Abstract

We use the introduction of covered bonds in Norway in 2007 together with administrative and supervisory data at the bank and loan level to investigate the effect of asset encumbrance, that is, pledging assets as collateral, on the composition of bank balance sheets and bank risk. We show that covered bonds—despite being collateralized with mortgages—lead to a shift in bank lending from mortgages to corporate loans. The marginal corporate borrower is young and low-rated, suggesting that overall credit risk increases. At the same time, we find that balance sheet liquidity increases. Overall, the beneficial effects of increased liquidity on bank risk outweighs any negative effects of increased credit risk, ultimately reducing risk premia on total and unsecured funding. The effects are driven by banks with initially low net holdings of liquid assets and low firm credit risk in their lending portfolios.

1. Introduction

Banks can collateralize their assets for various purposes. In many instances, the collateralized assets remain on bank balance sheets. This is in contrast to for instance the issuance of asset-backed securities (ABS), where the underlying assets are typically originated and distributed.1 Such asset encumbrance is predominant. Almost 30% of the outstanding assets by European banks were encumbered as of June 2020 (European Banking Authority 2021). In practice, asset encumbrance can take many different forms. Three of the most dominant drivers of asset encumbrance are repurchase agreements between banks and other financial institutions, borrowing agreements with the central bank and the issuance of covered bonds (European Banking Authority 2021).

The availability of asset encumbrance might substantially affect bank outcomes, such as bank risk and portfolio allocation. This has received a large amount of attention by policymakers and academics. For instance, International Monetary Fund (2013) and Ahnert et al. (2019) have raised concerns about how asset encumbrance might increase the risk of losses for the unsecured creditors of banks, as the quality of the pool of assets available to cover their demands in case of bank default goes down when asset encumbrance increases.2 Since typically only a part of bank assets are available for encumbrance, the potential for asset encumbrance might also affect banks’ incentives to issue certain forms of credit. For instance, Nicolaisen (2017) was worried in the context of covered bonds that asset encumbrance would—due to being based on mortgage lending—incentivize banks to supply mortgages, potentially fueling house price growth and the growth in household debt, while also crowding out corporate credit. Finally, one of the main purposes of asset encumbrance is to increase available stable funding for banks which ultimately can make banks less prone to refinancing risk. This could also have implications for bank portfolio allocations. Despite the debate about the effects of asset encumbrance and the potential impact it might have on bank outcomes, there is limited comprehensive overview of the effects of asset encumbrance on bank behavior. Filling that gap is the goal of this paper.

To isolate the effect of asset encumbrance on banks, we assess the causal effect of the introduction of covered bonds on banks’ portfolio choice and the implications for various dimensions of bank risk. Covered bonds are debt instruments issued with primarily mortgages as collateral. The covered bond market has shown substantial growth since the financial crisis of 2007–2009. In the Euro area, covered bond issuance relative to total bond issuance for banks grew from 26% in 2007 to 42% during the sovereign debt crisis of 2011 (Van Rixtel and Gasperini 2013). By the end of 2019, the total volume of covered bonds outstanding worldwide corresponded to EUR 2.7 trillion (European Covered Bond Council 2020), and covered bonds account for approximately 36% of all debt securities issued by European banks.3,4

In this paper, we analyze how covered bonds affect bank portfolio decisions and risk-taking. We focus on the introduction of covered bond legislation in Norway in 2007, which marked the start of covered bond issuance in Norway. As we show, the introduction of this legislation led to a boom in the issuance of covered bonds by Norwegian banks, with significant and large effects on bank credit allocation. We combine data from three different sources: detailed supervisory bank level data, loan level data on the universe of firm loans, and firm-level accounting data. This data-rich environment enables us to show the impact of covered bond issuance on bank portfolios at a granular level.

The analysis in this paper consists of four main steps. First, we exploit the fact that banks had different scope for issuing covered bonds due to different existing mortgage portfolios, implying that some banks were able to shift to covered bonds as a source of financing to a larger extent than others. Mortgages with loan-to-values (LTVs) below 75% were eligible for being used as the underlying assets of a covered bond, that is, being included in the “cover pool”. Our data contain a breakdown of mortgages according to their LTVs, thereby allow us to classify banks according to their ex ante scope for exploiting this new source of funding. We show that banks with an above-median fraction of mortgages with low LTVs (“high-exposure” banks) issued substantially more covered bonds after the legal change compared to other banks.

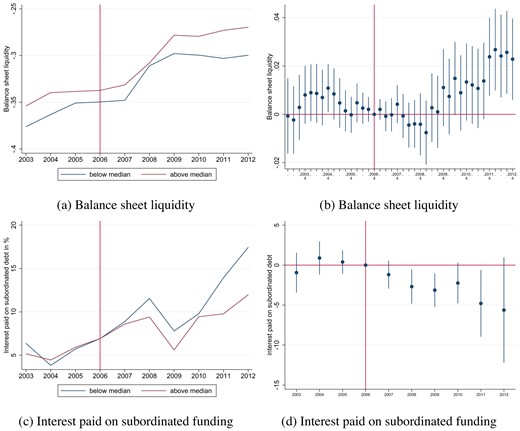

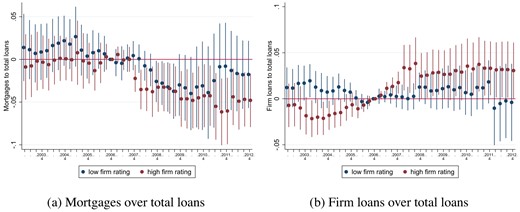

Second, we document in a dynamic difference-in-differences setup that the relative increase in covered bond issuance translates into substantial changes in bank portfolios. The results hold for a binary treatment definition, where we compare high- and low exposure banks, as well as for a continuous treatment definition in the vein of Callaway, Goodman-Bacon, and Sant’Anna (2024). Specifically, mortgages remain unchanged, while there is a relative increase in firm lending. This contributes to an increase in the portfolio share of firm lending for high-exposure banks by up to 7.4% compared with the pre-reform mean and compared with other banks following the introduction of covered bonds. This implies that, even though covered bonds are primarily collateralized by mortgages, covered bond issuance is accompanied by a portfolio rebalancing away from mortgages to firm loans. Using loan level data on the universe of firm loans in Norway, we show that covered bond issuance increases lending volumes and leads to weakly lower interest rates, conditional on a large set of firm controls such as high-dimensional fixed effects (FEs) combinations (Degryse et al. 2019), or firm |$\times$| year FEs (Khwaja and Mian 2008). The increase in firm credit is not uniform across firms, but tilted toward young firms and firms with low credit ratings, suggesting an increase in overall credit risk. Further, the introduction of covered bonds leads high-exposure banks to increase their holdings of liquid financial securities, and we show that balance sheet liquidity—a combined measure of asset and funding liquidity—increases for high-exposure banks.

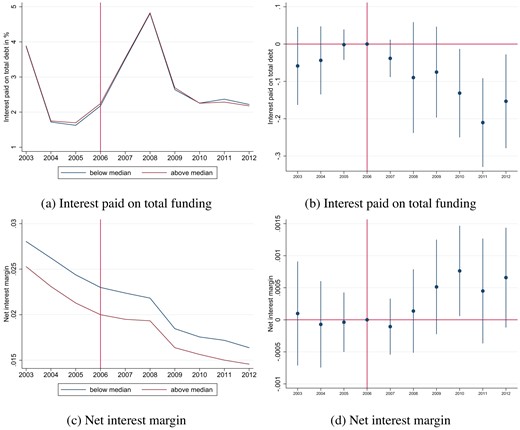

Third, we investigate the implications for overall bank risk. We proxy overall bank risk by using the risk premium on unsecured debt funding. This is an important step in our analysis, as the impacts of covered bond issuance on credit risk and liquidity risk move in opposite directions due to the portfolio rebalancing, that is, banks increase the share of risky firm lending while also increase their balance sheet liquidity. We document that the risk premium on unsecured debt funding declines for high-exposure banks, suggesting that the effect of increased credit risk on overall risk is offset by improved balance sheet liquidity.

Our identification relies on ex ante differences in the LTV distribution within banks, but it does not require banks to choose the LTV of mortgages randomly or that they are identical in terms of the levels of various covariates. It only requires that high- and low-exposure banks would have behaved similarly in terms of the outcomes we consider in absence of the introduction of covered bonds. To verify the plausibility of this assumption, we adopt two approaches. First, we adopt a flexible difference-in-differences design where we explicitly test for differences in the outcomes considered before the introduction of covered bonds. The raw data and the estimated coefficients are consistent with parallel trends for all the outcomes considered prior to the introduction of covered bonds. Second, we show that bank level changes after the introduction of covered bonds are unlikely to be driven by other confounding factors, such as differential exposure to the financial crisis across banks.5 The Norwegian economy was fairly insulated from the direct effects of the financial crisis. Unemployment rate remained relatively low and GDP growth relatively high, compared with other comparable countries (NOU 2011). Moreover, the Norwegian financial sector did not experience substantial losses (Kragh-Sørensen and Solheim 2014). The financial crisis primarily affected Norwegian banks indirectly through lower returns on financial assets and a temporary increase in interbank liquidity premia. Importantly, we show that the fraction of low-LTV mortgages in 2006 on which our exposure measure is based is orthogonal to reliance on interbank funding or holdings of financial assets, as well as a wide of range of other pre-crisis bank characteristics such as ex ante funding costs and the volatility of the return on assets. We rule out additional concerns that high exposure banks are larger in size and therefore might be exposed differently to the financial crisis thereby confounding our results. We exclude all large banks from the sample in robustness checks and show that our results still hold.

Fourth and finally, we analyze our baseline bank level findings through the lens of a simple theoretical framework to understand the conditions under which asset encumbrance induces bank portfolio rebalancing toward firm lending. In the model, we consider a bank that provides liquidity services and extends mortgages and risky firm loans. The bank is funded by uninsured depositors with a preference for liquidity. Firm loans are illiquid if an exogenously determined bad state of the economy is materialized. Hence, banks that have a larger fraction of firm loans will in equilibrium be charged a higher risk premium by depositors. Issuance of covered bonds has two countervailing effects on the portfolio allocation of banks. On the one hand, covered bond issuance reduces mortgage funding costs, thereby making mortgages more profitable. On the other hand, covered bond issuance improves banks’ funding liquidity via reducing funding cost, which enhances banks’ capability to engage in risky firm lending. This latter substitution effect is more likely to dominate when depositors have limited risk aversion and when the level of credit risk in firm lending is not too high. Importantly, the magnitude of the substitution effect also varies with initial bank liquidity. Banks with low initial holdings of net liquid assets have stronger incentives to switch to firm loans when the mortgage portfolio becomes more liquid. We then return to the data and show support for our theoretical model: The observed portfolio rebalancing from mortgage loans to firm loans is indeed driven by banks with low initial net liquidity as well as by banks with relatively low initial firm credit risk.

Related Literature. Our paper relates to the literature on how asset securitization affects bank outcomes. By exploring the pre-crisis credit boom in Spain, Jiménez et al. (2020) show how market funding through covered bonds and ABS together provided liquidity relief for banks and allowed them to increase the credit supply to new borrowers, at the expense of existing borrowers, which were crowded out. They also show that during the credit boom, banks with higher exposure to the real estate sector increased their risk-taking. Similarly, Chakraborty, Goldstein, and MacKinlay (2018) show that banks with higher exposure to the US real estate market increase mortgage lending and crowd out firm lending. They find similar results for banks that securitized compared to banks that did not securitize assets. Carbó-Valverde, Rosen, and Rodríguez-Fernández (2017) provide a comprehensive overview and comparison of ABS and covered bonds.

Focusing on asset encumbrance, that is, the securitization of bank assets where the the securitized assets are retained on bank balance sheets, Ahnert et al. (2019) show that asset encumbrance allows banks to raise cheaper funding through secured debt. At the same time, however, it reduces banks’ scope for repaying unsecured creditors out of unencumbered assets in the event of market stress, increasing the likelihood of bank failure. Using cross-country data with more than 100 listed banks in Europe over 2004–2013, Garcia-Appendini, Gatti, and Nocera (2023) find that a bank’s default risk is positively correlated with its covered bond issuance. They attribute such correlation to the fact that increasing encumbered assets for covered bond issuance leads to risk concentration in the unencumbered assets. Banal-Estañol, Benito, and Khametshin (2018) find that, after controlling for bank liquidity and capital ratios, a higher asset encumbrance ratio relates to lower spreads in banks’ credit default swaps.

Our main contribution to the literature is to isolate the impact of asset encumbrance on bank portfolio decisions, as well as to investigate the overall implications for bank risk. Our results highlight an interesting tension between the effects of covered bond issuance on credit risk and liquidity risk: On the one hand, credit risk increases in line with Ahnert et al. (2019) and International Monetary Fund (2013), whereas on the other hand, liquidity risk as measured according to balance sheet liquidity, decreases. As a result, the implications of covered bond issuance for overall bank risk are ambiguous. When focusing on the risk premium on unsecured bond funding, we show that overall bank risk—as is perceived by the market—declines despite an increase in credit risk. The empirical findings are therefore consistent with the seemingly different views in Ahnert et al. (2019) and Garcia-Appendini, Gatti, and Nocera (2023) versus Banal-Estañol, Benito, and Khametshin (2018).

Our paper proceeds as follows: In Section 2, we briefly present the institutional settings of the covered bond market. In Section 3, we outline the data sources we use and describe our empirical strategy. Then, in Section 4, we present results. We demonstrate how covered bond issuance leads to rebalancing of banks’ portfolios in Section 4.1, and how it impacts overall banks’ balance sheet liquidity, bank risk, and profitability in Section 4.2. In Section 4.3, we explore the mechanisms at work, guided by a simple, stylized model. We provide robustness checks to our identification strategy in Section 4.4. Section 5 concludes.

2. Institutional Background

In this section, we outline the institutional background of the covered bond market in Norway. A covered bond is a debt security issued by financial institutions that is collateralized by a pool of assets (“cover pool”).6 In Norway, by regulation, covered bonds must be issued by bank-owned mortgage companies whose sole purpose is the issuance of covered bonds. Specifically, when a bank initiates the issuance of a covered bond, the cover pool is sold from the bank to the mortgage company, which then issues the covered bond.7 Covered bonds are widely regarded as very safe financial assets, as a covered bond and its underlying cover pool are subject to three important types of restrictions. First, the quality of the underlying collateral must be high. Mortgage loans that are included in the cover pool must have sufficiently low LTV ratios. The value of the assets in the cover pool must exceed the face value of the covered bond itself, that is, covered bonds are over-collateralized. Second, the cover pool is dynamic: if the quality of certain assets in the covered pool deteriorates and violates the quality requirements, the issuer must replace these assets by other eligible assets or cash. Third and finally, if the issuer goes bankrupt within the maturity of a covered bond, the covered bond holders take control of the cover pool. These restrictions imply very low default risk, hence very low risk premium for covered bonds.

A mortgage company can either be a subsidiary of an individual bank, or co-owned by multiple banks. Particularly, as regional and municipal banks are too small to incur the fixed costs associated with the creation of their own mortgage companies, these banks usually establish co-owned mortgage companies that pool high-quality mortgage loans from their owner banks and issue covered bonds on behalf of their owners. In this way, even small banks are able to participate in covered bond markets and their covered bonds can achieve the same high ratings as those issued by large banks. For instance, covered bonds issued by Norwegian mortgage companies have been so far awarded the highest or second-highest credit ratings AAA or AA on the international market, so that small banks benefit from similarly low funding cost of covered bonds as large banks (Finance Norway 2018).

After the 2007–2009 global financial crisis, covered bond issuance started to gain momentum across Europe, especially after the European Central Bank accepted covered bonds as eligible collateral and included covered bond purchases in its unconventional monetary policy toolbox. As of 2019q4, covered bonds outstanding worldwide amount to EUR 2.705 trillion, about 90% of which is issued by banks in European countries. The largest covered bond markets in terms of volume of total outstanding covered bonds at the end of 2019 are Denmark, Germany, France, and Spain, followed by Sweden and Norway (European Covered Bond Council 2020).8

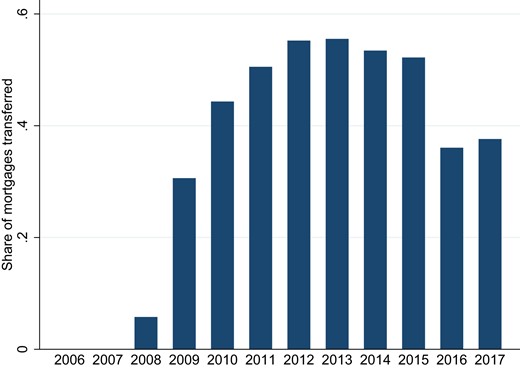

The context of our empirical analysis is Norway, where the necessary legislation for covered bond issuance was implemented on the 1st of June, 2007. Mortgages with an LTV below 75% were eligible for the cover pool. Norwegian banks started issuing the first covered bonds in the second half of 2007 (Finance Norway 2018). Covered bond issuance increased substantially thereafter. In the time period from the introduction of covered bond markets until 2012—the time period we focus on in the empirical analysis—the fraction of mortgages transferred to cover pools increased from 0 to approximately 55%, as highlighted in Figure 1.

Share of mortgages transferred. This figure shows the share of mortgages transferred over total mortgages from 2008q4 until 2017. Note that although banks started to transfer mortgages from 2007q3 onward, ORBOF provides data on transfers from 2008q4 onward only. Source: ORBOF, with authors’ own calculations.

The birth of the covered bond market was associated with a swap agreement allowing banks to exchange covered bonds for Treasury bills that was launched by the Ministry of Finance in October 2008. Although the Norwegian economy and financial system in general were relatively unaffected by the financial crisis and the Norwegian financial sector did not experience substantial losses (Kragh-Sørensen and Solheim 2014), as a precautionary measure, the Ministry of Finance initiated an arrangement in which the government gave banks treasury bills in exchange for covered bonds for an agreed period, so that banks could improve their asset liquidity. Norges Bank administered the arrangement and Treasury bills with a total value of NOK 230 billion were allocated. The swap agreement was terminated in October 2009; afterward, given that their liquidity pressure was eased, banks terminated their swap agreements and sold the covered bonds in the market. See Bakke and Rakkestad (2010) for more details.

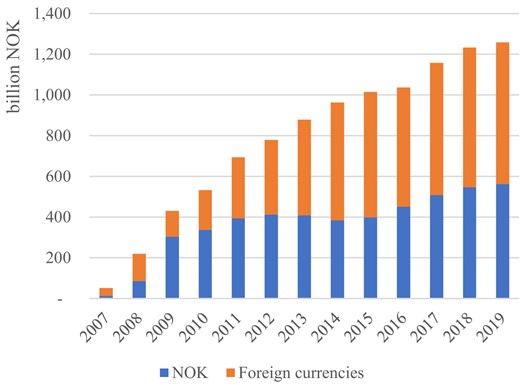

Although the swap arrangement was a temporary measure and only lasted for 1 year, it did kickoff the market and covered bond issuance continued to increase substantially. Particularly, as Figure 2 shows, the rapid growth in covered bond issuance after the termination of the swap agreement was largely driven by demand from foreign investors: As of the end of 2019, 55% of covered bonds outstanding are denominated in foreign currencies; among those foreign currency denominated outstanding covered bonds, 89% are denominated in euro and 6% are denominated in US dollar. Given that mortgage loans in Norway are mostly denominated in Norwegian krone while more than half of Norwegian covered bonds outstanding are denominated in foreign currencies, covered bonds issuing banks are exposed to the interest rate risks on the international bond market and exchange risks from the currency mismatch. Therefore, Norwegian covered bond issuers are required by law to hedge against the interest rate risks and exchange risks using swap contracts (Bakke and Rakkestad 2010). After the end of our sample period, covered bond issuance has continued to experience fast growth. As of 2020q3, covered bonds outstanding in Norway amount to 143 billion euros, equivalent to 43% of Norwegian GDP.

Outstanding debt and currency decomposition of Norwegian covered bonds. This figure shows the outstanding debt (in billion NOK) and currency decomposition (in NOK, denoted by the dark area, or other currencies, denoted by the lighter area) of covered bonds issued in Norway from 2007 until 2019. Source: Norwegian covered bonds statistics, Finance Norway.

3. Data and Methodology

In this section, we outline the data sources we use and describe our empirical approach.

3.1. Data

Our sample period is 2003–2012. Our data is merged from three different data sources. The first data source is quarterly balance sheet data used for supervisory purposes for all Norwegian banks (Statistisk Sentralbyrå 2017). We exclude foreign branches or subsidiaries in Norway and consider only banks issuing mortgages. We drop banks that only existed before the introduction of covered bonds and include new banks from their third quarter of existence onward.9 The data source covers 133 banks and 5,150 bank-quarter observations. It provides us with the volume of mortgage transfers from banks to mortgage companies from 2008q4 onward.

There are 21 mortgage companies in our sample, 11 are owned by one bank and 10 are co-owned by multiple banks.10 In total, 11 banks are not linked to any mortgage company. We consolidate balance sheet items of mortgage companies and banks. If multiple banks share a mortgage company, we consolidate on the basis of the share of mortgages stemming from bank i on the mortgage company’s balance sheet. Between 2008 and 2012, banks transferred on average 15.17% of mortgages to mortgage companies. In aggregate, 30.5% of all mortgages issued were transferred (see Figure 1). We have information on the share of loans on the banks’ balance sheets at LTV ratios above or below 80% in 2006q4.11 This will be important for constructing our treatment indicator, as highlighted in Section 3.2. Table 1 reports summary statistics at the bank-time level.

Summary statistics at the bank level.

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| Logs | ||||||

| Total assets | 5,150 | 14.957 | 1.409 | 11.934 | 14.674 | 21.519 |

| Total loans | 5,150 | 14.781 | 1.340 | 11.436 | 14.508 | 20.820 |

| Mortgage loans total | 5,150 | 14.506 | 6.226 | 10.087 | 14.302 | 20.283 |

| Mortgage loans transferred to credit company, 2008–2012 | 2,122 | 10.347 | 5.578 | 0.000 | 12.447 | 20.114 |

| Firm loans | 5,138 | 13.358 | 1.562 | 9.680 | 13.018 | 19.667 |

| Securities | 5,150 | 12.404 | 1.677 | 5.628 | 12.164 | 20.113 |

| Ratios | ||||||

| Mortgage loans over total assets | 5,150 | 0.654 | 0.123 | 0.044 | 0.676 | 0.954 |

| Mortgage loans over total loans | 5,150 | 0.773 | 0.128 | 0.051 | 0.793 | 1.000 |

| Firm loans over total assets | 5,138 | 0.219 | 0.083 | 0.010 | 0.209 | 0.810 |

| Firm loans over total loans | 5,138 | 0.261 | 0.101 | 0.010 | 0.251 | 0.935 |

| Securities over total assets | 5,150 | 0.089 | 0.045 | 0.000 | 0.079 | 0.374 |

| Net liquidity over total assets | 5,135 | 0.053 | 0.078 | −0.553 | 0.056 | 0.386 |

| Balance sheet liquidity over total assets | 5,150 | −0.324 | 0.074 | −0.648 | −0.324 | −0.046 |

| Interest income | ||||||

| Mean interest on firm lending in %, yearly | 1,006 | 5.890 | 0.699 | 3.140 | 5.909 | 7.720 |

| Ratio interest firm over interest other lending, yearly | 1,006 | 1.269 | 0.221 | 0.545 | 1.250 | 2.130 |

| Funding costs | ||||||

| Interest paid on total funding in %, yearly | 1,251 | 2.723 | 1.049 | 0.57 | 2.399 | 6.307 |

| Interest paid on subordinated funding in %, yearly | 421 | 8.178 | 5.149 | 0.398 | 6.947 | 46.057 |

| Profitability | ||||||

| Net interest margin, yearly | 1,251 | 0.020 | 0.006 | 0.001 | 0.020 | 0.040 |

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| Logs | ||||||

| Total assets | 5,150 | 14.957 | 1.409 | 11.934 | 14.674 | 21.519 |

| Total loans | 5,150 | 14.781 | 1.340 | 11.436 | 14.508 | 20.820 |

| Mortgage loans total | 5,150 | 14.506 | 6.226 | 10.087 | 14.302 | 20.283 |

| Mortgage loans transferred to credit company, 2008–2012 | 2,122 | 10.347 | 5.578 | 0.000 | 12.447 | 20.114 |

| Firm loans | 5,138 | 13.358 | 1.562 | 9.680 | 13.018 | 19.667 |

| Securities | 5,150 | 12.404 | 1.677 | 5.628 | 12.164 | 20.113 |

| Ratios | ||||||

| Mortgage loans over total assets | 5,150 | 0.654 | 0.123 | 0.044 | 0.676 | 0.954 |

| Mortgage loans over total loans | 5,150 | 0.773 | 0.128 | 0.051 | 0.793 | 1.000 |

| Firm loans over total assets | 5,138 | 0.219 | 0.083 | 0.010 | 0.209 | 0.810 |

| Firm loans over total loans | 5,138 | 0.261 | 0.101 | 0.010 | 0.251 | 0.935 |

| Securities over total assets | 5,150 | 0.089 | 0.045 | 0.000 | 0.079 | 0.374 |

| Net liquidity over total assets | 5,135 | 0.053 | 0.078 | −0.553 | 0.056 | 0.386 |

| Balance sheet liquidity over total assets | 5,150 | −0.324 | 0.074 | −0.648 | −0.324 | −0.046 |

| Interest income | ||||||

| Mean interest on firm lending in %, yearly | 1,006 | 5.890 | 0.699 | 3.140 | 5.909 | 7.720 |

| Ratio interest firm over interest other lending, yearly | 1,006 | 1.269 | 0.221 | 0.545 | 1.250 | 2.130 |

| Funding costs | ||||||

| Interest paid on total funding in %, yearly | 1,251 | 2.723 | 1.049 | 0.57 | 2.399 | 6.307 |

| Interest paid on subordinated funding in %, yearly | 421 | 8.178 | 5.149 | 0.398 | 6.947 | 46.057 |

| Profitability | ||||||

| Net interest margin, yearly | 1,251 | 0.020 | 0.006 | 0.001 | 0.020 | 0.040 |

Notes: This table reports summary statistics for 133 banks, or 5,150 bank-quarter-year observations. We follow Deep and Schaefer (2004) and define net liquidity over total assets as the share of net liquid assets over total assets as (marked-to-market (MM) assets + central bank reserves − interbank borrowings − certificates)/total assets. We define balance sheet liquidity over total assets as the negative of Berger and Bouwman (2009)’s definition of liquidity creation. We use Berger and Bouwman (2009)’s definition and adapt it to the availability of our balance sheet data. Illiquid assets encompass firm loans, intangible hold-to-maturity (HTM) assets, HTM owner assets and other assets. Liquid assets are assets at the central bank, HTM bonds, other HTM assets, and MM assets. Illiquid liabilites are subordinated debt and equity. Liquid liabilities are deposits and deposits from the central bank. We add the sum of illiquid assets and the sum of liquid liabilities with weights of 0.5 and subtract the sum of liquid assets and illiquid liabilities with weights of 0.5. We divide by total consolidated assets and multiply the index by −1. We estimate the interest on total funding costs in % as the share of interest costs over total liabilities, and the interest on subordinated funding in % as interest costs on subordinated funding over total subordinated debt. We truncate interest paid on subordinated debt at the 1st and the 99th percentile per year due to outliers and set negative values to missings.12

Summary statistics at the bank level.

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| Logs | ||||||

| Total assets | 5,150 | 14.957 | 1.409 | 11.934 | 14.674 | 21.519 |

| Total loans | 5,150 | 14.781 | 1.340 | 11.436 | 14.508 | 20.820 |

| Mortgage loans total | 5,150 | 14.506 | 6.226 | 10.087 | 14.302 | 20.283 |

| Mortgage loans transferred to credit company, 2008–2012 | 2,122 | 10.347 | 5.578 | 0.000 | 12.447 | 20.114 |

| Firm loans | 5,138 | 13.358 | 1.562 | 9.680 | 13.018 | 19.667 |

| Securities | 5,150 | 12.404 | 1.677 | 5.628 | 12.164 | 20.113 |

| Ratios | ||||||

| Mortgage loans over total assets | 5,150 | 0.654 | 0.123 | 0.044 | 0.676 | 0.954 |

| Mortgage loans over total loans | 5,150 | 0.773 | 0.128 | 0.051 | 0.793 | 1.000 |

| Firm loans over total assets | 5,138 | 0.219 | 0.083 | 0.010 | 0.209 | 0.810 |

| Firm loans over total loans | 5,138 | 0.261 | 0.101 | 0.010 | 0.251 | 0.935 |

| Securities over total assets | 5,150 | 0.089 | 0.045 | 0.000 | 0.079 | 0.374 |

| Net liquidity over total assets | 5,135 | 0.053 | 0.078 | −0.553 | 0.056 | 0.386 |

| Balance sheet liquidity over total assets | 5,150 | −0.324 | 0.074 | −0.648 | −0.324 | −0.046 |

| Interest income | ||||||

| Mean interest on firm lending in %, yearly | 1,006 | 5.890 | 0.699 | 3.140 | 5.909 | 7.720 |

| Ratio interest firm over interest other lending, yearly | 1,006 | 1.269 | 0.221 | 0.545 | 1.250 | 2.130 |

| Funding costs | ||||||

| Interest paid on total funding in %, yearly | 1,251 | 2.723 | 1.049 | 0.57 | 2.399 | 6.307 |

| Interest paid on subordinated funding in %, yearly | 421 | 8.178 | 5.149 | 0.398 | 6.947 | 46.057 |

| Profitability | ||||||

| Net interest margin, yearly | 1,251 | 0.020 | 0.006 | 0.001 | 0.020 | 0.040 |

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| Logs | ||||||

| Total assets | 5,150 | 14.957 | 1.409 | 11.934 | 14.674 | 21.519 |

| Total loans | 5,150 | 14.781 | 1.340 | 11.436 | 14.508 | 20.820 |

| Mortgage loans total | 5,150 | 14.506 | 6.226 | 10.087 | 14.302 | 20.283 |

| Mortgage loans transferred to credit company, 2008–2012 | 2,122 | 10.347 | 5.578 | 0.000 | 12.447 | 20.114 |

| Firm loans | 5,138 | 13.358 | 1.562 | 9.680 | 13.018 | 19.667 |

| Securities | 5,150 | 12.404 | 1.677 | 5.628 | 12.164 | 20.113 |

| Ratios | ||||||

| Mortgage loans over total assets | 5,150 | 0.654 | 0.123 | 0.044 | 0.676 | 0.954 |

| Mortgage loans over total loans | 5,150 | 0.773 | 0.128 | 0.051 | 0.793 | 1.000 |

| Firm loans over total assets | 5,138 | 0.219 | 0.083 | 0.010 | 0.209 | 0.810 |

| Firm loans over total loans | 5,138 | 0.261 | 0.101 | 0.010 | 0.251 | 0.935 |

| Securities over total assets | 5,150 | 0.089 | 0.045 | 0.000 | 0.079 | 0.374 |

| Net liquidity over total assets | 5,135 | 0.053 | 0.078 | −0.553 | 0.056 | 0.386 |

| Balance sheet liquidity over total assets | 5,150 | −0.324 | 0.074 | −0.648 | −0.324 | −0.046 |

| Interest income | ||||||

| Mean interest on firm lending in %, yearly | 1,006 | 5.890 | 0.699 | 3.140 | 5.909 | 7.720 |

| Ratio interest firm over interest other lending, yearly | 1,006 | 1.269 | 0.221 | 0.545 | 1.250 | 2.130 |

| Funding costs | ||||||

| Interest paid on total funding in %, yearly | 1,251 | 2.723 | 1.049 | 0.57 | 2.399 | 6.307 |

| Interest paid on subordinated funding in %, yearly | 421 | 8.178 | 5.149 | 0.398 | 6.947 | 46.057 |

| Profitability | ||||||

| Net interest margin, yearly | 1,251 | 0.020 | 0.006 | 0.001 | 0.020 | 0.040 |

Notes: This table reports summary statistics for 133 banks, or 5,150 bank-quarter-year observations. We follow Deep and Schaefer (2004) and define net liquidity over total assets as the share of net liquid assets over total assets as (marked-to-market (MM) assets + central bank reserves − interbank borrowings − certificates)/total assets. We define balance sheet liquidity over total assets as the negative of Berger and Bouwman (2009)’s definition of liquidity creation. We use Berger and Bouwman (2009)’s definition and adapt it to the availability of our balance sheet data. Illiquid assets encompass firm loans, intangible hold-to-maturity (HTM) assets, HTM owner assets and other assets. Liquid assets are assets at the central bank, HTM bonds, other HTM assets, and MM assets. Illiquid liabilites are subordinated debt and equity. Liquid liabilities are deposits and deposits from the central bank. We add the sum of illiquid assets and the sum of liquid liabilities with weights of 0.5 and subtract the sum of liquid assets and illiquid liabilities with weights of 0.5. We divide by total consolidated assets and multiply the index by −1. We estimate the interest on total funding costs in % as the share of interest costs over total liabilities, and the interest on subordinated funding in % as interest costs on subordinated funding over total subordinated debt. We truncate interest paid on subordinated debt at the 1st and the 99th percentile per year due to outliers and set negative values to missings.12

Our second data source is loan level data obtained from the Norwegian Tax Administration (Skatteetaten 2017). By the end of each year, all banks report all outstanding loan and deposit accounts to the tax administration for tax purposes. In total, we observe 3,885,845 firm-account-bank-year observations, based on 250,545 limited liability firms.13 We aggregate loans and deposits to the firm–bank-year level, which results in 1,627,319 firm–bank-year observations. In our dynamic regression estimation we use 1,355,289 firm–bank-year observations for which we can estimate the symmetric growth rate of loans (see below) from 220,059 firms. On average, a firm maintains a relationship to 1.19 banks, and 83.74% of firm-year observations are linked to one bank only. A firm has on average 1.57 loans with its bank conditional on the existence of a loan relationship. Table 2 reports summary statistics at the firm–bank-year level.

Summary statistics at firm–bank-year level.

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| Log(loans) | 1,355,289 | 4.552 | 6.567 | 0.000 | 0.000 | 23.363 |

| Number of loans per borrower|$|_{\text{loan}\gt 0}$| | 457,962 | 1.566 | 1.950 | 1.000 | 1.000 | 310.000 |

| Symmetric credit growth (|$\Delta L_{b,f,t}$|) | 1,355,289 | −0.067 | 0.710 | −2.000 | 0.000 | 2.000 |

| Interest rate (|$i_{b,f,t}$|, in %) | 401,673 | 6.614 | 3.595 | 0.000 | 6.166 | 35.473 |

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| Log(loans) | 1,355,289 | 4.552 | 6.567 | 0.000 | 0.000 | 23.363 |

| Number of loans per borrower|$|_{\text{loan}\gt 0}$| | 457,962 | 1.566 | 1.950 | 1.000 | 1.000 | 310.000 |

| Symmetric credit growth (|$\Delta L_{b,f,t}$|) | 1,355,289 | −0.067 | 0.710 | −2.000 | 0.000 | 2.000 |

| Interest rate (|$i_{b,f,t}$|, in %) | 401,673 | 6.614 | 3.595 | 0.000 | 6.166 | 35.473 |

Notes: This table reports summary statistics for 275,323 firm–bank relationships, or 220,059 firms.

Summary statistics at firm–bank-year level.

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| Log(loans) | 1,355,289 | 4.552 | 6.567 | 0.000 | 0.000 | 23.363 |

| Number of loans per borrower|$|_{\text{loan}\gt 0}$| | 457,962 | 1.566 | 1.950 | 1.000 | 1.000 | 310.000 |

| Symmetric credit growth (|$\Delta L_{b,f,t}$|) | 1,355,289 | −0.067 | 0.710 | −2.000 | 0.000 | 2.000 |

| Interest rate (|$i_{b,f,t}$|, in %) | 401,673 | 6.614 | 3.595 | 0.000 | 6.166 | 35.473 |

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| Log(loans) | 1,355,289 | 4.552 | 6.567 | 0.000 | 0.000 | 23.363 |

| Number of loans per borrower|$|_{\text{loan}\gt 0}$| | 457,962 | 1.566 | 1.950 | 1.000 | 1.000 | 310.000 |

| Symmetric credit growth (|$\Delta L_{b,f,t}$|) | 1,355,289 | −0.067 | 0.710 | −2.000 | 0.000 | 2.000 |

| Interest rate (|$i_{b,f,t}$|, in %) | 401,673 | 6.614 | 3.595 | 0.000 | 6.166 | 35.473 |

Notes: This table reports summary statistics for 275,323 firm–bank relationships, or 220,059 firms.

In the loan level regressions we use the symmetric growth rate of credit as dependent variable, defined as

where |$D_{b,f,t}$| is the outstanding credit volume between bank b and firm f in year t.

We use the fact that we observe both the outstanding debt volume and the interest paid to compute a proxy for the interest rate for every firm–bank-year combination. This interest rate proxy is defined as

We only include interest payments if we also observe a loan in year |$t-1$|. To limit the influence of outliers, we truncate |$i_{b,f,t}$| at the 1st and the 99th percentile.

Our third and final data source is firm-level data from a major credit rating agency on all major balance sheet items and other information on the universe of Norwegian limited liability firms (Bisnode 2017). We add information on firm age, rating, and balance sheet variables to investigate the role of firm characteristics in explaining banks’ potential change in credit allocation following the introduction of covered bonds. We exclude financial firms. Table 3 shows summary statistics. We merge 130,661 firms (933,746 firm-year observations). The median firm has total assets of approximately NOK 2,782,000,14 is 10 years old and has an A rating.15 We define a binary variable |${Rating}(0/1)$| which is 0 for low-rated firms (A, B, or C) and 1 for high-rated firms (AA or AAA).

Summary statistics at firm-year level.

| N | Mean | Sd | Min | p50 | Max | |

|---|---|---|---|---|---|---|

| Size and Age | ||||||

| Assets (in 1000s of NOK) | 933,746 | 42,270.250 | 1,563,833 | 0.000 | 2,782.000 | |$5.84\times 10^8$| |

| Age | 933,738 | 13.71379 | 13.00164 | 0.000 | 10.000 | 169.000 |

| Rating | ||||||

| Rating (AAA:5 - C:1) | 933,746 | 3.278 | 0.991 | 1.000 | 3.000 | 5.000 |

| Rating(0/1) | 933,746 | 0.425 | 0.494 | 0.000 | 0.000 | 1.000 |

| N | Mean | Sd | Min | p50 | Max | |

|---|---|---|---|---|---|---|

| Size and Age | ||||||

| Assets (in 1000s of NOK) | 933,746 | 42,270.250 | 1,563,833 | 0.000 | 2,782.000 | |$5.84\times 10^8$| |

| Age | 933,738 | 13.71379 | 13.00164 | 0.000 | 10.000 | 169.000 |

| Rating | ||||||

| Rating (AAA:5 - C:1) | 933,746 | 3.278 | 0.991 | 1.000 | 3.000 | 5.000 |

| Rating(0/1) | 933,746 | 0.425 | 0.494 | 0.000 | 0.000 | 1.000 |

Notes: This table reports summary statistics for 130,661 firms.

Summary statistics at firm-year level.

| N | Mean | Sd | Min | p50 | Max | |

|---|---|---|---|---|---|---|

| Size and Age | ||||||

| Assets (in 1000s of NOK) | 933,746 | 42,270.250 | 1,563,833 | 0.000 | 2,782.000 | |$5.84\times 10^8$| |

| Age | 933,738 | 13.71379 | 13.00164 | 0.000 | 10.000 | 169.000 |

| Rating | ||||||

| Rating (AAA:5 - C:1) | 933,746 | 3.278 | 0.991 | 1.000 | 3.000 | 5.000 |

| Rating(0/1) | 933,746 | 0.425 | 0.494 | 0.000 | 0.000 | 1.000 |

| N | Mean | Sd | Min | p50 | Max | |

|---|---|---|---|---|---|---|

| Size and Age | ||||||

| Assets (in 1000s of NOK) | 933,746 | 42,270.250 | 1,563,833 | 0.000 | 2,782.000 | |$5.84\times 10^8$| |

| Age | 933,738 | 13.71379 | 13.00164 | 0.000 | 10.000 | 169.000 |

| Rating | ||||||

| Rating (AAA:5 - C:1) | 933,746 | 3.278 | 0.991 | 1.000 | 3.000 | 5.000 |

| Rating(0/1) | 933,746 | 0.425 | 0.494 | 0.000 | 0.000 | 1.000 |

Notes: This table reports summary statistics for 130,661 firms.

3.2. Empirical Strategy

3.2.1. Endogenous Regressions

To assess whether banks change their portfolio composition when issuing covered bonds, an initial, naive approach would be to regress outcome variables such as mortgage lending on covered bond issuance. In such a case, however, reverse causality or omitted variable bias would be a potential issue and, as such, the coefficient should not be interpreted as causal. In Table 4, we show results for such an endogenous regression. We use log-level balance sheet positions as dependent variables and the share of mortgages transferred to cover pools as right-hand side variable. We observe that a higher share of mortgages transferred (|${transfers}_{t-1}$|) goes along with increased size of the balance sheet (column I), and an increased loan portfolio (column II). We find a mild positive correlation with mortgages (column III) and a strong positive correlation with firm loans (column IV). Also, securities holdings is positively correlated with transfers (column V). However, to the extent that mortgage lending affect banks’ ability to transfer loans to the cover pool, we likely overestimate the effect of covered bond issuance in particular on mortgage lending. For this reason, we develop the identification approach outlined below.

Endogenous regressions.

| (I) | (II) | (III) | (IV) | (V) | |

|---|---|---|---|---|---|

| Total assets | Total loans | Mortgages | Firm loans | Securities | |

| Transfers|$_{t-1}$| | 0.260*** | 0.151** | 0.131* | 0.323*** | 0.663*** |

| (0.068) | (0.070) | (0.067) | (0.103) | (0.206) | |

| Observations | 2,122 | 2,122 | 2,122 | 2,122 | 2,122 |

| R-squared | 0.588 | 0.561 | 0.561 | 0.253 | 0.250 |

| Number of banks | 130 | 130 | 130 | 130 | 130 |

| Bank FE | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes |

| (I) | (II) | (III) | (IV) | (V) | |

|---|---|---|---|---|---|

| Total assets | Total loans | Mortgages | Firm loans | Securities | |

| Transfers|$_{t-1}$| | 0.260*** | 0.151** | 0.131* | 0.323*** | 0.663*** |

| (0.068) | (0.070) | (0.067) | (0.103) | (0.206) | |

| Observations | 2,122 | 2,122 | 2,122 | 2,122 | 2,122 |

| R-squared | 0.588 | 0.561 | 0.561 | 0.253 | 0.250 |

| Number of banks | 130 | 130 | 130 | 130 | 130 |

| Bank FE | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes |

In this table, we show results from estimating the following regression: |$Y_{b, t} = \alpha _b + \alpha _T + \beta \: {Transfers}_{(t-1)} + \epsilon _{b,t}$|. |$Y_{b,t}$| are logs of total assets, total loans, mortgages, firm loans, and securities. |${Transfers}_{(t-1)}$| is the share of total mortgages which banks transfer to cover pools in the previous quarter. The regression covers the time period 2008q4–2012q4 due to data availability of transfers, and includes year FEs |$\alpha _T$|. Robust standard errors are clustered at the bank level and are depicted in parentheses. *, **, and *** indicate significant coefficients at the 10%, 5%, and 1% level, respectively.

Endogenous regressions.

| (I) | (II) | (III) | (IV) | (V) | |

|---|---|---|---|---|---|

| Total assets | Total loans | Mortgages | Firm loans | Securities | |

| Transfers|$_{t-1}$| | 0.260*** | 0.151** | 0.131* | 0.323*** | 0.663*** |

| (0.068) | (0.070) | (0.067) | (0.103) | (0.206) | |

| Observations | 2,122 | 2,122 | 2,122 | 2,122 | 2,122 |

| R-squared | 0.588 | 0.561 | 0.561 | 0.253 | 0.250 |

| Number of banks | 130 | 130 | 130 | 130 | 130 |

| Bank FE | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes |

| (I) | (II) | (III) | (IV) | (V) | |

|---|---|---|---|---|---|

| Total assets | Total loans | Mortgages | Firm loans | Securities | |

| Transfers|$_{t-1}$| | 0.260*** | 0.151** | 0.131* | 0.323*** | 0.663*** |

| (0.068) | (0.070) | (0.067) | (0.103) | (0.206) | |

| Observations | 2,122 | 2,122 | 2,122 | 2,122 | 2,122 |

| R-squared | 0.588 | 0.561 | 0.561 | 0.253 | 0.250 |

| Number of banks | 130 | 130 | 130 | 130 | 130 |

| Bank FE | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes |

In this table, we show results from estimating the following regression: |$Y_{b, t} = \alpha _b + \alpha _T + \beta \: {Transfers}_{(t-1)} + \epsilon _{b,t}$|. |$Y_{b,t}$| are logs of total assets, total loans, mortgages, firm loans, and securities. |${Transfers}_{(t-1)}$| is the share of total mortgages which banks transfer to cover pools in the previous quarter. The regression covers the time period 2008q4–2012q4 due to data availability of transfers, and includes year FEs |$\alpha _T$|. Robust standard errors are clustered at the bank level and are depicted in parentheses. *, **, and *** indicate significant coefficients at the 10%, 5%, and 1% level, respectively.

3.2.2. Cross-sectional Variation in Covered Bond Exposure

Our empirical strategy exploits the fact that only mortgages with an LTV below 75% (“low LTVs”) were eligible for being transferred to the cover pool. As a result, banks with different initial distributions of LTVs in their mortgage portfolios had different scope for issuing covered bonds. As described in Section 3.1, we observe the breakdown of the volume of mortgages with an LTV below and above 80%. We use this information to approximate the fraction of loans for each bank below the regulatory threshold of 75%. We construct a treatment indicator equal to 1 for banks that had a share of low LTV mortgages over total mortgages that is above the median of all banks in the quarter before the covered bond introduction (2006q4), that is, |$T_b =1$|. We set |$T_b =0$| for all other banks and refer to them as “low-exposure banks” or “other banks” throughout the text.16 On average, 84.2% of mortgages on banks’ balance sheets have low LTVs. Banks that we define as high-exposure had on average 89.2% low LTV mortgages, while other banks had on average 79.2% low LTV mortgages in 2006q4. In line with Callaway, Goodman-Bacon, and Sant’Anna (2024), we also use the continuous ratio of low LTV mortgages over total mortgages as the treatment measure in a robustness exercise and show that the results remain qualitatively similar. Table 5 shows summary statistics on our treatment indicators.

Summary statistics on treatment definitions.

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| |$T_b$| (treatment indicator at bank level) | 5,150 | 0.496 | 0.500 | 0.000 | 0.000 | 1.000 |

| Share of mortgages transferred to mortgage companies, 2007–2012 | 3,048 | 0.106 | 0.140 | 0.000 | 0.038 | 0.869 |

| Ratio of low LTV mortgages over total mortgages, 2006q4 | 133 | 0.842 | 0.064 | 0.662 | 0.850 | 1.000 |

| Ratio of low LTV mortgages over total mortgages, 2006q4, |$T_b = 1$| | 67 | 0.892 | 0.039 | 0.850 | 0.876 | 1.000 |

| Ratio of low LTV mortgages over total mortgages, 2006q4, |$T_b = 0$| | 66 | 0.792 | 0.039 | 0.662 | 0.799 | 0.844 |

| |$T_b$| (treatment indicator at loan level) | 1,355,289 | 0.880 | 0.325 | 0.000 | 1.000 | 1.000 |

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| |$T_b$| (treatment indicator at bank level) | 5,150 | 0.496 | 0.500 | 0.000 | 0.000 | 1.000 |

| Share of mortgages transferred to mortgage companies, 2007–2012 | 3,048 | 0.106 | 0.140 | 0.000 | 0.038 | 0.869 |

| Ratio of low LTV mortgages over total mortgages, 2006q4 | 133 | 0.842 | 0.064 | 0.662 | 0.850 | 1.000 |

| Ratio of low LTV mortgages over total mortgages, 2006q4, |$T_b = 1$| | 67 | 0.892 | 0.039 | 0.850 | 0.876 | 1.000 |

| Ratio of low LTV mortgages over total mortgages, 2006q4, |$T_b = 0$| | 66 | 0.792 | 0.039 | 0.662 | 0.799 | 0.844 |

| |$T_b$| (treatment indicator at loan level) | 1,355,289 | 0.880 | 0.325 | 0.000 | 1.000 | 1.000 |

Notes: This table reports summary statistics on variables used for the treatment definition for 133 banks, or 5,150 bank-quarter-year and for 275,323 firm–bank links.

Summary statistics on treatment definitions.

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| |$T_b$| (treatment indicator at bank level) | 5,150 | 0.496 | 0.500 | 0.000 | 0.000 | 1.000 |

| Share of mortgages transferred to mortgage companies, 2007–2012 | 3,048 | 0.106 | 0.140 | 0.000 | 0.038 | 0.869 |

| Ratio of low LTV mortgages over total mortgages, 2006q4 | 133 | 0.842 | 0.064 | 0.662 | 0.850 | 1.000 |

| Ratio of low LTV mortgages over total mortgages, 2006q4, |$T_b = 1$| | 67 | 0.892 | 0.039 | 0.850 | 0.876 | 1.000 |

| Ratio of low LTV mortgages over total mortgages, 2006q4, |$T_b = 0$| | 66 | 0.792 | 0.039 | 0.662 | 0.799 | 0.844 |

| |$T_b$| (treatment indicator at loan level) | 1,355,289 | 0.880 | 0.325 | 0.000 | 1.000 | 1.000 |

| N | Mean | Sd | Min | Median | Max | |

|---|---|---|---|---|---|---|

| |$T_b$| (treatment indicator at bank level) | 5,150 | 0.496 | 0.500 | 0.000 | 0.000 | 1.000 |

| Share of mortgages transferred to mortgage companies, 2007–2012 | 3,048 | 0.106 | 0.140 | 0.000 | 0.038 | 0.869 |

| Ratio of low LTV mortgages over total mortgages, 2006q4 | 133 | 0.842 | 0.064 | 0.662 | 0.850 | 1.000 |

| Ratio of low LTV mortgages over total mortgages, 2006q4, |$T_b = 1$| | 67 | 0.892 | 0.039 | 0.850 | 0.876 | 1.000 |

| Ratio of low LTV mortgages over total mortgages, 2006q4, |$T_b = 0$| | 66 | 0.792 | 0.039 | 0.662 | 0.799 | 0.844 |

| |$T_b$| (treatment indicator at loan level) | 1,355,289 | 0.880 | 0.325 | 0.000 | 1.000 | 1.000 |

Notes: This table reports summary statistics on variables used for the treatment definition for 133 banks, or 5,150 bank-quarter-year and for 275,323 firm–bank links.

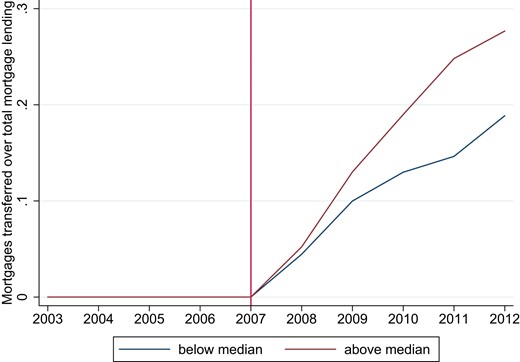

Note that our treatment definition does not exclude the possibility that low-exposure banks issue covered bonds. We merely capture the fact that high-exposure banks could more readily issue covered bonds due to the availability of eligible mortgages on their balance sheets. Hence, we capture the difference in the intensity of exposure to the introduction in covered bonds. To illustrate this difference, we show in Figure 3 the fraction of mortgages transferred to the cover pools for high-exposure banks and other banks, respectively. By 2011, the fraction of mortgages transferred by high-exposure banks was approximately 70% larger compared with other banks.17

Share of mortgages transferred for high-exposure and low-exposure banks. This figure shows the average share of mortgages transferred to credit companies over total mortgages issued by high-exposure banks in red (upper line), and other banks in blue (lower line). We define high exposed banks as having a share of low-LTV mortgages over total mortgages that is above the median of all banks before the covered bond introduction in 2006q4.

Over time, other banks can shift the supply of credit toward low-LTV mortgages relative to high-exposure banks. However, this is likely to be a slow-moving process, as shown in Figure C.1 in Online Appendix C, as the cross-sectional differences in the average LTV in banks’ mortgage portfolios not only reflect bank factors, but also relatively persistent regional factors such as house prices and borrower type heterogeneity more broadly. However, over time it is likely that banks can adjust the composition of mortgage credit to improve the scope for issuing covered bonds. Hence, our treatment measure |$T_b$| is meant to capture the short- and medium-run effects of exposure to the introduction of covered bonds. We therefore focus on the impact of covered bonds on bank outcomes only up until 6 years after the legal change was implemented.

At the bank level, the fraction of low-LTV mortgages has strong predictive power on post-treatment mortgage transfers to cover pools. In Table 6, we report the results from a univariate regression of the fraction of mortgages transferred post-treatment against the pre-treatment fraction of low-LTV mortgages. There is a strong and statistically significant relationship, suggesting that a 1 percentage point increase in the ratio of low-LTV mortgages to total mortgages pre-treatment is associated with a 0.19 percentage point increase in the fraction of transferred mortgages post-treatment. Moreover, the fraction of low-LTV mortgages explains roughly half of the variation in the fraction of mortgages transferred. We thus conclude that our exposure measure captures banks’ subsequent issuance of covered bonds well.

Share of eligible mortgages predict mortgage transfers.

| Mortgage transfers over total mortgages | |

|---|---|

| Eligible mortgages over total mortgages | 0.190** |

| (0.089) | |

| Observations | 5,150 |

| Number of banks | 133 |

| R-squared | 0.484 |

| Mortgage transfers over total mortgages | |

|---|---|

| Eligible mortgages over total mortgages | 0.190** |

| (0.089) | |

| Observations | 5,150 |

| Number of banks | 133 |

| R-squared | 0.484 |

Notes: This table shows the correlation of the share of eligible mortgages over total mortgages in 2006q4 and the actual share of mortgages transferred to mortgage companies over total mortgages issued. The regression includes quarter-year FEs. *, **, and *** indicate significant coefficients at the 10%, 5%, and 1% level, respectively.

Share of eligible mortgages predict mortgage transfers.

| Mortgage transfers over total mortgages | |

|---|---|

| Eligible mortgages over total mortgages | 0.190** |

| (0.089) | |

| Observations | 5,150 |

| Number of banks | 133 |

| R-squared | 0.484 |

| Mortgage transfers over total mortgages | |

|---|---|

| Eligible mortgages over total mortgages | 0.190** |

| (0.089) | |

| Observations | 5,150 |

| Number of banks | 133 |

| R-squared | 0.484 |

Notes: This table shows the correlation of the share of eligible mortgages over total mortgages in 2006q4 and the actual share of mortgages transferred to mortgage companies over total mortgages issued. The regression includes quarter-year FEs. *, **, and *** indicate significant coefficients at the 10%, 5%, and 1% level, respectively.

In Table B.1 in Online Appendix B, we report summary statistics on a range of outcomes for banks defined as high-exposure and other banks in the pre-reform period. We also include the results from t-tests on the difference between the two groups. Importantly, our identification strategy outlined below does not rely on similarities in these measures across high- and low-exposure banks. High-exposure banks are larger in size and issue slightly more mortgages and firm loans. The share of loans over total assets is slightly lower for the high-exposure banks, though the difference amounts to 0.007 percentage point only. The two groups do not differ in terms of mortgages and firm loans over total assets or over total loans. High-exposure banks hold less securities (HTM financial assets plus MM financial assets) over total assets compared with other banks. The difference is with 0.3 percentage points small, but statistically significantly different from zero. We include bank FEs in our regression specification in order to control for level differences. In the robustness check in Section 4.4, we further show that banks do not differ in terms of ex ante risk-taking behavior. Further, we provide evidence that results remain robust when we exclude the ten largest banks from the sample.

In the next subsections, we outline our empirical strategy at the different levels of analysis.

3.2.3. Bank Level

We estimate the following dynamic estimation equation at the bank level:

Dependent variables |$Y_{b,t}$| are balance sheet items of bank b in year-quarter t. We focus on outcomes in log levels and ratios. The regression includes bank FEs (|$\alpha _b$|) and quarter-year FEs (|$\delta _\tau$|). Standard errors are clustered at the bank level.

We interact the treatment variable |$T_b$| with indicators for every quarter-year. We leave out 2006q4 as the base quarter-year before the introduction of covered bonds in 2007. With this dynamic approach, we can trace the effect of the issuance of covered bonds on a quarterly basis. Moreover, we can investigate whether outcomes differ pre-treatment by testing whether |$\gamma _{\tau }$| is significantly different from zero for |$\tau \lt 2006q4$|.

3.2.4. Loan Level

We estimate the following dynamic estimation equation at the firm–bank level:

Dependent variables are symmetric growth of loans of firm f with bank b in year t defined as in equation (1), as well as the interest rate paid by firm f to bank b in year t, approximated as in equation (2). We interact the treatment variable |$T_b$| with indicators for every year. We leave out 2006 as the base year before the introduction of covered bonds in 2007. We include bank–firm FEs |$\alpha _{f,b}$|, as well as time FEs (|$\delta _\tau$|), and cluster standard errors at the bank level.

To control for firm-level demand shocks, we exploit the structure of our loan level data to control for different firm characteristics to ensure that we compare outcomes from relatively similar firms. Specifically, we follow two different approaches. First, we follow Degryse et al. (2019) and introduce industry-location-size-time FEs, defined as the two-digit industry code, two-digit zip-code, deciles of total assets, and year to control for local, industry-specific, and size-specific demand effects. Their approach is especially suitable for data consisting of many small firms with single bank links, as in our case (83.74% of firm-year observations are by firms linked to one bank only). Second, we follow Khwaja and Mian (2008) and introduce firm-time FEs in the sample of multi-bank firms.

3.3. Threats to Identification

Our identifying assumption is that the outcomes we consider would be similar—conditional on a set of FEs depending on the level of analysis—for high- and low-exposure banks in the absence of the introduction of covered bonds. Conditional on this assumption being true, we can then interpret our estimates as the causal effect of covered bond issuance on bank outcomes in the short- and medium-run. In this section, we discuss factors which may potentially invalidate this interpretation. It is useful to group the potential identification challenges into four: systematic differences, confounding credit demand shocks, confounding credit supply shocks, and anticipation effects.

3.3.1. Systematic Differences

The first threat to identification is that banks with different initial mortgage portfolios are structurally different in terms of outcomes. For instance, if banks with a high fraction of low LTV mortgages and thus a larger share of cover pool transfers increase their firm lending share throughout our sample period, we would estimate a positive and significant effect of low-LTV mortgages on firm lending that would not be due to the introduction of covered bonds.

An advantage in our dynamic difference-in-differences approach is that it allows us to directly test for systematic differences between banks according to the exposure measure, by estimating period-specific treatment effects also prior to the introduction of covered bonds. Specifically, we can explore if there were parallel trends among banks with different fractions of low-LTV mortgages prior to the transition by testing if |$\gamma _{\tau }=0 \forall \tau \lt 2006q4$| in equations (3) and (4).

3.3.2. Confounding Credit Demand Shocks

Even if banks with different exposures to the introduction of covered bonds are similar prior to 2007, they may experience different credit demand shocks in the subsequent years. This is a concern as the introduction of covered bonds coincided with the financial crisis, which could affect firms differently. Shocks to banks’ firm clients could affect our results if firms and banks are systematically linked. For instance, banks that are less exposed to the introduction of covered bonds could lend more to export-oriented firms, or more generally to regions with relatively high exposure to the international downturn associated with the financial crisis. In that case, differences in credit growth between banks with different initial fractions of low-LTV mortgages could be a result of a reduction in credit demand from customers of low-exposed banks rather than an increase in credit supply by high-exposed banks.

In order to alleviate this concern, we control for firm demand shocks with an extensive set of FEs, that is, industry-location-time-size FEs as well as firm-time FEs as described in Section 3.2.4. The latter approach holds firm factors fixed, provided that they are invariant at the firm |$\times$| year level. Moreover, by observing both quantities and prices at the loan level, we can exploit the fact that demand and supply shocks move prices in opposite directions. For instance, an increase in the volume of credit and a decline in the interest rate on loans from high-exposure banks would only be consistent with a relative expansion in the supply of credit.

3.3.3. Confounding Supply Shocks

A third threat to identification could arise if there are other factors affecting banks’ supply of credit that are correlated with our exposure measure. One potential concern is that banks with a large fraction of low-LTV mortgages were less exposed to the financial crisis and as a result had higher risk-bearing capacity than other banks, which in turn could induce them to rebalance their portfolio.

In general, the Norwegian economy and financial system were relatively unaffected by the financial crisis. Norwegian banks were affected indirectly in primarily two ways. First, banks to varying degrees invested in financial assets that would potentially depreciate in value ex post due to the ongoing crisis. This would especially be a relevant concern for financial instruments that are MM. Second, a more indirect contagion happened in the form of short-term liquidity stress in Norwegian interbank markets. The interbank spread increased substantially in mid-September 2008. It was lowered to pre-crisis level toward the end of 2008, but in theory this short-term disruption in access to liquidity could confound at least some of our results.

In order to gauge the severity of these concerns, we investigate how our treatment measure correlates with (1) banks’ holdings of financial instruments that are MM and (2) banks’ reliance on interbank funding, both measured at the end of 2006. A negative correlation between our treatment measure and these measures would indicate that exposure to the crisis through either measure could pose an identification concern.

Further, changes in risk-taking behavior during the financial crisis conditional on our treatment measure might confound our results. If low-exposed banks had a larger risk appetite before the financial crisis and became more risk averse during the crisis as in Guiso, Sapienza, and Zingales (2018), differential effects between high-exposure and other banks might be merely driven by relative changes in risk aversion over time. In order to address this concern, we investigate differences in ex ante risk-taking across high- and low-exposure banks using a wide range of proxies for risk-taking, including volatility of earnings, net liquidity, and equity ratios, and use all proxies as controls in our estimations.

Additionally, high exposure banks are larger banks, which might have been differently affected by the financial crisis compared to smaller banks. For example, larger banks might had a greater need to diversify during the financial crisis and hence increased supply of firm loans relative to smaller banks.18 We employ bank FEs to control for static differences in all regressions, as well as exclude the three, five, and ten largest banks from our sample in robustness checks to rule out that our results are driven by different exposure to the financial crisis due to size differentials.

A final potential confounding credit supply shock is the transition to Basel II. The transition to Basel II took place in 2007, and entailed for most banks a reduction in average risk-weights, applied to retail loans and mortgages with a low LTV. This could then imply that there was also a larger reduction in the effective capital requirement for banks that were high-exposure according to our measure and that this relative reduction in the capital requirement is driving our results. The largest absolute reduction in risk weights for banks computing risk weights under the standard method was for retail firm loans.19 As a robustness check, we therefore use balance sheet information and actual changes in risk weights to compute—bank by bank—the actual reduction in the capital requirement due to the Basel II transition. We can then correlate the capital requirement reduction with our treatment measure to investigate whether banks that were more exposed to the Basel II transition were also more exposed to the introduction of covered bonds.

3.3.4. Anticipation Effects

A final concern is that high-exposure banks according to our measures adjusted prior to the introduction of covered bonds. This is a valid concern if the introduction of covered bonds were known well in advance. Note that such anticipation effects are likely to lead us to underestimate the effects of covered bond issuance. Judging from Figure C.1 in Online Appendix C, it seems unlikely that banks selected themselves into the group of high-exposed banks, as the share of eligible mortgages in the pre period is fairly stable over time. Moreover, the flexible difference-in-differences approach allows us to explicitly map out when high-exposure banks adjust relative to the actual introduction of covered bonds and hence we can be somewhat agnostic about the exact timing of the treatment.

4. Results

In this section, we assess the impact of covered bond issuance on banks’ balance sheets. We also outline a theoretical model to explain how covered bond issuance affects bank portfolio allocation and test the model’s predictions. We end the section by showing a series of robustness exercises.

4.1. Results on Portfolio Rebalancing

4.1.1. Bank Level (levels)

We start by comparing the evolution of different asset classes at the bank level. We show results of differences across log level of total assets, as well as mortgage and firm loans in Figure 4, with corresponding statistics in Table 7.

Regression information corresponding to Figure 4.

| Dependent variable | Figure | N observations | N cluster | R2 | Mean dependent | SD dependent |

|---|---|---|---|---|---|---|

| Total assets | 4a | 5,150 | 133 | 0.882 | 14.957 | 1.409 |

| Mortgages | 4b | 5,150 | 133 | 0.867 | 14.506 | 1.340 |

| Firm loans | 4c | 5,138 | 133 | 0.679 | 13.358 | 1.562 |

| Dependent variable | Figure | N observations | N cluster | R2 | Mean dependent | SD dependent |

|---|---|---|---|---|---|---|

| Total assets | 4a | 5,150 | 133 | 0.882 | 14.957 | 1.409 |

| Mortgages | 4b | 5,150 | 133 | 0.867 | 14.506 | 1.340 |

| Firm loans | 4c | 5,138 | 133 | 0.679 | 13.358 | 1.562 |

Notes: This table reports statistics from estimating equation (3). The second column (“Figure”) refers to the corresponding coefficient plot.

Regression information corresponding to Figure 4.

| Dependent variable | Figure | N observations | N cluster | R2 | Mean dependent | SD dependent |

|---|---|---|---|---|---|---|

| Total assets | 4a | 5,150 | 133 | 0.882 | 14.957 | 1.409 |

| Mortgages | 4b | 5,150 | 133 | 0.867 | 14.506 | 1.340 |

| Firm loans | 4c | 5,138 | 133 | 0.679 | 13.358 | 1.562 |

| Dependent variable | Figure | N observations | N cluster | R2 | Mean dependent | SD dependent |

|---|---|---|---|---|---|---|

| Total assets | 4a | 5,150 | 133 | 0.882 | 14.957 | 1.409 |

| Mortgages | 4b | 5,150 | 133 | 0.867 | 14.506 | 1.340 |

| Firm loans | 4c | 5,138 | 133 | 0.679 | 13.358 | 1.562 |

Notes: This table reports statistics from estimating equation (3). The second column (“Figure”) refers to the corresponding coefficient plot.

First, consider how the introduction of covered bonds has affected total balance sheet size in Panel 4a. High exposure banks increase their balance sheets after the introduction of covered bonds in comparison to low exposure banks, measured according to the log of total assets. The difference is significantly different from zero after the introduction of covered bond markets up to the 1% level in 2011q4. Next, consider how the introduction of covered bonds has affected mortgage lending in Panel 4b. We do not find a difference in mortgage lending, measured according to the log of mortgages on banks’ balance sheets, between high exposure and low exposure banks. This lack of response is inconsistent with the view that covered bonds would lead to an expansion of mortgages as often discussed (Nicolaisen 2017). In contrast, however, we show that firm lending—in Panel 4c, increases for high exposure banks in comparison to low exposure banks after the introduction of covered bond markets suggesting that the exposure to covered bonds contributes to a relative shift of credit toward firm lending. The difference between high exposure and low exposure banks is statistically significantly different from zero up to the 1% level in 2008q4 and 2011q4. The results reflect findings from the endogenous regressions presented in Table 4. As argued, in the latter approach, we likely overestimate the relationship between covered bond issuance and outcome variables such as lending decisions. In contrast, with our estimation strategy, we find that as a response to the introduction of covered bond markets, banks do not change their mortgage lending, but increase firm lending.

Note that we observe differential effects in a period of overall loan growth. See Figure C.2 in Online Appendix C for the evolution of the mean stock of loans on banks’ balance sheets. Online Appendix Figure C.2 suggests that both, high- and low-exposure banks increase lending over time, though high exposure banks increase firm lending more than low exposure banks.

4.1.2. Bank Level (Portfolio Shares)

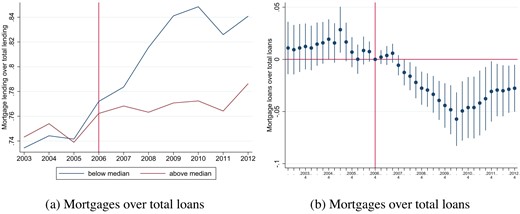

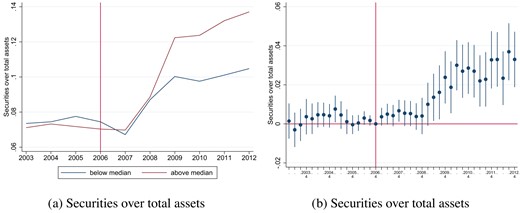

To further illustrate how covered bonds leads to a portfolio rebalancing toward firm lending, we continue by presenting results for portfolio rebalancing in ratios, that is, the proportions of the lending portfolio that go into mortgage lending or firm lending. We present the results in Figures 5 and 6. Accompanying statistics of the regression output are listed below in Table 8. Note that results hold also for the continuous treatment definition instead of the binary definition.20

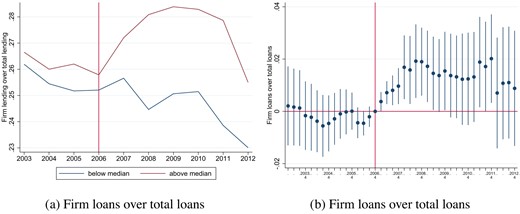

Bank portfolio re-balancing: total lending and mortgage lending. In this figure, we show the average loan and the average mortgage share over time on the left hand side. On the right hand side, we show the coefficient plots with confidence intervals at 90% from estimating equation (3). Statistics from estimations can be found in Table 8.

Bank lending portfolio re-balancing: firm lending. In this figure, we show the average firm share over time on the left hand side. On the right hand side, we show the coefficient plots with confidence intervals at 90% from estimating equation (3). Statistics from estimations can be found in Table 8.

| Dependent variable | Figure | N | No. of banks | R2 | Mean of dep. var. | Sd of dep. var. |

|---|---|---|---|---|---|---|

| Mortgage loans over total loans | 5b | 5,150 | 133 | 0.260 | 0.773 | 0.128 |

| Firm loans over total loans | 6b | 5,138 | 133 | 0.054 | 0.261 | 0.101 |

| Dependent variable | Figure | N | No. of banks | R2 | Mean of dep. var. | Sd of dep. var. |

|---|---|---|---|---|---|---|

| Mortgage loans over total loans | 5b | 5,150 | 133 | 0.260 | 0.773 | 0.128 |

| Firm loans over total loans | 6b | 5,138 | 133 | 0.054 | 0.261 | 0.101 |

Notes: This table reports statistics from estimating equation (3). The second column (“Figure”) refers to the corresponding coefficient plot.

| Dependent variable | Figure | N | No. of banks | R2 | Mean of dep. var. | Sd of dep. var. |

|---|---|---|---|---|---|---|

| Mortgage loans over total loans | 5b | 5,150 | 133 | 0.260 | 0.773 | 0.128 |

| Firm loans over total loans | 6b | 5,138 | 133 | 0.054 | 0.261 | 0.101 |

| Dependent variable | Figure | N | No. of banks | R2 | Mean of dep. var. | Sd of dep. var. |

|---|---|---|---|---|---|---|

| Mortgage loans over total loans | 5b | 5,150 | 133 | 0.260 | 0.773 | 0.128 |

| Firm loans over total loans | 6b | 5,138 | 133 | 0.054 | 0.261 | 0.101 |

Notes: This table reports statistics from estimating equation (3). The second column (“Figure”) refers to the corresponding coefficient plot.

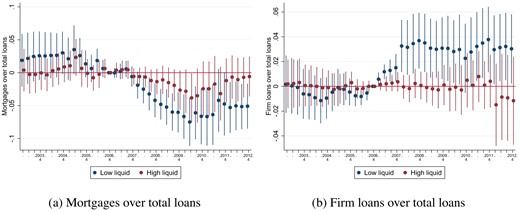

First, consider how the introduction of covered bonds affected the share of mortgage lending in total lending of banks. Figure 5a plots the raw data of the share of mortgage lending over total loans. There is a divergence in mortgage lending between the two groups from 2008 and onward, where the high-exposure banks have a relative decrease in the share of mortgages. Importantly, given that the data is consolidated at the bank-credit company level, this reduction in the fraction of mortgages is not mechanically related to mortgages being transferred to the mortgage company for the purpose of issuing covered bonds but rather reflects the fact that mortgage lending is unchanged while overall loans—due to the increase in firm lending—increases as documented in the previous section. In Figure 5b, we plot the coefficients from estimating equation (3) with mortgages over total loans as dependent variable. Before the introduction of covered bonds, there are no statistically significant time-varying differences between the two groups. After the introduction, high-exposure banks lower their mortgages to total loans ratio compared with other banks. The differences are statistically significantly different from zero at the 5% level from 2008q2 and at the 1% level from 2008q4 onward. The relative reduction in the mortgage share is driven by a relative increase in total lending due to the increase in firm lending, whereas total mortgage lending does not differ between the two groups, as we show in Figure 4. The reduction in the mortgage share is quantitatively large. High-exposure banks lowered the mortgage share by up to 5.7 percentage points compared with other banks over the post period. This compares to a pre-period mortgage share for high-exposure banks of 74.3%, suggesting that the relative reduction in the mortgage share in the post period is sizable and corresponds to around 7.7% of the average mortgage share of high-exposure banks in the pre period.

Next, we assess the fraction of firm loans relative to total loans. In Figure 6a, we illustrate that firm loans increase for high-exposure banks relative to other banks post-2007. In Figure 6b, we show that there are no differences between the two groups in the pre period compared with 2006q4. Differences in the post period are statistically significantly different from zero at the 1% level in 2007q2 and at the 5% level thereafter until 2009q2, with varying significance levels afterward. The firm lending share is up to 1.9 percentage points higher for high-exposure banks compared with other banks. This is an increase of 7.5% relative to the average share of firm lending for high-exposure banks in the pre period (25.7%). In terms of timing, effects as shown as in Figure 6b are particularly strong 2007–2009, when the growth rate of issuance of covered bonds was particularly strong (see Figure 2).

A valid concern against our identification could be that it is not the high-exposed banks which adjust their lending portfolios, but low-exposed banks which actually increase their mortgage lending in order to be able to participate in covered bond markets and hence we see a negative differential effect between high and low exposed banks in terms of the share of mortgages in their lending portfolio. However, there are two stylized facts which speak against this hypothesis: First, as we show in Figure 6a, there is a clear surge in the share of firm loans over total loans for high exposed banks after the introduction of covered bond markets. Second, there is actually no difference in mortgage lending between the two groups, as we show in Figure 4b, where we compare log level mortgage issuance. The difference between the two groups is driven by increases in firm lending by high exposed banks compared to low exposed banks (see Figure 4c).

4.1.3. Loan Level

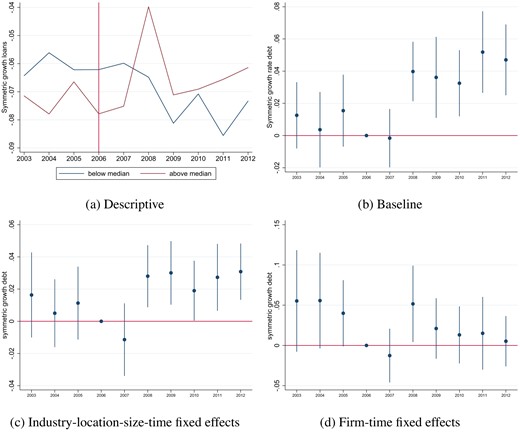

Next, we turn to the loan level to further shed light on the increase in firm lending. Using loan level data, we can tighten identification by adopting firm controls to address possible confounding firm-level demand shocks. We estimate the dynamic regression equation (4) with the symmetric growth rate of debt as defined in equation (1) and our interest proxy as defined in equation (2) as dependent variables. Further, we provide evidence for whether the increase in firm credit for high-exposure banks is uniform across all firms, or whether it is driven by a subset.

Loan growth and interest rates. In Figure 7a, we show the average of the symmetric growth rate of loans extended by high-exposure banks in red, and for loans extended by other banks in blue over time. After the introduction of covered bonds, loan growth for loans stemming from high-exposure banks increases, whereas loan growth decreases for loans from other banks. In Figure 7b, we plot the coefficients from estimating equation (4) with symmetric growth of debt as the dependent variable. Estimation results and accompanying statistics are reported in Table B.2 in Online Appendix B. Loan growth does not differ in the pre-reform period between the two groups. From 2008 onward, loan growth from high-exposure banks is larger than from other banks compared with base year 2006. The difference is statistically significantly different from zero at the 1% level for most years. High-exposure firm–bank pairs have a symmetric growth rate which is on average up to 0.05 higher than for other firm–bank pairs. The relative change is substantial: it compares to an average symmetric growth rate for loans from high-exposure banks in the pre-reform period of −0.073. These results are consistent with the findings at the bank level.21