Abstract

We empirically investigate the proposition that firms charge premia on cash prices in transactions involving trade credit. Using a comprehensive panel data set on product-level transaction prices and firm characteristics, we relate trade credit issuance to price setting. In a recession characterized by tightened credit conditions, we find that prices increase significantly more on products sold by firms issuing more trade credit, in response to higher opportunity costs of liquidity and counterparty risks. Our results thus demonstrate the importance of trade credit for price setting and show that trade credit issuance induces a channel through which financial conditions affect prices.

1. Introduction

Does trade credit issuance affect firms’ price-setting behavior? Research on the links between firm characteristics and price setting has demonstrated that due to capital market imperfections, firms’ leverage and liquidity positions make for important determinants of movements in price mark-ups over the business cycle (Gottfries 1991; Chevalier and Scharfstein 1996; Gilchrist et al. 2017). In this paper, we explore an additional channel at the firm level—the trade credit channel—through which financial conditions may affect price setting. We posit that product prices in transactions involving trade credit include a trade credit price premium, the size of which is determined by the contracted loan maturity and an implicit interest rate, which, in turn, is a function of the selling firm's liquidity costs and the buying firm's default risk. Our proposition implies that trade credit issuance introduces a countercyclical element into firms’ price-setting behavior, since increases in liquidity costs and counterparty risks, which typically accompany recessions and financial crises, cause firms to raise prices. The widespread use of trade credit in interfirm trade suggests that such fluctuations in the trade credit price premium could be quantitatively important determinants of inflation dynamics.1 However, empirical evidence on the effects of trade credit issuance on price setting is scarce, most likely due to a paucity of firm-level product price data.2

Our aim is to contribute toward a better understanding of trade credit pricing, and thereby also of product pricing in general, by investigating the prevalence and determinants of implicit interest rates in trade credit contracts. To this end, we make use of a rich data set comprising product-level data on prices and quantities for Swedish manufacturing firms; firm-level accounting data; loan-level data covering all loans extended by the four major Swedish banks to domestic corporations; firm-level data on credit ratings from the leading Swedish credit bureau; export data at the five-digit industry level; as well as data on all applications for the issuance of injunctions to settle overdue trade credit claims submitted by Swedish corporations to the Swedish Enforcement Agency. Our empirical strategy is based on exploiting the 2008–2009 recession in Sweden—which featured severe financial market distress, as well as a sharp downturn in the real economy—together with the cross-sectional variation in trade credit maturities that prevailed at the outset of the recession. The underlying logic of this empirical approach is that a given increase in the implicit trade credit interest rate is predicted to have a larger impact on product prices set by firms that issue trade credit with longer maturities. Hence, by exploiting an aggregate shock to liquidity costs and counterparty risks together with cross-sectional variation in trade credit maturities, we can test for the presence of a trade credit price premium, as well as quantify the average change in the implicit trade credit interest rate during the recession. Importantly, the richness of our data allows us to carefully consider the robustness of our results and to validate the plausibility of the identifying assumptions in several ways, not least by controlling for a large set of potential confounders.

Our main finding can be summarized as follows. Firms that issued trade credit with longer maturities, relative to firms that issued shorter maturities, increased their prices significantly more in the 2008–2009 recession. The annual change in the implicit trade credit interest rate was 20.9 percentage points higher during the crisis period than in noncrisis years; in terms of price changes, this implies that a maturity difference of 20 days—approximately equivalent to one standard deviation—is associated with a relative annual price adjustment of 1.1 percentage points. The magnitude of this effect can be put into perspective by the following considerations. First, our hypothesis is that the increase in trade credit interest rates in part reflects a deterioration in financing conditions and the associated rise in the opportunity cost of liquidity facing sellers, and in part a rise in default risks and credit risk premia, both of which were substantial during the crisis (see, e.g., Whited 1992, for the former aspect and Berndt et al. 2018, for the latter). Second, a reference point is the annualized interest rate in the well-known “2/10 net 30” two-part terms contract, which is 44.6%.3 Third, another point of reference is the cost of factoring services, that is, sales of sellers’ invoices to a third party priced at a discounted nominal invoice value. Factoring discounts in Sweden are currently in the range of 2%–5%, which in the case of the widely used net-30 contracts—featuring a 30-day credit period and no discount option—corresponds to implicit annualized interest rates of 24.6%–62.4%.4 Hence, the estimated increase in implicit trade credit interest rates during the recession is substantial but quite reasonable when considering the crisis-induced shifts in the underlying determinants of trade credit interest rates, the implicit interest rates in two-part contracts, and the costs associated with factoring services.

We also explore the mechanisms underlying the baseline finding that firms issuing longer trade credit maturities raised product prices more during the crisis. Our conjecture is that the association between trade credit issuance and price changes during the crisis is stronger for firms subject to larger increases in liquidity costs and counterparty risks. We test this using cross-sectional heterogeneity analyses, in which we estimate the baseline specification on subsamples of firms defined by a set of proxies for the hypothesized mechanisms. More specifically, we identify firms that experienced large increases in liquidity costs on the basis of various precrisis firm characteristics, as well as by exploiting the Baltic crisis and its effects on Swedish banks as a quasi-experiment. For increases in counterparty risk, we use, first, a set of industry-level measures of buyer risk calculated using input–output tables; and second, seller-level measures constructed using data on applications for the issuance of injunctions to enforce late trade credit payments. The results of the cross-sectional heterogeneity analyses show that the impact of trade credit issuance on prices indeed is observed primarily for firms that faced larger increases in liquidity costs and counterparty risks, respectively, which provides support for our conjecture about the underlying mechanisms.

This paper makes two key contributions. First, our findings contribute to the trade credit literature by advancing the understanding of how trade credit is priced. The existing literature on the pricing of trade credit is largely divided between two opposing views. The most commonly held is that trade credit is an expensive funding source, since the discount structure in two-part contracts, in which buyers are offered discounts for early payments, imply very high interest rates for buyers that choose to forgo the discount (see, e.g., Smith 1987; Petersen and Rajan 1997; Klapper, Laeven, and Rajan 2012). However, most trade credit is issued under net terms contracts, in which no discounts are offered, nor are explicit interest rates specified; hence, the discount structure in two-part contracts does not establish that trade credit is expensive in general.5 Instead, the predominance of net terms contracts has led others to draw the opposite conclusion, namely, that trade credit is typically supplied at zero interest (see, e.g., Daripa and Nilsen 2011). The absence of explicit interest rates does not imply that trade credit issued under net terms is free, however, since sellers may incorporate implicit interest rates in their product prices, as outlined and argued in this paper. Several papers, including Cuñat (2007) and Giannetti, Burkart, and Ellingsen (2011), have noted this possibility, but the available empirical evidence is scant. In sum, given that the vast majority of trade credit is issued under net terms, and that there exists little empirical evidence on the pricing of net terms contracts, the question of how trade credit is priced remains an open issue.6

Current evidence on the effect of trade credit issuance on product prices comes from two papers studying trade finance, that is, the financing of international trade transactions. Antràs and Foley (2015) study financing terms in international trade using transaction-level data from a large US exporter of food products. They show that the exporter charges higher product prices in trade credit transactions than in cash transactions when buyers are located in countries with weak enforcement of contracts. In contemporaneous work, Garcia-Marin, Justel, and Schmidt-Eisenlohr (2018) study trade credit extension in international trade using transaction-level data covering the exports of Chilean manufacturers. Like Antràs and Foley (2015), they find that product prices are higher in transactions involving trade credit and that premia are particularly high for exports to countries characterized by weak contract enforcement. These papers thus suggest that sellers price counterparty risk when extending trade credit, which is consistent with the results in this paper. We extend the findings in Antràs and Foley (2015) and Garcia-Marin, Justel, and Schmidt-Eisenlohr (2018) in several ways. First, we show that trade credit price premia feature prominently in interfirm trade in general, rather than being particular to international trade transactions. Second, we provide evidence indicating that the implicit interest rates in trade credit contracts are determined not only by counterparty risk, but also by sellers’ liquidity costs, and hence that trade credit issuance induces a channel through which financial market conditions affect prices. Third, we document that shifts in liquidity costs and counterparty risks cause the trade credit price premium to vary over time.

We also contribute to the macroeconomic literature on financial conditions and product pricing. One strand of this literature has proposed the existence of a cost channel of monetary policy, according to which hikes in nominal interest rates brought on by contractionary monetary policy generate cost-push inflation by increasing firms’ working capital costs (e.g., Christiano and Eichenbaum 1992; Christiano, Eichenbaum, and Evans 1997; Ravenna and Walsh 2006). Barth and Ramey (2001), among others, provide aggregate empirical evidence in support of the cost channel of monetary policy, whereas Gaiotti and Secchi (2006) document similar effects using firm-level data on prices and interest rates for a sample of Italian manufacturing firms. More recently, Christiano, Eichenbaum, and Trabandt (2015) show, on the basis of an estimated New Keynesian model, that the increase in credit spreads that occurred during the financial crisis of 2008–2009 dampened deflationary pressures through the cost channel. Our paper adds to this literature in two ways: first, we provide new microeconometric evidence on the effects of financial market distress on prices through the cost channel; second, our empirical framework allows us to separately assess the effects of the two main components of working capital, namely, accounts receivable and inventories. Finally, our paper is also consistent with and complementary to the strand of this literature that shows that liquidity constraints, in the presence of customer markets, constitute an important determinant of movements in price mark-ups over the business cycle (Gottfries 1991; Chevalier and Scharfstein 1996; Gilchrist et al. 2017).

The rest of the paper is organized as follows. The next section describes the 2008–2009 recession in Sweden, details our data resources, and provides descriptive statistics. Section 3 presents a conceptual framework that outlines the link between trade credit and product pricing, and describes the empirical approach by which we take its predictions to the data. Sections 4 and 5 present the results of the empirical analysis. Section 6 concludes.

2. Institutional Background and Data

2.1. The 2008–2009 Recession in Sweden

The 2008–2009 recession in Sweden is well-suited for testing the hypothesis that product prices include a trade credit premium, since it featured a sharp downturn in the real economy as well as severe distress in the banking sector, both of which were caused by external shocks hitting the Swedish economy in the wake of the global financial crisis.

The banking sector distress had two main causes. The first was the collapse of international financial markets following the outbreak of the global financial crisis. Although Swedish banks had little direct exposure to asset-backed securities issued in the United States, they are highly dependent on external wholesale funding and are therefore sensitive to funding conditions in international financial markets, which deteriorated rapidly after the onset of the crisis. The second cause was the severe economic crisis in the Baltic countries, which two of Sweden’s four major banks were highly exposed to as a result of having expanded in the Baltic market in the years prior to the crisis. These two shocks led to elevated distress in the financial system, although observers’ judgments differ somewhat as to the severity of the distress. According to the IMF’s banking crisis database, for example, Sweden suffered a “borderline” systemic banking crisis beginning in 2008 (Laeven and Valencia 2012), whereas Romer and Romer (2017), using a financial distress measure ranging from 0 to 15, classifies the level of distress in Sweden during 2008–2009 as 5 on average, with a peak value of 7.

The banking sector distress quickly led to a deterioration in the credit conditions facing corporate borrowers: beginning in 2008 and continuing throughout 2009, growth in bank lending to firms fell steadily (Finansinspektionen 2012), and many firms reported on a worsening access to external finance (Konjunkturinstitutet 2009; Sveriges Riksbank 2009). Meanwhile, the real economy fell into a sharp recession, with a decline in real GDP of around 6% in 2009, partly due to the domestic banking sector distress and partly due to the breakdown in international trade that occurred during this period (see, e.g., Levchenko et al. 2010), which affected the export-oriented Swedish economy badly. The recession did thus not only impair firms’ cash flows and their access to external finance—and thereby their liquidity positions—but also led to increased counterparty risks, not least manifested in a near-doubling of the aggregate bankruptcy rate. Moreover, it is conceivable that corporate credit risk premia increased even more dramatically than the bankruptcy rate. Berndt et al. (2018), for example, document that risk premia for public firms in the United States—measured as the difference between a firm’s credit default swap rate and its expected default loss rate—peaked in the financial crisis of 2008–2009, when the cost for credit insurance per unit of expected loss increased by a factor 10 on average.

2.2. Data and Variable Definitions

The empirical analysis is based on data from four sources, which we merge unambiguously by means of the unique identifier (organisationsnummer) attached to each Swedish firm. First, we obtain data on prices and quantities from “Industrins varuproduktion”, an annual survey conducted by Statistics Sweden comprising all manufacturing plants with at least 20 employees, as well as a sample of smaller plants. The data cover transaction prices and quantities of goods sold at the product-plant level (products are classified using 8/9-digit CN codes).7 Thus, for each product produced at a given plant, we observe the average transaction price (as opposed to the list price), as well as the quantity of goods sold in each year. We aggregate the price and quantity data to the firm-product level using the sales value for each product and plant as weights.

Second, we obtain firm-level accounting data from the database Serrano, which covers the universe of corporations in Sweden. Serrano is constructed based on data from several official sources, most importantly the Swedish Companies Registrations Office, to which all Swedish corporations are required to submit annual financial accounting statements in accordance with EU standards. Third, we use a loan-level database available at Sveriges Riksbank, which covers all loans and credit lines extended by the four major Swedish banks to Swedish corporations. Fourth, we obtain data on firm-level default probabilities from the credit bureau UC AB. Finally, we use data on applications for the issuance of injunctions to enforce late trade credit payments, submitted by sellers to the Swedish Enforcement Agency

We include two sets of control variables. The first set of controls, |${\bf{X}_{i,p,t}}$|, consists of two variables at the firm-product level: the log change in the quantity of sales of product p by firm i between years t − 1 and t, ΔQi, p, t; and a proxy for the change in unit input costs for product p produced by firm i between years t − 1 and t, |$\Delta {\textit {UIC}}_{i,p,t}$|, where unit input costs are defined as the sum of labor costs and intermediate input costs divided by physical output.9 The second set of controls, |${\bf{Z}_{i,t-1}}$|, comprises the following firm-level variables: cash and liquid assets, |${\textit {Cash}}/{\textit {Assets}}_{i,t-1}$|; bank loans, |${\textit {Bank}} \ {\textit {debt}}/{\textit {Assets}}_{i,t-1}$|; asset tangibility, |${\textit {Tangible}} \ {\textit {assets}}/{\textit {Assets}}]_{i,t-1}$|; cash flow, |${\textit {EBITDA}}/{\textit {Assets}}_{i,t-1}$|; inventories, |${\textit {Inventories}}/{\textit {Sales}}_{i,t-1}$|; and firm size, |$\ln {\textit {Assets}_{i,t-1}}$|. Explanatory variables are winsorized at the 1st and 99th percentiles—that is, observations above the 99th percentile are assigned the value of the observation at the 99th percentile, and correspondingly for observations below the 1st percentile—to reduce the influence of outliers.

2.3. Sample and Descriptive Statistics

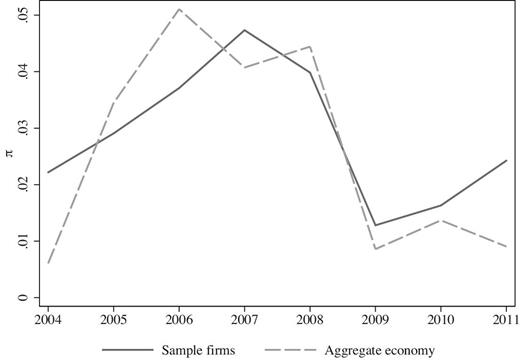

Table 1 reports descriptive statistics for all variables used in the empirical analysis. The mean (median) firm-product inflation rate, reported in panel A, is 2.9% (0.7%). The average value of |$\hat{\tau }_i^{07}$|, reported in panel B, is 0.097, which corresponds to a trade credit contract maturity of 35 days. Average cash holdings amount to 8.3% of total assets, whereas the average size of the unused part of firms’ credit lines is 4.3% of total assets. Panel C shows the values of the time-varying firm characteristics. The average firm has a book value of assets of 319 million SEK and sales of 390 million SEK (roughly 49 and 60 million USD, respectively, at the exchange rate prevailing at the end of 2007). The sample thus consists primarily of medium-sized and large firms. In Figure 1, we show that our sample is representative of the broader economy in terms of price changes. More specifically, the figure shows that the average annual firm-product inflation rates in our sample track the changes in the aggregate producer price index for the goods-producing sector of the economy quite closely over the sample period.

Price changes in sample and in the aggregate economy. The solid line shows the average annual firm-product inflation rate in our sample and the dashed line the annual change in the aggregate producer price index for the entire goods-producing economy (SNI/NACE sections A– E). We calculate the latter as the log change in the annual average of the monthly values of the producer price index. Source: Statistics Sweden and authors’ calculations.

Descriptive statistics.

| Mean | Median | SD | Pct. 25 | Pct. 75 | No. obs. | |

|---|---|---|---|---|---|---|

| A. Price and quantity variables (2004–2011) | ||||||

| Firm-product inflation rate (πi, p, t) | 0.029 | 0.007 | 0.159 | −0.031 | 0.093 | 45,953 |

| Change in quantity sold (ΔQi, p, t) | −0.007 | 0.005 | 0.442 | −0.147 | 0.154 | 45,953 |

| Change in unit input costs (ΔUICi, p, t) | 0.033 | 0.024 | 0.261 | −0.080 | 0.147 | 45,953 |

| B. Time-invariant firm characteristics (2007) | ||||||

| Trade credit maturity (|$\hat{\tau }_i^{07}$|) | 0.097 | 0.095 | 0.056 | 0.064 | 0.124 | 3,408 |

| |$ {{Inventories/Sales}}_i^{07}$| | 0.142 | 0.124 | 0.110 | 0.069 | 0.189 | 3,408 |

| |$ {{Export \ share}}_{j(i)}^{07}$| | 0.299 | 0.251 | 0.232 | 0.086 | 0.433 | 3,408 |

| |$ {{Cash/Assets}}_i^{07}$| | 0.083 | 0.024 | 0.127 | 0.002 | 0.112 | 3,408 |

| |$ {{Unused \, LC/Assets}}_i^{07}$| | 0.043 | 0.003 | 0.070 | 0.000 | 0.062 | 3,408 |

| ΔCustPDc(i) | 0.708 | 0.651 | 0.134 | 0.628 | 0.749 | 3,408 |

| ΔSalesc(i) | −0.070 | −0.047 | 0.103 | −0.125 | −0.008 | 3,408 |

| |$\Delta {Sales}_{c(i)}^{IV}$| | −0.042 | −0.057 | 0.037 | −0.072 | −0.002 | 3,408 |

| ΔSumInji | 0.115 | 0.000 | 0.744 | 0.000 | 0.000 | 3,408 |

| ΔNoInji | 0.110 | 0.000 | 0.715 | 0.000 | 0.000 | 3,408 |

| C. Time-varying firm characteristics (2004–2011) | ||||||

| Trade credit maturity (|$\hat{\tau }_{i,t}$|) | 0.090 | 0.090 | 0.048 | 0.060 | 0.117 | 18,025 |

| Cash/Assetsi, t | 0.081 | 0.022 | 0.124 | 0.002 | 0.111 | 18,025 |

| Bank debt/Assetsi, t | 0.126 | 0.028 | 0.164 | 0.000 | 0.232 | 18,025 |

| Tangible assets/Assetsi, t | 0.269 | 0.248 | 0.183 | 0.116 | 0.392 | 18,025 |

| Cash flow/Assetsi, t | 0.125 | 0.122 | 0.131 | 0.057 | 0.198 | 18,025 |

| Inventories/Salesi, t | 0.148 | 0.128 | 0.105 | 0.078 | 0.194 | 18,025 |

| Assetsi, t (in SEK 1,000) | 318,984 | 58,994 | 1,018,467 | 26,518 | 164,564 | 18,025 |

| Salesi, t (in SEK 1,000) | 390,197 | 101,013 | 1,003,049 | 45,561 | 258,046 | 18,025 |

| Mean | Median | SD | Pct. 25 | Pct. 75 | No. obs. | |

|---|---|---|---|---|---|---|

| A. Price and quantity variables (2004–2011) | ||||||

| Firm-product inflation rate (πi, p, t) | 0.029 | 0.007 | 0.159 | −0.031 | 0.093 | 45,953 |

| Change in quantity sold (ΔQi, p, t) | −0.007 | 0.005 | 0.442 | −0.147 | 0.154 | 45,953 |

| Change in unit input costs (ΔUICi, p, t) | 0.033 | 0.024 | 0.261 | −0.080 | 0.147 | 45,953 |

| B. Time-invariant firm characteristics (2007) | ||||||

| Trade credit maturity (|$\hat{\tau }_i^{07}$|) | 0.097 | 0.095 | 0.056 | 0.064 | 0.124 | 3,408 |

| |$ {{Inventories/Sales}}_i^{07}$| | 0.142 | 0.124 | 0.110 | 0.069 | 0.189 | 3,408 |

| |$ {{Export \ share}}_{j(i)}^{07}$| | 0.299 | 0.251 | 0.232 | 0.086 | 0.433 | 3,408 |

| |$ {{Cash/Assets}}_i^{07}$| | 0.083 | 0.024 | 0.127 | 0.002 | 0.112 | 3,408 |

| |$ {{Unused \, LC/Assets}}_i^{07}$| | 0.043 | 0.003 | 0.070 | 0.000 | 0.062 | 3,408 |

| ΔCustPDc(i) | 0.708 | 0.651 | 0.134 | 0.628 | 0.749 | 3,408 |

| ΔSalesc(i) | −0.070 | −0.047 | 0.103 | −0.125 | −0.008 | 3,408 |

| |$\Delta {Sales}_{c(i)}^{IV}$| | −0.042 | −0.057 | 0.037 | −0.072 | −0.002 | 3,408 |

| ΔSumInji | 0.115 | 0.000 | 0.744 | 0.000 | 0.000 | 3,408 |

| ΔNoInji | 0.110 | 0.000 | 0.715 | 0.000 | 0.000 | 3,408 |

| C. Time-varying firm characteristics (2004–2011) | ||||||

| Trade credit maturity (|$\hat{\tau }_{i,t}$|) | 0.090 | 0.090 | 0.048 | 0.060 | 0.117 | 18,025 |

| Cash/Assetsi, t | 0.081 | 0.022 | 0.124 | 0.002 | 0.111 | 18,025 |

| Bank debt/Assetsi, t | 0.126 | 0.028 | 0.164 | 0.000 | 0.232 | 18,025 |

| Tangible assets/Assetsi, t | 0.269 | 0.248 | 0.183 | 0.116 | 0.392 | 18,025 |

| Cash flow/Assetsi, t | 0.125 | 0.122 | 0.131 | 0.057 | 0.198 | 18,025 |

| Inventories/Salesi, t | 0.148 | 0.128 | 0.105 | 0.078 | 0.194 | 18,025 |

| Assetsi, t (in SEK 1,000) | 318,984 | 58,994 | 1,018,467 | 26,518 | 164,564 | 18,025 |

| Salesi, t (in SEK 1,000) | 390,197 | 101,013 | 1,003,049 | 45,561 | 258,046 | 18,025 |

Notes: This table reports descriptive statistics for all variables used in the empirical analysis, as well as for some additional firm characteristics. Each firm appears only once in panel B and only once per year in panel C, irrespective of how many products it sells and thus how many firm-product observations it has in a given year. Definitions of the variables are provided in the text.

Descriptive statistics.

| Mean | Median | SD | Pct. 25 | Pct. 75 | No. obs. | |

|---|---|---|---|---|---|---|

| A. Price and quantity variables (2004–2011) | ||||||

| Firm-product inflation rate (πi, p, t) | 0.029 | 0.007 | 0.159 | −0.031 | 0.093 | 45,953 |

| Change in quantity sold (ΔQi, p, t) | −0.007 | 0.005 | 0.442 | −0.147 | 0.154 | 45,953 |

| Change in unit input costs (ΔUICi, p, t) | 0.033 | 0.024 | 0.261 | −0.080 | 0.147 | 45,953 |

| B. Time-invariant firm characteristics (2007) | ||||||

| Trade credit maturity (|$\hat{\tau }_i^{07}$|) | 0.097 | 0.095 | 0.056 | 0.064 | 0.124 | 3,408 |

| |$ {{Inventories/Sales}}_i^{07}$| | 0.142 | 0.124 | 0.110 | 0.069 | 0.189 | 3,408 |

| |$ {{Export \ share}}_{j(i)}^{07}$| | 0.299 | 0.251 | 0.232 | 0.086 | 0.433 | 3,408 |

| |$ {{Cash/Assets}}_i^{07}$| | 0.083 | 0.024 | 0.127 | 0.002 | 0.112 | 3,408 |

| |$ {{Unused \, LC/Assets}}_i^{07}$| | 0.043 | 0.003 | 0.070 | 0.000 | 0.062 | 3,408 |

| ΔCustPDc(i) | 0.708 | 0.651 | 0.134 | 0.628 | 0.749 | 3,408 |

| ΔSalesc(i) | −0.070 | −0.047 | 0.103 | −0.125 | −0.008 | 3,408 |

| |$\Delta {Sales}_{c(i)}^{IV}$| | −0.042 | −0.057 | 0.037 | −0.072 | −0.002 | 3,408 |

| ΔSumInji | 0.115 | 0.000 | 0.744 | 0.000 | 0.000 | 3,408 |

| ΔNoInji | 0.110 | 0.000 | 0.715 | 0.000 | 0.000 | 3,408 |

| C. Time-varying firm characteristics (2004–2011) | ||||||

| Trade credit maturity (|$\hat{\tau }_{i,t}$|) | 0.090 | 0.090 | 0.048 | 0.060 | 0.117 | 18,025 |

| Cash/Assetsi, t | 0.081 | 0.022 | 0.124 | 0.002 | 0.111 | 18,025 |

| Bank debt/Assetsi, t | 0.126 | 0.028 | 0.164 | 0.000 | 0.232 | 18,025 |

| Tangible assets/Assetsi, t | 0.269 | 0.248 | 0.183 | 0.116 | 0.392 | 18,025 |

| Cash flow/Assetsi, t | 0.125 | 0.122 | 0.131 | 0.057 | 0.198 | 18,025 |

| Inventories/Salesi, t | 0.148 | 0.128 | 0.105 | 0.078 | 0.194 | 18,025 |

| Assetsi, t (in SEK 1,000) | 318,984 | 58,994 | 1,018,467 | 26,518 | 164,564 | 18,025 |

| Salesi, t (in SEK 1,000) | 390,197 | 101,013 | 1,003,049 | 45,561 | 258,046 | 18,025 |

| Mean | Median | SD | Pct. 25 | Pct. 75 | No. obs. | |

|---|---|---|---|---|---|---|

| A. Price and quantity variables (2004–2011) | ||||||

| Firm-product inflation rate (πi, p, t) | 0.029 | 0.007 | 0.159 | −0.031 | 0.093 | 45,953 |

| Change in quantity sold (ΔQi, p, t) | −0.007 | 0.005 | 0.442 | −0.147 | 0.154 | 45,953 |

| Change in unit input costs (ΔUICi, p, t) | 0.033 | 0.024 | 0.261 | −0.080 | 0.147 | 45,953 |

| B. Time-invariant firm characteristics (2007) | ||||||

| Trade credit maturity (|$\hat{\tau }_i^{07}$|) | 0.097 | 0.095 | 0.056 | 0.064 | 0.124 | 3,408 |

| |$ {{Inventories/Sales}}_i^{07}$| | 0.142 | 0.124 | 0.110 | 0.069 | 0.189 | 3,408 |

| |$ {{Export \ share}}_{j(i)}^{07}$| | 0.299 | 0.251 | 0.232 | 0.086 | 0.433 | 3,408 |

| |$ {{Cash/Assets}}_i^{07}$| | 0.083 | 0.024 | 0.127 | 0.002 | 0.112 | 3,408 |

| |$ {{Unused \, LC/Assets}}_i^{07}$| | 0.043 | 0.003 | 0.070 | 0.000 | 0.062 | 3,408 |

| ΔCustPDc(i) | 0.708 | 0.651 | 0.134 | 0.628 | 0.749 | 3,408 |

| ΔSalesc(i) | −0.070 | −0.047 | 0.103 | −0.125 | −0.008 | 3,408 |

| |$\Delta {Sales}_{c(i)}^{IV}$| | −0.042 | −0.057 | 0.037 | −0.072 | −0.002 | 3,408 |

| ΔSumInji | 0.115 | 0.000 | 0.744 | 0.000 | 0.000 | 3,408 |

| ΔNoInji | 0.110 | 0.000 | 0.715 | 0.000 | 0.000 | 3,408 |

| C. Time-varying firm characteristics (2004–2011) | ||||||

| Trade credit maturity (|$\hat{\tau }_{i,t}$|) | 0.090 | 0.090 | 0.048 | 0.060 | 0.117 | 18,025 |

| Cash/Assetsi, t | 0.081 | 0.022 | 0.124 | 0.002 | 0.111 | 18,025 |

| Bank debt/Assetsi, t | 0.126 | 0.028 | 0.164 | 0.000 | 0.232 | 18,025 |

| Tangible assets/Assetsi, t | 0.269 | 0.248 | 0.183 | 0.116 | 0.392 | 18,025 |

| Cash flow/Assetsi, t | 0.125 | 0.122 | 0.131 | 0.057 | 0.198 | 18,025 |

| Inventories/Salesi, t | 0.148 | 0.128 | 0.105 | 0.078 | 0.194 | 18,025 |

| Assetsi, t (in SEK 1,000) | 318,984 | 58,994 | 1,018,467 | 26,518 | 164,564 | 18,025 |

| Salesi, t (in SEK 1,000) | 390,197 | 101,013 | 1,003,049 | 45,561 | 258,046 | 18,025 |

Notes: This table reports descriptive statistics for all variables used in the empirical analysis, as well as for some additional firm characteristics. Each firm appears only once in panel B and only once per year in panel C, irrespective of how many products it sells and thus how many firm-product observations it has in a given year. Definitions of the variables are provided in the text.

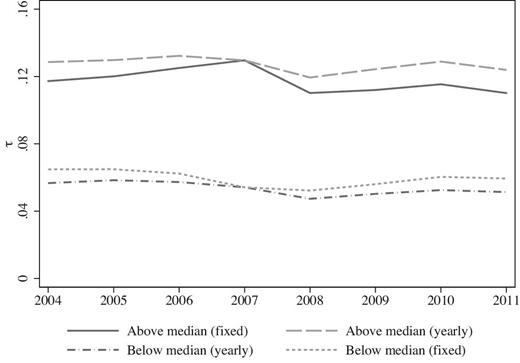

In Figure 2, finally, we document an important feature of trade credit maturities that will help inform our conceptual framework and empirical approach, namely, that maturities are persistent over time. More specifically, the figure plots average trade credit maturities, as measured by |$\hat{\tau }_{i,t}$|, for firms above and below the sample medians of |$\hat{\tau }_{i,t}$| and |$\hat{\tau }_{i}^{07}$|, respectively. Average trade credit maturities are very stable over the period 2004–2011 for both above- and below-median firms when using the yearly classification, whereas above-median firms, as classified based on |$\hat{\tau }_{i}^{07}$|, reduced maturities slightly during the crisis, with |$\hat{\tau }_{i,t}$| falling from 0.129 to 0.112.

Average trade credit maturities over time. The figure shows average trade credit maturities, as measured by |$\hat{\tau }_{i,t}$|, for firms above and below the sample medians of |$\hat{\tau }_{i,t}$| and |$\hat{\tau }_{i}^{07}$|, respectively, over the period 2004–2011. The solid and short-dashed lines show average maturities when the classification of firms is done on a year-by-year basis (|$\hat{\tau }_{i,t}$|), and the long-dashed and dashed-dotted lines when the classification is done based on the trade credit maturity distribution in 2007 (|$\hat{\tau }_{i}^{07}$|).

3. Conceptual Framework and Empirical Approach

3.1. Conceptual Framework

Since lending is associated with costs—most importantly due to funding and to credit risk exposure—prices charged in trade credit transactions likely surpass prices charged in cash transactions. Schwartz (1974) highlights this trade credit feature of price setting and suggests that firms add a trade credit premium to the cash price, determined by the contracted loan maturity and an implicit interest rate, in transactions involving trade credit. Our conceptual framework rests on the relationship proposed by Schwartz and we focus on its implications for the link between firms’ trade credit issuance and pricing decisions.

In line with Schwartz (1974), our hypothesis is that the trade credit interest rate, r, is determined by two factors: (i) the seller’s cost of liquidity and (ii) the risk of the buyer’s default in the transaction.10 That is, the implicit interest rate in product prices is increasing in sellers’ liquidity costs and credit risk exposures, all else equal. The cost of liquidity that applies to the issuance of trade credit is given by the opportunity cost of the marginal unit of liquidity facing a firm—the shadow cost of liquidity—and is thus equal to the external funding cost for financially unconstrained firms, but higher than this for firms that experience binding liquidity constraints due to external finance rationing (Whited 1992). Regarding counterparty risks, the Bankruptcy Code in Sweden provides trade credit debt with junior priority status, which means that sellers have little hope of recovering claims on failed buyers’ bankruptcy estates after prioritized holders of claims have been handled (Thorburn 2000).11 Hence, trade credit lending is associated with substantial credit risk (see Jacobson and von Schedvin (2015), for further empirical evidence on this).

3.2. Baseline Specification

The parameter of interest is β, which captures the difference between crisis and noncrisis years in the extent to which trade credit maturities affected firm-product inflation rates. In particular, on the basis of equation (4) and its embedded assumption of persistence over time in τ, |$\hat{\beta }$| provides an estimate of the difference in Δr between crisis and noncrisis years. Our empirical approach is thus based on the aggregate shocks to liquidity costs and counterparty risk arising in the 2008–2009 recession in Sweden, in combination with the cross-sectional variation in trade credit maturities that prevailed at the outset of this period.12 The underlying idea is twofold. First, as noted previously, the 2008–2009 recession in Sweden featured general and widespread increases in liquidity costs and counterparty risks, which, according to the hypothesis outlined in the previous section, should lead to upward shifts in implicit trade credit interest rates, ri, p. The crisis dummy is thus a proxy that captures the fact that changes in the underlying determinants of ri, p were higher in crisis years than in noncrisis years. Second, an increase in ri, p of a given size will have a greater impact on product prices set by firms that issue trade credit with longer maturities, in accordance with equation (4). Hence, within this framework we can test if product prices include a trade credit price premium by comparing firm-product inflation rates across crisis and noncrisis years, respectively, for firms that issue trade credit with long and short maturities.

3.3. Potential Threats to Identification

The identifying assumption underlying the empirical specification detailed in the previous section is that there are no omitted variables correlated with the interaction term |${\textit {Crisis}}_t \cdot \hat{\tau }_i^{07}$| that affect firm-product inflation rates, conditional on controls. This implies that a potential omitted variable needs to fulfill two conditions to be of concern: it has to be correlated with |$\hat{\tau }_i^{07}$| and its effect on firm-product inflation rates must vary between crisis and noncrisis years. Now, since our identifying variation is given by the cross-sectional differences in trade credit maturities that prevailed at the outset of the crisis, |$\hat{\tau }_i^{07}$|, and not by variation stemming from an exogenous shock, it is important to probe the sources of the variation in maturities. To this end, we compare firms with average trade credit maturities above and below the sample median, respectively, on all firm-level covariates used in the empirical analysis, measured in 2007. The comparison is conducted on the basis of four measures of covariate balance proposed by Imbens and Rubin (2015): normalized differences in means, logs of the ratios of standard deviations, and two measures of coverage frequency. The results of this comparison, presented in Table 2, show that firms issuing trade credit with long and short maturities are similar across the entire set of covariates under consideration.13 This is consistent with the findings in the previous literature, which has struggled to provide unambiguous evidence regarding the determinants of variation in trade credit maturities across sellers (see Ellingsen, Jacobson, and von Schedvin 2016 for empirical evidence and a review of the literature).

Covariate balance in the sample.

| A. High |$\hat{\tau }_i^{07}$| | B. Low |$\hat{\tau }_i^{07}$| | C. Covariate balance measures | ||||||

|---|---|---|---|---|---|---|---|---|

| Mean | SD | Mean | SD | Δh − l | Γh/ℓ | |$\pi _h^{.95}$| | |$\pi _\ell ^{.95}$| | |

| |${{Cash/Assets}}_i^{07}$| | 0.076 | 0.112 | 0.091 | 0.141 | −0.110 | −0.235 | 0.938 | 0.991 |

| |${{Bank \, debt/Assets}}_i^{07}$| | 0.146 | 0.165 | 0.111 | 0.159 | 0.217 | 0.038 | 0.976 | 0.971 |

| |${{Tangible \, assets/Assets}}_i^{07}$| | 0.235 | 0.174 | 0.270 | 0.195 | −0.190 | −0.116 | 0.912 | 0.974 |

| |${{Cash \, flow/Assets}}_i^{07}$| | 0.139 | 0.127 | 0.145 | 0.149 | −0.043 | −0.160 | 0.914 | 0.974 |

| |${{Inventories/Sales}}_i^{07}$| | 0.150 | 0.109 | 0.134 | 0.111 | 0.141 | −0.023 | 0.906 | 0.974 |

| |$\ln ( {Assets}_i^{07})$| | 10.947 | 1.281 | 11.166 | 1.585 | −0.153 | −0.213 | 0.877 | 0.983 |

| |${{Export \, share}}_{j(i)}^{07}$| | 0.305 | 0.229 | 0.293 | 0.234 | 0.052 | −0.019 | 0.950 | 0.966 |

| |${{Unused \, LC/Assets}}_i^{07}$| | 0.047 | 0.071 | 0.039 | 0.068 | 0.115 | 0.045 | 0.977 | 0.974 |

| ΔCustPDc(i) | 0.707 | 0.134 | 0.710 | 0.133 | −0.021 | 0.012 | 0.964 | 0.890 |

| ΔSalesc(i) | −0.083 | 0.100 | −0.056 | 0.105 | −0.264 | −0.048 | 0.856 | 0.955 |

| ΔSumInji | 0.121 | 0.740 | 0.108 | 0.748 | 0.018 | −0.011 | 1.000 | 1.000 |

| ΔNoInji | 0.119 | 0.705 | 0.100 | 0.725 | 0.027 | −0.029 | 1.000 | 1.000 |

| No. firms | 1,752 | 1,656 | ||||||

| A. High |$\hat{\tau }_i^{07}$| | B. Low |$\hat{\tau }_i^{07}$| | C. Covariate balance measures | ||||||

|---|---|---|---|---|---|---|---|---|

| Mean | SD | Mean | SD | Δh − l | Γh/ℓ | |$\pi _h^{.95}$| | |$\pi _\ell ^{.95}$| | |

| |${{Cash/Assets}}_i^{07}$| | 0.076 | 0.112 | 0.091 | 0.141 | −0.110 | −0.235 | 0.938 | 0.991 |

| |${{Bank \, debt/Assets}}_i^{07}$| | 0.146 | 0.165 | 0.111 | 0.159 | 0.217 | 0.038 | 0.976 | 0.971 |

| |${{Tangible \, assets/Assets}}_i^{07}$| | 0.235 | 0.174 | 0.270 | 0.195 | −0.190 | −0.116 | 0.912 | 0.974 |

| |${{Cash \, flow/Assets}}_i^{07}$| | 0.139 | 0.127 | 0.145 | 0.149 | −0.043 | −0.160 | 0.914 | 0.974 |

| |${{Inventories/Sales}}_i^{07}$| | 0.150 | 0.109 | 0.134 | 0.111 | 0.141 | −0.023 | 0.906 | 0.974 |

| |$\ln ( {Assets}_i^{07})$| | 10.947 | 1.281 | 11.166 | 1.585 | −0.153 | −0.213 | 0.877 | 0.983 |

| |${{Export \, share}}_{j(i)}^{07}$| | 0.305 | 0.229 | 0.293 | 0.234 | 0.052 | −0.019 | 0.950 | 0.966 |

| |${{Unused \, LC/Assets}}_i^{07}$| | 0.047 | 0.071 | 0.039 | 0.068 | 0.115 | 0.045 | 0.977 | 0.974 |

| ΔCustPDc(i) | 0.707 | 0.134 | 0.710 | 0.133 | −0.021 | 0.012 | 0.964 | 0.890 |

| ΔSalesc(i) | −0.083 | 0.100 | −0.056 | 0.105 | −0.264 | −0.048 | 0.856 | 0.955 |

| ΔSumInji | 0.121 | 0.740 | 0.108 | 0.748 | 0.018 | −0.011 | 1.000 | 1.000 |

| ΔNoInji | 0.119 | 0.705 | 0.100 | 0.725 | 0.027 | −0.029 | 1.000 | 1.000 |

| No. firms | 1,752 | 1,656 | ||||||

Notes: This table reports descriptive statistics for firms with average trade credit maturities, |$\hat{\tau }_{i}^{07}$|, above and below the sample median (panels A and B), as well as four measures of covariate balance proposed by Imbens and Rubin (2015) (panel C). The set of covariates comprises all firm-level control variables, measured in 2007, as well as all sample-split variables used in the empirical analysis. Δh − ℓ denotes a normalized difference and is calculated as |$(\bar{X}_h-\bar{X}_\ell) / \sqrt{( S_h^2+S_\ell ^2) /2}$|, where |$\bar{X}$| is the mean, S is the standard deviation, and subindices h and ℓ denote firms with trade credit maturities above and below the sample median, respectively. Γh/ℓ is the log of the ratio of the standard deviations for above-median and below-median firms. Finally, |$\pi _h^{.95}$| measures the share of below-median firms for which the value of a given variable lies in the 95% central range of the distribution of the same variable for above-median firms (and vice versa for |$\pi _\ell ^{.95}$|).

Covariate balance in the sample.

| A. High |$\hat{\tau }_i^{07}$| | B. Low |$\hat{\tau }_i^{07}$| | C. Covariate balance measures | ||||||

|---|---|---|---|---|---|---|---|---|

| Mean | SD | Mean | SD | Δh − l | Γh/ℓ | |$\pi _h^{.95}$| | |$\pi _\ell ^{.95}$| | |

| |${{Cash/Assets}}_i^{07}$| | 0.076 | 0.112 | 0.091 | 0.141 | −0.110 | −0.235 | 0.938 | 0.991 |

| |${{Bank \, debt/Assets}}_i^{07}$| | 0.146 | 0.165 | 0.111 | 0.159 | 0.217 | 0.038 | 0.976 | 0.971 |

| |${{Tangible \, assets/Assets}}_i^{07}$| | 0.235 | 0.174 | 0.270 | 0.195 | −0.190 | −0.116 | 0.912 | 0.974 |

| |${{Cash \, flow/Assets}}_i^{07}$| | 0.139 | 0.127 | 0.145 | 0.149 | −0.043 | −0.160 | 0.914 | 0.974 |

| |${{Inventories/Sales}}_i^{07}$| | 0.150 | 0.109 | 0.134 | 0.111 | 0.141 | −0.023 | 0.906 | 0.974 |

| |$\ln ( {Assets}_i^{07})$| | 10.947 | 1.281 | 11.166 | 1.585 | −0.153 | −0.213 | 0.877 | 0.983 |

| |${{Export \, share}}_{j(i)}^{07}$| | 0.305 | 0.229 | 0.293 | 0.234 | 0.052 | −0.019 | 0.950 | 0.966 |

| |${{Unused \, LC/Assets}}_i^{07}$| | 0.047 | 0.071 | 0.039 | 0.068 | 0.115 | 0.045 | 0.977 | 0.974 |

| ΔCustPDc(i) | 0.707 | 0.134 | 0.710 | 0.133 | −0.021 | 0.012 | 0.964 | 0.890 |

| ΔSalesc(i) | −0.083 | 0.100 | −0.056 | 0.105 | −0.264 | −0.048 | 0.856 | 0.955 |

| ΔSumInji | 0.121 | 0.740 | 0.108 | 0.748 | 0.018 | −0.011 | 1.000 | 1.000 |

| ΔNoInji | 0.119 | 0.705 | 0.100 | 0.725 | 0.027 | −0.029 | 1.000 | 1.000 |

| No. firms | 1,752 | 1,656 | ||||||

| A. High |$\hat{\tau }_i^{07}$| | B. Low |$\hat{\tau }_i^{07}$| | C. Covariate balance measures | ||||||

|---|---|---|---|---|---|---|---|---|

| Mean | SD | Mean | SD | Δh − l | Γh/ℓ | |$\pi _h^{.95}$| | |$\pi _\ell ^{.95}$| | |

| |${{Cash/Assets}}_i^{07}$| | 0.076 | 0.112 | 0.091 | 0.141 | −0.110 | −0.235 | 0.938 | 0.991 |

| |${{Bank \, debt/Assets}}_i^{07}$| | 0.146 | 0.165 | 0.111 | 0.159 | 0.217 | 0.038 | 0.976 | 0.971 |

| |${{Tangible \, assets/Assets}}_i^{07}$| | 0.235 | 0.174 | 0.270 | 0.195 | −0.190 | −0.116 | 0.912 | 0.974 |

| |${{Cash \, flow/Assets}}_i^{07}$| | 0.139 | 0.127 | 0.145 | 0.149 | −0.043 | −0.160 | 0.914 | 0.974 |

| |${{Inventories/Sales}}_i^{07}$| | 0.150 | 0.109 | 0.134 | 0.111 | 0.141 | −0.023 | 0.906 | 0.974 |

| |$\ln ( {Assets}_i^{07})$| | 10.947 | 1.281 | 11.166 | 1.585 | −0.153 | −0.213 | 0.877 | 0.983 |

| |${{Export \, share}}_{j(i)}^{07}$| | 0.305 | 0.229 | 0.293 | 0.234 | 0.052 | −0.019 | 0.950 | 0.966 |

| |${{Unused \, LC/Assets}}_i^{07}$| | 0.047 | 0.071 | 0.039 | 0.068 | 0.115 | 0.045 | 0.977 | 0.974 |

| ΔCustPDc(i) | 0.707 | 0.134 | 0.710 | 0.133 | −0.021 | 0.012 | 0.964 | 0.890 |

| ΔSalesc(i) | −0.083 | 0.100 | −0.056 | 0.105 | −0.264 | −0.048 | 0.856 | 0.955 |

| ΔSumInji | 0.121 | 0.740 | 0.108 | 0.748 | 0.018 | −0.011 | 1.000 | 1.000 |

| ΔNoInji | 0.119 | 0.705 | 0.100 | 0.725 | 0.027 | −0.029 | 1.000 | 1.000 |

| No. firms | 1,752 | 1,656 | ||||||

Notes: This table reports descriptive statistics for firms with average trade credit maturities, |$\hat{\tau }_{i}^{07}$|, above and below the sample median (panels A and B), as well as four measures of covariate balance proposed by Imbens and Rubin (2015) (panel C). The set of covariates comprises all firm-level control variables, measured in 2007, as well as all sample-split variables used in the empirical analysis. Δh − ℓ denotes a normalized difference and is calculated as |$(\bar{X}_h-\bar{X}_\ell) / \sqrt{( S_h^2+S_\ell ^2) /2}$|, where |$\bar{X}$| is the mean, S is the standard deviation, and subindices h and ℓ denote firms with trade credit maturities above and below the sample median, respectively. Γh/ℓ is the log of the ratio of the standard deviations for above-median and below-median firms. Finally, |$\pi _h^{.95}$| measures the share of below-median firms for which the value of a given variable lies in the 95% central range of the distribution of the same variable for above-median firms (and vice versa for |$\pi _\ell ^{.95}$|).

We assess potential threats to the identifying assumption in the following ways. First, we estimate the baseline specification augmented with, in turn, product-year fixed effects and industry-year fixed effects, which means that we effectively compare firms with high and low trade credit issuance selling the same product, or operating in the same industry, in a given year. These specifications thus address threats from the set of potentially confounding factors suggested by theories that posit that trade credit maturities are determined by product- or industry-specific factors (e.g., Lee and Stowe 1993; Long, Malitz, and Ravid 1993; Kim and Shin 2012; Kalemli-Özcan et al. 2014). Second, we estimate the baseline specification augmented with interactions between the crisis variable and specific potential confounders that can vary within product and industry clusters, and which are therefore not absorbed by product-year or industry-year fixed effects. Third, we address an alternative explanation for why trade credit issuance and prices may be positively related during periods of tight credit. Suppose that demand increases for goods sold by firms issuing trade credit with longer maturities as a consequence of trade credit becoming more valuable for buyers when other sources of financing dry up. Increased demand could then push up the prices set by these firms relative to the prices of firms that provide short maturities. To distinguish between the demand- and supply-side explanations, we estimate a version of the baseline specification with changes in the quantities of goods sold replacing changes in prices as outcome variable; if the explanation based on demand is correct, we should observe an increase in both prices and quantities for goods sold by firms that issue long trade credit maturities, whereas we would observe higher prices, but lower or unchanged quantities if the effects are supply-driven.

4. Main Results

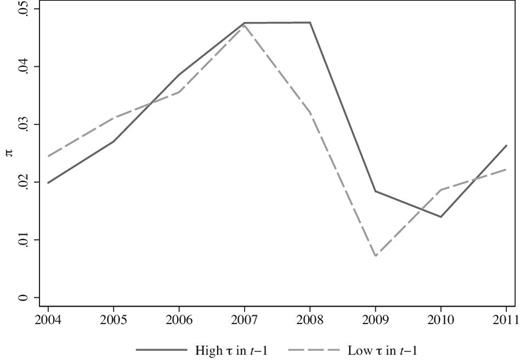

We begin the presentation of our empirical findings with a graphical illustration of our main result. Figure 3 shows average firm-product inflation rates over the period 2004–2011 for firms with average trade credit maturities above (solid line) and below (dashed line) the sample median in year t − 1. Inflation rates for the two groups of firms track each other closely in the four years leading up to the 2008–2009 recession, but then differ markedly during the crisis: although the average inflation rate falls in both groups of firms—which is what one would expect in a crisis period with deflationary pressures—it falls considerably less among firms that issue long trade credit maturities. In the post-crisis period, the inflation rates in the two groups of firms begin to follow each other more closely again. Figure 3 thus provides illustrative evidence for our hypothesis that increases in liquidity costs and counterparty risk lead firms to raise trade credit premia and thereby product prices. In what follows, we formalize this result by means of the empirical strategy outlined in the previous section.

Average firm-product inflation rates over time. The figure shows average firm-product inflation rates in each year of the sample period for firms above (solid line) and below (dashed line) the median of the trade credit maturity distribution in year t − 1, |$\hat{\tau }_{i,t-1}$|.

4.1. Baseline Results and Robustness Checks

Table 3 reports results for various estimations of the model specified in equation (5). We quantify the magnitude of the coefficients for the main explanatory variable, the interaction term |${\textit {Crisis}}_t \cdot \hat{\tau }_i^{07}$|, in two ways. First, we report the coefficients themselves, which, as noted previously, capture the difference in Δr between crisis and noncrisis years. Second, we calculate what the coefficients imply in terms of the difference in annual firm-product inflation rates between firms that issue long and short trade credit maturities by multiplying the coefficient with the difference in |$\hat{\tau }_i^{07}$| between firms located at the 75th and 25th percentiles, respectively, of the |$\hat{\tau }_i^{07}$|-distribution.14

Baseline results.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | |

|---|---|---|---|---|---|---|---|---|---|---|

| πi, p, t | πi, p, t | πi, p, t | |$\pi _{i,p,t}^{+}$| | πi, p, t | πi, p, t | πi, p, t | πi, p, t | πi, p, t | ΔQi, p, t | |

| |${{Crisis}}_t \cdot \hat{\tau }_i^{07}$| | 0.209*** | 0.154*** | 0.415** | 0.232*** | 0.125** | 0.182*** | 0.214*** | 0.230*** | −0.008 | |

| (3.4) | (3.2) | (2.4) | (3.9) | (2.5) | (3.4) | (3.6) | (3.8) | (−0.1) | ||

| |${{Crisis}}_t \cdot \hat{\tau }_i^{07}, {{High}}$| | 0.018*** | |||||||||

| (2.8) | ||||||||||

| |${{Crisis}}_t \cdot {{Export}} \ {{share}}_{j}^{07}$| | −0.046*** | |||||||||

| (−3.4) | ||||||||||

| |${{Crisis}}_t \cdot {{Inventories/Sales}}_{i}^{07}$| | −0.083*** | |||||||||

| (−2.9) | ||||||||||

| High versus low |$\hat{\tau }_i^{07}$| | 0.013 | 0.009 | — | 0.025 | 0.014 | 0.008 | 0.011 | 0.013 | 0.014 | 0.000 |

| Firm×product FE | Yes | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes |

| Product×year and firm FE | No | No | No | No | No | Yes | No | No | No | No |

| Industry×year FE | No | No | No | No | No | No | Yes | No | No | No |

| Firm- and product-level controls | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes | Yes |

| Weights | No | Yes | No | No | No | No | No | No | No | No |

| R2 | 0.429 | 0.420 | 0.429 | 0.319 | 0.214 | 0.590 | 0.458 | 0.430 | 0.429 | 0.306 |

| No. firms | 3,408 | 3,408 | 3,408 | 3,408 | 3,408 | 3,174 | 3,401 | 3,408 | 3,408 | 3,408 |

| No. observations | 45,953 | 45,953 | 45,953 | 45,953 | 45,953 | 35,971 | 45,921 | 45,953 | 45,953 | 45,953 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | |

|---|---|---|---|---|---|---|---|---|---|---|

| πi, p, t | πi, p, t | πi, p, t | |$\pi _{i,p,t}^{+}$| | πi, p, t | πi, p, t | πi, p, t | πi, p, t | πi, p, t | ΔQi, p, t | |

| |${{Crisis}}_t \cdot \hat{\tau }_i^{07}$| | 0.209*** | 0.154*** | 0.415** | 0.232*** | 0.125** | 0.182*** | 0.214*** | 0.230*** | −0.008 | |

| (3.4) | (3.2) | (2.4) | (3.9) | (2.5) | (3.4) | (3.6) | (3.8) | (−0.1) | ||

| |${{Crisis}}_t \cdot \hat{\tau }_i^{07}, {{High}}$| | 0.018*** | |||||||||

| (2.8) | ||||||||||

| |${{Crisis}}_t \cdot {{Export}} \ {{share}}_{j}^{07}$| | −0.046*** | |||||||||

| (−3.4) | ||||||||||

| |${{Crisis}}_t \cdot {{Inventories/Sales}}_{i}^{07}$| | −0.083*** | |||||||||

| (−2.9) | ||||||||||

| High versus low |$\hat{\tau }_i^{07}$| | 0.013 | 0.009 | — | 0.025 | 0.014 | 0.008 | 0.011 | 0.013 | 0.014 | 0.000 |

| Firm×product FE | Yes | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes |

| Product×year and firm FE | No | No | No | No | No | Yes | No | No | No | No |

| Industry×year FE | No | No | No | No | No | No | Yes | No | No | No |

| Firm- and product-level controls | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes | Yes |

| Weights | No | Yes | No | No | No | No | No | No | No | No |

| R2 | 0.429 | 0.420 | 0.429 | 0.319 | 0.214 | 0.590 | 0.458 | 0.430 | 0.429 | 0.306 |

| No. firms | 3,408 | 3,408 | 3,408 | 3,408 | 3,408 | 3,174 | 3,401 | 3,408 | 3,408 | 3,408 |

| No. observations | 45,953 | 45,953 | 45,953 | 45,953 | 45,953 | 35,971 | 45,921 | 45,953 | 45,953 | 45,953 |

Notes: This table reports results for estimations of various specifications based on equation (5). The dependent variable is the firm-product inflation rate, πi, p, t, in all specifications except those in column (4), where it is a dummy equal to one for price increases and zero otherwise, and in column (7), in which it is the change in the quantity of goods sold, ΔQi, p, t. The regression in column (2) is estimated using WLS, where the weight for each observation, ωi, p, t, is calculated as firm i’s sales of product p divided by firm i’s total sales in year t. The product fixed effects are based on 8/9-digit CN codes and the industry fixed effects on three-digit SNI/NACE codes. All regressions include year fixed effects except that in column (7), in which they are redundant. High versus low |$\hat{\tau }_i^{07}$| is calculated as the estimated difference in the dependent variable between firms located at the 75th and 25th percentiles of the |$\hat{\tau }_i^{07}$|-distribution. The estimation period is 2004–2011 in all columns. t-statistics calculated using robust standard errors clustered at the firm-level are reported in parentheses. **Significant at 5%; ***Significant at 1%.

Baseline results.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | |

|---|---|---|---|---|---|---|---|---|---|---|

| πi, p, t | πi, p, t | πi, p, t | |$\pi _{i,p,t}^{+}$| | πi, p, t | πi, p, t | πi, p, t | πi, p, t | πi, p, t | ΔQi, p, t | |

| |${{Crisis}}_t \cdot \hat{\tau }_i^{07}$| | 0.209*** | 0.154*** | 0.415** | 0.232*** | 0.125** | 0.182*** | 0.214*** | 0.230*** | −0.008 | |

| (3.4) | (3.2) | (2.4) | (3.9) | (2.5) | (3.4) | (3.6) | (3.8) | (−0.1) | ||

| |${{Crisis}}_t \cdot \hat{\tau }_i^{07}, {{High}}$| | 0.018*** | |||||||||

| (2.8) | ||||||||||

| |${{Crisis}}_t \cdot {{Export}} \ {{share}}_{j}^{07}$| | −0.046*** | |||||||||

| (−3.4) | ||||||||||

| |${{Crisis}}_t \cdot {{Inventories/Sales}}_{i}^{07}$| | −0.083*** | |||||||||

| (−2.9) | ||||||||||

| High versus low |$\hat{\tau }_i^{07}$| | 0.013 | 0.009 | — | 0.025 | 0.014 | 0.008 | 0.011 | 0.013 | 0.014 | 0.000 |

| Firm×product FE | Yes | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes |

| Product×year and firm FE | No | No | No | No | No | Yes | No | No | No | No |

| Industry×year FE | No | No | No | No | No | No | Yes | No | No | No |

| Firm- and product-level controls | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes | Yes |

| Weights | No | Yes | No | No | No | No | No | No | No | No |

| R2 | 0.429 | 0.420 | 0.429 | 0.319 | 0.214 | 0.590 | 0.458 | 0.430 | 0.429 | 0.306 |

| No. firms | 3,408 | 3,408 | 3,408 | 3,408 | 3,408 | 3,174 | 3,401 | 3,408 | 3,408 | 3,408 |

| No. observations | 45,953 | 45,953 | 45,953 | 45,953 | 45,953 | 35,971 | 45,921 | 45,953 | 45,953 | 45,953 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | |

|---|---|---|---|---|---|---|---|---|---|---|

| πi, p, t | πi, p, t | πi, p, t | |$\pi _{i,p,t}^{+}$| | πi, p, t | πi, p, t | πi, p, t | πi, p, t | πi, p, t | ΔQi, p, t | |

| |${{Crisis}}_t \cdot \hat{\tau }_i^{07}$| | 0.209*** | 0.154*** | 0.415** | 0.232*** | 0.125** | 0.182*** | 0.214*** | 0.230*** | −0.008 | |

| (3.4) | (3.2) | (2.4) | (3.9) | (2.5) | (3.4) | (3.6) | (3.8) | (−0.1) | ||

| |${{Crisis}}_t \cdot \hat{\tau }_i^{07}, {{High}}$| | 0.018*** | |||||||||

| (2.8) | ||||||||||

| |${{Crisis}}_t \cdot {{Export}} \ {{share}}_{j}^{07}$| | −0.046*** | |||||||||

| (−3.4) | ||||||||||

| |${{Crisis}}_t \cdot {{Inventories/Sales}}_{i}^{07}$| | −0.083*** | |||||||||

| (−2.9) | ||||||||||

| High versus low |$\hat{\tau }_i^{07}$| | 0.013 | 0.009 | — | 0.025 | 0.014 | 0.008 | 0.011 | 0.013 | 0.014 | 0.000 |

| Firm×product FE | Yes | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes |

| Product×year and firm FE | No | No | No | No | No | Yes | No | No | No | No |

| Industry×year FE | No | No | No | No | No | No | Yes | No | No | No |

| Firm- and product-level controls | Yes | Yes | Yes | Yes | No | Yes | Yes | Yes | Yes | Yes |

| Weights | No | Yes | No | No | No | No | No | No | No | No |

| R2 | 0.429 | 0.420 | 0.429 | 0.319 | 0.214 | 0.590 | 0.458 | 0.430 | 0.429 | 0.306 |

| No. firms | 3,408 | 3,408 | 3,408 | 3,408 | 3,408 | 3,174 | 3,401 | 3,408 | 3,408 | 3,408 |

| No. observations | 45,953 | 45,953 | 45,953 | 45,953 | 45,953 | 35,971 | 45,921 | 45,953 | 45,953 | 45,953 |

Notes: This table reports results for estimations of various specifications based on equation (5). The dependent variable is the firm-product inflation rate, πi, p, t, in all specifications except those in column (4), where it is a dummy equal to one for price increases and zero otherwise, and in column (7), in which it is the change in the quantity of goods sold, ΔQi, p, t. The regression in column (2) is estimated using WLS, where the weight for each observation, ωi, p, t, is calculated as firm i’s sales of product p divided by firm i’s total sales in year t. The product fixed effects are based on 8/9-digit CN codes and the industry fixed effects on three-digit SNI/NACE codes. All regressions include year fixed effects except that in column (7), in which they are redundant. High versus low |$\hat{\tau }_i^{07}$| is calculated as the estimated difference in the dependent variable between firms located at the 75th and 25th percentiles of the |$\hat{\tau }_i^{07}$|-distribution. The estimation period is 2004–2011 in all columns. t-statistics calculated using robust standard errors clustered at the firm-level are reported in parentheses. **Significant at 5%; ***Significant at 1%.

The baseline result is reported in column (1). The coefficient on the interaction term |${\textit {Crisis}}_t \cdot \hat{\tau }_i^{07}$| is positive and statistically significant, which suggests that firm-product inflation rates are increasing in trade credit maturities in the crisis period. The magnitude of the coefficient shows that Δr on average was 20.9 percentage points higher during the crisis than in noncrisis years.15 This estimate implies that the difference in annual firm-product inflation rates between firms that issue long and short trade credit maturities was 1.3 percentage points higher in crisis years than in noncrisis years.

Next, we re-estimate the baseline specification using weights that adjust for differences in the shares of each firm’s total sales accounted for by each of its products. More specifically, we estimate a weighted regression where the weight for each observation, ωi, p, t, is calculated as firm i’s sales of product p divided by firm i’s total sales. Hence, we effectively estimate the baseline regression at the firm level instead of at the firm-product level. The results are reported in column (2). The coefficient on the interaction term |${\textit {Crisis}}_t \cdot \hat{\tau }_i^{07}$| implies a difference in Δr of 15.4 percentage points and a difference in the annual firm-product inflation rate between firms that issue long and short trade credit maturities of 0.9 percentage points, which is slightly lower than in the previous specification. This suggests that sellers with more diversified product portfolios tend to make slightly larger price adjustments on average.

Although we winsorize all variables used in the estimations to reduce the influence of outliers, one may still be concerned that a small number of firms with very long trade credit maturities could influence the results unduly. We therefore estimate a version of the baseline specification in which the main explanatory variable is a dummy indicating whether a firm’s trade credit maturity was above or below the sample median in the last precrisis year. The results, reported in column (3), show that the difference in inflation rates between firms above and below the sample median of the trade credit maturity distribution was 1.8 percentage points higher in crisis years, which is consistent with the baseline result. Similarly, one may be concerned that a small number of very large price adjustments drive the baseline result. To address this, we estimate a version of the baseline specification in which the dependent variable is replaced by a dummy that takes the value one for price increases, and zero otherwise. The coefficient, reported in column (4), implies that the relative propensity of firms that issue long and short trade credit maturities to increase prices was 2.5 percentage points higher in crisis years. These findings suggest that outliers are not a concern for the baseline result.

4.2. Accounting for Alternative Explanations

In the remainder of this section we assess the plausibility of several alternative explanations for our results, by means of variations on the baseline specification. We begin by considering a bivariate regression specification, in which we drop all firm- and product-level control variables except the firm-product and year fixed effects. The purpose is to examine how the inclusion of the control variables in the vectors |${\bf{X}_{i,p,t}}$| and |${\bf{Z}_{i,t-1}}$| affect the baseline estimate, which is helpful for assessing the extent to which unobservables may confound our findings. The results of this exercise are reported in column (5) of Table 3. The point estimate (t-statistic) for the coefficient of interest is 0.232 (3.9), which is very close to the baseline coefficient, whereas R2 drops from 0.429 to 0.214. This indicates that although the firm- and product-level control variables add substantial explanatory power to the regression, their effect on the coefficient of interest is small, which is what one would expect given the similarity of firms that issue high and low trade credit maturities.

Next, the baseline specification includes firm-product fixed effects to control for time-invariant differences in inflation rates across products. Hypothetically, time-varying differences in inflation rates across products could be important: supposing that inflation rates during the crisis were higher for certain products, for reasons unrelated to trade credit issuance, and that the same products are customarily sold with long trade credit maturities, then our baseline result could be spurious. To address this possibility, we estimate a specification in which we replace the firm-product fixed effects with firm fixed effects and product-year fixed effects to control for the part of the variation in the inflation rate that is common to all producers of a given product. The resulting coefficient, reported in column (6), is positive and statistically significant, but its magnitude is only around three-fifths of the magnitude of the baseline coefficient, which suggests that our baseline result is partly associated with time-varying product-specific factors. Note, however, that the sample size falls by more than 20% in this estimation. This reduction occurs because many products are produced by only one firm in a given year and we can only make use of observations belonging to product-year cells with at least two observations in a specification with product-year fixed effects. Hence, the decline in effect magnitude—from 0.209 to 0.125—could be due to some combination of the change in sample composition and the introduction of product-year fixed effects. To test for the sample composition effect, we re-estimate the baseline specification on the subsample comprising observations belonging to product-year cells with at least two observations. This yields a coefficient estimate of 0.168 (3.4), which indicates that one half of the decline in the estimated coefficient can be attributed to the sample composition effect and the other half to the introduction of product-year fixed effects.

On a related note, we assess whether time-varying differences in inflation rates across industries could affect our results. We do this by estimating the baseline specification augmented with industry-year fixed effects, where industries are defined using two-digit SNI/NACE codes. The coefficient on the interaction term |${\textit {Crisis}}_t \cdot \hat{\tau }_i^{07}$|, reported in column (7), implies a difference in Δr of 18.2 percentage points and in the annual firm-product inflation rate between firms that issue long and short trade credit maturities of 1.1 percentage points.

The collapse of world trade that occurred during the global financial crisis had a large adverse impact on Sweden, a small open economy in which exports account for almost half of GDP. This could potentially influence our results, since (i) international trade typically is associated with longer trade credit maturities and (ii) exporting firms faced a substantial drop in demand during the crisis. We control for the potential influence of export demand by augmenting the baseline specification with an interaction term between the crisis dummy and a variable measuring the precrisis export share of total sales at the five-digit industry level, |${\textit {Export}}\ {\textit {share}}_j^{07}$|. The results of this estimation, reported in column (8), show that the coefficient on trade credit maturities is virtually unchanged compared with the baseline specification, whereas the coefficient on the export share is negative and statistically significant, which is what one would expect given the large decline in export demand during the crisis.

Next, some theories of trade credit predict that accounts receivable are negatively correlated with inventory holdings (see, e.g., Bougheas, Mateut, and Mizen 2009). Such a correlation could give rise to bias in our baseline estimates, if the size of a firm’s inventory holdings has a direct impact on its price setting during economic downturns. To examine this possibility, we estimate a version of the baseline specification in which the ratio of precrisis inventories to sales interacted with the crisis dummy is included as a control variable. The results of this estimation are reported in column (9). The coefficient for trade credit maturity is slightly larger than the baseline estimate, whereas the coefficient for inventories is negative and statistically significant, which suggests that firms that entered the crisis with high inventory holdings attempted to reduce these through price cuts. The different signs of the estimated effects of trade credit and inventories indicate that the mechanism that we document in this paper is specific to trade credit provisioning, and not merely an instance of a more general working capital channel.

Finally, another conceivable alternative explanation for our baseline finding is that it reflects a shift in demand during the crisis—away from sellers that issue short trade credit maturities and toward sellers that issue long maturities—as a result of longer trade credit maturities becoming more valuable for liquidity-constrained buyers during crises. To evaluate the demand-shift explanation, we regress the change in the quantity of sold goods, ΔQi, p, t, on the right-hand side of the baseline specification. The idea is that an upward shift in demand for goods sold by firms that issue long trade credit maturities should cause an increase in both prices and quantities. column (10) shows, however, that the coefficient in this specification is negative and insignificant, which speaks against the alternative explanation based on shifts in demand.

5. Mechanisms

In this section we propose to scrutinize the underlying mechanisms for the baseline finding that firms issuing longer trade credit maturities tended to raise product prices more during the crisis. Thus, we conjecture—in accordance with the hypothesis outlined in the conceptual framework—that the association between trade credit issuance and price changes is stronger for firms subject to larger increases in liquidity costs and counterparty risk. To this end, we conduct cross-sectional heterogeneity analyses, in which we estimate the baseline specification on subsamples of firms defined by proxies for changes in liquidity costs and counterparty risk during the crisis. The proxies we use capture firm characteristics obtaining in the crisis and we therefore restrict the sample period to 2006–2009 throughout this section.

5.1. The Liquidity-Cost Mechanism

We use two approaches to identify firms that experienced particularly large increases in liquidity costs during the crisis. First, we follow a common practice in the literature and identify firms based on precrisis characteristics that are likely to have been important determinants of their liquidity costs during the crisis. Second, we use the Baltic crisis and its detrimental effect on two Swedish banks as a quasi-experiment along the lines of Chodorow-Reich (2014).

5.1.1. Results Based on Precrisis Characteristics

We consider two measures of firms’ precrisis liquidity positions as sources of heterogeneity in liquidity costs across sellers during the crisis: cash and liquid assets, |${\textit {Cash}}/{\textit {Assets}}_{i,t-1}^{07}$|; and the size of unused credit lines, |${\textit {Unused}} \ {\textit {LC/Assets}}_{i,t-1}^{07}$|. For each variable, we construct two subsamples: one with the firms in the bottom three deciles and one with the firms in the top three deciles, the former of which corresponds to firms experiencing large increases in liquidity costs during the crisis, and the latter to firms for which this increase was smaller.16 The presumption underlying this exercise is that firms with weaker precrisis liquidity positions were more vulnerable to deteriorations in cash flow and access to external finance during the crisis, and therefore subject to larger increases in liquidity costs (see, e.g., Duchin, Ozbas, and Sensoy 2010; Gilchrist et al. 2017). Hence, we should observe a stronger relationship between trade credit maturities and price changes during the crisis in the group of vulnerable firms.

The results of the exercises based on firms’ precrisis liquidity positions are reported in panel A of Table 4. column (1) covers results for the sample splits based on the |${\textit {Cash}}/{\textit {Assets}}_{i,t-1}^{07}$| distribution. The coefficient is large and statistically significant for firms with low precrisis cash holdings, but small and statistically insignificant for firms with high precrisis cash holdings; the difference is statistically significant at the 1% level in a one-sided test. A similar pattern emerges in column (3), where we report the results for subsamples of firms with credit lines in the bottom and top of the |${\textit {Unused}} \ {\textit {LC/Assets}}_{i,t-1}^{07}$| distribution: the coefficient is large and significant in the former group, but smaller and insignificant in the latter; the difference is in this case statistically significant at the 10% level. These results thus support the notion that increases in liquidity costs partly account for the baseline relationship between trade credit issuance and price changes.

Mechanism I—Liquidity cost pass-through.

| (1) | (2) | ||

|---|---|---|---|

| |${{Cash/Assets}}_{i}^{07}$| | |${{Unused \, LC/Assets}}_{i}^{07}$| | ||

| Panel A. Precrisis balance-sheet measures | |||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot {\mathbb 1} \lbrace T_i \ge T^{70th} \rbrace$| | 0.024 | 0.081 | |

| (0.2) | (0.7) | ||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i \le T^{30th} \rbrace$| | 0.508*** | 0.307*** | |

| (4.3) | (3.3) | ||

| p-value for difference | 0.005 | 0.070 | |

| R2 | 0.246 | 0.262 | |

| No. firms in top/bottom deciles | 770/783 | 799/1,001 | |

| No. observations | 12,248 | 13,436 | |

| (1) | (2) | (3) | |

| All firms | Single-bank firms | Single-bank firms, not with D | |

| Panel B. The Baltic crisis experiment | |||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i=0 \rbrace$| | 0.210** | 0.192* | 0.172 |

| (2.1) | (1.7) | (1.3) | |

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i=1 \rbrace$| | 0.398** | 0.492*** | 0.492*** |

| (2.3) | (3.4) | (3.4) | |

| p-value for difference | 0.171 | 0.049 | 0.049 |

| R2 | 0.518 | 0.528 | 0.526 |

| No. control/treated firms | 1,321/643 | 1,003/551 | 748/551 |

| No. observations | 16,574 | 11,668 | 10,003 |

| (1) | (2) | ||

|---|---|---|---|

| |${{Cash/Assets}}_{i}^{07}$| | |${{Unused \, LC/Assets}}_{i}^{07}$| | ||

| Panel A. Precrisis balance-sheet measures | |||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot {\mathbb 1} \lbrace T_i \ge T^{70th} \rbrace$| | 0.024 | 0.081 | |

| (0.2) | (0.7) | ||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i \le T^{30th} \rbrace$| | 0.508*** | 0.307*** | |

| (4.3) | (3.3) | ||

| p-value for difference | 0.005 | 0.070 | |

| R2 | 0.246 | 0.262 | |

| No. firms in top/bottom deciles | 770/783 | 799/1,001 | |

| No. observations | 12,248 | 13,436 | |

| (1) | (2) | (3) | |

| All firms | Single-bank firms | Single-bank firms, not with D | |

| Panel B. The Baltic crisis experiment | |||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i=0 \rbrace$| | 0.210** | 0.192* | 0.172 |

| (2.1) | (1.7) | (1.3) | |

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i=1 \rbrace$| | 0.398** | 0.492*** | 0.492*** |

| (2.3) | (3.4) | (3.4) | |

| p-value for difference | 0.171 | 0.049 | 0.049 |

| R2 | 0.518 | 0.528 | 0.526 |

| No. control/treated firms | 1,321/643 | 1,003/551 | 748/551 |

| No. observations | 16,574 | 11,668 | 10,003 |

Notes: This table reports results for estimations of equation (5) on various subsamples of firms for the period 2006–2009. Column (1) in panel A reports results for estimations on subsamples consisting of firms in the top three and bottom three deciles, respectively, of the |${\textit {Cash}}/{\textit {Assets}}_{i,t-1}^{07}$| distribution, whereas column (2) reports results for a corresponding sample-split based on the |${\textit {Unused}} \ {\textit {LC/Assets}}_{i,t-1}^{07}$| distribution. The cutoffs used to construct the subsamples are defined at the firm level; hence, the number of firms in each subsample is approximately the same, whereas the number of observations differ somewhat (note, though, that the number of firms differs somewhat in the split based on credit lines due to the fact that more than 30% of firms have no unused credit line). Columns (1)–(3) in panel B concern estimations of equation (5) on treated firms and control firms in the Baltic crisis experiment. The samples underlying the estimations in the three columns comprise all firms with a precrisis bank relationship (column 1); all single-bank firms (column 2); and single-bank firms except those with bank D as their main lender (column 3). Reported p-values correspond to one-sided tests, where the null hypothesis is that the estimates of β are equal in each pair and the alternative hypothesis that the coefficients are larger for firms in the bottom deciles (panel A) and in the treatment group (Panel B). t-statistics calculated using robust standard errors clustered at the firm-level are reported in parentheses. *Significant at 10%; **significant at 5%; ***significant at 1%.

Mechanism I—Liquidity cost pass-through.

| (1) | (2) | ||

|---|---|---|---|

| |${{Cash/Assets}}_{i}^{07}$| | |${{Unused \, LC/Assets}}_{i}^{07}$| | ||

| Panel A. Precrisis balance-sheet measures | |||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot {\mathbb 1} \lbrace T_i \ge T^{70th} \rbrace$| | 0.024 | 0.081 | |

| (0.2) | (0.7) | ||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i \le T^{30th} \rbrace$| | 0.508*** | 0.307*** | |

| (4.3) | (3.3) | ||

| p-value for difference | 0.005 | 0.070 | |

| R2 | 0.246 | 0.262 | |

| No. firms in top/bottom deciles | 770/783 | 799/1,001 | |

| No. observations | 12,248 | 13,436 | |

| (1) | (2) | (3) | |

| All firms | Single-bank firms | Single-bank firms, not with D | |

| Panel B. The Baltic crisis experiment | |||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i=0 \rbrace$| | 0.210** | 0.192* | 0.172 |

| (2.1) | (1.7) | (1.3) | |

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i=1 \rbrace$| | 0.398** | 0.492*** | 0.492*** |

| (2.3) | (3.4) | (3.4) | |

| p-value for difference | 0.171 | 0.049 | 0.049 |

| R2 | 0.518 | 0.528 | 0.526 |

| No. control/treated firms | 1,321/643 | 1,003/551 | 748/551 |

| No. observations | 16,574 | 11,668 | 10,003 |

| (1) | (2) | ||

|---|---|---|---|

| |${{Cash/Assets}}_{i}^{07}$| | |${{Unused \, LC/Assets}}_{i}^{07}$| | ||

| Panel A. Precrisis balance-sheet measures | |||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot {\mathbb 1} \lbrace T_i \ge T^{70th} \rbrace$| | 0.024 | 0.081 | |

| (0.2) | (0.7) | ||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i \le T^{30th} \rbrace$| | 0.508*** | 0.307*** | |

| (4.3) | (3.3) | ||

| p-value for difference | 0.005 | 0.070 | |

| R2 | 0.246 | 0.262 | |

| No. firms in top/bottom deciles | 770/783 | 799/1,001 | |

| No. observations | 12,248 | 13,436 | |

| (1) | (2) | (3) | |

| All firms | Single-bank firms | Single-bank firms, not with D | |

| Panel B. The Baltic crisis experiment | |||

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i=0 \rbrace$| | 0.210** | 0.192* | 0.172 |

| (2.1) | (1.7) | (1.3) | |

| |${\textit{Crisis}}_t \cdot \hat{\tau }_i^{07} \cdot \mathbb {1} \lbrace T_i=1 \rbrace$| | 0.398** | 0.492*** | 0.492*** |

| (2.3) | (3.4) | (3.4) | |

| p-value for difference | 0.171 | 0.049 | 0.049 |

| R2 | 0.518 | 0.528 | 0.526 |

| No. control/treated firms | 1,321/643 | 1,003/551 | 748/551 |

| No. observations | 16,574 | 11,668 | 10,003 |