cities with two assets that even nowadays are important for succeeding in the insurance business: (i) capital (liquidity) invested in a diversified set of businesses, and (ii) a broad information network (e.g., Florentine merchants had very efficient courier services in Barcelona and Bruges). These two assets were key to pool risks and make selling insurance a profitable business.

Therefore, the increased demand by local sedentary merchants for protection from higher risks with known probabilities (natural risks) and new risks with unknown probabilities (human risks) met the private supply of protection through the invention of insurance contracts. A new market—the market for insurance—was born in both Florence and Genoa, and soon would spread to other Italian and, next, European commercial centers—consistent with one of the predictions of our conceptual framework. In turn, the rise of insurance markets made possible the volume of seaborne trade that, due to the inadequacy of ground transportation, was needed to support the expansion of trade that characterized the Commercial Revolution.

The newly developed insurance market was based on a practical understanding of probability that preceded, by at least a couple of centuries, the emergence of its theoretical understanding in the 16th and 17th centuries, most notably through the works of Cardano, Huygens, and Pascal. In this regard, consider this quote from the seminal mid-15th century business compendium written by Benedetto Cotrugli (1573):

Every ship needs to be insured, because one compensates for another, and if many are insured the merchant cannot but gain overall. And he must do this boldly, because if from excessive prudence he insures one ship and not another, if some misfortune befalls the uninsured ship, there will be no compensation for the loss.11

The relevance of frequencies and risk pooling for the insurance business was thus understood by Cotrugli. There is also evidence of a highly non-trivial practical understanding of probability in the medieval abacus schools (scuole d’abaco). These schools started after the appearance of the epoch-making Liber abbaci of the famous mathematician Fibonacci at the beginning of the 13th century. This book was the first serious piece of mathematics in western Europe after many centuries of silence and, inter alia, developed a commercial arithmetic based on Arabic numerals. Through the abacus schools, this arithmetic became a core subject in the education of Italian merchants (Sapori 1955; Goldthwaite 1972), who had high literacy rates for the times.12 As to the practical understanding of probability in abacus schools, a striking example can be found in a mid-15th century Florentine anonymous treatise for abacus schools that fully solved the so-called problem of points.13 This is a basic, but highly non-trivial, problem in probability that was solved by Pascal about two centuries later, in one of the developments that marked the beginning of modern probability. For our purposes, this anonymous treatise is evidence of the sophistication of the practical notion of probability that Italian merchants could learn in the widespread abacus schools.

4 Data

4.1 Sources

Three-fourths of the historical dataset we employ in the empirical analysis consist of data collected from previously unexplored archival sources as follows:

A total of 5,031 insurance contracts drafted by notaries or reported in merchants’ account books;

2,531 contracts from the State Archives of Genoa;

2,310 contracts from the State Archives of Palermo;

190 contracts from the Datini archives in Prato.

A total of 104 litigation cases dealing with insurance housed in the Fondo Mercanzia (merchants’ court) at the States Archives of Florence.

The remaining 1/4 of the dataset consists of data from secondary sources as follows:

A total of 1,882 insurance contracts drafted by notaries or reported in merchants’ account books;

We transcribed the entire text of each contract and court record in its original version, we reported the relevant information in a brief summary, and we then compiled the dataset using the information from these summaries. The following summaries of three contracts give a good idea of the type of information coming from these primary sources.

An insurance contract drafted by notary Stefano Amato in Palermo

Date: February 25, 1347

Route: from Palermo to Pisa

Goods shipped: 24 file of cheese and two balle of leather

Total value insured: 100 gold florins (fl.)

Names of parties

— insured: Francesco di Canigliano from Pisa

— insurer: Baldassarre Grillo, merchant and citizen of Genoa

Type of ship: galley owned by Oddone de Donna Bona

Insurance premium: 7.5%

Clauses (e.g., risks covered, deadline to liquidate damages)

— covered both natural and human risks from departure port to arrival port, including loading and unloading

— damage liquidated within 1 month

This deed is a typical example of a contract drafted in Palermo. Written in Latin, it concerns a shipment of cheese and leathers from Palermo to Pisa in 1347. The goods were insured from departure to arrival, including the unloading and uploading procedures. The contract insured the merchant “against the risks generated by the sea, by bad luck and by people.” The ship employed for the journey was an armed galley. The liquidation of the damage (if any) was conditional on the ship following the agreed itinerary (“eundo et exonerando pro rata viagio non mutuato”), with detours being allowed due to possible, yet unspecified, fair impediments (“iusto impedimento”) and was scheduled to take place in Palermo 1 month after reliable news of the damage occurred had been notified to the insurer (“certis novis de sinistro predicto”). The insurer, Baldassarre Grillo, was a Genoese citizen, member of the Grillo family, one of the most prominent and rich families of merchants in Genoa, whereas the insured was a Pisan merchant, Francesco di Canigliano.

Insurance contract from the Datini archives, I

Date: May19, 1387

Route: from Genoa to Valencia

Goods shipped: 300 sacche of woad (blue dye)

Total value insured: 900 gold florins (fl.)

Names of parties

— insured: Francesco di Marco Datini from Prato

— insurers (all Florentine merchants, with individual quotas of insurance): messer Niccolò di Pagnozzo & co. 300 fl.; Giovannozzo Biliotti & co: 300 fl.; Bartolomeo di Francesco banker 200 fl.; Lemmo di Balduccio & Doffo degli Spini & co. 100 fl.

Ship owned by Matteo Giolato from Barcelona

Insurance premium: 3%

Clauses: standard

This contract related to one of the most frequent routes in the dataset—connecting Genoa, one of the leading commercial centers in the Middle Ages, to one of the most attractive Catalan commercial hubs. Compared to the earlier contract drafted in Palermo where there was just one insurer; in this contract, we see what will become a common feature of later contracts in which more than one (in this case, four) insurers shared the risks involved in extending protection to the valuable shipment by Francesco Datini, the famous merchant from Prato, whose business activities stretched all over Europe.

Insurance contract from the Datini archives, II

Date: December 19, 1384

Route: from Porto Pisano (Tuscany) to Barcelona

Goods shipped: one balletta of veils (valuable cloth)

Total value insured: 130 gold florins (fl.)

Names of parties

— insured: Francesco di Marco Datini from Prato

— insurers: Filippo Burbassi 50 fl.; Geri and Lamberto di Domenico 80 fl.

Ship owned by Francesco Colombiere

Insurance premium: 6%

Negative event: on January 6, Istoldo di Lorenzo (Datini’s agent) notified the insurers that the ship was attacked by the galleys of King Charles and the merchandise taken. Within 2 months, the insurers had to repay the insured.

This contract is quite insightful because it reports information on one of the most frequent sources of risk in medieval trade in the western Mediterranean—the one generated by human activities, in this case, a military attack.

Before describing the data, we address potential concerns regarding the representativeness of the contracts included in the historical dataset that may generate selection issues. First, the set of cities for which we have insurance data may itself be selected in some ways. Second, even assuming that all contracts survived, one worries that the choice of the notaries whose records we analyzed, may generate biases. Third, contracts that survived to this day to be studied may be different from those that were lost.

Regarding the first concern—selection bias coming from the choice of cities included in the dataset—we chose to include Florence and Genoa because these are the cities in which insurance contracts were invented and spread to other commercial centers. In addition, the two cities were two of the major commercial hubs in medieval Europe connecting England and the Flanders all the way to the Middle East. We also include Prato (next to Florence) because it was the hometown of Francesco di Marco Datini, one of the wealthiest medieval merchants whose businesses and business associates were spread all over Europe, and whose archives host a wealth of insurance contracts, business letters, and account books. We then include Palermo and Barcelona because, like Florence and Genoa, they were among the most active commercial centers in medieval Europe, and Florentine and Genoese merchants actively trading all over the Mediterranean brought the newly developed insurance contracts there as early as the mid- and late-14th century.14 To sum up, Florence, Genoa, Prato, Palermo, and Barcelona were among the commercial leaders in medieval Europe, they either invented or were among the first cities to adopt insurance contracts and to develop insurance markets, and their archives host a wealth of insurance contracts.

As for the second concern—selection bias coming from including only a subset of notaries in the dataset—we explain in detail how we chose which notaries to include in each location.

For Genoa, it is well known among medieval historians that the wealth of records in the State Archives of Genoa is so enormous that it is literally impossible for anyone to collect all the available records in a reasonable amount of time. We then surveyed the volumes of notarial deeds and selected the notaries who drafted a very large number of insurance contracts under the assumption that these notaries were “the big players” in the insurance business. This is confirmed independently in the works of Giacchero (1984), who mentions that in the 1420s, notary Branca Bagnara basically held the monopoly of drafting insurance contracts in Genoa. Of course, the many insurance contracts of Branca Bagnara are included in our dataset, and similarly for other Genoese notaries for whom it appears that drafting insurance contracts was a significant portion of their overall business.

For Florence, merchants did not use the services of notaries when drafting insurance contracts. Florentine merchants drafted private deeds, often with the help of an intermediary (sensale) and kept these private deeds among their account books (ready to be shown in court should any litigation among insured and insurer arise). Hence, no selection biases coming from the choice of notaries plague the insurance contracts for Florence in our dataset.

For Prato, we collected and coded all the 190 insurance contracts found in Francesco Datini’s account books. So there are no issues of selection bias coming the selection of notaries for the data in Prato.

For Palermo, we include the surviving records of all notaries housed at the States Archives of Palermo from 1340 to 1510. By definition, we did not select any specific notaries.

To sum up, we feel confident that although selection bias coming from the choice of notaries considered cannot be excluded, this bias should be a minor one for 75% of the contracts in the dataset, which is based on sources coming from the archives of the aforementioned cities.15

With regards to the third concern—selection bias generated by the inclusion of information coming from surviving archival sources—there is no way to estimate the share of surviving contracts in any archives, and, hence, like in many historical studies using archival sources, it is not possible to address the issue of selection bias coming from this channel. However, in the next subsection, we show that the patterns of medieval trade (e.g., routes, types of commodities shipped from each location, volume of trade by location) emerging from the insurance contracts in our dataset match very well the patterns of medieval trade described in the works of leading historians. To give an example, it is well known that Palermo was the hub for shipping wheat and sugar during the Middle Ages (Nef 2013). The insurance contracts in our dataset indicate that most insurance contracts drafted in Palermo pertained to shipments of wheat or sugar. (whereas, if we found that the main commodity insured in Palermo was, say, textiles or wool, we would be concerned that the insurance contracts drafted in Palermo and surviving to today were not representative of the patterns of medieval trade.)

4.2 Dataset

The oldest insurance contract in the dataset was drafted in 1343 in Palermo, the latest in 1506 in Venice, with most contracts being drafted between 1428 and 1490. As the very first insurance contracts appeared around the early 1340s, it probably took a few years before a new market—the market for insurance—would emerge.

The information provided in the deeds is rich and detailed. Each insurance contract reports the date in which the deed was drawn up, with the journey typically starting within a few days, and never later than a couple of weeks. This pattern enables us to accurately identify the month, and hence, the season of the voyage.

Almost all contracts supply information on the route, starting from the port where the merchandise was loaded on the vessel, any intermediate stops, and the final destination where the merchandise was unloaded. A subset of the contracts specify if the journey was one way or round-trip, or if the ship was allowed to depart or arrive to a port different from the ones agreed upon.

All contracts list the names of the insured and the names of the insurers and their places of residence, whereas only a subset of the contracts reports the names of the owners and/or the captains of the vessels.

Many contracts report the type of vessels: ships, whale boats, galleys, caravels, boats, and saette. The first two types of vessels had the largest loading capacity (more than 380 tons). The galleys had a smaller capacity, but were usually defended by armed men and, hence, were considered the safest in the case of attack by corsairs. Caravels and boats were smaller vessels with a medium loading capacity (between 140 and 380 tons). Lastly, the saette had a small loading capacity (between 45 and 140 tons), but a were quite fast compared to the others (Piccinno 2016).

Most contracts indicate the commodities loaded on the insured vessels, which included wheat, sugar, a variety of spices including pepper and saffron, oil, wine, cheese, a variety of foods, animals, weapons, raw materials, dyes, wool, cotton, silk, clothes and textiles, leather products, coral, jewels, coins, and slaves. Especially in Genoa, it was common to insure the entire vessel with its load.

Many contracts report the coverage, that is, the sum of money that the insurers committed to refund to the insured in the case of a negative event that brought a partial or total loss of the cargo. For more than half of the deeds, the contracts report the insurance premium that the insured paid to the insurer(s).

As for the 104 court cases collected from the merchants’ court’s records (Fondo Mercanzia) housed at the State Archives of Florence, they span the 50 years from 1379 to 1430. The number of journeys that ended up with a litigation dealing with insurance was quite limited. Hence, the relatively small number of court cases per year that we found seems reasonable. In addition to the same detailed information provided in the insurance contracts, the court cases provide impressive details on the reasons involved in the litigation, which sheds light on how the insurance markets arose and evolved between the 14th and the 15th centuries.

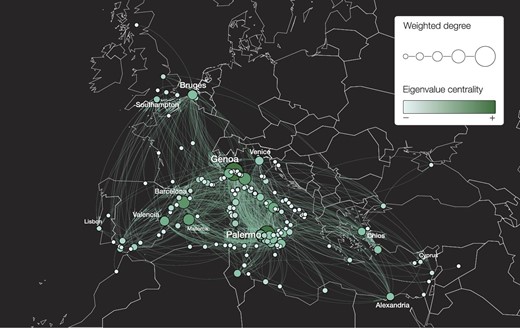

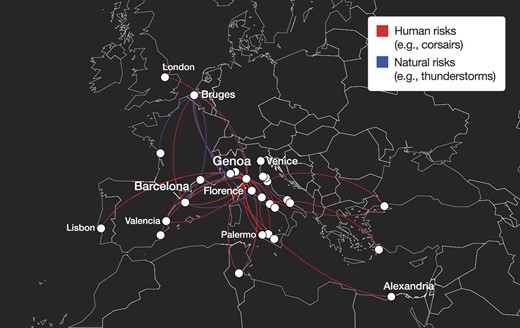

While we acknowledge several limitations of our dataset, we maintain that the main patterns of medieval trade emerging from the information supplied in the insurance contracts and court records match very well the main patterns of medieval trade that the works of historians have documented. We substantiate our claim by first showing the network structure of our dataset (Figure 1). Each node represents a port and each pair of nodes is connected by an undirected edge when there is at least one journey between them. The size of a node is proportional to its degree, that is, the number of other nodes to which it is directly connected. The color of the node, ranging from white to green, depends on its eigenvalue centrality, which measures how much it is central, hence important, in the network.

Medieval trade network.

The network representation enables to identify the main centers of maritime commerce from 1340 to 1500: in the North Sea, Bruges, Sluis, and Southampton; in the western Mediterranean, the Catalan cities of Barcelona and Valencia, the island of Mallorca and, to a smaller extent, the Provencal cities of Aigues Mortes and Marseille; in the Ligurian Sea, Genoa, which is the most central node in the network and the one with the highest degree; in the Tyrrhenian Sea, Florence (more precisely, Porto Pisano, which was the hub from which Florentine merchants shipped their merchandise), Rome, and Naples; in the Adriatic Sea, Venice (which plays a minor role in the dataset as Venetian merchants adopted much later the custom of insuring goods); in the eastern Mediterranean, the island of Chios and the city of Alexandria; in Sicily, Palermo, and next, the cities of Trapani, Catania, and Siracusa. These are most of the commercial centers and routes that historians have described to characterize medieval seaborne trade.

The size of the network is remarkable, with shipments going from Sluis in the Flanders to the island of Chios in the Aegean Sea in Greece, or from Genoa to Kaffa (today Feodosia) in southern Crimea. The longest journey in the dataset—3,134 nautical miles taking the shortest route—is dated 1410, with the shipment departing from Sluis and arriving in Alexandria in Egypt.16 To give an idea of traveling times, which depended on many factors, including the exact route, the winds (and, hence, the season), the type of boat, and the skills of the ship’s crew, the median time to go from Genoa to the Catalan island of Mallorca was between 10 and 12 days, whereas it took more than 20 days for a big cargo ship to reach the ports in the eastern Mediterranean from Genoa (Piccinno 2016).

Table 2 reports summary statistics for the main variables we employ in the empirical analysis. All variables display high variability, with outliers attaining extreme values and high values for the standard deviation. The total amount insured, for example, has a maximum value of 5,000 florins, whereas the minimum value is only 1.29 florins. The maximum number of insurers underwriting a single contract is 70 for a shipment of wheat in 1473 from Licata in Sicily to the Greek island of Rhodes with an intermediate stop in Barcelona. The insurance premium ranged from a minimum of 0.75% to a maximum of 22%, with a mean value of 5.59%.

Summary statistics.

| N | Mean | S.D. | Min | P25 | P50 | P75 | Max | |

|---|---|---|---|---|---|---|---|---|

| Quota insured (fl.) | 27659 | 57.31 | 58.25 | 0.65 | 21.43 | 42.86 | 100.00 | 2600.00 |

| Total amount insured | 5200 | 304.80 | 372.13 | 1.29 | 100.00 | 200.00 | 400.00 | 5000.00 |

| Insurers per contract | 6827 | 4.33 | 5.57 | 1.00 | 1.00 | 2.00 | 5.00 | 70.00 |

| Distance (n.m.) | 5292 | 678.06 | 583.50 | 8.00 | 286.00 | 490.00 | 792.00 | 3134.00 |

| Premium % | 2259 | 5.59 | 2.63 | 0.75 | 4.00 | 5.00 | 7.00 | 22.00 |

| N | Mean | S.D. | Min | P25 | P50 | P75 | Max | |

|---|---|---|---|---|---|---|---|---|

| Quota insured (fl.) | 27659 | 57.31 | 58.25 | 0.65 | 21.43 | 42.86 | 100.00 | 2600.00 |

| Total amount insured | 5200 | 304.80 | 372.13 | 1.29 | 100.00 | 200.00 | 400.00 | 5000.00 |

| Insurers per contract | 6827 | 4.33 | 5.57 | 1.00 | 1.00 | 2.00 | 5.00 | 70.00 |

| Distance (n.m.) | 5292 | 678.06 | 583.50 | 8.00 | 286.00 | 490.00 | 792.00 | 3134.00 |

| Premium % | 2259 | 5.59 | 2.63 | 0.75 | 4.00 | 5.00 | 7.00 | 22.00 |

Notes: The Quota is the value in Florins that one insurers undertakes in one contract. The Total is the value in Florins that is insured in a single contract by all insurers combined. The Distance is the shortest distance by sea between the origin and destination harbors.

Summary statistics.

| N | Mean | S.D. | Min | P25 | P50 | P75 | Max | |

|---|---|---|---|---|---|---|---|---|

| Quota insured (fl.) | 27659 | 57.31 | 58.25 | 0.65 | 21.43 | 42.86 | 100.00 | 2600.00 |

| Total amount insured | 5200 | 304.80 | 372.13 | 1.29 | 100.00 | 200.00 | 400.00 | 5000.00 |

| Insurers per contract | 6827 | 4.33 | 5.57 | 1.00 | 1.00 | 2.00 | 5.00 | 70.00 |

| Distance (n.m.) | 5292 | 678.06 | 583.50 | 8.00 | 286.00 | 490.00 | 792.00 | 3134.00 |

| Premium % | 2259 | 5.59 | 2.63 | 0.75 | 4.00 | 5.00 | 7.00 | 22.00 |

| N | Mean | S.D. | Min | P25 | P50 | P75 | Max | |

|---|---|---|---|---|---|---|---|---|

| Quota insured (fl.) | 27659 | 57.31 | 58.25 | 0.65 | 21.43 | 42.86 | 100.00 | 2600.00 |

| Total amount insured | 5200 | 304.80 | 372.13 | 1.29 | 100.00 | 200.00 | 400.00 | 5000.00 |

| Insurers per contract | 6827 | 4.33 | 5.57 | 1.00 | 1.00 | 2.00 | 5.00 | 70.00 |

| Distance (n.m.) | 5292 | 678.06 | 583.50 | 8.00 | 286.00 | 490.00 | 792.00 | 3134.00 |

| Premium % | 2259 | 5.59 | 2.63 | 0.75 | 4.00 | 5.00 | 7.00 | 22.00 |

Notes: The Quota is the value in Florins that one insurers undertakes in one contract. The Total is the value in Florins that is insured in a single contract by all insurers combined. The Distance is the shortest distance by sea between the origin and destination harbors.

5 Empirical Analysis

Thanks to the wealth of details provided in each contract, we document and discuss the extent and several features of seaborne trade during the Middle Ages. In addition, we describe the structure of the newly developed insurance market during the 150 years following its rise. Finally, we identify and analyze the factors correlated to the insurance premium, which was the key novel feature of the newly developed contracts. In doing so, we disentangle the role of natural versus human risks in shaping insurance in medieval seaborne trade. The main findings from the empirical analysis support the predictions of the conceptual framework we presented earlier.

5.1 Characteristics of Medieval Trade

5.1.1 Routes and Commercial Hubs

To understand the spatial characteristics of seaborne trade during the Middle Ages, we split the sample according to the locations (cities) in which insurance contracts were drafted and we build the network of shipments for each of these locations.

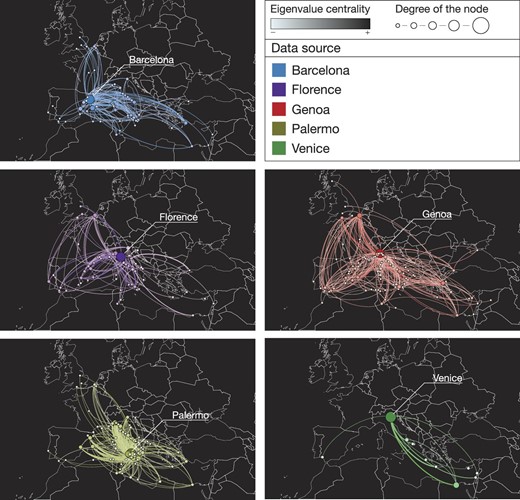

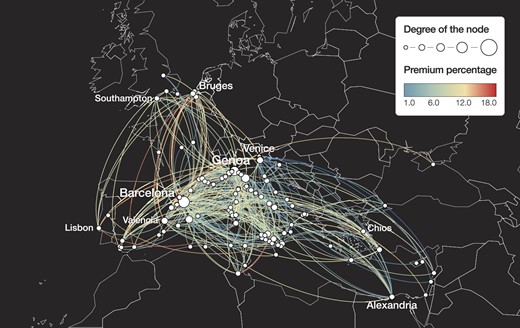

In Figure 2, the intensity of the color of a node increases with its eigenvalue centrality, whereas the size of the node increases with its degree. As expected, the central node in each network is the city in which the insurance contracts were undersigned. Not surprisingly, Genoa, Palermo, and Barcelona figured prominently in this trading network—making the Tyrrhenian Sea the most crowded area of the Mediterranean.

Trade network by city. Each panel represents one of the cities for which we have data. For each of the five networks, we compute the eigenvalue centrality and the degree of the nodes. The color of the edges is a mix of the colors of the origin and destination nodes. The intensity of the color of a node increases with its eigenvalue centrality, while the size of a node increases with its degree.

Genoa appears to be the port with the most direct connections with the North Sea, as well as with Andalusian harbors, which shipments heading to northern Europe used as intermediate stops. This pattern confirms the argument made by Melis (1985), namely that Genoese merchants pioneered the navigation toward the Atlantic. Many shipments also departed from Genoa with Sardinia and several harbors in Provence being the final destinations.

Consistent with the patterns described by historians, the network of insurance contracts drafted in Venice shows that most journeys included destinations in the eastern Mediterranean, especially Alexandria in Egypt, from which many shipments reached many other European markets. Venice appears connected primarily with a marginal area of the network, which explains why its eigenvalue centrality is low with respect to other cities with a similar degree when we consider the complete network represented in Figure 1.

Contracts drafted in Palermo insured shipments with a median distance of 403 nautical miles, which is more or less the distance between Genoa and Palermo, whereas the median distances are much higher for itineraries insured in the contracts drafted in Venice (884 nautical miles) and Genoa (925 nautical miles). In addition, insurance contracts drafted in Genoa exhibit the highest variance of the distance of the journey, including both short trips in the northern Tyrrhenian Sea and the very long voyages to northern Europe (Table 3).

5.1.2 Goods

Table 4 presents the share of the main goods insured in each city (except in Barcelona). The routes covered in the insurance contracts matched well the types of goods in which a city or region specialized.

Distances of journeys listed in insurance contracts.

| Distance in n.m. | Observations | Mean | S.D. | p10 | p25 | p50 | p75 | p90 | |

|---|---|---|---|---|---|---|---|---|---|

| Barcelona | 1587 | 609 | 408 | 203 | 286 | 558 | 704 | 1310 | |

| Florence | 211 | 735 | 578 | 240 | 360 | 496 | 1062 | 1408 | |

| Genoa | 1474 | 1061 | 789 | 213 | 356 | 925 | 1713 | 2212 | |

| Palermo | 1944 | 425 | 308 | 171 | 230 | 403 | 538 | 690 | |

| Venice | 76 | 1015 | 345 | 457 | 884 | 884 | 1212 | 1388 |

| Distance in n.m. | Observations | Mean | S.D. | p10 | p25 | p50 | p75 | p90 | |

|---|---|---|---|---|---|---|---|---|---|

| Barcelona | 1587 | 609 | 408 | 203 | 286 | 558 | 704 | 1310 | |

| Florence | 211 | 735 | 578 | 240 | 360 | 496 | 1062 | 1408 | |

| Genoa | 1474 | 1061 | 789 | 213 | 356 | 925 | 1713 | 2212 | |

| Palermo | 1944 | 425 | 308 | 171 | 230 | 403 | 538 | 690 | |

| Venice | 76 | 1015 | 345 | 457 | 884 | 884 | 1212 | 1388 |

Notes: Statistics in each row are computed using the subsample of contracts redacted in the city indicated in column (1).

Distances of journeys listed in insurance contracts.

| Distance in n.m. | Observations | Mean | S.D. | p10 | p25 | p50 | p75 | p90 | |

|---|---|---|---|---|---|---|---|---|---|

| Barcelona | 1587 | 609 | 408 | 203 | 286 | 558 | 704 | 1310 | |

| Florence | 211 | 735 | 578 | 240 | 360 | 496 | 1062 | 1408 | |

| Genoa | 1474 | 1061 | 789 | 213 | 356 | 925 | 1713 | 2212 | |

| Palermo | 1944 | 425 | 308 | 171 | 230 | 403 | 538 | 690 | |

| Venice | 76 | 1015 | 345 | 457 | 884 | 884 | 1212 | 1388 |

| Distance in n.m. | Observations | Mean | S.D. | p10 | p25 | p50 | p75 | p90 | |

|---|---|---|---|---|---|---|---|---|---|

| Barcelona | 1587 | 609 | 408 | 203 | 286 | 558 | 704 | 1310 | |

| Florence | 211 | 735 | 578 | 240 | 360 | 496 | 1062 | 1408 | |

| Genoa | 1474 | 1061 | 789 | 213 | 356 | 925 | 1713 | 2212 | |

| Palermo | 1944 | 425 | 308 | 171 | 230 | 403 | 538 | 690 | |

| Venice | 76 | 1015 | 345 | 457 | 884 | 884 | 1212 | 1388 |

Notes: Statistics in each row are computed using the subsample of contracts redacted in the city indicated in column (1).

Items insured by location.

| Market | 1st | 2nd | 3rd | 4th |

|---|---|---|---|---|

| Florence | Textiles (23%) | Silks (14%) | Food (10%) | Leather (5%) |

| Genoa | Ships and freights (20%) | |||

| Palermo | Food (39%) | Sugar (17%) | Textiles (9%) | Leather (5%) |

| Venice | Oil and wine (25%) | Luxury goods (10%) | Textiles (2%) |

| Market | 1st | 2nd | 3rd | 4th |

|---|---|---|---|---|

| Florence | Textiles (23%) | Silks (14%) | Food (10%) | Leather (5%) |

| Genoa | Ships and freights (20%) | |||

| Palermo | Food (39%) | Sugar (17%) | Textiles (9%) | Leather (5%) |

| Venice | Oil and wine (25%) | Luxury goods (10%) | Textiles (2%) |

Notes: The share of the types of goods with the most occurrences by city are presented here, in order of occurrences from left to right, and excluding Ships and freights (except for Genoa). Only one category is shown for Genoa because the vast majority of contracts was not reporting the item or was reporting various goods.

Items insured by location.

| Market | 1st | 2nd | 3rd | 4th |

|---|---|---|---|---|

| Florence | Textiles (23%) | Silks (14%) | Food (10%) | Leather (5%) |

| Genoa | Ships and freights (20%) | |||

| Palermo | Food (39%) | Sugar (17%) | Textiles (9%) | Leather (5%) |

| Venice | Oil and wine (25%) | Luxury goods (10%) | Textiles (2%) |

| Market | 1st | 2nd | 3rd | 4th |

|---|---|---|---|---|

| Florence | Textiles (23%) | Silks (14%) | Food (10%) | Leather (5%) |

| Genoa | Ships and freights (20%) | |||

| Palermo | Food (39%) | Sugar (17%) | Textiles (9%) | Leather (5%) |

| Venice | Oil and wine (25%) | Luxury goods (10%) | Textiles (2%) |

Notes: The share of the types of goods with the most occurrences by city are presented here, in order of occurrences from left to right, and excluding Ships and freights (except for Genoa). Only one category is shown for Genoa because the vast majority of contracts was not reporting the item or was reporting various goods.

Many contracts drafted in Palermo insured shipments from Palermo to Barcelona and Genoa. In fact, Sicily was the main supplier of wheat and sugar to several European cities including Barcelona and Genoa as many locations were often struggling to secure food for their growing populations. Sicily then became a key player for their political stability and the insurance contracts in the dataset document this pattern showing that the most important item transported and insured from Palermo to Barcelona, Genoa and other European locations was wheat. At the same time, the second most important item insured in the contracts drafted in Palermo was sugar, which is consistent with the increasing investment in the cultivation and processing of sugar cane that took place in Sicily during the 14th and 15th centuries.

Insurance contracts and court cases drafted in Florence confirm the well-known pattern that Florentine merchants were specialized in trading textiles: A large share of insured shipments from Florence took place to or from destinations in northern Europe where wool and raw textile materials were bought and manufactured textiles were sold.

The vast majority of insurance contracts drafted in Genoa extended protection over the vessels, their entire cargoes, and even the freights paid.

5.1.3 Vessels and Seasonality

Insurance contracts in the dataset mention six types of vessels: ships, galleys, boats, whaleboats, caravels, and saette. These vessels differed in loading capacity, safety, speed, and handling. Ships appear to be the vessels most frequently employed in the dataset; they were the biggest vessels, could carry large quantities of goods, and their structure made them suitable to overcome long journeys and winter seas.

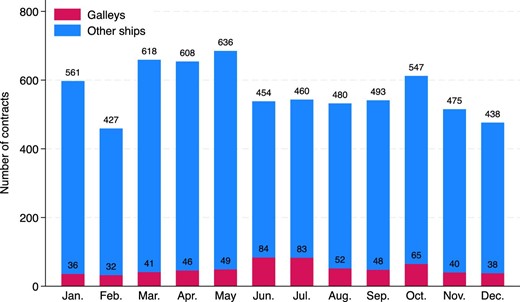

The most relevant distinction for our subsequent analysis of insurance premia is between galleys and all the other types of vessels. The armed galley represents one of the major nautical innovations of the 15th century as it exceeded the other vessels in safety and maneuverability, especially thanks to the high number of rowers and crossbowmen defending it from the attacks of corsairs, pirates, or the fleets of political and commercial competitors. Similar to the invention of insurance contracts, the galley was either an additional or an alternative way with which merchants could cope with the increased risks that corsairs in the Mediterranean posed to seaborne trade. Figure 3 shows the number of contracts relative to a generic vessel or a galley in each month. While navigation during the winter season was more risky due to the increased probability of natural risks, human risks (e.g., attacks by corsairs) were more likely to occur during the summer season, when corsairs could benefit more from attacking the increased number of shipments. Interestingly, the use of galleys increased during the summer, both in absolute and relative terms, suggesting that the use of the safer (but more costly) galley was a complement to the use of insurance contracts.

Monthly distribution of contracts.

With regards to seasonality, there seems to be not a large variation between the number of insurance contracts across months, which is consistent with the fact that advances in nautical technology during the Middle Ages made winter navigation feasible unlike in antiquity. The months with the lowest number of contracts are February and December (459 and 476 contracts, respectively), whereas the months with the highest number of contracts are May and March (685 and 659 contracts, respectively). The monthly distribution of the contracts might have followed the seasonality of the production and consumption of certain goods. In particular, since wheat shipments are a relevant part of our dataset, it is possible that the monthly fluctuations in the number of contracts coincided with fluctuations in the market for wheat (e.g., the increase in the number of contracts in September and October occurred right after August when wheat was harvested).

5.2 Structure of Medieval Insurance Markets

Let us first start with a narrative description of the participants in the insurance business. The most recurring insurer in our dataset is Tobia Usodimare, a Genoese merchant. Between 1422 and 1433, he participated as an insurer in 293 different contracts for a total insured amount of 21.625 florins (an astonishing amount at that time). The Usodimare family was a well-known aristocratic family of merchants. Among the big insurers from Genoa, we also find members of many important families such as De Marinis, De Mari, Grillo, Grimaldi, Spinola, Calvi, Cattaneo, Lomellino, and Lercari. All such families were part of the aristocratic mercantile establishment of Genoa and had great influence on the political life of the city. From the insurance contracts in the dataset, it is clear that they represented the core of the insurance market in Genoa.

In Palermo, the insurance market was more varied. We find members of different well-known families from Palermo, Genoa, and Tuscany as well as many Catalan insurers. The insurer with the highest number of contracts (253) is Federico Lanza from the noble Lanza family founded in the 10th century.

Moving to a more quantitative analysis of the dataset, the 7,000 insurance contracts show one clear pattern: in the first 150 years since their rise, medieval insurance markets feature two main types of insurers. The first group consists of a small group of merchants, bankers, and aristocrats who had substantial wealth from their broad and diversified businesses, could benefit from a wide trading and information network across the main commercial centers and ports, and, hence, could pool risks. We encounter their names over and over again among the underwriters, some of them even hundreds of times.

The second group of insurers, which is by far the largest group in our dataset, includes those who participated in the insurance market only once or seldom. Among the latter group, we encounter artisans insuring small quotas. This second group of insurers, however, accounted for only a small share of the market.

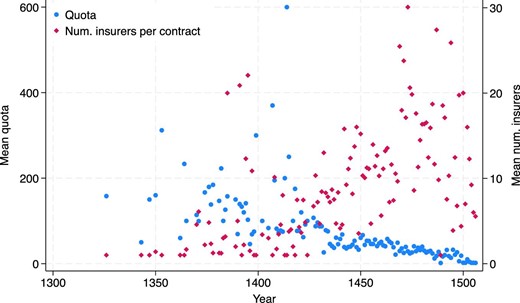

During the second half of the 14th century, most contracts involved a single insurer, typically a very wealthy merchant or banker, who alone took the risk of major losses (of the order of hundreds of florins). During the 15th century, though, the market broadened with many more individuals (often small artisans or merchants) entering the insurance business, often insuring small quotas. The number of insurers per contract increased to the extend that we even find 70 individuals involved in a single contract, with an average between 10 and 20 (Figure 4).

Mean quotas are yearly averages over insurer-contract pairs. Quotas are expressed in gold florins. Mean number of insurers is the yearly average of the number of insurers per contract.

Figure 4 also shows that while the average number of insurers per contract increased over time, the average quota insured by each of them diminished, and overall the average total value insured in each contract remained more or less stable during the period considered. With the development of insurance markets, merchants were buying more protection through a higher coverage and, at the same time, they were getting insured by more insurers, each insuring smaller quotas of the coverage.

Although many people were increasingly entering the insurance business, the supply side of insurance markets remained very concentrated until the end of the 15th century. Not only a few insurers underwrote most contracts, but they also participated insuring systematically bigger quotas of the total coverage. Consistent with the advice given by Cotrugli (1573) in his treatise on commerce, these merchants who were insuring high quotas did it several times, in order to reduce, on average, the risks undertaken. Table 5 shows the level of concentration in the insurance market. Insurers in the top percentile for number of contracts underwrote more than 35% of the contracts for more than 40% of the total value insured. Each of them undersigned at least 61 contracts. In contrast, insurers in the bottom half of the distribution accounted for around 8% of the market, both in terms of contracts and quotas insured, and insured only one shipment.

Supply side market shares.

| Contracts per insurer | 1 | 2–3 | 4–12 | 13–24 | 25–60 | 61–293 |

|---|---|---|---|---|---|---|

| Percentile | 1–55 | 56–74 | 75–89 | 90–94 | 95–98 | 99–100 |

| Shares: | ||||||

| Contracts | 8.39 | 6.34 | 15.12 | 12.93 | 22.15 | 35.07 |

| Quotas | 7.09 | 5.51 | 12.69 | 11.99 | 21.84 | 40.89 |

| Contracts per insurer | 1 | 2–3 | 4–12 | 13–24 | 25–60 | 61–293 |

|---|---|---|---|---|---|---|

| Percentile | 1–55 | 56–74 | 75–89 | 90–94 | 95–98 | 99–100 |

| Shares: | ||||||

| Contracts | 8.39 | 6.34 | 15.12 | 12.93 | 22.15 | 35.07 |

| Quotas | 7.09 | 5.51 | 12.69 | 11.99 | 21.84 | 40.89 |

Notes: Individual insurers are divided into six groups depending on how many contracts they insure. The corresponding percentiles are indicated in the second row. The third and fourth rows present the market share of the group in terms of contracts and quotas.

Supply side market shares.

| Contracts per insurer | 1 | 2–3 | 4–12 | 13–24 | 25–60 | 61–293 |

|---|---|---|---|---|---|---|

| Percentile | 1–55 | 56–74 | 75–89 | 90–94 | 95–98 | 99–100 |

| Shares: | ||||||

| Contracts | 8.39 | 6.34 | 15.12 | 12.93 | 22.15 | 35.07 |

| Quotas | 7.09 | 5.51 | 12.69 | 11.99 | 21.84 | 40.89 |

| Contracts per insurer | 1 | 2–3 | 4–12 | 13–24 | 25–60 | 61–293 |

|---|---|---|---|---|---|---|

| Percentile | 1–55 | 56–74 | 75–89 | 90–94 | 95–98 | 99–100 |

| Shares: | ||||||

| Contracts | 8.39 | 6.34 | 15.12 | 12.93 | 22.15 | 35.07 |

| Quotas | 7.09 | 5.51 | 12.69 | 11.99 | 21.84 | 40.89 |

Notes: Individual insurers are divided into six groups depending on how many contracts they insure. The corresponding percentiles are indicated in the second row. The third and fourth rows present the market share of the group in terms of contracts and quotas.

With regards to the demand side of insurance markets, we observe that, alongside merchants, many small artisans and business owners got insured. Some of them were shoemakers, cheese makers, blacksmiths, bakers, and furriers. The distribution of contracts among insured appears to be less uneven than the one among insurers. In the dataset, there are 2,391 individuals purchasing insurance. Among them, 1,623 bought insurance only once, 498 two or three times, and 270 more than three times. Unlike the supply side, the demand side was not much concentrated. Table 6 shows that in about a third of contracts, there was a merchant who bought insurance only once. Moreover, the top percentile of those who bought insurance, underwrote less than 15% of the contracts.

Demand side market shares.

| Number of contracts | 1 | 2 | 3–6 | 7–11 | 12–44 |

|---|---|---|---|---|---|

| Percentile | 1–67 | 68–82 | 83–94 | 95–98 | 99–100 |

| Shares: | |||||

| Contracts | 33.20 | 14.48 | 23.34 | 14.62 | 14.36 |

| Quotas | 31.87 | 13.90 | 24.82 | 14.61 | 14.80 |

| Number of contracts | 1 | 2 | 3–6 | 7–11 | 12–44 |

|---|---|---|---|---|---|

| Percentile | 1–67 | 68–82 | 83–94 | 95–98 | 99–100 |

| Shares: | |||||

| Contracts | 33.20 | 14.48 | 23.34 | 14.62 | 14.36 |

| Quotas | 31.87 | 13.90 | 24.82 | 14.61 | 14.80 |