ABSTRACT

Though designed by a selective group of regulators from the world’s largest financial centres, Basel banking standards are being implemented far beyond the financial core, and this is often seen as confirmation of their global relevance. Yet, we show that the implementation of Basel II and III is shallow and highly selective in most countries outside of the Basel Committee on Banking Supervision. Drawing on primary and secondary sources and regression analysis, we attribute shallow and highly selective adoption to the sheer complexity of the standards, and the fact that they need substantial modification before they can be fully implemented, particularly in developing countries. Implementation challenges are compounded by gaps in the financial market infrastructure, notably credit rating agencies, as well as shallow capital markets. Beyond this, we attribute cross-country variation in implementation to differences in the underlying political economy of the banking sector. Countries are likely to pursue relatively high levels of Basel II and III implementation when large foreign and internationally active domestic banks operate in their jurisdiction and when they have a market-oriented approach to the financial sector. Conversely, countries are likely to pursue relatively low levels of implementation when they have few internationally active banks and a more interventionist approach.

1. INTRODUCTION

Regulators from the world’s largest financial centres have long dominated global financial governance, including in international banking. The Basel Committee on Banking Supervision (BCBS), which sets international banking standards, has a select membership drawn from the world’s largest financial centres. These ‘standard-setting’ regulators ‘control the rules of the game for global finance’ including through the Basel Concordat and the Basel Accords and ‘the prowess of the financial intermediaries they house’.1 The majority of the world’s regulators are ‘standard-takers’ with regards to international banking standards, exerting little influence over the standard-setting process.

Although countries outside of the BCBS are under no formal obligation to implement Basel standards, many are implementing them nonetheless. By 2005, regulators from more than 120 countries were implementing Basel I,2 and as we discuss below more than 70 jurisdictions outside of the BCBS recently reported that they are implementing elements of Basel II, of which 41 jurisdictions reported they are also implementing elements of Basel III.

While scholars have extensively studied the negotiation and implementation of Basel banking standards among the relatively small number of standard-setting countries, much less attention has been paid to the ways in which countries in the rest of the world are responding. To date, scholars have identified several reasons for the adoption of international standards by regulators in standard-taking countries. International banking standards provide regulators with off-the-rack guidance, which is particularly welcome as designing sui generis regulation is daunting and costly.3 Regulators are often conservative in their approach to regulation, and following ‘international best practices’ and the practices of successful peers can help insulate them from attribution and attendant costs in the event of a financial crisis.4 Adopting the standards can facilitate the operations of foreign banks in the jurisdictions of non-member states and can help domestic banks access the markets of BCBS members.5 Moreover, non-member countries have been strongly encouraged by the World Bank and International Monetary Fund (IMF) to implement international financial standards, notably the Basel Core Principles and Basel I.6

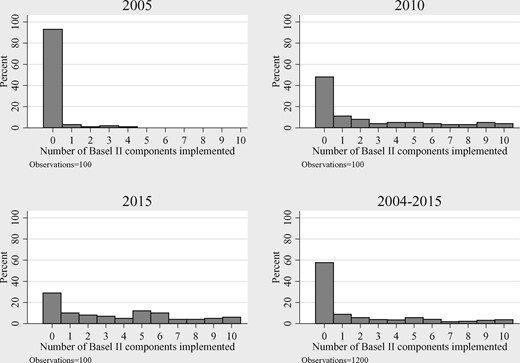

In this article, we contribute in two ways to the growing literature on Basel standards and standard-taking countries. First, we scrutinize in detail the level of Basel II and III adoption by countries outside of the BCBS and show that, despite perceptions that the standards have been widely adopted, this is only partly true. Although many countries have made moves to implement Basel II and III, when we disaggregate the data, we find that adoption is typically shallow and highly selective. More than 10 years after Basel II was agreed, non-members report that they are, on average, only implementing four of the 10 key components. Although Basel III is more recent so implementation is understandably more limited, four years after Basel III was agreed, non-members report that they are, on average, only implementing one of the eight key components. Implementation is particularly limited with regards to the internal model-based approaches for assessing risk under Basel II, and the macro-prudential elements of Basel III. We also find a high level of cross-country variation.

Our second contribution is to explain why the adoption of Basel II and III is highly selective and varies across countries. To do this we draw on the available primary evidence and the existing literature to identify possible explanations for the patterns of adoption that we see, and then explore their plausibility with a series of statistical tests. Given the small sample size and data gaps, we estimate simple regressions that offer proofs of concept for our different explanations.

We identify three over-arching explanations for the patterns of Basel II and III implementation that we see empirically. The first is politics within the banking sector. Implementation has distributive implications within the banking sector and we explain how large, internationally active banks typically gain from implementation, particularly of internal model-based approaches, while small and weakly capitalized banks typically lose. We, therefore, expect higher levels of Basel II and III implementation in countries where assets are concentrated in a few politically powerful, internationally active banks. We also expect the government’s wider policy approach to influence decisions over whether to adopt the standards, and expect higher levels of adoption among countries with relatively liberalized banking sectors and market-oriented approaches to financial sector regulation.

The second explanation is the sheer complexity of the Basel II and III. Implementation requires highly skilled supervisors with access to high levels of information, and a governance and legal environment that enables supervisors to use their judgement. In some instances, implementation may require new legislation that grants additional power to supervisors, particularly for the macro-prudential elements of Basel III. Regulators in developing countries face particularly acute resource challenges and also need to recalibrate Basel standards to reflect their local contexts. Basel standards were developed primarily for the supervision of internationally active banks in countries with sophisticated financial markets and specific elements either have limited relevance or require substantial revision before they can be implemented in many developing countries. Complexity and resource constraints are a persuasive explanation for particularly low levels of implementation of the most complex components of Basel, including the internal model-based approaches of Basel II and the macro-prudential elements of Basel III.

Finally, we explain why full implementation of Basel II and III requires well-developed financial market infrastructure, including credit ratings and credit information agencies, and well-developed capital markets. Where these are missing, we expect to find lower levels of implementation. The development of a local credit rating industry is particularly important for implementation of Basel II.

Our regression analysis provides initial support for many of these arguments. We consistently find that the level of financial sector depth is positively and strongly associated with the extent of Basel II and III adoption, as well as specific attributes of the wider financial infrastructure and depth of capital markets. We also find evidence that the internationalization of the banking sector, regulatory quality, and the wider regulatory approach matter for the extent of Basel II and III adoption.

A word about data is necessary at the outset. We rely on reported implementation of Basel II and III as captured in surveys conducted by the Financial Stability Institute (FSI). The surveys from which the dataset is compiled are voluntary and not externally verified, raising concerns about potential inaccuracies in the data. Spot-checking of national legislation and guidelines suggests that the survey data is in fact generally an accurate reflection of the extent of adoption.7 However, the survey data is vulnerable to selection bias, as regulators that are implementing the standards are perhaps more likely to respond than regulators that are not, so the data may exaggerate the level of implementation of Basel II and III among non-members. The fact that we nonetheless find implementation of the Basel standards to be patchy suggests that this is a robust finding. Finally, as Walter (2008, 2010) and Chey (2014) show, even when domestic legislation and regulatory guidelines reflect international standards, this does not necessarily translate into an alignment of the behaviour of banks and supervisors with international standards.8 Therefore, we focus our analysis on adoption and draw no inferences about substantive compliance.

2. THE WIDESPREAD YET HIGHLY SELECTIVE NATURE OF BASEL ADOPTION

The first Basel standard (Basel I) was agreed in 1988 and set minimum capital requirements for internationally active banks. The minimum ratio of regulatory capital to total risk-weighted assets (RWA) was set at 8 per cent, of which the ‘core capital’ element (a more restrictive definition of eligible capital defined as Tier 1 capital) would be at least 4 per cent. In 1996, Basel I was amended to introduce an additional capital charge to cover market risk in banks’ trading books. Although designed primarily for implementation by the members of the BCBS, by 1992, only four years after it was agreed, Basel I was being implemented by many non-member countries with internationally active banks.9 By 2005 it was reportedly implemented by 120 countries.10

(a) Basel II

Weaknesses in Basel I led to calls for reforms of the standards by the late 1990s. A concern with Basel I was that it did not sufficiently differentiate the risk associated with individual loans. This opened up opportunities for regulatory arbitrage, which banks capitalized on using a range of securitization techniques.11 In addition, Basel focused exclusively on credit and market risk, neglecting operational risk, and did little to strengthen supervisory institutions or improve corporate governance.

Basel II standards were agreed in 2004 following intense and protracted negotiation. The aim of the new standards was to ensure that the regulatory capital held by banks better reflected the actual risks that banks were undertaking. Basel II left some basic parameters of Basel I in place, including the definitions of eligible capital and the 8 per cent minimum capital adequacy requirement, but dramatically changed the system for risk-weighting assets. Basel II moved away from relatively simple compliance-based supervision to more complex risk-based supervision, and assigned a central role to market actors (banks and external credit rating agencies) in risk assessment. The innovation of Basel II was to allow banks to use their own models for assessing risk. Although banks must use metrics established by supervisors, banks typically have a comparative advantage over supervisors in resources, expertise, and experience for the sophisticated assessment of risks, enabling them to calibrate the models to their advantage.12

We trace the variation in adoption of both Basel II and III using data from surveys conducted by the FSI, from which we code adoption of 18 key components of the Basel standards over the period 2004–15 for 100 jurisdictions. The survey is aimed only at jurisdictions outside of the BCBS, and asks respondents to indicate the extent of implementation for individual subcomponents of the banking standard and, if adopted, the date of first adoption.13

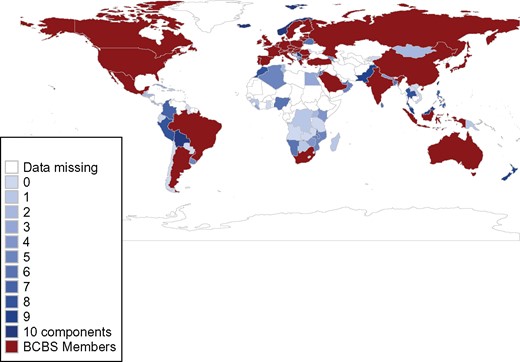

The FSI survey data shows that Basel II is being widely implemented by jurisdictions outside of the BCBS. By 2015, regulators from 71 of 100 responding jurisdictions reported that they were implementing at least one element of Basel II. A further 19 jurisdictions reported that they were in the process of implementing and had drafted rules in line with Basel II. Only 10 responding jurisdictions reported that they had not taken any steps to implement Basel II (Bhutan, Belize, East Caribbean Currency Union, Ghana, Laos, Madagascar, Moldova, St. Kitts and Nevis, Swaziland, and West African Monetary Union).

Map showing global uptake of Basel II.

Distribution of Basel II implementation over time among Basel non-members.

Regulators are being highly selective about which components they adopt. Basel II is divided into three ‘pillars’: Pillar 1 sets out the minimum capital requirements; Pillar 2 provides guidance on the supervisory oversight process; and Pillar 3 requires banks to publicly disclose key information on their risk profile and capitalization as a means of encouraging market discipline. While designed as a mutually reinforcing package, regulators can decide to implement any combination of these pillars they wish. Just over half (39 of 71) of the regulators that report adopting any of Basel II are indeed doing so as a package, having adopted components from all three pillars. Among the remaining jurisdictions, 16 adopted two pillars, and 14 adopted only one pillar. Of the latter, the vast majority adopted components only from Pillar 1 on capital requirements (12 of 14).

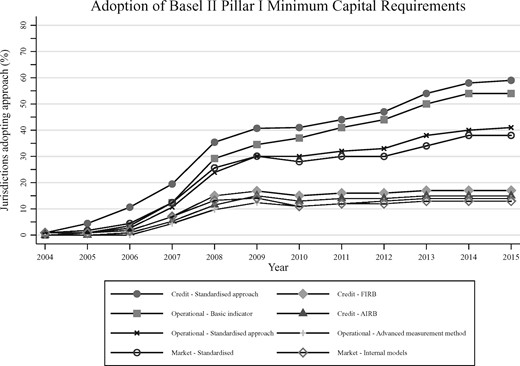

Pillar 1 provides regulators with different options for calculating credit risk (risk of default on a debt that may arise from a borrower failing to make required payments), operational risk (risk of loss resulting from inadequate or failed internal processes, people and systems or from external events), and market risk (risk of losses in on and off-balance sheet positions arising from adverse movements in market prices). The FSI survey data shows that within Pillar 1 regulators are more likely to adopt requirements for credit risk (59 of 66 jurisdictions adopting any element of Pillar 1) and operational risk (57 jurisdictions) than market risk (38 jurisdictions). In general, countries only adopted Basel II rules on market risk if they had already adopted Basel II standards for credit and operational risk.

Within each of these three categories of risk, Basel II provides regulators with different approaches to assess risk. There are four relatively simple approaches: the ‘standardised’ approach for assessing credit risk, the ‘basic indicator’ and ‘standardised’ approaches for assessing operational risk, and the ‘standardised’ approach for assessing market risk. The defining feature of these approaches is that while they are more complex than Basel I, key parameters for assessing risk are either given to banks by the supervisor or generated by third parties (private credit rating agencies as well as export credit agencies).14 Basel II also provides for a ‘simplified standardised’ approach for assessing credit risk, which is very similar to Basel I and is specifically designed for the use of developing countries.

The remaining four approaches15 allow banks to use their own internal models for assessing risk and these are then used as the basis for calculating capital requirements. There are two approaches for assessing credit risk. Under the ‘foundation approach’, banks are allowed to estimate probabilities of default for each borrower, while under the ‘advanced approach’ banks also estimate other parameters, such as loss given default and exposure at default.

Adoption of Basel II subcomponents from time of introduction among Basel non-members.

(b) Basel III

The global financial crisis of 2008 laid bare the weaknesses of the existing international regulatory regime for banking and led to further revisions of Basel standards.17 The risk-sensitivity of Basel II capital requirements was criticized for exacerbating pro-cyclicality and increasing the likelihood of crisis.18 The crisis also highlighted the need to better address risks associated with securitization, counterparty credit exposure stemming from derivatives, and repurchase and securities financing.19

Basel III was agreed in stages between September 2010 and late 2014 and aimed at addressing these shortcomings. Unlike Basel II, Basel III standards explicitly seek to increase the amount and quality of capital held by banks. Basel III also introduced liquidity standards and a series of macro-prudential measures aimed at containing the build-up of systemic risk. Although a clear improvement on Basel II, Basel III standards have also been criticized for being too weak.20

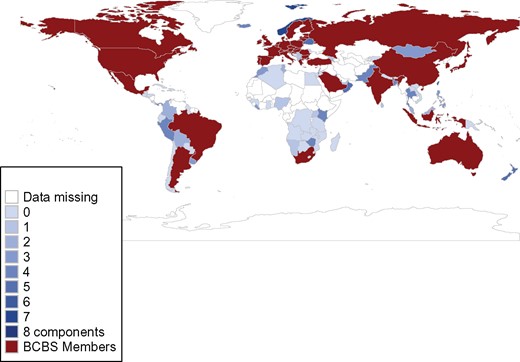

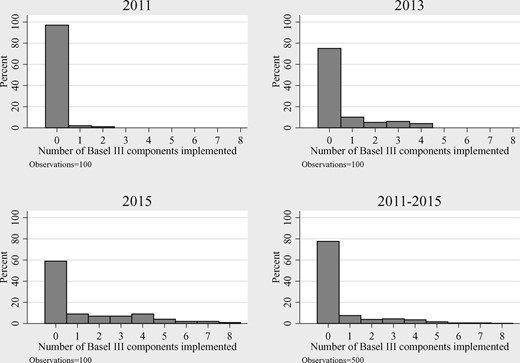

The FSI data shows that Basel III is being widely implemented by non-members of the BCBS. Although Basel III is relatively new, two-fifths of the jurisdictions in our dataset (41 of 100) reported that they were implementing at least one component by 2015. A further 40 jurisdictions had started the process of implementation, leaving only 17 responding jurisdictions that had not taken any steps at all towards implementation.

Map showing global uptake of Basel III.

Distribution of Basel III implementation over time among Basel non-members.

As Basel III is relatively new and the standards have been issued over several years, it is harder to discern trends in the data regarding the specific components that are being implemented. However, the data indicates that macro-prudential components are being implemented less frequently than other components.

Basel III sought to improve the quality and quantity of capital held by banks. It introduced stricter rules on the eligibility of instruments to be included in Tier 1 capital (definition of capital). Under Basel I and II, banks had to hold a minimum of 8 per cent of RWA, and this remains unchanged under Basel III. However, where Basel I and II stipulated that 4 per cent RWA had to be Tier 1, Basel III increases this to 6 per cent. In addition, Basel III differentiates between ‘common equity Tier 1’ and other forms of Tier 1 capital, and stipulates that banks must hold at least 4.5 per cent of the former at all times.21

A new capital conservation buffer of 2.5 per cent of RWA is introduced, which comprises common equity Tier 1 capital. This is established above the regulatory minimum capital requirement and is designed to ensure that banks build up capital buffers outside periods of stress, which can be drawn down as losses are incurred.22 Total capital requirements are thus raised to common equity Tier 1 capital of 7 per cent and Tier 1 capital of 8.5 per cent of RWA. While banks can hold less than this they face restrictions on pay-outs to shareholders and employees. Basel III also introduces measures to strengthen the capital requirements for counterparty credit exposures arising from banks’ derivatives, repurchase, and securities financing activities.23

Adoption of Basel III subcomponents from time of introduction among Basel non-members.

Liquidity standards were introduced under Basel III for the first time. The objective of the liquidity coverage ratio (LCR) is to promote the short-term resilience of the liquidity risk profile of banks by ensuring that banks have an adequate stock of unencumbered high-quality liquid assets that can be converted easily and immediately in private markets into cash to meet their liquidity needs for a 30-day liquidity stress scenario.24 The net stable funding ratio (NSFR) complements the LCR. It is a longer-term structural ratio that requires banks to maintain a stable funding profile in relation to the composition of their assets and off-balance sheet activities. This is intended to reduce the likelihood that disruptions to a bank’s regular sources of funding will erode its liquidity position in a way that would increase the risk of its failure.25

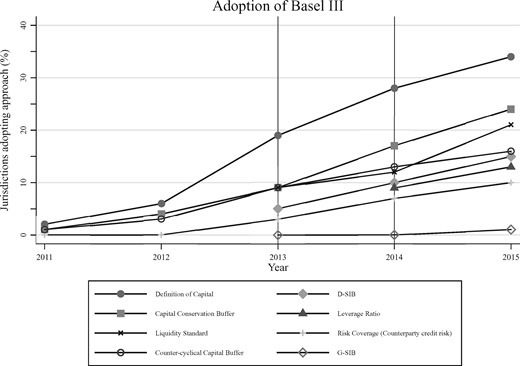

The FSI data shows a relatively rapid take-up of the LCR, with 21 of the 41 jurisdictions adopting it as at 2015 (Figure 6). Data is not yet available on the NSFR as it was only introduced towards the end of 2014.

The final element of Basel III we examine is the introduction of macro-prudential measures. A countercyclical buffer aims to ensure that banking sector capital requirements take account of the macro-financial environment in which banks operate. It enables regulators to require banks to increase the regulatory capital they hold by up to 2.5 per cent of common equity Tier 1 when they judge credit growth to be resulting in an unacceptable build-up of system-wide risk. Basel III also introduced a simple leverage ratio of capital to non-RWA of 3 per cent, to act as a ‘back-stop’ to the risk-based capital framework, seeking to restrict the build-up of excessive leverage in the banking sector.26

Specific additional standards are introduced for systemically important banks, based on the negative externalities they create that other regulatory policies do not fully address. Banks that are assessed by the BCBS as being systemically important on a global level (G-SIBs) face higher loss absorbency requirements of up to 3.5 per cent of RWA, comprised exclusively of common equity Tier 1 capital.27 Basel III also introduces measures for banks that are systemically important in the domestic market (D-SIBs), although it adopts a much less prescriptive approach than for G-SIBs, simply issuing a series of principles that national authorities should follow in assessing which banks are systemically important and in establishing the higher loss absorbency requirements.28

In general, macro-prudential components of Basel III have been adopted less frequently than other components. There has been a relatively rapid take-up of the leverage ratio, which has been adopted by 13 of the 41 jurisdictions implementing at least one element of Basel III, even though it was only introduced in 2013. Fifteen jurisdictions have adopted the new standards on D-SIBs, and 16 have adopted the counter-cyclical buffer. Only one of the reporting jurisdictions, Liechtenstein, had adopted the G-SIB standard by 2015, reflecting the fact that almost none of the regulators outside of the BCBS are home regulators of globally systemically important banks.

3. EXPLAINING SHALLOW AND SELECTIVE IMPLEMENTATION OF BASEL II AND III

Patterns of Basel implementation can be explained, we argue, with reference to several factors: politics within the banking sector; supervisory capacity, legal powers and the government’s regulatory approach; and development of financial infrastructure and the wider financial market. These factors can account for the fact many countries outside of the BCBS are moving to implement Basel II and III, but that implementation is generally shallow and highly selective.

(a) Banking sector politics

A substantial body of literature shows how the interests of large banks have shaped regulatory decisions, including through direct lobbying, revolving institutional doors, and intellectual and cognitive capture.29 Moreover, because of the strategic importance of the financial sector in the economy, even in the absence of such mechanisms of direct influence, regulators may be wary of introducing regulations that could disrupt the ‘golden goose’ of financial sector accumulation. Where governments have been able to introduce regulations that impose substantial costs on large banks this has often come about in the wake of a financial crisis. While regulatory capture is relatively easy during boom times when banking regulation has little political salience, it has been much harder in the wake of a financial crisis as public anger provides a political counterweight that makes redistributive reform possible.30

The design of Basel II and III has in many ways followed this logic. Basel II regulations were designed during a period of high growth and ‘derived directly from an agenda set by proposals from the private sector’.31 Arguably as a direct consequence of the influence they had over the decision-making process, Basel II lowered the amount of capital that the largest banks in Basel member countries were required to hold, by close to 30 per cent in some cases.32 Although Basel II introduced standards on operational risk, these increases in capital requirements were more than offset by the reduction that resulted from allowing banks to use their own internal models for assessing risk.33 Conversely, Basel III rules, which were designed in the wake of the global financial crisis, entail substantial (intended) adjustment costs for the largest banks as they required them to hold more and better quality capital.34

Might a similar logic hold for countries outside of the BCBS? Is it plausible that the patterns of implementation reflect the interests of large banks? We consider two ways in which large banks are likely to be affected by the implementation of Basel II and III standards: through the direct adjustment costs the new capital and liquidity standards impose, and by facilitating the cross-border operations of internationally active banks.

(i) Adjustment costs

In contrast to impact studies for Basel member countries, the available evidence suggests that neither Basel II nor Basel III implementation is likely to systematically affect the level of capital held by the large banks in the majority of non-member countries. The FSI survey data presented above shows that non-member countries that are implementing Basel II capital adequacy requirements are typically doing so for both credit and operational risks, without authorizing the use of internal model-based approaches. While we might expect this to result in substantial adjustment costs for large banks, this does not appear to be systematic. For instance, in a 2011 World Bank survey of regulators in Basel non-member jurisdictions, only 15 per cent of respondents stated that Basel II implementation had significantly impacted the level of bank capital and, where it did, it typically led to increases.35

Analysis of Basel III suggests that large banks in non-member countries will meet Basel III capital standards relatively easily, although adjustment costs vary greatly depending on the business characteristics of banks and variations in national tax regulations.36 A study covering 127 banks in 42 emerging and developing countries suggests that on average, only 10 per cent of core Tier 1 capital would need to be deducted to meet the most stringent Basel III standards. The main exception is for banks in Latin America and Caribbean region, which are expected to have to make deductions of up to 30 per cent,37 which might help explain why Basel III implementation is lower than average in this region.38 Another study of Basel III implementation in 47 emerging economies shows that banks in more advanced emerging economies are more likely to face adjustment costs than banks in secondary and frontier markets.39

These relatively low adjustment costs derive from the fact that banks in many developing countries typically hold capital well above the minimum international standards as the result of national regulatory requirements and the nature of the financial sector in which they operate. In many developing countries national authorities impose higher capital standards than the Basel minima and impose a broad range of restrictions on the composition of banking assets and liabilities, including restrictions on large loan concentrations, foreign exchange exposures, and activities that fall outside traditional banking.40 This does not mean that capital is necessarily of high quality as other factors, including accounting weaknesses, may put the quality of capital into question, but it does mean that nominal compliance with the Basel standards ought to be within reach. In Africa, for instance, more than one-third of national regulators impose higher capital standards than required under both Basel II and Basel III.41

Moreover, banks in many developing countries often hold more capital than the regulatory minima because of the volatility of their operating environment and/or the nature of their business environment. Banks in many developing countries are likely to be well positioned to meet the specific capital quality requirements of Basel III because their capital base is typically dominated by common shares and retained earnings.42

The adjustment costs associated with implementing liquidity standards are also expected to be relatively low in most non-member countries. However there is wide variation, with banks in Eastern Europe and Latin America and the Caribbean facing the greatest adjustment costs in meeting the NSFR.43 This is due to dependence on wholesale funding and high loan-to-deposit ratios, as well as low levels of government securities in asset portfolios. In some countries, banks may find it difficult to meet the LCR because they lack access to a sufficiently diversified portfolio of high quality liquid assets.44 In South Africa, for instance, the supply of government bonds domestically is expected to be insufficient to meet the expected demand from South African banks, while the ratings of most corporate bonds is below the minimum required for them to qualify as high quality under Basel III.45

In countries where large banks hold levels of capital close to the regulatory minimum, we expect large banks to lobby for the use of internal model-based approaches, as they did in Basel member countries, and there is evidence to this effect from Brazil, South Africa, and India.46 A recent report on Basel implementation in non-member countries hints that large banks continue to pressure supervisors in this way.47

Even where adjustment costs are relatively low, banks may be wary of specific aspects of Basel II and III, particularly requirements to increase public disclosure of financial information and those that impose additional capital requirements on systemically important domestic banks. In Malaysia and Thailand, for instance, powerful family-owned banks strongly resisted disclosure requirements that would have revealed high levels of related-party lending.48 Of course small and weaker banks are likely to oppose Basel implementation. However, we expect that regulators are more likely to adapt the national implementation of Basel standards in the face of opposition from small domestic banks, rather than decide not to implement them at all. In the USA and India, for instance, regulators have adopted a tiered approach to Basel that exempts smaller banks from the more complex regulations.

The patterns of Basel II and III implementation revealed by the FSI survey data are largely consistent with the argument that adjustment costs are not a major impediment to Basel implementation, and do not provide a ready answer for shallow and selective adoption. Among all the key components, the micro-prudential capital requirements of Basel II and III are adopted most frequently, suggesting that capital-related adjustment costs are not deterring implementation. While relatively few non-member countries are implementing the countercyclical buffer, we attribute this to the technical challenges associated with implementation rather than the adjustment costs it will impose on banks, as we discuss below. The FSI data shows a relatively rapid take-up of the LCR, which is also congruent with the analysis suggesting that high adjustment costs are unlikely to be a major obstacle to implementation. Although data is not yet available on the NSFR, the evidence reviewed above suggests that banks are unlikely to face high adjustment costs. However, the complexity of the NSFR gives rise to specific challenges, as we discuss below.

(ii) Internationalization of the Banking Sector

In addition to the magnitude of adjustment costs faced by large banks, it is important to consider other incentives that large banks have vis-à-vis the implementation of Basel II and III in non-member countries. Crucially, the more internationally active large banks are, the greater the likelihood that they will advocate Basel II and III implementation. Moreover, as the presence of international banks increases, so does the experience and expertise of regulators, which raises the likelihood that they will have the capacity to implement Basel II and III.49

It is reasonable to expect foreign banks in non-member countries, particularly those operating as locally incorporated subsidiaries and subject to host-regulation, to advocate for the implementation of Basel standards. Foreign banks that already comply with Basel standards at home can derive substantial competitive benefits from their adoption by host regulators in jurisdictions where competitor banks will struggle to meet the costs associated with compliance.50

Regulators may also implement Basel standards to help domestic banks expand overseas. As Simmons (2001) explains, large financial centres have sought to use threats of market exclusion to pressure other countries to adopt their regulations.51 The Basel framework explicitly requires host countries to review the supervisory and regulatory regimes of home countries with a view to determining whether the home country regime is ‘adequate’, where adequate is defined as compliance with the BCBS framework and other relevant international standards.52 Thus, as a matter of practical regulatory policy, Basel implementation is an important mechanism for helping domestic banks gain access to the markets of Basel member countries.53 This was a major driver of Basel I adoption in Taiwan and Korea in the 1990s and helps explain relatively high levels of Basel implementation among countries in the Persian Gulf.54

Even where Basel implementation is not a formal requirement, national authorities may adopt the standard to boost the international reputation of their internationally active banks.55 As the Executive Director of the Reserve Bank of India recently noted: ‘Any deviation [from global standards] will hurt us both by way of reputation and also in actual practice. The “perception” of a lower standard regulatory regime will put Indian banks at a disadvantage in global competition.’56 In China, state-owned banks have championed Basel II implementation, as it has allowed them to attract foreign investors and management techniques, improve their credit ratings, and expand their foreign activities.57

As cross-border banking activity increases, regulators also face strong incentives to adopt Basel standards to facilitate home–host supervisory coordination. Precisely because Basel standards are widely recognized, we expect them to act as a focal point for cross-border collaboration and to result in convergence on Basel. We expect this effect to be particularly powerful when host regulators engage in supervisory relationships with home regulators that are already implementing the latest Basel standards.

(b) Alignment with supervisory capacity, legal powers and regulatory approach

The second major explanation we consider for variation in Basel adoption is the degree of alignment between Basel II and III standards and the existing capacity and legal powers of national supervisors as well as the government’s broader approach to banking regulation.

The sheer complexity of Basel II and III standards and the extensive work involved in recalibrating them to reflect local conditions helps explain low adoption of the most complex components, particularly in developing countries. Even national authorities in long-standing Basel member countries have found implementation of Basel II and III challenging. As a senior official from the Bank of England notes in reflecting on the UK’s experience,

Implementation may also require new legislation granting additional power to supervisors, particularly for the macro-prudential elements of Basel III, though we expect this to slow down rather than wholly deter implementation.to use models and stress tests effectively requires intensive development and maintenance by firms and a highly skilled body of supervisors and a regime where judgement can be used. It also requires the supervisor to have a credible capacity to withdraw the permission given to a firm to use a particular model if the model is considered to be inadequate or the firm has not demonstrated the capacity to use it safely.58

(i) Supervisory capacity

Although supervisory capacity is a constraint in most non-member countries, it is a particularly acute constraint in the poorest developing countries and can be a major deterrent against moving from relatively simple compliance-based supervision under Basel I to risk-based supervision under Basel II and III.59 Even the simplest approaches for risk assessment under Basel II substantially increase the complexities of banking supervision when compared with Basel I. To effectively supervise the standardized approach to credit risk for instance, supervisors have the extra responsibility of defining and monitoring credit rating agencies, their credit ratings, and the extra task of ensuring that banks use those ratings appropriately.60

Basel III adds a further layer of complexity, exacerbating implementation challenges (as an indication, Basel I was 30 pages long, Basel II was more than 300 pages, and Basel III more than 600 pages in length). In a survey conducted by the Financial Stability Board, national supervisors from emerging and developing countries cited a shortage of high-quality human resources as the most important constraint to the implementation of Basel II and III.61 Human and financial constraints on the part of the Ethiopian authorities helps explain why they continue to implement Basel I.62 Capacity constraints are not confined to low-income countries: middle-income counties including Mauritius, Botswana, and Namibia also face substantial constraints.63

These challenges are compounded by the fact that national supervisors need to tailor Basel banking standards to the specific contexts in which they operate. There is consensus in academic and policy circles that in financial regulation one size does not fit all and there is an inevitable divergence between the international standards and the sui generis regulations that would be most appropriate to each jurisdiction’s industry structure, pre-existing financial regulation, and political preferences.64

The BCBS has recognized the need for differentiation and while they seek to provide a common set of minimum standards, they also allow national authorities a range of different options to consider when implementing the standards. However, as a World Bank report notes, in some small or lower-income countries, the full range of options proposed by the BCBS is not properly thought through, resulting in the adoption of overly complex regulations for the level of economic development and complexity of the financial system.65 Moreover, for many developing countries, Basel III is arguably over reliant on capital adequacy ratios and overlooks more important sources of financial risk arising from weaknesses in areas such as loan provisioning and consolidated supervision.66

(ii) Specific capacity challenges

Some elements of Basel II and III are particularly complex. Within Basel II, the internal model-based approaches are the most challenging components to implement, requiring high levels of technical expertise and historical data. Implementing the foundation approach to credit risk is particularly demanding as supervisors rather than banks provide key inputs (loss given default and exposure at default).67 Meanwhile, internal model-based approaches to market risk require supervisors to maintain staff with a high degree of technical skill and experience in reviewing banks’ trading operations. The internal model-based approaches to operational risk are perhaps the most challenging to implement as they give a high level of flexibility to banks and require substantial efforts by national authorities to ensure consistency in application.68

Large banks in some developing countries may find it hard to implement internal model-based approaches as they are generally less advanced than their counterparts in more developed countries in terms of developing and using internal rating methodologies, mapping those ratings into default probabilities, and establishing portfolio models of credit risk. Indeed, in many emerging countries, the supervisory agency’s main motivation for moving towards the Basel II internal model-based approaches may be to improve banks’ own internal risk management.69 However, supervisors run the risk that banks will use their comparative advantage over supervisors in resources, expertise, and experience to calibrate the models to their advantage, as they have in more developed countries.

Given the challenges of implementing internal model-based approaches, it is perhaps not surprising that these are the components of Basel II implemented least frequently. In Africa, a lack of supervisory capacity and historical data help explain slow implementation.70 Several experts argue that full implementation of Pillar 2 (which aims at strengthening supervision) is a prerequisite for the use of internal model-based approaches.71 Regulators appear to be following this advice. The FSI data shows that, as at 2015, among the 19 jurisdictions implementing a model-based approach, only Bahrain and Peru had done so without also implementing Pillar II.

As with Basel II, the components of Basel III vary in their complexity. Some elements are relatively straightforward for supervisors to implement, particularly the new definitions of capital, the capital conservation buffer, the simple leverage ratio, and the D-SIB standard. Others are more challenging. The additional resource demands of adopting a macro-prudential approach are considerable, particularly in skills, training, modelling, technology, and data. Moreover, macro-prudential standards under Basel III need to be adapted to reflect the main sources of systemic risk in many low-income countries, which often stem from external macro-economic shocks rather than the use of complex financial instruments and a high level of interconnectedness among banks.72 Moreover, national authorities may lack dedicated units for conducting macro-prudential surveillance and even where they do exist, they often face many practical challenges, including gathering data and specifying models to be used in stress testing.73

The design of the countercyclical buffer has been criticized for its mechanistic reliance on the credit to gross domestic product (GDP) ratio. While it is possible to design more effective buffers, many supervisory authorities lack the macro-economic tools and methodologies to do so. In particular, the effectiveness of the buffer depends heavily on the supervisor’s ability to accurately anticipate credit bubbles, which is particularly challenging in developing countries where the economy is changing rapidly.74

The LCR and NSFR are relatively more sophisticated than most other Basel methodologies and need to be calibrated to suit local contexts.75 Before implementing the LCR, national supervisors need to conduct granular quantitative impact studies to gauge whether there will be any challenges for banks in accessing the necessarily level and diversity of high-quality liquid assets. In developing and small economies where an LCR-like rule does not already exist and cross-border activities are minimal, the Basel Consultative Group proposes that the LCR should be introduced gradually.76

A specific critique of the NSFR is that it may deter banks from engaging in long-term lending, especially in developing countries with shallower capital markets and heavy reliance on banks for long-term financing. National authorities need to conduct impact assessments to assess whether the factors used to calculate the ‘available stable funding’ in the Basel NSFR framework are justified in their jurisdictions. For instance, in smaller jurisdictions where non-resident deposits play a big role or where large cross-border mobility of deposits is observed, these deposits might be less reliable than assumed in the Basel framework, and a lower available stable funding factor might be warranted.77 Given these constraints, basic approaches such as the simple customer loans-to-deposit ratio seen in some developing countries may be more appropriate and easier to implement than the liquidity standards specified under Basel III.78

(iii) Legal powers

Aside from the technical challenges of implementing complex standards, specific components of Basel II and III require substantial legal powers on the part of national supervisors. In countries where they have limited operational autonomy vis-à-vis local political authorities, supervisory authorities are likely to support implementation as a means of increasing their autonomy, as has been the case in China.79 Where governments are willing to grant these powers, new parliamentary legislation may be required, and this can slow down implementation.

Under Basel II, the implementation of Pillar 2 requires that national supervisors have the powers to ensure prompt corrective action, the legal mandate to impose higher capital requirements, and ability to conduct supervision at a consolidated level, while Pillar 3 requires the oversight of confidentiality rules.80 Full compliance with the internal model-based approaches relies on highly skilled regulators using judgment and discretion, thereby placing even more onus on regulators being independent, immune from lawsuits, and willing to challenge the well connected.81

The macro-prudential rules under Basel may require changes to the legal framework, as regulators may lack the legal authority for intervening on the basis of macro-prudential factors as opposed to institution-specific factors. The implementation of some components may require quite specialized powers. Implementation of the new ‘definitions of capital’ requires all regulatory capital instruments to be able to absorb losses in the event that the issuing bank reaches the point of non-viability. This in turn requires that supervisors have sufficient powers to make judgment calls about the point at which a bank is deemed to be unable to continue on its own. Similarly, for the capital conservation buffer to be effective, restrictions on the distribution of profits in cases of non-compliance should be automatic and imposed on banks through requirements set forth by national legislation. Where foreign banks have a systemically important local presence, supervisors may require increased supervisory powers over branches and the ability to require conversion of branches into subsidiaries to implement the requirements on D-SIBs, and prevent banks in host jurisdictions from circumventing the higher loss absorbency requirements.82

In many non-member countries, national authorities lack the political and operational independence as well as the required enforcement powers to fully implement Basel II and III.83 In francophone West Africa, for instance, the Banking Commission lacks sufficient power to enforce corrective measures in the case of non-compliance with regulations.84

(iv) Alignment with prevailing regulatory approach

Governments around the world take different approaches to regulating the banking sector. In statist systems, characterized by a high level of government ownership and control of banking, governments typically take an interventionist approach, including by directing credit and setting interest rates. Conversely, where the private sector dominates, the regulatory approach is often arms length, based on prudential norms and supervisory oversight.85

Basel II and III standards are part of a wider set of international financial standards that assume an arms-length relationship between the regulator and the regulated and, given the right information in a timely fashion, that private capital markets will operate efficiently.86 This policy orientation is deeply embedded across the Basel framework. The Basel Core Principles emphasize the need for supervisors to have operational independence, free from political interference, and the relevant legal powers to ensure compliance. They allocate a central role to ‘robust market discipline’ for ensuring that the banking sector is ‘safe and sound’ and accordingly emphasize the need for public disclosure and transparency. Policy-directed lending and the general use of financial intermediaries as instruments of government policy are identified as distorting market signals and impeding effective supervision.87

Basel II standards place greater emphasis on market actors and price signals than Basel I, with credit ratings agencies and banks accorded central roles in evaluating risks and the third pillar of Basel II dedicated to improving market discipline including through new public disclosure requirements. Compared with Basel I, Basel II and III also require governments to confer additional legal powers on supervisors.

In non-member countries where the government’s approach to the financial sector is very different from that promoted by the Basel framework, we expect lower levels of Basel II and III implementation. This is particularly likely in countries where the government directly allocates credit through policy-directed lending. This regulatory strategy tends to empower local banks and firms at the expense of foreign banks and firms, and any move away from the developmental state model is likely to provoke opposition from local elites who have been privileged.88 Analysis from Basel I implementation in Korea shows how a low level of regulatory alignment generated substantial resistance to implementation.89 In China, the introduction of Basel I was opposed by powerful factional elements within the party–state apparatus that benefited from the politically directed credit allocation, and implementation only began in earnest after the Asian financial crisis alerted the leadership to the risks associated with an unreformed financial sector.90

At the other end of the spectrum, some governments may go out of their way to implement Basel II and III as part of a wider regulatory strategy of signalling to attract international investors into the financial services sector. When a country’s commitment to transparency is low and its reputation for enforcement of national regulations is poor, then investors have less, and less trustworthy, information on which to base their decisions.91 Implementing Basel and other international standards is a mechanism for signalling commitment to transparency and more generally upholding international best practice. Financial centres that are trying to gain size and market share may find that the reputational payoffs for compliance with international standards are comparatively high, particularly when they are trying to convince investors of the sophistication of their financial centres.92 Conversely regulators may deliberately opt against the adoption of Basel and other international standards if they thrive on secrecy and regulatory forbearance, to signal commitment to continuing this approach.93

(c) Financial infrastructure and financial market gaps

The third and final explanation we consider is that the shallow and selective implementation of Basel II and III is due to weaknesses in the wider financial infrastructure, particularly gaps in the availability of credit ratings and credit information, and the fact that some elements of Basel II and III have little relevance in countries where capital markets are in their infancy.

Credit rating agencies play a central role in the Basel II framework, a role that has been widely criticized since the financial crisis, but persists nonetheless. However, many countries outside the BCBS do not have national ratings agencies and the penetration of global ratings agencies is limited to the largest corporations.94 The development of a local credit ratings industry is not straightforward—it requires, inter alia, a reporting and corporate governance framework for companies, strong accounting and external auditing rules, the existence of credit bureaus, as well as the collection and sharing of borrowers’ data.95 Where credit ratings are not available the standardized approach can still be used for assessing credit risk, but the risk weights applied to bank assets are very similar to Basel I, undermining the incentive for national supervisors to move from Basel I to Basel II.

The absence of external credit ratings may also impede implementation of the internal model-based approaches to assessing credit risk under Basel II. Although banks use their own internal models to generate credit ratings under these approaches, supervisors need to validate these models and they commonly benchmark the ratings generated by banks against those generated by external ratings agencies to do so. Where the market or external rating is shallow, validation becomes harder.

High quality data from credit reporting institutions, particularly credit registries, is particularly useful for implementing the macro-prudential components of Basel III. Although regulators can obtain information from individual financial institutions, credit registries enable regulators to obtain a more comprehensive picture of inter-connected risks in the financial sector because they typically contain information on all loans above a particular threshold made by regulated institutions. Credit registry data can provide the basis for evaluating the systemic importance of financial institutions, thereby informing D-SIB calculations, and assist supervisors to make decisions on the countercyclical buffer decisions, by increasing the accuracy of risk weighting in banks’ loan portfolios.96 A paucity of credit information may thus impede the implementation of macro-prudential standards.

Supervisors in countries with nascent capital markets may decide that specific components of Basel II and III are less relevant for their jurisdictions. Pillar 3 of Basel II aims to complement the other two Pillars by encouraging market discipline as a ‘counterweight’ to the increased discretion accorded to banks in the estimation of their own capital requirements. However, it is only likely to be useful in countries where banks are publicly listed and capital markets are sufficiently deep and liquid for the market to act as a source of discipline.97 Similarly, standards for counterparty credit risk will have little immediate impact where capital markets are thin, because bank activity in derivatives, repurchase agreements, and securities financing will be limited.

4. INSIGHTS FROM REGRESSION ANALYSIS

We estimate a number of OLS and probit models to probe the plausibility of our explanations. Given the small sample size and the high correlation between the covariates of interest, we choose to estimate simple regressions that nonetheless offer proofs of concept for our explanation of the variation in Basel adoption.

(a) Data description

Our data on the adoption of the Basel standards has largely been coded from surveys published by the Financial Stability Institute, which has surveyed the extent and date of Basel adoption in jurisdictions outside of the BCBS every year since 2012. To augment this, we gathered additional data on the level of Basel II adoption in jurisdictions that joined the BCBS in 2009. We code a country’s adoption of each component of Basel II and III and then combine this into a single index for each Basel II and III, encompassing the 10 components of Basel II and eight components of Basel III.98

For our analysis of Basel II, we use a cross-section of data on the extent of Basel II adoption in 2008, the year when the universe of standard takers was the largest, before the expansion of the BCBS in 2009. In 2008, the mean level of Basel II adoption among the 115 standard takers for which we have data was 2.11. In our regressions investigating the adoption of Basel III, we use data from the most recent available year, 2015. In that year, the mean level of adoption among the 100 standard takers in the dataset was 1.34 components. To probe specific explanations for particular components of the Basel standards we also include a few regressions with a binary dependent variable of the adoption of individual elements of the standard.

(b) Explanatory variables

We model the variation in Basel II and III adoption in line with the three explanations outlined: banking sector politics; alignment with supervisory capacity, legal power and regulatory approaches, and financial infrastructure and financial market gaps. We use the following measures to capture variation in standard-taking countries across these three explanations.

(i) Banking sector politics

To explore the expectation that Basel II and III adoption is determined by the adjustment costs faced by banks, we use data on the actual riskadjusted and non-riskadjusted capital ratio in the banking sector taken from Barth and others’ Bank Regulation and Supervision Dataset (2013).99 If adoption is in fact shaped by adjustment costs, then we ought to see a positive relationship between the actual capital ratio and the extent of Basel II and III adoption. However, as we explain above, we do not expect the level of capitalization to be the main impediment to Basel adoption, and thus predict a null finding.

To get at the distributive politics of banking regulation, we include four covariates. First, we test for the effect of banking sector concentration, measured as the assets held by the three largest commercial banks as a share of all banking assets and taken from the Global Financial Development Database. Secondly, we include an indicator of foreign bank presence, which is measured in terms of the percentage of a jurisdiction’s banking assets that are held by foreign banks and taken from Claessens and van Horen’s dataset on cross-border banking.100 Thirdly, we control for whether there are banks headquartered domestically that operate abroad, banks abroad, an indicator we recode from Claessens and van Horen’s dataset. We expect both indicators of banking sector internationalization to be positively correlated with the extent of Basel adoption. Fourthly, we include a measure of the number of government owned banks, taken from Barth and others’ Bank Regulation and Supervision survey. As a robustness check, we control for whether a jurisdiction has experienced a recent systemic banking crisis, using Laeven and Valencia’s (2012) dataset.101

(ii) Alignment with supervisory capacity, legal powers and regulatory approach

As we outline above, implementation of Basel II and III requires significant institutional capacity. To test for this, we first use the regulatory quality index taken from the World Bank’s World Governance Indicators as a measure of the government’s overall regulatory capacity. This index amalgamates perceptions of regulatory quality from different sources, including firm surveys and NGO assessments, and ranges from −2.5 to 2.5. We expect that jurisdictions evaluated as having better overall regulatory quality will adopt more of Basel II and III. For a more specific evaluation of the effect of the resources available to banking supervisors, we use data from Barth and others’ Bank Regulation and Supervision dataset to calculate the number of supervisors per bank, expecting that jurisdictions with more human resources will be better able to implement the complex elements of Basel II and III. We also draw from Barth and others’ dataset for the supervisory power index, which amalgamates responses to numerous survey questions about the tools available to banking supervisors to prevent and correct problems, and ranges from 0 to 16.5. As a robustness check, we test for the effect of corruption, using Transparency International’s corruption perception index.

The Basel standards also reflect a particular policy orientation. We, therefore, expect that adoption of the standards depends on their alignment with prevailing regulatory practices. We use several proxies to capture a jurisdiction’s regulatory approach, all from Barth and others’ Bank Regulation and Supervision dataset. First, the capital stringency index measures the responsiveness of capital requirements to credit risk, and ranges from 0 to 7. It includes whether jurisdictions use risk weighting in line with the Basel I guidelines.102 We expect jurisdictions with higher pre-existing capital stringency will be more aligned with the Basel standards, and therefore will implement them to a greater extent. Secondly, we include a binary indicator of accounting practices, which is equal to 1 if a jurisdiction uses either the International Financial Reporting Standards (IFRS) or the US Generally Accepted Accounting Principles (GAAP). The use of international accounting practices not only eases the introduction of the Basel capital requirements, but also reflects the convergence of a jurisdiction’s regulatory practices with international expectations. We expect jurisdictions that have adopted the accounting standards to adopt more of Basel II and III.

The Basel standards reflect an expectation that market actors will monitor banks’ behaviour. We use the measure private monitoring index to capture whether this aligns with a jurisdiction’s approach to regulation. This indicator ranges from 0 to 12, with higher values reflecting more private oversight. Finally, as a robustness check, we control for the external governance index, which is an overall indicator of the use of external standards and private bodies in the monitoring and oversight of the financial sector in a jurisdiction. It ranges from 0 to 19.

(iii) Financial infrastructure and financial market gaps

We expect the extent of Basel II and III adoption to vary with the appropriateness of the standard for the jurisdiction in question. We, therefore, include a number of measures intended to capture the development of domestic financial infrastructure and financial markets. We include financial sector depth, measured as the amount of credit provided to the private sector as a percentage of GDP, the commonly used indicator of the size of a financial sector.103 We expect that economies with deeper financial sectors will be more likely to adopt more of Basel II and III. We also control for market capitalization, which measures the capitalization of publicly listed companies as a percentage of GDP and is taken from the World Bank.

To account for the fact that both Basel II and III rely on data availability for risk calculations, particularly of credit risk, we include two proxies of the extent and quality of credit information available within a jurisdiction: the depth of information index and private credit bureau coverage. The first is a World Bank index of the depth of credit information, ranging from 0 to 8.104 However, there is risk of reverse causality in using this measure, since it is possible that a deepening of available credit information is a consequence of adoption of the Basel standards, rather than a pre-existing feature of the economy. Therefore, we also use a second indicator, private credit bureau coverage, which is taken from the World Bank and measures the percentage of the adult population whose credit information is documented by a private credit bureau. For both of these, we expect that jurisdictions with more credit information available will adopt more of Basel II and III.

(iv)Methodology

For our cross-sectional analysis of the extent of Basel II adoption in 2008 and the extent of Basel III adoption in 2015, we use OLS regressions with robust standard errors. To model the adoption of specific components of the Basel standards, we use probit regressions with robust standard errors. Covariates are lagged to avoid simultaneity bias, with most covariates averaged over the preceding three or five years.105 In models of Basel III adoption, we control for the level of Basel II adoption to account for path dependence. Among our sample of non-members of the BCBS, approximately 70 per cent are upper middle-income, lower middle-income, or low-income countries for which the data coverage on key covariates is often very limited.106 To maintain sample sizes and statistical power, we therefore choose to include each of the key covariates in turn, rather than in a large multivariate regression.107 We control for financial sector depth in all of our models, since this is the most reliable predictor of adoption.

(v) Results

Tables 1 and 2 below show the results of our models of Basel II and III adoption. To summarize, we consistently find that financial sector depth and other measures of financial infrastructure and financial market development predict the extent of Basel II and III adoption. We also find evidence that the internationalization of the banking sector and alignment with regulatory quality and approach matter for the extent of Basel II and III adoption. As expected, we find no relationship between the extent of adoption and the level of capitalization in the banking sector.

OLS models of extent of Basel II Adoption by non-members of the Basel Committee, 2008

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Financial sector depth | 0.05*** | 0.06*** | 0.04*** | 0.05*** | 0.03*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.04*** | 0.04*** | 0.05*** |

| (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | |

| Risk adjusted capital ratio | −2.91 | |||||||||||||

| (5.98) | ||||||||||||||

| Non–risk adjusted capital ratio | 2.25 | |||||||||||||

| (3.93) | ||||||||||||||

| Banking sector concentration | 0.02 | 0.03** | ||||||||||||

| (0.02) | (0.02) | |||||||||||||

| Foreign bank presence | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Banks abroad | 1.15* | |||||||||||||

| (0.63) | ||||||||||||||

| Number of government-owned banks | −0.01 | |||||||||||||

| (0.01) | ||||||||||||||

| Regulatory quality index | 1.42** | |||||||||||||

| (0.58) | ||||||||||||||

| Number of supervisors per bank | 0.03 | |||||||||||||

| (0.06) | ||||||||||||||

| Supervisory power index | 0.07 | |||||||||||||

| (0.09) | ||||||||||||||

| Capital stringency index | 0.24 | |||||||||||||

| (0.19) | ||||||||||||||

| Accounting practices | −0.02 | |||||||||||||

| (0.95) | ||||||||||||||

| Private monitoring index | 0.46*** | |||||||||||||

| (0.17) | ||||||||||||||

| External governance index | 0.10 | |||||||||||||

| (0.11) | ||||||||||||||

| Market capitalization | 0.01** | |||||||||||||

| (0.00) | ||||||||||||||

| Depth of information index | 0.14** | |||||||||||||

| (0.07) | ||||||||||||||

| Private credit bureau coverage | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Constant | 0.24 | −2.04* | −2.87** | 0.01 | 0.60 | −0.50 | −1.14 | −1.02 | −3.74** | −1.91 | −0.28 | 0.26 | −0.75** | −0.54* |

| (1.65) | (1.02) | (1.31) | (0.42) | (0.48) | (0.39) | (1.11) | (1.15) | (1.42) | (1.29) | (0.30) | (0.71) | (0.33) | (0.29) | |

| Observations | 66 | 59 | 80 | 86 | 87 | 82 | 88 | 77 | 80 | 36 | 98 | 49 | 88 | 79 |

| R2 | 0.36 | 0.36 | 0.31 | 0.38 | 0.43 | 0.43 | 0.37 | 0.40 | 0.40 | 0.35 | 0.36 | 0.31 | 0.39 | 0.50 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Financial sector depth | 0.05*** | 0.06*** | 0.04*** | 0.05*** | 0.03*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.04*** | 0.04*** | 0.05*** |

| (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | |

| Risk adjusted capital ratio | −2.91 | |||||||||||||

| (5.98) | ||||||||||||||

| Non–risk adjusted capital ratio | 2.25 | |||||||||||||

| (3.93) | ||||||||||||||

| Banking sector concentration | 0.02 | 0.03** | ||||||||||||

| (0.02) | (0.02) | |||||||||||||

| Foreign bank presence | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Banks abroad | 1.15* | |||||||||||||

| (0.63) | ||||||||||||||

| Number of government-owned banks | −0.01 | |||||||||||||

| (0.01) | ||||||||||||||

| Regulatory quality index | 1.42** | |||||||||||||

| (0.58) | ||||||||||||||

| Number of supervisors per bank | 0.03 | |||||||||||||

| (0.06) | ||||||||||||||

| Supervisory power index | 0.07 | |||||||||||||

| (0.09) | ||||||||||||||

| Capital stringency index | 0.24 | |||||||||||||

| (0.19) | ||||||||||||||

| Accounting practices | −0.02 | |||||||||||||

| (0.95) | ||||||||||||||

| Private monitoring index | 0.46*** | |||||||||||||

| (0.17) | ||||||||||||||

| External governance index | 0.10 | |||||||||||||

| (0.11) | ||||||||||||||

| Market capitalization | 0.01** | |||||||||||||

| (0.00) | ||||||||||||||

| Depth of information index | 0.14** | |||||||||||||

| (0.07) | ||||||||||||||

| Private credit bureau coverage | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Constant | 0.24 | −2.04* | −2.87** | 0.01 | 0.60 | −0.50 | −1.14 | −1.02 | −3.74** | −1.91 | −0.28 | 0.26 | −0.75** | −0.54* |

| (1.65) | (1.02) | (1.31) | (0.42) | (0.48) | (0.39) | (1.11) | (1.15) | (1.42) | (1.29) | (0.30) | (0.71) | (0.33) | (0.29) | |

| Observations | 66 | 59 | 80 | 86 | 87 | 82 | 88 | 77 | 80 | 36 | 98 | 49 | 88 | 79 |

| R2 | 0.36 | 0.36 | 0.31 | 0.38 | 0.43 | 0.43 | 0.37 | 0.40 | 0.40 | 0.35 | 0.36 | 0.31 | 0.39 | 0.50 |

Robust standard errors in parentheses.

p < 0.01,

p < 0.05,

p < 0.1

OLS models of extent of Basel II Adoption by non-members of the Basel Committee, 2008

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Financial sector depth | 0.05*** | 0.06*** | 0.04*** | 0.05*** | 0.03*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.04*** | 0.04*** | 0.05*** |

| (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | |

| Risk adjusted capital ratio | −2.91 | |||||||||||||

| (5.98) | ||||||||||||||

| Non–risk adjusted capital ratio | 2.25 | |||||||||||||

| (3.93) | ||||||||||||||

| Banking sector concentration | 0.02 | 0.03** | ||||||||||||

| (0.02) | (0.02) | |||||||||||||

| Foreign bank presence | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Banks abroad | 1.15* | |||||||||||||

| (0.63) | ||||||||||||||

| Number of government-owned banks | −0.01 | |||||||||||||

| (0.01) | ||||||||||||||

| Regulatory quality index | 1.42** | |||||||||||||

| (0.58) | ||||||||||||||

| Number of supervisors per bank | 0.03 | |||||||||||||

| (0.06) | ||||||||||||||

| Supervisory power index | 0.07 | |||||||||||||

| (0.09) | ||||||||||||||

| Capital stringency index | 0.24 | |||||||||||||

| (0.19) | ||||||||||||||

| Accounting practices | −0.02 | |||||||||||||

| (0.95) | ||||||||||||||

| Private monitoring index | 0.46*** | |||||||||||||

| (0.17) | ||||||||||||||

| External governance index | 0.10 | |||||||||||||

| (0.11) | ||||||||||||||

| Market capitalization | 0.01** | |||||||||||||

| (0.00) | ||||||||||||||

| Depth of information index | 0.14** | |||||||||||||

| (0.07) | ||||||||||||||

| Private credit bureau coverage | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Constant | 0.24 | −2.04* | −2.87** | 0.01 | 0.60 | −0.50 | −1.14 | −1.02 | −3.74** | −1.91 | −0.28 | 0.26 | −0.75** | −0.54* |

| (1.65) | (1.02) | (1.31) | (0.42) | (0.48) | (0.39) | (1.11) | (1.15) | (1.42) | (1.29) | (0.30) | (0.71) | (0.33) | (0.29) | |

| Observations | 66 | 59 | 80 | 86 | 87 | 82 | 88 | 77 | 80 | 36 | 98 | 49 | 88 | 79 |

| R2 | 0.36 | 0.36 | 0.31 | 0.38 | 0.43 | 0.43 | 0.37 | 0.40 | 0.40 | 0.35 | 0.36 | 0.31 | 0.39 | 0.50 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Financial sector depth | 0.05*** | 0.06*** | 0.04*** | 0.05*** | 0.03*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.05*** | 0.04*** | 0.04*** | 0.05*** |

| (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | |

| Risk adjusted capital ratio | −2.91 | |||||||||||||

| (5.98) | ||||||||||||||

| Non–risk adjusted capital ratio | 2.25 | |||||||||||||

| (3.93) | ||||||||||||||

| Banking sector concentration | 0.02 | 0.03** | ||||||||||||

| (0.02) | (0.02) | |||||||||||||

| Foreign bank presence | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Banks abroad | 1.15* | |||||||||||||

| (0.63) | ||||||||||||||

| Number of government-owned banks | −0.01 | |||||||||||||

| (0.01) | ||||||||||||||

| Regulatory quality index | 1.42** | |||||||||||||

| (0.58) | ||||||||||||||

| Number of supervisors per bank | 0.03 | |||||||||||||

| (0.06) | ||||||||||||||

| Supervisory power index | 0.07 | |||||||||||||

| (0.09) | ||||||||||||||

| Capital stringency index | 0.24 | |||||||||||||

| (0.19) | ||||||||||||||

| Accounting practices | −0.02 | |||||||||||||

| (0.95) | ||||||||||||||

| Private monitoring index | 0.46*** | |||||||||||||

| (0.17) | ||||||||||||||

| External governance index | 0.10 | |||||||||||||

| (0.11) | ||||||||||||||

| Market capitalization | 0.01** | |||||||||||||

| (0.00) | ||||||||||||||

| Depth of information index | 0.14** | |||||||||||||

| (0.07) | ||||||||||||||

| Private credit bureau coverage | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Constant | 0.24 | −2.04* | −2.87** | 0.01 | 0.60 | −0.50 | −1.14 | −1.02 | −3.74** | −1.91 | −0.28 | 0.26 | −0.75** | −0.54* |

| (1.65) | (1.02) | (1.31) | (0.42) | (0.48) | (0.39) | (1.11) | (1.15) | (1.42) | (1.29) | (0.30) | (0.71) | (0.33) | (0.29) | |

| Observations | 66 | 59 | 80 | 86 | 87 | 82 | 88 | 77 | 80 | 36 | 98 | 49 | 88 | 79 |

| R2 | 0.36 | 0.36 | 0.31 | 0.38 | 0.43 | 0.43 | 0.37 | 0.40 | 0.40 | 0.35 | 0.36 | 0.31 | 0.39 | 0.50 |

Robust standard errors in parentheses.

p < 0.01,

p < 0.05,

p < 0.1

OLS models of extent of Basel III Adoption by non-members of the Basel Committee, 2015

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Basel II adoption | 0.38*** | 0.30*** | 0.31*** | 0.33*** | 0.32*** | 0.31*** | 0.32*** | 0.34*** | 0.29*** | 0.32*** | 0.33*** | 0.33*** | 0.31*** | 0.30*** |

| (0.06) | (0.06) | (0.06) | (0.05) | (0.05) | (0.06) | (0.05) | (0.05) | (0.06) | (0.06) | (0.05) | (0.08) | (0.05) | (0.06) | |

| Financial sector depth | 0.01 | 0.01* | 0.01* | 0.01** | 0.01 | 0.01** | 0.01** | 0.01*** | 0.01** | 0.01** | 0.01** | 0.02** | 0.01** | 0.01** |

| (0.01) | (0.01) | (0.01) | (0.01) | (0.00) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.00) | (0.01) | (0.01) | (0.00) | |

| Risk adjusted capital ratio | −1.25 | |||||||||||||

| (2.10) | ||||||||||||||

| Non-risk adjusted capital ratio | 0.91 | |||||||||||||

| (1.62) | ||||||||||||||

| Banking sector concentration | 0.01 | 0.02* | ||||||||||||

| (0.01) | (0.01) | |||||||||||||

| Foreign bank presence | −0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Banks abroad | 0.76** | |||||||||||||

| (0.36) | ||||||||||||||

| Number of government owned banks | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Regulatory quality index | 0.37 | |||||||||||||

| (0.29) | ||||||||||||||

| Number of supervisors per bank | 0.03 | |||||||||||||

| (0.04) | ||||||||||||||

| Supervisory power index | −0.05 | |||||||||||||

| (0.06) | ||||||||||||||

| Capital stringency index | 0.26*** | |||||||||||||

| (0.09) | ||||||||||||||

| Accounting practices | 0.09 | |||||||||||||

| (0.31) | ||||||||||||||

| Private monitoring index | 0.16* | |||||||||||||

| (0.10) | ||||||||||||||

| External governance index | 0.05 | |||||||||||||

| (0.08) | ||||||||||||||

| Market capitalization | −0.01 | |||||||||||||

| (0.01) | ||||||||||||||

| Depth of information index | 0.04 | |||||||||||||

| (0.05) | ||||||||||||||

| Private credit bureau coverage | 0.00 | |||||||||||||

| (0.01) | ||||||||||||||

| Constant | −0.14 | −1.08 | −1.60** | −0.43* | −0.14 | −0.53* | 0.15 | −1.86*** | −1.59** | −1.20 | −0.30 | −0.55 | −0.48* | −0.32 |

| (0.58) | (0.73) | (0.70) | (0.23) | (0.29) | (0.30) | (0.74) | (0.54) | (0.74) | (1.14) | (0.22) | (0.51) | (0.26) | (0.24) | |

| Observations | 55 | 52 | 65 | 74 | 76 | 74 | 76 | 71 | 75 | 53 | 86 | 28 | 74 | 79 |

| R2 | 0.54 | 0.50 | 0.52 | 0.46 | 0.46 | 0.46 | 0.45 | 0.49 | 0.46 | 0.51 | 0.45 | 0.47 | 0.45 | 0.44 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Basel II adoption | 0.38*** | 0.30*** | 0.31*** | 0.33*** | 0.32*** | 0.31*** | 0.32*** | 0.34*** | 0.29*** | 0.32*** | 0.33*** | 0.33*** | 0.31*** | 0.30*** |

| (0.06) | (0.06) | (0.06) | (0.05) | (0.05) | (0.06) | (0.05) | (0.05) | (0.06) | (0.06) | (0.05) | (0.08) | (0.05) | (0.06) | |

| Financial sector depth | 0.01 | 0.01* | 0.01* | 0.01** | 0.01 | 0.01** | 0.01** | 0.01*** | 0.01** | 0.01** | 0.01** | 0.02** | 0.01** | 0.01** |

| (0.01) | (0.01) | (0.01) | (0.01) | (0.00) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.00) | (0.01) | (0.01) | (0.00) | |

| Risk adjusted capital ratio | −1.25 | |||||||||||||

| (2.10) | ||||||||||||||

| Non-risk adjusted capital ratio | 0.91 | |||||||||||||

| (1.62) | ||||||||||||||

| Banking sector concentration | 0.01 | 0.02* | ||||||||||||