Abstract

We exploit a variation in organizational hierarchy induced by a reorganization plan implemented in roughly 2,000 bank branches in India. We do so to investigate how organizational hierarchy affects the allocation of credit. We find that increased hierarchization of a branch induces credit rationing, reduces loan performance, and generates standardization in loan contracts. Additionally, we find that hierarchical structures perform better in environments characterized by a high degree of corruption, highlighting the benefits of hierarchies in restraining rent-seeking activities. Overall, our results are consistent with the view that valuable information may be lost in hierarchical structures.

Received May 4, 2018; editorial decision April 30, 2018 by Editor Itay Goldstein. Authors have furnished an Internet Appendix, which is available on the Oxford University Press Web site next to the link to the final published paper online.

Over recent years, there has been a substantial change in the lending landscape, with banks becoming larger, more globalized, and more complex (Mester 2012; Herring and Carmassi 2012). While there is evidence that banks might benefit from economies of scale (Focarelli and Panetta 2003), it is argued that hierarchical structures may be inferior when it comes to granting loans to small and medium sized enterprises (Stein 2002). Given the importance of small and entrepreneurial firms for innovation and economic growth, it is plausible that the shift toward hierarchical organizations hampers growth. In this paper, we examine how organizational hierarchy affects the allocation of credit.

There is now growing recognition that organizational design matters (Radner 1993; Bolton and Dewatripont 1994; Aghion and Tirole 1997; Garicano 2000; Dessein 2002). However, despite the abundance of theoretical literature on this topic, empirical research has been rather scant.1 Two obstacles hinder empirical research in this area. The first impediment comes from the paucity of good micro-level data. A researcher not only needs detailed data on the organizational design of banks, but also requires comprehensive information on outcome variables, to identify the effect of changes in organizational design. The second problem relates to the classic endogeneity problem. Even if one is fortunate enough to gain access to organizational-level micro data, one still has to grapple with the fact that the choice of organizational design is not random. While cross-sectional studies are informative about the plausible relationship, they are plagued by the problem of omitted variables. To make any causal claims, the researcher has to seek some exogenous variation in the organizational hierarchy.

In this paper, we use micro-level data from a large bank in India with roughly 2,000 branches, to examine how organizational hierarchy affects lending. The data set offers not only comprehensive information on financial contracts of individual borrowers but also micro-details on the organizational design of all branches of the bank. In particular, it provides a measure of organizational hierarchy: the number of managerial layers within a bank branch, where more layers capture a greater degree of hierarchization.

We exploit changes in the organizational design, brought about by a bank-level, predetermined reorganizational rule, and a difference-in-differences (DID) research design. Specifically, a branch receives an upgrade if its total business (deposits and loans) exceeds a certain threshold for eight quarters in a row. The reverse is true for a downgrade. The upgrade adds a new managerial layer to a branch office – the branch is now headed by a more senior manager, who by virtue of her seniority in the bank can approve larger loans. Thus, the upgrade generates two simultaneous affects. The addition of a new layer increases the hierarchical distance for smaller loans. The opposite is true for larger loans that can be approved internally after an upgrade due to the higher loan approval limit of the more senior manager. To allow for comparability, our experiment examines whether the lending behavior for loans that can be approved in the lowest managerial layer changes with the addition of another managerial layer.2

The following example illustrates the empirical strategy of the paper. Consider a level 2 branch that is upgraded to a level 3 branch. Further assume that the level 1 branch has the authority to approve loans below USD 5,000, the level 2 branch has the power to approve loans up to USD 10,000 and the level 3 branch has an approval limit of USD 20,000. Any loan above these limits would have to be sent to a higher level regional office3 for its approval, as it falls outside the branch’s loan approval limits. We compare how the lending behavior of a bank branch changes with the hierarchization for loans that are below the USD 5,000 threshold. To control for time trends and other omitted factors, our control group is another bank branch of the same bank in the same district in the same quarter.4

Existing theories posit that the cost of communicating and transmitting information increases with hierarchization (Radner 1993; Bolton and Dewatripont 1994; Aghion and Tirole 1997; Garicano 2000; Dessein 2002; Stein 2002). To the extent that hierarchy impedes information production (Stein 2002), it is natural to expect implications on bank lending. While the effect of information on lending can be rather subtle, the canonical models of credit argue that improving information in credit markets facilitates lending and broadens access to finance (Stiglitz and Weiss 1981). Because decentralization in decision-making increases banks’ ability to generate information, we expect there to be more lending (i.e., less credit rationing) in decentralized structures. In a similar vein, it is natural to expect that better information would allow banks to target credit to more profitable projects and away from less profitable ones, thus increasing the overall profitability of their portfolio. Furthermore, to the extent that better information allows the banks to discriminate between borrowers, one would expect a greater dispersion in loan contract terms (Cornell and Welch 1996; Cerqueiro et al. 2010; Rajan et al. 2015).

We find that organizational hierarchy affects both the quantity and the quality of loans originated by the bank. Specifically, we observe that an increase in hierarchy results in a 9.9% decline in total new loans issued by the bank branch and a 5.4% decline in the average loan size. Furthermore, we find that an increase in organizational hierarchy leads to a 4.5% reduction in the number of small retail borrowers. On examining the performance of these loans, we find that there is a substantial drop in the quality of loans after a branch becomes more hierarchical. Delinquencies of loans are 30% higher, and returns 15% lower. Overall, our results support the view that better information is generated in more decentralized branches.

To further sharpen our analysis, we examine the second moment of contract terms on loan agreements, in a similar spirit to Rajan et al. (2015).5Rajan et al. (2015) argue that an increase in information should increase the variance of the contract terms, as it allows banks to discriminate amongst borrowers. With better information, banks can target credit to more profitable borrowers and away from less profitable ones (to weed out bad borrowers). Consistent with this prediction, we find that a new layer in the hierarchy reduces the variance of contract terms (loan size) and generates contract standardization.

As pointed out above, higher level branches are headed by more senior managers, who have the authority (granted by the central office) to approve larger loans. Thus, these “large” loans are approved internally after an upgrade. We find that after hierarchization, a branch issues more of the “large” loans and generates more information on them. Given that these loans underwent a reduction in organizational distance, the results provide additional support for the view that an increase in organizational hierarchy reduces the information produced on loans.

This generates an interesting trade-off for the branch. While the upgraded branch loses out on small loans, it gains on larger loans that are now processed inside the branch. Interestingly, however, we find that the gains in large loans do not offset the losses on small loans. To assess the overall effect of branch-level reorganizations, however, one has to evaluate the profitability of the bank. Because upgrading a branch frees up resources at regional or higher level offices, these offices can be more effective in other bank-level assignments, such as business development and risk management. Our analysis focuses on only branch-level profitability, and not on the overall profitability of the bank. It should be noted, however, that during our sample the profitability of the bank increased. In addition, the bank opened new branches in 43 previously unbanked districts, thereby allowing it to access new markets. Thus, the overall effect for the bank is likely to be positive. Because we do not have a control group for the bank-level analysis, we refrain from making any causal claims on the overall profitability of the bank.

Next, we investigate how organizational hierarchy interacts with corruption. Delegation in the presence of corruption may be a double-edged sword (Tirole 1986; Banerjee et al. 2013). Delegation provides an extra incentive for an agent to perform a task. However, when the agent’s incentives are not aligned with those of the principal, it may be worthwhile taking this discretion away. To understand how organizational hierarchy interacts with rent extraction, we compare the effects in more corrupt states to those in less corrupt ones. Our proxy for corruption is provided by Transparency International. The index is particularly useful for our study, because it examines corruption in banking services. It measures the fraction of respondents who actually paid a bribe for obtaining these services. The study points out that the majority of these bribes were paid to secure a loan.6 Our estimates indicate that for corrupt states the effects of hierarchization are significantly reduced, highlighting the benefits of hierarchical structures in corrupt environments.

Results thus far are consistent with the view that an increase in organizational hierarchy adversely affects lending. However, it is plausible that other contemporaneous changes may have affected lending. As a first check, we confirm that our results remain strong after controlling for local shocks to credit demand within the same district and the same city.7 We also verify that our results are not driven by changes in branch managers. We carry out many other robustness tests and discuss some alternative stories in Section 6.

This paper adds to the literature on organizational hierarchy and information production. Theories in this area can be broadly categorized into one of two strands. The first one deals with information transmission in teams with incentive conflicts (Aghion and Tirole 1997; Stein 2002). The second one examines information processing in teams without incentive problems. These theories argue that hierarchy might be inferior, when communicating and processing information is very costly (Bolton and Dewatripont 1994; Garicano 2000). Both sets of theories predict that organizational hierarchy might lead to difficulties in processing and communicating information. This paper documents that organizational hierarchy leads to distortions in information production, but it is silent about which of the two classes of theories generates our results.

Our work is closest to Liberti and Mian (2009) and Liberti (2017), who show that more hierarchical organizational structures tend to rely more heavily on objective rather than subjective information.8Liberti et al. (2015) examine how banks change their organizational design in response to a change in external information with the introduction of a credit registry. Canales and Nanda (2012) document that banks with less discretionary power at branch offices are less responsive to the competitive environment. Qian et al. (2015) find that when the loan approval is delegated to an individual rather than a committee, the information quality improves. Finally, Cerqueiro et al. (2010) study whether higher dispersion in interest rates is consistent with more discretion in loan approval.9 We complement these papers by examining how a change in organizational hierarchy affects banks’ ability to generate information and to allocate credit. Furthermore, we provide new insights by highlighting some of the benefits associated with hierarchies in corrupt areas.

Our paper also contributes to the literature on distance in credit markets. These studies argue that the proximity between the borrower and the lender mitigates the information asymmetry (Petersen and Rajan 1995; Petersen and Rajan 2002; Degryse and Ongena 2005; Mian 2006; Liberti and Mian 2009; Alessandrini et al. 2009; Agarwal and Hauswald 2010; Brown et al. 2012; Berg et al. 2013; Fisman et al. 2017). The key distinction here is that we focus on hierarchical distance, as opposed to geographical distance (Petersen and Rajan 2002) or cultural distance (Fisman et al. 2017).

1. Theoretical Motivation

In this section, we briefly discuss the main theories with implications on organizational hierarchy and information. The first set of models considers information processing and communication in teams without incentive problems. Generally, these theories argue that organizational hierarchy is less attractive when communication costs are large. Bolton and Dewatripont (1994) consider an environment where a firm trades off gains from specialization against costs of communication.10 In their model, specialized agents collect information that is then communicated to the decision maker. If the costs of communication are high, specialization becomes less attractive. Similarly, Garicano (2000) considers knowledge based hierarchies. In his model, higher layers are solvers of complex problems, while lower layers are routine problem solvers. He proposes a trade-off between the cost of communication (matching a problem with the problem solver) and the cost of acquiring knowledge (the front line can pick up necessary skills and problem solvers are not necessary). If the costs of communication outweigh the costs of acquiring information, hierarchy is less attractive.

The second set of models analyzes information processing in teams with incentive problems. Aghion and Tirole (1997) and Stein (2002) argue that organizational hierarchy creates an ex ante disincentive to collect information. In their model, the subordinate is responsible for collecting information to be transmitted to the manager. Because the manager makes the final decision, there is a positive probability that the suggestion of a subordinate will be overruled. This likelihood of interference dulls the subordinate’s incentive to exert effort in collecting information ex ante. A similar point is raised by cheap talk models (most notably, Crawford and Sobel, 1982, Dessein, 2002). The informed agent sends a signal to a principal who will act on it and affect the welfare of both. If their incentives are misaligned, the agent is prone to misreport the true quality of their project. In this spirit, Harris and Raviv (1998) exploit the cost of auditing the information that is submitted by a subordinate. If the audit costs are very high, the decision will be delegated to the subordinate. In other words, hierarchy becomes less attractive in the presence of high audit costs and misaligned interests.

The effect of information on lending is rather complex. The cannonical models of credit predict that better information on borrowers facilitates lending and broadens access to finance (Stiglitz and Weiss 1981).11 However, the effect of information on overall profitability is less ambiguous. Better information on borrowers allows a bank to target loans to more profitable projects and away from less profitable ones, thereby increasing overall profitability. In addition, Cornell and Welch (1996) and Rajan et al. (2015) argue that better information is likely to increase the variance on loan contract terms, because the bank can use the extra information to increase lending to creditworthy borrowers and reduce lending to riskier borrowers.

In this paper, we document that organizational hierarchy affects lending. It should be noted that while we interpret our results through the lens of the two sets of organizational theories described above, the paper is not a horse race between them.

2. Data

The data for this study come from a large, state-owned Indian bank operating over 2,000 branches. The data set is rich in detail. It contains detailed information not only on all loan contracts but also on the organizational design of all of the bank’s branches.12 At the contract level, it includes the loan balance outstanding, the interest rate, the maturity, the type of collateral, the collateral value, and the number of days late in payment, among other information. On the organizational front, it provides us with information on the number of managerial layers in each branch office, the overall seniority of each manager and their loan approval limit. The sample spans 29 quarters from 1999 Q1 to 2006 Q1.

2.1 Loans and borrowers

We focus on first-time, individual (retail) borrowers. During our sample, the bank issued 1.75 million such contracts. For the purposes of this study, we aggregate the loan-level information and obtain 54,079 branch-quarter observations. In Table 1, we present means, medians, standard deviations, and the 1st and the 99th percentiles for the main variables of interest. The loan amounts are expressed in rupees.13

Summary statistics

| Mean | SD | p1 | p50 | p99 | |

|---|---|---|---|---|---|

| Branch-quarter statistics (N=54,079) | |||||

| New credit (1,000s of rupees) | 1,175.1 | 2,063.4 | 31.0 | 726.4 | 6,650.1 |

| Mean loan amount (1,000s of rupees) | 56.0 | 43.5 | 7.8 | 42.8 | 216.5 |

| # of borrowers | 24.5 | 39.1 | 2.0 | 15.0 | 143.0 |

| Fraction of borrowers delinquent within a year | 0.050 | 0.111 | 0.000 | 0.000 | 0.500 |

| Fraction of debt delinquent within a year | 0.042 | 0.111 | 0.000 | 0.000 | 0.570 |

| Return on loans (value-weighted) | 0.070 | 0.079 | -0.244 | 0.083 | 0.150 |

| Interest rate | 0.11 | 0.018 | 0.082 | 0.116 | 0.158 |

| Maturity (years) | 4.15 | 2.26 | 0.60 | 4.00 | 11.11 |

| Collateral-to-loan (median) | 6.75 | 406.98 | 0.00 | 1.42 | 19.12 |

| SD debt (1,000s of rupees) | 57.6 | 44.7 | 2.3 | 47.9 | 184.1 |

| IQR debt (1,000s of rupees) | 54.6 | 66.8 | 0.7 | 28.2 | 309.8 |

| Branch level | 1.4 | 0.6 | 1 | 1 | 3 |

| Branch level (treated) | 1.7 | 0.7 | 1 | 2 | 3 |

| Mean | SD | p1 | p50 | p99 | |

|---|---|---|---|---|---|

| Branch-quarter statistics (N=54,079) | |||||

| New credit (1,000s of rupees) | 1,175.1 | 2,063.4 | 31.0 | 726.4 | 6,650.1 |

| Mean loan amount (1,000s of rupees) | 56.0 | 43.5 | 7.8 | 42.8 | 216.5 |

| # of borrowers | 24.5 | 39.1 | 2.0 | 15.0 | 143.0 |

| Fraction of borrowers delinquent within a year | 0.050 | 0.111 | 0.000 | 0.000 | 0.500 |

| Fraction of debt delinquent within a year | 0.042 | 0.111 | 0.000 | 0.000 | 0.570 |

| Return on loans (value-weighted) | 0.070 | 0.079 | -0.244 | 0.083 | 0.150 |

| Interest rate | 0.11 | 0.018 | 0.082 | 0.116 | 0.158 |

| Maturity (years) | 4.15 | 2.26 | 0.60 | 4.00 | 11.11 |

| Collateral-to-loan (median) | 6.75 | 406.98 | 0.00 | 1.42 | 19.12 |

| SD debt (1,000s of rupees) | 57.6 | 44.7 | 2.3 | 47.9 | 184.1 |

| IQR debt (1,000s of rupees) | 54.6 | 66.8 | 0.7 | 28.2 | 309.8 |

| Branch level | 1.4 | 0.6 | 1 | 1 | 3 |

| Branch level (treated) | 1.7 | 0.7 | 1 | 2 | 3 |

This table reports branch-quarter summary statistics of new individual loans. The variable Branch level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. We report the mean, standard deviation, the 1st percentile, median, and the 99th percentile for all the variables.

Summary statistics

| Mean | SD | p1 | p50 | p99 | |

|---|---|---|---|---|---|

| Branch-quarter statistics (N=54,079) | |||||

| New credit (1,000s of rupees) | 1,175.1 | 2,063.4 | 31.0 | 726.4 | 6,650.1 |

| Mean loan amount (1,000s of rupees) | 56.0 | 43.5 | 7.8 | 42.8 | 216.5 |

| # of borrowers | 24.5 | 39.1 | 2.0 | 15.0 | 143.0 |

| Fraction of borrowers delinquent within a year | 0.050 | 0.111 | 0.000 | 0.000 | 0.500 |

| Fraction of debt delinquent within a year | 0.042 | 0.111 | 0.000 | 0.000 | 0.570 |

| Return on loans (value-weighted) | 0.070 | 0.079 | -0.244 | 0.083 | 0.150 |

| Interest rate | 0.11 | 0.018 | 0.082 | 0.116 | 0.158 |

| Maturity (years) | 4.15 | 2.26 | 0.60 | 4.00 | 11.11 |

| Collateral-to-loan (median) | 6.75 | 406.98 | 0.00 | 1.42 | 19.12 |

| SD debt (1,000s of rupees) | 57.6 | 44.7 | 2.3 | 47.9 | 184.1 |

| IQR debt (1,000s of rupees) | 54.6 | 66.8 | 0.7 | 28.2 | 309.8 |

| Branch level | 1.4 | 0.6 | 1 | 1 | 3 |

| Branch level (treated) | 1.7 | 0.7 | 1 | 2 | 3 |

| Mean | SD | p1 | p50 | p99 | |

|---|---|---|---|---|---|

| Branch-quarter statistics (N=54,079) | |||||

| New credit (1,000s of rupees) | 1,175.1 | 2,063.4 | 31.0 | 726.4 | 6,650.1 |

| Mean loan amount (1,000s of rupees) | 56.0 | 43.5 | 7.8 | 42.8 | 216.5 |

| # of borrowers | 24.5 | 39.1 | 2.0 | 15.0 | 143.0 |

| Fraction of borrowers delinquent within a year | 0.050 | 0.111 | 0.000 | 0.000 | 0.500 |

| Fraction of debt delinquent within a year | 0.042 | 0.111 | 0.000 | 0.000 | 0.570 |

| Return on loans (value-weighted) | 0.070 | 0.079 | -0.244 | 0.083 | 0.150 |

| Interest rate | 0.11 | 0.018 | 0.082 | 0.116 | 0.158 |

| Maturity (years) | 4.15 | 2.26 | 0.60 | 4.00 | 11.11 |

| Collateral-to-loan (median) | 6.75 | 406.98 | 0.00 | 1.42 | 19.12 |

| SD debt (1,000s of rupees) | 57.6 | 44.7 | 2.3 | 47.9 | 184.1 |

| IQR debt (1,000s of rupees) | 54.6 | 66.8 | 0.7 | 28.2 | 309.8 |

| Branch level | 1.4 | 0.6 | 1 | 1 | 3 |

| Branch level (treated) | 1.7 | 0.7 | 1 | 2 | 3 |

This table reports branch-quarter summary statistics of new individual loans. The variable Branch level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. We report the mean, standard deviation, the 1st percentile, median, and the 99th percentile for all the variables.

In a quarter, the average branch lends to 24 new retail borrowers, with a mean loan size of 56,000 rupees (roughly USD 1,300). Furthermore, the equally weighted delinquency rate, defined as 60 or more days late in repayment within a year after the origination of the loan, is 5.0%. In comparison, the value-weighted delinquency rate is only 4.2%, suggesting that larger debt is less likely to be late in repayment and is issued to better quality borrowers. In addition, the average value-weighted return on loans is 7.0%. Moreover, 90% of all loans are secured with a median ratio of collateral to loan value of 1.42. Finally, the average maturity and interest rate are 4.2 years and 11.4%, respectively.

2.2 Organizational design

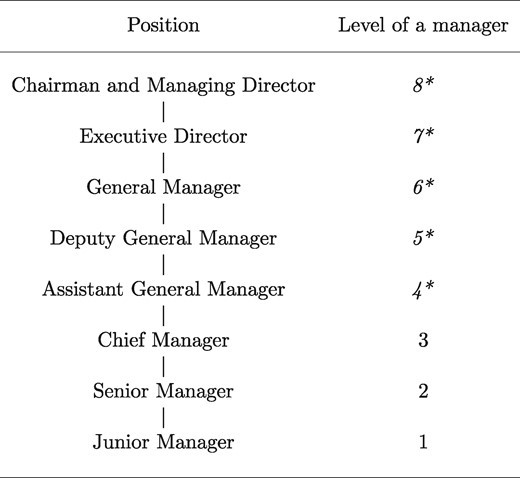

Figure 1 provides an illustration of the managerial hierarchy of the bank. In total, there are eight management levels. Employees in each layer are comparable in terms of their responsibilities, discretionary power as defined by their maximum loan approval limit, experience, and salary. The top five layers, starting with Assistant General Manager, constitute the senior management team. While they are mainly involved in business development, they also originate large loans. The lower ranked employees consist of junior managers, senior managers and chief managers who focus more on the operation side of lending as managers in branch offices. Every ranked employee has a credit origination limit, and that limit increases with the rank of the official.

Organizational design

The bank’s organizational design consists of the eight layers described in the figure. A higher-ranking manager has more decisional power and authority. The top-five layers, marked with an asterisk, are the senior management team, mainly involved in business development. The lower three focus on the operational side of lending.

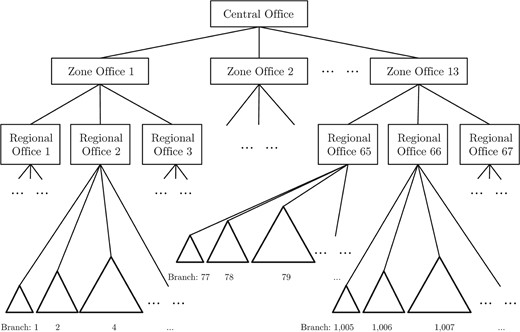

The organizational chart of the bank is as follows (see Figure 2): The Chairman and the Executive Directors of the bank operate from the central office and set all bank-wide policies, which are then executed in other lower-level branches. Zonal offices, which represent distinct geographical zones across the country, operate under the central office. Within each zone, several regional offices are responsible for business development in different regions of a zone. Finally, under each regional office, a large number of standardized branch offices (2,000+) exist and are headed by different levels of managers.

Internal organizational design

The figure shows a schematic illustration of the bank and its branches. Each level has a specified approval limit on the size of the loan. If the loan falls outside of the branch manager’s limits, it is sent to the regional, the zonal, or the head office for approval, depending on the size of the loan.

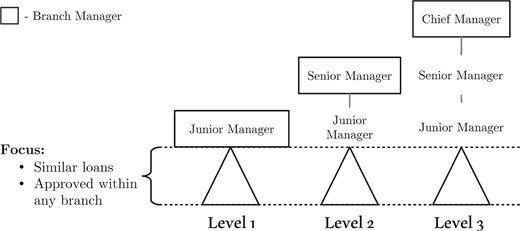

For the organizational design of branches, the branch head can be seen as the chief executive of the branch. They are responsible for the whole business of the branch, within the policy guidelines that are set by the central office. The branch manager can decide on whether to grant a loan and has considerable discretion over the terms of the loan contract, with the exception of the interest rate, which is set by the central office. For instance, all home improvement loans have the same interest rate as car loans with a maturity of up to 5 years (see, for example, Internet Appendix Table A1). In total, there are three branch structures (see Figure 3). The smallest branch (level 1) is typically headed by a junior branch manager, the next branch up (level 2) is headed by a senior branch manager, and finally the branch on level 3 is overseen by a chief manager. Higher-level branches have more layers of hierarchy associated with them. For example, in level 1 branches, branch managers directly interact with the borrowers. However, a level 3 branch would have three layers: junior managers, senior managers, and a chief manager. It should be noted that while the loan officers (or junior managers in our setting) in a branch can approve loans that are within their approval limit, the senior-level manager (if there is one in that branch) can overrule those decisions.

Branch office design

The figure shows a schematic illustration of the bank’s branches. Each level has a specified approval limit on the size of the loan. If the loan falls outside of the branch manager’s limits, it is sent to the regional, the zonal, or the head office for approval, depending on the size of the loan. Our sample consists of three organizational designs: decentralized (level 1), medium hierarchy (level 2), and centralized (level 3). The more hierarchical the branch, the higher the approval limits of its manager. Our analysis focuses on all new individual loans eligible for approval at any organizational design, that is, the loans that fall below the limit of the least hierarchical branch (the triangles at the bottom of the chart).

The lending process is relatively simple (see Figure 4). The borrower approaches the bank and fills in the application form. The application may be rejected by the loan officer, which ends the whole process. If not, the loan officer evaluates the loan application to assess the borrower’s credit risk. The loan officer and the borrower then meet to discuss the needs, collateral requirements and other possibilities. Once a loan officer and a borrower agree on the loan terms, the loan is approved by the loan officer (junior manager) if the agreed size of the loan falls within their discretionary powers (i.e., below 500k rupees). If the loan exceeds the loan officer’s approval limit, it goes to the next authority up for approval. If the requested loan is above the discretionary powers of the branch manager, the loan application, along with the branch’s assessment, is forwarded to a more senior manager in a regional, a zonal, or a central office. Nevertheless, the decision on whether to reject the application or send it for approval outside the branch remains with the head of the branch. On average, a loan application is assessed within 10 days when approved within a branch. The assessment period increases to 2 months when evaluated externally, because the credit files were mailed using postal services during our sample period.

Loan approval process

The flowchart describes the loan approval process. It starts with a loan application at the branch office and continues until the loan is approved or rejected at either the branch or another external office.

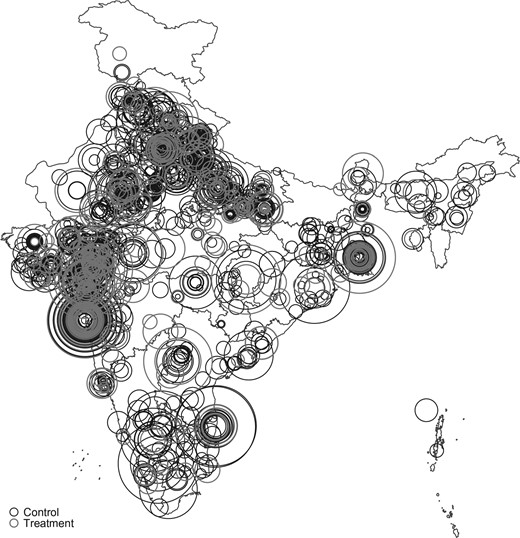

In terms of the geographic distribution, the bank is highly dispersed across India (Figure 5). We created a spatial map and calculated distances between branches, to better understand the market structure. Specifically, for a level 1 branch, the closest levels 2 and 3 branches are 23 and 90 kilometers away, respectively (see Table 2). For a level 2 branch, the closest level 3 branch is 73 kilometers away. On average, there are 1.67 branches per city. Out of all cities, 52% (or 1,396) have only one branch of the bank. Similarly, we find that there are 1.38 branches per ZIP code and 1.38 branches per banking area, as defined by the Reserve Bank of India.14 57% of ZIP codes (1,527) and 66% of banking areas (1,844) have a single branch of this bank. It is worthwhile to note that transportation in India, particularly in rural areas, is not very well developed. The 20-kilometer distance can come at a considerable travel cost.15 As a rule borrowers have to apply at their nearest branch.16

Geographical distribution of branches, weighted by total lending

The center indicates the location of the branch by postal code. The size corresponds to the total amount lent in the branch in 2006.

Distance to the closest branch within the bank

| Branch hierarchy | Regional office | Zonal office | ||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | ||||

| Hierarchy | ||||||

| 1 | 12.08 | 22.79 | 90.03 | 131.46 | 204.48 | |

| 2 | 15.47 | 18.18 | 73.82 | 116.25 | 193.08 | |

| 3 | 7.23 | 6.70 | 28.12 | 54.14 | 178.38 | |

| Branch hierarchy | Regional office | Zonal office | ||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | ||||

| Hierarchy | ||||||

| 1 | 12.08 | 22.79 | 90.03 | 131.46 | 204.48 | |

| 2 | 15.47 | 18.18 | 73.82 | 116.25 | 193.08 | |

| 3 | 7.23 | 6.70 | 28.12 | 54.14 | 178.38 | |

The table reports the average spatial distance in kilometers to the closest branch, regional office, or zonal office of the same bank. The location of branches is at the ZIP code level. Each row corresponds to the hierarchy of each branch from which the distance is calculated. For instance, for a branch with hierarchy 1, the closest branch with hierarchy 2 is 22.79 kilometers. For a branch with hierarchy 1, the average distance from regional and zonal offices is 131.46 and 204.48 kilometers.

Distance to the closest branch within the bank

| Branch hierarchy | Regional office | Zonal office | ||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | ||||

| Hierarchy | ||||||

| 1 | 12.08 | 22.79 | 90.03 | 131.46 | 204.48 | |

| 2 | 15.47 | 18.18 | 73.82 | 116.25 | 193.08 | |

| 3 | 7.23 | 6.70 | 28.12 | 54.14 | 178.38 | |

| Branch hierarchy | Regional office | Zonal office | ||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | ||||

| Hierarchy | ||||||

| 1 | 12.08 | 22.79 | 90.03 | 131.46 | 204.48 | |

| 2 | 15.47 | 18.18 | 73.82 | 116.25 | 193.08 | |

| 3 | 7.23 | 6.70 | 28.12 | 54.14 | 178.38 | |

The table reports the average spatial distance in kilometers to the closest branch, regional office, or zonal office of the same bank. The location of branches is at the ZIP code level. Each row corresponds to the hierarchy of each branch from which the distance is calculated. For instance, for a branch with hierarchy 1, the closest branch with hierarchy 2 is 22.79 kilometers. For a branch with hierarchy 1, the average distance from regional and zonal offices is 131.46 and 204.48 kilometers.

Table 3 reports the summary statistics by branch level. As can be seen from panel A, more hierarchical branches originate larger loans, serve fewer customers, and their loan book performs better, as measured by both delinquencies and returns. Hierarchical branches, however, are more likely to be located in metropolitan areas. Because borrowers might differ in terms of their size and profitability across geographical locations, a simple cross-sectional analysis could capture the heterogeneity of clientele, degree of competition, or other omitted variables rather than organizational design. In panel B, we restrict the sample to only metropolitan areas and find that branches are fairly similar across all levels.17 Our empirical strategy employs a difference-in differences research design to control for these omitted factors.

Summary statistics: Cross-section

| Fraction of debt | ||||||||

|---|---|---|---|---|---|---|---|---|

| Mean loan amount | # of borrowers | del. within a year | Return on loans | |||||

| Branch level (# Obs) | Mean | SD | Mean | SD | Mean | SD | Mean | SD |

| A. All areas | ||||||||

| Level 1 (34,068) | 46,303 | 35,698 | 24.65 | 30.48 | 0.046 | 0.116 | 0.066 | 0.083 |

| Level 2 (17,139) | 70,231 | 48,438 | 25.27 | 52.53 | 0.039 | 0.105 | 0.074 | 0.073 |

| Level 3 (2,872) | 85,918 | 57,944 | 17.94 | 35.20 | 0.024 | 0.083 | 0.078 | 0.067 |

| B. Metropolitan areas | ||||||||

| Level 1 | 90,169 | 60,584 | 13.65 | 14.89 | 0.034 | 0.107 | 0.084 | 0.067 |

| Level 2 | 87,127 | 59,267 | 13.31 | 13.76 | 0.034 | 0.104 | 0.081 | 0.078 |

| Level 3 | 92,702 | 63,363 | 12.06 | 15.27 | 0.022 | 0.083 | 0.080 | 0.071 |

| Fraction of debt | ||||||||

|---|---|---|---|---|---|---|---|---|

| Mean loan amount | # of borrowers | del. within a year | Return on loans | |||||

| Branch level (# Obs) | Mean | SD | Mean | SD | Mean | SD | Mean | SD |

| A. All areas | ||||||||

| Level 1 (34,068) | 46,303 | 35,698 | 24.65 | 30.48 | 0.046 | 0.116 | 0.066 | 0.083 |

| Level 2 (17,139) | 70,231 | 48,438 | 25.27 | 52.53 | 0.039 | 0.105 | 0.074 | 0.073 |

| Level 3 (2,872) | 85,918 | 57,944 | 17.94 | 35.20 | 0.024 | 0.083 | 0.078 | 0.067 |

| B. Metropolitan areas | ||||||||

| Level 1 | 90,169 | 60,584 | 13.65 | 14.89 | 0.034 | 0.107 | 0.084 | 0.067 |

| Level 2 | 87,127 | 59,267 | 13.31 | 13.76 | 0.034 | 0.104 | 0.081 | 0.078 |

| Level 3 | 92,702 | 63,363 | 12.06 | 15.27 | 0.022 | 0.083 | 0.080 | 0.071 |

This table reports branch-quarter summary statistics of new individual loans across organizational designs. Panel A considers all geographic areas, and panel B considers only metropolitan areas. The variable Branch level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. We report the mean and the standard deviation for all the variables.

Summary statistics: Cross-section

| Fraction of debt | ||||||||

|---|---|---|---|---|---|---|---|---|

| Mean loan amount | # of borrowers | del. within a year | Return on loans | |||||

| Branch level (# Obs) | Mean | SD | Mean | SD | Mean | SD | Mean | SD |

| A. All areas | ||||||||

| Level 1 (34,068) | 46,303 | 35,698 | 24.65 | 30.48 | 0.046 | 0.116 | 0.066 | 0.083 |

| Level 2 (17,139) | 70,231 | 48,438 | 25.27 | 52.53 | 0.039 | 0.105 | 0.074 | 0.073 |

| Level 3 (2,872) | 85,918 | 57,944 | 17.94 | 35.20 | 0.024 | 0.083 | 0.078 | 0.067 |

| B. Metropolitan areas | ||||||||

| Level 1 | 90,169 | 60,584 | 13.65 | 14.89 | 0.034 | 0.107 | 0.084 | 0.067 |

| Level 2 | 87,127 | 59,267 | 13.31 | 13.76 | 0.034 | 0.104 | 0.081 | 0.078 |

| Level 3 | 92,702 | 63,363 | 12.06 | 15.27 | 0.022 | 0.083 | 0.080 | 0.071 |

| Fraction of debt | ||||||||

|---|---|---|---|---|---|---|---|---|

| Mean loan amount | # of borrowers | del. within a year | Return on loans | |||||

| Branch level (# Obs) | Mean | SD | Mean | SD | Mean | SD | Mean | SD |

| A. All areas | ||||||||

| Level 1 (34,068) | 46,303 | 35,698 | 24.65 | 30.48 | 0.046 | 0.116 | 0.066 | 0.083 |

| Level 2 (17,139) | 70,231 | 48,438 | 25.27 | 52.53 | 0.039 | 0.105 | 0.074 | 0.073 |

| Level 3 (2,872) | 85,918 | 57,944 | 17.94 | 35.20 | 0.024 | 0.083 | 0.078 | 0.067 |

| B. Metropolitan areas | ||||||||

| Level 1 | 90,169 | 60,584 | 13.65 | 14.89 | 0.034 | 0.107 | 0.084 | 0.067 |

| Level 2 | 87,127 | 59,267 | 13.31 | 13.76 | 0.034 | 0.104 | 0.081 | 0.078 |

| Level 3 | 92,702 | 63,363 | 12.06 | 15.27 | 0.022 | 0.083 | 0.080 | 0.071 |

This table reports branch-quarter summary statistics of new individual loans across organizational designs. Panel A considers all geographic areas, and panel B considers only metropolitan areas. The variable Branch level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. We report the mean and the standard deviation for all the variables.

2.3 Employee incentives

Managers are evaluated annually, based on a range of criteria. These include quantitative measures such as the amount and profitability of lending, as well as qualitative considerations such as employee skill development and effective customer communication. These managers are held accountable for loan defaults even after moving branches, on average up to 3 years. After that the responsibility is transferred to a manager at the branch where the loan was originated.

While there is limited incentive pay, managers are motivated through the possibility of promotion to a higher rank or a better posting. Successful managers may be sent to locales with more or better perks such as higher pay (overseas), a larger house, a company car, or control over a larger portfolio (large branches). In a similar vein, poor performers might be moved to less desirable places, which have a weak infrastructure and poor schools. Accordingly, managers have strong incentives to issue profitable loans and score high on other qualitative dimensions that affect their annual evaluations.

3. Empirical Specification

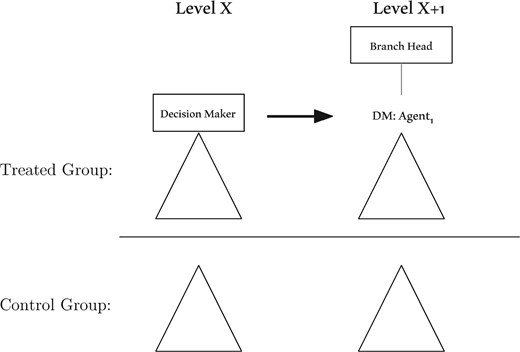

Our identification strategy employs a branch restructuring policy that is driven by predefined rules. A given branch is upgraded (downgraded) if over the last 2 years, the average outstanding balance of the combined loans and deposits exceeds (falls below) a fixed cutoff. In the event of an upgrade, a branch is allocated more resources, including more personnel to meet the rising demand for services in that district, and vice versa. The branch’s organizational hierarchy is also changed to resemble other branches on the same organizational level (see Figure 6). Because managers in a more senior level can approve larger loans, we focus on loans that are below the lowest approval limit, that is, that of junior managers. Therefore, our experiment examines whether the lending behavior for loans that can be approved in the lowest managerial layer changes with the addition of another managerial layer. During our sample period, roughly 500 of all branches were reorganized.

Identification strategy

The figure describes our difference-in-differences (DID) identification strategy. We estimate the effect of organizational design on a set of loans eligible for approval both before and after the treatment. Each quarter, the treatment group consists of all branches that are reorganized. Then we compare our estimated effect on the treatment group with the results of similar branches whose organizational design was left unchanged (control group).

We wish to highlight a few points about the reorganization of branches. First, these cutoffs were fixed in the central office by a new CEO of the bank, before the start of our sample. Thus, from the perspective of a single borrower, the organizational design of a branch is exogenous. Second, we again stress that we are examining the loans that are eligible for internal approval within all branches, that is, we are looking at loans of under 500,000 rupees (approx. USD 11,000). This allows us to analyze a similar set of loans across all types of organizational levels, ensuring that the approval limit does not interfere with the loan decisions. It is important to emphasize that most of the branches that we examine have loan approval limits that are significantly above this cutoff (more than double), so this constraint is not binding for most of the loans that we examine.

Our empirical strategy attempts to identify the effect of organizational hierarchy on the parameters of interest (e.g., contract standardization, delinquencies, or return on loans). We employ a difference-in-differences (DID) strategy and compare branches that were subject to a change in their organizational design against a control group of branches that were not affected by these reorganizations. Thus, the empirical specification is given by

where the dependent variable (e.g., defaults) is measured at the branch-quarter level; |$q$| and |$b$| index the quarter and the branch, respectively. |$Branch~level_{bq}$| stands for the organizational design of branch |$b$| in quarter |$q$|. It is a number between 1 and 3, where the lowest and highest values describe decentralized and hierarchical (i.e., four-layer) branches, respectively. The branch fixed effects |$\left(\tau_{b}\right)$| absorb any time invariant branch characteristics. The quarterly dummies |$\left(\tau_{q}\right)$| control for aggregate time trends. This strategy identifies the effect of organizational structure on the credit market outcomes, controlling for time and branch invariant effects. The coefficient |$\delta$| is our DID estimate of the effect of organizational hierarchy on, for example, the default rates.

A concern might be that some credit demand shocks coincide with the reorganization of branches. We control for this by including district-quarter fixed effects.18 In such a specification, one compares the default rates of a reorganized branch against a branch that was not reorganized in the same district and in the same quarter. If there is any aggregate change in the default rates at the district-quarter level, this specification would control for that. For robustness, we have saturated our model with city-quarter fixed effects and find similar results.19 With a dynamic specification, we show that there are no pretreatment trends to any of our results.

4. Results

4.1 Lending

We begin by reporting the effect of the organizational design on new credit quantities for new borrowers in Columns 1 to 3 in Table 4, estimated using the difference-in-differences methodology (specification 1). The estimated coefficient of interest is that on Branch level, a number between 1 and 3, where 1 stands for a decentralized branch and 3 for a hierarchical branch. Both columns include quarter and branch fixed effects. We find that an increase in organizational hierarchy reduces the total lending to new borrowers by 9.9% (Column 1) and the number of new borrowers by 4.5% (Column 2). The difference between the two values implies that the average loan declined by 5.4% (Column 3).

Credit rationing, number of borrowers, and total lending

| Dependent variable | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| |

|---|---|---|---|---|---|---|---|---|---|

| |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| Branch level | −0.099*** | −0.045* | −0.054*** | −0.083** | −0.031 | −0.052*** | |||

| (0.030) | (0.025) | (0.017) | (0.033) | (0.026) | (0.018) | ||||

| |$\mbox{Before}^{-2}$| | 0.032 | 0.039 | −0.006 | ||||||

| (0.040) | (0.032) | (0.024) | |||||||

| |$\mbox{Before}^{0}$| | −0.037 | 0.014 | −0.051** | ||||||

| (0.041) | (0.033) | (0.024) | |||||||

| |$\mbox{After}^{2}$| | −0.123*** | −0.055 | −0.068*** | ||||||

| (0.043) | (0.034) | (0.026) | |||||||

| |${\rm After}^{4+}$| | −0.123*** | −0.058* | −0.065*** | ||||||

| (0.039) | (0.033) | (0.022) | |||||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 |

| Adj-|$R^{2}$| | 0.396 | 0.450 | 0.403 | 0.464 | 0.539 | 0.444 | 0.396 | 0.450 | 0.403 |

| Branch FEs | Y | Y | Y | Y | Y | Y | Y | Y | Y |

| Quarter FEs | Y | Y | Y | N | N | N | Y | Y | Y |

| Quarter-district FEs | N | N | N | Y | Y | Y | N | N | N |

| Dependent variable | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| |

|---|---|---|---|---|---|---|---|---|---|

| |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| Branch level | −0.099*** | −0.045* | −0.054*** | −0.083** | −0.031 | −0.052*** | |||

| (0.030) | (0.025) | (0.017) | (0.033) | (0.026) | (0.018) | ||||

| |$\mbox{Before}^{-2}$| | 0.032 | 0.039 | −0.006 | ||||||

| (0.040) | (0.032) | (0.024) | |||||||

| |$\mbox{Before}^{0}$| | −0.037 | 0.014 | −0.051** | ||||||

| (0.041) | (0.033) | (0.024) | |||||||

| |$\mbox{After}^{2}$| | −0.123*** | −0.055 | −0.068*** | ||||||

| (0.043) | (0.034) | (0.026) | |||||||

| |${\rm After}^{4+}$| | −0.123*** | −0.058* | −0.065*** | ||||||

| (0.039) | (0.033) | (0.022) | |||||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 |

| Adj-|$R^{2}$| | 0.396 | 0.450 | 0.403 | 0.464 | 0.539 | 0.444 | 0.396 | 0.450 | 0.403 |

| Branch FEs | Y | Y | Y | Y | Y | Y | Y | Y | Y |

| Quarter FEs | Y | Y | Y | N | N | N | Y | Y | Y |

| Quarter-district FEs | N | N | N | Y | Y | Y | N | N | N |

This table reports the effect of organizational design on total new lending to small individual borrowers (Columns 1, 4, and 7), the number of new individual borrowers (Columns 2, 5, and 8), and loan size (Columns 3, 6, and 9), using specification (1). The unit of analysis is a branch-quarter. The variable Branch Level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. |${\rm Before}^{-2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) in one or two quarters. |${\rm Before}^{0}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded this quarter or one quarter ago. |${\rm After}^{2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) two or three quarters ago. |${\rm After}^{4+}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) four quarters ago or more. The standard errors are reported in parentheses and clustered at the branch level. * significant at 10%; ** significant at 5%; and *** significant at 1%.

Credit rationing, number of borrowers, and total lending

| Dependent variable | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| |

|---|---|---|---|---|---|---|---|---|---|

| |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| Branch level | −0.099*** | −0.045* | −0.054*** | −0.083** | −0.031 | −0.052*** | |||

| (0.030) | (0.025) | (0.017) | (0.033) | (0.026) | (0.018) | ||||

| |$\mbox{Before}^{-2}$| | 0.032 | 0.039 | −0.006 | ||||||

| (0.040) | (0.032) | (0.024) | |||||||

| |$\mbox{Before}^{0}$| | −0.037 | 0.014 | −0.051** | ||||||

| (0.041) | (0.033) | (0.024) | |||||||

| |$\mbox{After}^{2}$| | −0.123*** | −0.055 | −0.068*** | ||||||

| (0.043) | (0.034) | (0.026) | |||||||

| |${\rm After}^{4+}$| | −0.123*** | −0.058* | −0.065*** | ||||||

| (0.039) | (0.033) | (0.022) | |||||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 |

| Adj-|$R^{2}$| | 0.396 | 0.450 | 0.403 | 0.464 | 0.539 | 0.444 | 0.396 | 0.450 | 0.403 |

| Branch FEs | Y | Y | Y | Y | Y | Y | Y | Y | Y |

| Quarter FEs | Y | Y | Y | N | N | N | Y | Y | Y |

| Quarter-district FEs | N | N | N | Y | Y | Y | N | N | N |

| Dependent variable | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| | |${\ln}\left(\mbox{new ind.}\right.$| | |${\ln}\left(\mbox{# of}\right.$| | |${\ln}\left(\overline{\mbox{loan}}_{b,q}\right)$| |

|---|---|---|---|---|---|---|---|---|---|

| |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | |$\left.\mbox{debt}_{b,q}\right)$| | |$\left.\mbox{brwrs}_{b,q}\right)$| | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| Branch level | −0.099*** | −0.045* | −0.054*** | −0.083** | −0.031 | −0.052*** | |||

| (0.030) | (0.025) | (0.017) | (0.033) | (0.026) | (0.018) | ||||

| |$\mbox{Before}^{-2}$| | 0.032 | 0.039 | −0.006 | ||||||

| (0.040) | (0.032) | (0.024) | |||||||

| |$\mbox{Before}^{0}$| | −0.037 | 0.014 | −0.051** | ||||||

| (0.041) | (0.033) | (0.024) | |||||||

| |$\mbox{After}^{2}$| | −0.123*** | −0.055 | −0.068*** | ||||||

| (0.043) | (0.034) | (0.026) | |||||||

| |${\rm After}^{4+}$| | −0.123*** | −0.058* | −0.065*** | ||||||

| (0.039) | (0.033) | (0.022) | |||||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 |

| Adj-|$R^{2}$| | 0.396 | 0.450 | 0.403 | 0.464 | 0.539 | 0.444 | 0.396 | 0.450 | 0.403 |

| Branch FEs | Y | Y | Y | Y | Y | Y | Y | Y | Y |

| Quarter FEs | Y | Y | Y | N | N | N | Y | Y | Y |

| Quarter-district FEs | N | N | N | Y | Y | Y | N | N | N |

This table reports the effect of organizational design on total new lending to small individual borrowers (Columns 1, 4, and 7), the number of new individual borrowers (Columns 2, 5, and 8), and loan size (Columns 3, 6, and 9), using specification (1). The unit of analysis is a branch-quarter. The variable Branch Level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. |${\rm Before}^{-2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) in one or two quarters. |${\rm Before}^{0}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded this quarter or one quarter ago. |${\rm After}^{2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) two or three quarters ago. |${\rm After}^{4+}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) four quarters ago or more. The standard errors are reported in parentheses and clustered at the branch level. * significant at 10%; ** significant at 5%; and *** significant at 1%.

A concern regarding the above might be that our results are affected by simultaneous credit demand shocks. To account for this and other similar concerns, we saturate our main specification by including interacted quarter with district fixed effects. This specification controls for all time variation within those districts. As a result, we exploit the within-district variation between treated and nontreated branches. To the extent that local shocks affect all branches at a district level, such shocks are differenced out in our specification. As Columns 4 through 6 show, saturating the specification does not affect the qualitative nature of our results.20

In Columns 7 through 9, we investigate the dynamic effects of the organizational change. This test allows us to rule out differential pretreatment trends between treated and control branches. We replace the Branch level with four variables to track the effect of organizational design before and after the change: |$\mbox{Before}^{2}$| is a dummy variable that equals 1 (|$-1$|) for a branch that will be upgraded (downgraded) in one or two quarters; |$\mbox{Before}^{0}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded this quarter or one quarter ago; |$\mbox{After}^{2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) two or three quarters ago; and |$\mbox{After}^{4+}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) four or more quarters ago. The variable |$\mbox{Before}^{2}$| allows us to assess whether any effects can be found prior to the change. In fact, the estimated coefficient on the |$\mbox{Before}^{2}$| is economically small and statistically insignificant. Furthermore, we find that the coefficient on the |$\mbox{Before}^{0}$| is smaller than those on the |$\mbox{After}^{2}$| and |$\mbox{After}^{4+}$|, suggesting that the effect increases over the two quarters. In terms of the timing of the reorganization, we find that the effect on total lending is permanent after two quarters (Column 7), whereas the effect on average loan starts at the quarter of reorganization. The effect on the number of borrowers is slightly delayed and appears after four quarters. All in all, these results provide support to the view that information frictions generated by hierachization adversely affect lending quantities (see, e.g., Stiglitz and Weiss 1981). In the next section we examine how organizational hierarchy affects the quality of loans originated by a branch.

4.2 Loan repayment

If organizational hierarchy introduces information frictions, then one may expect a lower quality of originated loans (Stiglitz and Weiss 1981). To examine the effect of organizational hierarchy on future loan repayment, we estimate specification 1. We classify a loan as delinquent if it is more than 60 days past due within a year since origination. As before, we aggregate the loan-level default measure and obtain a branch-quarter delinquency rate.

We find that an increase in hierarchy increases loan delinquencies. The coefficients on the Branch level in Table 5 are economically large and statistically significant at 1%, for both equally weighted and value-weighted default rates in Columns 1 and 2, respectively. The absolute increase of value-weighted default rates is 1.4%, implying a 33% increase in the default relative to the mean value-weighted default rate of 4.2%. In comparison, the effect on the equally weighted measure is 1.0%, corresponding to a 20% increase relative to the mean. Moreover, the effects remain strong after controlling for local demand shocks through quarter-district fixed effects (Column 3).21 We also find a significant difference between the estimated value-weighted and equally weighted measures (Column 4). This is consistent with the view that less hierarchical branches are better informed and can allocate funds to more profitable projects. Finally, the dynamic effects of the change in organizational design (Columns 5 and 6) indicate that there is no pretreatment trend.

Effect of organizational design on loan repayment

| Defaults (60+ days late) | |||||||

|---|---|---|---|---|---|---|---|

| Equally weighted | Value weighted | Value weighted | Difference (2)-(1) | Equally weighted | Value weighted | ||

| (1) | (2) | (3) | (4) | (5) | (6) | ||

| Branch level | 0.010*** | 0.014*** | 0.009*** | 0.004*** | |||

| (0.003) | (0.003) | (0.003) | [0.008] | ||||

| |${\rm Before}^{-2}$| | 0.003 | 0.001 | |||||

| (0.004) | (0.004) | ||||||

| |${\rm Before}^{0}$| | 0.010*** | 0.013*** | |||||

| (0.004) | (0.004) | ||||||

| |${\rm After}^{2}$| | 0.009** | 0.013*** | |||||

| (0.004) | (0.003) | ||||||

| |${\rm After}^{4+}$| | 0.012*** | 0.015*** | |||||

| (0.004) | (0.003) | ||||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | ||

| Adj-|$R^{2}$| | 0.234 | 0.183 | 0.271 | 0.234 | 0.183 | ||

| Branch FEs | Y | Y | Y | Y | Y | ||

| Quarter FEs | Y | Y | N | Y | Y | ||

| Quarter-district FEs | N | N | Y | N | N | ||

| Defaults (60+ days late) | |||||||

|---|---|---|---|---|---|---|---|

| Equally weighted | Value weighted | Value weighted | Difference (2)-(1) | Equally weighted | Value weighted | ||

| (1) | (2) | (3) | (4) | (5) | (6) | ||

| Branch level | 0.010*** | 0.014*** | 0.009*** | 0.004*** | |||

| (0.003) | (0.003) | (0.003) | [0.008] | ||||

| |${\rm Before}^{-2}$| | 0.003 | 0.001 | |||||

| (0.004) | (0.004) | ||||||

| |${\rm Before}^{0}$| | 0.010*** | 0.013*** | |||||

| (0.004) | (0.004) | ||||||

| |${\rm After}^{2}$| | 0.009** | 0.013*** | |||||

| (0.004) | (0.003) | ||||||

| |${\rm After}^{4+}$| | 0.012*** | 0.015*** | |||||

| (0.004) | (0.003) | ||||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | ||

| Adj-|$R^{2}$| | 0.234 | 0.183 | 0.271 | 0.234 | 0.183 | ||

| Branch FEs | Y | Y | Y | Y | Y | ||

| Quarter FEs | Y | Y | N | Y | Y | ||

| Quarter-district FEs | N | N | Y | N | N | ||

This table reports the effect of organizational structure on loan repayment (Columns 1, 2, and 3) and its dynamics (Columns 5 and 6), using specification (1). Column 3 reports the effect on value-weighted default rates after controlling for local demand shocks through quarter-district fixed effects instead of quarterly fixed effects. Column 4 reports the difference between the estimated coefficients on equally weighted and value-weighted default rates. Defaults are measured as a fraction of loans that are over 60 days late 1-year forward, estimated at the branch-quarter level. The sample considers individual, new loans that can be approved within any branch. The variable Branch Level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. |${\rm Before}^{-2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) in one or two quarters. |${\rm Before}^{0}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded this quarter or one quarter ago. |${\rm After}^{2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) two or three quarters ago. |${\rm After}^{4+}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) four quarters ago or more. The standard errors are reported in parentheses and clustered at the branch level. p-values are reported in brackets. * significant at 10%; ** significant at 5%; and *** significant at 1%.

Effect of organizational design on loan repayment

| Defaults (60+ days late) | |||||||

|---|---|---|---|---|---|---|---|

| Equally weighted | Value weighted | Value weighted | Difference (2)-(1) | Equally weighted | Value weighted | ||

| (1) | (2) | (3) | (4) | (5) | (6) | ||

| Branch level | 0.010*** | 0.014*** | 0.009*** | 0.004*** | |||

| (0.003) | (0.003) | (0.003) | [0.008] | ||||

| |${\rm Before}^{-2}$| | 0.003 | 0.001 | |||||

| (0.004) | (0.004) | ||||||

| |${\rm Before}^{0}$| | 0.010*** | 0.013*** | |||||

| (0.004) | (0.004) | ||||||

| |${\rm After}^{2}$| | 0.009** | 0.013*** | |||||

| (0.004) | (0.003) | ||||||

| |${\rm After}^{4+}$| | 0.012*** | 0.015*** | |||||

| (0.004) | (0.003) | ||||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | ||

| Adj-|$R^{2}$| | 0.234 | 0.183 | 0.271 | 0.234 | 0.183 | ||

| Branch FEs | Y | Y | Y | Y | Y | ||

| Quarter FEs | Y | Y | N | Y | Y | ||

| Quarter-district FEs | N | N | Y | N | N | ||

| Defaults (60+ days late) | |||||||

|---|---|---|---|---|---|---|---|

| Equally weighted | Value weighted | Value weighted | Difference (2)-(1) | Equally weighted | Value weighted | ||

| (1) | (2) | (3) | (4) | (5) | (6) | ||

| Branch level | 0.010*** | 0.014*** | 0.009*** | 0.004*** | |||

| (0.003) | (0.003) | (0.003) | [0.008] | ||||

| |${\rm Before}^{-2}$| | 0.003 | 0.001 | |||||

| (0.004) | (0.004) | ||||||

| |${\rm Before}^{0}$| | 0.010*** | 0.013*** | |||||

| (0.004) | (0.004) | ||||||

| |${\rm After}^{2}$| | 0.009** | 0.013*** | |||||

| (0.004) | (0.003) | ||||||

| |${\rm After}^{4+}$| | 0.012*** | 0.015*** | |||||

| (0.004) | (0.003) | ||||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | ||

| Adj-|$R^{2}$| | 0.234 | 0.183 | 0.271 | 0.234 | 0.183 | ||

| Branch FEs | Y | Y | Y | Y | Y | ||

| Quarter FEs | Y | Y | N | Y | Y | ||

| Quarter-district FEs | N | N | Y | N | N | ||

This table reports the effect of organizational structure on loan repayment (Columns 1, 2, and 3) and its dynamics (Columns 5 and 6), using specification (1). Column 3 reports the effect on value-weighted default rates after controlling for local demand shocks through quarter-district fixed effects instead of quarterly fixed effects. Column 4 reports the difference between the estimated coefficients on equally weighted and value-weighted default rates. Defaults are measured as a fraction of loans that are over 60 days late 1-year forward, estimated at the branch-quarter level. The sample considers individual, new loans that can be approved within any branch. The variable Branch Level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. |${\rm Before}^{-2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) in one or two quarters. |${\rm Before}^{0}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded this quarter or one quarter ago. |${\rm After}^{2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) two or three quarters ago. |${\rm After}^{4+}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) four quarters ago or more. The standard errors are reported in parentheses and clustered at the branch level. p-values are reported in brackets. * significant at 10%; ** significant at 5%; and *** significant at 1%.

4.3 Return on loans

So far, we have shown that an increase in hierarchy leads to lower lending quantities and worsening of the credit quality of originated loans. To complete the picture, we next examine the effect of hierarchy on the profitability of loans. To calculate the return on loans (ROL), factors such as recovery rates and other contract terms need to be considered. We adapt the Khwaja and Mian (2005) methodology to generate this metric.22

We calculate the lifetime ROL for each loan separately, and then we aggregate the loan-level returns at the branch-quarter level. The return on a loan is estimated as follows:

where |$r_{bi\tilde{q}}$| is the quarterly interest rate for a borrower |$i$| at a branch |$b$| in the quarter |$q$|, |${\rm 1}\kern-0.24em{\rm I}_{{60+}_{bi\tilde{q}}}$| is a dummy variable equal to one if a loan is delinquent for 60 or more days within a year since the origination, |$\rho_{bi\tilde{q}}$| is the expected recovery rate; |$\hat{q}$| is the quarter when the loan is repaid in full, when the loan is 60+ days late, or the last quarter in our data set (whichever comes first). The important difference between us and Khwaja and Mian (2005) is that we use value-weighted returns over time |$\left(\omega={\rm Loan}_{biq}/\sum_{\tilde{q}=q}^{\bar{q}}{\rm Loan}_{bi\tilde{q}}\right)$|. 23 The weighting is important, because loans tend to have higher outstanding amounts in the beginning, and often, if a loan defaults, a considerable fraction is already repaid. A simple time-average would overestimate the effect of a default. All in all, the value-weighted ROL is a better measure for estimating the impact on a branch’s performance than the equally weighted measure.

When a loan becomes delinquent, the expected return is given by the following identity:

where |$\eta_{age_{i}}$| is the estimated value-weighted default probability, conditional on the age when the loan becomes 60+ days delinquent; and |$\delta_{\{s,u\}}$| is the value-weighted recovery rate from the defaulted loans, computed as the value recovered against the defaulted principal and interest due for secured |$\left(s\right)$| and unsecured |$\left(u\right)$| loans separately.

To account for censoring in our data (i.e., not all loans are repaid or default by the end of Q1:2006), in the last quarter of the data set we calculate the expected return on a loan in the following way:

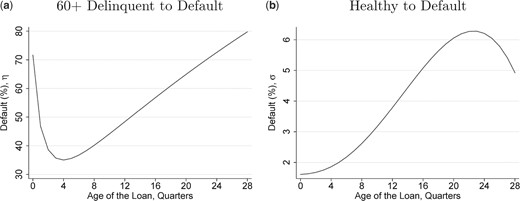

where |$\sigma_{age_{i}}$| is the transition probability of a healthy loan, or one that is less than 60 days late, defaulting eventually by loan age; and where |$r_{b,i,\tilde{q}}$| and |$\delta_{\{s,u\}}$| are the quarterly interest and the recovery rates, respectively. We then replace the term in brackets in the Equation (2) with the one calculated here |$\left(R_{b,i,\bar{q}}\right)$| for all healthy loans in Q1:2006. Lastly, the estimated default probabilities, required for computing the return on loans, are plotted in Figure 7.

Transition probabilities

The graphs plot the transition probabilities (value-weighted) of loans that subsequently defaulted (i.e., the legal proceedings with the borrower are finalized). The plot on the left presents the default probabilities for loans that are 60 or more days late, whereas the one on the right presents those for loans that are paid on time or are less than 60 days late. We track loans from the quarter they become 60+ days late and plot the average loans that default conditional on their age at the quarter becoming delinquent (panel A). Similarly, we track loans from their origination quarter and plot the average loans that default conditional on the age of a loan (panel B). Both graphs are smoothed using fractional-polynomial approximation.

We estimate the recovery rates for each organizational level separately, as well as whether or not the loan is secured. The recovery data are available only for the first quarter of 2006. The estimated value-weighted recovery rate for individual secured loans is 40%, whereas for unsecured loans it is only 16%, reflecting the importance of the realization value of the collateral when seized in default (see Table 6). Our average estimated recovery rate is similar to the 25% provided by the Doing Business database from World Bank (2013). For robustness, we also check our results using three other recovery rates:24 25% as suggested by the Doing Business Database of the World Bank, a pessimistic 15%, and an optimistic 50%. Qualitatively, the results remain the same.

Recovery rates

| Mean | SE | Obs | ||

|---|---|---|---|---|

| (1) | (2) | (3) | ||

| Recovery rate |$\left(\delta\right)$| | Branch hierarchy: | |||

| Secured | Decentralized | 48.07 | 0.56 | 2,516 |

| Medium | 39.76 | 0.70 | 2,240 | |

| Centralized | 40.77 | 1.69 | 358 | |

| Unsecured | Decentralized | 30.07 | 0.46 | 4,420 |

| Medium | 23.47 | 0.46 | 3,699 | |

| Centralized | 23.28 | 1.02 | 595 |

| Mean | SE | Obs | ||

|---|---|---|---|---|

| (1) | (2) | (3) | ||

| Recovery rate |$\left(\delta\right)$| | Branch hierarchy: | |||

| Secured | Decentralized | 48.07 | 0.56 | 2,516 |

| Medium | 39.76 | 0.70 | 2,240 | |

| Centralized | 40.77 | 1.69 | 358 | |

| Unsecured | Decentralized | 30.07 | 0.46 | 4,420 |

| Medium | 23.47 | 0.46 | 3,699 | |

| Centralized | 23.28 | 1.02 | 595 |

The table reports the mean (Column 1) and the standard error (Column 2) of our estimated recovery rates, which are used in return on loan calculations. Additionally, Column 3 reports the number of observations used in calculating the rates. We report value-weighted recovery rates from the defaulted loans computed as the value recovered against the defaulted principal and interest due for both secured and unsecured loans. Because of data limitations, the recovery rates are calculated only for loans written off in the first quarter of 2006. Unfortunately, we do not have the data from other quarters.

Recovery rates

| Mean | SE | Obs | ||

|---|---|---|---|---|

| (1) | (2) | (3) | ||

| Recovery rate |$\left(\delta\right)$| | Branch hierarchy: | |||

| Secured | Decentralized | 48.07 | 0.56 | 2,516 |

| Medium | 39.76 | 0.70 | 2,240 | |

| Centralized | 40.77 | 1.69 | 358 | |

| Unsecured | Decentralized | 30.07 | 0.46 | 4,420 |

| Medium | 23.47 | 0.46 | 3,699 | |

| Centralized | 23.28 | 1.02 | 595 |

| Mean | SE | Obs | ||

|---|---|---|---|---|

| (1) | (2) | (3) | ||

| Recovery rate |$\left(\delta\right)$| | Branch hierarchy: | |||

| Secured | Decentralized | 48.07 | 0.56 | 2,516 |

| Medium | 39.76 | 0.70 | 2,240 | |

| Centralized | 40.77 | 1.69 | 358 | |

| Unsecured | Decentralized | 30.07 | 0.46 | 4,420 |

| Medium | 23.47 | 0.46 | 3,699 | |

| Centralized | 23.28 | 1.02 | 595 |

The table reports the mean (Column 1) and the standard error (Column 2) of our estimated recovery rates, which are used in return on loan calculations. Additionally, Column 3 reports the number of observations used in calculating the rates. We report value-weighted recovery rates from the defaulted loans computed as the value recovered against the defaulted principal and interest due for both secured and unsecured loans. Because of data limitations, the recovery rates are calculated only for loans written off in the first quarter of 2006. Unfortunately, we do not have the data from other quarters.

Overall our results suggest that organizational hierarchy impedes information production and adversely affects not only the quality of loans but also their profitability. We find that the return on the same set of loans decreases after a branch becomes more hierarchical (Table 7). The value-weighted return on an individual loan decreases by 100 basis points (bps) (Column 2). Given that every quarter the bank earns 7.0% on every rupee lent (the value-weighted return), the 100-bps decline is equal to a 14% drop from the mean return. Similarly, for the equally weighted measure, the 70-bps fall in return (Column 1) is equivalent to a 10% slip in the branch’s performance. Further, the estimated results remain unchanged after controlling for local demand shocks through quarter-district fixed effects (Column 3) and do not have any pre-trend (Columns 5 and 6).25 Last, but not least, analogous to the delinquency result, we find a significant difference of 30 bps between value- and equally weighted measures (Column 4). This further supports the view that hierarchy leads to frictions in information production, suggesting that less hierarchical banks can allocate more money to profitable projects.

Return on loans

| ROL | ||||||

|---|---|---|---|---|---|---|

| Equally weighted | Value weighted | Value weighted | Difference (2)-(1) | Equally weighted | Value weighted | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Branch level | −0.007*** | −0.010*** | −0.006*** | −0.003** | ||

| (0.002) | (0.002) | (0.002) | [0.011] | |||

| |${\rm Before}^{-2}$| | −0.001 | −0.000 | ||||

| (0.003) | (0.003) | |||||

| |${\rm Before}^{0}$| | −0.007** | −0.010*** | ||||

| (0.003) | (0.003) | |||||

| |${\rm After}^{2}$| | −0.003 | −0.010*** | ||||

| (0.003) | (0.002) | |||||

| |${\rm After}^{4+}$| | −0.008*** | −0.012*** | ||||

| (0.003) | (0.002) | |||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | |

| Adj-|$R^{2}$| | 0.155 | 0.136 | 0.207 | 0.155 | 0.136 | |

| Branch FEs | Y | Y | Y | Y | Y | |

| Quarter FEs | Y | Y | N | Y | Y | |

| Quarter-district FEs | N | N | Y | N | N | |

| ROL | ||||||

|---|---|---|---|---|---|---|

| Equally weighted | Value weighted | Value weighted | Difference (2)-(1) | Equally weighted | Value weighted | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Branch level | −0.007*** | −0.010*** | −0.006*** | −0.003** | ||

| (0.002) | (0.002) | (0.002) | [0.011] | |||

| |${\rm Before}^{-2}$| | −0.001 | −0.000 | ||||

| (0.003) | (0.003) | |||||

| |${\rm Before}^{0}$| | −0.007** | −0.010*** | ||||

| (0.003) | (0.003) | |||||

| |${\rm After}^{2}$| | −0.003 | −0.010*** | ||||

| (0.003) | (0.002) | |||||

| |${\rm After}^{4+}$| | −0.008*** | −0.012*** | ||||

| (0.003) | (0.002) | |||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | |

| Adj-|$R^{2}$| | 0.155 | 0.136 | 0.207 | 0.155 | 0.136 | |

| Branch FEs | Y | Y | Y | Y | Y | |

| Quarter FEs | Y | Y | N | Y | Y | |

| Quarter-district FEs | N | N | Y | N | N | |

This table reports the effect of organizational structure on the equally weighted and value-weighted return on loans (Columns 1, 2, and 3) and its dynamics (Columns 5 and 6) using specification (1). Column 3 reports the effect on value-weighted returns after controlling for local demand shocks through quarter-district fixed effects instead of quarterly fixed effects. Column 4 reports the difference between the estimated coefficients on equally and value-weighted returns. The unit of analysis is branch-quarter return on loans. First, we estimate the return for each loan, as defined in Equation (2). Then we aggregate the loan-level estimate at the branch-quarter level using equal or value weights. The variable Branch Level is a number between 1 and 3, where the lowest value (level 1) and the highest value (level 3) characterize the least hierarchical branches and the most hierarchical branches, respectively. |$\mbox{Before}^{-2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) in one or two quarters. |$\mbox{Before}^{0}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded this quarter or one quarter ago. |$\mbox{After}^{2}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) two or three quarters ago. |$\mbox{After}^{4+}$| is a dummy variable that equals 1 (|$-1$|) if the branch was upgraded (downgraded) four quarters ago or more. Standard errors in parentheses are corrected for clustering at the branch level. p-values are reported in brackets. * significant at 10%; ** significant at 5%; and *** significant at 1%.

Return on loans

| ROL | ||||||

|---|---|---|---|---|---|---|

| Equally weighted | Value weighted | Value weighted | Difference (2)-(1) | Equally weighted | Value weighted | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Branch level | −0.007*** | −0.010*** | −0.006*** | −0.003** | ||

| (0.002) | (0.002) | (0.002) | [0.011] | |||

| |${\rm Before}^{-2}$| | −0.001 | −0.000 | ||||

| (0.003) | (0.003) | |||||

| |${\rm Before}^{0}$| | −0.007** | −0.010*** | ||||

| (0.003) | (0.003) | |||||

| |${\rm After}^{2}$| | −0.003 | −0.010*** | ||||

| (0.003) | (0.002) | |||||

| |${\rm After}^{4+}$| | −0.008*** | −0.012*** | ||||

| (0.003) | (0.002) | |||||

| Observations | 54,079 | 54,079 | 54,079 | 54,079 | 54,079 | |

| Adj-|$R^{2}$| | 0.155 | 0.136 | 0.207 | 0.155 | 0.136 | |

| Branch FEs | Y | Y | Y | Y | Y | |

| Quarter FEs | Y | Y | N | Y | Y | |

| Quarter-district FEs | N | N | Y | N | N | |

| ROL | ||||||

|---|---|---|---|---|---|---|

| Equally weighted | Value weighted | Value weighted | Difference (2)-(1) | Equally weighted | Value weighted | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Branch level | −0.007*** | −0.010*** | −0.006*** | −0.003** | ||

| (0.002) | (0.002) | (0.002) | [0.011] | |||

| |${\rm Before}^{-2}$| | −0.001 | −0.000 | ||||

| (0.003) | (0.003) | |||||

| |${\rm Before}^{0}$| | −0.007** | −0.010*** | ||||

| (0.003) | (0.003) | |||||