ABSTRACT

Despite the significance of repurchase agreements (repos) in market-based finance, European repo markets remain underexplored. Drawing on monetary hierarchy literature, we make three conceptual arguments. First, we argue that repos’ balance sheet mechanics differ depending on the counterparties’ relative hierarchical position. Vertical repos across hierarchical levels imply money creation; horizontal repos lend on pre-existing money. Second, we conceptualize the ‘inherently ambiguous’ whereabouts of the security used as repo collateral: it becomes the lender’s off-balance-sheet asset, paired with a liability to return it, while the Basel III regulations treat it as ‘encumbered’ on the borrower’s balance sheet. Third, we propose an on-balance-sheet notation of collateral frameworks that illustrates their function as a central bank policy tool which influences central counterparties’ general collateral baskets. Empirically, we study vertical repos of the Eurosystem and horizontal repos in European interbank markets with regard to their institutional evolution and principal role in the Eurocrisis. We show that in case of Eurosystem repos, the ‘inherent ambiguity’ helps conceal the security and enable sovereign debt funding compliant with the ‘monetary financing prohibition’. In case of interbank repos, the ‘inherent ambiguity’ facilitates the security’s effective bilocation as it gets simultaneously treated as the borrower’s encumbered asset and as disposable for the lender’s re-use.

I. INTRODUCTION

During World War I, a new financial instrument became fashionable for the Federal Reserve (Fed) to conduct its monetary policy operations: repurchase agreements or ‘repos’.1 The US central bank had been founded just before the war, after years of struggle between different political fractions about its design.2 The Federal Reserve Act of 1913 provided the Fed with a mandate to conduct monetary policy primarily by discounting short-term commercial paper, thus applying the traditional ‘real bills doctrine’,3 and only exceptionally with some forms of short-term government debt. The only legitimate counterparties were member banks, ie commercial banks that had become members of one of the Fed’s district central banks.4 Repos were a convenient way to circumvent these restrictions and extend the set of both eligible counterparties and eligible securities to receive central bank credit. Originally used to avoid a stamp tax on advances on promissory notes of member banks, the Fed harnessed repos to support the war finance activities of the US government after it had entered World War I in 1917.5 Organized as a sale and repurchase of a security, repos did not legally appear to be a lending operation regulated by the Federal Reserve Act. Hence, they allowed the Federal Reserve Bank of New York (FRBNY) to put significant shares of Liberty bonds, issued by the US Treasury as long-term debt to raise funds for the war, onto its balance sheet without discriminating between member and non-member banks.6 The Fed’s legal counsel argued that these transactions were not sales, as they pretended to be, but in fact secured loans and therefore ultra vires, ie beyond the scope of the Fed’s powers, but these reservations were brushed aside.7 In retrospect, repos proved to be a successful way to facilitate unprecedented financial expansion of central bank and treasury balance sheets because they have an inherent ambiguity about whether or not they involve credit creation—both of central bank money and a repo IOU (debt certificate, as in I owe you)—and conceal what happens with the security that is ‘allegedly’ being sold.8

Today, repos have become a key instrument in the world of globalized finance and are widely used by both central banks and private institutions. Since the 1950s, repos have been employed in US money markets to circumvent New Deal banking regulations, fostering what now is called the ‘shadow banking system’ or ‘market-based finance’.9 Even though rulings of common law courts and regulatory changes have at different times attempted to provide more clarification about the nature of repos,10 they remain an inherently ambiguous instrument that the literature in law and political economy sometimes refers to as a form of ‘shadow money’.11 In the present setting, repos are particularly attractive to market participants due to their special treatment under bankruptcy law.12 It is widely recognized that contractions in the repo market lay at the heart of the 2007–9 Global Financial Crisis (GFC).13 Some even perceived repos as the instrument that elevated a real estate crisis and the bursting of a mortgage securitization scheme to global proportions.14 After all, the part of Lehman Brothers that went bankrupt was the bank’s repo dealer, which had confused customers, regulators, and eventually itself about the volume of repos outstanding and the whereabouts of the repo collateral.15

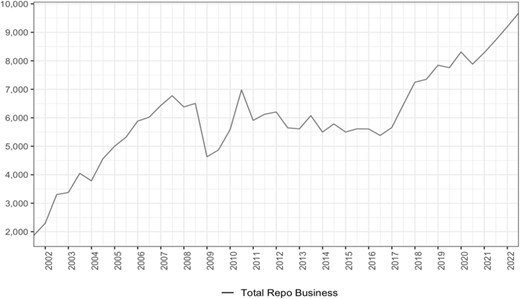

Less widely studied—both conceptually and empirically—are repos in Europe which have many similarities but also important differences to those in the US.16 Conceptually, there is a common tendency in the limited volume of literature on European repos not to systematically distinguish between repos used for the purpose of monetary policy implementation by the Eurosystem and those used between private financial market participants.17 Empirically, the macro-financial role of the European repo market in the 2009–12 Eurocrisis is still insufficiently explored. It is true that there have been in-depth quantitative analyses on the dynamics of European repo markets18 as well as pioneering work on the political economy of European repo regulation.19 Still, the actual crisis dynamics connected to European repo markets are insufficiently modelled. It is known that repos replaced unsecured interbank lending early on in the crisis and provided a channel for the spread of contagion through the European monetary and financial system during the looming default of Greece.20 However, there is no convincing explanation of how precisely it worked and why it happened. Repos were likely at the very heart of the crisis dynamics because they connect banking, shadow banking, and—via the sovereign debt securities posted as collateral—also fiscal balance sheets across countries. We believe that the underlying reason for this gap is connected to the fact that repos from the start had one paramount purpose: being ambiguous.

Balance sheet methodology—as developed, for example, by the Money View21 and the (critical) macro-finance literature22—has the potential to provide clarification about repos’ ambiguity and inform the literature on law and macro-finance interested in questions of financial regulation.23 While money creation is notoriously difficult to conceptualize,24 balance sheet methodology offers the appropriate analytical categories that are ‘true’ for the nature of the object of analysis.25 It acknowledges that the rules of double-entry book-keeping, according to which an instrument always must simultaneously exist as an asset and a liability on two balance sheets, do not just represent reality, they create reality. Thus, the shift towards analysing webs of interlocking balance sheets after the GFC was a quantum leap in new economic thinking.26 As repos connect the balance sheets of central banks, commercial banks, and non-bank financial institutions while typically using sovereign debt securities as collateral, they uniquely bridge all segments of the ‘monetary architecture’.27 This makes repos a quintessential use case for balance sheet methodology.

However, we believe that there are three conceptual issues related to balance sheet methodology that hinder a satisfactory analysis of repos in a European context and also impede the application of balance sheet methodology for debates on financial regulation.

First, there are open questions regarding the extent to which repos involve the creation of credit as well as credit money. If repos are more than a ‘credit-less’ sale and repurchase of a security (as their name may be misleadingly taken to insinuate28 and as the FRBNY insisted in 1917), in which way exactly do they expand the liability sides on the balance sheets of the counterparties involved? This applies both to the creation of the repo IOU, which we may or may not classify as ‘shadow money’, and the potentially associated creation of ‘standard’ forms of money such as central bank reserves or bank deposits.29 For instance, some attempts to make sense of repos on-balance-sheet involve a symmetric expansion of both counterparties’ balance sheets with a ‘repo’ against reserves,30 an ‘overnight repo’ against a ‘term repo’,31 or both,32 whereas others perceive the repo issuance as expanding only one of the counterparties’ balance sheet33 or as being balance sheet neutral.34 Alternative analyses of repos that make money creation analogies but do not explicitly use balance sheet visualizations argue on the basis of loanable funds theory35 or use concepts of fractional reserve banking theory such as the money multiplier.36

Second, there is presently no entirely satisfactory on-balance-sheet depiction of the repo mechanism that clarifies the whereabouts of the security used as collateral during the maturity period of the repo. This, however, would be crucial from the perspective of financial regulation. Many representations that emphasize the credit character of the repo transaction abstract from the security altogether,37 whilst others seek to integrate the security by abstracting from the repo IOU.38 Daniel Neilson comes closest to a full picture, but in his depiction the repo collateral seems to be simply held on the balance sheet of the repo lender, which cannot be the entire story.39 From our perspective, the lack of clarity on where the security is during the maturity period of the repo is the most important factor of what we perceive as repos’ inherent ambiguity.

Third, there is a conceptual gap in the literature that would allow the specific European context to be appropriately grasped, because repo analyses mostly refer to a US setting. From a ‘micro-financial’ view, it is not fully clear what the similarities and differences are between repos with the Eurosystem and interbank repos. Matters are further complicated by the fact that European countries have their own repo-related legacy structures and country-specific terminologies. A ‘macro-financial’ issue is how balance sheet methodology can clarify the systemic implications of the Eurosystem’s collateral framework and its function in providing a backstop to the European monetary architecture. While narrative accounts stress the importance of changing rules for collateral eligibility,40 there is not yet a solution for an on-balance-sheet representation of those mechanisms, which is in fact an important policy tool to affect the credit condition of the system.41

In this article, we propose a novel way to depict repos on-balance-sheet that remedies these issues. Drawing on the literature on monetary hierarchy,42 we make three conceptual arguments. First, we argue that the balance sheet mechanics of repos vary if the counterparties involved are located on different hierarchical levels (‘vertical repos’) or on the same hierarchical level (‘horizontal repos’). While the vertical repo mechanism implies money creation, the horizontal repo mechanism only lends on pre-existing money. Second, we provide a solution to coherently represent the whereabouts of the security posted as repo collateral during the repo’s maturity period. It is held as an off-balance-sheet position of the repo lender, combined with a liability to repay it. The Pillar 3 disclosure requirements of Basel III interpret this ambiguous status of the collateral as being ‘encumbered’ and not leaving the repo borrower’s balance sheet, but this provides only an imperfect regulatory fix. Third, we introduce an on-balance-sheet notation of the collateral framework as a means for the repo lender to alter the elasticity of the funding provided. In sum, we propose a notation style that allows to simultaneously depict the creation of a repo IOU, the creation or redistribution of hierarchically higher money, the whereabouts of the security used as collateral in a transactional balance sheet representation, and the collateral framework as a de facto policy tool for the repo lender in a static balance sheet representation.

To show the merits of our repo conceptualization, we apply it on the two most relevant cases for Europe’s monetary architecture and connect it with the publicly available data. On the one hand, vertical repos play a key role for monetary policy implementation of the Eurosystem. Our methodology clarifies that securities pledged as repo collateral are de facto off-balance-sheet positions of the national central banks. Moreover, the methodology allows depicting on-balance-sheet how the Eurosystem designed its collateral framework and changed it over time to affect the elasticity space on the balance sheets of both central banks and banks. On the other hand, horizontal repos are used for secured interbank borrowing and lending. Our methodology clarifies the balance sheet mechanics involved in both General Collateral and Special Collateral repos, whether carried out bilaterally or via a central counterparty (CCP). This allows us to show on-balance-sheet how CCPs have mimicked the transformation of the Eurosystem’s collateral framework and thus magnified the Eurosystem’s policy interventions to private repo markets.

We find that the inherent ambiguity of both vertical repos of the Eurosystem and horizontal repos between banks crucially shapes the contemporary European monetary architecture. Vertical repos facilitate the Eurosystem’s funding of sovereign debt despite the infamous ‘monetary financing prohibition’ because they conceal the security that banks pledge as collateral for central bank money creation. The inherent ambiguity here helps tweak the provisions of the Maastricht Treaty that are now found in article 123 of the Treaty on the Functioning of the European Union (TFEU). Horizontal repos, by contrast, facilitate the maintenance of a regulatory setting where the security used as collateral remains allegedly encumbered on the balance sheet of the repo borrower but simultaneously can be re-used by the repo lender in another repo transaction. The inherent ambiguity here helps create a bilocation of the security, exploiting inconsistencies between the Basel III regulation and the EU’s Directive on Financial Collateral Arrangements.

This assessment allows us to shed new light on the Eurocrisis and explain the role of repos in it. At its heart, the Eurocrisis was an implosion of the funding of sovereign debt securities via vertical and horizontal repos. For better or worse, the elasticity space on the ‘off-balance-sheet balance sheets’ of the repo lenders has become indispensable for funding sovereigns’ structural debt burden. Euro area Member States entered into a debt crisis when their sovereign debt securities stopped being eligible to tap this elasticity space. The eligibility depends on the collateral framework of the Eurosystem and the General Collateral baskets of CCPs, which were organized in a way that fostered the emergence of a self-fulling debt crisis. The failure to provide systemic funding for sovereign debt via vertical and horizontal repos was the main cause of the Eurocrisis, whose nature and origin continues to be misunderstood until the present day.

We contribute to several ongoing debates. Our conceptual arguments are relevant for scholars who work in the Money View or critical macro-finance frameworks and seek to carry out empirical analyses of repo markets worldwide. The distinction of vertical and horizontal repos clarifies under which conditions repo issuance coincides with the creation of ‘standard’ forms of money. The clarification that the collateral is held off-balance-sheet by the repo lender during the maturity period helps to explain repos’ inherent ambiguity and the ongoing struggles of regulators who now double down on the encumbrance concept.43 We hope that our proposed methodology can help advance more general debates on shadow banking, shadow money, and the wider institutional reality of market-based finance.44 Moreover, our empirical analysis contributes to studies of repos in Europe, both as a monetary policy tool and as a mechanism for secured interbank lending.45 We also speak to the literature on the implications of the Eurosystem’s collateral framework on the Eurocrisis.46 Our findings offer an entry point to reflect on the implications that the inherent ambiguity involved in repos may have for financial regulation. As Dan Awrey has argued, unveiling the real-world complexity of financial markets is required to provide a rational basis for improving financial regulation.47

The remainder of this article is organized as follows. Section II introduces our proposed balance sheet methodology to conceptualize vertical and horizontal repos. Section III applies this methodology to vertical repos as a monetary policy instrument in the Euro area, and section IV applies it to horizontal repos in the Euro area’s interbank market. Section V concludes.

II. BALANCE SHEET METHODOLOGY

1. Vertical and horizontal repos as different quadruple-entry-consistent operations

The literature on repos typically gives the impression that repos are one unitary category of financial instruments that can be put to use in different contexts—eg by central banks for monetary policy implementation;48 by banks for borrowing and lending on the secured interbank market;49 or by securities dealers for market making as part of the shadow banking daisy chain.50 In those instances, repos appear to be fundamentally the same type of instrument: the first leg of the repo transaction means the sale of a security while the counterparty borrows a form of money; the second leg is the reversal of this transaction when the security is returned and the money instrument is paid back.51

From our perspective, the view that there is only one type of repo misses out on important nuance. It is not wrong per se, but it conceals one important fact: that there are different types of balance sheet mechanisms to create repos. This nuance typically gets lost because the term ‘repo’ has a double meaning. It is both a type of instrument and a balance sheet mechanism to create such instruments. While there is only one type of repo instrument, there are two types of repo balance sheet mechanisms.

On the one hand, as instruments, repos appear simultaneously as IOUs on the asset and liability sides of the counterparties once a repo contract is concluded. In accounting terms, the ‘repo’ entry on the balance sheets refers to a ‘repo claim’ when on the asset side, and to a ‘repo liability’ when on the liability side. The repo claim is the temporary legal claim to the security posted as collateral, and not the security itself that appears on the asset side of the balance sheet. Similarly, a repo liability indicates the future promise to repurchase the legal ownership of the security posted as collateral at maturity.52

Note that a frequently-made distinction separates ‘repos’ and ‘reverse repos’, which may be taken to refer to different repo instruments. Yet, this distinction merely denotes a difference in perspective on who initiates the transaction and whether the motivation is to secure cash (‘repo’) or the security (‘reverse repo’).53 Both ‘repo’ and ‘reverse repo’ are in fact the same instrument, which appears simultaneously as a ‘repo claim’ on one balance sheet and as a ‘repo liability’ on another.

On the other hand, as a balance sheet mechanism, repos refer to the operation through which repo claims and repo liabilities are put into existence. The general shape of repos as a balance sheet mechanism varies with whether the counterparties are located on different hierarchical levels in the monetary architecture or whether they are on the same one.54 To help us distinguish both categories, we call the first balance sheet mechanism ‘vertical repo’ (as it crosses hierarchical layers) and the second one ‘horizontal repo’ (as it remains on the same hierarchical layer).

To substantiate our point that there are two balance sheet mechanisms which lead to the creation of repos, we mobilize the matrix of quadruple-entry-consistent financial transactions introduced by Daniel Neilson,55 depicted in Figure 1. The matrix offers a complete list of possible balance sheet operations between two counterparties that formally comply with the rules of double-entry book-keeping. This necessarily involves four booking entries of IOUs, two on each balance sheet, which are either additions or subtractions of instruments on the asset or liability side. The matrix is helpful to explore the appropriate notation style for repos as it introduces the formal criterion for quadruple-entry-consistency which informs our analysis and arguments. Importantly, for each individual balance sheet, the additions and subtractions must maintain the same length on both sides of the balance sheet. This gives rise to three options: a balance sheet expansion involves symmetric additions on both the asset and the liabilities side; a balance sheet contraction entails a symmetric subtraction on the sides of the balance sheet; and a balance sheet neutral transaction involves both an expansion and a contraction happening on the same side of a balance sheet, either the asset or the liability side. If we now look at the combination of both balance sheets involved, each of the 16 options will either correspond to net credit creation (if one balance sheet expands and the other one does not contract); to net credit destruction (if one balance sheet contracts and the other one does not expand); or to no change of net credit in the system (if both transactions are balance sheet neutral, or one expands and the other contracts).

Matrix of sixteen quadruple-entry-consistent financial transactions. Source: Daniel Neilson, ‘Quadruple-Entry Accounting’ (Soon Parted (blog), 2021) <https://www.soonparted.co/p/quadruple-entry.

The balance sheet mechanism to create repo instruments can either correspond to the operation that Neilson calls a ‘secured loan’ in the matrix, which involves an expansion of both balance sheets and could also be referred to as a ‘swap of IOUs’,56 or to ‘asset intermediation’, in which only one balance sheet expands while the other keeps the same length. Which of the two mechanisms applies depends on the relative position of both balance sheets vis-à-vis each other in the monetary hierarchy.57 The mechanism of a ‘secured loan’ (or ‘swap of IOUs’) sets in if one balance sheet is hierarchically higher than the other and thus corresponds to a ‘vertical repo’. The mechanism of ‘asset intermediation’ applies if both balance sheets are located on the same hierarchical level and are thus equivalent to a ‘horizontal repo’.

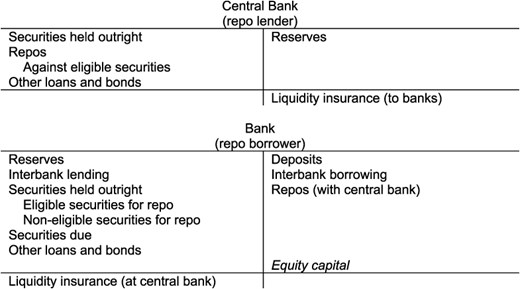

Figure 2 shows the balance sheet mechanism for the first leg of a vertical repo, when the counterparties are located on different hierarchical levels. This operation gets reversed with the second leg of the repo, which is not included in the figure. In this example, we choose a central bank and a bank as institutions and reserves as credit money instrument. Alternatively, we could also shift further down in the hierarchy and refer eg to a bank and a money market fund or a money-center and a peripheral bank as institutions and deposits as instruments. The hierarchically lower institution (‘repo borrower’) creates the repo as a liability that can be held as an asset on the balance sheet of the institution that is hierarchically higher (‘repo lender’). In return, the hierarchically higher institution creates an additional second liability that the hierarchically lower institution can treat as money.58

As the balance sheet mechanism of the vertical repo expands both balance sheets simultaneously, it coincides with the creation of new hierarchically higher money, here in the form of central bank reserves. By contrast, if the counterparties are located on the same level in the monetary hierarchy, the underlying balance sheet mechanism does not entail money creation, ie the issuance of a second liability in addition to the repo claim.

Vertical repos as new money creation.

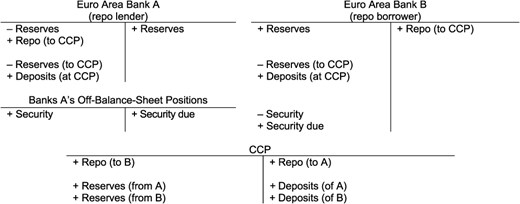

Figure 3 depicts the case of a horizontal repo, here in the form of securitized interbank lending. In this example, Bank B (‘repo borrower’) wants to borrow reserves from Bank A (‘repo lender’). To this end, Bank B issues a repo as a liability and transfers it to Bank A, which holds it as an asset. The operation will be reversed at maturity. As the balance sheet mechanism of a horizontal repo only involves a net expansion of one of the two balance sheets, the creation of the repo claim and the repo liability does not coincide with new money creation. Rather, the repo IOUs serve to lend out previously created money, here central bank reserves. The operation only implies an expansion of Bank B’s balance sheet, while Bank A replaces one asset in the form of reserves with another asset in the form of a repo IOU.

Horizontal repos as borrowing and lending pre-existing money.

In sum, the distinction between vertical and horizontal repos as two different quadruple-entry consistent balance sheet mechanisms helps clarify the question of whether the issuance of a repo corresponds to new money creation—it depends on the relative position of the counterparties within the hierarchy of money. Both vertical and horizontal repos formally imply net credit creation, but only if both balance sheets expand it is possible to refer to it as money creation following the logic of a swap of IOUs.

2. Collateral transfer in a second-quadruple-entry-consistent operation

The proposed depiction of vertical and horizontal repos still abstracts from the security that is used as collateral. This notation style does not clarify the difference between repo as collateralized lending in contrast to non-collateralized lending, and it does not provide an answer to the question of where the collateral is during the maturity of a repo.

Prima facie, as it seems to be the defining feature of a repo to be a sale and repurchase of a security, it could be natural to think of a repo transaction as an ‘asset swap’ (cf Figure 1) at t=0 and the reversal of the asset swap at t=1. Figure 4 visualizes this hypothetical case in which the asset is transferred from one balance sheet to another. The repo borrower (Counterparty B) passes on a security to the repo lender (Counterparty A) in exchange for reserves, and the transaction is reversed at maturity.

The depiction in Figure 4 would be the most literal on-balance-sheet representation of the repo mechanism in a way that abstracts entirely from any credit creation and conceals that it is a lending operation. It corresponds to the legal treatment of repos in the Euro area where they are considered an outright sale of a security with a full transfer of ownership (‘title transfer’)59—unlike in the US where the repo is treated as collateralized lending without full ‘title transfer’.60 However, both in the Euro area and the US, the accounting treatment of repos differs from the legal treatment.61 Repos are seen as a lending operation that clearly involves credit creation. How can we bring together the legal and accounting treatment with balance sheet methodology and align the aspect of credit creation in a repo with the exchange of the security used as collateral?

Repo imagined as asset swap with security changing balance sheets.

We argue that the discrepancy of legal and accounting treatment can be reconciled by integrating a second quadruple-entry-consistent operation that traces the whereabouts of the security. Figures 5 and 6 depict this for both vertical and horizontal repos, which include a given Security X used as collateral. These figures now show the ‘full’ repo transaction in a way that combines the lending transaction with a depiction of the collateral transfer.

Vertical repo with an encumbered security as collateral.

Horizontal repo with an encumbered security as collateral.

This notation style of the second quadruple-entry consistent operation combines conceptual arguments on repo accounting brought forth by Daniel Neilson62 as well as Albert Banal-Estañol, Enrique Benito, Dmitry Khametshin, and Jianxing Wei in a Banco de España publication.63

On the one hand, we follow Daniel Neilson concerning the collateral transfer and credit creation in the second operation.64 Accordingly, the security shifts its place on the asset side of the repo borrower’s balance sheet from being held outright to being ‘due’, awaiting to be transferred back. On the repo lender’s side, a balance sheet expansion takes place. The security is booked on the asset side whilst it is ‘due’ as a liability, indicating the promise to return it upon maturity of the repo. Other than pretending that the repo is an asset swap, ie a true sale of the security (as presented in the hypothetical Figure 4), this operation stresses the credit character involved in the transfer of the security. Looking back at Figure 1, the second operation is a quadruple-entry consistent transaction that follows the scheme of ‘asset intermediation’ which thus involves net credit creation.

On the other hand, we follow the argument of Albert Banal-Estañol and others that the security must be held as an off-balance-sheet position of the repo lender.65 To comply with the rules of quadruple-entry-consistent accounting, it is necessary for the repo lender to have a corresponding entry to the repo borrower’s booking of ‘– Security X’ and ‘+ Security X due’. At the same time, the security cannot formally touch the repo lender’s balance sheet as this would be equivalent to an outright sale of the security. Therefore, we introduce an ‘off-balance-sheet balance sheet’ for the repo lender to allow for a complete representation of the repo transaction.

The proposed notation style in Figures 5 and 6 offers what has so far been missing in the literature on balance-sheet methodology for repos and what would be needed to help inform debates on financial regulation. It simultaneously conveys, first, how credit creation takes place in the form of a repo IOU and, second, whether another credit money instrument is created, depending on whether the balance sheet mechanism corresponds to a vertical or a horizontal repo. Third, it includes the security that is used as collateral and shows how it ends up as the repo lender’s off-balance-sheet asset while creating yet another implicit credit claim.

Interpreting the security as being temporarily held as an asset off-balance-sheet by the repo lender with a corresponding off-balance-sheet liability to return the security introduces quadruple-entry consistency as an indispensable criterion for a formally correct balance sheet depiction and seems to offer an answer to the question where the security is during the maturity period of the repo contract. At the same time, it is far from self-evident what it means in practice that the repo lender holds the security off-balance-sheet while the repo borrower maintains an on-balance-sheet claim to receive it back.

In our view, it is precisely this logical tension in the second-quadruple entry consistent operation—which typically receives less analytical attention in attempts to conceptualize repos—that is the origin of the mechanism’s inherent ambiguity. The pretense of a sale and repurchase, combined with the vagary of the involved credit operation, gives interpretative leeway to the counterparties regarding the whereabouts of the security used as collateral. Depending on context, this can be resolved in such a way that the security is with the repo lender, the repo borrower, with both, or in fact nowhere. This helps clarify why financial regulators have been consistently grappling with the repo regulation. Let us look at three examples for this.

First, consider the US war finance effort when the Fed supported the liberty bonds issuance in 1917. The inherent ambiguity of the repo mechanism made it possible for the Fed to accept the securities of non-member banks as collateral without having to let them formally touch its balance sheet, which was prohibited by the Federal Reserve Act. Repos complied with the letter of the law because by accepting them as repo collateral, the securities were held off-balance-sheet, not on-balance-sheet.66

Second, Kenneth Garbade gives a convincing example of how the inherent ambiguity of repos contributed to their success as a financial instrument on US private markets. In the 1970s and early 1980s, when the shadow banking system was just developing, it was never fully specified what happened to the security in the repo contract, ie whether it was an outright sale or a collateralized loan. Garbade quotes a repo dealer at the time:

We left [the characterization of a repo] purposely vague because doing so fit our needs. If a customer said, ‘I can’t do repo,’ we said, ‘OK, we will sell you securities and buy them back.’ If another customer said he could not buy securities, we said, ‘Fine, we will borrow money from you and give you collateral.’ It was all very convenient ...67

Hence, the inherent ambiguity regarding the whereabouts of the security and the credit creation involved was a feature that not just public actors but also private profit-oriented actors used to their advantage. It was part of their business model.

Third, the inherent ambiguity of repos is connected to what eventually led to the bankruptcy of Lehman Brothers. To hide the extent to which it was leveraged, Lehman used so-called ‘Repo 105’ and ‘Repo 108’ devices in their books. These accounted for its repo transactions as ‘sales’ (effectively as in our hypothetical Figure 4) and entirely dropped the credit nature of the transaction. This practice started in 2001 but was used much more extensively in 2007 and 2008 as the bank entered into financial strains.68 Repo 105 and 108 made use of a special clause in the Generally Accepted Accounting Practices, which allowed Lehman to book the repo transactions as a sale rather than a loan as long as it put up at least 102 per cent of the value of the loan in collateral.69 Hence, Lehman’s practice was to hide the whereabouts of the security by pretending that it had permanently left their balance sheet and that there was no obligation to buy it back. When this practice could no longer be maintained and the hidden credit positions re-appeared, Lehman’s bankruptcy set in.

Regulators have repeatedly sought to tackle the problem and reduce the inherent ambiguity of repos. For instance, after the bankruptcies of Drysdale Government Securities and Lombard-Wall in 1982, a court attempted to provide legal certainty about repos and properly define where the underlying securities were and who owned them. The bankruptcy court announced that repos would be treated as secured loans, not as outright transactions. This implied that the creditor’s right to liquidate the securities was now in principle subject to the ‘automatic stay’ of bankruptcy law. It was not well received by repo practitioners who saw their business model endangered. The solution found—heavily influenced by the lobbying of Federal Reserve Chairman Paul Volcker—was that repos were exempted from bankruptcy law. The exemption was passed into law via the Bankruptcy Amendments and Federal Judgeship Act of 1984.70

The latest change of repo regulation materialized after the Lehman bankruptcy—the introduction of ‘encumbrance’.71 In line with the introduction of the Basel III framework and its Pillar 3 disclosure requirements, the regulatory treatment now foresees that the security used as collateral in a repo transaction does not leave the balance sheet of the repo borrower.72 Instead, the asset swap on the repo borrower’s balance sheet is taken to mean that the security becomes ‘encumbered’ in a repo transaction.73

The EU implemented the Basel III framework by means of Directive 2013/36/EU5, the Capital Requirements Directive (CRD), and Regulation (EU) No 575/2013, the Capital Requirements Regulation (CRR). Article 100 of the CRR introduces reporting requirements on ‘repurchase agreements, securities lending and all forms of encumbrance of assets’.74 This framing conveys by implication that repo transactions involve encumbrance. Moreover, security encumbrance has been codified via the ECB guideline 2016/2249 on the legal framework for accounting and financial reporting in the European System of Central Banks (ECB/2016/34), where it is mentioned that the securities sold under repo agreements shall be treated as if the assets in question were still part of the portfolio from which they were sold.75

Further specifications of encumbrance are to be found in Annex XVII of Regulation (EU) No 680/2014 (ITS on Supervisory Reporting), which provides technical standards for Regulation (EU) No 575/2013.76 The Annex defines an asset as encumbered `if it has been pledged or if it is subject to any form of arrangement to secure, collateralise or credit enhance any transaction from which it cannot be freely withdrawn. […T]his definition is not based on an explicit legal definition, such as title transfer, but rather on economic principles, as the legal frameworks may differ in this respect across countries'.77

In addition, the Annex provides numerous ‘types of contracts being well covered by the definition’, among them ‘secured financing transactions, including repurchase contracts and agreements, securities lending and other forms of secured lending’. It refers to both ‘repo/matching repo’ and ‘central bank funding’, stating that similar reporting rules apply to it because ‘collateralised central bank funding is only a specific case of a collateralised deposit or a repo transaction in which the counterparty is a central bank’.78

In our view, the stipulation that the security used as collateral gets encumbered during the maturity period of the repo transaction is a new regulatory attempt to grasp the underlying balance sheet mechanics expressed in Figures 5 and 6. Even though the Capital Requirements Directive and Regulation do not portray ‘encumbrance’ as a fundamental regulatory innovation but merely as an update of reporting standards, they nevertheless generalize an interpretative norm for what happens with the collateral that previously has been used only occasionally by some financial institutions.79 As the Lehman bankruptcy made it urgent to provide a better definition of the whereabouts of the security during the maturity period of the repo, the new reporting standard seeks to mitigate the repetition of the ‘Repo 105’ and ‘Repo 108’ devices. The encumbrance logic is meant to provide an assessment of the liquidity position on the repo borrower’s balance sheet. Hence, it seeks to prevent that the accounting entry ‘– Security X’ is read as if the collateral leaves the balance sheet permanently while the ‘+ Security X due’ position gets dropped.

However, the introduction of encumbrance into regulation does not change anything fundamental about repos’ underlying balance sheet mechanics and the ambiguity that the second quadruple-entry consistent operation generates. On the one hand, the encumbrance formulation de-emphasizes that a title transfer of the security takes place to the repo lender. It is telling in this regard that Annex XVII of Regulation (EU) No 680/2014 refuses to give a clear legal definition of encumbrance that in any way could conflict with a title transfer taking place and only vaguely refers to ‘economic principles’ that are not further specified. On the other hand, the encumbrance definition does not reflect in any way that the repo lender receives an obligation to return the security, which is a form of credit creation. The International Capital Markets Association (ICMA), for instance, expresses its skepticism about this regulatory treatment in its repo FAQ when it describes the argument that repos encumber assets as ‘largely illusory’.80 Hence, we interpret the regulatory treatment of encumbrance as a temporary fix that will stay with us for some time until it is replaced by the next attempt to cope with repos’ inherent ambiguity.

In sum, our proposed notation style depicts consistently on-balance-sheet what happens with regard to the creation of the repo instruments, what the origin is of the hierarchically higher monetary instrument, and where the collateral is during the repo’s maturity period. Using balance sheet methodology to specify the on-balance-sheet position of all three instruments that are part of this operation makes the inherent ambiguity explicit that comes along with the ‘alleged sale’ of the security by the repo borrower and the off-balance-sheet nature of the transaction for the repo lender. This inherent ambiguity is often rationalized in the literature on financial regulation as a discrepancy of the legal and accounting treatment.81 The nature of the second quadruple-entry consistent operation opens the possibility for flexible interpretations according to which the collateral may be located on the balance sheet of the repo lender or the repo borrower, on neither, or even on both—depending on context.

III. The collateral framework on the repo lender’s balance sheet

While the on-balance-sheet representation of horizontal and vertical repos via two quadruple-entry-consistent financial transactions clarifies the whereabouts of the security posted as collateral during the maturity period, it does not give any information on the specific securities that are eligible to be used as collateral in the repo operation. The visualizations in Figure 5 and 6 are transactional balance sheets that focus on micro-level flows. From a macro-financial perspective, it is also of interest to be able to depict static balance sheets as stocks that indicate which specific securities can be used as collateral to acquire a credit money instrument via repos and thus be put on the ‘off-balance-sheet balance sheet’ of the repo lender.

Figure 7 presents a notation style for such a macro-financial stock perspective. Drawing on the ‘Monetary Architecture’ framework, it places ‘actual’ assets and liabilities on the upper part of the balance sheet and ‘contingent’ liabilities such as liquidity insurance on the lower part.82 Our example shows a central bank (‘repo lender’) and a bank (‘repo borrower’) that form a vertical repo relationship. The bank issues repos as its liability, which the central bank holds as an asset. We specify which securities are eligible for repo on the balance sheet of the central bank as it is ultimately the repo lender’s power to determine which securities to accept as collateral, even though the security does not formally touch the repo lender’s balance sheet. On the repo borrower’s balance sheet, we distinguish the securities held outright into those that are eligible for repos and those that are non-eligible. Moreover, we indicate securities that already are used as collateral in a repo transaction, which as to contemporary regulations are to be classified as encumbered and which could be recorded as off-balance-sheet positions of the central bank.

Determining collateral eligibility via the repo lender’s balance sheet.

The depiction in Figure 7 shows how the securities devised as eligible for repo can be readily converted into hierarchically higher money: here reserves. This conveys why eligible securities may be considered a ‘secondary reserve’. Changing the eligibility criteria for repo collateral thus means granting or withdrawing secondary reserve-status to the involved securities. This has major implications for both the institutions that hold them as assets (here the bank) and the institutions that issue them as their liabilities. If an institution’s debt issued as a liability qualifies as eligible repo collateral, the demand for this instrument will be significantly higher and the interest to be paid will be significantly lower. The issuers of the security do not feature in Figure 7 but could be added in a more comprehensive ‘Monetary Architecture’ visualization.

The repo lender is in the position to stipulate collateral eligibility either ad hoc or in a more formalized way, for instance via a collateral framework. Collateral frameworks are used by central banks and other repo lenders to define the set of eligible collateral through which repo borrowers can engage in transactions with them, as well as the haircut imposed on the security posted.83 The design of a collateral framework has a paramount influence on the market liquidity of the securities included in it—ie, the ease with which they are traded—as well as the funding liquidity of the repo borrowers—ie, the ease with which they can obtain funding.84 Repo lenders can modify the collateral framework upon their discretion. A tightening of the collateral framework implies a reduction of ‘elasticity space’85 on both counterparties’ balance sheets, whereas a widening of the collateral framework expands the balance sheets’ elasticity space. In the case of vertical repos, the hierarchically higher institution can impose effective constraints on credit money creation on its balance sheet. In the case of a horizontal repo, the repo lender can influence the ease of obtaining pre-existing credit money instruments. Our proposed notation style allows making collateral frameworks—which usually are obscured by opacity86—explicit and transparent.

To substantiate the merits of our proposed notation style of vertical and horizontal repos with two quadruple-entry consistent operations and the collateral framework made a property of the repo lender’s balance sheet, we apply it in the subsequent sections on two quintessential cases that are of profound relevance for the European monetary architecture: the Eurosystem’s monetary policy operations that are based on vertical repos, as well as the secured interbank market of the Euro area, which uses the horizontal repo mechanism both for General and Special Collateral Repos. The two case studies investigate the institutional setup around vertical and horizontal repos as well as the historical transformations which have taken place since the inception of the Economic and Monetary Union (EMU), in particular in relation to the Global Financial Crisis and the Eurocrisis.

VERTICAL REPOS AS MONETARY POLICY INSTRUMENTS IN THE EURO AREA

1. Eurosystem monetary policy operations on-balance-sheet

Our first case study addresses vertical repos, which play a central role for monetary policy in the Eurosystem. In the original monetary policy framework, repos were foreseen as the primary mechanism to implement monetary policy. The main alternative—outright purchases of securities—was only attributed a subordinate role.87 The National Central Banks (NCBs) are the hierarchically higher balance sheets chosen to carry out the monetary policy operations set by the ECB Governing Council.88 They thus create reserves—ie, provide liquidity—for ‘their’ banking system in accordance with ECB rules and the capital key.89 The ECB balance sheet was not originally operationalized for monetary policy activities.90

Table 1 provides a systematic overview on the role of vertical repos in the original monetary policy framework, which was developed prior to the start of the European monetary union in 1999. On the one hand, open market operations (OMOs) are monetary policy operations carried out at the initiative of the Eurosystem. The regular OMOs comprise the Main Refinancing Operations (MRO) and the Longer-Term Refinancing Operations (LTROs). Fine-tuning operations and structural operations are extemporary OMOs. On the other hand, the standing facilities can be used upon the initiative of banks to absorb and provide liquidity. The Marginal Lending Facility (MLF) allows them to borrow reserves overnight, whilst the Deposit Facility allows banks to deposit remunerated reserves at the Eurosystem. For both OMOs and standing facilities repos and outright purchases are the main transaction types.91

The original monetary policy framework of the Eurosystem.

| Monetary policy operation | Types of transactions | Maturity | Frequency | Procedure | |

|---|---|---|---|---|---|

| Liquidity providing | Liquidity absorbing | ||||

| OPEN MARKET OPERATIONS | |||||

| Main refinancing operations (MRO) | * Repo | – | * 2 weeks | * Weekly | * Standard tenders |

| Longer-term refinancing operations (LTROs) | * Repo | – | * 3 months | * Monthly | * Standard tenders |

| Fine-tuning operations | * Repo * FX swaps | * Repo * FX swaps * Collection of fixed-term deposits | * Non-standardized | * Non-regular | *Quick tenders * Bilateral procedures |

| * Outright purchases | * Outright sales | – | * Non-regular | * Bilateral procedures | |

| Structural operations | * Repo | * Issuance of debt certificates | * Standardized/ non-standardized | * Regular + non-regular | * Standard tenders |

| * Outright purchases | * Outright sales | – | * Non-regular | * Bilateral procedures | |

| STANDING FACILITIES | |||||

| Marginal lending facility (MLF) | * Repo | – | * Overnight | * Access at the discretion of counterparties | |

| Deposit facility (DF) | – | * Deposit | * Overnight | * Access at the discretion of counterparties | |

| Monetary policy operation | Types of transactions | Maturity | Frequency | Procedure | |

|---|---|---|---|---|---|

| Liquidity providing | Liquidity absorbing | ||||

| OPEN MARKET OPERATIONS | |||||

| Main refinancing operations (MRO) | * Repo | – | * 2 weeks | * Weekly | * Standard tenders |

| Longer-term refinancing operations (LTROs) | * Repo | – | * 3 months | * Monthly | * Standard tenders |

| Fine-tuning operations | * Repo * FX swaps | * Repo * FX swaps * Collection of fixed-term deposits | * Non-standardized | * Non-regular | *Quick tenders * Bilateral procedures |

| * Outright purchases | * Outright sales | – | * Non-regular | * Bilateral procedures | |

| Structural operations | * Repo | * Issuance of debt certificates | * Standardized/ non-standardized | * Regular + non-regular | * Standard tenders |

| * Outright purchases | * Outright sales | – | * Non-regular | * Bilateral procedures | |

| STANDING FACILITIES | |||||

| Marginal lending facility (MLF) | * Repo | – | * Overnight | * Access at the discretion of counterparties | |

| Deposit facility (DF) | – | * Deposit | * Overnight | * Access at the discretion of counterparties | |

Source: ECB, ‘The Single Monetary Policy in Stage Three’, General Documentation on Eurosystem Monetary Policy Instruments and Procedures (2000) 7.

The original monetary policy framework of the Eurosystem.

| Monetary policy operation | Types of transactions | Maturity | Frequency | Procedure | |

|---|---|---|---|---|---|

| Liquidity providing | Liquidity absorbing | ||||

| OPEN MARKET OPERATIONS | |||||

| Main refinancing operations (MRO) | * Repo | – | * 2 weeks | * Weekly | * Standard tenders |

| Longer-term refinancing operations (LTROs) | * Repo | – | * 3 months | * Monthly | * Standard tenders |

| Fine-tuning operations | * Repo * FX swaps | * Repo * FX swaps * Collection of fixed-term deposits | * Non-standardized | * Non-regular | *Quick tenders * Bilateral procedures |

| * Outright purchases | * Outright sales | – | * Non-regular | * Bilateral procedures | |

| Structural operations | * Repo | * Issuance of debt certificates | * Standardized/ non-standardized | * Regular + non-regular | * Standard tenders |

| * Outright purchases | * Outright sales | – | * Non-regular | * Bilateral procedures | |

| STANDING FACILITIES | |||||

| Marginal lending facility (MLF) | * Repo | – | * Overnight | * Access at the discretion of counterparties | |

| Deposit facility (DF) | – | * Deposit | * Overnight | * Access at the discretion of counterparties | |

| Monetary policy operation | Types of transactions | Maturity | Frequency | Procedure | |

|---|---|---|---|---|---|

| Liquidity providing | Liquidity absorbing | ||||

| OPEN MARKET OPERATIONS | |||||

| Main refinancing operations (MRO) | * Repo | – | * 2 weeks | * Weekly | * Standard tenders |

| Longer-term refinancing operations (LTROs) | * Repo | – | * 3 months | * Monthly | * Standard tenders |

| Fine-tuning operations | * Repo * FX swaps | * Repo * FX swaps * Collection of fixed-term deposits | * Non-standardized | * Non-regular | *Quick tenders * Bilateral procedures |

| * Outright purchases | * Outright sales | – | * Non-regular | * Bilateral procedures | |

| Structural operations | * Repo | * Issuance of debt certificates | * Standardized/ non-standardized | * Regular + non-regular | * Standard tenders |

| * Outright purchases | * Outright sales | – | * Non-regular | * Bilateral procedures | |

| STANDING FACILITIES | |||||

| Marginal lending facility (MLF) | * Repo | – | * Overnight | * Access at the discretion of counterparties | |

| Deposit facility (DF) | – | * Deposit | * Overnight | * Access at the discretion of counterparties | |

Source: ECB, ‘The Single Monetary Policy in Stage Three’, General Documentation on Eurosystem Monetary Policy Instruments and Procedures (2000) 7.

With the advent of unconventional monetary policy, new types of repo operations and outright Asset Purchasing Programmes (APPs) were added to the original monetary policy framework. Table 2 presents an overview of those unconventional monetary programs. On the one hand, it shows the different rounds of non-regular repo operations, starting with the first Targeted Longer-Term Refinancing Operations (TLTROs) in 2014 up to the Pandemic Emergency Longer-Term Refinancing Operations (PELTRO) introduced in 2020. On the other hand, the table lists the four non-regular Asset Purchasing Programmes introduced after the GFC and the Eurocrisis as well as the Pandemic Emergency Purchase Programme (PEPP).

Unconventional Monetary Policy Programmes of the Eurosystem (as of 2024).

| NON-REGULAR REPO OPERATIONS | |||||

|---|---|---|---|---|---|

| Monetary policy operation | Types of transactions | Maturity | Frequency | Procedure | |

| Liquidity providing | Liquidity absorbing | ||||

| Targeted longer-term refinancing operations (TLTRO) I | * Repo | - | * 4 years | * Quarterly | * Standard tenders |

| TLTRO II | * Repo | - | * 4 years | * Quarterly | * Standard tenders |

| TLTRO III | * Repo | - | * 3 years | * Quarterly | * Standard tenders |

| Bridge LTRO | * Repo | - | * 1 year | * Weekly | * Standard tenders |

| Pandemic emergency longer-term refinancing operations (PELTRO) | * Repo | - | * 1 year | * Quarterly | * Standard tenders |

| NON-REGULAR TEMPORARY ASSET PURCHASING PROGRAMMES | |||||

| Monetary policy operation | Balance sheet carrying out the operation | Maturity | Frequency | Procedure | |

| Corporate Sector Purchase Programme (CSPP) | Six NCBs do all the buying; risk-sharing according to capital keya | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Public Sector Purchase Programme (PSPP) | All Eurosystem NCBs buy the securities issued by their respective governments and bear all the risk; capital key is upper limit | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Asset-Backed Securities Purchase Programme (ABSPP) | Only those NCBs that act as internal asset managers conduct the purchasesb | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Covered Bond Purchase Programme (CBPP) | All Eurosystem NCBs buy according to ECB’s capital key | * Non-standardized | * Non-regular | * Bilateral procedures | |

| NON-REGULAR TEMPORARY ASSET PURCHASING PROGRAMMES—COVID PANDEMIC SPECIAL | |||||

| Pandemic Emergency Purchase Programme (PEPP) | All Eurosystem NCBs buy the securities issued by their respective governments and bear all the risk; divergence from capital key is possible | * Non-standardized | * Non-regular | * Bilateral procedures | |

| NON-REGULAR REPO OPERATIONS | |||||

|---|---|---|---|---|---|

| Monetary policy operation | Types of transactions | Maturity | Frequency | Procedure | |

| Liquidity providing | Liquidity absorbing | ||||

| Targeted longer-term refinancing operations (TLTRO) I | * Repo | - | * 4 years | * Quarterly | * Standard tenders |

| TLTRO II | * Repo | - | * 4 years | * Quarterly | * Standard tenders |

| TLTRO III | * Repo | - | * 3 years | * Quarterly | * Standard tenders |

| Bridge LTRO | * Repo | - | * 1 year | * Weekly | * Standard tenders |

| Pandemic emergency longer-term refinancing operations (PELTRO) | * Repo | - | * 1 year | * Quarterly | * Standard tenders |

| NON-REGULAR TEMPORARY ASSET PURCHASING PROGRAMMES | |||||

| Monetary policy operation | Balance sheet carrying out the operation | Maturity | Frequency | Procedure | |

| Corporate Sector Purchase Programme (CSPP) | Six NCBs do all the buying; risk-sharing according to capital keya | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Public Sector Purchase Programme (PSPP) | All Eurosystem NCBs buy the securities issued by their respective governments and bear all the risk; capital key is upper limit | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Asset-Backed Securities Purchase Programme (ABSPP) | Only those NCBs that act as internal asset managers conduct the purchasesb | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Covered Bond Purchase Programme (CBPP) | All Eurosystem NCBs buy according to ECB’s capital key | * Non-standardized | * Non-regular | * Bilateral procedures | |

| NON-REGULAR TEMPORARY ASSET PURCHASING PROGRAMMES—COVID PANDEMIC SPECIAL | |||||

| Pandemic Emergency Purchase Programme (PEPP) | All Eurosystem NCBs buy the securities issued by their respective governments and bear all the risk; divergence from capital key is possible | * Non-standardized | * Non-regular | * Bilateral procedures | |

Notes:

aThe NCBs conducting the purchases are (1) the Nationale Bank van België/Banque Nationale de Belgique; (2) the Deutsche Bundesbank; (3) the Banco de España; (4) the Banca d’Italia; (5) the Banque de France; and (6) the Suomen Pankki—Finlands Bank.

bThe national central bank carrying out the operations depends on the country of the ABSs’ underlying collateral. In terms of the geographical coverage, the following allocation applies: (1) Banque Nationale de Belgique: Belgium; (2) Deutsche Bundesbank: Germany; (3) Banco de España: Spain; (4) Banque de France: Finland, France, Ireland, Luxembourg and Portugal; (5) Banca d’Italia: Italy; and (6) De Nederland Che Bank: Netherlands.

Sources: ECB, ‘ECB Extends Pandemic Emergency Longer-Term Refinancing Operations’, Press Release (10 December 2020) <https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.pr201210~8acfa5026f.en.html; ECB, ‘Monetary Policy Decisions’, Press Release (12 March 2020) <https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.mp200312~8d3aec3ff2.en.html; ECB, ‘Asset Purchase Programmes’ (ECB, 2022), <https://www.ecb.europa.eu/mopo/implement/app/html/index.en.html; ECB, ‘Pandemic Emergency Purchase Programme (PEPP)’ (ECB, 2022) <https://www.ecb.europa.eu/mopo/implement/pepp/html/index.en.html; ECB, ‘Targeted Longer-Term Refinancing Operations (TLTROs)’ (ECB, 2022) <https://www.ecb.europa.eu/mopo/implement/omo/tltro/html/index.en.html.

Unconventional Monetary Policy Programmes of the Eurosystem (as of 2024).

| NON-REGULAR REPO OPERATIONS | |||||

|---|---|---|---|---|---|

| Monetary policy operation | Types of transactions | Maturity | Frequency | Procedure | |

| Liquidity providing | Liquidity absorbing | ||||

| Targeted longer-term refinancing operations (TLTRO) I | * Repo | - | * 4 years | * Quarterly | * Standard tenders |

| TLTRO II | * Repo | - | * 4 years | * Quarterly | * Standard tenders |

| TLTRO III | * Repo | - | * 3 years | * Quarterly | * Standard tenders |

| Bridge LTRO | * Repo | - | * 1 year | * Weekly | * Standard tenders |

| Pandemic emergency longer-term refinancing operations (PELTRO) | * Repo | - | * 1 year | * Quarterly | * Standard tenders |

| NON-REGULAR TEMPORARY ASSET PURCHASING PROGRAMMES | |||||

| Monetary policy operation | Balance sheet carrying out the operation | Maturity | Frequency | Procedure | |

| Corporate Sector Purchase Programme (CSPP) | Six NCBs do all the buying; risk-sharing according to capital keya | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Public Sector Purchase Programme (PSPP) | All Eurosystem NCBs buy the securities issued by their respective governments and bear all the risk; capital key is upper limit | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Asset-Backed Securities Purchase Programme (ABSPP) | Only those NCBs that act as internal asset managers conduct the purchasesb | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Covered Bond Purchase Programme (CBPP) | All Eurosystem NCBs buy according to ECB’s capital key | * Non-standardized | * Non-regular | * Bilateral procedures | |

| NON-REGULAR TEMPORARY ASSET PURCHASING PROGRAMMES—COVID PANDEMIC SPECIAL | |||||

| Pandemic Emergency Purchase Programme (PEPP) | All Eurosystem NCBs buy the securities issued by their respective governments and bear all the risk; divergence from capital key is possible | * Non-standardized | * Non-regular | * Bilateral procedures | |

| NON-REGULAR REPO OPERATIONS | |||||

|---|---|---|---|---|---|

| Monetary policy operation | Types of transactions | Maturity | Frequency | Procedure | |

| Liquidity providing | Liquidity absorbing | ||||

| Targeted longer-term refinancing operations (TLTRO) I | * Repo | - | * 4 years | * Quarterly | * Standard tenders |

| TLTRO II | * Repo | - | * 4 years | * Quarterly | * Standard tenders |

| TLTRO III | * Repo | - | * 3 years | * Quarterly | * Standard tenders |

| Bridge LTRO | * Repo | - | * 1 year | * Weekly | * Standard tenders |

| Pandemic emergency longer-term refinancing operations (PELTRO) | * Repo | - | * 1 year | * Quarterly | * Standard tenders |

| NON-REGULAR TEMPORARY ASSET PURCHASING PROGRAMMES | |||||

| Monetary policy operation | Balance sheet carrying out the operation | Maturity | Frequency | Procedure | |

| Corporate Sector Purchase Programme (CSPP) | Six NCBs do all the buying; risk-sharing according to capital keya | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Public Sector Purchase Programme (PSPP) | All Eurosystem NCBs buy the securities issued by their respective governments and bear all the risk; capital key is upper limit | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Asset-Backed Securities Purchase Programme (ABSPP) | Only those NCBs that act as internal asset managers conduct the purchasesb | * Non-standardized | * Non-regular | * Bilateral procedures | |

| Covered Bond Purchase Programme (CBPP) | All Eurosystem NCBs buy according to ECB’s capital key | * Non-standardized | * Non-regular | * Bilateral procedures | |

| NON-REGULAR TEMPORARY ASSET PURCHASING PROGRAMMES—COVID PANDEMIC SPECIAL | |||||

| Pandemic Emergency Purchase Programme (PEPP) | All Eurosystem NCBs buy the securities issued by their respective governments and bear all the risk; divergence from capital key is possible | * Non-standardized | * Non-regular | * Bilateral procedures | |

Notes:

aThe NCBs conducting the purchases are (1) the Nationale Bank van België/Banque Nationale de Belgique; (2) the Deutsche Bundesbank; (3) the Banco de España; (4) the Banca d’Italia; (5) the Banque de France; and (6) the Suomen Pankki—Finlands Bank.

bThe national central bank carrying out the operations depends on the country of the ABSs’ underlying collateral. In terms of the geographical coverage, the following allocation applies: (1) Banque Nationale de Belgique: Belgium; (2) Deutsche Bundesbank: Germany; (3) Banco de España: Spain; (4) Banque de France: Finland, France, Ireland, Luxembourg and Portugal; (5) Banca d’Italia: Italy; and (6) De Nederland Che Bank: Netherlands.

Sources: ECB, ‘ECB Extends Pandemic Emergency Longer-Term Refinancing Operations’, Press Release (10 December 2020) <https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.pr201210~8acfa5026f.en.html; ECB, ‘Monetary Policy Decisions’, Press Release (12 March 2020) <https://www.ecb.europa.eu/press/pr/date/2020/html/ecb.mp200312~8d3aec3ff2.en.html; ECB, ‘Asset Purchase Programmes’ (ECB, 2022), <https://www.ecb.europa.eu/mopo/implement/app/html/index.en.html; ECB, ‘Pandemic Emergency Purchase Programme (PEPP)’ (ECB, 2022) <https://www.ecb.europa.eu/mopo/implement/pepp/html/index.en.html; ECB, ‘Targeted Longer-Term Refinancing Operations (TLTROs)’ (ECB, 2022) <https://www.ecb.europa.eu/mopo/implement/omo/tltro/html/index.en.html.

From the perspective of balance sheet mechanics, there is no difference if a monetary policy operation is carried out upon the initiative of the central bank (as in the case of OMOs) or the banks (as in the case of standing facilities). It does differ, however, if the monetary policy operation is implemented via a repo or an outright transaction.

Figure 8 depicts the monetary policy operations that are carried out as a vertical repo transaction. In line with our proposed notation style, a Euro area bank receives reserves as an asset which the NCB creates on the spot. In return, the bank creates a repo as its liability which the NCB receives as an asset. In the second quadruple-entry consistent operation, the security used as repo collateral becomes ‘due’ for the Euro area bank but according to Basel III regulations does not leave its balance sheet and is put into ‘encumbered’ status. The NCB could record the securities received as an off-balance-sheet position, but it does not formally touch its asset book.

Monetary policy operation between NCB and bank as a vertical repo.

The empirical data that corresponds to this transaction can be retrieved from the official documentation of the Eurosystem’s disaggregated financial statements.92 The NCB’s repo lending is recorded in item 5 called ‘lending to euro area credit institutions related to monetary policy operations denominated in euro’; as sub-categories, this item encompasses MROs, LTROs, MLF, fine-tuning reverse operations, and credits related to margin calls. Off-balance-sheet positions are not officially recorded.

Figure 9 depicts the outright transaction which is a more straightforward case. The NCB creates reserves as its liability and obtains a security. For the Euro area bank, the transaction is an asset swap of reserves against security. In the official documentation of the Eurosystem’s disaggregated balance sheet, the security received by the NCB is recorded under ‘assets’ in item 7 called ‘securities of euro area residents denominated in euro’, which has two sub-categories: ‘securities held for monetary policy purposes’ and ‘other purposes’.

Monetary policy operation between NCB and bank as outright purchase.

The reserves created by the NCB in either repo or outright transactions are recorded under ‘liabilities’ in item 2 called ‘liabilities to euro area credit institutions related to monetary policy operations denominated in euro’. As sub-categories, this item primarily comprises ‘Current accounts (covering the minimum reserve system)’, which are not remunerated, as well as the ‘deposit facility’, which is remunerated at a set rate. Other, less important reserve types in this item are ‘fixed-term deposits’, ‘fine-tuning reverse operations’, as well as ‘deposits related to margin calls’. Item 3 contains ‘other liabilities to euro area credit institutions denominated in euro’. The reserves created through repos or outright purchases primarily appear as reserves in the current account or in the deposit facility. Which type of reserve is created does not correspond to a specific programme but is decided on a case-by-case basis depending on what the Eurosystem offers and what the bank chooses.93

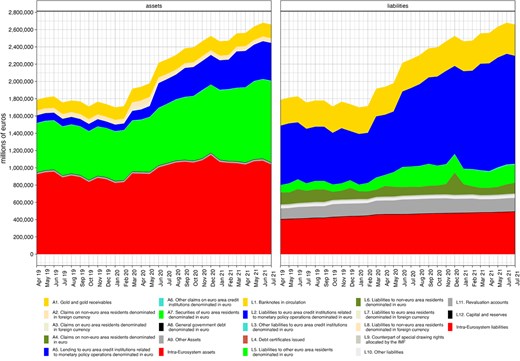

To provide empirical context for those items, Figure 10 plots a visualization of the asset and liability structure of Deutsche Bundesbank from 2019 to 2021. Items 5 and 7 pertaining to vertical repos and outright purchases can be found in the left panel (cf A5 and A7); items 2 and 3 on the different types of reserves feature in the right panel (cf L2 and L3).

Deutsche Bundesbank Balance Sheet, Assets and Liabilities, 2019–21. Notes: Labels starting with ‘A’ apply to the ‘asset’ panel, and with ‘L’ to the ‘liabilities’ panel. Source: Disaggregated Financial Statement of the Eurosystem.

Figure 11 looks at the Eurosystem as a whole and presents the volumes of monetary policy operations as to the official documentation from 1999 to 2022. Panel 1 shows repo transactions, Panel 2 outright purchases. The individual entries fit to the categories of operations introduced in Tables 1 and 2. Panel 3 depicts the volume of central bank liabilities to Euro area banks, subdivided into the different types of reserves. The black line plots the level of required reserves.

Eurosystem Aggregated Financial Statement, weekly balance, in mn EUR (1999–2022). Notes: Euro area changing composition, only items denominated in euro. LTROs include all LTROs and TLTROs. Source: ECB, ‘Internal Liquidity Management (ILM)’ (ECB, 2024) <https://data.ecb.europa.eu/data/datasets/ILM/data-information#:~:text=ILM%20statistics%20refer%20to%20the,the%20banking%20system%27s%20liquidity%20position.&text=The%20data%20refer%20to%20or,financial%20statement%20of%20the%20Eurosystem>.

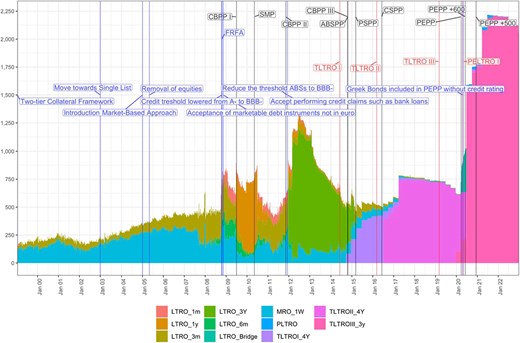

The three panels in Figure 11 display the relative empirical importance of vertical repos in the history of the European monetary union and their impact on central bank money creation. Vertical repos were the Eurosystem’s main mechanism for monetary policy implementation prior to the GFC. In this period, the Eurosystem had a ‘lean’ balance sheet. Reserves were almost exclusively kept in the current accounts and matched the level of required reserves. Outright purchases of securities merely played a subordinate role, as originally intended. The sea change in the composition of Eurosystem balance sheets started on 6 October 2008 when the Eurosystem—under the pressure resulting from the Lehman Brothers bankruptcy on 19 September 2008—shifted its policy in the MROs to ‘fixed-rate full allotment’ (FRFA). Rather than auctioning an ex ante defined volume of central bank reserves, Euro area banks could now use vertical repos to borrow central bank liquidity to an unlimited extent.94 As a result, repo volumes spiked and banks started systematically using the deposit facility, which caused the emergence of excess reserves. Soon after, the relative importance of repos as monetary policy instrument began to shrink. In July 2009, the first Covered Bond Purchase Programme (CBPP-1) ushered in a new era of outright purchases.95 Paralleling the Fed’s Dealer of Last Resort operations at the time,96 the securities bought under CBPP-1 are not classified as ‘securities held for monetary policy purposes’ but rather as ‘other securities’. In 2014, the Eurosystem’s APPs commenced. The most significant impact on the Eurosystem balance sheet came from the purchases of Asset-backed Securities (ABSs) with the Asset-Backed Securities Purchase Programme (ABSPP), which began in November 2014, as well as the Pandemic Emergency Purchase Programme (PEPP), which started in March 2020.97 Both programmes gave rise to a massive increase of central bank reserve creation that impacted both the current account and the deposit facility. Due to the APPs, outright purchases today play a substantially larger role than vertical repos for the creation of central bank reserves.

As repos declined in relative importance to outright purchases, the data shows substantial dynamics in the volume of vertical repos. To understand the spikes as they happened for instance in 2012, 2017, and 2020, we have to look at the Eurosystem’s collateral framework.

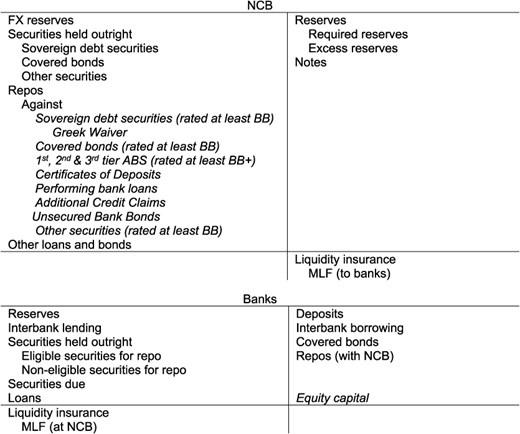

2. The Eurosystem’s collateral framework and its transformations

The Eurosystem’s collateral framework determines which securities banks can post as collateral when they want to engage in vertical repos with ‘their’ NCB to borrow reserves from it and, vice versa, which securities the NCB accepts as assets on its hypothetical off-balance-sheet positions. Hence, the collateral framework grants the Eurosystem discretion to influence the elasticity space on both the NCBs’ and the banks’ balance sheet. It also plays a crucial role in influencing the market liquidity of securities by determining whether they have a central bank backstop and thus receive the status of a ‘secondary reserve’.

The Eurosystem’s collateral framework is the sum of its ‘General Collateral Framework’, which determines collateral eligibility in normal times, and the ‘Temporary Collateral Framework’, which can be changed on short notice to react to crisis situations and overrules the general framework.98 The collateral framework not only applies to securities in standard and non-standard repo transactions but also to securities purchased outright in standard and non-standard operations as both OMOs and APPs have so far followed the stipulations of the collateral framework, even though this is not a strict necessity.99 Since the European monetary union became effective, the ECB Governing Council has subjected the Eurosystem’s collateral framework to a tremendous transformation, pointing to its significance as a de facto policy tool.

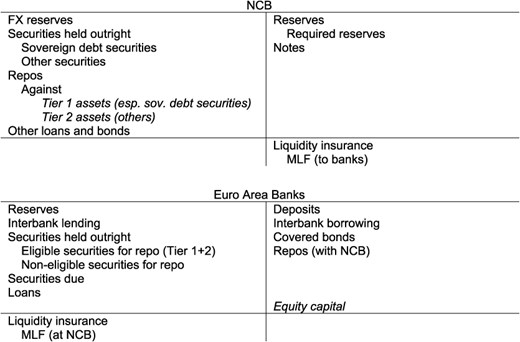

As the result of the preparatory work at the European Monetary Institute (EMI) in the mid-1990s, the Eurosystem adopted a two-tier collateral framework in 1998 which became effective when the European monetary union became operational in 1999. Accordingly, ‘Tier 1 assets’ comprised debt instruments with harmonized eligibility criteria across the monetary union and pooled risk among all members of the Eurosystem. By contrast, ‘Tier 2 assets’ were individually proposed by the NCBs, which solely bore the risk, and were connected to the legacy collateral framework dating back to the time before European monetary unification.100

Figure 12 depicts this original two-tier framework on-balance-sheet, integrated in the hierarchical relationship between a Euro area NCB and one of the banks in its inner-Euro area jurisdiction. The NCB issues reserves as liabilities, which the banks hold as assets, and provides liquidity insurance in the form of the Marginal Lending Facility as a contingent liability, which constitutes a contingent asset for the banks. The NCB balance sheet comprises both securities held outright and repos, for which the list of eligible collateral is stipulated. The bank has posted this eligible collateral in vertical repo transaction with the NCB and thus has Tier 1 and Tier 2 assets as securities in a repo transaction. Tier 1 securities mainly comprise sovereign debt securities. Tier 2 assets are more diverse and also include more unusual instruments such as equities.

NCB and banks in Euro area with two-tiered collateral framework (as of 1999).

As the two-tier collateral framework had only been seen as a temporary solution, the Eurosystem soon started working on harmonizing the collateral framework within the monetary union.101 The goal was the introduction of a ‘Single List’, in which the distinction of Tier 1 and Tier 2 assets would be replaced with a distinction of ‘marketable’ and ‘non-marketable’ assets. While marketable assets comprised what previously were Tier 1 assets, non-marketable assets were defined as credit claims such as bank loans and retail mortgage-backed debt instruments.102 In 2003, the Governing Council approved the move towards a ‘Single List’ and its introduction in two steps. In May 2005, it completed the first step which involved the removal of equities as acceptable collateral, refining the eligibility criteria, and introducing certain euro-denominated securities issued outside of the European Economic Area.103 In 2007, as the level of segmentation in financial markets subsided, the move to a ‘Single List’ was completed. NCBs were no longer able to choose eligible collateral for their monetary policy transactions as this became a function exclusively exercised by the ECB.104

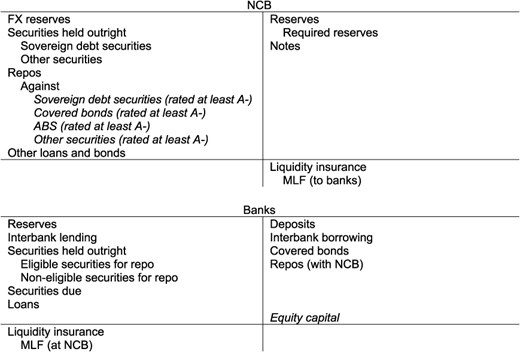

As part of the 2005 reforms, the Eurosystem introduced a market-based approach for government bonds in their collateral framework. According to the new rules, a security required a minimum credit standard of ‘single A’, which meant ‘A-’ by Fitch or Standard & Poor’s, or ‘A3’ by Moody’s, to be eligible for repo transactions with the Eurosystem.105 As a consequence, this reform made the eligibility of liquidity insurance dependent on market sentiment and the assessment of credit rating agencies, instead of generally accepting all sovereign debt securities independently of the market situation. Athanasios Orphanides explains this as an attempt by the ECB to enforce the Stability and Growth Pact (SGP).106 An alternative interpretation by Martin Marcussen is a pure scientization of monetary policy.107 Jens van ’t Klooster argues that the primary reason was to depoliticize the choice of collateral in order to avoid contestation of the ECB’s legitimacy.108

Figure 13 depicts the relationship between the NCB and banks with the changed collateral framework after the introduction of the Single List. The pool of eligible collateral consisted of at least ‘A-’-rated central government securities, regional government securities, unsecured bank bonds, covered bonds, corporate bonds, asset-backed securities (ABSs), and other marketable assets. The changes had reduced the available elasticity space on the NCBs’ and banks’ balance sheets.

NCB and banks in Euro area with Single List collateral framework (as of June 2007).