Abstract

We compare causal effects of forward guidance about future interest rates on households’ expectations of inflation and nominal mortgage rates to the effects of communication about inflation in a randomized control trial using more than 20,000 U.S. consumers in the Nielsen Homescan Panel. We elicit consumers’ expectations, and then provide 22 different forms of information regarding past, current, and/or future interest rates and inflation. Information treatments about current or future interest rates all have similar and offsetting effects on interest rate and inflation expectations, yielding limited pass-through into perceived real rates. Information about mortgage rates has much more powerful effects on interest rate perceptions, with no offsetting effects on inflation expectations, thereby delivering much larger changes in perceived real rates. Revisions in perceived real rates causally lead to changes in the ex-post purchases of durable goods by households.

“Under the empirically reasonable assumption that what matters for aggregate spending is the entire expected path of short-term rates rather than just the current level, [forward guidance] enables the Fed to provide substantial additional accommodation during zero lower bound episodes. The strategy also potentially supports aggregate demand by raising inflation expectations, thereby lowering real long-term rates relative to a Taylor Rule type baseline.” Janet Yellen, September 2018.1

“After all, it is the everyday economic decisions of people and companies that we seek to influence with our policy and communication. If our language is not accessible, our policy will be less effective.” Christine Lagarde, February 2020.2

“The limits to forward guidance depend on what the public understands, and what it believes. In normal times, the general public does not pay much attention to central bank statements, so robust policies should be designed to be effective even if they are followed closely only by financial market participants. ... policymakers must communicate consistently and intelligibly.” Ben Bernanke, January 2020.3

1. Introduction

As monetary policymakers in many advanced economies pushed short-term interest rates to zero both during the financial crisis and during the recent COVID-19 pandemic, attention quickly turned to other tools that could be used to further stimulate economic activity. Along with quantitative easing, forward guidance about the path of future interest rates became one of the main tools that central banks developed to address the exceptional circumstances they have been facing. Understanding how forward guidance affects economic outcomes is therefore a central question. But because the mechanism of forward guidance is via expectations and these are not readily observable, it has been difficult to establish how announcements about the future actually affect individual economic actors.

In this paper, we implement a large-scale randomized control trial (RCT) on a representative sample of about 20,000 U.S. consumers to whom we provide, in a randomized fashion, different pieces of information about the evolution of future interest rates as well as about past and current policy rates and inflation. This RCT approach provides a transparent way to assess whether the exogenous provision of information about interest rates and inflation changes households’ economic expectations. The large scale of the experiment allows us to characterize in unprecedented detail how the magnitude of the treatment as well as the time horizon of the announcement affects the size of consumers’ forecast revisions and how they change their views about different economic variables (e.g. long-term interest rates vs. inflation). We can also assess whether the resulting variation in perceived real interest rates of households changes their actual spending decisions on both durables and non-durables.

Households’ expectations play a central role in the transmission of forward guidance into economic outcomes through several channels. Forward guidance operates in part via financial markets, which determine changes in long-term nominal interest rates. The pass-through of these interest rates into consumption and saving decisions then determines how large the effect of forward guidance through the financial markets channel is. It is well documented that households exhibit considerable inertia in their borrowing decisions (e.g. in refinancing their fixed rate mortgages in a period of declining interest rates; see Campbell 2006; Andersen et al. 2020) . Recently, D’Acunto et al. (2018b) find that many households do not adjust their mortgage choices to changes in interest rates. We provide new evidence on households’ perceptions of market interest rates and how they respond to different types of information that speaks directly to the potential strength of this channel.

An additional channel through which forward guidance should stimulate spending is via the inflation expectations of households: If households anticipate larger price increases in the future, then they have an incentive to spend more today. We show that in standard New Keynesian models this is often the most powerful transmission channel of forward guidance. However, prior work should give one pause before placing much faith in this channel. D’Acunto, Hoang, and Weber (2022), for example, show that European households did not adjust their inflation expectations in the months bracketing the initial forward guidance announcement by the European Central Bank (ECB). Our results speak to the potential strength of this additional channel by characterizing how inflation expectations respond to different types of information about current and future interest rates.

We document a number of new results from this large-scale experiment. First, prior to any information treatment, we find that households’ knowledge about market interest rates is limited: The cross-sectional dispersion in their beliefs about the level of the 30-year mortgage rate is as high as previously documented for their beliefs about inflation (e.g. Coibion, Gorodnichenko, and Weber 2022). This lack of knowledge on the part of many consumers about one key interest rate is suggestive that pass-through of forward guidance from financial markets to households may be limited. Second, we find that the provision of information to households about current, past, and future policy rates of the Federal Reserve has only limited effects on households’ perceptions of both current and future market interest rates even though they result in large actual changes in mortgage rates (Eichenbaum, Rebelo, and Wong 2022). Households place a weight of 80%–90% on their prior beliefs about interest rates when they receive signals about past, current, or future policy rates. This again suggests that communication about policy rates is unlikely to lead to large changes in household spending. Third, providing information about current, past, and future policy rates leads households to revise their inflation expectations by large amounts: those with initially high inflation expectations lower them while those with low expectations raise them. Households place a weight of only 10%–20% on their prior inflation expectations when provided with information about policy rates. Despite the limited effect of information treatments about policy interest rates on the expected interest rates of households, their perceived real interest rates still change due to the sensitivity of their inflation expectations: The implied weight on their prior beliefs about real rates relative to the control group is on the order of 40%–60% depending on the specific information treatment. We then confirm that exogenous variation in the perceived real interest rates of households affects their subsequent durable goods purchases.

We find even more promising results for communication strategies focusing on long-term market interest rates themselves. One of our information treatments consists of informing households about the current 30-year mortgage rate. This treatment leads to a very strong response in households’ perceptions of the mortgage rate (an almost complete convergence in beliefs to the provided information), which extends into households’ expectations about future long-term rates as well. In addition, and unlike what was found with either policy rate or inflation rate treatments, providing information to households about the mortgage rate leads to almost no revision in their inflation expectations. The resulting effect on their perceived real interest rate is much larger than what we observe with other treatments: Implied weights on prior beliefs about real rates are only about 10%–30%, indicating that this treatment leads to large average revisions in perceived real interest rates. Consistent with Angeletos and Sastry (2021), this result implies that communication about the target (in this case, the mortgage interest rate) may be a more effective form of forward guidance than communication about the policy rate. And since we also show below that exogenously generated changes in households’ perceived real interest rates affect households’ ex-post purchases of durable goods, communication about market interest rates could provide a much more powerful way of stimulating consumption than forward guidance about future policy rates.

To measure how households’ expectations change in response to information treatments, we first elicit households’ expectations on a host of variables including inflation and nominal mortgage rates. Subsequently, we provide information treatments to households, and finally, elicit household expectations again, both shortly after the treatment as well as after 3 and 6 months. The latter allows us to characterize how persistent the effects of different information treatments are on households’ expectations. We document that treatments about policy rates and inflation have somewhat persistent effects, present after 3 months but significantly dampened after 6 months. In contrast, the treatment involving mortgage rates dissipates much more rapidly.

Because our survey has such a large cross-section, we can consider an exceptionally large number of different treatments relative to previous work and perform multiple comparisons. Specifically, we vary (i) the variable on which we provide information: policy rates, inflation, and mortgage rates; (ii) the horizon over which we provide information: current, past, and future periods up to 3 years into the future and for the longer run; and (iii) the interest rate trajectories: central tendency, upper range, and lower range. This variety in treatments is the source of our ability to identify in such detail what types of information affect households’ beliefs most and which dimensions are less important. For example, we find very little effect stemming from the time horizon of information about policy rates: Whether the information is only about current rates or extends to several years out seems to have little marginal effect on beliefs. The fact that households do not adjust their expectations to a larger extent to information beyond 1 year provides empirical support to theories that model decision makers with limited capacity to collect and process information: for example, limited planning horizons (Woodford 2018), bounded rationality (Gabaix 2020), level-k thinking (Farhi and Werning 2019), or lack of common information (Angeletos and Lian 2018). While the exact micro foundations differ across studies, they share the feature that agents with limited abilities are not necessarily more responsive to information in the far future relative to information about the current and immediate future.

The recent focus of policymakers on forward guidance originates in part from the fact that conventional monetary policy was no longer feasible once policy rates hit the effective lower bound. One potential caveat of our survey could therefore be that we implemented it during a period in which the U.S. had already normalized interest rates to positive levels. We believe our findings still provide important insights for several reasons. First, many households have expectations and perceptions of current interest rates that deviate significantly from the actual rates so their reaction in the survey is informative about how individuals would actually react to a forward guidance announcement. Second, the use of forward guidance long predates the Great Recession and the extent to which forward guidance affects financial markets has been studied not only during the zero bound but also outside of it (Gürkaynak et al. 2005). Third, central bankers anticipate that forward guidance and other communications-based policies can become a more conventional tool in the future (Blinder et al. 2017). Fourth, to the extent we exploit cross-sectional variation, we keep constant the level of interest rates and exploit differences in the reaction of individuals to different information treatments. This cross-sectional variation, because it identifies the weight households place on their priors, nonetheless also speaks to the weight that households place on new information and therefore to the first-round effects of communication strategies.

Randomized controlled trials have recently become more common in macroeconomics (e.g. Binder and Rodrigue 2018; Armona, Fuster, and Zafar 2019; Coibion et al. 2020a, 2021; D’Acunto et al. 2020; Roth and Wohlfart 2020). Following the design of research in applied micro and development, these papers typically study how randomized treatments affect individuals’ expectations and decisions in domains that are directly affected by the treatments. Yet, in macroeconomic contexts, feedback effects, general equilibrium effects, and the expectations on how other aggregate variables move in response to the treatment are important for the overall response of individuals. A central innovation in our survey design is the fact that we can jointly study the response of several economic expectations to our different treatments to better predict how individuals form expectations jointly and how they might react to actual announcements by central banks on how the future path of policy rates or inflation might evolve. Furthermore, we study how information about past, current, and future policy rates influence expectations of households and contrast these responses with those of households who are informed about inflation, a powerful force for moving households’ expectations about macroeconomic variables (e.g. Coibion, Gorodnichenko, and Weber 2022) as well as a strong determinant of households’ consumption (e.g. D’Acunto et al. 2016; Coibion et al. 2019) in the U.S.4

Our paper is closely related to an extensive body of work on the effect of forward guidance (Campbell et al. 2012; Del Negro et al. 2015; Andrade and Ferroni 2021). However, we differ from this work along a number of dimensions. First, much of this work (e.g. Chodorow-Reich 2014) has concentrated on how forward guidance affects financial markets and nominal interest rates of different maturities. We complement this literature by providing evidence on how households respond to information about interest rates. We show, for example, that providing information about future interest rates changes not just the perceived path of nominal rates but also inflation expectations, so that the pass-through to households’ real interest rates is much less than one-for-one. In addition, households may be sensitive not just to the level of long-term interest rates but also to their expected path: The timing of durable goods purchases is likely to depend on whether households expect interest rates to rise or fall in the future because purchases of durable goods have a very high intertemporal elasticity of substitution (e.g. House and Shapiro 2008). We regard our results on the response of households’ interest and inflation expectations as complementary to earlier work focusing on financial markets by helping to identify additional channels through which forward guidance shapes economic outcomes. Because households’ income expectations could also change in response to forward guidance, our results should not be interpreted as necessarily fully characterizing the response of households, and other expectations channels could also be important.5

Another strand of literature focuses on the aggregate effects of forward guidance, primarily using time series analysis (e.g. Swanson 2021; see Bhattarai and Neely 2012 for a survey). This research is of direct use in measuring how the economy responds to forward guidance, but it does not speak directly to the underlying mechanisms at work. Our approach is complementary: We are able to identify how households’ expectations and spending respond to information about current and future interest rates, but are unable to speak directly to the general equilibrium effects that would obtain were all households to respond in a similar fashion. However, by more precisely identifying the mechanisms, the horizon over which forward guidance operates, and the variable which central banks give guidance about, we hope that our work can be used to differentiate between and quantify models of forward guidance, which in turn can then be used for policy analysis and counterfactuals.

A recent strand of the theoretical literature develops models that limit the power of forward guidance either through deviations from full information rational expectations (Angeletos and Lian 2018; Woodford 2018; Farhi and Werning 2019; Gabaix 2020) or via introducing market incompleteness and constraints (Werning 2015; McKay et al. 2016; Kaplan et al. 2018; Hagedorn et al. 2019). We empirically add to this literature and study how individuals adjust their expectations to news about interest rates and inflation, how they adjust their consumption choices, and heterogeneity in the responses.

Our paper also relates to a much broader literature on central bank communication and how this communication shapes household expectations and decision-making. This literature has emphasized two general stylized facts for advanced economies. First, households (and firms) are often inattentive to policy and relatively uninformed about macroeconomic aggregates. Second, despite this inattention, households’ expectations about future aggregate conditions affect their decisions (see Coibion et al. 2020b; Weber et al. 2022; D’Acunto et al. 2022a for surveys of this literature). The results in this paper corroborate these two stylized facts but do so in the specific context of forward guidance. This growing body of evidence supports the recent interest among policymakers in rethinking their communication strategies with the public and suggests a need for more research to better understand the link between policy announcements and the decision-making process of economic agents.

Finally, some features of our approach are worth clarifying. First, most households do not actively follow central bank announcements (Lamla and Vinogradov 2019), even when major policy changes are made (Coibion et al. 2020a). In our survey experiment, we focus on an intensive margin of central bank communication, that is, we provide different information to agents and study which message is most effective in moving expectations, but we cannot speak to the extensive margin of information acquisition. Hence, our results on the effect of communication on expectations inform policymakers on the potential power of forward guidance to the extent they are able to reach consumers with their communication. Second, actual forward guidance announcements often provide additional context on the state of the economy, the economic outlook, and potential state dependence in the guidance such as a level of unemployment rate that has to be reached before considering interest rate changes. Previous work (Coibion, Gorodnichenko, and Weber 2022) finds that households revise their expectations similarly regardless of whether they only receive summary statistics for inflation or policy rates (as we provide here) or whether they are provided with substantially more details from actual policy statements. Third, forward guidance in practice is often about the future path of policy rates. We provide information not just about future rates but also about current and past interest rates, as well as on inflation and mortgage rates, because no systematic evidence exists so far on which form of guidance is most powerful in shaping individuals’ expectations. Policy rates are not directly relevant for most consumer decisions. Mortgage rates, on the other hand, are an important transmission channel of monetary policy (Wong 2020). Given that most mortgages in the U.S. are fixed rate mortgages, households have an incentive to be informed about the evolution of these rates to determine refinancing decisions (Berger et al. 2021; Eichenbaum et al. 2022). Last, inflation expectations are a key determinant of households’ saving and consumption decisions and, in New Keynesian models, forward guidance often operates primarily through inflation expectations.

2. Expectations and Consumption

A common narrative used by policymakers to describe how forward guidance affects household consumption is as follows: Forward guidance about future short-term rates will lower long-term rates, households will then reduce their saving and increase their spending while their inflation expectations remain well-anchored. We will refer to this as the “policy narrative”. In the context of the equation above, this narrative is built on the idea that forward guidance leads to a change in the long-term rate |$(di_t^m)$| , that households observe and respond to market rates |$(di_t^{hh}=di_t^m)$|, and that “well-anchored” inflation expectations are stable, that is, |$d(\sum _{j=0}^{\infty }E_t^{hh}\pi _{t+j+1})\approx 0$|. In short, the change in consumption from the policy narrative is |$dc_t^{ {pol}}=-\sigma di_t^m$|. In this narrative, all that is needed to evaluate the effect of forward guidance on consumption is the degree to which financial markets responded to the announcement, which is summarized by the response of the long-term nominal interest rate.

In standard New Keynesian models, the effect of forward guidance is generally quite large and certainly larger than what is implied by the policy narrative. With full-information rational expectations, household expectations of the long-rate are identical to the market rate, so |$i_t^m-i_t^{hh}=0$| and pass-through of changes in market interest rates into spending is complete. In addition, to the extent that forward guidance should induce higher inflation in subsequent periods and households anticipate this |$(d(\sum _{j=0}^{\infty }E_t^{hh}\pi _{t+j+1})> 0)$|, the expected inflation channel will also be present. Thus, |$dc_t^{NK}=-\sigma di_t^{m}+\sigma d(\sum _{j=0}^{\infty }E_t^{hh}\pi _{t+j+1})$|. Importantly, it is the inflation expectations of households, not of financial markets, which magnifies the effect of forward guidance on consumption decisions in standard macroeconomic models. Understanding how these household inflation expectations respond in practice therefore can help explain how much forward guidance affects economic outcomes.

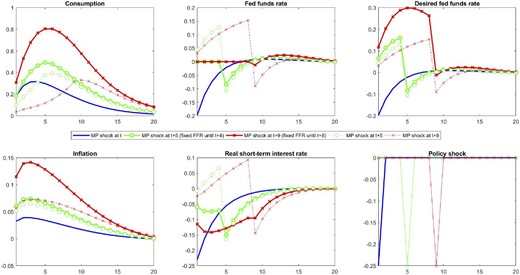

To illustrate how either channel can dominate in driving the response of consumption, we plot responses to different types of monetary shocks in the benchmark Smets and Wouters (2007) model in Figure 1. The first such shock is a standard contemporaneous expansionary 25 basis points monetary policy shock. The associated persistent decline in the policy rate implies that the contemporaneous long-term (10-year) interest rate falls on impact (by 0.04% points) while expected inflation rises (by 0.03% points per year over 10 years), so that the real long-term interest rate falls sharply due to both channels, leading to a rise in consumption. With forward guidance shocks, however, the expected inflation channel becomes more important. For example, Figure 1 plots the effects of pre-announced expansionary monetary shocks 5 and 9 quarters later, assuming the policy rate is unconstrained before. The expected decline in future short-term rates leads to a rise in expected inflation and a boom in current activity. These announcements also induce a sharp rise in short-term interest rates before the monetary shocks are realized. In these cases, the contemporaneous long-term interest rate rises following the forward guidance announcement. The contemporaneous increase in consumption is therefore driven by the persistent rise in households’ expectations of future inflation. In this case, focusing on how long-term nominal interest rates set in financial markets responded to this shock would mischaracterize the effect on consumption.

Response to current and anticipated policy shocks in the baseline Smets–Wouters model.

Notes: The figure plots impulse responses to different monetary shocks in the baseline Smets and Wouters (2007) model. The model uses parameter values estimated in Smets and Wouter (2007). “MP shock at time t” is the case of a 25 basis point shock to the Taylor rule happening contemporaneously (at time 1). “MP shock at time t|$+$|5(t|$+$|9)” is the case in which a 25 basis point expansionary monetary shock is pre-announced 1 year (2 years) prior, that is, the announcement is made at time 1 but the shock only occurs in quarter 5 (9). “MP shock at time t|$+$|5 (fixed FFR until t|$+$|4)” is the case of a 25 basis point monetary shock happening in quarter 5 but pre-announced at time 1, with the policy rate made to be fixed until the shock is realized. “MP shock at time t|$+$|9 (fixed FFR until t|$+$|8)” is analogous to previous case but with a 2-year gap between announcement and policy shock.

Even if we assume that policy rates are fixed prior to the pre-announced shock (also shown in Figure 1) so that the long-term interest rate must fall on impact, then the expected inflation effect quantitatively drives the behavior of consumption. For example, when the shock is pre-announced by 1 year, the long-term (10-year) nominal interest rate falls by only 1 basis point, while the change in expected inflation is six times larger. The effect of forward guidance on consumption in a standard macroeconomic model therefore hinges on households’ expectations of future inflation, not just the response of long-term nominal interest rates set in financial markets.

Moving beyond full-information models, one can also allow for the possibility that changes in market interest rates are not fully incorporated into households’ perceptions of these rates (i.e. |$di_t^{hh}\ne di_t^m$|). In that case, changes in consumption depend on how households’ perceptions of market rates change with forward guidance, as well as their inflation expectations |$dc_t^{{gen}}=-\sigma di_t^{hh}+\sigma d(\sum _{j=0}^{\infty }E_t^{hh}\pi _{t+j+1})$|. Abstracting from general equilibrium effects, forward guidance can have larger effects than in the standard model if household expectations over-react relative to markets (as in e.g. Bordalo et al. 2020). If instead households are very inattentive and do not change their perceptions of interest rates and their inflation expectations at all, then forward guidance can be impotent in affecting consumption |$(dc_t^{{gen}}=0$|) regardless of what happens in financial markets.

3. Data and Survey Design

This section describes our survey design to elicit expectations, the various treatments, and provides descriptive statistics for a range of expectations and perceptions. We first detail the Nielsen Homescan panel on which we run the survey and provide more information on the structure of the survey.

3.1. Nielsen Panel

In March, June, and September of 2019, we fielded three waves of the Chicago Booth Expectations and Communications Survey inviting participation by all household members in the Kilts–Nielsen Consumer Panel (KNCP). The KNCP represents a panel of approximately 80,000 households that report to Nielsen (i) their static demographic characteristics, such as household size, income, ZIP code of residence, and marital status, and (ii) the dynamic characteristics of their purchases, that is, which products they purchase, at which outlets, and at which prices. Panelists update their demographic information at an annual frequency to reflect changes in household composition or marital status.

Nielsen attempts to balance the panel on nine dimensions: household size, income, age of household head, education of female household head, education of male household head, presence of children, race/ethnicity, and occupation of the household head. Panelists are recruited online, but the panel is balanced using Nielsen’s traditional mailing method. Nielsen checks the sample characteristics on a weekly basis and performs adjustments when necessary.

Nielsen provides households with various incentives to ensure the accuracy and completeness of the information they report. These incentives include monthly prize drawings, providing points for each instance of data submission, and engaging in ongoing communication with households. Panelists can use points to purchase gifts from a Nielsen-specific award catalog. Nielsen structures the incentives to not bias the shopping behavior of their panelists. The KNCP has a retention rate of more than 80% at the annual frequency. Nielsen validates the reported consumer spending with the scanner data of retailers on a quarterly frequency to ensure high data quality and filters households that do not report a minimum amount of spending over the previous 12 months.

3.2. Chicago Booth Expectations and Communication Survey

Nielsen runs surveys on a monthly frequency on a subset of panelists in the KNCP, the online panel, but also offers customized solutions for longer surveys. Retailers and fast-moving consumer-goods producers purchase this information and other services from Nielsen for product design and target-group marketing. At no point of the survey did Nielsen tell their panelists that the survey we fielded was a part of academic research which minimizes the concerns of survey demand effects (de Quidt et al. 2018).

In early 2019, we designed a customized survey consisting of 34 questions in total in cooperation with Nielsen, the Chicago Booth Expectations and Communication Survey. The survey also contains 22 different information treatments, one placebo treatment as well as one control group. Our survey design builds on the Michigan Survey of Consumers, the New York Fed Survey of Consumer Expectations (SCE), the Dutch National Bank’s Household Survey as well as D’Acunto et al. (2021b), Coibion, Gorodnichenko, and Weber (2022), and Coibion et al. (2020b).

Nielsen fielded the first wave of the survey in March of 2019. The survey sample was 92,982 households. 26,929 individuals (from 24,886 households) responded for a response rate of 26.80% and an average response time of 19 minutes and 35 seconds. The second and third waves consisted mostly of follow-up questions, with median response times of about 19 minutes and 28,580 unique respondents for the second wave (June 2019; 16,726 participated in the initial wave) and 15,912 unique respondents for the third wave (September 2019; 8,152 participated in the initial wave). Nielsen provides weights to ensure representativeness of the households participating in the survey. The response rate compares favorably with other ad-hoc surveys and is similar to other studies running surveys on Nielsen, such as D’Acunto et al. (2021b). For example, Qualtrics estimates an average response rate between 5 and 10% across their surveys (D’Acunto et al. 2022b).

The initial wave of the survey covers a wide range of questions. First, respondents are presented with a series of questions about their demographic characteristics, which are more detailed relative to the basic demographic information the KNCP provides. We collect information on employment status, current occupation, financial constraints, savings and portfolio choice, homeownership status, and past spending behavior in various categories, including expenses that are not covered in the KNCP, and we identify the primary shopper of the household among all the responding members (D’Acunto, Malmendier, and Weber 2019). Participants are then asked a sequence of questions about their perceptions and expectations of inflation. We follow the design in the SCE and ask specifically about inflation, because asking about prices might induce individuals to think about specific items whose prices they recall rather than about overall inflation (see Crump et al. 2022 for a recent paper using the SCE data). We first ask individuals about their perception of past inflation, that is, inflation over the previous 12 months. We then ask them about their expectations for 12-month-ahead inflation. We elicit a full probability distribution of expectations by asking participants to assign probabilities to different possible levels of the inflation rate. Finally, we also ask survey participants on their expectations regarding interest rates on a 30-years fixed rate mortgage at the end of 2019, 2020, 2021, and in the next 5–10 years. Subsequent waves largely follow the same structure. Hence, the follow-up surveys are primarily used to measure individuals’ perceptions and expectations of inflation and nominal mortgage rates.

3.3. Information Treatments

After respondents answered the initial set of questions in the first wave, they were assigned to one of 24 groups: a control group, one placebo treatment group, and 22 treatment groups. We designed the treatments to disentangle the effects of different possible types of forward guidance. We vary the target that is communicated: We not only communicate inflation forecasts or expected future policy rates but also vary the length of the forecast horizon, the exact information of the forecast, central tendency, upper range, or lower range, or all jointly, as well as different combinations. All future policy forecasts are taken from the Survey of Economic Projections submitted by Federal Open Market Committee (FOMC) members, which provide both central tendencies as well as a range of forecasts from FOMC members. In addition to information about future policy rates, some survey participants only received information about current/past rates. The latter treatments allow us to study the extent to which consumers might have differential responses to backward-looking versus forward-looking information. We also fielded a placebo treatment to differentiate true learning from spurious anchoring effects. Each group consists of approximately 1/24th of the total sample that received the survey and the treatments are randomly assigned. Online Appendix Table A.3 confirms that assignment of treatment was not predictable by respondents’ observable household and individual characteristics. Although the number of treatments is large and thus one may be concerned about inflated p-values due to multiple hypothesis testing, our sample size is so large and our estimates are so precise that p-values adjusted for multiple hypothesis testing are nearly identical to the conventional p-values.6

Our choice of treatments is motivated by a number of practical and theoretical considerations. Central banks often give forward guidance directly about the future path of their policy instrument, the Fed Funds Rate (FFR) in the U.S., with the goal of influencing contemporaneous long-term interest rates via the expectations hypothesis for interest rates, that is, changing financial market participants’ expectations of future short-term interest rates should be reflected in current long term interest rates. The transmission to the real economy then occurs because these long-term rates affect households’ and firms’ borrowing decisions and the purchase of durable goods and investment goods as the introductory quote by former Fed Chair Janet Yellen indicates.

Theoretically, forward guidance typically operates through affecting household expectations of inflation and the consumer Euler equation (Eggertson and Woodford 2003). Promises to keep interest rates low until after the end of the liquidity trap will be inflationary in the future and hence, households should already update upwards their inflation expectations today which during the liquidity trap period will translate into lower real rates and stimulate consumption. Therefore, we also directly provide treatments about the future path of interest rates and inflation to study whether forecasts for inflation or the path of interest rates are more effective in moving consumers’ expectations. Moreover, given that central banks often focus on a transmission mechanism through financial markets and household borrowing, we also directly study the reaction of individuals’ expectations regarding future mortgage rates and contrast the effects with the reaction of inflation expectations that are the focus in the academic literature and in virtually all models used by leading central banks.

Empirically, forward guidance appears to be less powerful than standard theory predicts, a phenomenon commonly referred to as the forward guidance puzzle (Del Negro et al. 2015; D’Acunto et al. 2022). Recent theoretical attempts (e.g. Angeletos and Lian 2018; Woodford 2018; Farhi and Werning 2019; Gabaix 2020) at resolving this puzzle that emerges in a representative agent New Keynesian model propose deviations from rational expectations as a possible resolution. While the exact microfoundations differ, they all attribute an important role to some form of limited cognition on the part of the consumer. These models attribute lower effectiveness of communication in the future on current day expectations to the fact that the agents in the model either do not plan that far into the future or they discount the information heavily. While we do not aim to disentangle the exact mechanism at play, the treatments with different horizons for the provided information can help assess whether these models are broadly consistent with the data.

Empirically, inflation expectations of households are widely dispersed suggesting some form of information friction. Given the evidence that many individuals are not well informed about the prevailing inflation rate and the possibility that agents form expectations adaptively, we also provided treatments that only informed households about the current inflation rate and policy rate. We then compare the reaction in forecasts to treatments about past, future or both pieces of information to better understand whether forward- or backward-looking expectations are a better description of expectations on average. The large cross-sectional component of our sample also allows us to study which type of consumers might have either forward- or backward-looking expectations.

Mortgage rates play a key role in the practice of monetary policy, yet central bankers typically do not directly communicate about mortgage rates or inflation (Wong 2020). D’Acunto et al. (2018b) find that many households do not change their borrowing behavior in response to changes in policy rates, possibly because they do not understand the implications of changes in policy rates on their borrowing rates. We therefore also directly provided some households with information about current mortgage rates with reference to a 30-year fixed rate mortgage (the most prevalent mortgage product in the U.S.). Thus, we examine whether communication about interest rates that are of direct interest to households might be more effective in guiding households’ expectations and decision-making.

Randomized control trials have gained interest in recent empirical macro studies but it is not yet clear how the provision of information on one macro variable jointly affects agents’ forecast for other variables that also affect economic behavior. Andre et al. (2022) find that many households differ in their reaction to fundamental shocks compared with the reaction of experts and models but nonetheless often revise expectations about different variables after structural shocks. Empirically, Coibion et al. (2019) find in an information provision experiment that households with exogenously higher inflation expectations lowered their spending on durables after the treatment because their overall economic outlook became more negative. Our setting allows us to study whether treatments about inflation or interest rates over different horizons might be a more promising communication tool for central banks to stimulate household spending because we can directly compare their effects on expectations but crucially also study in a systematic fashion how these treatments affect consumer expectations about inflation and mortgage rates jointly.

Finally, we also vary the trajectory for the future path of interest rates, that is, the high, central, and low forecasts for future interest rates. By varying the trajectory of future interest rates across treatment arms, we aim to understand whether these nuanced differences affect consumers’ expectations. Importantly, when we provided the different trajectories, we made clear that these were only one of the forecasts by the Federal Reserve and never mentioned whether it corresponded to the high, central, or low path. Also note that we use only Fed forecasts to avoid potential heterogeneity in the responses due to differences in the credibility of sources (see Coibion, Gorodnichenko, and Weber 2022). Our placebo treatment provided the actual fact that the U.S. population grew by 2.2% between 2015 and 2017. We report the treatments as part of the overall survey in the Online Appendix and provide a summary in Table 1.

Description of treatments.

| Horizon of provided information | ||||||||

|---|---|---|---|---|---|---|---|---|

| Treatment | Current | Future years | Past years | |||||

| ‘19 | ‘20 | ‘21 | LR | ‘15 | ‘16 | ‘17 | ||

| T2 (Population growth) | 2.2% | |||||||

| T3 (Current FFR) | 2.5% | |||||||

| T4 (FG FFR: LR high) | 2.5% | 3.1% | 3.6% | 3.6% | 3.5% | |||

| T5 (FG FFR: LR low) | 2.5% | 2.4% | 2.4% | 2.4% | 2.5% | |||

| T6 (FG FFR: LR central) | 2.5% | 2.8% | 3.1% | 3.0% | 2.8% | |||

| T7 (FG FFR: 1yr central) | 2.5% | 2.8% | ||||||

| T8 (FG FFR: 1yr high) | 2.5% | 3.1% | ||||||

| T9 (FG FFR: 1yr low) | 2.5% | 2.4% | ||||||

| T10 (FG FFR: 2yr central) | 2.5% | 2.8% | 3.1% | |||||

| T11 (FG FFR: 2yr central–high) | 2.5% | 2.8% | 3.6% | |||||

| T12 (FG FFR: 2yr central–low) | 2.5% | 2.8% | 2.4% | |||||

| T13 (FG FFR: 3yr central) | 2.5% | 2.8% | 3.1% | 3.0% | ||||

| T14 (FG FFR: 3yr central–high) | 2.5% | 2.8% | 3.1% | 3.6% | ||||

| T15 (FG FFR: 3yr central–low) | 2.5% | 2.8% | 3.1% | 2.4% | ||||

| T16 (FG FFR: LR central–high) | 2.5% | 2.8% | 3.1% | 3.0% | 3.5% | |||

| T17 (FG FFR: LR central–low) | 2.5% | 2.8% | 3.1% | 3.0% | 2.5% | |||

| T18 (FG FFR: LR central |$+$| past FFR) | 2.5% | 2.8% | 3.1% | 3.0% | 2.8% | 0.1% | 0.4% | 1.0% |

| T19 (Current FFR |$+$| past FFR) | 2.5% | 0.1% | 0.4% | 1.0% | ||||

| T20 (Inflation last year) | 1.8% | |||||||

| T21 (Average inflation over last 3 years) | 1.6% | |||||||

| T22 (Inflation last year |$+$| 3yr ahead inflation path forecast) | 1.8% | 1.9% | 2.1% | 2.1% | 2.0% | |||

| T23 (Inflation last year |$+$| 3yr ahead inflation average forecast) | 1.8% | 2.0% | ||||||

| T24 (Current mortgage rate) | 4.6% | |||||||

| Horizon of provided information | ||||||||

|---|---|---|---|---|---|---|---|---|

| Treatment | Current | Future years | Past years | |||||

| ‘19 | ‘20 | ‘21 | LR | ‘15 | ‘16 | ‘17 | ||

| T2 (Population growth) | 2.2% | |||||||

| T3 (Current FFR) | 2.5% | |||||||

| T4 (FG FFR: LR high) | 2.5% | 3.1% | 3.6% | 3.6% | 3.5% | |||

| T5 (FG FFR: LR low) | 2.5% | 2.4% | 2.4% | 2.4% | 2.5% | |||

| T6 (FG FFR: LR central) | 2.5% | 2.8% | 3.1% | 3.0% | 2.8% | |||

| T7 (FG FFR: 1yr central) | 2.5% | 2.8% | ||||||

| T8 (FG FFR: 1yr high) | 2.5% | 3.1% | ||||||

| T9 (FG FFR: 1yr low) | 2.5% | 2.4% | ||||||

| T10 (FG FFR: 2yr central) | 2.5% | 2.8% | 3.1% | |||||

| T11 (FG FFR: 2yr central–high) | 2.5% | 2.8% | 3.6% | |||||

| T12 (FG FFR: 2yr central–low) | 2.5% | 2.8% | 2.4% | |||||

| T13 (FG FFR: 3yr central) | 2.5% | 2.8% | 3.1% | 3.0% | ||||

| T14 (FG FFR: 3yr central–high) | 2.5% | 2.8% | 3.1% | 3.6% | ||||

| T15 (FG FFR: 3yr central–low) | 2.5% | 2.8% | 3.1% | 2.4% | ||||

| T16 (FG FFR: LR central–high) | 2.5% | 2.8% | 3.1% | 3.0% | 3.5% | |||

| T17 (FG FFR: LR central–low) | 2.5% | 2.8% | 3.1% | 3.0% | 2.5% | |||

| T18 (FG FFR: LR central |$+$| past FFR) | 2.5% | 2.8% | 3.1% | 3.0% | 2.8% | 0.1% | 0.4% | 1.0% |

| T19 (Current FFR |$+$| past FFR) | 2.5% | 0.1% | 0.4% | 1.0% | ||||

| T20 (Inflation last year) | 1.8% | |||||||

| T21 (Average inflation over last 3 years) | 1.6% | |||||||

| T22 (Inflation last year |$+$| 3yr ahead inflation path forecast) | 1.8% | 1.9% | 2.1% | 2.1% | 2.0% | |||

| T23 (Inflation last year |$+$| 3yr ahead inflation average forecast) | 1.8% | 2.0% | ||||||

| T24 (Current mortgage rate) | 4.6% | |||||||

Notes: The table shows information provided in each treatment. FFR is fed funds rate. FG is forward guidance. Treatments T3–T19 include information about fed funds rate.

Description of treatments.

| Horizon of provided information | ||||||||

|---|---|---|---|---|---|---|---|---|

| Treatment | Current | Future years | Past years | |||||

| ‘19 | ‘20 | ‘21 | LR | ‘15 | ‘16 | ‘17 | ||

| T2 (Population growth) | 2.2% | |||||||

| T3 (Current FFR) | 2.5% | |||||||

| T4 (FG FFR: LR high) | 2.5% | 3.1% | 3.6% | 3.6% | 3.5% | |||

| T5 (FG FFR: LR low) | 2.5% | 2.4% | 2.4% | 2.4% | 2.5% | |||

| T6 (FG FFR: LR central) | 2.5% | 2.8% | 3.1% | 3.0% | 2.8% | |||

| T7 (FG FFR: 1yr central) | 2.5% | 2.8% | ||||||

| T8 (FG FFR: 1yr high) | 2.5% | 3.1% | ||||||

| T9 (FG FFR: 1yr low) | 2.5% | 2.4% | ||||||

| T10 (FG FFR: 2yr central) | 2.5% | 2.8% | 3.1% | |||||

| T11 (FG FFR: 2yr central–high) | 2.5% | 2.8% | 3.6% | |||||

| T12 (FG FFR: 2yr central–low) | 2.5% | 2.8% | 2.4% | |||||

| T13 (FG FFR: 3yr central) | 2.5% | 2.8% | 3.1% | 3.0% | ||||

| T14 (FG FFR: 3yr central–high) | 2.5% | 2.8% | 3.1% | 3.6% | ||||

| T15 (FG FFR: 3yr central–low) | 2.5% | 2.8% | 3.1% | 2.4% | ||||

| T16 (FG FFR: LR central–high) | 2.5% | 2.8% | 3.1% | 3.0% | 3.5% | |||

| T17 (FG FFR: LR central–low) | 2.5% | 2.8% | 3.1% | 3.0% | 2.5% | |||

| T18 (FG FFR: LR central |$+$| past FFR) | 2.5% | 2.8% | 3.1% | 3.0% | 2.8% | 0.1% | 0.4% | 1.0% |

| T19 (Current FFR |$+$| past FFR) | 2.5% | 0.1% | 0.4% | 1.0% | ||||

| T20 (Inflation last year) | 1.8% | |||||||

| T21 (Average inflation over last 3 years) | 1.6% | |||||||

| T22 (Inflation last year |$+$| 3yr ahead inflation path forecast) | 1.8% | 1.9% | 2.1% | 2.1% | 2.0% | |||

| T23 (Inflation last year |$+$| 3yr ahead inflation average forecast) | 1.8% | 2.0% | ||||||

| T24 (Current mortgage rate) | 4.6% | |||||||

| Horizon of provided information | ||||||||

|---|---|---|---|---|---|---|---|---|

| Treatment | Current | Future years | Past years | |||||

| ‘19 | ‘20 | ‘21 | LR | ‘15 | ‘16 | ‘17 | ||

| T2 (Population growth) | 2.2% | |||||||

| T3 (Current FFR) | 2.5% | |||||||

| T4 (FG FFR: LR high) | 2.5% | 3.1% | 3.6% | 3.6% | 3.5% | |||

| T5 (FG FFR: LR low) | 2.5% | 2.4% | 2.4% | 2.4% | 2.5% | |||

| T6 (FG FFR: LR central) | 2.5% | 2.8% | 3.1% | 3.0% | 2.8% | |||

| T7 (FG FFR: 1yr central) | 2.5% | 2.8% | ||||||

| T8 (FG FFR: 1yr high) | 2.5% | 3.1% | ||||||

| T9 (FG FFR: 1yr low) | 2.5% | 2.4% | ||||||

| T10 (FG FFR: 2yr central) | 2.5% | 2.8% | 3.1% | |||||

| T11 (FG FFR: 2yr central–high) | 2.5% | 2.8% | 3.6% | |||||

| T12 (FG FFR: 2yr central–low) | 2.5% | 2.8% | 2.4% | |||||

| T13 (FG FFR: 3yr central) | 2.5% | 2.8% | 3.1% | 3.0% | ||||

| T14 (FG FFR: 3yr central–high) | 2.5% | 2.8% | 3.1% | 3.6% | ||||

| T15 (FG FFR: 3yr central–low) | 2.5% | 2.8% | 3.1% | 2.4% | ||||

| T16 (FG FFR: LR central–high) | 2.5% | 2.8% | 3.1% | 3.0% | 3.5% | |||

| T17 (FG FFR: LR central–low) | 2.5% | 2.8% | 3.1% | 3.0% | 2.5% | |||

| T18 (FG FFR: LR central |$+$| past FFR) | 2.5% | 2.8% | 3.1% | 3.0% | 2.8% | 0.1% | 0.4% | 1.0% |

| T19 (Current FFR |$+$| past FFR) | 2.5% | 0.1% | 0.4% | 1.0% | ||||

| T20 (Inflation last year) | 1.8% | |||||||

| T21 (Average inflation over last 3 years) | 1.6% | |||||||

| T22 (Inflation last year |$+$| 3yr ahead inflation path forecast) | 1.8% | 1.9% | 2.1% | 2.1% | 2.0% | |||

| T23 (Inflation last year |$+$| 3yr ahead inflation average forecast) | 1.8% | 2.0% | ||||||

| T24 (Current mortgage rate) | 4.6% | |||||||

Notes: The table shows information provided in each treatment. FFR is fed funds rate. FG is forward guidance. Treatments T3–T19 include information about fed funds rate.

Following each information treatment (as well as for the control group), respondents were again asked about their inflation forecasts, but this time in the form of a point estimate to avoid them having to answer the exact same question twice. This allows us to measure the instantaneous revision in expectations (if any) after the information treatments compared with the control group. The treatments were only applied in the first wave of the survey. In subsequent waves, respondents were again asked for their inflation expectations and perceptions, using identical questionnaires across all respondents in the two follow-up waves. We elicited inflation expectations via a full distribution in the follow-up wave and use the mean of the distribution and the inflation perception via point estimates. The first follow-up was 3 months after the initial wave and the second follow-up was after 6 months.

3.4. Preliminary Facts and External Validity

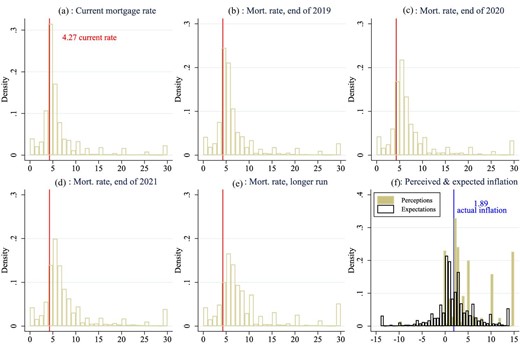

Table 2 shows descriptive statistics on consumer perceptions and expectations, both from the raw data and Huber (1964) robust moments that filter out outliers, with reference to inflation and nominal mortgage interest rates. The first panel (pre-treatment data) displays unconditional statistics before any information treatment is provided. For completeness, the second panel (post-treatment data) shows statistics collected after the information experiment. However, these are not directly comparable with pre-treatment statistics as they are aggregated over various groups receiving different treatments and the control group. To provide further insights into the heterogeneity of responses across consumers, we plot the distributions of (pre-treatment) perceptions and expectations about inflation and mortgage rates (Figure 2).

Distribution of pre-treatment perceptions and expectations of mortgage rate and inflation.

Notes: Mortgage rates are censored at 30%. Perceived inflation rate (point prediction) is censored at |$-$|10% and 15%. The blue vertical line shows actual inflation rate at the time of the survey. The red vertical line shows actual mortgage rate at the time of the survey. Expected inflation rate is based on the mean implied by the reported probability distribution for the 1-year-ahead inflation forecast.

Descriptive statistics.

| Robust moments | Moments | ||||

|---|---|---|---|---|---|

| Mean | Standard Deviation | Mean | Median | Standard Deviation | |

| (1) | (2) | (3) | (4) | (5) | |

| Pre-treatment data | |||||

| Perceived inflation, previous 12 months | 2.88 | 2.41 | 7.41 | 3.00 | 13.23 |

| Expected inflation, 12-month ahead | 2.32 | 2.02 | 3.62 | 2.60 | 3.69 |

| Perceived and expected mortgage rate for a “person like you” | |||||

| Current | 4.55 | 1.19 | 7.13 | 4.80 | 8.63 |

| End of 2019 | 4.90 | 1.44 | 7.59 | 5.00 | 8.74 |

| End of 2020 | 5.28 | 1.65 | 8.20 | 5.50 | 9.26 |

| End of 2021 | 5.53 | 1.92 | 8.74 | 6.00 | 10.07 |

| Next 5–10 years | 5.95 | 2.35 | 9.78 | 6.00 | 11.71 |

| Post-treatment data | |||||

| Expected inflation, 12-month ahead | 1.89 | 1.54 | 4.06 | 2.00 | 9.63 |

| Expected inflation, next 3–5 years | 2.42 | 1.79 | 4.65 | 3.00 | 9.47 |

| Perceived and expected mortgage rate for a “person with excellent credit” | |||||

| Current | 4.13 | 1.07 | 5.72 | 4.00 | 7.33 |

| End of 2019 | 4.39 | 1.09 | 6.02 | 4.50 | 6.96 |

| End of 2020 | 4.73 | 1.37 | 6.52 | 5.00 | 7.40 |

| End of 2021 | 4.97 | 1.57 | 6.88 | 5.00 | 7.83 |

| Next 5–10 years | 5.36 | 1.90 | 7.70 | 5.50 | 9.24 |

| Robust moments | Moments | ||||

|---|---|---|---|---|---|

| Mean | Standard Deviation | Mean | Median | Standard Deviation | |

| (1) | (2) | (3) | (4) | (5) | |

| Pre-treatment data | |||||

| Perceived inflation, previous 12 months | 2.88 | 2.41 | 7.41 | 3.00 | 13.23 |

| Expected inflation, 12-month ahead | 2.32 | 2.02 | 3.62 | 2.60 | 3.69 |

| Perceived and expected mortgage rate for a “person like you” | |||||

| Current | 4.55 | 1.19 | 7.13 | 4.80 | 8.63 |

| End of 2019 | 4.90 | 1.44 | 7.59 | 5.00 | 8.74 |

| End of 2020 | 5.28 | 1.65 | 8.20 | 5.50 | 9.26 |

| End of 2021 | 5.53 | 1.92 | 8.74 | 6.00 | 10.07 |

| Next 5–10 years | 5.95 | 2.35 | 9.78 | 6.00 | 11.71 |

| Post-treatment data | |||||

| Expected inflation, 12-month ahead | 1.89 | 1.54 | 4.06 | 2.00 | 9.63 |

| Expected inflation, next 3–5 years | 2.42 | 1.79 | 4.65 | 3.00 | 9.47 |

| Perceived and expected mortgage rate for a “person with excellent credit” | |||||

| Current | 4.13 | 1.07 | 5.72 | 4.00 | 7.33 |

| End of 2019 | 4.39 | 1.09 | 6.02 | 4.50 | 6.96 |

| End of 2020 | 4.73 | 1.37 | 6.52 | 5.00 | 7.40 |

| End of 2021 | 4.97 | 1.57 | 6.88 | 5.00 | 7.83 |

| Next 5–10 years | 5.36 | 1.90 | 7.70 | 5.50 | 9.24 |

Notes: Pre-treatment expected inflation (12 months ahead) is computed as mean implied from the reported probability distribution over a range of bins. All other measures of inflation are reported as point predictions. Pre-treatment expected inflation excludes responses reporting deflation. Perceived and expected mortgage rates are elicited for “a person like you” at the pre-treatment stage and for “someone with excellent credit” at the post-treatment stage. Moments in columns (1) and (2) are computed using the Huber-robust method. The number of observations is 26,891.

Descriptive statistics.

| Robust moments | Moments | ||||

|---|---|---|---|---|---|

| Mean | Standard Deviation | Mean | Median | Standard Deviation | |

| (1) | (2) | (3) | (4) | (5) | |

| Pre-treatment data | |||||

| Perceived inflation, previous 12 months | 2.88 | 2.41 | 7.41 | 3.00 | 13.23 |

| Expected inflation, 12-month ahead | 2.32 | 2.02 | 3.62 | 2.60 | 3.69 |

| Perceived and expected mortgage rate for a “person like you” | |||||

| Current | 4.55 | 1.19 | 7.13 | 4.80 | 8.63 |

| End of 2019 | 4.90 | 1.44 | 7.59 | 5.00 | 8.74 |

| End of 2020 | 5.28 | 1.65 | 8.20 | 5.50 | 9.26 |

| End of 2021 | 5.53 | 1.92 | 8.74 | 6.00 | 10.07 |

| Next 5–10 years | 5.95 | 2.35 | 9.78 | 6.00 | 11.71 |

| Post-treatment data | |||||

| Expected inflation, 12-month ahead | 1.89 | 1.54 | 4.06 | 2.00 | 9.63 |

| Expected inflation, next 3–5 years | 2.42 | 1.79 | 4.65 | 3.00 | 9.47 |

| Perceived and expected mortgage rate for a “person with excellent credit” | |||||

| Current | 4.13 | 1.07 | 5.72 | 4.00 | 7.33 |

| End of 2019 | 4.39 | 1.09 | 6.02 | 4.50 | 6.96 |

| End of 2020 | 4.73 | 1.37 | 6.52 | 5.00 | 7.40 |

| End of 2021 | 4.97 | 1.57 | 6.88 | 5.00 | 7.83 |

| Next 5–10 years | 5.36 | 1.90 | 7.70 | 5.50 | 9.24 |

| Robust moments | Moments | ||||

|---|---|---|---|---|---|

| Mean | Standard Deviation | Mean | Median | Standard Deviation | |

| (1) | (2) | (3) | (4) | (5) | |

| Pre-treatment data | |||||

| Perceived inflation, previous 12 months | 2.88 | 2.41 | 7.41 | 3.00 | 13.23 |

| Expected inflation, 12-month ahead | 2.32 | 2.02 | 3.62 | 2.60 | 3.69 |

| Perceived and expected mortgage rate for a “person like you” | |||||

| Current | 4.55 | 1.19 | 7.13 | 4.80 | 8.63 |

| End of 2019 | 4.90 | 1.44 | 7.59 | 5.00 | 8.74 |

| End of 2020 | 5.28 | 1.65 | 8.20 | 5.50 | 9.26 |

| End of 2021 | 5.53 | 1.92 | 8.74 | 6.00 | 10.07 |

| Next 5–10 years | 5.95 | 2.35 | 9.78 | 6.00 | 11.71 |

| Post-treatment data | |||||

| Expected inflation, 12-month ahead | 1.89 | 1.54 | 4.06 | 2.00 | 9.63 |

| Expected inflation, next 3–5 years | 2.42 | 1.79 | 4.65 | 3.00 | 9.47 |

| Perceived and expected mortgage rate for a “person with excellent credit” | |||||

| Current | 4.13 | 1.07 | 5.72 | 4.00 | 7.33 |

| End of 2019 | 4.39 | 1.09 | 6.02 | 4.50 | 6.96 |

| End of 2020 | 4.73 | 1.37 | 6.52 | 5.00 | 7.40 |

| End of 2021 | 4.97 | 1.57 | 6.88 | 5.00 | 7.83 |

| Next 5–10 years | 5.36 | 1.90 | 7.70 | 5.50 | 9.24 |

Notes: Pre-treatment expected inflation (12 months ahead) is computed as mean implied from the reported probability distribution over a range of bins. All other measures of inflation are reported as point predictions. Pre-treatment expected inflation excludes responses reporting deflation. Perceived and expected mortgage rates are elicited for “a person like you” at the pre-treatment stage and for “someone with excellent credit” at the post-treatment stage. Moments in columns (1) and (2) are computed using the Huber-robust method. The number of observations is 26,891.

The (robust) mean of perceived inflation over the 12 months preceding the survey is 2.88% (i.e. almost 1% point higher than the official inflation rate), in line with evidence from various consumer surveys according to which consumers tend to over-estimate recent inflation (see, e.g., D’Acunto et al. 2021a). The distribution of perceived inflation (Panel (a), Figure 2) shows a non-trivial fraction of respondents reporting focal values in excess of 10%, as in previous work (Binder 2017; D’Acunto et al. 2018a, 2019b).

To measure expected inflation, we use the probabilistic type of question asked in the SCE in which respondents are invited to assign probabilities over a range of inflation/deflation bins. However, the ordering of the inflation ranges presented in the survey began with deflation options before offering inflation ranges. This appears to have confused some respondents, who assigned all their weight to deflation outcomes but later provided positive answers to point forecast questions about inflation (even in the control group). To address this confounding factor, we drop expectations of inflation that have a negative implied mean from the distributional question (|$\approx$|20% of answers).7 Gorodnichenko and Sergeyev (2021) show that across a wide range of surveys and countries, the fraction of households expecting deflation is consistently under 1%. The discrepancy between all other household surveys studied in Gorodnichenko and Sergeyev (2021) and the large fraction of negative forecasts obtained in this setting is a clear indication that the ordering of bins confused some survey participants.8 Once we drop negative forecasts, the resulting expected inflation (12 months ahead) implied from the reported probability distribution is 2.3%. Comparable moments from the NY Fed’s SCE and Michigan Survey of Consumers were 2.8% and 2.9%, respectively, while professional forecasters were predicting CPI inflation of 2.3%. The consistency of the resulting mean forecasts in our survey after dropping deflationary expectations with the SCE and MSC provides another indication that the negative forecasts were mostly anomalous.

Moreover, the survey asks consumers about current and expected nominal interest rates with reference to a fixed rate 30-year mortgage. Mortgages with a 30-year fixed rate period represent the most popular mortgage product in the U.S., accounting for more than 70% of mortgages originated over the period 2013–2016.9 In our survey, respondents are asked to provide an estimate of the nominal interest rate for such a mortgage both at the time of the interview and over different time horizons (i.e. 1 year ahead; 2 years ahead; 3 years ahead; and in the next 5–10 years).10 The robust mean of the (perceived) current mortgage rate is 4.55% and the median is 4.80%. These moments are comparable with those derived from a similar question asked in the SCE (median: 4.3%; mean: 5.2%).11 Moreover, they are in line with Freddie Mac Primary Mortgage Market Survey, according to which the interest rate for a 30-year fixed rate mortgage was on average between 4.06% and 4.41% in March 2019.12 However, this masks significant heterogeneity in beliefs about interest rates. The robust standard deviation is 1.19%.13 Hence, for many households in the U.S., perceived market interest rates are quite far from actual interest rates. In the context of the Euler equation in Section 2, this means that |$i_t^{m}\ne i_t^{hh}$| for many households.

The expected mortgage rate 1 year ahead is 4.90% (i.e. 35 basis points higher, on average, than the perceived one at the time of the interview). As regards longer horizons, expected interest rates rise, on average, to 5.28%, 5.53%, and 5.95% with reference to 2 years ahead, 3 years ahead, and next 5–10 years, respectively. This implies that consumers expect somewhat higher mortgage rates in future periods. These trends are well aligned with the ones recorded in the SCE. Specifically, in the SCE the expected rate changes for 1 year ahead and 3 years ahead, compared with the current ones, are on average, 37 and 130 basis points respectively. Their counterparts in our survey are 35 and 98 basis points.

In Online Appendix Figure A.1 and Online Appendix Table A.1, we show various correlations between inflation expectations (1 year ahead) and other expectations asked in our survey. The raw data suggest a weak positive association between expected inflation and the expected mortgage interest rate 1 year ahead, yet considerable heterogeneity exists in this pattern. To this end, we examine not only how consumers respond to (exogenously) elevated inflation and nominal interest rate expectations but also to updates in the real rate expectations.

In short, our survey results for Nielsen panelists are consistent with those of other surveys of households. Average levels of perceived and expected inflation and interest rates are somewhat higher than actual levels and, strikingly, display large amounts of cross-sectional heterogeneity. Unlike other surveys, our results are based on a much larger cross-section of households (approximately 20,000 vs. 1,500 in the SCE and 500 in the MSC) and allow for randomized treatments that generate exogenous variation in beliefs within the same survey population and time period.

4. Econometric Framework

While estimating specification (1), we use sampling weights to correct for possible imbalances in the sample. Because expectations can take extreme values, we use Huber-robust regressions (1964) to minimize the adverse effects of influential observations and outliers. Huber-robust regressions differ from using winsorized data in standard regressions because they also take correlations across variables into account. Whether we include controls in specification (1) affects only the precision of the estimates because the assignment of treatment is random. To maximize statistical power and improve readability of our results, we estimate specification (1) with some treatments aggregated to coarser groups. We report detailed treatment effects in the Online Appendix.

Coefficient |$\alpha$| measures the persistence of expectations for the control group. Although one may naturally expect |$\alpha =1$| for post-treatment beliefs measured shortly after pre-treatment beliefs are elicited (the control group receives no information), the design of the survey as well as the nature of survey responses can result in estimates of |$\alpha$| different from one. First, pre- and post-treatment responses even in the control group can differ because respondents may have noise in their responses, leading to mean-reversion in answers. Second, as households participating in surveys do not like responding to the same question twice, we often formulate pre- and post-treatment questions differently. For example, we elicit inflation expectations before treatments by asking respondents to assign probabilities to a range of bins for possible inflation outcomes and use the reported probability distributions to compute the implied mean for expected inflation, whereas we gather the post-treatment inflation expectations as point predictions. Because responses often vary with the design of the survey questions (e.g. Bruine de Bruin et al. 2017), one may obtain |$\alpha \ne 1$|.16

Because survey responses can take implausible values, we drop some extreme observations. Specifically, for inflation forecasts, we drop responses of 100% or |$-$|100% for point predictions (drop 0.2% of the sample). We also drop observations with perceived/expected mortgage rates that are greater than 50% (drop less than 0.1% of the sample) and we censor mortgage rates at 30% if the responses are between 30% and 50% (applies to approximately 2% of the sample).

5. Effects of Different Information Treatments

In this section, we present and discuss how different treatments affect the expectations of individuals. To preserve space, we focus on the reaction of expectations immediately after the treatment and relegate results for beliefs in follow-up waves to the Online Appendix. In addition, we focus on estimates that pool across some different treatments to ease presentation but present full set of results for each treatment separately in Online Appendix Tables A.6–A.11.

5.1. The Effect of Forward Guidance Treatments on Interest Rate Beliefs

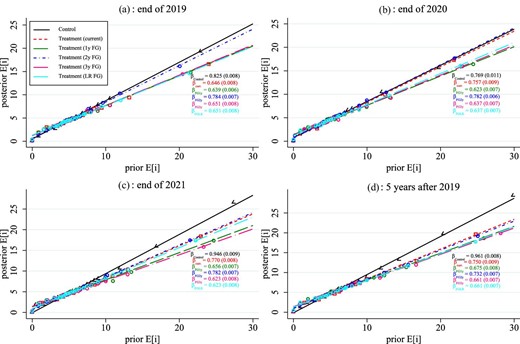

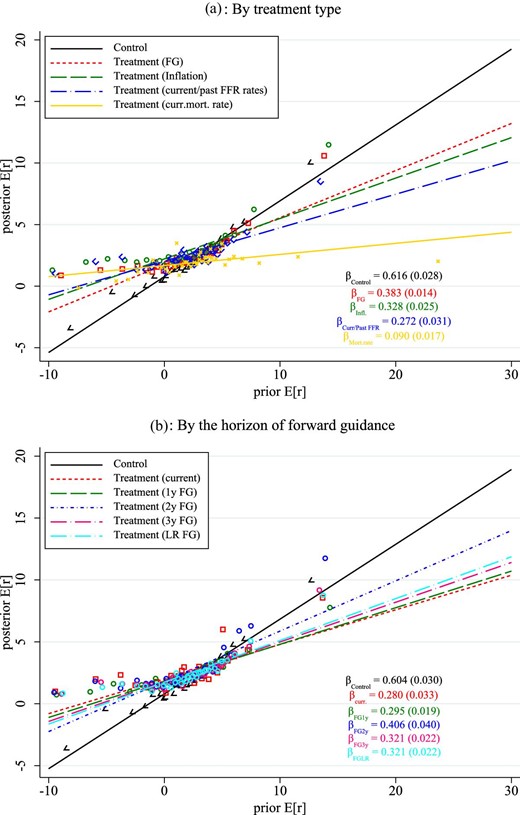

We begin by focusing on treatments regarding the future path of the federal funds rate relative to treatments focusing only on current and recent levels of the policy rate. Figure 3 first presents the cross-sectional relationship between prior and posterior beliefs for respondents receiving information about the Federal Funds Rate at different horizons. For each horizon, we present estimates pooled across treatments of the same horizon. Figure 4 (Panel (a)) presents how contemporaneous mortgage rate expectations of respondents then change when presented with information about different paths of the Federal Funds rate. For the control group that gets no information, the slope linking pre-treatment expectations to post-treatment expectations is close to 1 |${(\hat\alpha }=0.996$|, see Online Appendix Table A.9), indicating that measurement error in these expectations is quite small (as this would bias the estimated |$\alpha$| to values smaller than 1).17

Response of nominal mortgage rate expectations by forecast horizon and the horizon of forward guidance (FG). Notes: Each panel shows binscatter plots for revisions in nominal mortgage rates when treatments are combined into information provision about current rates (“current”: T3, T19, and T24), 1-year forward guidance (“1y FG”: T7, T8, and T9), 2-year forward guidance (“2y FG”: T10, T11, and T12), 3-year forward guidance (“3y FG”: T13, T14, and T15), and longer-run forward guidance (“LR FG”: T4, T5, T6, T16, T17, and T18). The title of each panel indicates the horizon of the forecasts for mortgage rates. Estimated regression coefficients are reported in Online Appendix Table A.7.

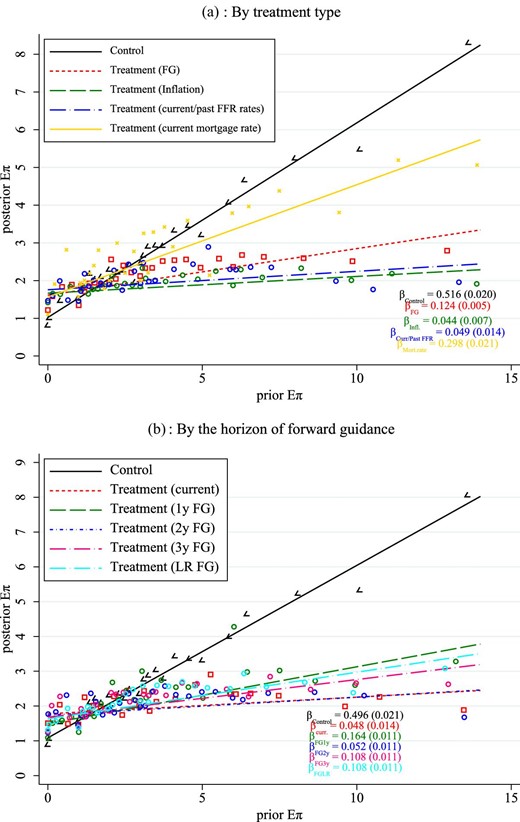

Response of nominal mortgage rate expectations by treatment and horizon. Notes: Each panel shows binscatter plots for revisions in nominal mortgage rates when treatments are combined into information provision about current rates (“Current/past rates”: T3, T19, and T24), forward guidance (“FG”: T4–T19), and inflation (“Inflation”: T20–T23). The title of each panel indicates the horizon of the forecasts for mortgage rates. Estimated regression coefficients are reported in Online Appendix Table A.6. Panel A: by treatment type.

For those receiving information about only current and recent FFR (i.e. treatments 3 and 19), the slope of the relationship between priors and posteriors is flatter than the control group (approximately 0.8), as illustrated in Panel (a) of Figure 3. This indicates that telling households about current and recent levels of the policy rate has non-trivial effects on their beliefs about the current mortgage rate relative to their priors. Treatments that provide additional information about the path of the future FFR lead to indistinguishable effects on the perceived level of the current mortgage rate: treatments at the 1 year horizon (T7–T9), 2 year horizon (T10–T12), 3 year horizon (T13–T15), and longer horizon (T4–T6 and T16–T18) all lead to very similar slope relationships (|${\approx }$|0.8). Similar results hold for households’ beliefs about future mortgage rates (Panels (b)–(d)). Providing future estimates of the FFR leads to only small revisions in current perceptions of the mortgage rate, despite the fact that current information about the FFR is still included in the treatments. Similar results obtain for expected future mortgage rates, with few differences across treatments at longer horizons. A slope of 0.8 in the cross-sectional relationship between posteriors and priors implies that the average weight assigned to signals is only 0.2. We should therefore expect the response of households’ expectations of interest rates to be 20% of that of fully informed financial markets.

While the horizon of the guidance does not seem to have any effect on the degree to which households’ expectations respond, the level of interest rates in the guidance does. To see this, Table 3 reports the average revision in expectations about the nominal rate for treatments involving a high trajectory of interest rates (T4, T8, T11, T14, and T16), a medium trajectory (T6, T10, T13, and T18), or a low trajectory (T5, T9, T12, T15, and T17). Differences in the level of the signal should not affect the slope between posteriors and priors but only the intercept, which are captured by the average revisions in Table 3. We find that average revisions in beliefs about nominal interest rates, especially future ones, are generally smaller (more negative) for low trajectory treatments than high trajectory treatments, consistent with the level of the treatment affecting the average level of beliefs.

Response of expectations revisions by aggregated trajectory.

| Dependent variable: | Nominal mortgage rate | ||||

|---|---|---|---|---|---|

| revisions in perceptions or | Current | 1-year [2019] | 2-year [2020] | 3-year [2021] | Longer run |

| expectations of mortgage rate | (1) | (2) | (3) | (4) | (5) |

| Control | |$-$|0.191*** | |$-$|0.263*** | |$-$|0.330*** | |$-$|0.362*** | |$-$|0.358*** |

| (0.014) | (0.019) | (0.022) | (0.025) | (0.026) | |

| FG: high trajectory of FFR | |$-$|0.030* | |$-$|0.038* | |$-$|0.032 | |$-$|0.038 | 0.025 |

| (0.016) | (0.022) | (0.026) | (0.029) | (0.030) | |

| FG: central trajectory of FFR | |$-$|0.036** | |$-$|0.034 | |$-$|0.046* | |$-$|0.004 | |$-$|0.010 |

| (0.017) | (0.022) | (0.027) | (0.029) | (0.031) | |

| FG: low trajectory of FFR | |$-$|0.032** | |$-$|0.077*** | |$-$|0.072*** | |$-$|0.041 | |$-$|0.063** |

| (0.016) | (0.022) | (0.026) | (0.028) | (0.030) | |

| Current FFR rate | |$-$|0.042* | |$-$|0.051 | |$-$|0.099*** | |$-$|0.026 | |$-$|0.043 |

| (0.024) | (0.031) | (0.038) | (0.040) | (0.044) | |

| Current mortgage rate | 0.058** | 0.037 | 0.032 | |$-$|0.022 | 0.035 |

| (0.025) | (0.031) | (0.038) | (0.041) | (0.044) | |

| Inflation | |$-$|0.001 | |$-$|0.002 | |$-$|0.001 | 0.044 | 0.004 |

| (0.016) | (0.022) | (0.026) | (0.029) | (0.030) | |

| Observations | 19,425 | 19,909 | 20,313 | 20,370 | 20,247 |

| R-squared | 0.001 | 0.002 | 0.001 | 0.001 | 0.001 |

| Dependent variable: | Nominal mortgage rate | ||||

|---|---|---|---|---|---|

| revisions in perceptions or | Current | 1-year [2019] | 2-year [2020] | 3-year [2021] | Longer run |

| expectations of mortgage rate | (1) | (2) | (3) | (4) | (5) |

| Control | |$-$|0.191*** | |$-$|0.263*** | |$-$|0.330*** | |$-$|0.362*** | |$-$|0.358*** |

| (0.014) | (0.019) | (0.022) | (0.025) | (0.026) | |

| FG: high trajectory of FFR | |$-$|0.030* | |$-$|0.038* | |$-$|0.032 | |$-$|0.038 | 0.025 |

| (0.016) | (0.022) | (0.026) | (0.029) | (0.030) | |

| FG: central trajectory of FFR | |$-$|0.036** | |$-$|0.034 | |$-$|0.046* | |$-$|0.004 | |$-$|0.010 |

| (0.017) | (0.022) | (0.027) | (0.029) | (0.031) | |

| FG: low trajectory of FFR | |$-$|0.032** | |$-$|0.077*** | |$-$|0.072*** | |$-$|0.041 | |$-$|0.063** |

| (0.016) | (0.022) | (0.026) | (0.028) | (0.030) | |

| Current FFR rate | |$-$|0.042* | |$-$|0.051 | |$-$|0.099*** | |$-$|0.026 | |$-$|0.043 |

| (0.024) | (0.031) | (0.038) | (0.040) | (0.044) | |

| Current mortgage rate | 0.058** | 0.037 | 0.032 | |$-$|0.022 | 0.035 |

| (0.025) | (0.031) | (0.038) | (0.041) | (0.044) | |

| Inflation | |$-$|0.001 | |$-$|0.002 | |$-$|0.001 | 0.044 | 0.004 |

| (0.016) | (0.022) | (0.026) | (0.029) | (0.030) | |

| Observations | 19,425 | 19,909 | 20,313 | 20,370 | 20,247 |

| R-squared | 0.001 | 0.002 | 0.001 | 0.001 | 0.001 |

Notes: The table reports estimates of coefficients on treatment indicator variables when treatments are aggregated by the trajectory of forward guidance (FG) for the Federal Funds Rate (FFR). The estimated specification is |$X_j^{\textit {post}} - X_j^{\textit {pre}} = \alpha + \mathop \sum \nolimits _{k\ = \ 2}^{24} {\beta }_k {\textit Treatment}_j^{( k )} + {\textit {error}}_j$|. Coefficients for groups other than the control group are relative to the coefficient for the control group. All estimates are based on Huber-robust regressions. Regressions use sampling weights. No household/respondent controls are included. Robust standard errors are in parentheses.

Aggregation treatments: current FFR rate: T3; high trajectory: T4, T8, T10, T13, and T16; central trajectory: T6, T7, T11, and T14; low trajectory: T5, T9, T12, T15, and T17; current mortgage rate: T24; and inflation rate: T20–T23.*, **, and *** denote statistical significance at 10%, 5%, and 1% levels, respectively.

Response of expectations revisions by aggregated trajectory.

| Dependent variable: | Nominal mortgage rate | ||||

|---|---|---|---|---|---|

| revisions in perceptions or | Current | 1-year [2019] | 2-year [2020] | 3-year [2021] | Longer run |

| expectations of mortgage rate | (1) | (2) | (3) | (4) | (5) |

| Control | |$-$|0.191*** | |$-$|0.263*** | |$-$|0.330*** | |$-$|0.362*** | |$-$|0.358*** |

| (0.014) | (0.019) | (0.022) | (0.025) | (0.026) | |

| FG: high trajectory of FFR | |$-$|0.030* | |$-$|0.038* | |$-$|0.032 | |$-$|0.038 | 0.025 |

| (0.016) | (0.022) | (0.026) | (0.029) | (0.030) | |

| FG: central trajectory of FFR | |$-$|0.036** | |$-$|0.034 | |$-$|0.046* | |$-$|0.004 | |$-$|0.010 |

| (0.017) | (0.022) | (0.027) | (0.029) | (0.031) | |

| FG: low trajectory of FFR | |$-$|0.032** | |$-$|0.077*** | |$-$|0.072*** | |$-$|0.041 | |$-$|0.063** |

| (0.016) | (0.022) | (0.026) | (0.028) | (0.030) | |

| Current FFR rate | |$-$|0.042* | |$-$|0.051 | |$-$|0.099*** | |$-$|0.026 | |$-$|0.043 |

| (0.024) | (0.031) | (0.038) | (0.040) | (0.044) | |

| Current mortgage rate | 0.058** | 0.037 | 0.032 | |$-$|0.022 | 0.035 |

| (0.025) | (0.031) | (0.038) | (0.041) | (0.044) | |

| Inflation | |$-$|0.001 | |$-$|0.002 | |$-$|0.001 | 0.044 | 0.004 |

| (0.016) | (0.022) | (0.026) | (0.029) | (0.030) | |

| Observations | 19,425 | 19,909 | 20,313 | 20,370 | 20,247 |

| R-squared | 0.001 | 0.002 | 0.001 | 0.001 | 0.001 |

| Dependent variable: | Nominal mortgage rate | ||||

|---|---|---|---|---|---|

| revisions in perceptions or | Current | 1-year [2019] | 2-year [2020] | 3-year [2021] | Longer run |

| expectations of mortgage rate | (1) | (2) | (3) | (4) | (5) |

| Control | |$-$|0.191*** | |$-$|0.263*** | |$-$|0.330*** | |$-$|0.362*** | |$-$|0.358*** |

| (0.014) | (0.019) | (0.022) | (0.025) | (0.026) | |

| FG: high trajectory of FFR | |$-$|0.030* | |$-$|0.038* | |$-$|0.032 | |$-$|0.038 | 0.025 |

| (0.016) | (0.022) | (0.026) | (0.029) | (0.030) | |

| FG: central trajectory of FFR | |$-$|0.036** | |$-$|0.034 | |$-$|0.046* | |$-$|0.004 | |$-$|0.010 |

| (0.017) | (0.022) | (0.027) | (0.029) | (0.031) | |

| FG: low trajectory of FFR | |$-$|0.032** | |$-$|0.077*** | |$-$|0.072*** | |$-$|0.041 | |$-$|0.063** |

| (0.016) | (0.022) | (0.026) | (0.028) | (0.030) | |

| Current FFR rate | |$-$|0.042* | |$-$|0.051 | |$-$|0.099*** | |$-$|0.026 | |$-$|0.043 |

| (0.024) | (0.031) | (0.038) | (0.040) | (0.044) | |

| Current mortgage rate | 0.058** | 0.037 | 0.032 | |$-$|0.022 | 0.035 |

| (0.025) | (0.031) | (0.038) | (0.041) | (0.044) | |

| Inflation | |$-$|0.001 | |$-$|0.002 | |$-$|0.001 | 0.044 | 0.004 |

| (0.016) | (0.022) | (0.026) | (0.029) | (0.030) | |

| Observations | 19,425 | 19,909 | 20,313 | 20,370 | 20,247 |

| R-squared | 0.001 | 0.002 | 0.001 | 0.001 | 0.001 |

Notes: The table reports estimates of coefficients on treatment indicator variables when treatments are aggregated by the trajectory of forward guidance (FG) for the Federal Funds Rate (FFR). The estimated specification is |$X_j^{\textit {post}} - X_j^{\textit {pre}} = \alpha + \mathop \sum \nolimits _{k\ = \ 2}^{24} {\beta }_k {\textit Treatment}_j^{( k )} + {\textit {error}}_j$|. Coefficients for groups other than the control group are relative to the coefficient for the control group. All estimates are based on Huber-robust regressions. Regressions use sampling weights. No household/respondent controls are included. Robust standard errors are in parentheses.

Aggregation treatments: current FFR rate: T3; high trajectory: T4, T8, T10, T13, and T16; central trajectory: T6, T7, T11, and T14; low trajectory: T5, T9, T12, T15, and T17; current mortgage rate: T24; and inflation rate: T20–T23.*, **, and *** denote statistical significance at 10%, 5%, and 1% levels, respectively.