Abstract

Euro-area sovereign bond and interbank interest rate spreads spiked in the 2007–2009 Global Financial Crisis and the subsequent European Debt Crisis, substantially elevating financing costs. I use a model-free measure of market liquidity to precisely identify the relative contribution of credit versus liquidity to spreads in these episodes. In the Financial Crisis, liquidity is paramount, accounting for 36% of trough-to-peak widening, after controlling for credit. However, default risk becomes relatively more important to sovereign spreads in the Debt Crisis. Aggregate bond liquidity explains a substantial portion of interbank spreads throughout the sample.

1. Introduction

The 2007–2009 Global Financial Crisis and the European Debt Crisis were marked by extraordinary interest rate spread widening and heightened volatility in asset prices, contributing to a broad tightening of financial conditions. One example is the increase in Euro-area government bond spreads, which rose by more than an order of magnitude in the Financial Crisis, to levels not seen since the introduction of the common currency in 1999. In the money market, spreads between unsecured interbank borrowing rates (EURIBOR) and overnight-indexed swap (OIS) rates of comparable maturities also rose by more than an order of magnitude in the Financial Crisis; EURIBOR-OIS spreads reached their widest levels since the inception of the OIS market, and peaked to an all-time high in October 2008. Spreads generally narrowed in 2010, before widening again in the subsequent Sovereign Debt Crisis. Despite the enormity of these interest rate movements, there has been a lack of consensus on the dominant driver. One hurdle to identification is the difficulty in precisely capturing the risk components in prices. This article documents a model-free measure of Euro-area market liquidity, constructed directly from asset prices. The measure is used to parse these historic movements, and to compare and contrast the spread widening drivers in the two crisis periods. The results show that aggregate market liquidity is an important contributor to euro-area sovereign debt and money market spreads over the entire sample period. However, the importance of liquidity relative to default risk differs by country and over time in a way that is consistent with important credit and liquidity events in asset markets during the Financial and Debt Crises (e.g., the Greek government’s debt restructuring and the central banks’ extraordinary liquidity provision).

In the sovereign bond market, an equal-weighted average across countries and maturities attributes 36% of the trough-to-peak spread widening over the Financial Crisis to deteriorating sovereign bond market liquidity and 22% to heightened default risk (consistent with the finding of Bao, Pan, and Wang, 2011, in the corporate bond market over this period). In contrast, during the subsequent Debt Crisis, default risk becomes a relatively larger driver of average sovereign spread widening. Interbank spreads show a strong role for aggregate bond market liquidity, over and above the effects of interbank credit and liquidity throughout the sample period.

Beyond the expected path of future short-horizon interest rates, it is difficult to empirically determine what drives sovereign bond yields or interbank rates, especially at times of market stress. Two possible influences that are explored in this article are credit, reflecting compensation for heightened default risk (McAndrews, Sarkar, and Wang, 2008; Taylor and Williams, 2009; Beber, Brandt, and Kavajecz, 2009; Afonso, Kovner, and Schoar, 2011; Filipović and Trolle, 2013), and market liquidity, reflecting trading conditions in asset markets (Michaud and Upper, 2008; Acharya and Skeie, 2011). The years after 2007 are an ideal period to study the liquidity and credit components of sovereign and interbank spreads because they were so variable both over time and in the cross section. In contrast, before 2007, these spreads were roughly constant near zero, making identification almost impossible.

Understanding the default and liquidity components in interest rates is important for portfolio allocation and policy decisions. Investors with the longest horizons should prefer to hold higher yielding assets if the elevated yields represent compensation for deteriorating market conditions, but not necessarily if they represent a greater risk of loss due to default. Amihud and Mendelson (1986) and Longstaff (2009) both propose models with different types of investors, in which the longer-horizon investors receive a premium for holding less liquid assets. From the perspective of policymakers, efforts to improve market functioning could help to dampen the effects of poor asset market liquidity on yields, mitigating the knock-on effects of higher financing costs. For example, an exchange of more-liquid for less-liquid bonds (such as in the Federal Reserve’s securities lending facility) could reduce liquidity premia. On the other hand, if higher yields are largely attributable to a credit shock, then this argues for addressing solvency.

This article first documents the tremendous deterioration in euro-area market liquidity during the Global Financial Crisis and the Sovereign Debt Crisis, using the yield differential between two duration-matched bonds with an identical credit guarantee to construct a measure of euro-area market liquidity. This yield spread identifies any deviation in an asset’s price from its hold-to-maturity value, fully capturing market liquidity effects impounded in prices. Specifically, the yield of a German federal government bond is compared to that of its less-liquid agency counterpart, KfW (Kreditanstalt für Wiederaufbau). The German federal government bond systematically commands a premium across maturity points over the sample period. I refer to this yield differential as the K-spread. While this article is the first to construct the K-spread, comparing two types of government-guaranteed securities goes back to Longstaff (2004), who explained the yield differential between Refcorp (Resolution Funding Corporation) and U.S. Treasury bonds as a measure of Treasury market liquidity. In this article, the K-spread is used to identify the contribution of aggregate market liquidity to the unprecedented widening of various interest rate spreads across euro-area countries.

Prior to the Global Financial Crisis, the K-spread typically remained below 10 basis points. During the Crisis, the spread became unusually wide and volatile. At the 5-year maturity, it spiked as high as 90 basis points in December 2008. The spread also widened sharply in the more recent Sovereign Debt Crisis, but remained below its Financial Crisis peak. The K-spread is a model-free identification of euro-area market liquidity—it does not rely on a single interpretation of liquidity frictions. It is also tradable in that an investor can form a portfolio comprised of a long KfW bond position and a corresponding short German federal bond position. This position earns the “liquidity spread” and hedges against credit fluctuations.

This article uses the K-spread and other measures to parse euro-area sovereign bond and interbank interest rate spreads into liquidity and credit components over the Global Financial Crisis and the European Debt crisis. Researchers have proposed theoretical models in which liquidity can have an important effect on bond yields, especially during a crisis (Manganelli and Wolswijk, 2009; Favero, Pagano, and von Thadden, 2010; Acharya and Skeie, 2011). Separately, there is evidence of a common factor driving liquidity premia across markets (Chordia, Sarkar, and Subrahmanyam, 2005; Brunnermeier and Pedersen, 2009). In the decomposition of euro-area sovereign yields spreads, the single K-spread’s identification of liquidity relies on commonality across the different member countries’ sovereign bond markets. The results show a strong and significant influence of aggregate market liquidity on sovereign spreads that is robust to controlling for country-specific default risk. The common liquidity component in spreads also explains more variation than is explained by several extant country-specific liquidity measures jointly. The finding that liquidity is an important driver of bond spreads during the Financial Crisis is familiar in the corporate bond literature (e.g., Bao, Pan, and Wang, 2011; Bongaerts, de Jong, and Driessen, 2017). This article highlights the importance of a single liquidity factor for sovereign bond and interbank spreads during crises.

Brunnermeier and Pedersen (2009) and Bolton, Santos, and Scheinkman (2011), model the relationship between aggregate market liquidity and idiosyncratic funding liquidity to explain market features seen in the early stages of the Financial Crisis. To consider a possible link between aggregate bond market liquidity and money markets, I use the K-spread to decompose unsecured interbank rates, assuming proportionality in bond and funding market liquidity. In order to measure credit and liquidity specific to the interbank market, I obtain a novel dataset of high-frequency interbank transactions. I find that the K-spread, constructed in the sovereign bond market, explains a substantial share of interbank spreads beyond what is captured by the interbank measures of credit and liquidity. Both sovereign and interbank spreads are affected by a common liquidity factor. One possible explanation is the close link between the liquidity of sovereign bonds used as collateral in funding markets and the funding rates themselves.1

The plan for the remainder of the article is as follows. Section 2 introduces the data including the liquidity measure’s construction. Section 3 parses the euro-area sovereign bond yield spreads into liquidity and credit components. Section 4 identifies these two effects in interbank interest rate spreads. Section 5 concludes with the article’s contributions and implications.

2. Data

The sample period for this article is January 1, 2007 through December 31, 2014. This captures the nascent Financial Crisis in the summer of 2007, the height of asset price volatility following Lehman Brothers’ bankruptcy, the broad reversal in asset prices in the spring and summer of 2009, and the subsequent return to extreme price volatility during the European Debt Crisis. This section describes the euro-area sovereign debt and EURIBOR-OIS spreads, and discusses the construction of the various measures of liquidity and credit used in this article.

2.1 Sovereign Bond Yield Spreads

Starting with the sovereign bond market, the data sample includes 77 country-maturity pairs: the government debt securities for 11 euro-area member countries (Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Portugal, and Spain) at seven specific maturity points (1, 2, 3, 4, 5, 7, and 10 years).2 To precisely compare these yields, I estimate a smoothed zero-coupon yield curve, for each maturity m, each country c, and each day t, by applying the six-parameter model of Svensson (1994) to the prices of all euro-denominated nominal coupon sovereign debt securities. Bond prices are obtained from Bloomberg.3

The European Central Bank (ECB) is responsible for setting a single monetary policy for the euro-area member countries, giving euro-area interest rates a common term structure. Correlations of euro-area sovereign bond yield levels rose around the time of the 1999 monetary union—see Ehrmann et al. (2011)—largely reflecting the common component in rates influenced by the stance of euro-area monetary policy. To difference out this common term structure, I take German bonds as a benchmark.4 Then, I consider the spread of other countries’ sovereign bond yields relative to those of Germany.5

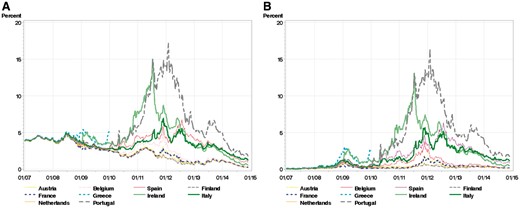

Figure 1 illustrates the movements in sovereign bond yield levels (Panel A) and yield spreads (Panel B), respectively, for the countries in the sample. At the start of the Global Financial Crisis, yield levels mostly declined, but yield spreads widened sharply across countries. After narrowing modestly toward the end of 2009, these spreads widened substantially more during the European Debt Crisis that followed. Higher yields meant that the cost of rolling over existing sovereign debt rose, even in the absence of net new debt issuance. Table 1 gives summary statistics at the 2-, 5-, and 10-year maturities for each country in the sample. Most of the country-maturity yield spreads show a standard deviation over the sample that exceeds the magnitude of the sample-average spread. The onset of this unusual bond market volatility sparked substantial debate; did wider spreads mean that investors were demanding extra compensation amid heightened default likelihood or that market participants were facing increased difficulty in executing transactions?

Euro-area government bond market. (A): Country yields, 5-year maturity; (B): Yield spreads (country yields minus German yield), 5-year maturity. This figure shows sovereign bond yield levels (A), and yield spreads relative to Germany (B), for each of the euro-area countries in the sample, at the 5-year maturity. These are based on zero-coupon yields, formed from smoothed curves fitted to all coupon securities, estimated separately for each country, on each day. The sample period is January 1, 2007 through December 31, 2014, except for Greece, which ends on January 1, 2010. The data are shown at the weekly frequency.

Sovereign bond market summary statistics

| Panel A: Country yield spreads and credit and liquidity measures (deviations from Germany) | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Yield spread | CDS spread | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | Quanto CDS | |||||||||

| (Basis points) | (Basis points) | (Basis points) | (€ million) | (€ million) | (€ million) | (Ratio) | (Basis points) | |||||||||

| Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | |

2-Year Maturity | ||||||||||||||||

| Austria | 19.90 | 23.22 | 19.75 | 26.48 | 0.68 | 1.15 | −20.59 | 63.80 | 0.53 | 4.14 | −8.11 | 297.85 | −0.03 | 0.55 | 6.15 | 9.39 |

| Belgium | 42.34 | 55.45 | 34.79 | 47.88 | 0.44 | 1.18 | −1.26 | 70.57 | 0.80 | 4.17 | −26.09 | 375.34 | −0.18 | 0.52 | 13.58 | 14.89 |

| Spain | 126.35 | 125.22 | 103.54 | 102.17 | 0.58 | 1.24 | −3.83 | 73.31 | −0.17 | 4.54 | −3.98 | 299.49 | −0.05 | 0.75 | 39.43 | 28.23 |

| Finland | 8.17 | 8.68 | 1.39 | 7.21 | 0.08 | 1.20 | −18.91 | 66.07 | 0.06 | 4.27 | −32.95 | 298.35 | 0.00 | 0.58 | −3.28 | 5.79 |

| France | 15.23 | 17.50 | 13.94 | 19.01 | 0.39 | 0.79 | 17.46 | 81.93 | 0.48 | 4.38 | −20.28 | 304.52 | −0.11 | 0.49 | 9.48 | 10.88 |

| Greece | 190.24 | 283.90 | 172.01 | 274.50 | 0.48 | 1.10 | −27.32 | 78.56 | −1.54 | 3.83 | −1.61 | 267.50 | −0.03 | 0.41 | 0.00 | 0.00 |

| Ireland | 204.15 | 280.03 | 215.88 | 283.72 | 0.51 | 1.33 | −24.50 | 63.64 | −1.73 | 4.62 | 44.38 | 261.58 | −0.07 | 0.90 | 27.81 | 23.68 |

| Italy | 123.32 | 121.86 | 102.27 | 106.98 | −0.25 | 0.80 | 310.74 | 240.20 | −2.14 | 3.72 | −15.32 | 331.84 | −0.27 | 0.46 | 26.06 | 17.44 |

| Netherlands | 3.67 | 9.44 | 7.31 | 11.14 | −0.36 | 0.92 | 13.75 | 140.79 | 1.77 | 4.96 | 18.51 | 611.72 | −0.23 | 0.48 | 1.47 | 6.26 |

| Portugal | 333.40 | 427.42 | 320.38 | 445.58 | −0.05 | 1.18 | −7.41 | 71.20 | −0.83 | 4.42 | −20.06 | 364.76 | −0.32 | 0.49 | 37.02 | 31.41 |

5-Year Maturity | ||||||||||||||||

| Austria | 38.19 | 31.76 | 26.56 | 29.79 | 4.81 | 3.70 | −1.78 | 42.35 | 1.78 | 3.94 | −20.63 | 248.16 | 0.08 | 1.43 | 6.14 | 7.11 |

| Belgium | 64.75 | 61.64 | 45.31 | 48.77 | 3.91 | 2.73 | 40.52 | 79.53 | 2.28 | 3.19 | −37.97 | 306.02 | −0.35 | 1.13 | 17.41 | 11.11 |

| Spain | 163.40 | 146.86 | 120.80 | 102.05 | 4.06 | 3.47 | 38.82 | 89.30 | 0.89 | 3.56 | 9.88 | 272.61 | −0.04 | 1.56 | 38.48 | 21.37 |

| Finland | 22.36 | 16.24 | 1.09 | 8.54 | 3.37 | 3.00 | 10.54 | 58.09 | 2.48 | 3.40 | −57.68 | 336.68 | −0.18 | 1.10 | −11.47 | 13.39 |

| France | 32.75 | 30.34 | 22.50 | 22.27 | 3.83 | 2.24 | 40.69 | 84.59 | 1.55 | 3.26 | −6.90 | 245.16 | −0.20 | 1.10 | 15.83 | 11.12 |

| Greece | 197.08 | 263.49 | 161.67 | 224.82 | 2.70 | 2.97 | 4.00 | 50.21 | −0.24 | 2.98 | 10.60 | 185.95 | −0.15 | 1.23 | 0.00 | 0.00 |

| Ireland | 244.75 | 249.38 | 200.15 | 219.85 | 5.39 | 3.86 | −9.33 | 35.34 | −0.44 | 3.59 | −9.44 | 219.18 | 0.55 | 3.48 | 24.03 | 16.05 |

| Italy | 154.79 | 134.29 | 124.46 | 104.64 | 2.56 | 2.65 | 239.20 | 283.73 | −0.70 | 2.72 | −5.07 | 320.85 | −0.45 | 1.03 | 25.83 | 13.71 |

| Netherlands | 27.22 | 17.90 | 9.00 | 11.29 | 1.31 | 2.57 | 71.42 | 273.14 | 3.38 | 3.93 | 78.52 | 846.50 | −0.50 | 0.97 | 0.22 | 8.00 |

| Portugal | 363.40 | 390.42 | 293.36 | 331.60 | 5.25 | 3.69 | 14.76 | 71.52 | 0.53 | 3.20 | −2.96 | 283.63 | −0.45 | 1.00 | 26.56 | 17.55 |

10-Year Maturity | ||||||||||||||||

| Austria | 38.76 | 29.82 | 26.45 | 28.47 | 8.68 | 5.78 | −6.43 | 44.58 | 1.22 | 3.37 | 12.40 | 265.12 | 0.85 | 2.96 | 6.10 | 7.91 |

| Belgium | 68.03 | 54.95 | 45.20 | 42.30 | 5.66 | 6.73 | 24.95 | 78.87 | 2.54 | 3.15 | 11.68 | 392.37 | −0.20 | 2.74 | 17.46 | 8.66 |

| Spain | 170.82 | 144.29 | 118.14 | 89.47 | 8.29 | 6.30 | 5.98 | 65.88 | 0.49 | 3.47 | −9.14 | 279.64 | 1.76 | 4.74 | 34.07 | 19.41 |

| Finland | 22.54 | 15.19 | −0.02 | 9.72 | 3.82 | 6.65 | 16.61 | 59.60 | 3.40 | 3.00 | −113.39 | 410.31 | −0.66 | 2.26 | −16.50 | 15.28 |

| France | 40.27 | 32.88 | 26.29 | 22.95 | 7.37 | 6.86 | 15.87 | 85.65 | 1.06 | 3.70 | 11.20 | 288.61 | 0.48 | 2.87 | 16.93 | 10.61 |

| Greece | 172.38 | 213.25 | 149.62 | 191.31 | 9.79 | 7.37 | −12.07 | 55.17 | −1.10 | 2.89 | 7.09 | 260.92 | 1.39 | 2.70 | 0.00 | 0.00 |

| Ireland | 241.83 | 205.13 | 177.90 | 172.73 | 8.24 | 5.68 | −13.95 | 40.75 | −0.25 | 3.59 | 0.40 | 243.19 | 1.10 | 5.19 | 18.45 | 16.21 |

| Italy | 164.73 | 128.88 | 124.96 | 93.77 | 6.46 | 6.17 | 120.20 | 202.58 | −1.41 | 2.74 | −12.75 | 308.20 | 0.51 | 2.90 | 21.29 | 14.62 |

| Netherlands | 20.77 | 12.17 | 8.94 | 11.59 | 5.39 | 8.51 | 47.18 | 271.52 | 1.83 | 4.76 | 139.04 | 1261.1 | 0.09 | 2.83 | −0.03 | 10.47 |

| Portugal | 325.68 | 314.68 | 257.96 | 258.16 | 6.31 | 6.69 | 7.47 | 64.65 | −0.04 | 2.74 | −28.48 | 323.31 | 0.04 | 2.41 | 257.96 | 258.16 |

| Panel A: Country yield spreads and credit and liquidity measures (deviations from Germany) | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Yield spread | CDS spread | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | Quanto CDS | |||||||||

| (Basis points) | (Basis points) | (Basis points) | (€ million) | (€ million) | (€ million) | (Ratio) | (Basis points) | |||||||||

| Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | |

2-Year Maturity | ||||||||||||||||

| Austria | 19.90 | 23.22 | 19.75 | 26.48 | 0.68 | 1.15 | −20.59 | 63.80 | 0.53 | 4.14 | −8.11 | 297.85 | −0.03 | 0.55 | 6.15 | 9.39 |

| Belgium | 42.34 | 55.45 | 34.79 | 47.88 | 0.44 | 1.18 | −1.26 | 70.57 | 0.80 | 4.17 | −26.09 | 375.34 | −0.18 | 0.52 | 13.58 | 14.89 |

| Spain | 126.35 | 125.22 | 103.54 | 102.17 | 0.58 | 1.24 | −3.83 | 73.31 | −0.17 | 4.54 | −3.98 | 299.49 | −0.05 | 0.75 | 39.43 | 28.23 |

| Finland | 8.17 | 8.68 | 1.39 | 7.21 | 0.08 | 1.20 | −18.91 | 66.07 | 0.06 | 4.27 | −32.95 | 298.35 | 0.00 | 0.58 | −3.28 | 5.79 |

| France | 15.23 | 17.50 | 13.94 | 19.01 | 0.39 | 0.79 | 17.46 | 81.93 | 0.48 | 4.38 | −20.28 | 304.52 | −0.11 | 0.49 | 9.48 | 10.88 |

| Greece | 190.24 | 283.90 | 172.01 | 274.50 | 0.48 | 1.10 | −27.32 | 78.56 | −1.54 | 3.83 | −1.61 | 267.50 | −0.03 | 0.41 | 0.00 | 0.00 |

| Ireland | 204.15 | 280.03 | 215.88 | 283.72 | 0.51 | 1.33 | −24.50 | 63.64 | −1.73 | 4.62 | 44.38 | 261.58 | −0.07 | 0.90 | 27.81 | 23.68 |

| Italy | 123.32 | 121.86 | 102.27 | 106.98 | −0.25 | 0.80 | 310.74 | 240.20 | −2.14 | 3.72 | −15.32 | 331.84 | −0.27 | 0.46 | 26.06 | 17.44 |

| Netherlands | 3.67 | 9.44 | 7.31 | 11.14 | −0.36 | 0.92 | 13.75 | 140.79 | 1.77 | 4.96 | 18.51 | 611.72 | −0.23 | 0.48 | 1.47 | 6.26 |

| Portugal | 333.40 | 427.42 | 320.38 | 445.58 | −0.05 | 1.18 | −7.41 | 71.20 | −0.83 | 4.42 | −20.06 | 364.76 | −0.32 | 0.49 | 37.02 | 31.41 |

5-Year Maturity | ||||||||||||||||

| Austria | 38.19 | 31.76 | 26.56 | 29.79 | 4.81 | 3.70 | −1.78 | 42.35 | 1.78 | 3.94 | −20.63 | 248.16 | 0.08 | 1.43 | 6.14 | 7.11 |

| Belgium | 64.75 | 61.64 | 45.31 | 48.77 | 3.91 | 2.73 | 40.52 | 79.53 | 2.28 | 3.19 | −37.97 | 306.02 | −0.35 | 1.13 | 17.41 | 11.11 |

| Spain | 163.40 | 146.86 | 120.80 | 102.05 | 4.06 | 3.47 | 38.82 | 89.30 | 0.89 | 3.56 | 9.88 | 272.61 | −0.04 | 1.56 | 38.48 | 21.37 |

| Finland | 22.36 | 16.24 | 1.09 | 8.54 | 3.37 | 3.00 | 10.54 | 58.09 | 2.48 | 3.40 | −57.68 | 336.68 | −0.18 | 1.10 | −11.47 | 13.39 |

| France | 32.75 | 30.34 | 22.50 | 22.27 | 3.83 | 2.24 | 40.69 | 84.59 | 1.55 | 3.26 | −6.90 | 245.16 | −0.20 | 1.10 | 15.83 | 11.12 |

| Greece | 197.08 | 263.49 | 161.67 | 224.82 | 2.70 | 2.97 | 4.00 | 50.21 | −0.24 | 2.98 | 10.60 | 185.95 | −0.15 | 1.23 | 0.00 | 0.00 |

| Ireland | 244.75 | 249.38 | 200.15 | 219.85 | 5.39 | 3.86 | −9.33 | 35.34 | −0.44 | 3.59 | −9.44 | 219.18 | 0.55 | 3.48 | 24.03 | 16.05 |

| Italy | 154.79 | 134.29 | 124.46 | 104.64 | 2.56 | 2.65 | 239.20 | 283.73 | −0.70 | 2.72 | −5.07 | 320.85 | −0.45 | 1.03 | 25.83 | 13.71 |

| Netherlands | 27.22 | 17.90 | 9.00 | 11.29 | 1.31 | 2.57 | 71.42 | 273.14 | 3.38 | 3.93 | 78.52 | 846.50 | −0.50 | 0.97 | 0.22 | 8.00 |

| Portugal | 363.40 | 390.42 | 293.36 | 331.60 | 5.25 | 3.69 | 14.76 | 71.52 | 0.53 | 3.20 | −2.96 | 283.63 | −0.45 | 1.00 | 26.56 | 17.55 |

10-Year Maturity | ||||||||||||||||

| Austria | 38.76 | 29.82 | 26.45 | 28.47 | 8.68 | 5.78 | −6.43 | 44.58 | 1.22 | 3.37 | 12.40 | 265.12 | 0.85 | 2.96 | 6.10 | 7.91 |

| Belgium | 68.03 | 54.95 | 45.20 | 42.30 | 5.66 | 6.73 | 24.95 | 78.87 | 2.54 | 3.15 | 11.68 | 392.37 | −0.20 | 2.74 | 17.46 | 8.66 |

| Spain | 170.82 | 144.29 | 118.14 | 89.47 | 8.29 | 6.30 | 5.98 | 65.88 | 0.49 | 3.47 | −9.14 | 279.64 | 1.76 | 4.74 | 34.07 | 19.41 |

| Finland | 22.54 | 15.19 | −0.02 | 9.72 | 3.82 | 6.65 | 16.61 | 59.60 | 3.40 | 3.00 | −113.39 | 410.31 | −0.66 | 2.26 | −16.50 | 15.28 |

| France | 40.27 | 32.88 | 26.29 | 22.95 | 7.37 | 6.86 | 15.87 | 85.65 | 1.06 | 3.70 | 11.20 | 288.61 | 0.48 | 2.87 | 16.93 | 10.61 |

| Greece | 172.38 | 213.25 | 149.62 | 191.31 | 9.79 | 7.37 | −12.07 | 55.17 | −1.10 | 2.89 | 7.09 | 260.92 | 1.39 | 2.70 | 0.00 | 0.00 |

| Ireland | 241.83 | 205.13 | 177.90 | 172.73 | 8.24 | 5.68 | −13.95 | 40.75 | −0.25 | 3.59 | 0.40 | 243.19 | 1.10 | 5.19 | 18.45 | 16.21 |

| Italy | 164.73 | 128.88 | 124.96 | 93.77 | 6.46 | 6.17 | 120.20 | 202.58 | −1.41 | 2.74 | −12.75 | 308.20 | 0.51 | 2.90 | 21.29 | 14.62 |

| Netherlands | 20.77 | 12.17 | 8.94 | 11.59 | 5.39 | 8.51 | 47.18 | 271.52 | 1.83 | 4.76 | 139.04 | 1261.1 | 0.09 | 2.83 | −0.03 | 10.47 |

| Portugal | 325.68 | 314.68 | 257.96 | 258.16 | 6.31 | 6.69 | 7.47 | 64.65 | −0.04 | 2.74 | −28.48 | 323.31 | 0.04 | 2.41 | 257.96 | 258.16 |

Sovereign bond market summary statistics

| Panel A: Country yield spreads and credit and liquidity measures (deviations from Germany) | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Yield spread | CDS spread | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | Quanto CDS | |||||||||

| (Basis points) | (Basis points) | (Basis points) | (€ million) | (€ million) | (€ million) | (Ratio) | (Basis points) | |||||||||

| Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | |

2-Year Maturity | ||||||||||||||||

| Austria | 19.90 | 23.22 | 19.75 | 26.48 | 0.68 | 1.15 | −20.59 | 63.80 | 0.53 | 4.14 | −8.11 | 297.85 | −0.03 | 0.55 | 6.15 | 9.39 |

| Belgium | 42.34 | 55.45 | 34.79 | 47.88 | 0.44 | 1.18 | −1.26 | 70.57 | 0.80 | 4.17 | −26.09 | 375.34 | −0.18 | 0.52 | 13.58 | 14.89 |

| Spain | 126.35 | 125.22 | 103.54 | 102.17 | 0.58 | 1.24 | −3.83 | 73.31 | −0.17 | 4.54 | −3.98 | 299.49 | −0.05 | 0.75 | 39.43 | 28.23 |

| Finland | 8.17 | 8.68 | 1.39 | 7.21 | 0.08 | 1.20 | −18.91 | 66.07 | 0.06 | 4.27 | −32.95 | 298.35 | 0.00 | 0.58 | −3.28 | 5.79 |

| France | 15.23 | 17.50 | 13.94 | 19.01 | 0.39 | 0.79 | 17.46 | 81.93 | 0.48 | 4.38 | −20.28 | 304.52 | −0.11 | 0.49 | 9.48 | 10.88 |

| Greece | 190.24 | 283.90 | 172.01 | 274.50 | 0.48 | 1.10 | −27.32 | 78.56 | −1.54 | 3.83 | −1.61 | 267.50 | −0.03 | 0.41 | 0.00 | 0.00 |

| Ireland | 204.15 | 280.03 | 215.88 | 283.72 | 0.51 | 1.33 | −24.50 | 63.64 | −1.73 | 4.62 | 44.38 | 261.58 | −0.07 | 0.90 | 27.81 | 23.68 |

| Italy | 123.32 | 121.86 | 102.27 | 106.98 | −0.25 | 0.80 | 310.74 | 240.20 | −2.14 | 3.72 | −15.32 | 331.84 | −0.27 | 0.46 | 26.06 | 17.44 |

| Netherlands | 3.67 | 9.44 | 7.31 | 11.14 | −0.36 | 0.92 | 13.75 | 140.79 | 1.77 | 4.96 | 18.51 | 611.72 | −0.23 | 0.48 | 1.47 | 6.26 |

| Portugal | 333.40 | 427.42 | 320.38 | 445.58 | −0.05 | 1.18 | −7.41 | 71.20 | −0.83 | 4.42 | −20.06 | 364.76 | −0.32 | 0.49 | 37.02 | 31.41 |

5-Year Maturity | ||||||||||||||||

| Austria | 38.19 | 31.76 | 26.56 | 29.79 | 4.81 | 3.70 | −1.78 | 42.35 | 1.78 | 3.94 | −20.63 | 248.16 | 0.08 | 1.43 | 6.14 | 7.11 |

| Belgium | 64.75 | 61.64 | 45.31 | 48.77 | 3.91 | 2.73 | 40.52 | 79.53 | 2.28 | 3.19 | −37.97 | 306.02 | −0.35 | 1.13 | 17.41 | 11.11 |

| Spain | 163.40 | 146.86 | 120.80 | 102.05 | 4.06 | 3.47 | 38.82 | 89.30 | 0.89 | 3.56 | 9.88 | 272.61 | −0.04 | 1.56 | 38.48 | 21.37 |

| Finland | 22.36 | 16.24 | 1.09 | 8.54 | 3.37 | 3.00 | 10.54 | 58.09 | 2.48 | 3.40 | −57.68 | 336.68 | −0.18 | 1.10 | −11.47 | 13.39 |

| France | 32.75 | 30.34 | 22.50 | 22.27 | 3.83 | 2.24 | 40.69 | 84.59 | 1.55 | 3.26 | −6.90 | 245.16 | −0.20 | 1.10 | 15.83 | 11.12 |

| Greece | 197.08 | 263.49 | 161.67 | 224.82 | 2.70 | 2.97 | 4.00 | 50.21 | −0.24 | 2.98 | 10.60 | 185.95 | −0.15 | 1.23 | 0.00 | 0.00 |

| Ireland | 244.75 | 249.38 | 200.15 | 219.85 | 5.39 | 3.86 | −9.33 | 35.34 | −0.44 | 3.59 | −9.44 | 219.18 | 0.55 | 3.48 | 24.03 | 16.05 |

| Italy | 154.79 | 134.29 | 124.46 | 104.64 | 2.56 | 2.65 | 239.20 | 283.73 | −0.70 | 2.72 | −5.07 | 320.85 | −0.45 | 1.03 | 25.83 | 13.71 |

| Netherlands | 27.22 | 17.90 | 9.00 | 11.29 | 1.31 | 2.57 | 71.42 | 273.14 | 3.38 | 3.93 | 78.52 | 846.50 | −0.50 | 0.97 | 0.22 | 8.00 |

| Portugal | 363.40 | 390.42 | 293.36 | 331.60 | 5.25 | 3.69 | 14.76 | 71.52 | 0.53 | 3.20 | −2.96 | 283.63 | −0.45 | 1.00 | 26.56 | 17.55 |

10-Year Maturity | ||||||||||||||||

| Austria | 38.76 | 29.82 | 26.45 | 28.47 | 8.68 | 5.78 | −6.43 | 44.58 | 1.22 | 3.37 | 12.40 | 265.12 | 0.85 | 2.96 | 6.10 | 7.91 |

| Belgium | 68.03 | 54.95 | 45.20 | 42.30 | 5.66 | 6.73 | 24.95 | 78.87 | 2.54 | 3.15 | 11.68 | 392.37 | −0.20 | 2.74 | 17.46 | 8.66 |

| Spain | 170.82 | 144.29 | 118.14 | 89.47 | 8.29 | 6.30 | 5.98 | 65.88 | 0.49 | 3.47 | −9.14 | 279.64 | 1.76 | 4.74 | 34.07 | 19.41 |

| Finland | 22.54 | 15.19 | −0.02 | 9.72 | 3.82 | 6.65 | 16.61 | 59.60 | 3.40 | 3.00 | −113.39 | 410.31 | −0.66 | 2.26 | −16.50 | 15.28 |

| France | 40.27 | 32.88 | 26.29 | 22.95 | 7.37 | 6.86 | 15.87 | 85.65 | 1.06 | 3.70 | 11.20 | 288.61 | 0.48 | 2.87 | 16.93 | 10.61 |

| Greece | 172.38 | 213.25 | 149.62 | 191.31 | 9.79 | 7.37 | −12.07 | 55.17 | −1.10 | 2.89 | 7.09 | 260.92 | 1.39 | 2.70 | 0.00 | 0.00 |

| Ireland | 241.83 | 205.13 | 177.90 | 172.73 | 8.24 | 5.68 | −13.95 | 40.75 | −0.25 | 3.59 | 0.40 | 243.19 | 1.10 | 5.19 | 18.45 | 16.21 |

| Italy | 164.73 | 128.88 | 124.96 | 93.77 | 6.46 | 6.17 | 120.20 | 202.58 | −1.41 | 2.74 | −12.75 | 308.20 | 0.51 | 2.90 | 21.29 | 14.62 |

| Netherlands | 20.77 | 12.17 | 8.94 | 11.59 | 5.39 | 8.51 | 47.18 | 271.52 | 1.83 | 4.76 | 139.04 | 1261.1 | 0.09 | 2.83 | −0.03 | 10.47 |

| Portugal | 325.68 | 314.68 | 257.96 | 258.16 | 6.31 | 6.69 | 7.47 | 64.65 | −0.04 | 2.74 | −28.48 | 323.31 | 0.04 | 2.41 | 257.96 | 258.16 |

| Panel A: Country yield spreads and credit and liquidity measures (deviations from Germany) | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Yield spread | CDS spread | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | Quanto CDS | |||||||||

| (Basis points) | (Basis points) | (Basis points) | (€ million) | (€ million) | (€ million) | (Ratio) | (Basis points) | |||||||||

| Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | Mean | St Dev | |

2-Year Maturity | ||||||||||||||||

| Austria | 19.90 | 23.22 | 19.75 | 26.48 | 0.68 | 1.15 | −20.59 | 63.80 | 0.53 | 4.14 | −8.11 | 297.85 | −0.03 | 0.55 | 6.15 | 9.39 |

| Belgium | 42.34 | 55.45 | 34.79 | 47.88 | 0.44 | 1.18 | −1.26 | 70.57 | 0.80 | 4.17 | −26.09 | 375.34 | −0.18 | 0.52 | 13.58 | 14.89 |

| Spain | 126.35 | 125.22 | 103.54 | 102.17 | 0.58 | 1.24 | −3.83 | 73.31 | −0.17 | 4.54 | −3.98 | 299.49 | −0.05 | 0.75 | 39.43 | 28.23 |

| Finland | 8.17 | 8.68 | 1.39 | 7.21 | 0.08 | 1.20 | −18.91 | 66.07 | 0.06 | 4.27 | −32.95 | 298.35 | 0.00 | 0.58 | −3.28 | 5.79 |

| France | 15.23 | 17.50 | 13.94 | 19.01 | 0.39 | 0.79 | 17.46 | 81.93 | 0.48 | 4.38 | −20.28 | 304.52 | −0.11 | 0.49 | 9.48 | 10.88 |

| Greece | 190.24 | 283.90 | 172.01 | 274.50 | 0.48 | 1.10 | −27.32 | 78.56 | −1.54 | 3.83 | −1.61 | 267.50 | −0.03 | 0.41 | 0.00 | 0.00 |

| Ireland | 204.15 | 280.03 | 215.88 | 283.72 | 0.51 | 1.33 | −24.50 | 63.64 | −1.73 | 4.62 | 44.38 | 261.58 | −0.07 | 0.90 | 27.81 | 23.68 |

| Italy | 123.32 | 121.86 | 102.27 | 106.98 | −0.25 | 0.80 | 310.74 | 240.20 | −2.14 | 3.72 | −15.32 | 331.84 | −0.27 | 0.46 | 26.06 | 17.44 |

| Netherlands | 3.67 | 9.44 | 7.31 | 11.14 | −0.36 | 0.92 | 13.75 | 140.79 | 1.77 | 4.96 | 18.51 | 611.72 | −0.23 | 0.48 | 1.47 | 6.26 |

| Portugal | 333.40 | 427.42 | 320.38 | 445.58 | −0.05 | 1.18 | −7.41 | 71.20 | −0.83 | 4.42 | −20.06 | 364.76 | −0.32 | 0.49 | 37.02 | 31.41 |

5-Year Maturity | ||||||||||||||||

| Austria | 38.19 | 31.76 | 26.56 | 29.79 | 4.81 | 3.70 | −1.78 | 42.35 | 1.78 | 3.94 | −20.63 | 248.16 | 0.08 | 1.43 | 6.14 | 7.11 |

| Belgium | 64.75 | 61.64 | 45.31 | 48.77 | 3.91 | 2.73 | 40.52 | 79.53 | 2.28 | 3.19 | −37.97 | 306.02 | −0.35 | 1.13 | 17.41 | 11.11 |

| Spain | 163.40 | 146.86 | 120.80 | 102.05 | 4.06 | 3.47 | 38.82 | 89.30 | 0.89 | 3.56 | 9.88 | 272.61 | −0.04 | 1.56 | 38.48 | 21.37 |

| Finland | 22.36 | 16.24 | 1.09 | 8.54 | 3.37 | 3.00 | 10.54 | 58.09 | 2.48 | 3.40 | −57.68 | 336.68 | −0.18 | 1.10 | −11.47 | 13.39 |

| France | 32.75 | 30.34 | 22.50 | 22.27 | 3.83 | 2.24 | 40.69 | 84.59 | 1.55 | 3.26 | −6.90 | 245.16 | −0.20 | 1.10 | 15.83 | 11.12 |

| Greece | 197.08 | 263.49 | 161.67 | 224.82 | 2.70 | 2.97 | 4.00 | 50.21 | −0.24 | 2.98 | 10.60 | 185.95 | −0.15 | 1.23 | 0.00 | 0.00 |

| Ireland | 244.75 | 249.38 | 200.15 | 219.85 | 5.39 | 3.86 | −9.33 | 35.34 | −0.44 | 3.59 | −9.44 | 219.18 | 0.55 | 3.48 | 24.03 | 16.05 |

| Italy | 154.79 | 134.29 | 124.46 | 104.64 | 2.56 | 2.65 | 239.20 | 283.73 | −0.70 | 2.72 | −5.07 | 320.85 | −0.45 | 1.03 | 25.83 | 13.71 |

| Netherlands | 27.22 | 17.90 | 9.00 | 11.29 | 1.31 | 2.57 | 71.42 | 273.14 | 3.38 | 3.93 | 78.52 | 846.50 | −0.50 | 0.97 | 0.22 | 8.00 |

| Portugal | 363.40 | 390.42 | 293.36 | 331.60 | 5.25 | 3.69 | 14.76 | 71.52 | 0.53 | 3.20 | −2.96 | 283.63 | −0.45 | 1.00 | 26.56 | 17.55 |

10-Year Maturity | ||||||||||||||||

| Austria | 38.76 | 29.82 | 26.45 | 28.47 | 8.68 | 5.78 | −6.43 | 44.58 | 1.22 | 3.37 | 12.40 | 265.12 | 0.85 | 2.96 | 6.10 | 7.91 |

| Belgium | 68.03 | 54.95 | 45.20 | 42.30 | 5.66 | 6.73 | 24.95 | 78.87 | 2.54 | 3.15 | 11.68 | 392.37 | −0.20 | 2.74 | 17.46 | 8.66 |

| Spain | 170.82 | 144.29 | 118.14 | 89.47 | 8.29 | 6.30 | 5.98 | 65.88 | 0.49 | 3.47 | −9.14 | 279.64 | 1.76 | 4.74 | 34.07 | 19.41 |

| Finland | 22.54 | 15.19 | −0.02 | 9.72 | 3.82 | 6.65 | 16.61 | 59.60 | 3.40 | 3.00 | −113.39 | 410.31 | −0.66 | 2.26 | −16.50 | 15.28 |

| France | 40.27 | 32.88 | 26.29 | 22.95 | 7.37 | 6.86 | 15.87 | 85.65 | 1.06 | 3.70 | 11.20 | 288.61 | 0.48 | 2.87 | 16.93 | 10.61 |

| Greece | 172.38 | 213.25 | 149.62 | 191.31 | 9.79 | 7.37 | −12.07 | 55.17 | −1.10 | 2.89 | 7.09 | 260.92 | 1.39 | 2.70 | 0.00 | 0.00 |

| Ireland | 241.83 | 205.13 | 177.90 | 172.73 | 8.24 | 5.68 | −13.95 | 40.75 | −0.25 | 3.59 | 0.40 | 243.19 | 1.10 | 5.19 | 18.45 | 16.21 |

| Italy | 164.73 | 128.88 | 124.96 | 93.77 | 6.46 | 6.17 | 120.20 | 202.58 | −1.41 | 2.74 | −12.75 | 308.20 | 0.51 | 2.90 | 21.29 | 14.62 |

| Netherlands | 20.77 | 12.17 | 8.94 | 11.59 | 5.39 | 8.51 | 47.18 | 271.52 | 1.83 | 4.76 | 139.04 | 1261.1 | 0.09 | 2.83 | −0.03 | 10.47 |

| Portugal | 325.68 | 314.68 | 257.96 | 258.16 | 6.31 | 6.69 | 7.47 | 64.65 | −0.04 | 2.74 | −28.48 | 323.31 | 0.04 | 2.41 | 257.96 | 258.16 |

Continued

| Panel B: K-Spread and German microstructure liquidity measure statistics and correlation | |||||||

|---|---|---|---|---|---|---|---|

| K-Spread | Correlation with K-Spread | ||||||

| (Basis points) | (Basis points) | ||||||

| Mean | St Dev | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | |

| 2-Year Maturity | 26.02 | 20.43 | 0.50 | −0.13 | −0.05 | 0.06 | 0.15 |

| 5-Year Maturity | 35.80 | 19.73 | 0.75 | −0.18 | −0.04 | −0.06 | 0.36 |

| 10-Year Maturity | 30.35 | 16.14 | 0.33 | −0.17 | −0.30 | 0.14 | 0.23 |

| Panel B: K-Spread and German microstructure liquidity measure statistics and correlation | |||||||

|---|---|---|---|---|---|---|---|

| K-Spread | Correlation with K-Spread | ||||||

| (Basis points) | (Basis points) | ||||||

| Mean | St Dev | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | |

| 2-Year Maturity | 26.02 | 20.43 | 0.50 | −0.13 | −0.05 | 0.06 | 0.15 |

| 5-Year Maturity | 35.80 | 19.73 | 0.75 | −0.18 | −0.04 | −0.06 | 0.36 |

| 10-Year Maturity | 30.35 | 16.14 | 0.33 | −0.17 | −0.30 | 0.14 | 0.23 |

| Panel C: Liquidity and credit measure correlation | ||||||||

|---|---|---|---|---|---|---|---|---|

| K-Spread | Sovereign CDS | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | Quanto CDS | |

2-Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.20 | 1.00 | ||||||

| Bid-ask | −0.19 | −0.09 | 1.00 | |||||

| Daily volume | −0.02 | −0.02 | −0.14 | 1.00 | ||||

| Trade size | 0.07 | −0.21 | −0.04 | 0.03 | 1.00 | |||

| Order flow | 0.00 | −0.02 | −0.02 | 0.14 | 0.11 | 1.00 | ||

| BW index | −0.12 | −0.17 | 0.26 | −0.16 | −0.33 | −0.02 | 1.00 | |

| Quanto CDS | 0.38 | 0.68 | −0.08 | 0.03 | −0.12 | −0.02 | −0.12 | 1.00 |

5- Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.27 | 1.00 | ||||||

| Bid-ask | −0.15 | 0.17 | 1.00 | |||||

| Daily volume | −0.04 | −0.04 | −0.13 | 1.00 | ||||

| Trade size | −0.01 | −0.25 | −0.12 | 0.14 | 1.00 | |||

| Order flow | 0.04 | 0.00 | −0.03 | 0.36 | 0.14 | 1.00 | ||

| BW index | −0.19 | −0.15 | 0.27 | −0.14 | −0.36 | −0.03 | 1.00 | |

| Quanto CDS | 0.24 | 0.57 | 0.06 | −0.01 | −0.26 | 0.03 | −0.05 | 1.00 |

10-Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.33 | 1.00 | ||||||

| Bid-ask | 0.20 | 0.01 | 1.00 | |||||

| Daily volume | −0.04 | −0.05 | −0.18 | 1.00 | ||||

| Trade size | 0.14 | −0.12 | −0.09 | 0.22 | 1.00 | |||

| Order flow | −0.02 | −0.02 | −0.01 | 0.52 | 0.17 | 1.00 | ||

| BW index | −0.07 | −0.04 | 0.33 | −0.16 | −0.38 | −0.02 | 1.00 | |

| Quanto CDS | 0.24 | 0.48 | 0.09 | −0.06 | −0.22 | −0.02 | 0.10 | 1.00 |

| Panel C: Liquidity and credit measure correlation | ||||||||

|---|---|---|---|---|---|---|---|---|

| K-Spread | Sovereign CDS | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | Quanto CDS | |

2-Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.20 | 1.00 | ||||||

| Bid-ask | −0.19 | −0.09 | 1.00 | |||||

| Daily volume | −0.02 | −0.02 | −0.14 | 1.00 | ||||

| Trade size | 0.07 | −0.21 | −0.04 | 0.03 | 1.00 | |||

| Order flow | 0.00 | −0.02 | −0.02 | 0.14 | 0.11 | 1.00 | ||

| BW index | −0.12 | −0.17 | 0.26 | −0.16 | −0.33 | −0.02 | 1.00 | |

| Quanto CDS | 0.38 | 0.68 | −0.08 | 0.03 | −0.12 | −0.02 | −0.12 | 1.00 |

5- Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.27 | 1.00 | ||||||

| Bid-ask | −0.15 | 0.17 | 1.00 | |||||

| Daily volume | −0.04 | −0.04 | −0.13 | 1.00 | ||||

| Trade size | −0.01 | −0.25 | −0.12 | 0.14 | 1.00 | |||

| Order flow | 0.04 | 0.00 | −0.03 | 0.36 | 0.14 | 1.00 | ||

| BW index | −0.19 | −0.15 | 0.27 | −0.14 | −0.36 | −0.03 | 1.00 | |

| Quanto CDS | 0.24 | 0.57 | 0.06 | −0.01 | −0.26 | 0.03 | −0.05 | 1.00 |

10-Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.33 | 1.00 | ||||||

| Bid-ask | 0.20 | 0.01 | 1.00 | |||||

| Daily volume | −0.04 | −0.05 | −0.18 | 1.00 | ||||

| Trade size | 0.14 | −0.12 | −0.09 | 0.22 | 1.00 | |||

| Order flow | −0.02 | −0.02 | −0.01 | 0.52 | 0.17 | 1.00 | ||

| BW index | −0.07 | −0.04 | 0.33 | −0.16 | −0.38 | −0.02 | 1.00 | |

| Quanto CDS | 0.24 | 0.48 | 0.09 | −0.06 | −0.22 | −0.02 | 0.10 | 1.00 |

This table reports summary statistics for euro-area sovereign bonds, at the 2-, 5-, and 10-year maturities. Panel A reports the mean and standard deviation for sovereign zero-coupon bond yield spreads, CDS spreads, Quanto CDS and microstructure liquidity measures for 10 euro-area countries. Each measure is expressed as the country indicator’s deviation from the German indicator. Panel B reports the K-spread’s mean, standard deviation and its correlation with the microstructure liquidity indicators for Germany. Panel C reports correlations among the K-spread liquidity measure and the other sovereign bond market liquidity and credit indicators that are reported in Panel A. The correlations are run separately for each maturity, using all country data. The K-spread is formed as the KfW agency bond yield minus the German federal government bond yield. The CDS spread is each country’s sovereign debt premium minus German sovereign debt premium. The Quanto CDS measure is each country’s Quanto CDS spread minus the German Quanto CDS spread. The market microstructure liquidity measures are formed using sovereign bond transaction data from the MTS trading platform, as the country measure minus the German measure. All statistics are formed from daily frequency data. The sample period is from January 1, 2007 to December 31, 2014, except that the Greek data ends on January 1, 2010, and the Quanto CDS variable starts on January 1, 2010 for all countries.

Continued

| Panel B: K-Spread and German microstructure liquidity measure statistics and correlation | |||||||

|---|---|---|---|---|---|---|---|

| K-Spread | Correlation with K-Spread | ||||||

| (Basis points) | (Basis points) | ||||||

| Mean | St Dev | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | |

| 2-Year Maturity | 26.02 | 20.43 | 0.50 | −0.13 | −0.05 | 0.06 | 0.15 |

| 5-Year Maturity | 35.80 | 19.73 | 0.75 | −0.18 | −0.04 | −0.06 | 0.36 |

| 10-Year Maturity | 30.35 | 16.14 | 0.33 | −0.17 | −0.30 | 0.14 | 0.23 |

| Panel B: K-Spread and German microstructure liquidity measure statistics and correlation | |||||||

|---|---|---|---|---|---|---|---|

| K-Spread | Correlation with K-Spread | ||||||

| (Basis points) | (Basis points) | ||||||

| Mean | St Dev | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | |

| 2-Year Maturity | 26.02 | 20.43 | 0.50 | −0.13 | −0.05 | 0.06 | 0.15 |

| 5-Year Maturity | 35.80 | 19.73 | 0.75 | −0.18 | −0.04 | −0.06 | 0.36 |

| 10-Year Maturity | 30.35 | 16.14 | 0.33 | −0.17 | −0.30 | 0.14 | 0.23 |

| Panel C: Liquidity and credit measure correlation | ||||||||

|---|---|---|---|---|---|---|---|---|

| K-Spread | Sovereign CDS | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | Quanto CDS | |

2-Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.20 | 1.00 | ||||||

| Bid-ask | −0.19 | −0.09 | 1.00 | |||||

| Daily volume | −0.02 | −0.02 | −0.14 | 1.00 | ||||

| Trade size | 0.07 | −0.21 | −0.04 | 0.03 | 1.00 | |||

| Order flow | 0.00 | −0.02 | −0.02 | 0.14 | 0.11 | 1.00 | ||

| BW index | −0.12 | −0.17 | 0.26 | −0.16 | −0.33 | −0.02 | 1.00 | |

| Quanto CDS | 0.38 | 0.68 | −0.08 | 0.03 | −0.12 | −0.02 | −0.12 | 1.00 |

5- Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.27 | 1.00 | ||||||

| Bid-ask | −0.15 | 0.17 | 1.00 | |||||

| Daily volume | −0.04 | −0.04 | −0.13 | 1.00 | ||||

| Trade size | −0.01 | −0.25 | −0.12 | 0.14 | 1.00 | |||

| Order flow | 0.04 | 0.00 | −0.03 | 0.36 | 0.14 | 1.00 | ||

| BW index | −0.19 | −0.15 | 0.27 | −0.14 | −0.36 | −0.03 | 1.00 | |

| Quanto CDS | 0.24 | 0.57 | 0.06 | −0.01 | −0.26 | 0.03 | −0.05 | 1.00 |

10-Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.33 | 1.00 | ||||||

| Bid-ask | 0.20 | 0.01 | 1.00 | |||||

| Daily volume | −0.04 | −0.05 | −0.18 | 1.00 | ||||

| Trade size | 0.14 | −0.12 | −0.09 | 0.22 | 1.00 | |||

| Order flow | −0.02 | −0.02 | −0.01 | 0.52 | 0.17 | 1.00 | ||

| BW index | −0.07 | −0.04 | 0.33 | −0.16 | −0.38 | −0.02 | 1.00 | |

| Quanto CDS | 0.24 | 0.48 | 0.09 | −0.06 | −0.22 | −0.02 | 0.10 | 1.00 |

| Panel C: Liquidity and credit measure correlation | ||||||||

|---|---|---|---|---|---|---|---|---|

| K-Spread | Sovereign CDS | Bid-Ask | Daily Volume | Trade Size | Order Flow | BW Index | Quanto CDS | |

2-Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.20 | 1.00 | ||||||

| Bid-ask | −0.19 | −0.09 | 1.00 | |||||

| Daily volume | −0.02 | −0.02 | −0.14 | 1.00 | ||||

| Trade size | 0.07 | −0.21 | −0.04 | 0.03 | 1.00 | |||

| Order flow | 0.00 | −0.02 | −0.02 | 0.14 | 0.11 | 1.00 | ||

| BW index | −0.12 | −0.17 | 0.26 | −0.16 | −0.33 | −0.02 | 1.00 | |

| Quanto CDS | 0.38 | 0.68 | −0.08 | 0.03 | −0.12 | −0.02 | −0.12 | 1.00 |

5- Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.27 | 1.00 | ||||||

| Bid-ask | −0.15 | 0.17 | 1.00 | |||||

| Daily volume | −0.04 | −0.04 | −0.13 | 1.00 | ||||

| Trade size | −0.01 | −0.25 | −0.12 | 0.14 | 1.00 | |||

| Order flow | 0.04 | 0.00 | −0.03 | 0.36 | 0.14 | 1.00 | ||

| BW index | −0.19 | −0.15 | 0.27 | −0.14 | −0.36 | −0.03 | 1.00 | |

| Quanto CDS | 0.24 | 0.57 | 0.06 | −0.01 | −0.26 | 0.03 | −0.05 | 1.00 |

10-Year Maturity | ||||||||

| K-Spread | 1.00 | |||||||

| Sovereign CDS | 0.33 | 1.00 | ||||||

| Bid-ask | 0.20 | 0.01 | 1.00 | |||||

| Daily volume | −0.04 | −0.05 | −0.18 | 1.00 | ||||

| Trade size | 0.14 | −0.12 | −0.09 | 0.22 | 1.00 | |||

| Order flow | −0.02 | −0.02 | −0.01 | 0.52 | 0.17 | 1.00 | ||

| BW index | −0.07 | −0.04 | 0.33 | −0.16 | −0.38 | −0.02 | 1.00 | |

| Quanto CDS | 0.24 | 0.48 | 0.09 | −0.06 | −0.22 | −0.02 | 0.10 | 1.00 |

This table reports summary statistics for euro-area sovereign bonds, at the 2-, 5-, and 10-year maturities. Panel A reports the mean and standard deviation for sovereign zero-coupon bond yield spreads, CDS spreads, Quanto CDS and microstructure liquidity measures for 10 euro-area countries. Each measure is expressed as the country indicator’s deviation from the German indicator. Panel B reports the K-spread’s mean, standard deviation and its correlation with the microstructure liquidity indicators for Germany. Panel C reports correlations among the K-spread liquidity measure and the other sovereign bond market liquidity and credit indicators that are reported in Panel A. The correlations are run separately for each maturity, using all country data. The K-spread is formed as the KfW agency bond yield minus the German federal government bond yield. The CDS spread is each country’s sovereign debt premium minus German sovereign debt premium. The Quanto CDS measure is each country’s Quanto CDS spread minus the German Quanto CDS spread. The market microstructure liquidity measures are formed using sovereign bond transaction data from the MTS trading platform, as the country measure minus the German measure. All statistics are formed from daily frequency data. The sample period is from January 1, 2007 to December 31, 2014, except that the Greek data ends on January 1, 2010, and the Quanto CDS variable starts on January 1, 2010 for all countries.

2.2 Interbank Interest Rate Spreads

In the money market, I consider euro interbank borrowing rates (EURIBOR). EURIBOR is the reference rate at which large euro-area banks borrow some notional amount of euro currency, uncollateralized, for a specified term.6 EURIBOR contains a common risk-free term structure and risk components. To remove the common component, I consider the spreads of EURIBOR relative to the euro overnight-index swap (OIS) rate, which I take as a proxy for the risk-free rate. An OIS is a money market derivative, with a payoff determined by the future path of overnight interest rates plus a pure term premium. There is no payment required at inception of the contract. For any maturity of OIS contract, the fixed rate reflects a sequence of refreshed overnight bank credits. For these and other reasons,7 default and liquidity premia in OIS rates are negligible (Brunnermeier, 2009; Packer and Baba, 2009), allowing for the EURIBOR-OIS spread to be interpreted as interbank risk premia.

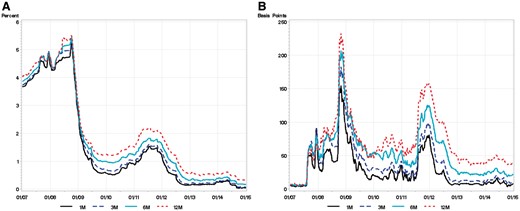

I consider the 1-, 3-, 6-, and 12-month maturity EURIBOR-OIS interest rate spreads, which are the EURIBOR maturities commonly referenced in financial contracts. Panel A of Figure 2 shows a steep decline in the level of EURIBOR rates of roughly 450 basis points across the different maturities over the sample period. This drop was largely driven by the ECB’s crisis-driven monetary policy easing, and thus a lower risk-free rate. During 2008 and 2009, the ECB cut its policy repo rate from 4.25% to 1%. However, Panel B shows a sharp rise in the spread between EURIBOR and OIS rates, first in August 2007, and then most dramatically following Lehman’s Brothers’ bankruptcy in September 2008. In contrast to the all-time high levels that sovereign debt spreads reached during the European Debt Crisis (Figure 1, Panel B), money market spreads peaked during the Global Financial Crisis (Figure 2, Panel B) with the 3- and 6-month EURIBOR-OIS spreads exceeding 150 and 240 basis points, respectively, in the fall of 2008. The unusually steep rise in interbank rates received considerable attention in the press and from policymakers. Higher EURIBOR-OIS spreads worked directly counter to the effect of lower ECB policy rates. Wider spreads mean less accommodative financial conditions ceteris paribus, since many private lending rates are tied to term interbank rates; swap rates, forward rates, interest rate futures, and many mortgage rates in the euro area reference EURIBOR.

Euro-area money market. This figure shows euro-area interbank money market rate levels (A) and spreads (B) for the 1-, 3-, 6- and 12-month maturities. (A) shows the level of the EURIBOR; (B) shows the EURIBOR-OIS interest rate spread, defined as the EURIBOR minus the comparable-maturity OIS rate. The sample period is January 1, 2007 through December 31, 2014. The data are shown at the weekly frequency.

2.3 The K-Spread Measure of Market Liquidity

Market liquidity is the premium demanded for buying or selling a large quantity of an asset, such as a sovereign bond, with immediacy.8 Measuring this empirically is challenging. To identify the liquidity component of euro-area interest rate spreads, I construct a measure of market liquidity that compares the yields of German government bonds with German agency bonds, at specific maturities. German government bonds are highly liquid euro-area securities, backed by the full faith and credit of the German federal government. Their less-liquid counterparts are bonds issued by the German federal government-owned development bank, KfW, which was founded in 1948 to facilitate post-war reconstruction. A key feature of the KfW agency bonds, which safeguards the liquidity measure against any credit effects, is that the German federal government has an explicit iron-clad guarantee—written into the German constitution—for all of KfW’s current and future obligations, equally and without any difference in priority relative to the federal government bond issues. Credit and asset characteristics are entirely controlled for in the measure’s construction.

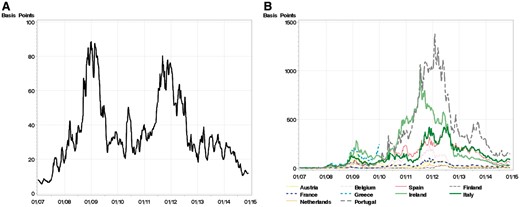

Panel A of Figure 3 plots the K-spread at the 5-year maturity. The spread remains positive over the sample, reflecting the relative ease with which the federal government debt is traded as compared to the agency debt. The liquidity yield differential rises to a local peak of 47 basis points early in the sample period, around the collapse of Bear Stearns in March 2008, and then it reaches a global peak of 90 basis points later that year following Lehman Brothers’ bankruptcy. The K-spread widened again during the Sovereign Debt Crisis, not quite reaching the same magnitude as in the Financial Crisis, but remaining elevated for a protracted period. Since the K-spread is constructed from observed bond prices, identification is not limited to any single model of liquidity frictions (e.g., asymmetric information). The K-spread’s evolution reflects all information impounded in bond yields, including forward-looking future liquidity conditions, a potentially large dimension of liquidity not captured by market microstructure or transaction-based measures that are typically used to measure market liquidity.

K-liquidity spread and country cds spreads. This figure shows a time series of the 5-year maturity K-spread liquidity measure (A) and the 5-year maturity sovereign CDS spread credit measure (B). The K-spread is constructed as the KfW yield minus the comparable-maturity German federal government yield (both zero-coupon yields, formed from smoothed curves fitted to all coupon securities, estimated separately for each day). The Credit Default Swap (CDS) spreads for the sovereign debt of each of the euro-area countries in the sample are relative to that of Germany. The sample period is January 1, 2007 through December 31, 2014, except for Greece, which ends on January 1, 2010. The data are shown at the weekly frequency.

There are some institutional differences between KfW and German federal government bonds that could contribute to their liquidity differential. Although they share the same creditworthiness, KfW and German federal government bonds are not fungible, even in the absence of any difference in characteristics. For instance, there is an active futures market for German 2-, 5- and 10-year federal government bonds, but the comparable-maturity KfW securities cannot be delivered into these futures contracts.9 Federal government bond issuance is also larger and trading volume is higher than for KfW securities.10 Moreover, euro repo funding rates are consistently slightly higher for KfW collateral than for German federal government collateral, reflecting the relative attractiveness of the federal government securities as collateral in funding markets.11 The financing rate differential could be both a cause and a consequence of their greater liquidity (Brunnermeier and Pedersen, 2009; Gorton and Metrick, 2012).

2.4 Market Microstructure Liquidity Measures

In order to compare the proposed K-spread liquidity measure with traditional liquidity measures, and to allow for market-specific liquidity effects, I obtain detailed data on interbank borrowing and sovereign bond transactions. With these data, I construct a set of five microstructure liquidity measures, separately for the sovereign bond market and the interbank market. The measures are: trade size, trading volume, bid-ask spread, order flow, and the bid-ask spread scaled by trading volume (the liquidity index of Bollen and Whaley, 1998), each of which is expressed as a daily average value.

The sovereign bond transactions come from MTS, a large electronic European bond trading platform.12 To allow for the independent variation of each country’s liquidity at various horizons, I construct a separate microstructure measure for each of the 77 country-maturity pairs. Table 1 reports the country-level summary statistics. The measures are expressed relative to their maturity-matched German counterparts, in parallel with the construction of the yield spreads. For instance, the positive sign on Italian bond trading volume at each maturity point means that a greater quantity of Italian debt is traded each day as compared to German debt, on average over the sample. At the 2-year maturity, the daily average transaction volume in Italian bonds (€311 million in excess of German bonds) is higher than that of any other country’s bonds in the sample. However, the average Italian trade sizes are the smallest of any country; the relatively high Italian trading volume is achieved through a high frequency of small trades.

Interbank borrowing transactions, data which are notoriously opaque and difficult to access, are sourced directly from e-MID, a large electronic euro-area interbank trading platform.13 Euro interbank borrowing is concentrated at the very shortest maturities.14 Because of sparse observations at longer horizons, the interbank microstructure measures are formed with overnight transactions. Table 2 summarizes statistics for the interbank measures. The sample-average interbank bid-ask spread is only 5.1 basis points, shown in Panel B. Transaction volume averages €6.7 billion each day, with an average trade size of €27.3 million over the sample.

Interbank money market summary statistics

| Panel A: Interest rates and spreads | ||||||

|---|---|---|---|---|---|---|

| EURIBOR (Percentage points) | OIS (Percentage points) | EURIBOR-OIS (Basis points) | ||||

| Mean | St Dev | Mean | St Dev | Mean | St Dev | |

| 1-Month Maturity | 1.56 | 1.68 | 1.28 | 1.56 | 28.23 | 27.70 |

| 3-Month Maturity | 1.67 | 1.70 | 1.28 | 1.57 | 38.97 | 33.80 |

| 6-Month Maturity | 1.84 | 1.66 | 1.30 | 1.58 | 53.79 | 37.29 |

| 12-Month Maturity | 2.05 | 1.61 | 1.36 | 1.58 | 68.74 | 41.26 |

| Panel A: Interest rates and spreads | ||||||

|---|---|---|---|---|---|---|

| EURIBOR (Percentage points) | OIS (Percentage points) | EURIBOR-OIS (Basis points) | ||||

| Mean | St Dev | Mean | St Dev | Mean | St Dev | |

| 1-Month Maturity | 1.56 | 1.68 | 1.28 | 1.56 | 28.23 | 27.70 |

| 3-Month Maturity | 1.67 | 1.70 | 1.28 | 1.57 | 38.97 | 33.80 |

| 6-Month Maturity | 1.84 | 1.66 | 1.30 | 1.58 | 53.79 | 37.29 |

| 12-Month Maturity | 2.05 | 1.61 | 1.36 | 1.58 | 68.74 | 41.26 |

| Panel B: Liquidity and credit measures | ||||||||

|---|---|---|---|---|---|---|---|---|

| K-Spread (Basis points) | Bank-Tiering (Basis points) | Bank CDS (Basis points) | Bid-Ask (Basis points) | Daily Volume (€ billion) | Trade Size (€ billion) | Order Flow (€ billion) | BW Index (Ratio) | |

| Mean | 15.52 | 8.55 | 158.47 | 5.13 | 6.66 | 27.26 | −0.42 | 1.17 |

| Standard deviation | 20.09 | 12.60 | 146.64 | 6.34 | 6.61 | 12.56 | 0.29 | 1.36 |

Correlation | ||||||||

| K-Spread | 1.00 | |||||||

| Bank-tiering | 0.53 | 1.00 | ||||||

| Bank CDS | 0.16 | 0.37 | 1.00 | |||||

| Bid-ask | 0.61 | 0.81 | 0.27 | 1.00 | ||||

| Daily volume | 0.09 | −0.09 | −0.46 | 0.01 | 1.00 | |||

| Trade size | 0.08 | −0.10 | −0.32 | −0.04 | 0.85 | 1.00 | ||

| Order flow | −0.35 | −0.18 | 0.23 | −0.27 | −0.41 | −0.16 | 1.00 | |

| BW index | 0.37 | 0.72 | 0.44 | 0.81 | −0.29 | −0.30 | −0.12 | 1.00 |

| Panel B: Liquidity and credit measures | ||||||||

|---|---|---|---|---|---|---|---|---|

| K-Spread (Basis points) | Bank-Tiering (Basis points) | Bank CDS (Basis points) | Bid-Ask (Basis points) | Daily Volume (€ billion) | Trade Size (€ billion) | Order Flow (€ billion) | BW Index (Ratio) | |

| Mean | 15.52 | 8.55 | 158.47 | 5.13 | 6.66 | 27.26 | −0.42 | 1.17 |

| Standard deviation | 20.09 | 12.60 | 146.64 | 6.34 | 6.61 | 12.56 | 0.29 | 1.36 |

Correlation | ||||||||

| K-Spread | 1.00 | |||||||

| Bank-tiering | 0.53 | 1.00 | ||||||

| Bank CDS | 0.16 | 0.37 | 1.00 | |||||

| Bid-ask | 0.61 | 0.81 | 0.27 | 1.00 | ||||

| Daily volume | 0.09 | −0.09 | −0.46 | 0.01 | 1.00 | |||

| Trade size | 0.08 | −0.10 | −0.32 | −0.04 | 0.85 | 1.00 | ||

| Order flow | −0.35 | −0.18 | 0.23 | −0.27 | −0.41 | −0.16 | 1.00 | |

| BW index | 0.37 | 0.72 | 0.44 | 0.81 | −0.29 | −0.30 | −0.12 | 1.00 |

This table reports summary statistics for euro-area interbank money markets. Panel A gives the mean and standard deviation of the EURIBOR, the OIS rate and the EURIBOR-OIS interest rate spread at 1-, 3-, 6-, and 12-month maturities. Panel B reports the mean and standard deviation for the 1-year maturity K-spread liquidity measure, the overnight bank-tiering credit measure, the overnight interbank market microstructure liquidity measures and the one-year EURIBOR-member bank average CDS premia. Correlations among these indicators are also reported. The K-spread is formed as the KfW agency bond yield minus the same maturity German federal government bond yield. The bank-tiering credit measure is formed as the average unsecured interbank borrowing rate paid by the highest risk quintile of banks minus that of the lowest risk quintile (described in the Appendix) on each day, using transaction data on overnight interbank borrowing from the e-MID electronic interbank trading platform. The market microstructure liquidity measures are also formed as daily averages, using the overnight interbank data from e-MID. The bank CDS measure is the simple average of the EURIBOR panel banks’ one-year CDS premia on each day. The sample period is from January 1, 2007 to December 31, 2014.

Interbank money market summary statistics

| Panel A: Interest rates and spreads | ||||||

|---|---|---|---|---|---|---|

| EURIBOR (Percentage points) | OIS (Percentage points) | EURIBOR-OIS (Basis points) | ||||

| Mean | St Dev | Mean | St Dev | Mean | St Dev | |

| 1-Month Maturity | 1.56 | 1.68 | 1.28 | 1.56 | 28.23 | 27.70 |

| 3-Month Maturity | 1.67 | 1.70 | 1.28 | 1.57 | 38.97 | 33.80 |

| 6-Month Maturity | 1.84 | 1.66 | 1.30 | 1.58 | 53.79 | 37.29 |

| 12-Month Maturity | 2.05 | 1.61 | 1.36 | 1.58 | 68.74 | 41.26 |

| Panel A: Interest rates and spreads | ||||||

|---|---|---|---|---|---|---|

| EURIBOR (Percentage points) | OIS (Percentage points) | EURIBOR-OIS (Basis points) | ||||

| Mean | St Dev | Mean | St Dev | Mean | St Dev | |

| 1-Month Maturity | 1.56 | 1.68 | 1.28 | 1.56 | 28.23 | 27.70 |

| 3-Month Maturity | 1.67 | 1.70 | 1.28 | 1.57 | 38.97 | 33.80 |

| 6-Month Maturity | 1.84 | 1.66 | 1.30 | 1.58 | 53.79 | 37.29 |

| 12-Month Maturity | 2.05 | 1.61 | 1.36 | 1.58 | 68.74 | 41.26 |

| Panel B: Liquidity and credit measures | ||||||||

|---|---|---|---|---|---|---|---|---|

| K-Spread (Basis points) | Bank-Tiering (Basis points) | Bank CDS (Basis points) | Bid-Ask (Basis points) | Daily Volume (€ billion) | Trade Size (€ billion) | Order Flow (€ billion) | BW Index (Ratio) | |

| Mean | 15.52 | 8.55 | 158.47 | 5.13 | 6.66 | 27.26 | −0.42 | 1.17 |

| Standard deviation | 20.09 | 12.60 | 146.64 | 6.34 | 6.61 | 12.56 | 0.29 | 1.36 |

Correlation | ||||||||

| K-Spread | 1.00 | |||||||

| Bank-tiering | 0.53 | 1.00 | ||||||

| Bank CDS | 0.16 | 0.37 | 1.00 | |||||

| Bid-ask | 0.61 | 0.81 | 0.27 | 1.00 | ||||

| Daily volume | 0.09 | −0.09 | −0.46 | 0.01 | 1.00 | |||

| Trade size | 0.08 | −0.10 | −0.32 | −0.04 | 0.85 | 1.00 | ||

| Order flow | −0.35 | −0.18 | 0.23 | −0.27 | −0.41 | −0.16 | 1.00 | |

| BW index | 0.37 | 0.72 | 0.44 | 0.81 | −0.29 | −0.30 | −0.12 | 1.00 |

| Panel B: Liquidity and credit measures | ||||||||

|---|---|---|---|---|---|---|---|---|

| K-Spread (Basis points) | Bank-Tiering (Basis points) | Bank CDS (Basis points) | Bid-Ask (Basis points) | Daily Volume (€ billion) | Trade Size (€ billion) | Order Flow (€ billion) | BW Index (Ratio) | |

| Mean | 15.52 | 8.55 | 158.47 | 5.13 | 6.66 | 27.26 | −0.42 | 1.17 |

| Standard deviation | 20.09 | 12.60 | 146.64 | 6.34 | 6.61 | 12.56 | 0.29 | 1.36 |

Correlation | ||||||||

| K-Spread | 1.00 | |||||||

| Bank-tiering | 0.53 | 1.00 | ||||||

| Bank CDS | 0.16 | 0.37 | 1.00 | |||||

| Bid-ask | 0.61 | 0.81 | 0.27 | 1.00 | ||||

| Daily volume | 0.09 | −0.09 | −0.46 | 0.01 | 1.00 | |||

| Trade size | 0.08 | −0.10 | −0.32 | −0.04 | 0.85 | 1.00 | ||

| Order flow | −0.35 | −0.18 | 0.23 | −0.27 | −0.41 | −0.16 | 1.00 | |

| BW index | 0.37 | 0.72 | 0.44 | 0.81 | −0.29 | −0.30 | −0.12 | 1.00 |

This table reports summary statistics for euro-area interbank money markets. Panel A gives the mean and standard deviation of the EURIBOR, the OIS rate and the EURIBOR-OIS interest rate spread at 1-, 3-, 6-, and 12-month maturities. Panel B reports the mean and standard deviation for the 1-year maturity K-spread liquidity measure, the overnight bank-tiering credit measure, the overnight interbank market microstructure liquidity measures and the one-year EURIBOR-member bank average CDS premia. Correlations among these indicators are also reported. The K-spread is formed as the KfW agency bond yield minus the same maturity German federal government bond yield. The bank-tiering credit measure is formed as the average unsecured interbank borrowing rate paid by the highest risk quintile of banks minus that of the lowest risk quintile (described in the Appendix) on each day, using transaction data on overnight interbank borrowing from the e-MID electronic interbank trading platform. The market microstructure liquidity measures are also formed as daily averages, using the overnight interbank data from e-MID. The bank CDS measure is the simple average of the EURIBOR panel banks’ one-year CDS premia on each day. The sample period is from January 1, 2007 to December 31, 2014.

2.5 Credit Risk Measures

To identify the credit component in interest rates, I form a new short-horizon measure of interbank credit risk that uses the daily tiering of bank credit that is priced into their borrowing rates, motivated by the default horizon mismatch of credit default swaps (CDS) with interbank spreads (discussed in the next paragraph). The measure is formed by taking the daily difference in the actual borrowing rates of banks with differing creditworthiness. It is constructed with the entire universe of overnight transactions on the e-MID trading platform. The use of this measure assumes that the dispersion and level of credit risk are proportional. This proportionality has been employed by several researchers to explain events in the Financial Crisis. For example, Heider, Hoerova, and Holthausen (2015) model this relationship specifically in interbank markets. Gorton and Ordoñez (2014) use variation in the cross-section of stock returns as a proxy for the level of perceived collateral value. The Appendix describes the proposed bank-tiering measure in detail.

In the sovereign bond market, I consider CDS spreads for each country and maturity in the sample. In the interbank market, I consider the CDS premia for each EURIBOR survey-member bank, as an alternative credit measure to bank-tiering.15 I treat these measures as directly observable credit metrics. The sovereign bond credit measure is defined as the deviation of each country’s CDS spread from the benchmark German CDS spread, on each day for each maturity point, denoted . Measuring interbank credit risk with bank CDS faces the challenge that the EURIBOR-OIS spreads reflect short-horizon risk, while CDS contracts are concentrated at the 5-year maturity. Very short- (or long-) maturity CDS contracts are less likely to be precise measures of default risk, (Pan and Singleton, 2008). To approach the short horizon of the interbank spreads, I use the 1-year CDS premia. Then, I average the CDS premia over the member banks on each day, as in the calculation of EURIBOR.16 All CDS data are obtained from Markit.

Panel B of Figure 3 shows the large rise in sovereign CDS spreads that peaks in the Sovereign Debt Crisis, similar to the sovereign bond spreads shown in Panel B of Figure 1. The interbank credit measures in Figure 4 also both peak in the Debt Crisis. Consistent with the different risk horizons impounded in these measures, the spikes in the bank-tiering measure tend to be steeper and shorter-lived (Panel A) than those of the 1-year bank CDS measure (Panel B).

Money market credit measures. This figure plots the time series of euro-area interbank credit measures. The overnight bank-tiering credit measure (A) is formed as the difference in the average unsecured interbank borrowing rates paid by the banks in the highest and lowest risk quintiles (described in the Appendix) on each day. The bank CDS measure (B) is the simple daily average of the EURIBOR panel banks’ one-year CDS premia. The sample period is January 1, 2007 through December 31, 2014. The data are shown at the weekly frequency.

2.6 Redenomination Risk

Quanto CDS are defined as the spread of a dollar-denominated CDS contract minus the spread of a euro-denominated CDS contract on the same issuer, giving the price of foreign exchange swaps embedded in CDS. To measure redenomination risk in this article, I take each country’s sovereign quanto CDS minus the German sovereign quanto CDS, following De Santis (2015). Panel A of Table 1 shows that the measure is positive for nearly all maturities and countries, consistent with the idea of a premium for protection against risk embedded in the euro currency. Finland and the Netherlands are the exceptions, the two countries with the smallest average CDS spreads. The correlation between quanto CDS and sovereign CDS spreads is 0.68, showing a relatively strong and positive relationship between redenomination and default risk. It makes sense that a higher likelihood of sovereign default increases the likelihood of departure from the currency union.

3. Credit versus Liquidity in Euro-Area Sovereign Bond Spreads

The results of equation (3) are shown in Table 3 at the 2-, 5-, and 10-year maturities. Results are broken out into three samples: the entire sample (Panel A); the period up to the end of 2009, corresponding to the Global Financial Crisis (Panel B); and the period starting in 2010, corresponding to the European Debt crisis (Panel C).17 The full sample results in Panel A show that the pricing of market liquidity conditions is pervasive in euro-area sovereign yields. The coefficient estimates on the K-spread are highly significant and positive for all maturities and countries except Portugal, even controlling for credit. The regression R-squared values from the full-sample estimation show that credit and liquidity jointly explain 44% of the variation in sovereign spreads, averaged over all countries and maturities.

Credit versus liquidity in the sovereign bond market

| Dependent variable: Sovereign yield spread changescmt | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Regressions onto K-Spread Changesmt and CDS Spread Changescmt | |||||||||

| Panel A: Full sample period (January 1, 2007 to December 31, 2014) | |||||||||

| Austria | Belgium | Finland | France | Ireland | Italy | Netherlands | Portugal | Spain | |

2-Year Maturity | |||||||||

| K-Spread2 | 0.41*** | 0.59*** | 0.29*** | 0.29*** | 1.19*** | 1.10*** | 0.24*** | 1.10*** | 0.71*** |

| (0.07) | (0.13) | (0.04) | (0.06) | (0.43) | (0.21) | (0.05) | (0.56) | (0.19) | |

| CDS Spreadc2 | 0.16*** | 0.67*** | 0.09** | 0.28*** | 1.13*** | 0.66*** | 0.14*** | 0.80*** | 0.81*** |

| (0.03) | (0.04) | (0.04) | (0.03) | (0.04) | (0.03) | (0.04) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.21 | 0.46 | 0.13 | 0.25 | 0.63 | 0.52 | 0.11 | 0.56 | 0.61 |

5-Year Maturity | |||||||||

| K-Spread5 | 0.61*** | 0.71*** | 0.40*** | 0.57*** | 0.55** | 1.04*** | 0.38*** | 0.55 | 0.65*** |

| (0.06) | (0.09) | (0.04) | (0.06) | (0.25) | (0.16) | (0.04) | (0.34) | (0.14) | |

| CDS Spreadc5 | 0.28*** | 0.76*** | 0.20*** | 0.42*** | 0.91*** | 0.72*** | 0.28*** | 0.93*** | 0.86*** |

| (0.03) | (0.03) | (0.05) | (0.04) | (0.03) | (0.03) | (0.04) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.40 | 0.63 | 0.19 | 0.42 | 0.66 | 0.61 | 0.32 | 0.66 | 0.70 |

10-Year Maturity | |||||||||

| K-Spread10 | 0.59*** | 0.55*** | 0.30*** | 0.53*** | 0.45** | 0.87*** | 0.25*** | 0.43 | 0.67*** |

| (0.06) | (0.09) | (0.04) | (0.07) | (0.22) | (0.14) | (0.03) | (0.29) | (0.13) | |

| CDS Spreadc10 | 0.27*** | 0.56*** | 0.14*** | 0.35*** | 0.55*** | 0.60*** | 0.18*** | 0.63*** | 0.68*** |

| (0.02) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.42 | 0.52 | 0.14 | 0.34 | 0.54 | 0.62 | 0.25 | 0.57 | 0.65 |

| Dependent variable: Sovereign yield spread changescmt | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Regressions onto K-Spread Changesmt and CDS Spread Changescmt | |||||||||

| Panel A: Full sample period (January 1, 2007 to December 31, 2014) | |||||||||

| Austria | Belgium | Finland | France | Ireland | Italy | Netherlands | Portugal | Spain | |

2-Year Maturity | |||||||||

| K-Spread2 | 0.41*** | 0.59*** | 0.29*** | 0.29*** | 1.19*** | 1.10*** | 0.24*** | 1.10*** | 0.71*** |

| (0.07) | (0.13) | (0.04) | (0.06) | (0.43) | (0.21) | (0.05) | (0.56) | (0.19) | |

| CDS Spreadc2 | 0.16*** | 0.67*** | 0.09** | 0.28*** | 1.13*** | 0.66*** | 0.14*** | 0.80*** | 0.81*** |

| (0.03) | (0.04) | (0.04) | (0.03) | (0.04) | (0.03) | (0.04) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.21 | 0.46 | 0.13 | 0.25 | 0.63 | 0.52 | 0.11 | 0.56 | 0.61 |

5-Year Maturity | |||||||||

| K-Spread5 | 0.61*** | 0.71*** | 0.40*** | 0.57*** | 0.55** | 1.04*** | 0.38*** | 0.55 | 0.65*** |

| (0.06) | (0.09) | (0.04) | (0.06) | (0.25) | (0.16) | (0.04) | (0.34) | (0.14) | |

| CDS Spreadc5 | 0.28*** | 0.76*** | 0.20*** | 0.42*** | 0.91*** | 0.72*** | 0.28*** | 0.93*** | 0.86*** |

| (0.03) | (0.03) | (0.05) | (0.04) | (0.03) | (0.03) | (0.04) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.40 | 0.63 | 0.19 | 0.42 | 0.66 | 0.61 | 0.32 | 0.66 | 0.70 |

10-Year Maturity | |||||||||

| K-Spread10 | 0.59*** | 0.55*** | 0.30*** | 0.53*** | 0.45** | 0.87*** | 0.25*** | 0.43 | 0.67*** |

| (0.06) | (0.09) | (0.04) | (0.07) | (0.22) | (0.14) | (0.03) | (0.29) | (0.13) | |

| CDS Spreadc10 | 0.27*** | 0.56*** | 0.14*** | 0.35*** | 0.55*** | 0.60*** | 0.18*** | 0.63*** | 0.68*** |

| (0.02) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.42 | 0.52 | 0.14 | 0.34 | 0.54 | 0.62 | 0.25 | 0.57 | 0.65 |

Credit versus liquidity in the sovereign bond market

| Dependent variable: Sovereign yield spread changescmt | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Regressions onto K-Spread Changesmt and CDS Spread Changescmt | |||||||||

| Panel A: Full sample period (January 1, 2007 to December 31, 2014) | |||||||||

| Austria | Belgium | Finland | France | Ireland | Italy | Netherlands | Portugal | Spain | |

2-Year Maturity | |||||||||

| K-Spread2 | 0.41*** | 0.59*** | 0.29*** | 0.29*** | 1.19*** | 1.10*** | 0.24*** | 1.10*** | 0.71*** |

| (0.07) | (0.13) | (0.04) | (0.06) | (0.43) | (0.21) | (0.05) | (0.56) | (0.19) | |

| CDS Spreadc2 | 0.16*** | 0.67*** | 0.09** | 0.28*** | 1.13*** | 0.66*** | 0.14*** | 0.80*** | 0.81*** |

| (0.03) | (0.04) | (0.04) | (0.03) | (0.04) | (0.03) | (0.04) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.21 | 0.46 | 0.13 | 0.25 | 0.63 | 0.52 | 0.11 | 0.56 | 0.61 |

5-Year Maturity | |||||||||

| K-Spread5 | 0.61*** | 0.71*** | 0.40*** | 0.57*** | 0.55** | 1.04*** | 0.38*** | 0.55 | 0.65*** |

| (0.06) | (0.09) | (0.04) | (0.06) | (0.25) | (0.16) | (0.04) | (0.34) | (0.14) | |

| CDS Spreadc5 | 0.28*** | 0.76*** | 0.20*** | 0.42*** | 0.91*** | 0.72*** | 0.28*** | 0.93*** | 0.86*** |

| (0.03) | (0.03) | (0.05) | (0.04) | (0.03) | (0.03) | (0.04) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.40 | 0.63 | 0.19 | 0.42 | 0.66 | 0.61 | 0.32 | 0.66 | 0.70 |

10-Year Maturity | |||||||||

| K-Spread10 | 0.59*** | 0.55*** | 0.30*** | 0.53*** | 0.45** | 0.87*** | 0.25*** | 0.43 | 0.67*** |

| (0.06) | (0.09) | (0.04) | (0.07) | (0.22) | (0.14) | (0.03) | (0.29) | (0.13) | |

| CDS Spreadc10 | 0.27*** | 0.56*** | 0.14*** | 0.35*** | 0.55*** | 0.60*** | 0.18*** | 0.63*** | 0.68*** |

| (0.02) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.42 | 0.52 | 0.14 | 0.34 | 0.54 | 0.62 | 0.25 | 0.57 | 0.65 |

| Dependent variable: Sovereign yield spread changescmt | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Regressions onto K-Spread Changesmt and CDS Spread Changescmt | |||||||||

| Panel A: Full sample period (January 1, 2007 to December 31, 2014) | |||||||||

| Austria | Belgium | Finland | France | Ireland | Italy | Netherlands | Portugal | Spain | |

2-Year Maturity | |||||||||

| K-Spread2 | 0.41*** | 0.59*** | 0.29*** | 0.29*** | 1.19*** | 1.10*** | 0.24*** | 1.10*** | 0.71*** |

| (0.07) | (0.13) | (0.04) | (0.06) | (0.43) | (0.21) | (0.05) | (0.56) | (0.19) | |

| CDS Spreadc2 | 0.16*** | 0.67*** | 0.09** | 0.28*** | 1.13*** | 0.66*** | 0.14*** | 0.80*** | 0.81*** |

| (0.03) | (0.04) | (0.04) | (0.03) | (0.04) | (0.03) | (0.04) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.21 | 0.46 | 0.13 | 0.25 | 0.63 | 0.52 | 0.11 | 0.56 | 0.61 |

5-Year Maturity | |||||||||

| K-Spread5 | 0.61*** | 0.71*** | 0.40*** | 0.57*** | 0.55** | 1.04*** | 0.38*** | 0.55 | 0.65*** |

| (0.06) | (0.09) | (0.04) | (0.06) | (0.25) | (0.16) | (0.04) | (0.34) | (0.14) | |

| CDS Spreadc5 | 0.28*** | 0.76*** | 0.20*** | 0.42*** | 0.91*** | 0.72*** | 0.28*** | 0.93*** | 0.86*** |

| (0.03) | (0.03) | (0.05) | (0.04) | (0.03) | (0.03) | (0.04) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.40 | 0.63 | 0.19 | 0.42 | 0.66 | 0.61 | 0.32 | 0.66 | 0.70 |

10-Year Maturity | |||||||||

| K-Spread10 | 0.59*** | 0.55*** | 0.30*** | 0.53*** | 0.45** | 0.87*** | 0.25*** | 0.43 | 0.67*** |

| (0.06) | (0.09) | (0.04) | (0.07) | (0.22) | (0.14) | (0.03) | (0.29) | (0.13) | |

| CDS Spreadc10 | 0.27*** | 0.56*** | 0.14*** | 0.35*** | 0.55*** | 0.60*** | 0.18*** | 0.63*** | 0.68*** |

| (0.02) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | (0.03) | |

| R2-adjusted (%) | 0.42 | 0.52 | 0.14 | 0.34 | 0.54 | 0.62 | 0.25 | 0.57 | 0.65 |

Continued

| Panel B: Global financial crisis subsample (January 1, 2007 to December 31, 2009) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Austria | Belgium | Finland | France | Greece | Ireland | Italy | Netherlands | Portugal | Spain | |

2-Year Maturity | ||||||||||

| K-Spread2 | 0.25*** | 0.38*** | 0.20*** | 0.19*** | 0.78*** | 0.69*** | 0.71*** | 0.27*** | 0.47*** | 0.36*** |

| (0.07) | (0.06) | (0.05) | (0.03) | (0.19) | (0.19) | (0.08) | (0.06) | (0.09) | (0.06) | |

| CDS Spreadc2 | 0.11*** | 0.10*** | 0.07 | 0.01 | 0.63*** | 0.36*** | 0.22*** | 0.05 | 0.23*** | 0.16*** |

| (0.02) | (0.03) | (0.05) | (0.04) | (0.06) | (0.05) | (0.04) | (0.05) | (0.04) | (0.03) | |

| R2-adjusted (%) | 0.25 | 0.27 | 0.11 | 0.16 | 0.52 | 0.30 | 0.46 | 0.12 | 0.23 | 0.32 |

5-Year Maturity | ||||||||||

| K-Spread5 | 0.45*** | 0.46*** | 0.34*** | 0.36*** | 1.16*** | 0.53*** | 0.90*** | 0.39*** | 0.69*** | 0.40*** |

| (0.07) | (0.05) | (0.06) | (0.05) | (0.17) | (0.16) | (0.08) | (0.06) | (0.10) | (0.07) | |

| CDS Spreadc5 | 0.23*** | 0.57*** | 0.39*** | −0.22 | 0.76*** | 0.33*** | 0.35*** | 0.44*** | 0.34*** | 0.35*** |

| (0.03) | (0.06) | (0.11) | (0.14) | (0.05) | (0.04) | (0.05) | (0.06) | (0.07) | (0.05) | |

| R2-adjusted (%) | 0.47 | 0.62 | 0.18 | 0.30 | 0.59 | 0.36 | 0.59 | 0.43 | 0.36 | 0.40 |

10-Year Maturity | ||||||||||

| K-Spread10 | 0.44*** | 0.29*** | 0.34*** | 0.22*** | 0.80*** | 0.24 | 0.59*** | 0.20*** | 0.56*** | 0.28*** |

| (0.07) | (0.08) | (0.05) | (0.05) | (0.18) | (0.20) | (0.12) | (0.06) | (0.12) | (0.09) | |

| CDS Spreadc10 | 0.24*** | 0.44*** | 0.10 | 0.29*** | 0.58*** | 0.32*** | 0.44*** | 0.15*** | 0.43*** | 0.40*** |

| (0.02) | (0.05) | (0.08) | (0.07) | (0.05) | (0.05) | (0.04) | (0.03) | (0.06) | (0.05) | |

| R2-adjusted (%) | 0.52 | 0.39 | 0.22 | 0.09 | 0.48 | 0.30 | 0.37 | 0.22 | 0.32 | 0.37 |

| Panel B: Global financial crisis subsample (January 1, 2007 to December 31, 2009) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Austria | Belgium | Finland | France | Greece | Ireland | Italy | Netherlands | Portugal | Spain | |

2-Year Maturity | ||||||||||

| K-Spread2 | 0.25*** | 0.38*** | 0.20*** | 0.19*** | 0.78*** | 0.69*** | 0.71*** | 0.27*** | 0.47*** | 0.36*** |

| (0.07) | (0.06) | (0.05) | (0.03) | (0.19) | (0.19) | (0.08) | (0.06) | (0.09) | (0.06) | |

| CDS Spreadc2 | 0.11*** | 0.10*** | 0.07 | 0.01 | 0.63*** | 0.36*** | 0.22*** | 0.05 | 0.23*** | 0.16*** |

| (0.02) | (0.03) | (0.05) | (0.04) | (0.06) | (0.05) | (0.04) | (0.05) | (0.04) | (0.03) | |

| R2-adjusted (%) | 0.25 | 0.27 | 0.11 | 0.16 | 0.52 | 0.30 | 0.46 | 0.12 | 0.23 | 0.32 |

5-Year Maturity | ||||||||||