Abstract

Received wisdom suggests that most exporters sell most of their output domestically. We show, however, that the distribution of export intensity varies substantially across countries and is often bimodal, displaying “twin peaks”—that is, large shares of both low- and high-intensity exporters coexisting alongside each other within a country. We reconcile this new stylized fact with an otherwise standard model of trade in which firms face firm-destination-specific revenue shifters that follow a lognormal distribution with sufficiently high dispersion. We structurally estimate the model and show that differences in countries’ size relative to the rest of the world can account for most of the observed cross-country variation in the distribution of export intensity in our data. While policies that incentivize firms to export a high share of their output account for a substantial share of the variation in the dispersion of firm-destination revenue shifters, they cannot fully account for the widespread prevalence of twin peaks around the world.

A set of Teaching Slides to accompany this article are available online as Supplementary Data.

1. Introduction

Received wisdom suggests that the majority of exporters in a country sell most of their output domestically, while only a very small minority of them concentrate their sales abroad (Bernard et al. 2003; Brooks 2006; Arkolakis 2010; Eaton, Kortum, and Kramarz 2011). In this paper, we show that this perception—based primarily on data from large and developed economies—fails to characterize the distribution of export intensity, the share of a firm’s revenues accounted for by exports (conditional on exporting) in small or developing countries.

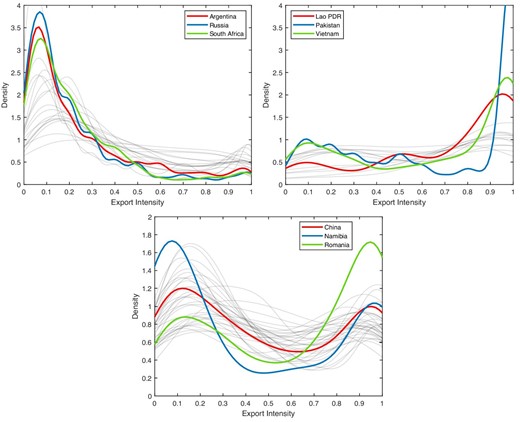

Our first contribution is to show that export intensity distributions vary tremendously across countries and—crucially—that rather than being an oddity, distributions featuring twin peaks are quite common across the world. This is vividly illustrated in Figure 1. Countries like Argentina, Russia, and South Africa, shown in the uppermost panel of the figure, exhibit the same pattern identified in previous studies: Firms with an export intensity below 0.2 constitute more than half of exporters, while firms with an export intensity above 0.8 account for less than 10% of exporters. In Lao PDR, Pakistan, and Vietnam, we observe the opposite pattern—the share of exporters with an intensity below 0.2 and above 0.8 is, on average, 16% and 54%, respectively. A large number of countries—as many as 47 out of the 72 in our data—and as diverse as China, Namibia, and Romania, instead exhibit “twin peaks”, that is, a high concentration of firms on both ends of the export intensity distribution.

Export Intensity Distribution across countries and selected examples. The figure depicts the kernel density of export intensity, or the share of total sales accounted for by exports among exporters, for each country in our data (in light gray lines) with selected examples (in bold colored lines). The data comes from several waves of the World Bank Enterprise Survey and are described in detail in Section 3. Countries are partitioned in three groups based on the value of the Hartigan and Hartigan (1985) dip test of unimodality presented in Figure 5 below. The countries included in each panel of the figure are listed in Appendix D.

In previous work, Lu (2010) and Defever and Riaño (2017a) documented the marked bimodality of the distribution of export intensity in China. We now show that twin peaks in the distribution of export intensity are not a phenomenon specific to China. In so doing, we contribute to the literature pioneered by Bernard and Jensen (1995), Roberts and Tybout (1996), and Bernard and Jensen (1999) that uncovered the key stylized facts characterizing the behavior of exporters and spurred the heterogeneous firm revolution in international trade.1

Using harmonized firm-level data for 72 (mostly developing and transition) countries drawn from the World Bank Enterprise Surveys (WBESs), we show that bimodality remains a salient feature of the distribution of export intensity regardless of how we slice our data. Since we observe a significant share of low-intensity exporters in most countries, twin peaks arise where large numbers of high-intensity exporters operate as well. We find that these are more likely to be foreign-owned, engaged in assembly and processing activities; they are also more prevalent in certain sectors (e.g. textiles and clothing), in less developed countries; and where subsidies subject to export share requirements (ESRs) are available. While these results are consistent with the existing empirical evidence available (see e.g. Díaz de Astarloa et al. 2013; Antràs and Yeaple 2014; Dai, Maitra, and Yu 2016; Manova and Yu 2016; Defever and Riaño 2017a), they do not fully account for the high prevalence of twin peaks we observe across the world. As a case in point, even when we exclude firms that export all their output, we find that one-third of the countries in our data still have bimodal export intensity distributions. Export intensity distributions are also bimodal within industries, at the bilateral level (in the limited number of cases for which we observe firms’ exports to specific destinations), and when we consider datasets other than WBESs.

Our second contribution is to show that a simple model with isoelastic demand à la Melitz (2003) can naturally generate twin peaks and account for the observed variation in the distribution of export intensity across countries quite successfully. The key assumption we require is heterogeneity at the firm-destination-level, rather than just at the firm level, as it is the case in most workhorse models of trade with heterogeneous firms.2 A large body of empirical work has shown that firm-destination-specific factors account for a substantial share of the variation of firm-level exports (e.g. Kee and Krishna 2008; Crozet, Head, and Mayer 2012; Lawless and Whelan 2014; Munch and Nguyen 2014; Bas, Mayer, and Thoenig 2017). Heterogeneity at the firm-destination-level can be due to multiple causes such as cross-country differences in tastes (Crozet, Head, and Mayer 2012), differences in the quality necessary to sell products in a given market (Brooks 2006; Verhoogen 2008), firms’ participation in global value chains (Antràs and de Gortari 2020) or distortions such as privileged access to export markets (Khandelwal, Schott, and Wei 2014), fiscal incentives offered in special economic zones (SEZs) only to high-intensity exporters (Defever and Riaño 2017a; Defever et al. 2019), and export subsidies granted to firms selling only in specific foreign markets (Defever et al. 2020), just to mention a few.

Treating the firm-destination-specific revenue shifters that generate this heterogeneity in our model as random variables following lognormal distributions, we derive a closed-form expression for the probability density function (pdf) of export intensity. We show that this distribution is bimodal when the sum of the variances of domestic and export revenue shifters is sufficiently high. The modes are located near 0 and 1, and their “height” is determined by a country’s relative market size with respect to the rest of the world: that is, in relatively large countries, most exporters operate with a low export intensity, while in small countries, the majority of exporters tend to be high-intensity ones; in countries of intermediate size, the distribution of export intensity exhibits twin peaks instead—just as Figure 1 shows.3

We estimate the structural parameters that govern the distribution of export intensity of each country—the sum of the variances of revenue shifters (the shape parameter) and relative market size (the scale parameter)—using the WBES data. To do so, we first show that there is a one-to-one relationship that is independent of the shape parameter between a country’s median export intensity and its relative market size vis-à-vis the rest of the world. This allows us to tease out the latter directly from the data without having to solve for the full general equilibrium of the model.4 Conditional on relative market size, we then estimate the shape parameter by maximum likelihood. The identification of this parameter is very transparent: If the conditions for twin peaks are satisfied, then greater dispersion of revenue shifters increases the distribution’s mass in the boundaries of the support. Conversely, if dispersion is low, then the distribution of export intensity is unimodal, and its mass is tightly concentrated around the median in the interior of the support.

The estimates of the shape and scale parameters reveal that the conditions for bimodality are satisfied for all countries in our data. How can we reconcile this result with the fact that statistical tests indicate that one-third of the countries in our data have unimodal distributions? To investigate this, we pool all our data across countries and estimate a single-shape-parameter model in which firms from all countries draw their domestic and export revenue shifters from distributions with the same shape parameter. Doing so implies that all cross-country variation in the distribution of export intensity is due to differences in relative size. The results we obtain are remarkable. Our model not only accounts for most of the variation in the distribution of export intensity we observe across the world, but can also explain the “discrepancy” we outlined above—relatively small and large countries have distributions that “look” unimodal—in the sense that a statistical test does not reject unimodality—while countries of intermediate size display prominent twin peaks.

We leverage the single-shape-parameter model and estimate it across several subsets of observations (various types of exporters, industries, and countries) with two objectives: to determine whether the conditions for bimodality are met for each subsample, and to gauge the contribution of each group to the magnitude of the overall dispersion of revenue shifters. Our results reveal that observable characteristics that are associated with higher firm-level export intensity, such as foreign ownership, participation in export processing, and having been an exporter for a long time, among others, account—individually—for between 7% and 25% of the overall variance of revenue shifters, depending on the specification. Excluding firms that export all their output altogether reduces the variance of revenue shifters by 42%. Crucially, however, even under these stringent conditions, the level of dispersion we estimate is still sufficiently high to generate twin peaks. Thus, our results show that policies that incentivize firms to export a high share of their output, which have been shown to have the potential to be highly distortive by Defever and Riaño (2017a) and Brooks and Wang (2016), account for a substantial share of the dispersion of revenue shifters. Nevertheless, these cannot fully account for the ubiquity of export intensity distributions characterized by twin peaks that we observe across the world.

Ours is not the first paper to incorporate sources of heterogeneity in addition to productivity to a model of international trade with heterogeneous firms. Among these, our paper is most closely related to state-of-the-art quantitative models of exports at the firm-level, such as Eaton, Kortum, and Kramarz (2011) and Fernandes et al. (2018), which also feature lognomal-distributed firm-destination-specific revenue shifters. We differ from Eaton, Kortum, and Kramarz (2011) and Fernandes et al. (2018) in two key respects, however: the dimensions of the data we aim to explain and the use we give to our quantitative model. While Eaton, Kortum, and Kramarz (2011) seek to reproduce the variation in French firms’ sales across markets and Fernandes et al. (2018) focus on the intensive margin of exports, we are interested instead in explaining the differences in the distribution of export intensity across countries. In a similar vein, we utilize our model to investigate what are the observable characteristics that account for the high dispersion in firms’ sales across markets and that in turn generate twin peaks, while Eaton, Kortum, and Kramarz and Fernandes et al. focus on quantifying the effect of a reduction in trade costs on welfare. Our finding that a high dispersion of exporters’ sales across markets allows us to explain why export intensity distributions differ so much around the world is similar in spirit to the results of Armenter and Koren (2015). They show that the Melitz (2003) model requires a substantial amount of size-independent heterogeneity to reproduce simultaneously the share of exporters and their size premium observed in US data.

The rest of the paper is organized as follows. Section 2 discusses why it is important to understand the export intensity distribution and model it accurately. Section 3 presents the data used in the paper, documents the prevalence of twin peaks in the distribution of export intensity across countries and different subsamples, reports statistical tests of unimodality and contrasts the distributions generated by the WBES data to those obtained from more representative datasets. Section 4 presents our theoretical framework. In it, we derive a closed-form expression for the pdf of export intensity and characterize the conditions under which the distribution of export intensity is bimodal. Section 5 presents our identification strategy and the estimates from our structural model. With our estimates at hand, we explore the relationship between twin peaks and relative market size and gauge the contribution of different factors to the prevalence of bimodality across countries. Section 6 concludes.

2. Why is the Export Intensity Distribution Important?

Export intensity measures the relative importance of foreign sales for a firm. For this reason, the mean export intensity has been used extensively in models of trade with heterogeneous firms to pin down the magnitude of costs that impede international flows of goods. Notable examples include Melitz and Redding (2015) and Head, Mayer, and Thoenig (2014) in models with two symmetric countries, Eaton, Kortum, and Kramarz (2011) in a multi-country environment and Atkeson and Burstein (2010) and Alessandria and Choi (2014) in dynamic models.

A common feature of these models is that the variable cost associated with exporting is the same for all firms selling to a given destination. Several policies that distort the relative incentives to export vis-à-vis selling domestically are firm-specific, however. Some prominent examples include the allocation of export quota rights (Khandelwal, Schott, and Wei 2014) and the provision of subsidies targeted at specific subsets of firms, for example, according to their location or foreign ownership status (Farole and Akinci 2011), whether they export the majority of their output or sell it in specific markets (Defever and Riaño 2017a; Defever et al. 2019, 2020), or if they produce goods considered to be of “‘strategic importance” (Westphal 1990; Kalouptsidi 2018). The common theme across these different policies is that they distort the incentives to export relative to selling domestically differently across firms.

In order to quantify the impact of these policies on aggregate outcomes such as productivity and welfare, it is therefore necessary to infer what the distribution of export intensity would have been in the absence of distortions. The idea is analogous to the approach pioneered by Guner, Ventura, and Yi (2008), Restuccia and Rogerson (2008), and Hsieh and Klenow (2009) to measure the consequences of the mis-allocation of resources across firms. Defever and Riaño (2017a) provide one example of this approach. They study how a tax deduction granted to firms exporting more than 70% of their output affects aggregate welfare in China. They show that this policy distorts the export intensity distribution by inducing a subset of firms to export a larger share of their output than they would otherwise do. The welfare cost is increasing in the difference between the observed distribution of export intensity and the counterfactual distribution that would have arisen had the policy not been in place. The welfare cost of a given subsidy is larger in a country that is relatively large with respect to the rest of the world like China—where the majority of exporters would have naturally operated at a low export intensity—than in a smaller country like Sri Lanka or Vietnam, where export requirement would not be binding for most firms and making subsidies subject to these less distortive. Defever and Riaño construct the undistorted counterfactual distribution by combining the export intensity distributions of large developing countries that do not provide subsidies subject to ESRs. Alternatively, Brooks and Wang (2016) use a two-country Melitz (2003) model, which predicts a degenerate export intensity distribution as their starting point, and interpret any differences across firms as wedges in the efficient allocation of sales across markets. In this context, they then show that the variance of the ratio of export to domestic sales is a sufficient statistic for welfare when wedges follow a lognormal distribution.

Recent research has shown that firms’ response to external shocks—most notably to real exchange rate (RER) depreciations—is substantially heterogeneous across the distribution of export intensity. Alfaro et al. (2017) find that while firms in East Asia increase their productivity, experience faster growth in sales and invest more in R&D following an RER depreciation, firms in Latin America respond in the diametrically opposite way, and firms in industrialized countries do not exhibit any significant change. They show that this heterogeneous response is due to the fact that firms in Latin America are substantially less export-intensive than firms in East Asia—a pattern that we also observe in our data and that our model can readily reproduce (see Figure 8 below). RER depreciations increase firms’ demand the most when firms have a high export intensity, and in so doing, also help to relax financial constraints, allowing firms to overcome the fixed costs involved in R&D investment. Closely related, Kohn, Leibovici, and Szkup (2020) show that the response of aggregate exports to large RER depreciations is fundamentally shaped by the distribution of export intensity when firms rely on foreign currency borrowing to finance their investment. Under these circumstances, a large RER depreciation increases a firm’s demand for exports, while simultaneously raising its borrowing costs and tightening financial constraints. In an economy in which the majority of exporters have low export intensity, firms can expand their exports much faster in response to a depreciation because they can reallocate their sales from the domestic to the export market without having to expand their capital stock. This margin of adjustment, on the other hand, is dampened in countries where high-intensity exporters are more prevalent.

The shape of the export intensity distribution also affects the sales diversification benefits that firms achieve from exporting. When firms are buffeted by idiosyncratic demand shocks across markets, selling both domestically and abroad reduces the volatility of the growth rate of their sales (Riaño 2011; Vannoorenberghe 2012). In Defever and Riaño (2017b), we show that there is a U-shaped relationship between the volatility of a firm’s sales growth and its export intensity. This implies that when a country’s export intensity distribution exhibits twin peaks, the volatility-dampening benefits of exporting are significantly reduced because most exporters have intensities either near 0 or 1.

3. Data and Stylized Fact

3.1. Data Description

Our data comes from several waves of the WBESs spanning the period 2002–2016. These surveys are carried out by the World Bank’s Enterprise Analysis Unit using a uniform methodology and core questionnaire and are designed to be representative of a country’s non-agricultural private economy.5 The unit of observation is the establishment, that is, a physical location where business is carried out or industrial operations take place, which should have its own management and control over its own workforce. Since the vast majority of establishments surveyed report to be single-establishment firms, hereafter we refer to them as “firms”. We use data for the manufacturing sector only—that is, firms that belong to ISIC Rev. 3.1 sectors 15–37.

The WBES provides information on firms’ main sector of operation, age, total sales, export intensity, ownership status (whether the firm is domestic or foreign-owned), labor productivity, and the share of material inputs accounted for by imports. Some survey waves provide information on the first year a firm began exporting, the number of products it produces (at the 4-digit ISIC industry level) and bilateral export sales to specific destinations. Export intensity—our key variable of interest—is defined as the share of sales that a firm exports directly or indirectly through an intermediary in a fiscal year and therefore takes values in the interval (0,1].6

Table 1 provides information on the number of exporters and the number of WBES survey waves per country. Our sample consists of 72 developing and transition countries (with the exception of Ireland and Sweden), for which we observe at least 97 exporting firms when we pool the data across all available survey waves.7 In terms of geographic coverage, the countries in our data are evenly distributed across Eastern Europe, Latin America and the Caribbean, Asia, and the Middle East and Africa; Ireland and Sweden are the only two countries from Western Europe. Table 1 also indicates whether a country provides subsidies subject to ESRs—incentives directly conditioned on firms’ export intensity. Examples of these incentives, which are most frequently used in SEZs and duty-drawback regimes, include cash transfers, tax holidays and deductions, and the provision of utilities at below-market rates (Defever and Riaño 2017a; Defever et al. 2019).8 Table 1 shows that half the countries in our data offer this class of subsidies.

Sample composition.

| Country | Code | Survey waves | # Exporters | ESR | Country | Code | Survey waves | # Exporters | ESR | |

|---|---|---|---|---|---|---|---|---|---|---|

| Albania | ALB | 2002, 05, 07, 13 | 116 | No | Lithuania | LTU | 2002, 04, 05, 09, 13 | 258 | No | |

| Argentina | ARG | 2006, 10 | 1,140 | No | Madagascar | MDG | 2005, 09, 13 | 256 | Yes | |

| Armenia | ARM | 2002, 05, 09, 13 | 170 | No | Malaysia | MYS | 2002, 15 | 735 | Yes | |

| Bangladesh | BGD | 2002, 07, 13 | 1,255 | Yes | Mauritius | MUS | 2005, 09 | 183 | No | |

| Belarus | BLR | 2002, 05, 08, 13 | 146 | Yes | Mexico | MEX | 2006, 10 | 727 | No | |

| Bolivia | BOL | 2006, 10 | 242 | No | Moldova | MDA | 2002, 03, 05, 09, 13 | 221 | No | |

| Bosnia-Herzegovina | BIH | 2002, 05, 09, 13 | 200 | Yes | Morocco | MAR | 2004, 13 | 585 | Yes | |

| Brazil | BRA | 2003, 09 | 832 | Yes | Namibia | NAM | 2006, 14 | 109 | Yes | |

| Bulgaria | BGR | 2002, 04, 05, 07, 09, 13 | 538 | No | Nicaragua | NIC | 2003, 06, 10 | 283 | Yes | |

| Chile | CHL | 2004, 06, 10 | 1,001 | No | Nigeria | NGA | 2007, 14 | 316 | Yes | |

| China | CHN | 2002, 03, 12 | 1,439 | Yes | Pakistan | PAK | 2002, 07, 13 | 534 | Yes | |

| Colombia | COL | 2006, 10 | 703 | No | Panama | PAN | 2006, 10 | 134 | No | |

| Costa Rica | CRI | 2005, 10 | 238 | Yes | Paraguay | PRY | 2006, 10 | 246 | Yes | |

| Croatia | HRV | 2002, 05, 07, 13 | 335 | No | Peru | PER | 2006, 10 | 701 | Yes | |

| Czech Republic | CZE | 2002, 05, 09, 13 | 232 | No | Philippines | PHL | 2003, 09, 15 | 914 | Yes | |

| Ecuador | ECU | 2003, 06, 10 | 385 | No | Poland | POL | 2002, 03, 05, 09, 13 | 439 | No | |

| Egypt | EGY | 2004, 13 | 676 | Yes | Romania | ROU | 2002, 05, 09, 13 | 290 | No | |

| El Salvador | SLV | 2003, 06, 10, 16 | 840 | No | Russian Fed. | RUS | 2002, 05, 09, 12 | 468 | No | |

| Estonia | EST | 2002, 05, 09, 13 | 175 | No | Senegal | SEN | 2003, 07, 14 | 148 | Yes | |

| Ethiophia | ETH | 2002, 11, 15 | 118 | Yes | Serbia | SRB | 2002, 03, 05, 09, 13 | 330 | No | |

| FYR Macedonia | MKD | 2002, 05, 09, 13 | 191 | No | Slovak Republic | SVK | 2002, 05, 09, 13 | 164 | No | |

| Ghana | GHA | 2007, 13 | 159 | Yes | Slovenia | SVN | 2002, 05, 09, 13 | 245 | No | |

| Guatemala | GTM | 2003, 06, 10 | 580 | Yes | South Africa | ZAF | 2003, 07 | 558 | No | |

| Honduras | HND | 2003, 06, 10 | 345 | Yes | Sri Lanka | LKA | 2004, 11 | 403 | Yes | |

| Hungary | HUN | 2002, 05, 09, 13 | 300 | No | Sweden | SWE | 2014 | 286 | No | |

| India | IND | 2002, 06, 14 | 2,212 | Yes | Syrian Arab Republic | SYR | 2003 | 251 | No | |

| Indonesia | IDN | 2003, 09, 15 | 720 | Yes | Tanzania | TZA | 2003, 06, 13 | 222 | Yes | |

| Ireland | IRL | 2005 | 97 | No | Thailand | THA | 2004, 16 | 1,066 | Yes | |

| Jordan | JOR | 2006, 13 | 377 | No | Tunisia | TUN | 2013 | 213 | Yes | |

| Kazakhstan | KAZ | 2002, 05, 09, 13 | 116 | No | Turkey | TUR | 2002, 04, 05, 08, 13 | 2,152 | Yes | |

| Kenya | KEN | 2003, 07, 13 | 511 | No | Uganda | UGA | 2003, 06, 13 | 221 | Yes | |

| Korea, Republic | KOR | 2005 | 99 | No | Ukraine | UKR | 2002, 05, 08, 13 | 435 | No | |

| Kyrgyz Republic | KGZ | 2002, 03, 05, 09, 13 | 126 | No | Uruguay | URY | 2006, 10 | 467 | No | |

| Lao PDR | LAO | 2006, 12, 16 | 128 | No | Uzbekistan | UZB | 2002, 03, 05, 08, 13 | 112 | Yes | |

| Latvia | LVA | 2002, 05, 09, 13 | 161 | No | Vietnam | VNM | 2005, 09, 15 | 1,251 | Yes | |

| Lebanon | LBN | 2006, 13 | 252 | No | Zambia | ZMB | 2002, 07, 13 | 146 | Yes |

| Country | Code | Survey waves | # Exporters | ESR | Country | Code | Survey waves | # Exporters | ESR | |

|---|---|---|---|---|---|---|---|---|---|---|

| Albania | ALB | 2002, 05, 07, 13 | 116 | No | Lithuania | LTU | 2002, 04, 05, 09, 13 | 258 | No | |

| Argentina | ARG | 2006, 10 | 1,140 | No | Madagascar | MDG | 2005, 09, 13 | 256 | Yes | |

| Armenia | ARM | 2002, 05, 09, 13 | 170 | No | Malaysia | MYS | 2002, 15 | 735 | Yes | |

| Bangladesh | BGD | 2002, 07, 13 | 1,255 | Yes | Mauritius | MUS | 2005, 09 | 183 | No | |

| Belarus | BLR | 2002, 05, 08, 13 | 146 | Yes | Mexico | MEX | 2006, 10 | 727 | No | |

| Bolivia | BOL | 2006, 10 | 242 | No | Moldova | MDA | 2002, 03, 05, 09, 13 | 221 | No | |

| Bosnia-Herzegovina | BIH | 2002, 05, 09, 13 | 200 | Yes | Morocco | MAR | 2004, 13 | 585 | Yes | |

| Brazil | BRA | 2003, 09 | 832 | Yes | Namibia | NAM | 2006, 14 | 109 | Yes | |

| Bulgaria | BGR | 2002, 04, 05, 07, 09, 13 | 538 | No | Nicaragua | NIC | 2003, 06, 10 | 283 | Yes | |

| Chile | CHL | 2004, 06, 10 | 1,001 | No | Nigeria | NGA | 2007, 14 | 316 | Yes | |

| China | CHN | 2002, 03, 12 | 1,439 | Yes | Pakistan | PAK | 2002, 07, 13 | 534 | Yes | |

| Colombia | COL | 2006, 10 | 703 | No | Panama | PAN | 2006, 10 | 134 | No | |

| Costa Rica | CRI | 2005, 10 | 238 | Yes | Paraguay | PRY | 2006, 10 | 246 | Yes | |

| Croatia | HRV | 2002, 05, 07, 13 | 335 | No | Peru | PER | 2006, 10 | 701 | Yes | |

| Czech Republic | CZE | 2002, 05, 09, 13 | 232 | No | Philippines | PHL | 2003, 09, 15 | 914 | Yes | |

| Ecuador | ECU | 2003, 06, 10 | 385 | No | Poland | POL | 2002, 03, 05, 09, 13 | 439 | No | |

| Egypt | EGY | 2004, 13 | 676 | Yes | Romania | ROU | 2002, 05, 09, 13 | 290 | No | |

| El Salvador | SLV | 2003, 06, 10, 16 | 840 | No | Russian Fed. | RUS | 2002, 05, 09, 12 | 468 | No | |

| Estonia | EST | 2002, 05, 09, 13 | 175 | No | Senegal | SEN | 2003, 07, 14 | 148 | Yes | |

| Ethiophia | ETH | 2002, 11, 15 | 118 | Yes | Serbia | SRB | 2002, 03, 05, 09, 13 | 330 | No | |

| FYR Macedonia | MKD | 2002, 05, 09, 13 | 191 | No | Slovak Republic | SVK | 2002, 05, 09, 13 | 164 | No | |

| Ghana | GHA | 2007, 13 | 159 | Yes | Slovenia | SVN | 2002, 05, 09, 13 | 245 | No | |

| Guatemala | GTM | 2003, 06, 10 | 580 | Yes | South Africa | ZAF | 2003, 07 | 558 | No | |

| Honduras | HND | 2003, 06, 10 | 345 | Yes | Sri Lanka | LKA | 2004, 11 | 403 | Yes | |

| Hungary | HUN | 2002, 05, 09, 13 | 300 | No | Sweden | SWE | 2014 | 286 | No | |

| India | IND | 2002, 06, 14 | 2,212 | Yes | Syrian Arab Republic | SYR | 2003 | 251 | No | |

| Indonesia | IDN | 2003, 09, 15 | 720 | Yes | Tanzania | TZA | 2003, 06, 13 | 222 | Yes | |

| Ireland | IRL | 2005 | 97 | No | Thailand | THA | 2004, 16 | 1,066 | Yes | |

| Jordan | JOR | 2006, 13 | 377 | No | Tunisia | TUN | 2013 | 213 | Yes | |

| Kazakhstan | KAZ | 2002, 05, 09, 13 | 116 | No | Turkey | TUR | 2002, 04, 05, 08, 13 | 2,152 | Yes | |

| Kenya | KEN | 2003, 07, 13 | 511 | No | Uganda | UGA | 2003, 06, 13 | 221 | Yes | |

| Korea, Republic | KOR | 2005 | 99 | No | Ukraine | UKR | 2002, 05, 08, 13 | 435 | No | |

| Kyrgyz Republic | KGZ | 2002, 03, 05, 09, 13 | 126 | No | Uruguay | URY | 2006, 10 | 467 | No | |

| Lao PDR | LAO | 2006, 12, 16 | 128 | No | Uzbekistan | UZB | 2002, 03, 05, 08, 13 | 112 | Yes | |

| Latvia | LVA | 2002, 05, 09, 13 | 161 | No | Vietnam | VNM | 2005, 09, 15 | 1,251 | Yes | |

| Lebanon | LBN | 2006, 13 | 252 | No | Zambia | ZMB | 2002, 07, 13 | 146 | Yes |

Sample composition.

| Country | Code | Survey waves | # Exporters | ESR | Country | Code | Survey waves | # Exporters | ESR | |

|---|---|---|---|---|---|---|---|---|---|---|

| Albania | ALB | 2002, 05, 07, 13 | 116 | No | Lithuania | LTU | 2002, 04, 05, 09, 13 | 258 | No | |

| Argentina | ARG | 2006, 10 | 1,140 | No | Madagascar | MDG | 2005, 09, 13 | 256 | Yes | |

| Armenia | ARM | 2002, 05, 09, 13 | 170 | No | Malaysia | MYS | 2002, 15 | 735 | Yes | |

| Bangladesh | BGD | 2002, 07, 13 | 1,255 | Yes | Mauritius | MUS | 2005, 09 | 183 | No | |

| Belarus | BLR | 2002, 05, 08, 13 | 146 | Yes | Mexico | MEX | 2006, 10 | 727 | No | |

| Bolivia | BOL | 2006, 10 | 242 | No | Moldova | MDA | 2002, 03, 05, 09, 13 | 221 | No | |

| Bosnia-Herzegovina | BIH | 2002, 05, 09, 13 | 200 | Yes | Morocco | MAR | 2004, 13 | 585 | Yes | |

| Brazil | BRA | 2003, 09 | 832 | Yes | Namibia | NAM | 2006, 14 | 109 | Yes | |

| Bulgaria | BGR | 2002, 04, 05, 07, 09, 13 | 538 | No | Nicaragua | NIC | 2003, 06, 10 | 283 | Yes | |

| Chile | CHL | 2004, 06, 10 | 1,001 | No | Nigeria | NGA | 2007, 14 | 316 | Yes | |

| China | CHN | 2002, 03, 12 | 1,439 | Yes | Pakistan | PAK | 2002, 07, 13 | 534 | Yes | |

| Colombia | COL | 2006, 10 | 703 | No | Panama | PAN | 2006, 10 | 134 | No | |

| Costa Rica | CRI | 2005, 10 | 238 | Yes | Paraguay | PRY | 2006, 10 | 246 | Yes | |

| Croatia | HRV | 2002, 05, 07, 13 | 335 | No | Peru | PER | 2006, 10 | 701 | Yes | |

| Czech Republic | CZE | 2002, 05, 09, 13 | 232 | No | Philippines | PHL | 2003, 09, 15 | 914 | Yes | |

| Ecuador | ECU | 2003, 06, 10 | 385 | No | Poland | POL | 2002, 03, 05, 09, 13 | 439 | No | |

| Egypt | EGY | 2004, 13 | 676 | Yes | Romania | ROU | 2002, 05, 09, 13 | 290 | No | |

| El Salvador | SLV | 2003, 06, 10, 16 | 840 | No | Russian Fed. | RUS | 2002, 05, 09, 12 | 468 | No | |

| Estonia | EST | 2002, 05, 09, 13 | 175 | No | Senegal | SEN | 2003, 07, 14 | 148 | Yes | |

| Ethiophia | ETH | 2002, 11, 15 | 118 | Yes | Serbia | SRB | 2002, 03, 05, 09, 13 | 330 | No | |

| FYR Macedonia | MKD | 2002, 05, 09, 13 | 191 | No | Slovak Republic | SVK | 2002, 05, 09, 13 | 164 | No | |

| Ghana | GHA | 2007, 13 | 159 | Yes | Slovenia | SVN | 2002, 05, 09, 13 | 245 | No | |

| Guatemala | GTM | 2003, 06, 10 | 580 | Yes | South Africa | ZAF | 2003, 07 | 558 | No | |

| Honduras | HND | 2003, 06, 10 | 345 | Yes | Sri Lanka | LKA | 2004, 11 | 403 | Yes | |

| Hungary | HUN | 2002, 05, 09, 13 | 300 | No | Sweden | SWE | 2014 | 286 | No | |

| India | IND | 2002, 06, 14 | 2,212 | Yes | Syrian Arab Republic | SYR | 2003 | 251 | No | |

| Indonesia | IDN | 2003, 09, 15 | 720 | Yes | Tanzania | TZA | 2003, 06, 13 | 222 | Yes | |

| Ireland | IRL | 2005 | 97 | No | Thailand | THA | 2004, 16 | 1,066 | Yes | |

| Jordan | JOR | 2006, 13 | 377 | No | Tunisia | TUN | 2013 | 213 | Yes | |

| Kazakhstan | KAZ | 2002, 05, 09, 13 | 116 | No | Turkey | TUR | 2002, 04, 05, 08, 13 | 2,152 | Yes | |

| Kenya | KEN | 2003, 07, 13 | 511 | No | Uganda | UGA | 2003, 06, 13 | 221 | Yes | |

| Korea, Republic | KOR | 2005 | 99 | No | Ukraine | UKR | 2002, 05, 08, 13 | 435 | No | |

| Kyrgyz Republic | KGZ | 2002, 03, 05, 09, 13 | 126 | No | Uruguay | URY | 2006, 10 | 467 | No | |

| Lao PDR | LAO | 2006, 12, 16 | 128 | No | Uzbekistan | UZB | 2002, 03, 05, 08, 13 | 112 | Yes | |

| Latvia | LVA | 2002, 05, 09, 13 | 161 | No | Vietnam | VNM | 2005, 09, 15 | 1,251 | Yes | |

| Lebanon | LBN | 2006, 13 | 252 | No | Zambia | ZMB | 2002, 07, 13 | 146 | Yes |

| Country | Code | Survey waves | # Exporters | ESR | Country | Code | Survey waves | # Exporters | ESR | |

|---|---|---|---|---|---|---|---|---|---|---|

| Albania | ALB | 2002, 05, 07, 13 | 116 | No | Lithuania | LTU | 2002, 04, 05, 09, 13 | 258 | No | |

| Argentina | ARG | 2006, 10 | 1,140 | No | Madagascar | MDG | 2005, 09, 13 | 256 | Yes | |

| Armenia | ARM | 2002, 05, 09, 13 | 170 | No | Malaysia | MYS | 2002, 15 | 735 | Yes | |

| Bangladesh | BGD | 2002, 07, 13 | 1,255 | Yes | Mauritius | MUS | 2005, 09 | 183 | No | |

| Belarus | BLR | 2002, 05, 08, 13 | 146 | Yes | Mexico | MEX | 2006, 10 | 727 | No | |

| Bolivia | BOL | 2006, 10 | 242 | No | Moldova | MDA | 2002, 03, 05, 09, 13 | 221 | No | |

| Bosnia-Herzegovina | BIH | 2002, 05, 09, 13 | 200 | Yes | Morocco | MAR | 2004, 13 | 585 | Yes | |

| Brazil | BRA | 2003, 09 | 832 | Yes | Namibia | NAM | 2006, 14 | 109 | Yes | |

| Bulgaria | BGR | 2002, 04, 05, 07, 09, 13 | 538 | No | Nicaragua | NIC | 2003, 06, 10 | 283 | Yes | |

| Chile | CHL | 2004, 06, 10 | 1,001 | No | Nigeria | NGA | 2007, 14 | 316 | Yes | |

| China | CHN | 2002, 03, 12 | 1,439 | Yes | Pakistan | PAK | 2002, 07, 13 | 534 | Yes | |

| Colombia | COL | 2006, 10 | 703 | No | Panama | PAN | 2006, 10 | 134 | No | |

| Costa Rica | CRI | 2005, 10 | 238 | Yes | Paraguay | PRY | 2006, 10 | 246 | Yes | |

| Croatia | HRV | 2002, 05, 07, 13 | 335 | No | Peru | PER | 2006, 10 | 701 | Yes | |

| Czech Republic | CZE | 2002, 05, 09, 13 | 232 | No | Philippines | PHL | 2003, 09, 15 | 914 | Yes | |

| Ecuador | ECU | 2003, 06, 10 | 385 | No | Poland | POL | 2002, 03, 05, 09, 13 | 439 | No | |

| Egypt | EGY | 2004, 13 | 676 | Yes | Romania | ROU | 2002, 05, 09, 13 | 290 | No | |

| El Salvador | SLV | 2003, 06, 10, 16 | 840 | No | Russian Fed. | RUS | 2002, 05, 09, 12 | 468 | No | |

| Estonia | EST | 2002, 05, 09, 13 | 175 | No | Senegal | SEN | 2003, 07, 14 | 148 | Yes | |

| Ethiophia | ETH | 2002, 11, 15 | 118 | Yes | Serbia | SRB | 2002, 03, 05, 09, 13 | 330 | No | |

| FYR Macedonia | MKD | 2002, 05, 09, 13 | 191 | No | Slovak Republic | SVK | 2002, 05, 09, 13 | 164 | No | |

| Ghana | GHA | 2007, 13 | 159 | Yes | Slovenia | SVN | 2002, 05, 09, 13 | 245 | No | |

| Guatemala | GTM | 2003, 06, 10 | 580 | Yes | South Africa | ZAF | 2003, 07 | 558 | No | |

| Honduras | HND | 2003, 06, 10 | 345 | Yes | Sri Lanka | LKA | 2004, 11 | 403 | Yes | |

| Hungary | HUN | 2002, 05, 09, 13 | 300 | No | Sweden | SWE | 2014 | 286 | No | |

| India | IND | 2002, 06, 14 | 2,212 | Yes | Syrian Arab Republic | SYR | 2003 | 251 | No | |

| Indonesia | IDN | 2003, 09, 15 | 720 | Yes | Tanzania | TZA | 2003, 06, 13 | 222 | Yes | |

| Ireland | IRL | 2005 | 97 | No | Thailand | THA | 2004, 16 | 1,066 | Yes | |

| Jordan | JOR | 2006, 13 | 377 | No | Tunisia | TUN | 2013 | 213 | Yes | |

| Kazakhstan | KAZ | 2002, 05, 09, 13 | 116 | No | Turkey | TUR | 2002, 04, 05, 08, 13 | 2,152 | Yes | |

| Kenya | KEN | 2003, 07, 13 | 511 | No | Uganda | UGA | 2003, 06, 13 | 221 | Yes | |

| Korea, Republic | KOR | 2005 | 99 | No | Ukraine | UKR | 2002, 05, 08, 13 | 435 | No | |

| Kyrgyz Republic | KGZ | 2002, 03, 05, 09, 13 | 126 | No | Uruguay | URY | 2006, 10 | 467 | No | |

| Lao PDR | LAO | 2006, 12, 16 | 128 | No | Uzbekistan | UZB | 2002, 03, 05, 08, 13 | 112 | Yes | |

| Latvia | LVA | 2002, 05, 09, 13 | 161 | No | Vietnam | VNM | 2005, 09, 15 | 1,251 | Yes | |

| Lebanon | LBN | 2006, 13 | 252 | No | Zambia | ZMB | 2002, 07, 13 | 146 | Yes |

Table 2 provides a first pass at the WBES data comparing exporters, across the distribution of export intensity, with domestic firms. Columns (1)–(3) provide information on firm size and productivity relative to the average value of the respective statistic in each country-survey year pair, while columns (4) and (5) report the percentage of foreign-owned firms and the use of imported inputs in each cell, respectively. Table 2 reveals that—consistent with the evidence summarized by Bernard et al. (2007) and Melitz and Redding (2014)—exporters are larger (both in terms of employment and output) and more productive than domestic firms. Looking across the export intensity distribution, we find that although there is a positive correlation between firm size and export intensity, there is not a clear relationship between labor productivity and export intensity.9 Columns (4) and (5) show that exporters—and high-intensity ones in particular—are more likely to be foreign-owned and to use imported intermediate inputs more intensively than domestic firms, consistent with the evidence documented by Antràs and Yeaple (2014) and Amiti and Konings (2007).

Firm characteristics by export status and export intensity.

| Employment | Output | Output per worker | % foreign-owned | % imported inputs | |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| Non-exporters | 0.5 | 0.5 | 0.8 | 6.0 | 23.7 |

| Exporters | |||||

| Export intensity: | |||||

| |$\; \; \in (0.0,0.2]$| | 1.7 | 2.1 | 1.4 | 17.4 | 37.7 |

| |$\; \; \in (0.2,0.4]$| | 1.5 | 1.8 | 1.3 | 18.8 | 35.6 |

| |$\; \; \in (0.4,0.6]$| | 1.7 | 1.9 | 1.3 | 21.0 | 35.2 |

| |$\; \; \in (0.6,0.8]$| | 2.3 | 2.3 | 1.4 | 23.0 | 35.4 |

| |$\; \; \in (0.8,1.0]$| | 2.2 | 2.3 | 1.6 | 31.1 | 41.0 |

| Employment | Output | Output per worker | % foreign-owned | % imported inputs | |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| Non-exporters | 0.5 | 0.5 | 0.8 | 6.0 | 23.7 |

| Exporters | |||||

| Export intensity: | |||||

| |$\; \; \in (0.0,0.2]$| | 1.7 | 2.1 | 1.4 | 17.4 | 37.7 |

| |$\; \; \in (0.2,0.4]$| | 1.5 | 1.8 | 1.3 | 18.8 | 35.6 |

| |$\; \; \in (0.4,0.6]$| | 1.7 | 1.9 | 1.3 | 21.0 | 35.2 |

| |$\; \; \in (0.6,0.8]$| | 2.3 | 2.3 | 1.4 | 23.0 | 35.4 |

| |$\; \; \in (0.8,1.0]$| | 2.2 | 2.3 | 1.6 | 31.1 | 41.0 |

Notes. Columns (1)–(3) report the average across countries of the relative size and labor productivity of exporters and domestic firms relative to the mean value of each variable calculated in each country-survey year cell. Thus, for instance, domestic firms across all countries in our sample are 50% smaller (in terms of employment) than the average firm, while exporters with an export intensity lower than 20% are 70% larger than the average firm. Column (4) reports the percentage of foreign-owned firms (firms with a share of foreign equity at least 10% or greater), and column (5) presents the percentage of imported inputs in total intermediate inputs in each export intensity bin.

Firm characteristics by export status and export intensity.

| Employment | Output | Output per worker | % foreign-owned | % imported inputs | |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| Non-exporters | 0.5 | 0.5 | 0.8 | 6.0 | 23.7 |

| Exporters | |||||

| Export intensity: | |||||

| |$\; \; \in (0.0,0.2]$| | 1.7 | 2.1 | 1.4 | 17.4 | 37.7 |

| |$\; \; \in (0.2,0.4]$| | 1.5 | 1.8 | 1.3 | 18.8 | 35.6 |

| |$\; \; \in (0.4,0.6]$| | 1.7 | 1.9 | 1.3 | 21.0 | 35.2 |

| |$\; \; \in (0.6,0.8]$| | 2.3 | 2.3 | 1.4 | 23.0 | 35.4 |

| |$\; \; \in (0.8,1.0]$| | 2.2 | 2.3 | 1.6 | 31.1 | 41.0 |

| Employment | Output | Output per worker | % foreign-owned | % imported inputs | |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| Non-exporters | 0.5 | 0.5 | 0.8 | 6.0 | 23.7 |

| Exporters | |||||

| Export intensity: | |||||

| |$\; \; \in (0.0,0.2]$| | 1.7 | 2.1 | 1.4 | 17.4 | 37.7 |

| |$\; \; \in (0.2,0.4]$| | 1.5 | 1.8 | 1.3 | 18.8 | 35.6 |

| |$\; \; \in (0.4,0.6]$| | 1.7 | 1.9 | 1.3 | 21.0 | 35.2 |

| |$\; \; \in (0.6,0.8]$| | 2.3 | 2.3 | 1.4 | 23.0 | 35.4 |

| |$\; \; \in (0.8,1.0]$| | 2.2 | 2.3 | 1.6 | 31.1 | 41.0 |

Notes. Columns (1)–(3) report the average across countries of the relative size and labor productivity of exporters and domestic firms relative to the mean value of each variable calculated in each country-survey year cell. Thus, for instance, domestic firms across all countries in our sample are 50% smaller (in terms of employment) than the average firm, while exporters with an export intensity lower than 20% are 70% larger than the average firm. Column (4) reports the percentage of foreign-owned firms (firms with a share of foreign equity at least 10% or greater), and column (5) presents the percentage of imported inputs in total intermediate inputs in each export intensity bin.

3.2. The Distribution of Export Intensity Across Countries

Figure 2 provides a bird’s eye view of the export intensity distribution across all countries in our data. In it we calculate the share of exporters across five export intensity bins in each country and present the distribution of these shares in each bin. Figure 2 shows that in the majority of countries, exporters concentrate in the first and last export intensity bins—that is, they either sell most of their output domestically or abroad—while the shares of exporters in the middle bins are substantially lower. The figure also shows that there is a high degree of heterogeneity across countries in terms of the share of high- and low-intensity exporters.

![Cross-country distribution of the share of exporters operating in different export intensity bins—all exporters. For each country in our data, we calculate the share of exporters operating across five export intensity bins ((0,0.2], (0.2,0.4], (0.4,0.6], (0.6,0.8], and (0.8,1]). The figure presents the main quantiles of the distribution of these shares across countries for each export intensity bin. The median is denoted by a circle; the top and bottom sides of each box denote, respectively, the 25th and 75th percentiles; the bottom and top of the “whiskers” (represented with dashed lines) indicate the minimum and maximum, respectively.](https://oup.silverchair-cdn.com/oup/backfile/Content_public/Journal/jeea/20/3/10.1093_jeea_jvac006/2/m_jvac006fig2.jpeg?Expires=1749047555&Signature=CpOtQGfeA7Co7XPTb~Pk4qTuHbsd7SsTp4HdhbqJtNFJlgDTTBCmGTtvF5iXByAp8n5nDODn8~3lkZg-clmqyukPj3QmQTmJbWWEPtCI4xreBB7yJ~p4o~NxmaJiCwuWzIXBWNazZ8vbP0~PDLLDAYZ5KufMoqII8WMm9qjgwP0N35N04HRW-g~HUc5qpRmRSESGGYdfmZ9ntTljBLjMSVfOs~QT6UxUpiqln9pOh5ZOCYHJkpMURFYzqkZttLL~cMI75Eb03RZVtp2YXBAvhTxOV1ermuxA9c6WvkMJjjmtzj4a~-5SP8gZQCK0zzUDGh0Q4yHn0ImuoeZJbm-j9w__&Key-Pair-Id=APKAIE5G5CRDK6RD3PGA)

Cross-country distribution of the share of exporters operating in different export intensity bins—all exporters. For each country in our data, we calculate the share of exporters operating across five export intensity bins ((0,0.2], (0.2,0.4], (0.4,0.6], (0.6,0.8], and (0.8,1]). The figure presents the main quantiles of the distribution of these shares across countries for each export intensity bin. The median is denoted by a circle; the top and bottom sides of each box denote, respectively, the 25th and 75th percentiles; the bottom and top of the “whiskers” (represented with dashed lines) indicate the minimum and maximum, respectively.

One plausible explanation for the existence of twin peaks in the export intensity distribution is that the distribution at the country level is a mixture of “standard” low-intensity exporters and a significant number of firms that export most of their output. We take advantage of the rich information available in WBESs to ascertain whether the twin peaks of the export intensity distribution are due to a composition effect driven by specific types of high-intensity exporters.

There are several factors that could potentially account for the prevalence of high-intensity exporters. For instance, Antràs and Yeaple (2014) document that foreign-owned affiliates are more export oriented than locally-owned firms in their respective host countries, while Ruhl and Willis (2017) find that exporters increase their export intensity gradually over time. Firms specialized in processing and assembly activities tend to exhibit high export intensities because they are required to export all goods that incorporate duty-free inputs (Dai, Maitra, and Yu 2016; Manova and Yu 2016). Lower wages in poorer countries also induce local exporters to specialize in more upstream stages of production, leading them to ship all their output downstream along global value chains, as Antràs and de Gortari (2020) show. Yet another possibility is a composition effect of the export intensity distributions of different industries, be it due to technology differences or comparative advantage (Brooks 2006; Bernard et al. 2007).

WBES identifies firms as being foreign-owned if the share of foreign equity is at least 10%. We classify firms as “processing exporters” if imports account for 90% or more of their expenditure on intermediate inputs, since WBES does not directly identify firms that rely on a processing customs regime to export. We denote “pure exporters” as those firms that export all their output. This group encompasses firms engaged in assembly activities or that belong to a global value chain (regardless of whether they are foreign-owned or not) as well as firms producing goods with no domestic demand, such as woolen sweaters sown in Bangladesh (Díaz de Astarloa et al. 2013). Single-product exporters are defined at the 4-digit ISIC industry level10 and “old” exporters are those with 10 years or more of exporting experience.11 The data on exports to specific destinations is available for a few countries, and the respective destinations considered vary according to the country of origin.12

Trade policy can also induce firms to export a high share of their output. Over the last three decades, developing countries have relied intensively on industrial policies aimed at fostering exports—most notably, the provision of generous fiscal incentives to firms located in SEZs (Rodrik 2004). Similarly, firms located in countries offering subsidies subject to ESRs—which as we have noted above, account for half of the countries in our sample—are only eligible to receive these if their export intensity exceeds a specified threshold (Defever and Riaño 2017a; Defever et al. 2019). Since developing countries tend to rely more intensively on distortive commercial policies than developed countries, as Goldberg and Pavcnik (2016) document, it is also plausible that twin peaks tend to arise mostly among the former. We are therefore interested in determining whether the shape of export intensity distributions is systematically related to a country’s level of development.

Figure 3 presents the share of exporters operating in each export intensity bin for the different subsets of exporters defined above and Figure 4 does the same across manufacturing sectors. The key message delivered by Figure 2 still holds regardless of how we slice the data: Most exporters operate at either a very low or very high export intensity—that is, they either sell less of 20% of their sales abroad, or they export more than 80% of them. Bimodality is a salient feature of the export intensity distribution—even within industries and for bilateral exports.13

![Cross-country distribution of the share of exporters operating in different export intensity bins across subsamples. For each country with more than 50 exporters in our data, we calculate the share of exporters operating across five export intensity bins ((0,0.2], (0.2,0.4], (0.4,0.6], (0.6,0.8], and (0.8,1]). The figure presents the main quantiles of the distribution of these shares across countries for each export intensity bin. The median is denoted by a circle, the top and bottom sides of each box denote, respectively, the 25th and 75th percentiles; the bottom and top of the “whiskers” (represented with dashed lines) indicate the minimum and maximum, respectively. The first panel in the first row excludes firms that are foreign-owned; the second excludes processing exporters and the third excludes firms with export intensity exactly equal to 1 (pure exporters). In the second row, the first panel excludes single-product exporters; the second excludes “old” exporters (firms that have exported for more than 10 years) and the third excludes observations from countries that offer subsidies subject to ESRs. In the third row, we present the distributions for OECD and non-OECD countries in the first two panels, respectively; the last panel presents the distribution based on the subsample of firms for which we observe their bilateral export intensity to selected destinations—that is, the share of total sales of firms in the origin country accounted for by exports sold only in the destination country.](https://oup.silverchair-cdn.com/oup/backfile/Content_public/Journal/jeea/20/3/10.1093_jeea_jvac006/2/m_jvac006fig3.jpeg?Expires=1749047555&Signature=46W4MOH9zuzuLUglHZftEkalVsPgSpHyj~qV9f2EvMmYhlbpuUPIXAwjD~cRM4c3OP~36GG9PvCrCNZjfsxO090PD-Xm75tYBlmcqw8jtYf5YVGp2aYpVgRoEqFbD9eXHOOKDfLESxs7wTuZ9mvttHX7XQz~5pyGaA53sSMIaU26o4W94Ni2jaiSihRTLsAXPCaxDhn4DnC-GHQN-qRrT6ANRGp~Phmnia~QQlnbH6l4prBwaugOSC6tHwFnC6O76OazjL18FcKcA7LUKsAdY~RAx83wifpnHPKdUsBMknEHdNXYRJj2tZ~tNk60MCDbl7nN80X7F3RrkhF~bvdoow__&Key-Pair-Id=APKAIE5G5CRDK6RD3PGA)

Cross-country distribution of the share of exporters operating in different export intensity bins across subsamples. For each country with more than 50 exporters in our data, we calculate the share of exporters operating across five export intensity bins ((0,0.2], (0.2,0.4], (0.4,0.6], (0.6,0.8], and (0.8,1]). The figure presents the main quantiles of the distribution of these shares across countries for each export intensity bin. The median is denoted by a circle, the top and bottom sides of each box denote, respectively, the 25th and 75th percentiles; the bottom and top of the “whiskers” (represented with dashed lines) indicate the minimum and maximum, respectively. The first panel in the first row excludes firms that are foreign-owned; the second excludes processing exporters and the third excludes firms with export intensity exactly equal to 1 (pure exporters). In the second row, the first panel excludes single-product exporters; the second excludes “old” exporters (firms that have exported for more than 10 years) and the third excludes observations from countries that offer subsidies subject to ESRs. In the third row, we present the distributions for OECD and non-OECD countries in the first two panels, respectively; the last panel presents the distribution based on the subsample of firms for which we observe their bilateral export intensity to selected destinations—that is, the share of total sales of firms in the origin country accounted for by exports sold only in the destination country.

![Cross-country distribution of the share of exporters operating in different export intensity bins across manufacturing sectors. For each country-sector pair with more than 50 exporters in our data, we calculate the share of exporters operating across five export intensity bins ((0,0.2], (0.2,0.4], (0.4,0.6], (0.6,0.8], and (0.8,1]). The figure presents the main quantiles of the distribution of these shares across countries for each export intensity bin for each manufacturing sector. The median is denoted by a circle, the top and bottom sides of each box denote, respectively, the 25th and 75th percentiles; the bottom and top of the “whiskers” (represented with dashed lines) indicate the minimum and maximum, respectively.](https://oup.silverchair-cdn.com/oup/backfile/Content_public/Journal/jeea/20/3/10.1093_jeea_jvac006/2/m_jvac006fig4.jpeg?Expires=1749047555&Signature=cEFA66ReSXBHzUiw2BtyS~uOCSqFc~MnKhCIYDY47Lbjvl33UpyaFwt6iBva9YlPK-XHXB~C22YCtLKjQJH5-GcVT64Z-XUgQQr1HmhpiWCtQrF-6zNOH0reLqgyxqbO7zvcNbDzHOl96oIYXHmjSEueb8m69MiFrMHWmqLJZ2Xn~KWrnoZX27ejwyPsPH2uCok1jFxqyaVRZKZrauo0-ZRLj2WT0hCR2VsYwDZE8SkXxbNmC2wBuFGP3AhYXonG84yrEGexy4xa~skGOYmazyR72E2gzuein~AWjiK5pX6HyOXUlodyDkzVwsxwLShIB5F4mGCOQ4VVLQXoaWWZKw__&Key-Pair-Id=APKAIE5G5CRDK6RD3PGA)

Cross-country distribution of the share of exporters operating in different export intensity bins across manufacturing sectors. For each country-sector pair with more than 50 exporters in our data, we calculate the share of exporters operating across five export intensity bins ((0,0.2], (0.2,0.4], (0.4,0.6], (0.6,0.8], and (0.8,1]). The figure presents the main quantiles of the distribution of these shares across countries for each export intensity bin for each manufacturing sector. The median is denoted by a circle, the top and bottom sides of each box denote, respectively, the 25th and 75th percentiles; the bottom and top of the “whiskers” (represented with dashed lines) indicate the minimum and maximum, respectively.

3.3. Test of Unimodality

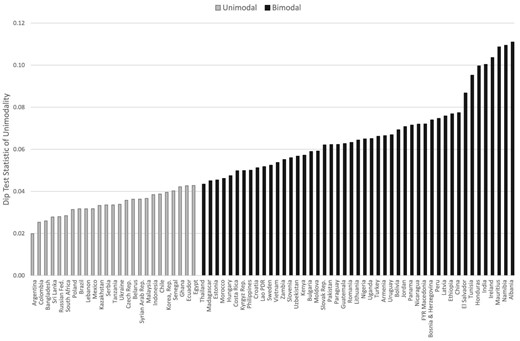

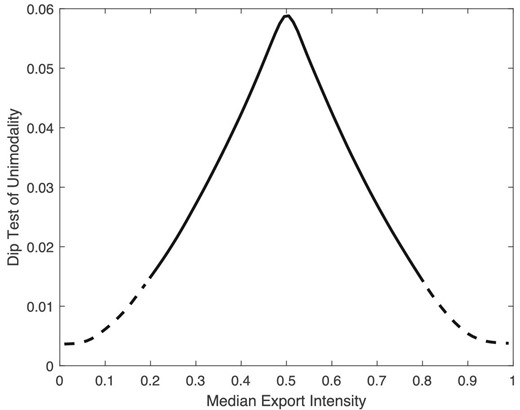

We now shift our focus to the distribution of export intensity within countries; more specifically, we seek to identify which countries have bimodal export intensity distributions and which ones do not. We use the dip test statistic proposed by Hartigan and Hartigan (1985) to do so.14 The dip statistic measures departures from unimodality in the empirical cumulative distribution function (cdf), by relying on the fact that a unimodal distribution has a unique inflection point.15 As Henderson, Parmeter, and Russell (2008) note, the dip measures the amount of “stretching” needed to render the empirical cdf of a multi-modal distribution unimodal; therefore, a higher value of the dip leads to a rejection of the null hypothesis of unimodality.16

It is important to note that the dip test only allows us to infer whether the null hypothesis of unimodality is rejected or not, while kernel density based tests, such as Silverman (1981), can identify the number of modes in the data. There are two reasons why we prefer the dip test over the Silverman (1981) one to classify countries. First, unlike the dip test, density-based tests are highly sensitive to the choice of the bandwidth parameter. Second, the Silverman test is not well suited for data that, while continuous in nature like our export intensity data, exhibits clustering at figures that are multiples of 5%.17 The dip test, on the other hand, can be adjusted to take into account the discreteness of the data. Despite the advantages of the dip statistic, calculating the Silverman test reveals that the number of modes never exceeds two in any country in our data. Therefore, we classify a country as having a unimodal export intensity distribution if its dip test statistic is not rejected at the 1% significance level; otherwise, we consider it to be bimodal.

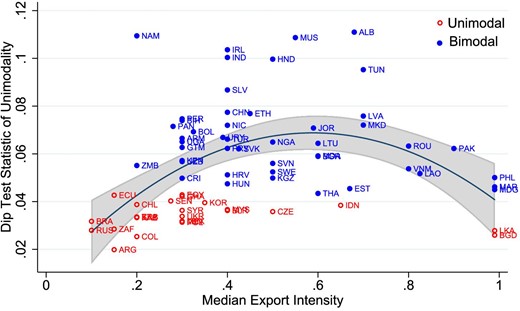

Figure 5 presents the dip statistic for each country in our sample. We find that the distribution of export intensity is bimodal in 47 out of 72 countries. This result stands in sharp contrast with the existing literature suggesting that this distribution is generally unimodal, with a majority of exporters selling a small share of their output abroad.

Dip test of unimodality of export intensity. The figure reports the value of the Hartigan and Hartigan (1985) dip test statistic of unimodality. Countries are identified as having a unimodal export intensity distribution if their dip statistic does not reject the null hypothesis of unimodality at the 1% confidence level; otherwise, they are identified as bimodal. The reported value of the dip statistic is calculated as the mean across 1,000 bootstrapped samples of 200 exporters drawn for each country. The algorithm used to calculate the dip test statistic is adjusted to take into account the discreteness of the export intensity data.

We next calculate the dip test across the different subsamples presented in Figure 3. Excluding foreign-owned and processing exporters has little effect on the number of countries we classify as bimodal, although countries such as Costa Rica, Croatia, and Hungary—notable for their success in attracting multinational firms—are reclassified as being unimodal. While we observe bimodality in the distributions of OECD and non-OECD countries, we find that this feature is more prevalent among countries that incentivize high-intensity exporters. Excluding firms that export all their output from the data altogether makes a significant dent in the prevalence of bimodality, increasing the number of countries with unimodal distributions from 25 to 46. Thus, our results show that the existence of twin peaks is not fully accounted for by the prevalence of a specific type of exporter operating within countries. Lastly, we calculate the dip statistic for country-sector pairs with more than 50 exporters and find that among the countries that we identify as bimodal based on their aggregate export intensity distribution, more than half of the distributions within sectors are themselves bimodal.

3.4. Comparing WBES with More Representative Surveys

An important concern is that twin peaks could be an artefact of the WBES data. Asker, Collard-Wexler, and Loecker (2014), for instance, note that the stratification procedure across sectors, size categories, and geographic locations used in the construction of the WBES leads to oversampling of larger firms. Although it is not clear why this would necessarily increase the likelihood of observing bimodal export intensity distributions, we show that twin peaks in the distribution of export intensity also arise in more representative datasets.

To this end, we asked fellow researchers to calculate for us the share of exporters across export intensity bins using well-known firm-level manufacturing surveys for a subsample of 13 countries in our data, which we then compared with the same moments calculated from WBES.18 The countries that we consider include five that we classify as unimodal (Argentina, Chile, Colombia, Indonesia, and South Africa) and eight that are bimodal (China, Hungary, India, Ireland, Pakistan, Thailand, Uruguay, and Vietnam). Most surveys we used for this analysis include all manufacturing firms with more than 10–20 employees, although the data for China and Ireland are based on surveys of larger firms. It is also important to note that the distribution of export intensity based on manufacturing surveys is calculated with data for a single year, whereas our main data set pools exporters from all survey waves available for a given country in the WBES.

Table 3 presents the results of our comparison and shows that the WBES provides an accurate picture of the distribution export intensity. Both the WBES and the different alternative data sources yield similar results with regard to the existence or not of twin peaks—even in the cases in which there are sizeable differences in the share of exporters in individual bins (such as Hungary and India). Crucially, in all countries but one, the share of exporters with export intensity in the middle bins is higher in the WBES than in the more representative data. Thus, the results presented in Figure 5 seem to, if anything, underestimate how common bimodal export intensity distributions are across the world.

Comparison of export intensity distributions—WBESs versus other surveys.

| # | Share of exporters with export intensity |$\in$|: | ||||||

|---|---|---|---|---|---|---|---|

| Country | Survey | Exporters | (0.0,0.2] | (0.2,0.4] | (0.4,0.6] | (0.6,0.8] | (0.8,1.0] |

| Argentina | ENIT | 830 | 0.660 | 0.123 | 0.071 | 0.065 | 0.081 |

| WBES | 1,140 | 0.535 | 0.225 | 0.102 | 0.067 | 0.071 | |

| Chile | ENIA | 900 | 0.582 | 0.116 | 0.113 | 0.093 | 0.096 |

| WBES | 1,001 | 0.490 | 0.186 | 0.098 | 0.065 | 0.162 | |

| China | NBS | 50,902 | 0.221 | 0.101 | 0.091 | 0.101 | 0.486 |

| WBES | 1,439 | 0.282 | 0.198 | 0.116 | 0.093 | 0.311 | |

| Colombia | EAM | 1,332 | 0.643 | 0.157 | 0.068 | 0.038 | 0.095 |

| WBES | 703 | 0.459 | 0.273 | 0.128 | 0.067 | 0.073 | |

| Hungary | APEH | 7,143 | 0.488 | 0.127 | 0.081 | 0.079 | 0.225 |

| WBES | 300 | 0.243 | 0.207 | 0.160 | 0.123 | 0.267 | |

| India | Prowess | 3,133 | 0.576 | 0.136 | 0.088 | 0.071 | 0.129 |

| WBES | 2,212 | 0.260 | 0.214 | 0.116 | 0.072 | 0.338 | |

| Indonesia | Census | 3,949 | 0.124 | 0.097 | 0.089 | 0.127 | 0.563 |

| WBES | 720 | 0.125 | 0.172 | 0.144 | 0.139 | 0.419 | |

| Ireland | FAME | 151 | 0.371 | 0.093 | 0.079 | 0.099 | 0.358 |

| WBES | 97 | 0.330 | 0.155 | 0.113 | 0.082 | 0.320 | |

| Pakistan | FRBP | 6,043 | 0.207 | 0.056 | 0.041 | 0.043 | 0.652 |

| WBES | 534 | 0.148 | 0.146 | 0.109 | 0.062 | 0.536 | |

| South Africa | SARS-NT | 7,530 | 0.844 | 0.076 | 0.036 | 0.025 | 0.019 |

| WBES | 558 | 0.529 | 0.279 | 0.113 | 0.020 | 0.060 | |

| Thailand | OIE | 1,591 | 0.302 | 0.136 | 0.111 | 0.121 | 0.331 |

| WBES | 1,066 | 0.147 | 0.151 | 0.134 | 0.141 | 0.427 | |

| Uruguay | EAAE | 389 | 0.424 | 0.131 | 0.090 | 0.095 | 0.260 |

| WBES | 467 | 0.328 | 0.173 | 0.105 | 0.103 | 0.291 | |

| Vietnam | ASE | 4,946 | 0.292 | 0.108 | 0.094 | 0.115 | 0.391 |

| WBES | 1,251 | 0.173 | 0.128 | 0.065 | 0.104 | 0.530 | |

| # | Share of exporters with export intensity |$\in$|: | ||||||

|---|---|---|---|---|---|---|---|

| Country | Survey | Exporters | (0.0,0.2] | (0.2,0.4] | (0.4,0.6] | (0.6,0.8] | (0.8,1.0] |

| Argentina | ENIT | 830 | 0.660 | 0.123 | 0.071 | 0.065 | 0.081 |

| WBES | 1,140 | 0.535 | 0.225 | 0.102 | 0.067 | 0.071 | |

| Chile | ENIA | 900 | 0.582 | 0.116 | 0.113 | 0.093 | 0.096 |

| WBES | 1,001 | 0.490 | 0.186 | 0.098 | 0.065 | 0.162 | |

| China | NBS | 50,902 | 0.221 | 0.101 | 0.091 | 0.101 | 0.486 |

| WBES | 1,439 | 0.282 | 0.198 | 0.116 | 0.093 | 0.311 | |

| Colombia | EAM | 1,332 | 0.643 | 0.157 | 0.068 | 0.038 | 0.095 |

| WBES | 703 | 0.459 | 0.273 | 0.128 | 0.067 | 0.073 | |

| Hungary | APEH | 7,143 | 0.488 | 0.127 | 0.081 | 0.079 | 0.225 |

| WBES | 300 | 0.243 | 0.207 | 0.160 | 0.123 | 0.267 | |

| India | Prowess | 3,133 | 0.576 | 0.136 | 0.088 | 0.071 | 0.129 |

| WBES | 2,212 | 0.260 | 0.214 | 0.116 | 0.072 | 0.338 | |

| Indonesia | Census | 3,949 | 0.124 | 0.097 | 0.089 | 0.127 | 0.563 |

| WBES | 720 | 0.125 | 0.172 | 0.144 | 0.139 | 0.419 | |

| Ireland | FAME | 151 | 0.371 | 0.093 | 0.079 | 0.099 | 0.358 |

| WBES | 97 | 0.330 | 0.155 | 0.113 | 0.082 | 0.320 | |

| Pakistan | FRBP | 6,043 | 0.207 | 0.056 | 0.041 | 0.043 | 0.652 |

| WBES | 534 | 0.148 | 0.146 | 0.109 | 0.062 | 0.536 | |

| South Africa | SARS-NT | 7,530 | 0.844 | 0.076 | 0.036 | 0.025 | 0.019 |

| WBES | 558 | 0.529 | 0.279 | 0.113 | 0.020 | 0.060 | |

| Thailand | OIE | 1,591 | 0.302 | 0.136 | 0.111 | 0.121 | 0.331 |

| WBES | 1,066 | 0.147 | 0.151 | 0.134 | 0.141 | 0.427 | |

| Uruguay | EAAE | 389 | 0.424 | 0.131 | 0.090 | 0.095 | 0.260 |

| WBES | 467 | 0.328 | 0.173 | 0.105 | 0.103 | 0.291 | |

| Vietnam | ASE | 4,946 | 0.292 | 0.108 | 0.094 | 0.115 | 0.391 |

| WBES | 1,251 | 0.173 | 0.128 | 0.065 | 0.104 | 0.530 | |

Notes. Argentina: National Survey on Innovation and Technological Behavior of Industrial Argentinean Firms (ENIT) for the year 2001; this is a representative sample of establishments with more than ten employees. Chile: Annual National Industrial Survey (ENIA) for the year 2000, covering the universe of Chilean manufacturing plants with ten or more workers. Colombia: Annual Manufacturing Survey (EIA) for the year 1991, covering the universe of Colombian manufacturing plants with 10 or more workers. China: National Bureau of Statistics (NBS) Manufacturing Survey for the year 2003, which includes state-owned enterprises and private firms with sales above 5 million Chinese Yuan. Hungary: the universe of manufacturing firms for the year 2014 drawn from APEH, the Hungarian tax authority. India: Prowess database collected by the Centre for Monitoring the Indian Economy (CMIE) for the year 2001. Indonesia: Indonesian Census of Manufacturing Firms for the year 2009, which surveys all registered manufacturing plants with more than 20 employees. Ireland: FAME database collected by Bureau van Dijk for the year 2007. Pakistan: export intensity is constructed from two administrative datasets from the Federal Board of Revenue of Pakistan (FBRP); export figures are from customs records and domestic sales from VAT data records. The data records all firms with an annual turnover above 2.5 million Pakistani rupees for the year 2013. South Africa: South African Revenue Service and National Treasury Firm-Level Panel (SARS-NT) for the year 2010, which covers the universe of all tax-registered firms. Thailand: Annual Survey of Thailand’s Manufacturing Industries by the Office of Industrial Economics (OIE) for the year 2014. The questionnaire’s response rate is about 60% of all firms, accounting for about 95% of total manufacturing. Uruguay: Annual Survey of Economic Activity (EAAE), which covers all manufacturing plants with ten or more employees for the year 2005. Vietnam: Annual Survey on Enterprises (ASE) for the year 2010, which covers all state-owned enterprises, foreign-owned firms, and domestic private firms with more than ten employees.

Comparison of export intensity distributions—WBESs versus other surveys.

| # | Share of exporters with export intensity |$\in$|: | ||||||

|---|---|---|---|---|---|---|---|

| Country | Survey | Exporters | (0.0,0.2] | (0.2,0.4] | (0.4,0.6] | (0.6,0.8] | (0.8,1.0] |

| Argentina | ENIT | 830 | 0.660 | 0.123 | 0.071 | 0.065 | 0.081 |

| WBES | 1,140 | 0.535 | 0.225 | 0.102 | 0.067 | 0.071 | |

| Chile | ENIA | 900 | 0.582 | 0.116 | 0.113 | 0.093 | 0.096 |

| WBES | 1,001 | 0.490 | 0.186 | 0.098 | 0.065 | 0.162 | |

| China | NBS | 50,902 | 0.221 | 0.101 | 0.091 | 0.101 | 0.486 |

| WBES | 1,439 | 0.282 | 0.198 | 0.116 | 0.093 | 0.311 | |

| Colombia | EAM | 1,332 | 0.643 | 0.157 | 0.068 | 0.038 | 0.095 |

| WBES | 703 | 0.459 | 0.273 | 0.128 | 0.067 | 0.073 | |

| Hungary | APEH | 7,143 | 0.488 | 0.127 | 0.081 | 0.079 | 0.225 |

| WBES | 300 | 0.243 | 0.207 | 0.160 | 0.123 | 0.267 | |

| India | Prowess | 3,133 | 0.576 | 0.136 | 0.088 | 0.071 | 0.129 |

| WBES | 2,212 | 0.260 | 0.214 | 0.116 | 0.072 | 0.338 | |

| Indonesia | Census | 3,949 | 0.124 | 0.097 | 0.089 | 0.127 | 0.563 |

| WBES | 720 | 0.125 | 0.172 | 0.144 | 0.139 | 0.419 | |

| Ireland | FAME | 151 | 0.371 | 0.093 | 0.079 | 0.099 | 0.358 |

| WBES | 97 | 0.330 | 0.155 | 0.113 | 0.082 | 0.320 | |

| Pakistan | FRBP | 6,043 | 0.207 | 0.056 | 0.041 | 0.043 | 0.652 |

| WBES | 534 | 0.148 | 0.146 | 0.109 | 0.062 | 0.536 | |

| South Africa | SARS-NT | 7,530 | 0.844 | 0.076 | 0.036 | 0.025 | 0.019 |

| WBES | 558 | 0.529 | 0.279 | 0.113 | 0.020 | 0.060 | |

| Thailand | OIE | 1,591 | 0.302 | 0.136 | 0.111 | 0.121 | 0.331 |

| WBES | 1,066 | 0.147 | 0.151 | 0.134 | 0.141 | 0.427 | |

| Uruguay | EAAE | 389 | 0.424 | 0.131 | 0.090 | 0.095 | 0.260 |

| WBES | 467 | 0.328 | 0.173 | 0.105 | 0.103 | 0.291 | |

| Vietnam | ASE | 4,946 | 0.292 | 0.108 | 0.094 | 0.115 | 0.391 |

| WBES | 1,251 | 0.173 | 0.128 | 0.065 | 0.104 | 0.530 | |

| # | Share of exporters with export intensity |$\in$|: | ||||||

|---|---|---|---|---|---|---|---|

| Country | Survey | Exporters | (0.0,0.2] | (0.2,0.4] | (0.4,0.6] | (0.6,0.8] | (0.8,1.0] |

| Argentina | ENIT | 830 | 0.660 | 0.123 | 0.071 | 0.065 | 0.081 |

| WBES | 1,140 | 0.535 | 0.225 | 0.102 | 0.067 | 0.071 | |

| Chile | ENIA | 900 | 0.582 | 0.116 | 0.113 | 0.093 | 0.096 |

| WBES | 1,001 | 0.490 | 0.186 | 0.098 | 0.065 | 0.162 | |

| China | NBS | 50,902 | 0.221 | 0.101 | 0.091 | 0.101 | 0.486 |

| WBES | 1,439 | 0.282 | 0.198 | 0.116 | 0.093 | 0.311 | |

| Colombia | EAM | 1,332 | 0.643 | 0.157 | 0.068 | 0.038 | 0.095 |

| WBES | 703 | 0.459 | 0.273 | 0.128 | 0.067 | 0.073 | |

| Hungary | APEH | 7,143 | 0.488 | 0.127 | 0.081 | 0.079 | 0.225 |

| WBES | 300 | 0.243 | 0.207 | 0.160 | 0.123 | 0.267 | |

| India | Prowess | 3,133 | 0.576 | 0.136 | 0.088 | 0.071 | 0.129 |

| WBES | 2,212 | 0.260 | 0.214 | 0.116 | 0.072 | 0.338 | |

| Indonesia | Census | 3,949 | 0.124 | 0.097 | 0.089 | 0.127 | 0.563 |

| WBES | 720 | 0.125 | 0.172 | 0.144 | 0.139 | 0.419 | |

| Ireland | FAME | 151 | 0.371 | 0.093 | 0.079 | 0.099 | 0.358 |

| WBES | 97 | 0.330 | 0.155 | 0.113 | 0.082 | 0.320 | |

| Pakistan | FRBP | 6,043 | 0.207 | 0.056 | 0.041 | 0.043 | 0.652 |

| WBES | 534 | 0.148 | 0.146 | 0.109 | 0.062 | 0.536 | |

| South Africa | SARS-NT | 7,530 | 0.844 | 0.076 | 0.036 | 0.025 | 0.019 |

| WBES | 558 | 0.529 | 0.279 | 0.113 | 0.020 | 0.060 | |

| Thailand | OIE | 1,591 | 0.302 | 0.136 | 0.111 | 0.121 | 0.331 |

| WBES | 1,066 | 0.147 | 0.151 | 0.134 | 0.141 | 0.427 | |

| Uruguay | EAAE | 389 | 0.424 | 0.131 | 0.090 | 0.095 | 0.260 |

| WBES | 467 | 0.328 | 0.173 | 0.105 | 0.103 | 0.291 | |

| Vietnam | ASE | 4,946 | 0.292 | 0.108 | 0.094 | 0.115 | 0.391 |

| WBES | 1,251 | 0.173 | 0.128 | 0.065 | 0.104 | 0.530 | |

Notes. Argentina: National Survey on Innovation and Technological Behavior of Industrial Argentinean Firms (ENIT) for the year 2001; this is a representative sample of establishments with more than ten employees. Chile: Annual National Industrial Survey (ENIA) for the year 2000, covering the universe of Chilean manufacturing plants with ten or more workers. Colombia: Annual Manufacturing Survey (EIA) for the year 1991, covering the universe of Colombian manufacturing plants with 10 or more workers. China: National Bureau of Statistics (NBS) Manufacturing Survey for the year 2003, which includes state-owned enterprises and private firms with sales above 5 million Chinese Yuan. Hungary: the universe of manufacturing firms for the year 2014 drawn from APEH, the Hungarian tax authority. India: Prowess database collected by the Centre for Monitoring the Indian Economy (CMIE) for the year 2001. Indonesia: Indonesian Census of Manufacturing Firms for the year 2009, which surveys all registered manufacturing plants with more than 20 employees. Ireland: FAME database collected by Bureau van Dijk for the year 2007. Pakistan: export intensity is constructed from two administrative datasets from the Federal Board of Revenue of Pakistan (FBRP); export figures are from customs records and domestic sales from VAT data records. The data records all firms with an annual turnover above 2.5 million Pakistani rupees for the year 2013. South Africa: South African Revenue Service and National Treasury Firm-Level Panel (SARS-NT) for the year 2010, which covers the universe of all tax-registered firms. Thailand: Annual Survey of Thailand’s Manufacturing Industries by the Office of Industrial Economics (OIE) for the year 2014. The questionnaire’s response rate is about 60% of all firms, accounting for about 95% of total manufacturing. Uruguay: Annual Survey of Economic Activity (EAAE), which covers all manufacturing plants with ten or more employees for the year 2005. Vietnam: Annual Survey on Enterprises (ASE) for the year 2010, which covers all state-owned enterprises, foreign-owned firms, and domestic private firms with more than ten employees.

4. Theoretical Framework

4.1. Model

We assume that the revenue shifters |$z_i\!(\omega )$| are random variables following a lognormal distribution with mean 0, variance |$\sigma ^2_{ zi}$| and pdf |$f(z_i)$| for |$i\in \lbrace d,x\rbrace$|. The lognormal distribution has gained increased prominence in the international trade literature (see e.g. Head, Mayer, and Thoenig 2014; Nigai 2017; Hanson, Lind, and Muendler 2018; Mrázová, Neary, and Parenti 2021). Recent work has shown that it not only fits better the complete distribution of sales—rather than just the right tail as the Pareto distribution—but also delivers more realistic implications for the trade elasticity and the welfare gains from trade (Bas, Mayer, and Thoenig 2017; Fernandes et al. 2018).

The lognormal distribution has two key properties that we take advantage of for our purposes: (i) it is closed under scalar multiplication, which means that the scaled revenue shifters, |$Z_d\!(\omega )\equiv s_dz_d\!(\omega )$| and |$Z_x\!(\omega )\equiv s_xz_x\!(\omega )$| defined in (2), are also lognormal; and (ii) the ratio of two lognormal random variables is also lognormal. Since |$E$| can be expressed as a strictly increasing function of the ratio of export to domestic revenue shifters, |$Z\equiv Z_x/Z_d$|, the latter property allows us to apply the method of transformations for random variables to derive a closed-form expression for the pdf of export intensity. This yields our first result.

See Appendix A.1.

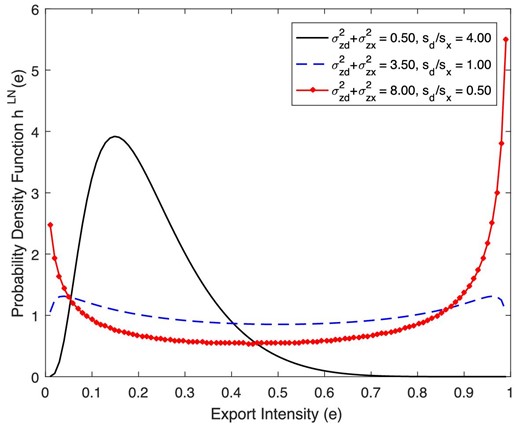

As equation (3) shows, the distribution of export intensity is characterized by two parameters, the relative size of the domestic market compared to the foreign one, |$s_d/s_x$| (which we will also refer to as the scale parameter), and the sum of the variances of domestic and export revenue shifters, |$\sigma ^2_{ zd}+\sigma ^2_{ zx}$| (the shape parameter). Figure A.1 in Appendix A.1 provides examples of the pdf of export intensity for different values of the shape and scale parameters. The distribution (3) is known in statistics as the logit-normal distribution;20 its key properties have been derived by Johnson (1949).

We now move to describe the conditions under which the distribution of export intensity is bimodal. These are spelled out in our second proposition.

See Appendix A.2.

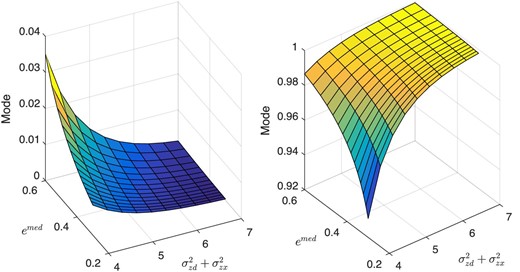

Proposition 2 says that when the sum of the variances of revenue shifters is sufficiently high, the distribution of export intensity exhibits twin peaks. The intuition is that because the revenue shifters are independent across destinations, the likelihood that firms face very high demand in only one of the two markets they serve—thereby generating export intensities close to either 0 or 1—is higher when the sum of the variance of revenue shifters is high. Figure A.2 in Appendix A.2 shows how the two modes of the export intensity distribution relate to its shape and scale parameters. Increasing the variance of revenue shifters makes the twin peaks more prominent by shifting probability mass towards the boundaries of the support.

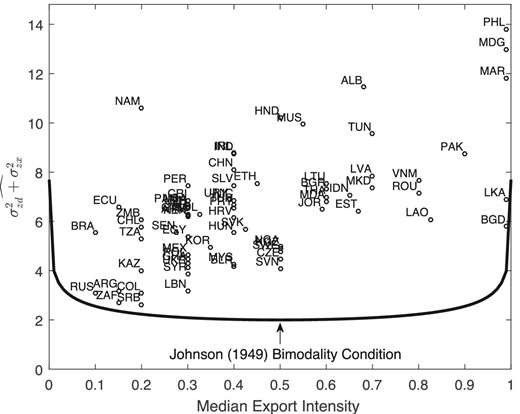

Equation (5) defines a U-shaped curve in the space |$\lbrace(\sigma ^2_{ zd}+\sigma ^2_{ zx}), e^{ {med}}\rbrace$|, which determines the level of the variance of revenue shifters necessary to produce bimodality given the relative market size. Thus, for countries that are either very small or very large vis-à-vis the foreign market and therefore have substantial probability mass near 0 or 1, respectively, the necessary cutoff for the shape parameter to produce a bimodal distribution is higher than for countries for which |$s_d/s_x$| is closer to 1 (or equivalently, the median export intensity is close to 0.5).

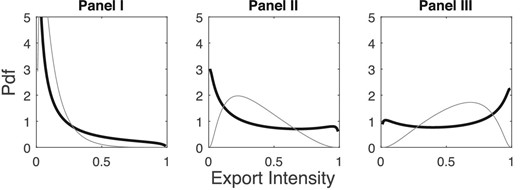

Figure 6 shows how changes in |$s_d/s_x$|—caused, for instance, by a reduction of the iceberg trade cost faced by home exporters—affect the distribution of export intensity.21 As we move from Panel I on the left to Panel III on the right, the relative size of the foreign market increases.22 The figure also compares two distributions: The darker line shows the distribution of export intensity when |$\sigma ^2_{ zd}+\sigma ^2_{ zx}=4$|—thus, producing a bimodal distribution—while the lighter line represents a unimodal distribution (when the shape parameter is equal to 1).

Reduction in export costs with and without twin peaks. The figure plots the pdf of export intensity when revenue shifters are lognormal with |$\sigma ^2_{ zd}+\sigma ^2_{ zx}=4$| (darker line) and |$\sigma ^2_{ zd}+\sigma ^2_{ zx}=1$| (lighter line) for different values of the ratio of scale parameters, namely, |$s_d/s_x=10$| in Panel I, 2 in Panel II, and 0.667 in Panel III.

In Panel I of Figure 6, trade costs are so high that most exporters sell only a small share of their output abroad regardless of the level of dispersion in revenue shifters, and therefore, the two export intensity distributions look quite similar. As trade costs fall, the intensity of all exporters increases, and the distribution of export intensity shifts to the right. However, the difference in the distribution with and without twin peaks also becomes starker. When the variance of revenue shifters is sufficiently large, greater access to foreign markets increases the prevalence of high-intensity exporters moving mass from the left to the right tail of the distribution. In contrast, when dispersion is lower, the increase in the intensity of exporters following liberalization is more gradual.23

Our last theoretical result shows that there is a one-to-one relationship between relative market size and the median export intensity.

See Appendix A.3.

As will become clearer in Section 5 below, this result greatly facilitates the identification and estimation of the parameters of interest.

4.2. Alternative Assumptions