Abstract

In response to a change in interest rates, younger firms not paying dividends adjust both their capital expenditure and borrowing significantly more than older firms paying dividends. The reason is that the debt of younger non-dividend payers is far more sensitive to fluctuations in collateral values, which are significantly affected by monetary policy. The results are robust to a wide range of possible confounding factors. Other channels, including movements in interest payments, product demand, profitability, and mark-ups, are also significant but seem unlikely to explain the heterogeneity in the response of capital expenditure. Our findings suggest that these types of financial frictions play an important role in the transmission of monetary policy.

1. Introduction

Investment plays an important role in the business cycle. It accounts for a significant share of domestic output, is one of its most volatile components and plays a prominent role in many macroeconomic theories. From a policy perspective, a commonly held view is that investment is a key channel of monetary transmission. This is reflected in a sizable literature in empirical macroeconomics, which, using aggregate time series data, finds that movements in interest rates have a large and persistent impact on business investment.

There remains, however, a surprising degree of uncertainty about the specific channels through which monetary policy affects investment. On the one hand, neoclassical models emphasize the direct effects of interest rate changes on the user cost of capital and firms’ expected returns. In contrast, the financial accelerator literature appeals to the more indirect effects that work through the revaluation of assets and net worth, which subsequently affects firms’ ability to borrow for investment (see, for instance, Kiyotaki and Moore 1997; Bernanke, Gertler, and Gilchrist 1999). In this second strand of the literature, monetary policy can gain extra traction over investment by influencing the borrowing constraints facing firms. There has been much debate about the empirical relevance of these financial accelerator effects, especially in the aftermath of the 2008 financial crisis, but evidence remains elusive.1

We use firm-level panel data for the United States to examine the relevance of a financial accelerator in the transmission of monetary policy. The first challenge we face is that financial constraints are not directly observable. In this paper, we focus on firm age and whether a firm pays dividends as likely correlates of exposure to a financial accelerator mechanism at the firm-level. The motivation for this comes from a number of observations. First, firms that (i) pay dividends and (ii) use debt counter-cyclically are unlikely to be constrained. A main reason is that, in the face of adverse shocks, dividend payers can reduce payouts. But, non-dividend payers are more likely to require external finance and face a larger wedge between internal and external funding costs. Indeed, in a number of models with financial frictions, credit constrained firms do not pay dividends, particularly in transition to their optimal scale.2 Second, and relatedly, firms are more likely to face financial constraints earlier in their life cycle, when they typically lack stable cash flows and have yet to develop a long credit history, a point emphasized in the firm dynamics literature (e.g. Haltiwanger, Jarmin, and Miranda 2013 and Davis and Haltiwanger 2019). Moreover, younger firms secure a far larger share of their borrowing using assets rather than earnings, whereas the opposite is true for older companies (Lian and Ma 2021). As a result, these firms are more likely to be exposed to the traditional financial accelerator type mechanisms.3

We establish four main findings. First, both the investment and borrowing of younger firms not paying dividends exhibit a large and significant decline in response to a tightening of monetary policy. Second, collateral values fall significantly for all firms when interest rates increase. Third, the borrowing of the younger non-dividend payers is far more sensitive to fluctuations in collateral values than other firms. Fourth, relative to younger non-dividend payers, the investment adjustments of older companies are much smaller (both in terms of economic and statistical significance) and the change in borrowing is insignificant. The heterogeneity we document is robust to a wide range of sensitivity analyses, including controlling for other individual characteristics such as size, leverage, and liquidity, exploiting within-firm variation over the life-cycle and using alternative strategies to identify monetary policy innovations.

What do these findings tell us about the transmission mechanism? Our preferred interpretation is that younger non-dividend payers are more likely to be constrained by the value of their assets. In particular, we show that our results are consistent with a mechanism where falling collateral values leads to tighter borrowing constraints, which amplifies the effects of monetary policy on the investment of constrained firms. In the Online Appendix, we corroborate this intuition using a stylized financial accelerator model featuring a collateral constraint. Firms differ in their optimal scale and the borrowing constraint may become less binding as they approach the optimal size. We interpret distance to optimal scale as firm age. When the indirect effects via asset prices are large, the investment and borrowing of constrained firms are more sensitive to changes in the interest rate. In Section 5, we show that other channels, including direct movements in interest payments, product demand, profitability, firms’ costs, and mark-ups are associated with more homogeneous effects and, thus, cannot easily account for the estimated heterogeneity in the investment and borrowing responses we find across groups.

Turning to the aggregate implications, we document that, despite accounting for less than one tenth of aggregate investment, younger firms paying no dividends account for around two thirds of the average effect on the investment rate (which normalizes capital expenditure by the firm’s capital stock) and for about one quarter of the response of aggregate investment to monetary policy. Furthermore, differences in the behavior across groups is informative about the importance of the indirect effects associated with financial accelerator type frictions. Our results suggest that these indirect effects—working through changes in collateral values and corporate debt—can account for around one third of the dynamic effects of monetary policy on aggregate investment. As a result, these types of channels remain an important part of the monetary transmission mechanism.

Looking at financial heterogeneity has a long tradition in empirical macroeconomics and finance. Yet, a more recent literature has shown that traditional characteristics—such as size, liquidity, and leverage—are unlikely to measure financial conditions. For instance, Crouzet and Mehrotra (2020) find that the investment of small firms is more sensitive to the business cycle than for large firms but their debt is not, which is hard to square with size capturing access to credit. Indeed, while many firms are born small and wish to grow over time, others have no ambition to expand (see Hurst and Pugsley 2011). According to Bates, Kahle, and Stulz (2009), firms tend to accumulate cash holdings to hedge against future borrowing constraints, implying that businesses with high liquidity may not be unconstrained. Finally, Lian and Ma (2021) note that many companies tend to finance M&A activities with debt rather than equity, thereby becoming significantly more levered despite having good access to financial markets.

More generally, many of the individual characteristics that have been previously used to measure heterogeneity in financial conditions tend to mix-up firms at different points in their life cycle. This chimes with the conclusion in Dinlersoz et al. (2018), who argue that one cannot fully understand the link between firm characteristics and financial frictions without conditioning on age. Our results based on age/dividend status are robust to controlling for other individual characteristics (such as size, leverage, and liquidity), whereas the heterogeneity estimated along these latter dimensions tends to disappear after controlling for age/dividend status. Furthermore, our strategy has a significant econometric advantage. Grouping strategies based on size, liquidity, and leverage suffer from several endogeneity and selection issues discussed in Section 2. In contrast, age is fully pre-determined and dividends payouts occur independently from monetary policy changes: We find that when firms begin paying dividends, they rarely stop.

Based on the age/dividend grouping strategy, our empirical analysis looks at heterogeneity in the dynamic responses of groups of firms to interest rate changes across a wide range of firm-level variables. We focus on U.S. public firms from S&P Compustat, which has excellent coverage and a long time dimension. In the working paper version of our work (Cloyne et al. 2018), we also show a companion set of results for the United Kingdom. To study the dynamic effects of monetary policy, we need a time series of identified exogenous innovations to policy interest rates. This ensures that our exogenous variation is not driven by other macro factors and also limits any potential reverse causality issues. We exploit the high frequency surprises in interest rate futures contracts within a 30 minute window around policy announcements, following Gürkaynak, Sack, and Swanson (2005), Gertler and Karadi (2015), and Nakamura and Steinsson (2018a). We then employ a local projection instrumental variable (LP-IV) panel approach to estimate the dynamic effects of monetary policy. To explore heterogeneity across firms, we interact policy rates with bins of the age/size/leverage/liquidity distribution. This strategy allows us to conduct a semi-parametric multivariate analysis by flexibly defining our bins using the outer product of various firm characteristics. For instance, we can compare the behavior of younger and smaller firms with the relative behavior of younger and larger companies to isolate the contribution of size conditional on age. A similar strategy allows us to examine the contribution of age conditional on size, for example.

Related Literature.

Our findings connect to four strands of empirical work. A important recent line of research reveals that the use of asset-based, cash flow-based, interest coverage-based covenants, and credit lines is pervasive among U.S. public firms (Drechsel 2023; Greenwald 2019; Greenwald, Krainer, and Paul 2021; Lian and Ma 2021) and both the incidence and the nature of the constraint could matter. In particular, Lian and Ma (2021) report that asset-based borrowing is the primary form of corporate debt among small, young, and low-profit firms, whereas large, old, and high-margin companies rely mainly on cash flow-based lending. Our strategy can therefore shed particular light the importance of the asset-based financial accelerator type mechanism: young non-dividend paying firms are indeed the group whose (i) investment and borrowing exhibit the largest and most significant response to interest rate changes and (ii) borrowing is most correlated with changes in collateral values.

A well-established empirical literature, exemplified by the studies of Davis, Haltiwanger, and Schuh (1996), Haltiwanger, Jarmin, and Miranda (2013), Dinlersoz et al. (2018), Pugsley, Sedláček, and Sterk (2021), and Sedláček (2020) has shown that firm age is a key determinant of employment and leverage dynamics over the business cycle. Relative to these influential works, we focus on identified monetary policy changes and investigate the dynamic responses of investment, borrowing, debt composition, and collateral values at the firm-level across demographic groups.

The importance of collateral constraints for firms is the focus of Chaney, Sraer, and Thesmar (2012), Liu, Wang, and Zha (2013), Catherine et al. (2022), and Bahaj, Foulis, and Pinter (2020). Relative to these contributions, we look at heterogeneity in the response of borrowing by age/dividends and associate this with heterogeneity in the investment responses to identified monetary policy shocks. The behavior of constrained and unconstrained firms is particularly important for assessing the indirect effects of monetary policy via financial frictions.

A large empirical literature on investment has proposed various measures of financial conditions, including cash flows (Fazzari, Hubbard, and Petersen 1988, Oliner and Rudebusch 1992), size (Gertler and Gilchrist 1994), paying dividends (Fazzari, Hubbard, and Petersen 1988), bank debt (Ippolito, Ozdagli, and Perez-Orive 2018), leverage (Ottonello and Winberry 2020 and Lakdawala and Moreland 2021), and liquidity (Jeenas 2019).4 We find that sorting firms along the joint distribution of age and dividend payouts (i) generates the largest and most significant comovement between investment and borrowing, and (ii) is robust to further conditioning on size, leverage, and liquidity, while the reverse is not true.

On the theoretical side, our evidence provides support for the notion that financial frictions amplify the effects of macroeconomic shocks in the spirit of Kiyotaki and Moore (1997) and Bernanke, Gertler, and Gilchrist (1999). Unlike these contributions where constrained firms are more levered, however, we show that being younger and paying no dividends is a far stronger predictor of a significant comovement between investment and debt, consistent with those firms being more dependent on external finance to fund their projects. Albuquerque and Hopenhayn (2004), Khan and Thomas (2013), and Begenau and Salomao (2019) feature models where firms may grow out of their borrowing constraints as they approach their optimal scale but, along this path, dividends are zero.

Structure of the Paper.

In Section 2, we present the data, discuss our age/dividend grouping strategy and document how balance sheet variables and other characteristics vary over a firm’s life-cycle. In Section 3, we discuss our empirical framework and identification strategy before presenting the average effect in our firm-level panel data. The heterogeneous response of capital expenditure following a change in monetary policy is the focus of Section 4. We show that our grouping strategy based on age and dividends predicts a larger capital expenditure response than size, leverage, and liquidity, but also that our finding is robust to conditioning on these more traditional proxies. In Section 5, we investigate the channels that may explain the heterogeneous effects on investment and show that the response of borrowing and collateral values to changes in the interest rate is the most likely candidate. We also conduct a simple calculation of the likely contribution of these asset-based financial frictions to the aggregate investment response to monetary policy shocks. In Section 6, we show that our results are robust to exploiting variation within firms and across collateral shares, to alternative strategies for identifying the time series of monetary policy shocks and to potential sub-sample instability across sectors and over time. The Online Appendix contains further robustness checks and a simple financial accelerator model whose predictions are consistent with our empirical findings.

2. Data

In this section, we briefly describe the firm-level data and discuss the construction of the main variables of interest for our empirical analysis. In particular, we introduce our measure of firm age and argue that, together with dividend payment status, are informative of the financial and life-cycle position of a firm. Finally, we present a number of descriptive statistics suggesting that younger firms may face worse access to financial markets. A more detailed description of the sources, definitions, and sample selection can be found in Online Appendix A.

2.1. Sources and Variables Definition

Detailed, high quality balance sheet and income statement data for publicly listed companies are available quarterly from Compustat. Consistent information for a sufficiently large number of firms and variables only begins around 1986, when our sample starts. The sample ends in 2016, when the data were collected for this project. Turning to our main variables of interest, the investment rate is defined as capital expenditures in period |$t$| relative to the level of physical capital, as measured by net plant, property, and equipment at the beginning of the period.5 In addition to being a widely-used measure (see e.g. Chaney, Sraer, and Thesmar 2012), it allows us to compare the investment decision of firms with different levels of capital.

The main balance sheet variables of interest are cash-flows, which we proxy with EBITDA (earnings before interest, tax, depreciation, and allowances) as is common in the literature, total and long term debt, collateral values (market value of corporate real estate), sales, and interest expenditure. In our analysis, we will also use information on dividends paid, firm size (book value of total assets), leverage (total debt divided by the book value of total assets), liquidity (short term cash and investments divided by the book value of total assets), growth (growth in total assets), and Tobin’s (average) Q (the ratio of market value of assets to book value).6 More detailed information on data sources, variable definitions, and sample selection are provided in Online Appendix A.

As a first step toward a macro analysis with micro data, we are interested in understanding how much of the aggregate investment dynamics is captured by publicly traded firms.7 To do so, we aggregate the investment reported by each firm for a given period of time into a measure of investment at calendar frequency. Online Appendix A Figure A.1 compares the growth rate of this series from Compustat with the growth rate of aggregate investment from the U.S. Bureau of Economic Analysis, which includes investment by both public and private firms.

While publicly listed companies account for about 60% of the level of investment in the U.S. economy, the dynamics of the capital expenditure series aggregated from micro data are very similar to the dynamics of the official investment data from national accounts. More specifically, the correlation of the growth rate of capital expenditure from the micro data and the growth rate of official aggregate business investment is around 0.8. Understanding the dynamic behavior of publicly listed companies can therefore provide important insights about the transmission of economic shocks to the aggregate economy.

Finally, to the extent that private firms face similar or even tighter financial conditions than public firms, our findings may be interpreted as a lower bound for the relevance of financial frictions for the transmission of monetary policy to business investment.

2.2. Grouping Firms by Age and Dividend Payouts

The first step in our research design is to identify which type of firm is most likely to face some form of financial constraint. In a broad class of theoretical macro finance models, it can be shown that financially constrained firms do not engage in dividend payouts, see, for example, Khan and Thomas (2013), Albuquerque and Hopenhayn (2004) and Begenau and Salomao (2019). In these set-ups, a firm that is currently financially constrained (or may become so in the near future) might eventually grow and become unconstrained. Until that happens, however, the firm finds it optimal to use any available resources for growth and it does not pay dividends along this path. Contributions in the financial accelerator tradition such as Crouzet and Mehrotra (2020), Ottonello and Winberry (2020), and Jeenas (2019) also feature constrained firms that do not pay dividends.

As for age, a long-standing tradition in the empirical literature on consumption using household-level data (see e.g. Attanasio and Browning 1995; Wong 2021) and on employment using firm-level data (see, for instance, Haltiwanger, Jarmin, and Miranda 2013; Davis and Haltiwanger 2019) has provided evidence consistent with the notion that being young is correlated with the unobserved characteristics driving access to external finance. Younger firms typically have less experience in credit markets, have a shorter credit history (and therefore lower rating), and tend to have lower earnings and fewer assets to pledge than their older counterparts, implying they might have less funds available for investment.

Taking these two sets of results together, younger firms paying no dividends may face a more limited access to credit markets than older dividend payers. Our favourite interpretation is that, we are capturing a firm at the point in their life cycle when they are most likely to face financial constraints: when they are younger and not paying dividends. Younger firms are likely to be further away from their optimal scale, are seeking to grow but may lack the credit history to reduce their costs of external finance.8 Moreover, these are the firms that may be most subject to traditional financial accelerator type mechanisms as their borrowing is more likely to be secured against assets (Lian and Ma 2021). Our empirical approach therefore sheds light on the importance this mechanism.

Other measures of heterogeneity in financial conditions suffer from several potential challenges and are likely to mix-up firms at different points in their life cycle. This is consistent with Dinlersoz et al. (2018), who show that, to understand the relationship between firm characteristics and financial frictions, it is important to consider the age of the firm. As documented by Hurst and Pugsley (2011), most small businesses have little ambition to grow and while young businesses tend not to be large, many old companies choose to remain small and are therefore likely to be unconstrained. The absolute size measure of financial conditions traditionally used in earlier applied work would classify these old firms as constrained simply because they are small in absolute sense. In contrast, younger firms paying no dividends are more likely to be faraway from their optimal size and, as such, face a higher probability that financial constraints might constrain their growth. In this sense, firm age is capturing a firm’s relative size.

Similar concerns apply to using liquidity or leverage as measures of financial conditions at the firm-level. A large body of empirical work has shown that firms hold more cash to hedge against the possibility of a financial constraint binding in the future (Bates, Kahle, and Stulz 2009): Firms with large cash holding have a strong precautionary motive that makes them fundamentally different from businesses with low liquidity. As noted by Lian and Ma (2021) and Begenau and Salomao (2019), many older and larger firms have a higher leverage ratio because they have good access to capital markets and tend to finance large projects with debt rather than equity. On the other hand, a lower debt to asset ratio may be the very result of a younger company with insufficient internal funds being denied further external funds.9

Another advantage of our age/dividend grouping strategy is rank invariance. A company’s starting date is fully pre-determined and age cannot vary as a result of changes in monetary policy or the business cycle. Furthermore, we find that the decision to pay dividends is independent from movements in interest rates and when a company starts paying dividends it rarely stops.10 In contrast, size, leverage, and liquidity endogenously respond to shocks or vary over the cycle, which affect the ranking of firms in the distribution of these variables. Accordingly, it is hard to interpret any (ex-post) heterogeneity as being driven exclusively (or even partially) by ex-ante differences in these specific firm characteristics.11

Many papers examining firm-level investment have focused on U.S. Compustat data where the native age variable is sparsely populated. Interestingly, however, the year of incorporation is available for U.S. publicly listed companies from WorldScope. We therefore merge these datasets to provide a consistent measure of the incorporation date. To help address some missing observations as well as the issue of mergers and acquisitions, we also make use of the first date the firm appears in the Center for Research in Security Prices data. More details on the construction of the age variable are provided in Online Appendix A. While it is possible to use information on the founding years of firms, these are only available for a limited number of companies.12 Reassuringly, however, the descriptive statistics reported in the next section using our age proxy are very similar to the correlations reported by Dinlersoz et al. (2018) measuring age as years since foundation among publicly listed companies using the Census Bureau’s Longitudinal Business Database from 2005 to 2012.

2.3. Descriptive Statistics

In the previous section, we have discussed the conceptual reasons for why capturing a firm at a particular point in its life cycle might be a better proxy for financial constraints, particularly if we are interested in the role of financial accelerator type mechanisms. In this section, we want to establish the main empirical characteristics of younger and older companies to illustrate this point further. While the evidence in this section is of course only suggestive, in the rest of the paper, we will show that younger non-dividend payers is the group of firms displaying the strongest positive comovement between investment and debt following a monetary policy shock. This comovement is consistent with the predictions of a class of financial frictions models emphasizing the role of collateral constraints.

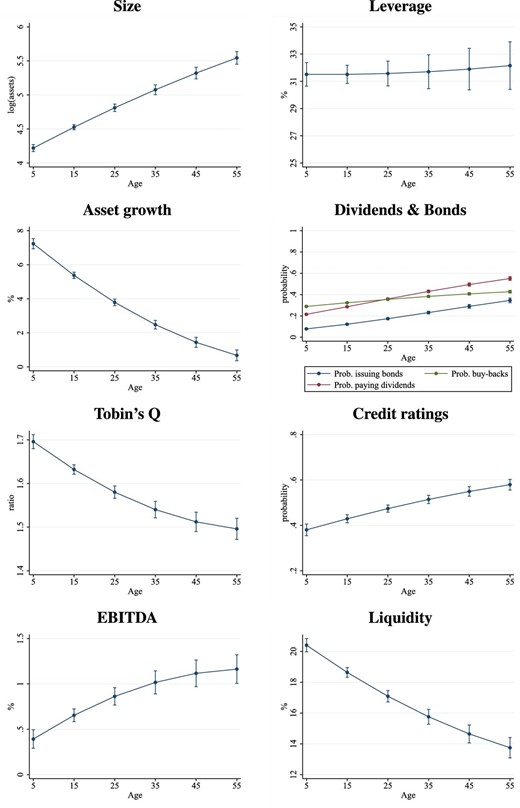

A simple but formal way of assessing the association between our measure of corporate age and other firm characteristics is to regress each of the characteristics of interest against a polynomial in age together with a measure of firm size (for all regressions except the one for size) and the interaction between sector and year fixed effects, which are designed to clean for common trends at the sectoral level. This specification is similar to the regressions used by Dinlersoz et al. (2018) and facilitates a comparison with their results based on administrative data.13 Our dependent variables in the first column of Figure 1 are (i) size, in the first row (ii) asset growth, in the second row, (iii) Tobin’s Q, in the third row, and (iv) EBITDA (as a share of past assets), in the fourth row. In the second column, we report the relationship between age and selected firms’ financial variables such as: (v) leverage, in the first row, (vi) the probability of having engaged in dividend payouts or buy back shares in the previous year or ever having issued bonds, in the second row, (vii) credit performance—measured by credit ratings among bond issuers—in the third row, and (viii) liquidity, in the last row.14

Descriptive statistics by age. Each panel reports the predicted values for each variable by age. Each panel uses a regression of the variable of interest on age and age squared conditional on sector-time fixed effects and firms’ controls as detailed in Section 2. 90% standard error bands. Standard errors are clustered by firm and time. Size is measured by the log of total assets. Asset growth is the growth rate of total assets. Tobin’s Q is the ratio of the market value of total assets to the book value. EBITDA is earnings before interest tax and depreciation, measured as sales net of costs divided by total assets. Leverage is total debt relative to total assets. Dividends and bonds are based the probability of paying cash dividends, buying back stock or having a issued a bond. Credit rating captures the probability that a firm of a given age has an investment grade (higher than BBB) rating on its (short or long term) debt. Liquidity means total short term cash and investments relative to total assets.

The top row in the first column of Figure 1 reveals that firm size is monotonically increasing with age, both in the full sample of firms that record assets and the smaller sample reporting also the number of employees. In line with Davis, Haltiwanger, and Schuh (1996), the second row confirms a sharp negative association between growth and years since incorporation; The third row shows that older companies tend to have lower Tobin’s Q values, while the fourth row reveals that younger firms have smaller or even negative operating profits early in their life.

The second column of Figure 1 examines the financial variables. Less experienced companies appear (weakly) less levered (first row),15 are less likely to pay dividends or issue bonds (second row), have worse credit scores (third row) and tend to hold a higher share of liquid assets (last row).16 The results on the relationship between leverage and age is consistent with the results based on years since foundation for publicly listed companies in Dinlersoz et al. (2018). The statistical association of age with the probability of paying dividends and Tobin’s Q is consistent with the predictions of the model in Cooley and Quadrini (2001).

In summary, our descriptive analysis reveals that, on average, younger firms are smaller, have lower cash-flows/earnings, worse credit scores, and a lower probability of paying dividends or issuing bonds. On average, they also grow faster, have a higher Tobin’s Q, hold more cash, and have lower leverage, although, interestingly, it is hard to see much difference in leverage across the age distribution. Finally, a comparison with the results in Dinlersoz et al. (2018) suggests that years since incorporation (used in this paper) and years since foundation (used in their paper) correlate similarly with other firm characteristics.

3. Empirical Framework

In this section, we describe our identification and empirical strategy. In particular, we first discuss the way we construct the time series of monetary policy shocks. We then move to our main empirical specifications. In the final part of this section, we present the estimates of the average effect of interest rate changes on investment in the micro-data at the firm-level and show this compares well with standard results from the macro literature using data from national statistics.

3.1. Identification

Identifying the dynamic causal effects of monetary policy on investment requires tackling the potential reverse causality: interest rates respond to the economy and also affect it. This is a standard problem in the empirical macro literature (see Nakamura and Steinsson 2018b), but it poses a further challenge in the context of our panel micro data analysis. We need our estimated effects to be driven by exogenous changes in monetary policy and by not some other macro factors causing movements in interest rates. Furthermore, some of the firm groups that we consider account for sizable movements in aggregate variables. This implies that some monetary policy responses to aggregate conditions may be, in fact, correlated with specific conditions in a particular group. As in the macro literature, we need some exogenous variation in policy rates.

Our identification strategy is based on the proxy-VAR/external instrument approach of Mertens and Ravn (2013) and Stock and Watson (2018), applied to monetary policy by Gertler and Karadi (2015). The idea is to isolate interest rate surprises using the movements in financial markets data within a short window around central bank policy announcements. Building on Gürkaynak, Sack, and Swanson (2005), Gertler and Karadi (2015) measure financial market surprises from Fed Funds Futures, using a 30 minutes interval around the FOMC policy announcements. The plausible identifying assumption is that nothing else occurs within this time window, which could drive both private sector behavior and monetary policy decisions. The technical innovation in Gertler and Karadi (2015) is to use these high frequency surprises as proxies for the true structural monetary policy shocks in a Vector Autoregression.17

Data on Fed Funds Futures are available since 1991, while the firm-level data span the period 1986–2016. One advantage of the Mertens and Ravn (2013) and Stock and Watson (2018) proxy-VAR used by Gertler and Karadi (2015) is that even if the identification of the contemporaneous causal relationships is based on the sample for which the proxy/instrument is available, the VAR can be estimated over a longer sample. This allows us to identify a sequence of monetary policy shocks for a longer period than the instrument is available for. We use the implied monetary policy shocks from the Gertler and Karadi (2015) VAR as our measure of monetary policy shocks in the micro data, obtaining a time series of monetary policy innovations for the full sample: 1986–2016.18 The approach only requires the high frequency surprises to be contemporaneously exogenous and the VAR will purge any remaining predictability. Furthermore, by directly following Gertler and Karadi (2015), our micro results will be more directly comparable to the macro literature (as we show in Online Appendix C). For all these reasons, this method is preferable to using the financial surprises directly in the panel estimation.19

We estimate a reduced-form VAR for the period 1986–2016, keeping as close as possible to the specification in Gertler and Karadi (2015). The VAR includes a measure of interest rates, log industrial production, the log of the consumer prices index, and two proxies for financial conditions.20 The time series of the monetary policy shocks is shown in Online Appendix B, together with the time series of the high-frequency monetary policy surprises. These policy shocks are then used in our firm panel regressions: As these are exogenous disturbances, there is no need to include further macro controls. We have also verified that our estimates do not suffer from a weak instrument problem.

To estimate the dynamic causal effects from the micro data, we use a panel LP-IV set up, following Jordà, Schularick, and Taylor (2020). This is very flexible and allows us to estimate impulse response functions on firm-level panel data using the identified monetary shocks as instruments for interest rate changes. There are two advantages of using the monetary policy shocks as an instrument rather than as a regressor directly. First, the scale of the shock (from the proxy-VAR) is indeterminate but as shown by Stock and Watson (2018) (page 11), the LP-IV estimation automatically imposes the unit effect normalization, implying that the size of the shock can then be interpreted in terms of the units of the endogenous variable, namely the interest rate. Second, as discussed by Wooldridge (2002, p. 117), generated instruments do not suffer from the inference problem associated with generated regressors highlighted by Pagan (1984).21

3.2. Baseline Specification

In order to capture the heterogeneous effects of monetary policy, in our benchmark empirical specification, we estimate impulse response functions using an instrumental variable (IV) variation of the LP approach, LP-IV:

Time is denoted by |$t$| and the data are quarterly. |$i$| denotes a firm. The dependent variable |$X$| will be the variable of interest: the investment rate in Section 4 and borrowing, collateral value, sales, and cash flows in Section 5.22|$\Delta R_t$| is change in the one year interest rate used in Gertler and Karadi (2015), instrumented using our extracted series of monetary policy shocks.23|$Z_{t-1}$| is a set of firm characteristics and the indicator function takes a value of 1 if the firm characteristic falls in a particular “bin” of the distribution, which we will refer to as the firm’s group. Importantly, |$Z$| can be multidimensional and we can have separate slopes for finer groups, for example, young/small/low leverage, old/large/high leverage, etc. In essence, this is a semi-parametric way of estimating the heterogeneous effects of monetary policy by different (and possibly multivariate) firm characteristics. We are not, therefore, imposing the restrictive assumption of linearity in these interactions. This is something that turns out to be important and also distinguishes us from virtually all earlier contributions working on investment heterogeneity at the firm-level. We also do not include other time or sector-time fixed effects as we want to interpret these coefficients as group specific impulse response functions, including any general equilibrium effects. This allows us to estimate conditional impulse response function as flexibly as possible.24 But we do add firm fixed effects, which not only absorb any sector fixed effect but also allows us to exploit also within-firm variation. Furthermore, we include quarterly dummies to control for seasonal factors.25 The end of quarter interest rate (interacted with the dummies) will be instrumented by the monetary policy shock (also interacted with the dummies). Standard errors are clustered by firm and time using the approach in Driscoll and Kraay (1998) for dealing with possible serial correlation in the forecast errors |$\epsilon _{i,t+h}$|, which is potentially a feature of LPs. The number of lags is set to 12. Finally, we estimate IRFs over a forecast horizon of 5 years, so we restrict the sample to firms that we observe for at least 5 years (20 quarters).

3.3. The Average Effect

Before presenting the results for different groups, it is useful to estimate the average response of the investment rate to a change in monetary policy in our firm-level panel data. This provides a benchmark against which we can evaluate the contribution of each group of firms. It also allows us to see whether the dynamic response of investment in the micro data resembles the impulse response functions we typically see in the time series macro literature.

To estimate the average effect, we drop the group dummies from equation (1) and replace the group-specific coefficients on the interest rate with a single parameter |$\beta _{h}$|. |$\beta _{h}$| therefore captures the average effect of interest rates on the investment rate at horizon |$h$|.

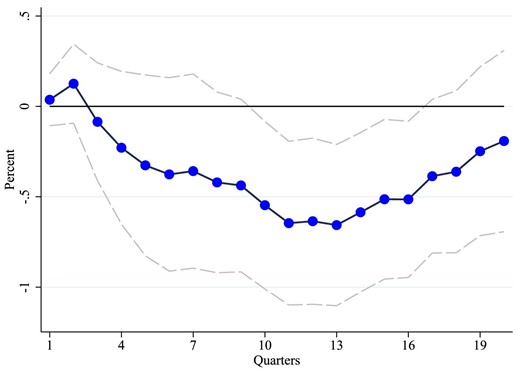

Figure 2 reports the impulse response function up to 20 quarters. The investment rate declines significantly following a 25 bp rise in the interest rate. The effect becomes significant towards the end of the first year and the peak effect is reached between the second and third year after the shock, at a value around |$-0.5$|pp. The shape of the dynamic response is broadly consistent with the impulse response functions obtained using aggregate data. These are shown in Online Appendix C. The dynamics of the average investment rate (estimated from the micro data) therefore lines up well with the macro response of business investment from national statistics. Online Appendix C also shows that our empirical approach generates results that reflect the macroeconomic effects found in Gertler and Karadi (2015). We are therefore starting from a standard set of benchmark macro results.

Average response of investment to an increase in interest rates. This figure shows the impulse response function (IRF) for the investment rate following a 25 bp increase in the one year interest rate. The IRFs are estimated using the LP-IV approach described in the text. The regression does not allows for heterogeneity across groups and the IRF is therefore the average effect across all firms in the sample and facilitates comparison with macroeconomic IRFs using time series data. Dotted lines are 90% standard error bands. Standard errors are computed using the Driscoll–Kraay method, clustering by firm and time, which is robust to very general forms of cross-sectional and temporal dependence.

Having established a benchmark against which to study the heterogeneous responses of capital expenditure across different groups of firms, our goal in the next section is to “disaggregate” this average effect and examine which groups drive the response and why.

4. The Response of Investment across Firms

In the previous section, we have shown that younger firms tend to be smaller, earn less, have lower a credit rating and (weakly) lower leverage, pay no dividends, issue no bonds, and accumulate more cash. While we have argued that these descriptive statistics are consistent with worse access to credit markets, our goal is to evaluate this claim by looking at the joint behavior of investment and the firm balance sheet in response to a change in monetary policy. The hypothesis is that in the presence of financial accelerator type frictions, which link net worth or asset values to a firm’s borrowing capacity, constrained firms should adjust both their investment and debt more than unconstrained firms. This logic is sketched out in the simple model in Online Appendix M.

In this section, we show that younger non-dividend payers indeed change their capital expenditure far more than any other group. We also show that while more traditional proxies of financial frictions—such as size, liquidity, and leverage—also generate some heterogeneity in the dynamic effects of monetary policy, the marginal predictive power of each of these traditional measures disappears once we conditions on our age/dividends proxy. The reverse, however, is not true: The heterogeneity by age and dividends status is robust to controlling for other proxies. Finally, we quantify the contribution of younger firms paying no dividends to the average investment response to monetary policy and find that this is significant. In the next section, we examine the channels of monetary transmission in more detail by showing the responses of debt and other variables.

4.1. Results Based on Age and Dividends

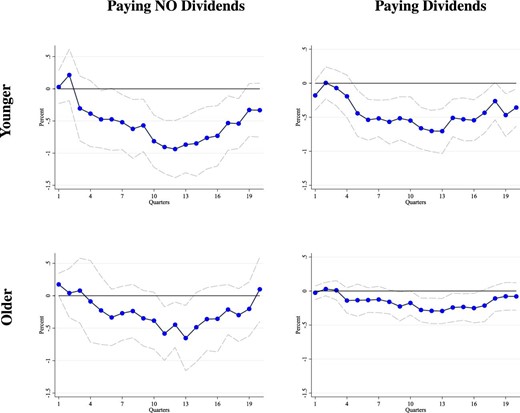

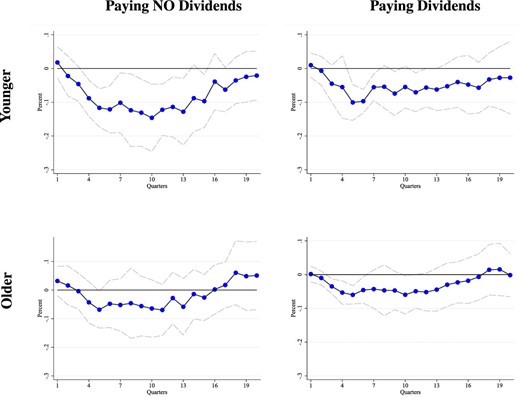

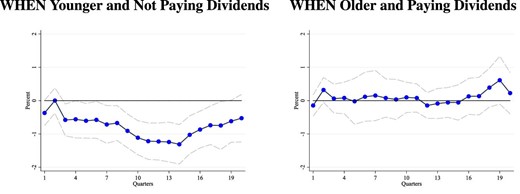

In this section, we explore the role of financial heterogeneity using our grouping strategy. More specifically, we allow the effects of monetary policy to vary across the age and the dividend status distribution. We split the sample into four groups depending on whether a firm is younger (less than 15 years since incorporation) and whether it paid dividends before the monetary policy shock. While there is no conceptual reason to prefer one specific age cutoff over another, the results are not sensitive to the precise threshold.26 The first (second) row of Figure 3 shows the impulse response functions for younger (older) firms. The first (second) column in each block refers to non-dividend (dividend) payers. Comparing the two rows reveals the marginal contribution of age, controlling for dividend status. Comparing the columns reveals the marginal contribution of paying dividends, controlling for age.

Response of investment by age and dividend status. This figure shows the impulse response functions for the investment rate following a 25 bp increase in the one year interest rate. The interest rate is interacted with binary indicators based on age and dividend status. Younger refers to <15 years since incorporation and older refers to >15 years since incorporation. No dividends means the firm did not pay cash dividends in the previous year. The IRFs are estimated using the LP-IV approach described in the text. Dotted lines are 90% standard error bands. Standard errors are computed using the Driscoll–Kraay method, clustering by firm and time, which is robust to very general forms of cross-sectional and temporal dependence.

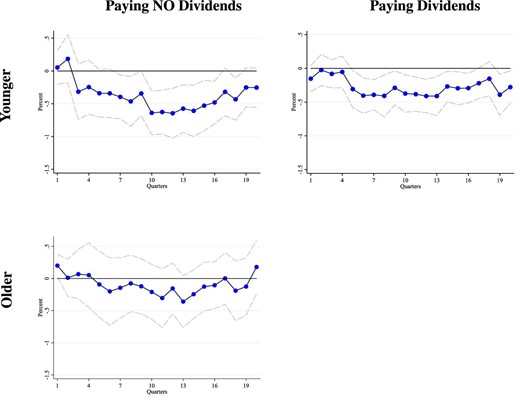

There are three main results that emerge from Figure 3. First, the initial effect over the first few quarters is small and insignificant for all groups, but the peak for younger non-dividend payers is more than one third larger than for younger firms paying dividends.27 Second, among non-dividend payers, younger firms (top-left corner) have the largest and most significant response, with the peak effect around 1% in absolute value. Third, the adjustment of capital expenditure to a monetary policy shock for older dividend payers (bottom-right corner) is much smaller, being around one fourth on average of the response of younger firms paying no dividends.28 To assess formally the statistical difference between groups, in Figure 4, we re-run our baseline regressions adding the interest rate as a separate regressor and making older dividend payers the base category (given that this is the set of firms most likely to be unconstrained). While this strategy has the disadvantage of losing track of the average effect of monetary policy, it has the advantage of allowing us to formalize a test of whether the estimated impulse response for each group at each horizon is statistically different from the estimated impulse response of the base group, which is old-dividend payers. The figure shows that the investment response of younger non-dividend payers is significantly larger than for older dividend payers at almost all horizons. In contrast, there seems to be no statistical difference between the two groups of old companies. Finally, the capital expenditure adjustment of young dividend payers is also significantly larger than the adjustment of old dividend payers, although the relative effect is smaller (in absolute magnitude) than for younger non-dividend payers.29

Response of investment by age and dividends relative to older firms paying dividends. This figure shows the impulse response functions for the investment rate following a 25 bp increase in the one year interest rate. The interest rate is interacted with binary indicators based on age and dividend status. Younger refers to <15 years since incorporation and older refers to >15 years since incorporation. No dividends means the firm did not pay cash dividends in the previous year. Relative to the results in Figure 3, this specification includes the interest rate as a regressor on its own. The IRFs are relative to older dividend-paying firms. The IRFs are estimated using the LP-IV approach described in the text. Dotted lines are 90% standard error bands. Standard errors are computed using the Driscoll–Kraay method, clustering by firm and time, which is robust to very general forms of cross-sectional and temporal dependence.

In Online Appendix D, we report results based on splitting the sample only along the age dimension (Figure D.1) or only according to whether a firm paid dividend or not (Figure D.2). Consistent with the estimates in Figure 3, we find in Figure D.1 that younger firms respond far more than either middle-aged firms (with incorporation date between fifteen and fifty years before the shock) or older firms (with more than fifty years since incorporation). Similarly, in Figure D.2, we document that non-dividend payers respond far more than dividend payers. Interestingly, however, the response of younger non-dividend payers in Figure 3 is larger than either younger firms in Figure D.1 or non-dividend payers in Figure D.2. Indeed, this is the reason why we conclude that the combination of age and dividends status is a stronger predictor of a larger investment response than each of these dimensions in isolation. We see dividend status and age as complementary indicators, where the goal is to capture a firm precisely at the point in its life cycle where particular asset-based financial constraints are most acute.

4.2. Conditioning on Other Firm-Level Characteristics

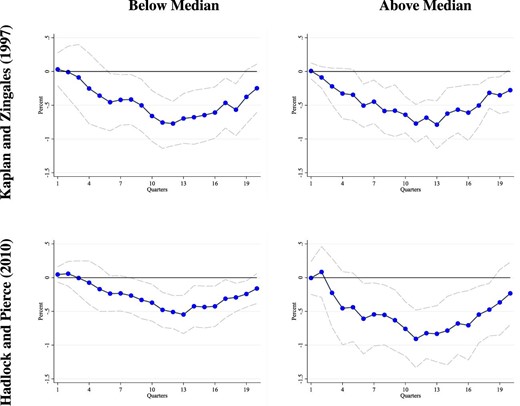

The evidence above reveals that being younger and paying no dividends is a strong predictor of a larger response of investment to monetary policy changes. In Section 2, we have shown that younger firms tend to be smaller, hold more cash, and are weakly less levered relative to older firms. In Online Appendix E, we consider each of these dimensions in isolation and find that the adjustment of smaller firms is stronger than for larger ones, that the investment response of less levered companies is larger than for more levered ones and that businesses with higher liquidity change capital expenditure more than firms holding less cash. This is not surprising given that all these proxies, including age, are correlated with each other. In Section 2, we have argued on a conceptual basis that age and dividend paying status combined are likely to be better proxies for certain types of financial constraints than these more traditional characteristics. In this section, we want to assess the relative merits of the age-dividend split on statistical grounds.30

Unlike traditional panel regression analyses in which the identification exploits exogenous variation in the cross section, our identification strategy is based on exogenous changes (in monetary policy) that vary over time but are common across firms, while allowing for heterogeneous slopes along a variety of dimensions. Accordingly, the notion of “controlling for other characteristics” requires a different approach than simply adding further regressors to our baseline empirical specification. To examine the marginal contribution of age conditional on other characteristics, we interact the four age/dividends groups with quartiles of the size/leverage/liquidity distribution. This is essentially controlling for the third variable in a semi-parametric manner, a strategy that we refer to as triple-cutting the data or triple sorting.

By looking at the differences between the response of smaller-younger-paying no dividends firms and the estimated effects on smaller-older-paying dividends companies, for instance, one can infer the marginal contribution of age and paying dividends status for a given (smaller) size. Similarly, by comparing smaller-younger-paying no dividends firms to larger-younger-paying no dividends companies, we will be able to assess the marginal contribution of size for a given (younger) age and (paying no) dividends status.

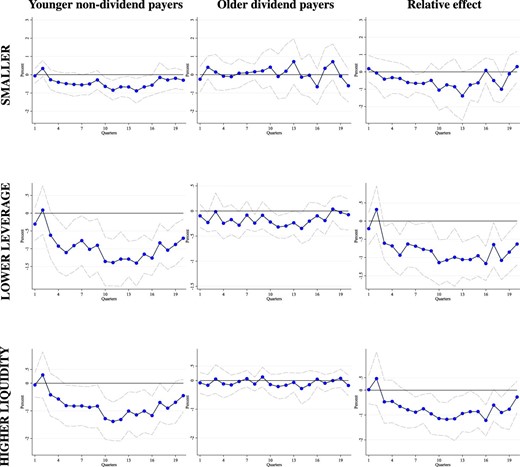

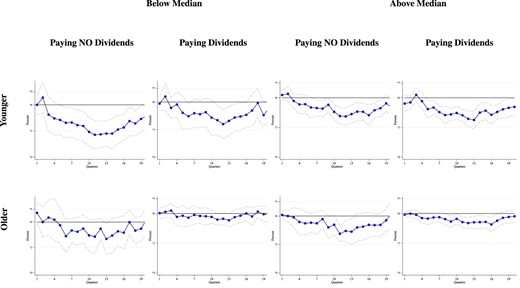

As triple sorting is very demanding on the data, we maximize the number of observations per sub-group by using only two categories for age and two categories for the other characteristics. We maintain the same two age groups from above (based on fifteen years since incorporation). Dividend status is already binary. In terms of the third dimension of interest, we use the most responsive quartile versus the rest of the distribution. To stick with the size example, this means comparing the bottom quartile of size (smaller firms) with the rest of the distribution. This outer product generates eight bins. The results by size, leverage, and liquidity in isolation are reported in Online Appendix E. The full set of impulse response functions for all 8 groups generated by the triple-interaction are reported in Online Appendix F. For sake of exposition, Figure 5 focuses on younger firms paying no dividends versus older firms paying dividends, conditional on the most responsive group according to the third dimension.

Controlling for other firm characteristics. This figure shows the IRFs for the investment rate following a 25 bp increase in the one year interest rate. We run separate regressions for each row. In each row, the interest rate is interacted with three sets of group dummies based on a firm’s age, dividend status and their position in either the size, leverage or liquidity distribution. Younger means less than 15 years since incorporation. Size refers to total assets in the previous year. Leverage is total debt relative to assets in the previous year. Liquidity is cash relative to total assets in the previous year. For size, leverage and liquidity we display the results using the most responsive quartile when the data are cut using these variables alone (see Online Appendix E). Smaller and lower leverage refers to the bottom quartile of each distribution. Higher liquidity refers to the top quartile of the liquidity distribution. The relative effect column refers to separate specifications where the IRFs are estimated relative to older firms paying dividends. The IRFs are estimated using the LP-IV approach described in the text. Dotted lines are 90% standard error bands. Standard errors are computed using the Driscoll–Kraay method, clustering by firm and time, which is robust to very general forms of cross-sectional and temporal dependence.

In the first row of Figure 5, we show that among the smaller companies, only the younger non-dividend payers in the first column adjust their capital expenditure significantly after a monetary policy shock. In contrast, the investment response of small older dividend payers in the second column is not statistically significant. The third column shows the relative effect. As in Figure 4, this column formalizes the test of a difference between the two groups. The third column of the first row therefore shows that small younger-non dividend payers have a much larger response and this is statistically significant at various points in the impulse response horizon. The rest of Figure 5 paints a very similar picture for leverage and liquidity. Among the firms with lower leverage (second row) or with more liquidity (third row), younger non-dividend payers is always the group that adjusts investment the most, as measured by the point estimates. Furthermore, the relative effect in the third column reveals that the response of younger non-dividend payers is significantly larger than for old paying dividend firms.31

Overall, the results in Figure 5 show that younger non-dividend payers drive the larger responses of smaller firms, of less levered companies and of more liquid businesses reported in Online Appendix E (where we split the sample according to each of these characteristics in isolation). Finally, the predictive power of size, leverage, and liquidity is not robust to “controlling for” age. The results are shown in Online Appendix Figure F.1: Once we condition on being young and paying no dividends, we find little differences among firms based on size, leverage, and liquidity. This means that our age based measure is a more direct proxy for the underlying characteristics that predict a larger sensitivity to monetary policy. Once we condition on age, the power of other common proxies is greatly muted. The full set of results for all groups are also shown in Online Appendix F.

In summary, age and dividend status are strong predictors of significant heterogeneity in the response of capital expenditure to changes in monetary policy. This is true over and above any possible heterogeneity by size, leverage, and liquidity. In contrast, the heterogeneity along these traditional (and arguably endogenous) proxies for financial constraints appears weaker than the heterogeneity based on age and dividend status and, more importantly, becomes marginally insignificant once we condition on being young and paying no dividends.

4.3. Contribution to the Average Effect and the Aggregate Investment Response

The evidence in Figure 3 suggests that younger non-dividend payers are likely to drive the average effect on the investment rate in Figure 2. To verify this more formally, we now compute the share of the average response accounted for by this group. We first calculate the (discounted) cumulative percent response in the investment rate for younger non-dividend payers and multiply this by their average investment share (relative to the total investment in the sample). Dividing this object by the sum of the same statistics across all groups provides an estimate of the contribution of younger no-dividend firms to the average response of the investment rate. As might be expected from Figures 2 and 3, this is a sizable number: younger non-dividend payers account for around 2/3 of the average movement in the investment rate in the sample.

A related question is about the contribution of younger non-dividend payers to the response of aggregate investment (rather than of the average investment rate, which normalizes a firm’s capital expenditure by its capital stock). To answer this, we make use of the approximation in continuous time below. A detailed derivation can be found in Online Appendix G. The contribution of each group to the effect of monetary policy on aggregate investment (|$I_{t}$|) can be expressed as a function of the response of the investment rate |$i_{j,t}$| for firm group |$j$| and the size of that group. Specifically, the overall percentage change in aggregate investment, |$\dot{I}_{t}/I_{t}$| can be decomposed as follows:

where |$\omega _{j,t}^{k} \equiv k_{j,t}/K_{t}$| (average capital for group |$j$| relative to the aggregate capital stock) and |$\omega _{j,t}^{I}\equiv I_{j,t}/I_{t}$| (average investment for group |$j$| relative to aggregate investment). |$\dot{i}^{\mathit {net}}_{j,t} \equiv \partial (i_{j,t}-\delta )/\partial r_{t}$| is the estimated group response of the investment rate to monetary policy in Figure 3 and |$\omega _{j,t}^{k}$|, |$\omega _{j,t}^{I}$|, and |$I_{t}/K_{t}$| are computed from Compustat. Finally, |$t$| refers to the entire IRF horizon and we focus on the average response over 20 quarters.

Applying this decomposition reveals that young non-dividend payers account for around |$21\%$| of the response of aggregate investment to monetary policy. This is remarkable given that the capital stock of this group is only |$6\%$| and their share of aggregate investment is only |$8\%$|.32 In short, while younger no dividend firms account for a rather small share of the investment level, their contribution to the aggregate investment changes due to monetary policy is considerably larger.33

5. The Channels of Monetary Transmission

In the previous section, we have shown that younger firms paying no dividends exhibit the largest and most significant adjustment in capital expenditure following a change in interest rates. While traditional proxies of financially constrained firms—such as size, leverage and liquidity—also generate heterogeneity in capital expenditure, the differences across groups are smaller and disappear after conditioning on age and dividend status.

In this section, we examine why younger non-dividend payers respond more. Specifically, to assess the hypothesis that these firms are more exposed to a financial accelerator mechanism, we look at a number of variables from firms’ balance sheet and income statements, paying special attention to the response of collateral values and debt. In particular, we show that the heterogeneity in the response of capital expenditure is mirrored by the response of debt. In contrast, the change in earnings, sales, and interest payments are more homogeneous across groups. This sizable comovement of debt and investment supports the idea that our proxy is indeed capturing a particular form of financial constraints, which are more acute for younger non-dividend payers. This latter group is populated by firms that are also more profitable, growing faster, and/or exhibit higher return volatility. These factors, however, do not explain the results in the previous section: We will show that, although more profitable and higher volatility companies tend to respond more to monetary policy, the effect is driven by the sub-group of younger non-dividend payers.

5.1. Borrowing, Collateral Values, and Financial Frictions

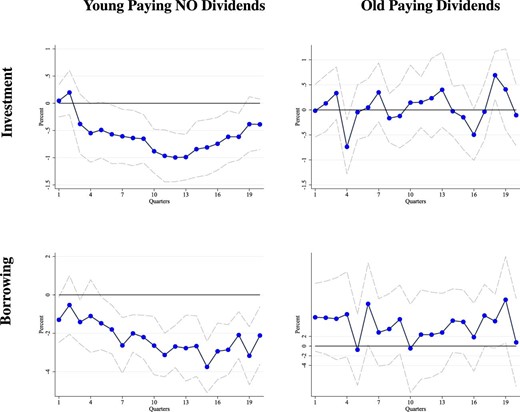

A number of theories emphasize the role of firm balance sheets in amplifying the effects of changes in monetary policy. Higher interest rates lower asset prices and push down equity values. This may lead to a rise in the external finance premium and generate a further decline in investment (as in Bernanke, Gertler, and Gilchrist 1999). Higher interest rates can also trigger a fall in collateral values and lead to a tightening of borrowing constraints whenever a significant portion of debt is secured against collateral (as in Kiyotaki and Moore 1997). The key is that these indirect effects are sufficiently large to trigger amplification though a sizable reduction in borrowing and investment for constrained firms. The simple model in Online Appendix M corroborates this interpretation.34 Since these asset-based channels have important implications for firms’ financing decisions and their balance sheets, in this section we look at how firms’ borrowing decisions and collateral values respond to changes in monetary policy.

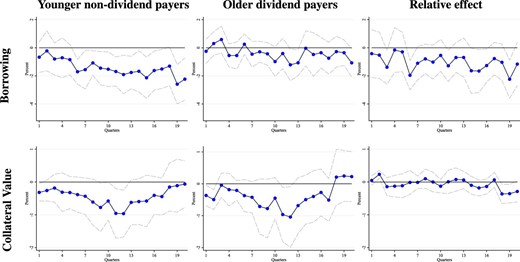

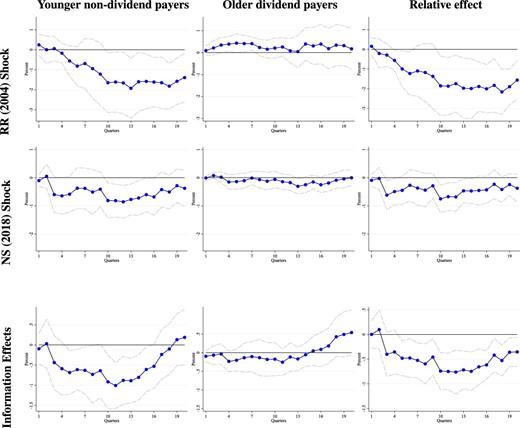

A natural place to start is with the response of borrowing. Financial accelerator theories predict that the borrowing of constrained firms should respond more whenever (i) their debt is secured against collateral, and (ii) collateral values are highly sensitive to changes in monetary policy. In the top row of Figure 6, we report the response real debt growth, which we take as a measure of debt issuance. In the bottom row, we show the response of firms’ collateral at market value (bottom row). This is constructed using changes in the book value of real estate collateral and movements in real estate prices at the state-level, in the spirit of Lian and Ma (2021) and Chaney, Sraer, and Thesmar (2012).35 The left column shows the findings for younger non-dividend payers, the middle column refers to older firms paying dividends. As before, to formally test for a statistically significant difference between the groups, the third column estimates the relative response of younger no-dividend firms, using older dividend payers as reference group in a specification that also includes the interest rate as a separate regressor.

Response of firm finance: borrowing and collateral. This figure shows the IRFs for the investment rate following a 25 bp increase in the one year interest rate. We run separate regressions per each row. The first row shows the response of total real debt growth (annualized). The second row shows the response of real collateral value growth (market value). The market value of collateral is constructed using the change in the book value of corporate real estate assets and using state house price variation as discussed in the data appendix (Online Appendix A). Young refers to less than 15 years since incorporation. The relative effect column refers to separate specifications where the IRFs are estimated relative to older firms paying dividends. The IRFs are estimated using the LP-IV approach described in the text. Dotted lines are 90% standard error bands. Standard errors are computed using the Driscoll–Kraay method, clustering by firm and time, which is robust to very general forms of cross-sectional and temporal dependence.

Two main findings emerge from Figure 6. First, the decline in borrowing after a monetary policy tightening is large and significant at most horizons for younger non-dividend payers.36 In contrast, the change in borrowing for older firms paying dividends is economically modest, being on average less than one third of the effects for younger non-dividend payers and statistically insignificant at almost all horizons. Second, collateral values (in the bottom row) decline for all firms after an increase in interest rates. This is consistent with the notion that credit conditions tighten for financially constrained firms whose borrowing is secured against the value of their collateral.37

To examine further whether the debt of younger non-dividend payers is more sensitive to fluctuations in collateral values, we follow a recent and growing literature on debt covenants, which has documented significant heterogeneity in the types of borrowing contracts across groups of firms. Lian and Ma (2021), for instance, report that asset-based borrowing is more prevalent among younger firms, who lack stable cash flows and typically have not an extensive credit history. On the other hand, earning-based borrowing is predominant among old and large companies. To explore this heterogeneity, we project changes in long-term debt on collateral values and earnings, measured by EBITDA as in Lian and Ma (2021) and Drechsel (2023). We also control for firm fixed effects, as well as other characteristics including size, leverage, liquidity, and Tobin’s Q. Our focus is on heterogeneity in the correlations of borrowing with collateral values and with earnings, by age/dividend status. Standard errors are clustered by firm and time. Table 1 reports the results. The first four rows display the sum of the coefficients on collateral (real estate at market value scaled by lagged total assets), while the bottom four rows show the coefficients on earnings scaled by lagged total assets. The four columns analyze the sensitivity of our estimates across several specifications where we vary the fixed effects included in the regression.

The correlation of borrowing with collateral values and earnings.

| (1) | (2) | (3) | (4) | ||

|---|---|---|---|---|---|

| Baseline | No group FEs | Sector FEs | Region FEs | ||

| (1) | (2) | (3) | (4) | ||

| Collateral | Young no dividends | 0.106*** | 0.106*** | 0.099*** | 0.106*** |

| (0.024) | (0.024) | (0.023) | (0.025) | ||

| Young paying dividends | 0.071* | 0.088** | 0.074* | 0.075* | |

| (0.033) | (0.031) | (0.032) | (0.032) | ||

| Old no dividends | 0.034 | 0.026 | 0.031 | 0.038 | |

| (0.022) | (0.022) | (0.020) | (0.022) | ||

| Old paying dividends | 0.058** | 0.061*** | 0.059*** | 0.059** | |

| (0.017) | (0.017) | (0.016) | (0.017) | ||

| Earnings | Young no dividends | 0.022 | 0.022 | 0.020 | 0.020 |

| (0.013) | (0.013) | (0.013) | (0.013) | ||

| Young paying dividends | 0.070* | 0.070* | 0.067* | 0.069* | |

| (0.030) | (0.031) | (0.030) | (0.030) | ||

| Old no dividends | 0.019 | 0.020 | 0.015 | 0.014 | |

| (0.019) | (0.019) | (0.019) | (0.020) | ||

| Old paying dividends | 0.137*** | 0.137*** | 0.125*** | 0.114*** | |

| (0.028) | (0.028) | (0.026) | (0.028) | ||

| Time varying firm controls | |$\times$| | |$\times$| | |$\times$| | |$\times$| | |

| Firm FE | |$\times$| | |$\times$| | |$\times$| | |$\times$| | |

| Group FE | |$\times$| | |$\times$| | |$\times$| | ||

| Sector |$\times$| Time FE | |$\times$| | ||||

| Region |$\times$| Time FE | |$\times$| | ||||

| (1) | (2) | (3) | (4) | ||

|---|---|---|---|---|---|

| Baseline | No group FEs | Sector FEs | Region FEs | ||

| (1) | (2) | (3) | (4) | ||

| Collateral | Young no dividends | 0.106*** | 0.106*** | 0.099*** | 0.106*** |

| (0.024) | (0.024) | (0.023) | (0.025) | ||

| Young paying dividends | 0.071* | 0.088** | 0.074* | 0.075* | |

| (0.033) | (0.031) | (0.032) | (0.032) | ||

| Old no dividends | 0.034 | 0.026 | 0.031 | 0.038 | |

| (0.022) | (0.022) | (0.020) | (0.022) | ||

| Old paying dividends | 0.058** | 0.061*** | 0.059*** | 0.059** | |

| (0.017) | (0.017) | (0.016) | (0.017) | ||

| Earnings | Young no dividends | 0.022 | 0.022 | 0.020 | 0.020 |

| (0.013) | (0.013) | (0.013) | (0.013) | ||

| Young paying dividends | 0.070* | 0.070* | 0.067* | 0.069* | |

| (0.030) | (0.031) | (0.030) | (0.030) | ||

| Old no dividends | 0.019 | 0.020 | 0.015 | 0.014 | |

| (0.019) | (0.019) | (0.019) | (0.020) | ||

| Old paying dividends | 0.137*** | 0.137*** | 0.125*** | 0.114*** | |

| (0.028) | (0.028) | (0.026) | (0.028) | ||

| Time varying firm controls | |$\times$| | |$\times$| | |$\times$| | |$\times$| | |

| Firm FE | |$\times$| | |$\times$| | |$\times$| | |$\times$| | |

| Group FE | |$\times$| | |$\times$| | |$\times$| | ||

| Sector |$\times$| Time FE | |$\times$| | ||||

| Region |$\times$| Time FE | |$\times$| | ||||

Notes: Standard errors are in parentheses. Collateral|$_t$| is the market value of real estate (calculated using the method outlined in the text and the Online appendix) in period |$t$| relative to total assets at the beginning of the year. Earnings refers to EBITDA in period |$t$| relative to total assets at the beginning of the year. The table shows the sum of the coefficients for years |$t$| and |$t-1$| for both collateral and earnings. Firm and time-two-digit-sector fixed effects are included. Additional firm-level controls are total debt, cash holdings, and cash flows from operations all measured relative to total assets, and Tobin’s Q. Standard errors are clustered by firm and time. Standard errors in parentheses |$^{*} p<0.05$|, |$^{**} p<0.01$|, |$^{***} p<0.001.$|

The correlation of borrowing with collateral values and earnings.

| (1) | (2) | (3) | (4) | ||

|---|---|---|---|---|---|

| Baseline | No group FEs | Sector FEs | Region FEs | ||

| (1) | (2) | (3) | (4) | ||

| Collateral | Young no dividends | 0.106*** | 0.106*** | 0.099*** | 0.106*** |

| (0.024) | (0.024) | (0.023) | (0.025) | ||

| Young paying dividends | 0.071* | 0.088** | 0.074* | 0.075* | |

| (0.033) | (0.031) | (0.032) | (0.032) | ||

| Old no dividends | 0.034 | 0.026 | 0.031 | 0.038 | |

| (0.022) | (0.022) | (0.020) | (0.022) | ||

| Old paying dividends | 0.058** | 0.061*** | 0.059*** | 0.059** | |

| (0.017) | (0.017) | (0.016) | (0.017) | ||

| Earnings | Young no dividends | 0.022 | 0.022 | 0.020 | 0.020 |

| (0.013) | (0.013) | (0.013) | (0.013) | ||

| Young paying dividends | 0.070* | 0.070* | 0.067* | 0.069* | |

| (0.030) | (0.031) | (0.030) | (0.030) | ||

| Old no dividends | 0.019 | 0.020 | 0.015 | 0.014 | |

| (0.019) | (0.019) | (0.019) | (0.020) | ||

| Old paying dividends | 0.137*** | 0.137*** | 0.125*** | 0.114*** | |

| (0.028) | (0.028) | (0.026) | (0.028) | ||

| Time varying firm controls | |$\times$| | |$\times$| | |$\times$| | |$\times$| | |

| Firm FE | |$\times$| | |$\times$| | |$\times$| | |$\times$| | |

| Group FE | |$\times$| | |$\times$| | |$\times$| | ||

| Sector |$\times$| Time FE | |$\times$| | ||||

| Region |$\times$| Time FE | |$\times$| | ||||

| (1) | (2) | (3) | (4) | ||

|---|---|---|---|---|---|

| Baseline | No group FEs | Sector FEs | Region FEs | ||

| (1) | (2) | (3) | (4) | ||

| Collateral | Young no dividends | 0.106*** | 0.106*** | 0.099*** | 0.106*** |

| (0.024) | (0.024) | (0.023) | (0.025) | ||

| Young paying dividends | 0.071* | 0.088** | 0.074* | 0.075* | |

| (0.033) | (0.031) | (0.032) | (0.032) | ||

| Old no dividends | 0.034 | 0.026 | 0.031 | 0.038 | |

| (0.022) | (0.022) | (0.020) | (0.022) | ||

| Old paying dividends | 0.058** | 0.061*** | 0.059*** | 0.059** | |

| (0.017) | (0.017) | (0.016) | (0.017) | ||

| Earnings | Young no dividends | 0.022 | 0.022 | 0.020 | 0.020 |

| (0.013) | (0.013) | (0.013) | (0.013) | ||

| Young paying dividends | 0.070* | 0.070* | 0.067* | 0.069* | |

| (0.030) | (0.031) | (0.030) | (0.030) | ||

| Old no dividends | 0.019 | 0.020 | 0.015 | 0.014 | |

| (0.019) | (0.019) | (0.019) | (0.020) | ||

| Old paying dividends | 0.137*** | 0.137*** | 0.125*** | 0.114*** | |

| (0.028) | (0.028) | (0.026) | (0.028) | ||

| Time varying firm controls | |$\times$| | |$\times$| | |$\times$| | |$\times$| | |

| Firm FE | |$\times$| | |$\times$| | |$\times$| | |$\times$| | |

| Group FE | |$\times$| | |$\times$| | |$\times$| | ||

| Sector |$\times$| Time FE | |$\times$| | ||||

| Region |$\times$| Time FE | |$\times$| | ||||

Notes: Standard errors are in parentheses. Collateral|$_t$| is the market value of real estate (calculated using the method outlined in the text and the Online appendix) in period |$t$| relative to total assets at the beginning of the year. Earnings refers to EBITDA in period |$t$| relative to total assets at the beginning of the year. The table shows the sum of the coefficients for years |$t$| and |$t-1$| for both collateral and earnings. Firm and time-two-digit-sector fixed effects are included. Additional firm-level controls are total debt, cash holdings, and cash flows from operations all measured relative to total assets, and Tobin’s Q. Standard errors are clustered by firm and time. Standard errors in parentheses |$^{*} p<0.05$|, |$^{**} p<0.01$|, |$^{***} p<0.001.$|

The estimates in Table 1 offer two main insights. First, the borrowing of younger non-dividend payers is significantly correlated only with firm collateral.38 The coefficient on earnings is much smaller and statistically indistinguishable from zero. Second, older-dividend payers exhibit a sizable and very significant coefficient on earnings, which is much larger than their coefficient on collateral. Interestingly, young dividend payers display occasionally significant estimates on both collateral and earnings, which are roughly of equal magnitude, which connects to the discussion Section 4.3 about heterogeneity in this group of firms. As in Figure 6, these findings reveal that the borrowing of younger non-dividend payers is far more correlated with collateral values than for older companies or for firms paying dividends. The results in this section are in line with the evidence on debt covenants presented by Lian and Ma (2021), who show that—among U.S. traded companies—only the borrowing of younger firms is predominantly secured against assets, whereas the majority of older firms’ debt is secured against earnings. Lian and Ma’s finding points to the prevalence of asset-based borrowing constraints among younger non-dividend payers, consistent with the large responses and comovement between investment and debt for this group that we have documented above.

Our inference, that the response of younger-non dividend payers reflects tightening borrowing constraints, chimes with two additional pieces of evidence. First, using data on corporate bond yields, Anderson and Cesa-Bianchi (2018) show that the corporate spread increases significantly only for firms with a lower credit rating (younger firms in our sample) following a monetary policy contraction. Second, the aggregate evidence from national statistics in Online Appendix C reveals that, on average, corporate spreads and the policy rate are positively correlated after a monetary policy shock. The positive correlation between interest rates and corporate spreads is also consistent with the evidence in Gertler and Karadi (2015) and Caldara and Herbst (2019). The first finding is consistent with younger firms facing more severe financial frictions; the second result is consistent with financial frictions amplifying the effects of monetary policy.

5.2. The Responses of Cash Flows

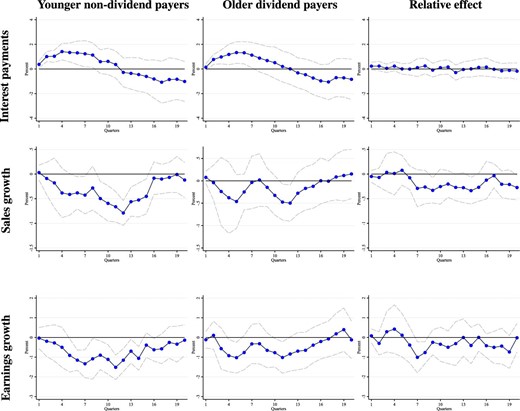

In the previous section, we discussed a prominent example of an amplification channel: monetary policy affects firm investment via collateral values and tighter borrowing conditions. In this section, we look at three cash-flow variables that could reflect alternative channels. First, some younger non-dividend payers may have a larger share of shorter maturity debt and/or more variable rate debt. Accordingly, direct movements in interest payments might account for the heterogeneity in the capital expenditure responses reported in Section 4. Furthermore, younger firms paying no-dividends might face a product demand or a cost schedule with a higher cyclical sensitivity. If so, the response of gross sales and earnings (which are essentially sales net of costs) will be informative about whether this is driving the heterogeneous effects of monetary policy on investment. These potential explanations are explored in Figure 7, where the rows report the response of interest payments, sales, and earnings, respectively, for younger firms not paying dividends (left column) and older companies paying dividends (middle column). The relative effect between these two groups is reported in the third column for formal hypothesis testing purposes.

Response of firm finance: sales, earnings, and interest payments. This figure shows the IRFs for the investment rate following a 25 bp increase in the one year interest rate. We run separate regressions per each row. The first row shows the response of (log) interest payments. The second row shows the response of real sales growth (year on year). The third row shows the response of real earnings growth (measured using the real growth rate of EBITDA). The relative effect column refers to separate specifications where the IRFs are estimated relative to older firms paying dividends. Young means less than 15 years since incorporation. The IRFs are estimated using the LP-IV approach described in the text. Dotted lines are 90% standard error bands. Standard errors are computed using the Driscoll–Kraay method, clustering by firm and time, which is robust to very general forms of cross-sectional and temporal dependence.

At face value, the response of interest expenditure is hard to interpret because this is a function of both interest rates and debt decisions. However, the time profile of the impulse responses in the first row of Figure 7 is very revealing. Within the first year of the shock, interest payments increase significantly. As we have seen in Figures 3 and 6, however, neither investment nor debt respond significantly within the first year, suggesting that the movement in interest expenditure is more likely to reflect the increase in the interest rate. During the second year, the adjustment of interest payments become insignificant and after the second year it turns negative. This is consistent with the significant decline in borrowing during the first year after the shock in Figure 6 but is inconsistent with interest payments being a main driver of the significant investment responses at two and three years in Figure 3. Furthermore, there is little heterogeneity in the responses of interest payments across groups, which is formally verified in the third column of Figure 7.

Younger non-dividend paying firms may also respond more to monetary policy because the demand for their product may be more sensitive to changes in interest rates. This interpretation can be assessed from the second row of Figure 7, which reports the results for the growth of sales. These charts show that the response of sales growth over the first two years after the shock is far more homogeneous than the response of investment, with the relative difference recorded in the third column being statistically insignificant. For example, the average effect in the first six quarters is around 0.2% for both younger non-dividends payers and older dividend payers. Interestingly, some heterogeneity emerges only during the third year (after the investment responses in Figure 3 have peaked), with the highest point estimate for younger non-dividend payers around |$-0.8$| and for older dividend payers at about |$-0.5$|. We conclude that the time profile of the impulse responses of sales is inconsistent with the hypothesis that heterogeneity in product demand is a main driver of the heterogeneity in investment after a change in interest rates.