Abstract

We study the optimal progressivity of personal income taxes in a general equilibrium overlapping generations model where individuals are exposed to idiosyncratic shocks to labor productivity and health status over the lifecycle. Our results—based on a calibration to the US economy—indicate that both, the presence of health risk and the available insurance institutions, have a strong effect on the optimal level of tax progressivity. Given the fragmented and non-universal health insurance system in the US, a welfare maximizing income tax system is substantially more progressive than the current US income tax. The higher progressivity provides additional redistribution and social insurance, especially for unhealthy low income individuals who have limited access to health insurance. When exposure to health risk is removed or reduced by introducing more comprehensive health insurance systems, we observe large decreases in the optimal level of income tax progressivity, and the optimal tax system resembles findings from the previous literature. These findings highlight the importance of accounting for the unique characteristics of health risk and the design of the health insurance system when characterizing optimal income taxes.

1. Introduction

The US income tax system is progressive and plays a key role in shaping the income distribution across households and over time. Traditionally, the optimal taxation literature has investigated optimal progressivity levels in heterogeneous agent models with income risk and incomplete markets (Varian 1980; Conesa and Krueger 2006; Heathcote et al. 2017). In particular, Heathcote et al. (2017) find that in their model, the optimal income tax system is less progressive than the existing system in the US. What is currently missing from the discussion on optimal tax progressivity is the consideration of health risk and limited access to health insurance, which have both been identified as a prominent source of risk and lifecycle inequality (Capatina 2015; De Nardi, Pashchenko, and Porapakkarm 2018). The purpose of this paper is to revisit the optimal tax progressivity in a new analytical framework that explicitly models health risk and institutional features of the US health insurance system.

The presence of health risk as an additional source of agent heterogeneity, in addition to income risk, introduces a new channel that influences the traditional roles of a progressive income tax system.1 In the context of the US policy settings where the health insurance system is fragmented and only provides partial health insurance, we find that the optimal income tax system is more progressive in order to provide a sufficient level of redistribution and social health insurance to unhealthy low income individuals who have limited access to health insurance. However, when more inclusive health insurance systems such as “Medicare for all”—we refer to this as universal public health insurance (UPHI)—are introduced, we observe large decreases in the optimal level of income tax progressivity. When the exposure to health risk is already largely mitigated through the UPHI system, not much additional social health insurance is required from the progressive income tax system and therefore the optimal level of progressivity decreases. Our findings highlight the importance of accounting for health risk and insurance arrangement when characterizing the optimal progressive income system.

We show that the progressive income tax system has two channels that increase welfare: one that reduces post tax earnings inequality and the other that provides support to low income individual who have limited access to health insurance. The former traditionally appears in any models without market mechanisms to hedge against initial skill endowments; meanwhile, the latter appears in this model where the health insurance system fails to protect the poor from high health expenditure. We refer the latter as “health-related tax progressivity” channel.

We next formulate a quantitative model of the US economy and use it to simulate how this health-related tax progressivity channel plays out in a general equilibrium framework. Our quantitative model is an overlapping generations economy model with a consumption, savings, labor, and insurance choice and household heterogeneity due to idiosyncratic shocks to labor productivity and health status. More specifically, our benchmark model combines the key ingredients of a standard heterogeneous agent model with idiosyncratic income risk (Bewley 1986; Huggett 1993; Aiyagari 1994) and ingredients of a heterogeneous agent model with health risk (Jeske and Kitao 2009). Importantly, our model incorporates important institutional features of the US health insurance system, including private individual health insurance (IHI) plans, employer sponsored group health insurance (GHI) plans, Medicaid for the poor, and Medicare for retirees. Individuals have limited access to certain types of health insurance plans and rely partially on precautionary saving and labor supply to smooth consumption spending over the lifecycle. Health expenditure shocks affect household utility via reducing funds available for purchasing final consumption goods. In this incomplete markets setting, the simultaneous presence of both income and health risks shapes the distributions of income, wealth, and consumption. Progressive income taxes and public health insurance simultaneously serve as policy tools that provide social insurance against income and health risks.

We calibrate the model to US data. Our benchmark model is capable of matching labor supply, asset holdings, consumption, health expenditures, and health insurance take-up rates over the lifecycle similar to observable US data. We next use the model to quantify the optimal level of income tax progressivity, using ex-ante expected utility of a newborn agent in a stationary equilibrium as the welfare criterion.

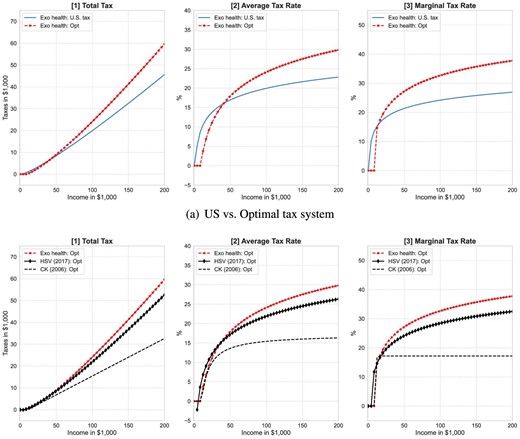

We use a two parameter polynomial tax function following Benabou (2002) to approximate the US income tax code.2 The optimal income tax system is highly progressive and comprises a tax break for income up to |${\$}$|8,800 followed by a steep increase in the marginal tax rate to |$20\%$| at the income level of |${\$}$|20,000. The marginal tax rate then increases further to over |$30\%$| for income above |${\$}$|70,000 and to over 35 percent for income above |${\$}$|150,000. The zero tax bracket at the low end of the income distribution is mainly driven by the high demand for social health insurance for the low income, unhealthy population who has limited access to the US health insurance system. The high tax rates at the upper end of the income distribution are required to meet the financing needs of government spending programs. The optimal income tax system found in our model has much higher marginal tax rates than the optimal ones reported in the previous literature that largely abstract from health risk and insurance (Conesa and Krueger 2006; Heathcote et al. 2017).

In order to compare the progressivity levels of the different income tax regimes, we follow Suits (1977) and compute a tax progressivity (Suits) index, which is a Gini coefficient for income tax contributions by income group.3 The US income tax system in the benchmark model has a Suits index of 0.122. The optimal US tax system is substantially more progressive with a Suits index of 0.218, which reduces income inequality significantly. The after-tax-income Gini coefficient decreases from 0.352 in the benchmark economy to 0.320 after the progressivity level is optimized. Moderate welfare gains of |$0.102\%$| of compensating lifetime consumption at the aggregate level can be realized. These gains are mainly driven by large welfare gains of low and middle income individuals who dominate the welfare losses of the higher income group.

Our results highlight the quantitative importance of the social health insurance role of progressive income taxes. More specifically, in our incomplete markets setting with income and health risks, the redistribution of income via the progressive income tax system provides implicit insurance for both, income and health risks. The latter is a new channel that is missing in prior studies that abstract from modeling health risk. In our model with exogenous health expenditure shocks, unhealthy individuals are more likely to have lower income as health shocks correlate with labor productivity. In addition, lower income workers are less likely to be matched with employers who offer group health insurance and therefore have higher out-of-pocket medical expenditures. Many of these lower income individuals are uninsured as they are not poor enough to qualify for Medicaid and not rich enough to buy private health insurance on their own or through their employers.4 The “poor working class” benefits strongly from the optimized tax system in terms of welfare gains as they benefit from the expanded zero tax threshold. As a result, these individuals are in a better position to smooth consumption fluctuations due to uncertainty in health expenditure and income shocks. The consumption of the uninsured indeed increases under the optimal income tax system. This novel mechanism emphasizes the importance of accounting for health risk and the institutional features of the US healthcare system, when studying the optimal design of a progressive income tax system in the US context.

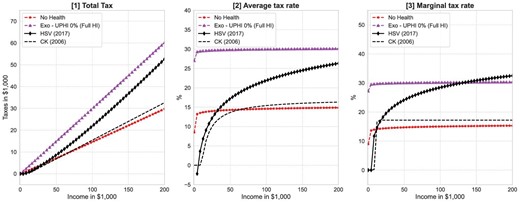

In order to isolate quantitatively the importance of the health-related tax progressivity channel, we take a step back and consider a framework where health risk is no longer present in the model. The demand for health insurance becomes redundant in this reduced model.5 The social health insurance role of the progressive income tax system—the health-related tax progressivity channel—is therefore removed from the model. Our quantitative analysis based on this model indicates that the optimal income tax system is much less progressive than the US status quo tax system and exhibits similar features of the optimal progressive tax code found in Conesa and Krueger (2006). We conclude that health risk, as another source of agent heterogeneity, in addition to income risk, plays an important role in shaping the optimal level of progressivity of the US income tax system. The absence of health risk diminishes the social insurance function of the redistributive income tax system and results in a much lower level of tax progressivity in the optimum.

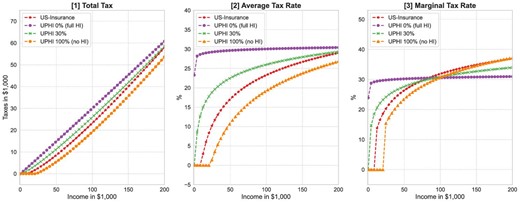

We next investigate how different designs of the US health insurance system affect the optimal design of the progressive income tax system. We focus on two alternative health insurance scenarios: (i) a system where all public and private health insurance are eliminated and individuals rely exclusively on self-insurance (No health insurance), and (ii) a system with Medicare for all workers and retirees that we refer to as universal public health insurance (UPHI). Under the no health insurance scenario, the optimal level of tax progressivity increases significantly and exhibits a much higher tax progressivity (Suits) index of 0.369. Conversely, when an inclusive UPHI system is introduced, the optimal level of tax progressivity decreases significantly. The reason is that the UPHI system already removes a large portion of the health spending risk. In particular, with a coinsurance rate of |$30\%$| the tax break at the lower end of the income distribution decreases significantly to |${\$}$|200, and the marginal tax rates imposed on top earners are lower at approximately |$32\%$| for income over |${\$}$|150,000. The tax progressivity (Suits) index decreases to 0.07 under the UPHI system. Thus, the introduction of UPHI significantly reduces the residual demand for social health insurance provided by the progressive income tax system.

Furthermore, the optimal level of tax progressivity varies significantly across alternative designs of UPHI coinsurance. There is indeed an inverse relationship between UPHI coinsurance rate and optimal tax progressivity. When the UPHI system is more generous with lower coinsurance rates, the optimal tax system becomes less progressive. When the UPHI coinsurance rate is set to zero, namely full health insurance, the optimal tax system resembles a proportional tax schedule found in Conesa and Krueger (2006). When the UPHI system is less generous with higher coinsurance rates, the optimal tax system becomes more progressive and looks more similar to the one found in Heathcote, Storesletten, and Violante (2017). This result again confirms a strong connection between the available health insurance arrangement and the optimal tax progressivity in a model with health and income risks.

As robustness checks we relax several modeling assumptions. Our main results are robust to alternative values of preference parameters, the addition of health-dependent preferences similar to De Nardi, French, and Jones (2010), the addition of state and local taxes as well as corporate taxes similar to Guner, Lopez-Daneri, and Ventura (2016), changes to the labor productivity process, and a higher minimum consumption floor.6

The paper is structured as follows. Section 2 presents the quantitative model. Section 3 describes our calibration strategy. Section 4 describes our experiments and quantitative results. Section 5 is devoted to extensions and sensitivity analyses. Section 6 concludes. The appendices provide additional results from the benchmark model, the model description of the model without health shocks, more details about the data we used for calibration, and a description of the computational algorithm we used to solve the model.

Related Literature.

In a seminal paper, Varian (1980) shows analytically how social insurance can be provided via a progressive tax system. Building on this insight, there exists a large quantitative literature on the optimal design of the progressive income tax code. Examples include Conesa and Krueger (2006), Erosa and Koreshkova (2007), Chambers, Garriga, and Schlagenhauf (2009), Krueger and Ludwig (2016), Stantcheva (2017), Heathcote et al. (2017), and McKay and Reis (2021). However, none of these papers studies progressive income taxes in combination with health insurance policies as our paper does.

Our paper uses an incomplete markets macroeconomic models with heterogeneous agent as pioneered by Bewley (1986) and extended by Huggett (1993) and Aiyagari (1994). The Bewley-type model has been applied widely to quantify the welfare effects of providing social insurance against income risk (Hansen and Imrohoroglu 1992; İmrohoroğlu, İmrohoroğlu, and Joines 1995; Golosov and Tsyvinski 2006; Heathcote, Storesletten, and Violante 2008; Conesa, Kitao, and Krueger 2009; Huggett and Parra 2010). We contribute to this literature a quantitative model with health risk and health insurance arrangement. We highlight that the presence of health-related spending adds a new channel, which affects the social insurance role of a progressive income tax system.

Our work contributes to a growing macro-public finance literature that focuses on health shocks and healthcare policy. Early studies usually view health shocks as health expenditure shocks (Palumbo 1999; Jeske and Kitao 2009). Recent studies endogenize health expenditure (Jung and Tran 2007; Scholz and Seshadri 2013; Jung and Tran 2016; Yogo 2016; Cole, Kim, and Krueger 2019; Fonseca et al. 2021). However, none of these papers analyze the social insurance role of progressive income taxes, which is the focus of this paper. In addition, there is an analogy to the literature that emphasizes the complementarity between progressive taxes and education policies, dated back to an influential work by Bovenberg and Jacobs (2005). Recently, Krueger and Ludwig (2016) provide a quantitative analysis. Our quantitative model contains a similar fiscal externality as it has a similar modeling approach. Different from theirs, our paper aims to better understand the interaction of optimal progressive taxes with health insurance policies.

Finally, our paper is connected to the literature on high marginal tax rates for top income earners. Diamond and Saez (2011) advocates for taxing labor earnings at the high end of the distribution at high marginal rates in excess of |$75\%$|. Badel, Huggett, and Luo (2020) assess the consequences of increasing the marginal tax rate on US top income earners using a human capital model. Guner, Lopez-Daneri, and Ventura (2016) analyze the effectiveness of progressive income tax systems in raising tax revenue, and Kindermann and Krueger (2022) show that high marginal labor income tax rates are an effective tool for social insurance in an overlapping generations model. Different from these studies, we base our analysis on a new model where health risk is an additional source of heterogeneity. We show that high marginal tax rates at the top are an essential component of the optimal progressive tax system.

2. The Quantitative Model

We formulate a baseline quantitative model based on an overlapping generations (OLG), incomplete market model with uninsurable idiosyncratic income risk in the spirit of Conesa and Krueger (2006), augmented by exogenous ex-post heterogeneity in health status due to health risk and a fragmented health insurance system due to the US institutional settings. In the model, the utility maximizing households are exposed to exogenous labor productivity shocks and health expenditure shocks, while having limited access to private or public health insurance contracts. The profit maximizing firm produces a final consumption good and government provides Social Security, Medicare, Medicaid, and consumption insurance for low income households.

2.1. Demographics, Endowments, and Preferences

Individuals are born and become economically active at the age of 21 and live to a maximum of J periods. Individuals are allowed to work for a maximum of JW periods. In each period, individuals of age j face an exogenous survival probability πj(εh) that depends on their exogenous health state εh. Due to the mortality risk, individuals will leave accidental bequests.

In addition, the population grows exogenously at an annual rate |${\mathit {n}}$|. We assume stable demographic patterns, so that age j agents make up a constant fraction μj of the entire population at any point in time. The relative sizes of the cohorts alive μj and the mass of individuals dying |$\tilde{\mu }_{j}$| in each period (conditional on survival up to the previous period) can be recursively defined as

where |$\textit {years}$| denotes the number of years per model period and μj(εh) is the mass of individuals with health εh.

In each period, households are endowed with one unit of time that can be used for work ℓ or leisure. Conditional on labor force participation, a household earns before-tax wage income yj = w × ej(ϑ, εn, εh) × nj at age j, where w is the wage rate, and ej is a labor productivity endowment that depends on age j, a permanent income group ϑ, an idiosyncratic productivity shock εn, and idiosyncratic health state εh. Labor shocks follow a Markov process with transition probability matrix Πn. Parameter |$\bar{n}_{j}$| denotes age-dependent fixed cost of working.

The period utility function |$u(c_{j},\ell _{j};\bar{n}_{j}\cdot 1_{[0\le n_{j}]})$| depends on consumption (c), leisure (ℓ), and labor force participation status, which is only equal to 1 if labor supply exceeds a minimum threshold.

2.2. Health Status, Expenditure, and Insurance

Individuals are different in their health status εh, which evolves exogenously over their life time. Specifically, health status follows a Markov process that depends on age and the permanent income group. The conditional transition probabilities are elements of matrix Πh(j, ϑ). A specific level of health expenditures m(j, ϑ, εh) is linked directly to health status and fluctuates accordingly. In addition, the permanent income type and age also affect the fluctuation of exogenous health expenditure. It is important to note that health affects consumption and utility indirectly via exogenous shocks to health expenditure and labor productivity in the household budget constraint in this baseline model (namely the budget channel). In an extension, we will relax this assumption and allow for the exogenous health state to directly affect household preferences (namely a morbidity channel).

Workers can buy two types of private health insurance policies: a group health insurance plan (GHI) via their employer or an individual health insurance plan (IHI). In the US setting, GHI is not only more strictly regulated than IHI but also subsidized via the US tax system via tax deductible premium payments. This makes GHI a particularly attractive form of health insurance. Agents are required to buy insurance before the realization of their health state and the associated medical expenditures and insurance needs to be renewed each period. GHI can only be bought by workers who receive a GHI offer from their employer. Let εGHI be a binary random variable that indicates the state of the GHI offer from the employer. The GHI offers follow a Markov process summarized as the two state transition matrix ΠGHI(j, ϑ) that depends also on age and an individuals permanent income group. A fraction ψ ∈ [0, 1] of the insurance premium for GHI, |$\text{prem}_{j}^{\text{GHI}}$|, is paid for by the employer, the remainder of the premium |$\widehat{\text{prem}}_{j}^{\text{GHI}}=(1-\psi )\text{prem}_{j}^{\text{GHI}}$| is tax deductible and paid by the worker. This premium is group rated so that insurance companies are not allowed to screen workers by health.7 If a worker is not offered GHI by their employer, then the worker can buy IHI. In this case, the insurance premium is not tax deductible and the insurance company screens the workers by age and health status, |$\text{$\text{prem}$}^{\text{IHI}}(j,\epsilon ^{h})$|.8

There are two public health insurance programs in the US health insurance system: Medicaid for the poor workers and Medicare for retirees. To be eligible for Medicaid, agents are required to pass an income and asset test. After retirement (j > JW + 1) all agents are covered by public health insurance, which is a combination of Medicare and Medicaid. Let inj denote the insurance state, which can take on the following values:

The out-of-pocket health expenditure oj(m) depends on health insurance status

where 0 ≤ γin ≤ 1 are the coinsurance rates of the different insurance types.

2.3. Insurance Companies

We abstain from modeling insurance companies as profit maximizing firms and simply allow for a premium markup ω. Since insurance companies in the individual market screen customers by age and health, we impose separate clearing conditions for each age-health type, so that premiums, premIHI(j, h), adjust to balance

where |$x_{j,-\epsilon ^{h}}$| is the state vector for cohort age j not containing health state εh since we do not want to aggregate over the health state vector εh in this case. The clearing condition for the group health insurances is simpler as only one price, premGHI, adjusts to balance

where |$\omega _{j,h}^{\text{IHI}}$| and ωGHI are markup factors that determine loading costs (fixed costs) and γIHI and γGHI are coinsurance rates. The respective left-hand-sides in the above expressions summarize aggregate payments made by insurance companies, whereas the right-hand-sides aggregate the premium collections one period prior. Since premiums are invested for one period, they enter the capital stock and we therefore multiply the term with the after tax gross interest rate R.

2.4. Technology and Factor Prices

The production sector is modeled by a representative firm that uses physical capital K and effective labor services N to produce output. The representative firm solves the following maximization problem:

taking the rental rate of capital q and the wage rate w as given. Capital depreciates at rate δ in each period.

Similarly to Jeske and Kitao (2009), we assume that the firm offering GHI to its workers subsidizes a fraction ψ of the premium cost. The firm passes these costs on to its employees by lowering the efficiency wage. To ensure the zero profit condition the firm subtracts the cost cE from the wage rate, which is just enough to cover the total premium cost of the firm. The effective wage rate received by the household with a GHI offer is therefore |$\widehat{w}=(w-1_{[\text{$\epsilon $}^{\text{GHI}}=1]}\times c_{E}).$| The zero profit condition implies that the wage reduction equals

In this scenario, high productivity workers effectively pay higher contributions toward financing the employer contribution to GHI as their wage deductions are larger in absolute terms. The remaining share of the GHI premium |$\widehat{\text{prem}}{}^{\text{GHI}}=\left(1-\psi \right)\times \text{prem$^{\text{GHI}}$}$| is income tax deductible and paid by the worker directly.

2.5. Government and Fiscal Policy

The government has the following fiscal activities.

Spending Programs.

The government runs five main spending programs: Social Security, Medicare, Medicaid, Social Transfers, and general government consumption. Social Security benefits are available only to the retirees after the eligibility age (j > JW). The benefit payment is determined by the average earnings history of a permanent income type |$\bar{y}^{\vartheta }$|. Retiring households are also eligible for Medicare after age j > JW at which point they start paying a Medicare premium premMCare every period. The surplus/deficit of Social Security and Medicare are given by

Medicaid is a public health insurance program for the poor. Working households are eligible for Medicaid payments if they pass the income and asset tests |$y_{j}<\bar{y}^{\text{MAid}}$| and |$a_{j}<\bar{a}^{\text{MAid}}$|, respectively. Social Security, Medicare, and Medicaid are included into the overall government budget constraint.9 Social Transfers bSI is a social insurance program that targets low income earners to guarantee a minimum consumption level |$\underline{c}$|. Finally, general government consumption CG is a residual (unproductive) government spending program.

Taxes.

The government raises revenues by imposing various taxes on income, consumption, and assets. This includes a progressive income tax |$T^{y}(y_{j}^{\text{T}})$| on taxable income |$y_{j}^{\text{T}}$|, which is the sum of labor income and capital interest income net of some deductibles as described in the next section. In addition, the government collects payroll taxes |$T^{{\rm SS}}(y_{j}^{{\rm SS}};\, \bar{y}^{{\rm SS}})$| and |$T^{{\rm MCare}}(y_{j}^{{\rm SS}})$| for Social Security and Medicare, respectively. The tax base for these payroll taxes |$y_{j}^{{\rm SS}}$| is defined as labor income minus GHI premiums. GHI premiums can be deducted from the progressive income tax base as well as the payroll tax base. In addition, the payroll tax for Social Security is proportional but capped at the maximum taxable earnings of |$\bar{y}^{{\rm SS}}$|. Finally, the government taxes consumption at a rate of τc and bequests at a rate of τBeq.

The progressive income tax schedule is modeled via a parametric function |$\tilde{\tau }(y^{\text{T}})=y^{\text{T}}-\lambda \times (y^{\text{T}})^{(1-\tau )}$|, where |$\tilde{\tau }(y^{\text{T}})$| denotes tax revenue as a function of taxable income yT, τ is the progressivity parameter, and λ is a scaling factor to match the US income tax revenue. This tax function is fairly general and captures the common cases:

This tax function has a long tradition in public finance (Musgrave 1959; Kakwani 1977) and was implemented into a dynamic setting by Benabou (2002) and more recently used in Heathcote et al. (2017). This tax function is flexible and can be used to model the transfer programs. Note that, Heathcote et al. (2017) abstract from modeling government transfer programs explicitly, but allow negative income taxes to act as implicit government transfers. We instead model the US institutional details of government transfer program explicitly via Social Security, Medicare, Medicaid, and Social Transfers. To avoid double counting, we impose a non-negative income tax restriction

This non-negative restriction eliminates all government transfers embedded in the tax function.

Budget Balancing.

The government budget constraint is given by

where surplus = surplusSS + surplusMCare is the combined surplus/deficit of Medicare and Social Security. The government adjusts the progressive income tax to balance its budget.

2.6. The Household Problem

In the model, we distinguish between workers and retirees.

Workers.

The state vector of a worker at a particular age is defined as |$x_{j}=\lbrace \vartheta ,a_{j},\text{$\text{in}_{j}$},\epsilon _{j}^{n},\epsilon ^{h},\epsilon _{j}^{\text{GHI}}\rbrace \in \lbrace 1,2,3\rbrace \times R^{+}\times \lbrace 0,1,2,3\rbrace \times \lbrace 1,2,3,4,5\rbrace \times \lbrace 1,2,3,4,5\rbrace \times \lbrace 0,1\rbrace$|, where ϑ denotes the permanent income group of no-high-school, high-school, and college types, aj denotes the beginning-of-period assets, inj denotes the health insurance state, |$\epsilon _{j}^{n}$| denotes the labor shock, and εh denotes the exogenous health state, and |$\epsilon _{j}^{\text{GHI}}$| is the employer (with group health insurance) matching shock. After the realization of the state variables, agents simultaneously chose from their choice set

where cj is consumption, ℓj is leisure, aj+1 are asset holdings for the next period, and inj+1 is the health insurance state for next period in order to maximize their lifetime expected utility. All choice variables in the optimization problem are functions of the state vector but we suppress this notation in order to not clutter the exposition. The household problem of the working household can be recursively written as

where β is a time preference factor, πj(εh) is the age and health state dependent survival probability, w is the market wage rate, r is the interest rate, o(mj) is out-of-pocket medical spending, and premin is the insurance premium paid. The indicator functions are defined as 1[true] = 1 and 1[false] = 0. Accidental bequests bBeq are redistributed to surviving households in a lump-sum fashion.10 Labor income |$y_{j}^{n}$|, total taxable income |$y_{j}^{\text{T}}$|, and payroll tax eligible income |$y_{j}^{ss}$| are defined as

where private GHI premiums are tax deductible as are out-of-pocket health expenses that exceed |$7.5\%$| of adjusted gross income.11

Consumption is taxed with rate τc, lump-sum bequests bBeq are taxed at rate τBeq and the remaining taxes are defined as

where Ty is a progressive income tax function of taxable household income |$y_{j}^{\text{T}}$|, τSS is the social security payroll tax levied on “social security wages”—essentially wages minus GHI premiums—and an upper contribution limit of |$\bar{y}^{{\rm SS}}$|, and |$T^{{\rm MCare}}$| is a Medicare payroll function with the same tax base but without an upper limit.12 Social transfers are defined as

and ensure a minimum consumption floor |$\underline{c}$| after medical expenses and taxes are paid for. A household consuming at the lower bound cannot save into the next period or purchase private insurance.

Average past labor earnings for each permanent income group ϑ follow

where |$\boldsymbol{x}\left(\vartheta \right)$| is the mass of households belonging to permanent income group ϑ.

Retirees.

Households can stop working at any time. Households retire at age j > JW at which point they receive Social Security benefits and qualify for Medicare.13 The state vector of a retiree at a particular age is defined as xj = {ϑ, aj, εh} ∈ {1, 2, 3} × R+ × {1, 2, 3, 4, 5}. The household optimization problem reduces to

where taxable income |$y_{j}^{\text{T}}$| is defined as

For retirees out-of-pocket expenses plus Medicare premiums that exceed 7.5% of gross income are tax deductible.14 Social insurance transfers are defined as

Since we force every retired individual into the combined Medicare/Medicaid program, the social insurance transfers include the Medicare premium.

Aggregation.

We denote |$\boldsymbol{x}\equiv \lbrace j,\, x_{j}\rbrace$| as the augmented state vector including age j and |$\Lambda \left(\boldsymbol{x}\right)$| is the measure of households with state |$\boldsymbol{x}$|, which incorporates the relative cohort sizes μj.

2.7. Competitive Equilibrium

The competitive equilibrium of the model with exogenous health spending risk is defined as follows. Given the transition probability matrices |$\lbrace \Pi _{j}^{n},\Pi _{j}^{h},\Pi _{j,\vartheta }^{\text{GHI}}\rbrace _{j=1}^{J}$| for ϑ ∈ {1, 2, 3}, the survival probabilities |$\lbrace \pi _{j} (\epsilon ^{h})\rbrace _{j=1}^{J}$| and the exogenous government policies exogenous government policies |$\lbrace T_{j}^{y},b_{j}^{\text{SI}},b_{j}^{{\rm SS}} \rbrace _{j=1}^{J}$| and |$\lbrace \tau ^{c},\tau ^{{\rm SS}},\tau ^{{\rm MCare}},\text{prem}^{{\rm MCare}},\gamma ^{{\rm MCare}},\gamma ^{\text{MAid}},C_{G}\rbrace ,$| a competitive equilibrium is a collection of sequences of distributions |$\Lambda \left(\boldsymbol{x}\right)$| of household decisions |$\lbrace c(\boldsymbol{x}),\ell (\boldsymbol{x}),a(\boldsymbol{x}),\text{in}\left(\boldsymbol{x}\right)\rbrace ,$| aggregate stocks of physical capital and effective labor services {K, N}, factor prices {w, q, R}, and insurance premiums {premIHI(j, εh), premGHI} such that:

|$\left\lbrace c\left(\boldsymbol{x}\right),\ell \left(\boldsymbol{x}\right),a\left(\boldsymbol{x}\right),in\left(\boldsymbol{x}\right)\right\rbrace$| solves the consumer problem (8, 9) ,

- the firm first order conditions hold$$\begin{eqnarray} w & = \frac{\partial F\left(K,N\right)}{\partial N},\\ q & = \frac{\partial F\left(K,N\right)}{\partial K},\\ R & = 1+q-\delta =1+r, \end{eqnarray}$$

- markets clear(16)$$\begin{eqnarray} K&=\int a(\boldsymbol{x})+\text{Prem}^{\text{GHI}}\left(\boldsymbol{x}\right)+\text{Prem}^{\text{IHI}}\left(\boldsymbol{x}\right)d\Lambda (\boldsymbol{x}) \end{eqnarray}$$(17)$$\begin{eqnarray} N&=\int e(\boldsymbol{x})\left(1-\ell (\boldsymbol{x})\right)d\Lambda (\boldsymbol{x}).\\ B^{\text{Beq}} & = \sum \limits _{j=1}^{J}\tilde{\mu }_{j}\int a_{j}(x_{j})d\Lambda (x_{j}), \end{eqnarray}$$

- the aggregate resource constraint holds$$\begin{eqnarray} C_{G}+\int \left(c\left(\boldsymbol{x}\right)+m\left(\boldsymbol{x}\right)+a\left(\boldsymbol{x}\right)\right)d\Lambda \left(\boldsymbol{x}\right)=Y+\left(1-\delta \right)K, \end{eqnarray}$$

the government programs clear so that (5),(6), and (7) hold,

the budget conditions of the insurance companies (2) and (3) hold, and

- the distribution is stationary$$\begin{eqnarray} (\mu _{j+1},\Lambda (x_{j+1}))=T_{\mu ,\Lambda }(\mu _{j},\Lambda (x_{j})), \end{eqnarray}$$where Tμ, Λ is a one period transition operator on the measure distribution$$\begin{eqnarray} \Lambda (\boldsymbol{x^{\prime }})=T_{\Lambda }(\Lambda (\boldsymbol{x})). \end{eqnarray}$$

3. Calibration

We calibrate the model to match data of the US economy between 1999 and 2009. Macroeconomic data moments include capital accumulation, patterns of labor supply, and health insurance take-up rates over the life cycle. For the calibration we distinguish between two sets of parameters: (i) externally selected parameters, and (ii) internally calibrated parameters. Externally selected parameters are estimated independently from our model and are either based on our own estimates using data from the Medical Expenditure Panel Survey (MEPS) or estimates provided by other studies. The model unit is an individual that we calibrate using information from the male and female heads of Health Insurance Eligibility Units (HIEU), which is a subset of a household in MEPS and comprises |$44\%$| women.15

We summarize these external parameters in Table 1. Internally calibrated parameters are assigned values so that model-generated data match a given set of targets from US data. These parameters are presented in Table 2. Model generated data moments and target moments from US data are juxtaposed in Table 3.16

3.1. Demographics, Endowments, and Preferences

Demographics.

We model households from age 21 to age 95. One model period is defined as 5 years, which results in J = 15 model periods. A typical individual works for nine periods and retiree for six periods. Once the individual enters period Jr+1 = 9, corresponding to the age of 65, she is forced to retire. We set the population annual growth rate to |$\mathit {n}=0.01$|, and we take the age and health specific survival probabilities π(h(εh)) from İmrohoroğlu and Kitao (2012) shown panel [8] of Figure 1. For the purpose of survival probabilities, we distinguish between healthy and sick individuals. The nature of exogenous health states εh is described in Section 2.2.

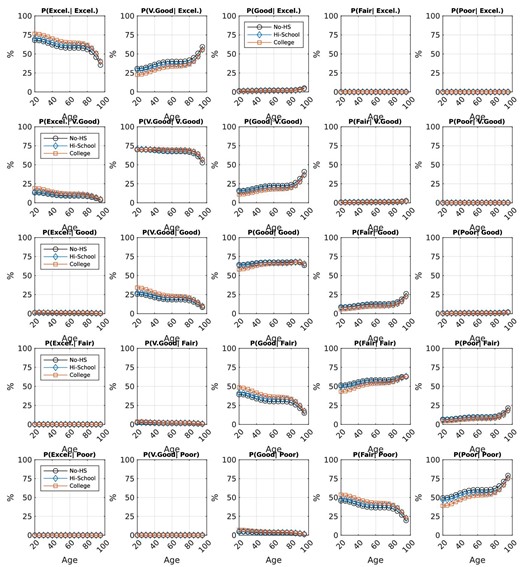

![Data input: exogenous health state process and health spending. Healthy is defined as an individual reporting either Excellent, Very Good, or Good health. Sick is defined as Fair or Poor health. Panels [1]–[4] show the average medical spending per age group (20–24, 25–29, 30–34, ...), self-reported health status, and permanent income group (no high school, high school, or college and higher). Panel [5] shows the average out-of-pocket health expenditures by age group and permanent income type. Panel [6] shows the medical spending distribution of the model period of 5 years. Panel [7] shows the self-reported health states by age group. The survival probabilities in panel [8] are from İmrohoroğlu and Kitao (2012), who base their estimates on data from the Health and Retirement Study and life table estimates in Bell and Miller (2005). Data source is MEPS 1999–2009. The observational unit is the head of a Health Insurance Eligibility Unit (HIEU), which is a subset of a household. We apply population weights.](https://oup.silverchair-cdn.com/oup/backfile/Content_public/Journal/jeea/21/5/10.1093_jeea_jvad010/2/m_jvad010fig1.jpeg?Expires=1750198579&Signature=mZIbAeh7aIr1eL096~HqAzLehdMuJ5CGB0GNI5OoBTE79ABfbngoSXyTHDfiokx7vRIgYdtaIlFG~5jpv2NbmMo2hc1UxREl9Yu36CWoOs43fw5y-xJPETMNuM6BcsWwdZ-m9S~6SvGfffkJ8RF9ncozG0DIG0V9EHUK-W7bYZvxBozy5oQ1wkb5n4cKpqMCVoFNvt1jvSyxOx4jSrO77tZnm9DN5z~y1ZGhlHg1iFvUbE6-9jWqf1TB3w4p3uHseeKIo~FYYuSvrQ7LuhPf4VB4MSeOiefGeO~uYWtJMR7dSp3dbevBSnk9ZleuEnFpK~OuaPMB1MuCfH6BpCFgow__&Key-Pair-Id=APKAIE5G5CRDK6RD3PGA)

Data input: exogenous health state process and health spending. Healthy is defined as an individual reporting either Excellent, Very Good, or Good health. Sick is defined as Fair or Poor health. Panels [1]–[4] show the average medical spending per age group (20–24, 25–29, 30–34, ...), self-reported health status, and permanent income group (no high school, high school, or college and higher). Panel [5] shows the average out-of-pocket health expenditures by age group and permanent income type. Panel [6] shows the medical spending distribution of the model period of 5 years. Panel [7] shows the self-reported health states by age group. The survival probabilities in panel [8] are from İmrohoroğlu and Kitao (2012), who base their estimates on data from the Health and Retirement Study and life table estimates in Bell and Miller (2005). Data source is MEPS 1999–2009. The observational unit is the head of a Health Insurance Eligibility Unit (HIEU), which is a subset of a household. We apply population weights.

Endowments.

We model the labor income process by assuming that labor productivity at age j is driven by an age, income group, and stochastic health state dependent component |$\bar{e}_{j}(\vartheta ,\, h(\epsilon ^{h}))$| and a residual stochastic labor shock component |$\epsilon _{j}^{n}$|

The permanent income group is defined as the education level ϑ in the first model period.

Using 1999–2009 MEPS data, we construct cohort adjusted and bias corrected wage profiles for each education–health subgroup (ϑ, h(εh)) limiting the sample to heads of health insurance eligibility units (HIEU) with labor incomes larger than |${\$}$|400.17 We distinguish between three permanent educational groups

and two health states

These are standard definitions for healthy and sick in the health macro literature. Panel [3] in Figure 4 depicts the fraction of healthy individuals. We then deflate hourly wage observations with the urban CPI and remove cohort effects. Following the procedure in Casanova (2013) and Rupert and Zanella (2015), we subsequently estimate a selection model to remove the selection bias that is typically associated with wage observations to get an average wage offer rate for each (ϑ, h(εh)) subgroup. We finally smooth the wage profiles with a second degree polynomial in age.18

Data input: conditional health status Markov transition probabilities. The estimates of the conditional health state transition probabilities are based on an ordered logit model. Data source is MEPS 1999–2009, heads of HIEU, population weighted.

![Calibration targets: Labor market and insurance percentages. Labor participation (5 year averages) in Panel [1] and average work hours in Panel [2] are calibration targets that determine the fixed cost of labor participation as well as the consumption versus leisure weight in the utility function. Panels [3]–[6] show the fraction of individuals with individual health insurance (IHI), employer provided group health insurance (GHI), as well as the recipients of Medicaid and Medicare. Data source is MEPS 1999–2009, heads of HIEU, population weighted.](https://oup.silverchair-cdn.com/oup/backfile/Content_public/Journal/jeea/21/5/10.1093_jeea_jvad010/2/m_jvad010fig3.jpeg?Expires=1750198579&Signature=oOPtg4SVWkWkLsY-3cev2tFUenSutZBD4rDkrAUSU6cCnd64HQRORyZ89swB~MNdAL8q2lo82yMBLJK8lRRRa72r0xnZMf3ctCpYigKApvnA32o1kMti6TiL1q4iIJVC5VTTI5WF7wU693SzSieDLtavU-s7cPpyUV27zTVjd5qAwEoaHmo08U-ieou7TofFpfb2FNHftj60qwJLUZnCvCXxwLXQxHtBtnxwZYUi9Z2IJoye9O4L5M7yrC6PcEjdkZMQFqqggso7kYT5fz002KbRYFdELCTfjzJFeY7Phl1eOvHgq4hqYdyKSupJzXiL-t-22t7vQsjlgp23N4vXKQ__&Key-Pair-Id=APKAIE5G5CRDK6RD3PGA)

Calibration targets: Labor market and insurance percentages. Labor participation (5 year averages) in Panel [1] and average work hours in Panel [2] are calibration targets that determine the fixed cost of labor participation as well as the consumption versus leisure weight in the utility function. Panels [3]–[6] show the fraction of individuals with individual health insurance (IHI), employer provided group health insurance (GHI), as well as the recipients of Medicaid and Medicare. Data source is MEPS 1999–2009, heads of HIEU, population weighted.

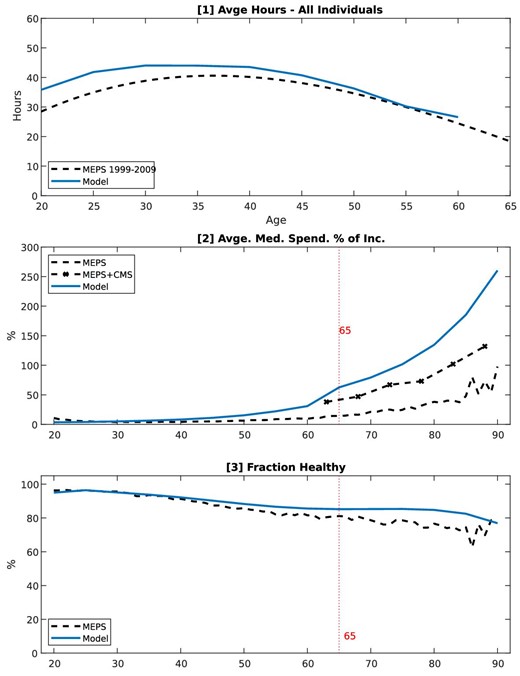

Model performance: Lifecycle profiles. These are not calibration targets. Data source is MEPS 1999–2009, heads of HIEU, population weighted.

The stochastic component is modeled as an auto-regressive process so that

with persistence parameter ρ and a white-noise disturbance |$\varepsilon \sim N\left(0,\sigma _{\varepsilon }^{2}\right)$|. To calibrate the stochastic component εn, we use ρ = 0.977 and |$\sigma _{\epsilon }^{2}=0.0141$| based on estimates in French (2005), who uses Panel Study of Income Dynamics (PSID) data and controls for cohort effects and health states. We approximate the joint distribution of the persistent and transitory shocks using a five-state first-order discrete Markov process following Tauchen and Hussey (1991).

Preferences.

We specify period utility as

We set the relative risk aversion parameter σ to 3, and the intertemporal discount factor β to 0.99 to match the capital–output ratio target in equilibrium. Labor is chosen from a grid n ∈ {0, nmin , …, nmax }, where the minimum amount of non-zero labor possible is nmin = 300 hours per year. The fixed cost of working |$\bar{n}_{j}$| is set to match the average labor participation rate per 5-year age group from MEPS. The consumption intensity parameter η is 0.272 to match average labor hours of the working population. The resulting Frisch labor elasticity is state dependent and the average Frisch elasticity of age j individuals can be calculated based on individuals that are working as19

where |$1_{[0\le n_{j}(x_{j})]}$| is an indicator function equal to 1 if an individual is working. Our calibration results in average Frisch elasticities between 1.19 for younger workers and 1.51 for older workers.20 Section 5.3 provides robustness checks using parameter values for σ and η that result in slightly lower Frisch elasticities. Finally, in our model the intertemporal elasticity of substitution (IES) is |$\frac{1}{3}.$|21

3.2. Health Status, Health Expenditure, and Insurance

Health Status And Expenditure.

We group individuals into five health groups εh ∈ {1, 2, 3, 4, 5} by self-reported health status: 1. excellent health, 2. very good health, 3. good health, 4. fair health, and 5. poor health. We then use data from MEPS 1999–2009 to estimate the magnitude of the age dependent health expenditure shocks m(j, ϑ, εh) as well as the 5 × 5 Markov transition probability matrix Πh(j, ϑ) that contains the conditional health state transition probabilities |$\Pr (\epsilon _{j+1}^{h}|\epsilon _{j}^{h},\vartheta ).$|

We calculate average medical spending of each health state type by age group (20–24, 25–29, 30–34, etc.) and education level (no high school, high school, or college and higher) to determine the magnitude of the health spending shocks m(j, ϑ, εh) for a model period. Since MEPS only accounts for about 65%–70% of health care spending in the national accounts (see Sing et al. 2006; Bernard et al. 2012) we scale up the medical spending profiles for individuals older than 65 similar to Pashchenko and Porapakkarm (2013). The resulting spending profiles are shown in panels [1]–[4] of Figure 1.22

We next estimate an ordered logit model with the future health state as dependent variable. We regress this on current health state, a 4th order age polynomial, and indicator variables for relationship status, gender, race, schooling type, region, birth cohort, and a variable controlling for household income. We then use these estimates and predict the probability to move between health states by age and schooling type. This results in conditional transition probabilities |$\Pr (\epsilon _{t+1}^{h}|\epsilon _{t}^{h},j,\vartheta )$|, where t is the current year and t + 1 is the future year. We collect these annual transition probabilities into a transition probability matrix Πh(t, ϑ), and then transform these annual conditional probabilities into 5-year period probabilities according to Πh(j = 1, ϑ) = Πh(t = 20, ϑ) × Πh(t = 21, ϑ) × … × Πh(t = 24, ϑ) using matrix multiplication. As an example, the resulting model transition probability in the first row/first column of matrix Πh(j = 1, ϑ) is |$\Pr (\epsilon _{j+1}^{h}=\text{excellent}|\epsilon _{j}^{h}=\text{excellent},\vartheta )$| or the conditional probability of a 20 year old person in excellent health to still be in excellent health 5 years later. The transition probabilities between all health states are summarized in Figure 2.

Note that, our modeling choice of the health spending process has two important limitations. First, the Markov assumption cannot fully capture the complex health transition dynamics in the real world as recently discussed in Bianco and Moro (2022), Hosseini, Kopecky, and Zhao (2022), and De Nardi, Pashchenko, and Porapakkarm (2018). Second, the 5-year frequency in the model is likely to understate the variation in medical spending. For instance, the model assumes that a 20 year old person in excellent health has the average medical spending of people in excellent health aged 20–24 in MEPS. The person is assumed to be “stuck” with excellent health for 5 years, which underestimates her true health spending risk. Similarly, a 20 year old person in poor health is assumed to have the average medical spending of individuals in poor health aged 20–24 in MEPS. This person is assumed to be “stuck” with poor health for 5 years which, on average, overestimates the true health spending of this type.

Group Insurance Offer.

We estimate a Markov process that governs the group insurance offer probability using MEPS, which contains information about whether agents have received a group health insurance offer from their employer, offer shock εGHI = {0, 1}, where 0 indicates no offer and 1 indicates a group insurance offer. Since the probability of a GHI offer |$\Pr (\epsilon _{j+1}^{\text{GHI}}|\epsilon _{j}^{\text{GHI}},\vartheta )$| is highly correlated with income, we construct the group offer transition matrix |$\Pi _{j,\vartheta }^{\text{GHI}}$| by education type ϑ based on estimates of a logit model. Figure C.6 in Online Appendix C shows the conditional transition probabilities.

Coinsurance Rates.

We define the coinsurance rate as the fraction of out-of-pocket health expenditures over total health expenditures. The coinsurance rates used in our model, therefore, include copays and other direct out-of-pocket payments. We use MEPS data from 1999 to 2000 and calculate the average coinsurance rate of heads of HIEUs (population weighted) by age for all four insurance types represented in the model. Consequently, we set the coinsurance rates for the different types of insurance plans to γIHI = 0.46, γGHI = 0.31,

3.3. Insurance Companies

Age and health dependent markups |$\omega _{j,\epsilon ^{h}}^{\text{IHI}}$| in expression (2) are set to zero. The GHI markup ωGHI in expression (3) is set to |$6\%$|, which is below the estimate of loading costs of |$11\%$| by Kahn et al. (2005). IHI premiums |$\text{prem}_{j,\epsilon ^{h}}^{\text{IHI}}$| and GHI premium premGHI clear the zero-profit conditions (2) and (3), respectively.23

3.4. Technology and Factor Prices

We assume that output is produced using a Cobb–Douglas production function with capital K and labor N inputs so that

where α is the share of capital in total income. We set the capital share α = 0.35 and the annual capital depreciation rate at δ = 0.064 according to new estimates in Koh, Santaeulàlia-Llopis, and Zheng (2020). Total factor productivity A is normalized to unity. The fraction ψ = 0.8 as in Jeske and Kitao (2009).

3.5. Fiscal Policy

Taxes.

The consumption tax rate, τC, is set to |$5\%$|. The tax progressivity level τ is set to 0.053 based on Guner, Lopez-Daneri, and Ventura (2016).24 We calibrate the tax scaling parameter to match the relative size of the government budget so that λ = 1.017.

Social Security, Medicare, and Medicaid.

The Social Security system is partly financed via a payroll tax with a contribution limit. The Social Security payroll tax is |$\tau ^{{\rm SS}}=10.6\%$|. The Social Security payroll tax is collected on labor income up to a maximum of |${\$}$|106,800.25

The Medicare system is also self-financed via a payroll tax and Medicare premium payments. The Medicare payroll tax is |$\tau ^{{\rm MCare}}=2.9\%$|. It is not restricted by an upper limit (see SSA 2007). Overall, the model results in total income tax revenue of |$25\%$| of GDP, Social Security tax revenue of |$8.1\%$| of GDP and Medicare tax revenue of |$1.9\%$| of GDP.

Expenditures.

The government uses income tax revenue to make lump-sum transfers to maintain a minimum level of consumption |$\underline {c}$| of |${\$}$|2,500, which is close to the estimated level from De Nardi, French, and Jones (2010). Residual unproductive government consumption CG of |$15\%$| of GDP.

Social Security.

In the model, social security transfers are defined as a function of average labor income per skill type |$\bar{y}^{\vartheta }$|. Let |$T^{{\rm SS}}(\vartheta )=\Psi \times \bar{y}^{\vartheta }$| be type specific pension payments, where Ψ is the average replacement rate that determines the size of the pension payments. In the model, total pension payments amount to |$6\%$| of GDP. This is close to the number reported in the budget tables of the Office of Management and Budget (OMB) for 2008, which is close to |$5\%$|.

Medicare and Medicaid for Retirees.

According to data from the National Health Expenditure Accounts (NHEA 2020a), Medicare spending in 2010 was |$3.47\%$| of GDP and Medicaid spending (Federal and State) was |$2.65\%$| of GDP. We use data from CMS (Keehan et al. 2011) and calculate that the share of total Medicaid spending that is spent on individuals older than 65 is about |$36\%$|. Adding this amount to the total size of Medicare results in a combined total of 4.4% of GDP of public health insurance reimbursements for the old, while the residual Medicaid program that covers workers is about |$1.7\%$| of GDP.

Since MEPS only accounts for about 65%–70% of health care spending in the national accounts (see Sing et al. 2006; Bernard et al. 2012), we would not be able to meet this target of health spending of the elderly. Based on communication with CMS (Office of the Actuary), we therefore scale up the MEPS based health spending shocks to match the adjusted medical spending over income ratios in panel [3] of Figure A.3 in the Online Appendix. Given the estimated coinsurance rate of γMCare from MEPS and the exogenous, scaled up, health expenditure shocks, the size of the combined Medicare/Medicaid program in the model is |$3.1\%$| of GDP. We fix the premium for Medicare at |$2.11\%$| of per-capita GDP as in Jeske and Kitao (2009). The Medicare tax τMcare is set to 2.9%.26

Medicaid for Workers.

According to Kaiser (2013), 16 states have Medicaid eligibility thresholds below |$50\%$| of the FPL, 17 states have eligibility levels between |$50\%$| and |$99\%$|, and 18 states have eligibility levels that exceed |$100\%$| of the FPL.27 In addition, state regulations vary greatly with respect to the asset test of Medicaid. According to MEPS data, |$9.2\%$| of working age individuals have some form of public health insurance. In the model, we therefore calibrate the Medicaid income eligibility level to |$70\%$| of the FPL (|$\bar{y}^{\text{MAid}}=0.7\times$|FPL) to match the fraction of 20–39 year old individuals on Medicaid. We then calibrate the asset test level, |$\bar{a}^{{{\rm MAid}}}$| to |$17\%$| of the FPL, so match the fraction of individuals aged 40–64 on Medicaid according to panel [6] in Figure 3. Overall |$5.7\%$| of the working age population becomes eligible for Medicaid.

3.6. Model Performance

Table 3 and Figure 3 show the targeted moments of the calibration. In addition, we perform checks of non-targeted data moments in Figure 4. The model results in medical spending as fraction of GDP of |$17.2\%$|, which is close to the |$17.3\%$| reported in CMS data for 2010.28 The percent of workers on Medicaid is |$15\%$| and slightly below the percentage of workers on Medicaid reported in MEPS. The capital output ratio is 3.0, which is a standard value in the calibration literature. The Frisch labor supply elasticities increase with age and range from 1.19 to 1.51, which is within the range of estimated macro elasticities from 1.1 to 1.7 (Fiorito and Zanella 2012). The interest rate in the model is |$5.9\%$|, which falls within the range of estimated capital returns in Gomme, Ravikumar, and Rupert (2011).

External parameters.

| Parameter descriptions | Parameter values | Sources |

|---|---|---|

| Periods J | 15 | |

| Periods work JW | 9 | Age 20–64 |

| Years modeled | 75 | Age 20–95 |

| Total factor productivity A | 1 | Normalization |

| Capital share in productivity α | 0.36 | Koh, Santaeulàlia-Llopis, and Zheng (2020) |

| Capital depreciation δ | |$6.4\%$| | Koh, Santaeulàlia-Llopis, and Zheng (2020) |

| Firm share of premGHI ψ | 0.8 | Jeske and Kitao (2009) |

| Relative risk aversion σ | 3 | Standard values between 2.5 and 3.5 |

| Survival probabilities πj(h(εh)) | Panel 8, Figure 1 | İmrohoroğlu and Kitao (2012) |

| Health shocks |$\epsilon _{j}^{h}$| | Panel 7, Figure 1 | MEPS 1999–2009 |

| Medical spending shocks m(j, ϑ, εh) | Panel 1–3, Figure 1 | MEPS 1999–2009 |

| Health transition probabilities |$\Pi _{j}^{h}$| | Online Appendix C | MEPS 1999–2009 |

| Persistent labor shock auto-correlation ρ | 0.977 | French (2005) |

| Variance transitory labor shock |$\sigma _{\varepsilon }^{2}$| | 0.0141 | French (2005) |

| Bias adjusted wage profile |$\bar{e}_{j}\left(\vartheta ,h\left(\epsilon ^{h}\right)\right)$| | Online Appendix C, Figure C.3 | MEPS 1999–2009 |

| Private HI coins. γIHI | 0.46 | MEPS 1999–2009 |

| Private group HI coins. γGHI | 0.31 | |

| Medicaid coins. γMAid | $\begin{array}{c}0.11\end{array}$ | MEPS 1999–2009 |

| Medicare coins. γMCare | 0.30 | MEPS 1999–2009 |

| Medicare premiums/GDP | |$2.11\%$| | Jeske and Kitao (2009) |

| Consumption tax τC | |$5\%$| | IRS |

| Bequest tax τBeq | |$20\%$| | De Nardi and Yang (2014) |

| Payroll tax social security τSS | |$12.4\%$| | SSA (2007) |

| Payroll tax Medicare τMCare | |$2.9\%$| | SSA (2007) |

| Government consumption CG/Y | |$15\%$| | BEA 2009 |

| Tax progressivity parameterτ | 0.053 | Guner, Lopez-Daneri, and Ventura (2016) |

| Consumption floor cmin | |${\$}$|2,500 | De Nardi, French, and Jones (2010) |

| Parameter descriptions | Parameter values | Sources |

|---|---|---|

| Periods J | 15 | |

| Periods work JW | 9 | Age 20–64 |

| Years modeled | 75 | Age 20–95 |

| Total factor productivity A | 1 | Normalization |

| Capital share in productivity α | 0.36 | Koh, Santaeulàlia-Llopis, and Zheng (2020) |

| Capital depreciation δ | |$6.4\%$| | Koh, Santaeulàlia-Llopis, and Zheng (2020) |

| Firm share of premGHI ψ | 0.8 | Jeske and Kitao (2009) |

| Relative risk aversion σ | 3 | Standard values between 2.5 and 3.5 |

| Survival probabilities πj(h(εh)) | Panel 8, Figure 1 | İmrohoroğlu and Kitao (2012) |

| Health shocks |$\epsilon _{j}^{h}$| | Panel 7, Figure 1 | MEPS 1999–2009 |

| Medical spending shocks m(j, ϑ, εh) | Panel 1–3, Figure 1 | MEPS 1999–2009 |

| Health transition probabilities |$\Pi _{j}^{h}$| | Online Appendix C | MEPS 1999–2009 |

| Persistent labor shock auto-correlation ρ | 0.977 | French (2005) |

| Variance transitory labor shock |$\sigma _{\varepsilon }^{2}$| | 0.0141 | French (2005) |

| Bias adjusted wage profile |$\bar{e}_{j}\left(\vartheta ,h\left(\epsilon ^{h}\right)\right)$| | Online Appendix C, Figure C.3 | MEPS 1999–2009 |

| Private HI coins. γIHI | 0.46 | MEPS 1999–2009 |

| Private group HI coins. γGHI | 0.31 | |

| Medicaid coins. γMAid | $\begin{array}{c}0.11\end{array}$ | MEPS 1999–2009 |

| Medicare coins. γMCare | 0.30 | MEPS 1999–2009 |

| Medicare premiums/GDP | |$2.11\%$| | Jeske and Kitao (2009) |

| Consumption tax τC | |$5\%$| | IRS |

| Bequest tax τBeq | |$20\%$| | De Nardi and Yang (2014) |

| Payroll tax social security τSS | |$12.4\%$| | SSA (2007) |

| Payroll tax Medicare τMCare | |$2.9\%$| | SSA (2007) |

| Government consumption CG/Y | |$15\%$| | BEA 2009 |

| Tax progressivity parameterτ | 0.053 | Guner, Lopez-Daneri, and Ventura (2016) |

| Consumption floor cmin | |${\$}$|2,500 | De Nardi, French, and Jones (2010) |

Notes: These parameters are based on our own estimates from MEPS and CMS data as well as other studies.

External parameters.

| Parameter descriptions | Parameter values | Sources |

|---|---|---|

| Periods J | 15 | |

| Periods work JW | 9 | Age 20–64 |

| Years modeled | 75 | Age 20–95 |

| Total factor productivity A | 1 | Normalization |

| Capital share in productivity α | 0.36 | Koh, Santaeulàlia-Llopis, and Zheng (2020) |

| Capital depreciation δ | |$6.4\%$| | Koh, Santaeulàlia-Llopis, and Zheng (2020) |

| Firm share of premGHI ψ | 0.8 | Jeske and Kitao (2009) |

| Relative risk aversion σ | 3 | Standard values between 2.5 and 3.5 |

| Survival probabilities πj(h(εh)) | Panel 8, Figure 1 | İmrohoroğlu and Kitao (2012) |

| Health shocks |$\epsilon _{j}^{h}$| | Panel 7, Figure 1 | MEPS 1999–2009 |

| Medical spending shocks m(j, ϑ, εh) | Panel 1–3, Figure 1 | MEPS 1999–2009 |

| Health transition probabilities |$\Pi _{j}^{h}$| | Online Appendix C | MEPS 1999–2009 |

| Persistent labor shock auto-correlation ρ | 0.977 | French (2005) |

| Variance transitory labor shock |$\sigma _{\varepsilon }^{2}$| | 0.0141 | French (2005) |

| Bias adjusted wage profile |$\bar{e}_{j}\left(\vartheta ,h\left(\epsilon ^{h}\right)\right)$| | Online Appendix C, Figure C.3 | MEPS 1999–2009 |

| Private HI coins. γIHI | 0.46 | MEPS 1999–2009 |

| Private group HI coins. γGHI | 0.31 | |

| Medicaid coins. γMAid | $\begin{array}{c}0.11\end{array}$ | MEPS 1999–2009 |

| Medicare coins. γMCare | 0.30 | MEPS 1999–2009 |

| Medicare premiums/GDP | |$2.11\%$| | Jeske and Kitao (2009) |

| Consumption tax τC | |$5\%$| | IRS |

| Bequest tax τBeq | |$20\%$| | De Nardi and Yang (2014) |

| Payroll tax social security τSS | |$12.4\%$| | SSA (2007) |

| Payroll tax Medicare τMCare | |$2.9\%$| | SSA (2007) |

| Government consumption CG/Y | |$15\%$| | BEA 2009 |

| Tax progressivity parameterτ | 0.053 | Guner, Lopez-Daneri, and Ventura (2016) |

| Consumption floor cmin | |${\$}$|2,500 | De Nardi, French, and Jones (2010) |

| Parameter descriptions | Parameter values | Sources |

|---|---|---|

| Periods J | 15 | |

| Periods work JW | 9 | Age 20–64 |

| Years modeled | 75 | Age 20–95 |

| Total factor productivity A | 1 | Normalization |

| Capital share in productivity α | 0.36 | Koh, Santaeulàlia-Llopis, and Zheng (2020) |

| Capital depreciation δ | |$6.4\%$| | Koh, Santaeulàlia-Llopis, and Zheng (2020) |

| Firm share of premGHI ψ | 0.8 | Jeske and Kitao (2009) |

| Relative risk aversion σ | 3 | Standard values between 2.5 and 3.5 |

| Survival probabilities πj(h(εh)) | Panel 8, Figure 1 | İmrohoroğlu and Kitao (2012) |

| Health shocks |$\epsilon _{j}^{h}$| | Panel 7, Figure 1 | MEPS 1999–2009 |

| Medical spending shocks m(j, ϑ, εh) | Panel 1–3, Figure 1 | MEPS 1999–2009 |

| Health transition probabilities |$\Pi _{j}^{h}$| | Online Appendix C | MEPS 1999–2009 |

| Persistent labor shock auto-correlation ρ | 0.977 | French (2005) |

| Variance transitory labor shock |$\sigma _{\varepsilon }^{2}$| | 0.0141 | French (2005) |

| Bias adjusted wage profile |$\bar{e}_{j}\left(\vartheta ,h\left(\epsilon ^{h}\right)\right)$| | Online Appendix C, Figure C.3 | MEPS 1999–2009 |

| Private HI coins. γIHI | 0.46 | MEPS 1999–2009 |

| Private group HI coins. γGHI | 0.31 | |

| Medicaid coins. γMAid | $\begin{array}{c}0.11\end{array}$ | MEPS 1999–2009 |

| Medicare coins. γMCare | 0.30 | MEPS 1999–2009 |

| Medicare premiums/GDP | |$2.11\%$| | Jeske and Kitao (2009) |

| Consumption tax τC | |$5\%$| | IRS |

| Bequest tax τBeq | |$20\%$| | De Nardi and Yang (2014) |

| Payroll tax social security τSS | |$12.4\%$| | SSA (2007) |

| Payroll tax Medicare τMCare | |$2.9\%$| | SSA (2007) |

| Government consumption CG/Y | |$15\%$| | BEA 2009 |

| Tax progressivity parameterτ | 0.053 | Guner, Lopez-Daneri, and Ventura (2016) |

| Consumption floor cmin | |${\$}$|2,500 | De Nardi, French, and Jones (2010) |

Notes: These parameters are based on our own estimates from MEPS and CMS data as well as other studies.

Exogenous health model: internal (calibrated) parameters.

| Parameters | Values | Calibration targets | Model generated moments | Data | Sources |

|---|---|---|---|---|---|

| Discount factor β | 0.995 | |$\frac{K}{Y}$| | 3 | 3 | Standard value |

| Population adjustment rate n | 0.01 | Fraction of pop 65+ | |$17.5\%$| | |$17.5\%$| | US census 2010 |

| Fixed time cost of labor |$\bar{n_{j}}$| | [0.05, 0.17] | Labor participation by age | Panel 1, Figure 3 | MEPS 1999–2009 | |

| Preference consumption vs. leisure η | 0.272 | Average work hours workers | Panel 2, Figure 3 | MEPS 1999–2009 | |

| GHI premium scaling φGHI | 0.75 | GHI take-up of 25 year olds | Panel 4, Figure 3 | MEPS 1999–2009 | |

| Tax scaling parameter λ | 1.016 | Clear govt BC with CG/Y | |$15\%$| | |$15\%{-}17\%$| | BEA 2009 |

| Pension scaling Ψ | 0.32 | Size of social security/Y | |$5\%$| | |$4.8\%$| | SSA (2010) |

| Medicaid asset test |$\bar{a}^{\text{MAid}}$| | |${\$}$|75,000 | Workers age 40–64 on Medicaid | Panel 6, Figure 3 | MEPS 1999–2009 | |

| Medicaid income test |$\bar{y}^{\text{MAid}}$| | |${\$}$|5,500 | Workers age 20–39 on Medicaid | Panel 6, Figure 3 | MEPS 1999–2009 |

| Parameters | Values | Calibration targets | Model generated moments | Data | Sources |

|---|---|---|---|---|---|

| Discount factor β | 0.995 | |$\frac{K}{Y}$| | 3 | 3 | Standard value |

| Population adjustment rate n | 0.01 | Fraction of pop 65+ | |$17.5\%$| | |$17.5\%$| | US census 2010 |

| Fixed time cost of labor |$\bar{n_{j}}$| | [0.05, 0.17] | Labor participation by age | Panel 1, Figure 3 | MEPS 1999–2009 | |

| Preference consumption vs. leisure η | 0.272 | Average work hours workers | Panel 2, Figure 3 | MEPS 1999–2009 | |

| GHI premium scaling φGHI | 0.75 | GHI take-up of 25 year olds | Panel 4, Figure 3 | MEPS 1999–2009 | |

| Tax scaling parameter λ | 1.016 | Clear govt BC with CG/Y | |$15\%$| | |$15\%{-}17\%$| | BEA 2009 |

| Pension scaling Ψ | 0.32 | Size of social security/Y | |$5\%$| | |$4.8\%$| | SSA (2010) |

| Medicaid asset test |$\bar{a}^{\text{MAid}}$| | |${\$}$|75,000 | Workers age 40–64 on Medicaid | Panel 6, Figure 3 | MEPS 1999–2009 | |

| Medicaid income test |$\bar{y}^{\text{MAid}}$| | |${\$}$|5,500 | Workers age 20–39 on Medicaid | Panel 6, Figure 3 | MEPS 1999–2009 |

Notes: We choose these parameters in order to match a set of target moments in the data.

Exogenous health model: internal (calibrated) parameters.

| Parameters | Values | Calibration targets | Model generated moments | Data | Sources |

|---|---|---|---|---|---|

| Discount factor β | 0.995 | |$\frac{K}{Y}$| | 3 | 3 | Standard value |

| Population adjustment rate n | 0.01 | Fraction of pop 65+ | |$17.5\%$| | |$17.5\%$| | US census 2010 |

| Fixed time cost of labor |$\bar{n_{j}}$| | [0.05, 0.17] | Labor participation by age | Panel 1, Figure 3 | MEPS 1999–2009 | |

| Preference consumption vs. leisure η | 0.272 | Average work hours workers | Panel 2, Figure 3 | MEPS 1999–2009 | |

| GHI premium scaling φGHI | 0.75 | GHI take-up of 25 year olds | Panel 4, Figure 3 | MEPS 1999–2009 | |

| Tax scaling parameter λ | 1.016 | Clear govt BC with CG/Y | |$15\%$| | |$15\%{-}17\%$| | BEA 2009 |

| Pension scaling Ψ | 0.32 | Size of social security/Y | |$5\%$| | |$4.8\%$| | SSA (2010) |

| Medicaid asset test |$\bar{a}^{\text{MAid}}$| | |${\$}$|75,000 | Workers age 40–64 on Medicaid | Panel 6, Figure 3 | MEPS 1999–2009 | |

| Medicaid income test |$\bar{y}^{\text{MAid}}$| | |${\$}$|5,500 | Workers age 20–39 on Medicaid | Panel 6, Figure 3 | MEPS 1999–2009 |

| Parameters | Values | Calibration targets | Model generated moments | Data | Sources |

|---|---|---|---|---|---|

| Discount factor β | 0.995 | |$\frac{K}{Y}$| | 3 | 3 | Standard value |

| Population adjustment rate n | 0.01 | Fraction of pop 65+ | |$17.5\%$| | |$17.5\%$| | US census 2010 |

| Fixed time cost of labor |$\bar{n_{j}}$| | [0.05, 0.17] | Labor participation by age | Panel 1, Figure 3 | MEPS 1999–2009 | |

| Preference consumption vs. leisure η | 0.272 | Average work hours workers | Panel 2, Figure 3 | MEPS 1999–2009 | |

| GHI premium scaling φGHI | 0.75 | GHI take-up of 25 year olds | Panel 4, Figure 3 | MEPS 1999–2009 | |

| Tax scaling parameter λ | 1.016 | Clear govt BC with CG/Y | |$15\%$| | |$15\%{-}17\%$| | BEA 2009 |

| Pension scaling Ψ | 0.32 | Size of social security/Y | |$5\%$| | |$4.8\%$| | SSA (2010) |

| Medicaid asset test |$\bar{a}^{\text{MAid}}$| | |${\$}$|75,000 | Workers age 40–64 on Medicaid | Panel 6, Figure 3 | MEPS 1999–2009 | |

| Medicaid income test |$\bar{y}^{\text{MAid}}$| | |${\$}$|5,500 | Workers age 20–39 on Medicaid | Panel 6, Figure 3 | MEPS 1999–2009 |

Notes: We choose these parameters in order to match a set of target moments in the data.

Exogenous health model: performance of the benchmark model.

| Moments | Model | Data | Sources |

|---|---|---|---|

| Medical expenses/Y | |$16.5\%$| | |$15.2\%$| | NHEA (2020b) |

| Gini medical spending | 0.56* | 0.60 | MEPS 1999–2009 |

| Gini gross income | 0.40* | 0.46 | MEPS 1999–2009 |

| Gini labor income | 0.55* | 0.54 | MEPS 1999–2009 |

| Gini assets | 0.58 | 0.69 | PSID 1999–2009 |

| Frisch labor supply elasticities | 1.19–1.51 | 1.1–1.7 | Fiorito and Zanella (2012) |

| Interest rate: r | |$5.9\%$| | |$5.2\%$|–|$5.9\%$| | Gomme, Ravikumar, and Rupert (2011) |

| Size of Medicare/Y | |$5.5\%$| | |$4.4\%\, (3.47\%)^{**}$| | NHEA (2020a) |

| Size of Medicaid/Y | |$0.68\%$| | |$1.7\%\, (2.65\%)^{***}$| | NHEA (2020a) |

| Moments | Model | Data | Sources |

|---|---|---|---|

| Medical expenses/Y | |$16.5\%$| | |$15.2\%$| | NHEA (2020b) |

| Gini medical spending | 0.56* | 0.60 | MEPS 1999–2009 |

| Gini gross income | 0.40* | 0.46 | MEPS 1999–2009 |

| Gini labor income | 0.55* | 0.54 | MEPS 1999–2009 |

| Gini assets | 0.58 | 0.69 | PSID 1999–2009 |

| Frisch labor supply elasticities | 1.19–1.51 | 1.1–1.7 | Fiorito and Zanella (2012) |

| Interest rate: r | |$5.9\%$| | |$5.2\%$|–|$5.9\%$| | Gomme, Ravikumar, and Rupert (2011) |

| Size of Medicare/Y | |$5.5\%$| | |$4.4\%\, (3.47\%)^{**}$| | NHEA (2020a) |

| Size of Medicaid/Y | |$0.68\%$| | |$1.7\%\, (2.65\%)^{***}$| | NHEA (2020a) |

Notes: These are not calibration targets.*The Gini coefficients of flow variables from the model are based on 5 year averages, whereas the Gini coefficients based on MEPS data are based on annual flow variables. MEPS is an overlapping panel, where individuals are only observed over two consecutive years so that 5 year averages cannot be computed for a particular individual.**We do not distinguish between Medicare and Medicaid for the population older than 65. We therefore compare the size of Medicare in the model to the spending of Medicare plus Medicaid on individuals older than 65 to capture the out-of-pocket spending of the older generation more realistically without explicitly modeling Medicaid past the age of 65. According to NHEA (2010) aggregate, Medicare spending in 2010 was approximately 3.47% of GDP. More details are provided in Section 3.5. ***Medicaid in the model refers to the portion of Medicaid that targets the working age population. According to NHEA (2010) aggregate, Medicaid payments for individuals younger than 65 in 2010 was approximately 1.7% of GDP. More details are provided in Section 3.5.

Exogenous health model: performance of the benchmark model.

| Moments | Model | Data | Sources |

|---|---|---|---|

| Medical expenses/Y | |$16.5\%$| | |$15.2\%$| | NHEA (2020b) |

| Gini medical spending | 0.56* | 0.60 | MEPS 1999–2009 |

| Gini gross income | 0.40* | 0.46 | MEPS 1999–2009 |

| Gini labor income | 0.55* | 0.54 | MEPS 1999–2009 |

| Gini assets | 0.58 | 0.69 | PSID 1999–2009 |

| Frisch labor supply elasticities | 1.19–1.51 | 1.1–1.7 | Fiorito and Zanella (2012) |

| Interest rate: r | |$5.9\%$| | |$5.2\%$|–|$5.9\%$| | Gomme, Ravikumar, and Rupert (2011) |

| Size of Medicare/Y | |$5.5\%$| | |$4.4\%\, (3.47\%)^{**}$| | NHEA (2020a) |

| Size of Medicaid/Y | |$0.68\%$| | |$1.7\%\, (2.65\%)^{***}$| | NHEA (2020a) |

| Moments | Model | Data | Sources |

|---|---|---|---|

| Medical expenses/Y | |$16.5\%$| | |$15.2\%$| | NHEA (2020b) |

| Gini medical spending | 0.56* | 0.60 | MEPS 1999–2009 |

| Gini gross income | 0.40* | 0.46 | MEPS 1999–2009 |

| Gini labor income | 0.55* | 0.54 | MEPS 1999–2009 |

| Gini assets | 0.58 | 0.69 | PSID 1999–2009 |

| Frisch labor supply elasticities | 1.19–1.51 | 1.1–1.7 | Fiorito and Zanella (2012) |

| Interest rate: r | |$5.9\%$| | |$5.2\%$|–|$5.9\%$| | Gomme, Ravikumar, and Rupert (2011) |

| Size of Medicare/Y | |$5.5\%$| | |$4.4\%\, (3.47\%)^{**}$| | NHEA (2020a) |

| Size of Medicaid/Y | |$0.68\%$| | |$1.7\%\, (2.65\%)^{***}$| | NHEA (2020a) |

Notes: These are not calibration targets.*The Gini coefficients of flow variables from the model are based on 5 year averages, whereas the Gini coefficients based on MEPS data are based on annual flow variables. MEPS is an overlapping panel, where individuals are only observed over two consecutive years so that 5 year averages cannot be computed for a particular individual.**We do not distinguish between Medicare and Medicaid for the population older than 65. We therefore compare the size of Medicare in the model to the spending of Medicare plus Medicaid on individuals older than 65 to capture the out-of-pocket spending of the older generation more realistically without explicitly modeling Medicaid past the age of 65. According to NHEA (2010) aggregate, Medicare spending in 2010 was approximately 3.47% of GDP. More details are provided in Section 3.5. ***Medicaid in the model refers to the portion of Medicaid that targets the working age population. According to NHEA (2010) aggregate, Medicaid payments for individuals younger than 65 in 2010 was approximately 1.7% of GDP. More details are provided in Section 3.5.

The model reproduces the hump shaped pattern of average work hours (see panel [1] of Figure 4). The model also tracks the fraction of healthy individuals as shown in panel [2] of Figure 4. In addition, the model reproduces the lifecycle patterns of labor income, work hours, and labor participation by education group and health state.29 Finally, the model generates realistic Gini coefficients for medical spending (0.56 in model vs. 0.60 in data) and labor income (0.547 in model vs. 0.54 in data).

4. Quantitative Analysis

We first quantify the optimal income tax system in the benchmark calibrated economy using a parametric income tax function from Benabou (2002) and Heathcote et al. (2017). We then analyze quantitatively how the optimal level of tax progressivity changes under different assumptions on health risk and insurance arrangement.

4.1. The Optimal Degree of Tax Progressivity with Exogenous Health Risk

The Government Problem.

In order to characterize the optimal level of progressivity in the tax function in this large-scale OLG model with uninsurable idiosyncratic income and health risks, we follow the Ramsey tradition and restrict the choice dimension of the government similar to Conesa, Kitao, and Krueger (2009).30 We assume that the social welfare function–defined as the ex-ante lifetime utility of an individual born into the stationary equilibrium–depends on the two parameters of the income tax polynomial: WF(λ, τ) = ∫V(xj=1|λ, τ)dΛ(xj=1). The government’s objective is to choose the tax parameter values {λ, τ} that maximize the social welfare function taking the decision rules of consumers and firms as well as competitive equilibrium conditions into account. All other policy variables are kept unchanged.

We implement the government problem as a grid-search over values of progressivity parameter τ, while letting the scaling parameter λ adjust to keep the government budget balanced. We fix the level of exogenous government consumption CG to the benchmark government consumption level |$\overline{C_{G}}$|. The tax maximization problem can be written as

where the terms on the right hand side of the constraint are aggregates that depend on the tax parameters due to tax distortions and general equilibrium price effects. The optimal tax policy and the reported welfare results are based on the comparison between two steady states.

Aggregate Effects.

Table 4 summarizes the macroeconomic and welfare effects. Optimal income tax progressivity implies that the government does not collect taxes on annual income below |${\$}$|8,810, while it imposes higher marginal taxes than under current tax law on income exceeding this threshold. This increase in progressivity affects the work and savings decisions of households as follows. Low income households that were close to the income threshold for Medicaid would decide to either not work or work little in order to qualify for public health insurance. Once the tax free threshold is increased, some of these workers begin to participate in the labor market again, which allows them to move out of Medicaid. We can observe this in the increase of the labor participation rate from 67.14% to 69.21% and the decrease in workers insured by Medicaid from 8.8% to 5.8%. These are primarily younger and low risk workers. Once they join the labor force, they purchase IHI or GHI and since they are lower risk, the premiums in both insurance markets decrease, which leads to previously uninsured individuals enter the insurance markets as well. Overall, we therefore observe an increase in individuals with IHI from 7.8% to 10.17% and an increases of individuals with GHI from 63.8% to 65.7%. Higher income individuals, on the other hand, have to pay higher income taxes, which raises the marginal taxes for both labor income and interest income. These workers therefore do not only reduce their work hours but also their saving. As a result, the capital stock decreases by almost 10% and weekly hours worked decrease by about |$6\%$|. This leads to subsequent losses of output. Overall GDP decreases by about |$6.6\%$|.

Optimal tax progressivity in model with exogenous health and income risk.

| (1) Benchmark | (2) Optimized progressivity τ* | |

|---|---|---|

| Output (GDP) | 100 | 93.36 |

| Capital (K) | 100 | 90.77 |

| Non-medical consumption (C) | 100 | 93.25 |

| Labor participation rate | 67.14 | 69.21 |

| Weekly hours worked | 100 | 93.92 |

| Workers IHI (%) | |$7.8\%$| | |$10.17\%$| |

| Workers GHI (%) | |$63.8\%$| | |$65.7\%$| |

| Workers Medicaid (%) | |$8.8\%$| | |$5.8\%$| |

| Average IHI premium | 100 | 90.11 |

| Average GHI premium | 100 | 90.30 |

| Interest rate |$(r\text{ in $\%$})$| | 5.9 | 6.16 |

| Wage rate (w) | 100.00 | 98.48 |

| Gini (net income) | 0.352 | 0.320 |

| Gini (OOP health expenditure) | 0.548 | 0.543 |

| Suits index (income tax) | 0.122 | 0.218 |

| Tax progressivity (τ) | 0.053 | 0.113 |

| Scaling parameter (λ) | 1.017 | 1.277 |