Abstract

For the Blue Foods economy—those sectors that gain value from the biological productivity of the oceans such as fisheries and aquaculture—climate shocks pose an existential threat. Species range shifts, harmful algal blooms, marine heatwaves, low oxygen events, coral bleaching, and hurricanes all present a serious economic risk to these industries, and yet there exist few financial tools for managing these risks. This contrasts with agriculture, where financial tools such as insurance are widely available for managing numerous weather-related shocks. Designing financial tools to aid risk management, such as insurance, for equitable resilience against marine climate shocks will give coastal communities access to the necessary means for reducing their sensitivity to climate shocks and improving their long-term adaptive capacity. We suggest that a convergence of the insurance industry and marine sectors, fostered through collaboration with governments, academics, and NGOs will help usher in new forms of insurance, such as ocean-index or parametric insurance. These new risk-management tools have the potential to help incentivize sustainable use of living marine resources, as well as strengthening the economic resilience of coastal communities to climate change.

Coping with marine climate shocks

Globally, “blue foods”—fish, invertebrates, and algae captured or cultured in marine ecosystems (Naylor et al., 2021)—are crucial for the food and income security of billions of people (Bennett et al., 2021). As a critical source of protein, fatty acids, and micronutrients, blue foods are essential in combating conditions related to undernutrition or diseases (e.g. Dalton et al., 2009; Weiser et al., 2016; Headey et al., 2018; Kokubun et al., 2020) and are the foundation of the cultures (; Toniello et al., 2019) and economies (Teh and Sumaila, 2013) of coastal communities around the world. With global demand for blue foods expected to double over the next ca. 30 years (Naylor et al., 2021), increasing the resilience of the supply of blue foods, especially in the face of climate change, is urgent (Barange et al., 2018; Cinner and Barnes 2019; Davis et al., 2021; Mason et al. 2021). We argue that modern financial risk management tools, in particular insurance (Beach and Viator, 2008), are central to our ability to bolster the resilience of blue food supply chains and coastal communities, more broadly, to climate shocks (Little et al. 2014, 2015). In land-based food production systems insurance is an omnipresent tool across several social and economic contexts for improving food and income security (Hazell and Hess, 2010). It is used by agriculturalists and cattle farmers to protect their livelihood against adverse weather events (e.g. McIntosh et al., 2013) and for improving access to credit, which can be important for maintaining equipment and buying seeds and fertilizer (Farrin and Miranda, 2015; see Figure 1 for a basic illustration of the parallels between terrestrial and marine climate shocks). Currently, however, there is relatively little use of financial risk management tools such as insurance, especially newer forms such as index or parametric insurance, to help operators manage the impacts of marine-related climate shocks on production in both aquaculture and wild-capture fisheries (Watson et al., 2018; Henriksson et al., 2021).

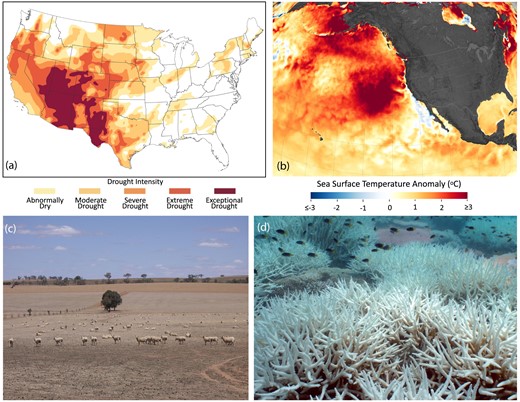

Illustration showing the parallels between climate shocks on land (a; drought) and marine climate shocks (b; marine heatwaves). For terrestrial food production systems, like agriculture and cattle systems (c), many financial tools exist (e.g. parametric insurance) that operators can buy in order to manage these climate risks. At sea, fishers, aquaculturalists, and marine tourism operators depend on the biological productivity of the oceans. Marine climate shocks such as marine heatwaves can impact this productivity, for example, by creating conditions where corals bleach (d). Figures a and b are from the NASA Earth Observatory; c is a photograph taken by VirtualSteve, Wikipedia; and d is from Damian Thomson, CSIRO.

Climate change in our oceans is having increasing impacts on marine industries and coastal communities globally (e.g. Cinner et al. 2015; Jardine et al., 2020). Long-term shifts driven by climate change include changes in marine species ranges, diversity and abundance, species migration pathways, and habitat distributions (Ainsworth et al., 2011; Hobday and Lough, 2011; Cheung, 2018; Payne et al., 2021; Pinsky et al., 2021). Against this increasing background pressure, climate shocks such as marine heatwaves, harmful algal blooms, low oxygen events, and hurricanes can have devastating impacts (Frölicher and Laufkötter, 2018). These events can lead to reduced growth, coral bleaching, poor productivity, increased disease risk, and fish kills (Wolff et al. 2018; Jardine et al., 2020). Additionally, the increasing frequency and intensity of storms can have direct impacts on crucial physical infrastructure, such as boats, gear, net pens, and shoreside access points (Callaway et al., 2012). Climate shocks thus give rise to increased costs and reduced profits for blue food producers (Fisher et al., 2021) and can reduce both the overall resilience of coastal communities to these shocks and their ability to adapt to the longer-term impacts of climate change (Daw et al., 2009). The continued exposure to these shocks is a serious threat to the maintenance of blue food supply chains and the associated food and income security of those individuals that work in these industries. These risks can dictate short- and long-term profitability, and ultimately solvency, across the full range of blue-food sectors from artisanal fisheries to industrial fisheries to transnational aquaculture firms (Burgess et al., 2018; Klinger et al., 2018).

Insurance maintains the capital reserves that blue-food actors hold by reducing the volatility in income. This enables blue-food actors to invest in the means to cope with future shocks. More specifically, insurance does not simply provide access to financial assets—insurance transfers risk (Sethi, 2010), typically via an insurance contract between the actor experiencing the realized risk (e.g. a farmer) and a different actor that can better absorb the risk (i.e. an insurance firm). Food producers generally agree to pay a premium to an insurer (e.g. a private insurance company), who will in turn pay an amount back should a loss in production occur due to one of these events, helping maintain solvency. This is a key mechanism by which food producers can limit the various ways climate shocks can impact production (Falco et al., 2014). For example, when a peril (like a storm) prevents a business (like a farm) from carrying on operations, this would be classed as a “business interruption.” Additionally, a climate shock might also damage critical infrastructure (e.g. a fishing boat) or harm a worker. Importantly, the climate shock can impact the biological productivity underpinning operations. For example, a heatwave on land can result in below-average yields simply because these are not good growing conditions for the specific crop (Ummenhofer et al. 2009), and a marine heatwave might have similar impacts on the catch per unit effort of fishers or the growth of shellfish in an aquaculture operation. Different insurance policies can be designed for each of these issues, but there are always several major challenges to overcome for insurance to become a viable option. Specifically, moral hazard, adverse selection, and the issue of accurately pricing risk (see the Table 1 for an overview of terms relating to climate and financial risk). For the blue-foods sectors, these challenges present themselves as major barriers to the use of insurance as a tool for protecting coastal communities from climate shocks (Mumford et al., 2009; Sainsbury et al., 2019; Maltby et al., 2022).

Glossary of climate adaptation and financial risk management terms.

| Climate adaptation terminology | Financial risk management terminology |

|---|---|

| Vulnerability is a term broadly used to describe how a certain community might be negatively impacted by climate change. There is an equation that defines vulnerability as exposure multiplied by sensitivity divided by adaptive capacity. These additional terms are described below. In this way, the vulnerability of a given actor, group, or community is increased by sensitivity and exposure but reduced by adaptive capacity. | Risk avoidance is simply when people/communities move away from the area exposed to the threat. In the case of fisheries, this could be in terms of geography, when fishers move away from areas affected by marine heatwaves to different fishing grounds, or economically, when fishers change their target species to those not affected by the risk. Risk transfer is when the negative impacts of a shock are transferred to someone else (e.g. an insurance company). This is essentially what insurance facilitates. |

| Exposure to a stressor (e.g. a climate event or trend) can be thought of as being directly analogous to risk, the probability of a stressor/threat/hazard being realized. The greater the risk, the more frequently the community is exposed to the stressor. For example, certain coastal communities are periodically exposed to marine heatwaves, and this directly impacts their vulnerability. Reducing the exposure to a stressor (or reducing the probability of being hit by a shock) is achieved through three means: risk avoidance and transfer. | Insurance is a form of risk management represented by a contractual arrangement called a policy, in which one party is indemnified against financial losses by an insurer. The insurer pools funds across similarly insured parties, who pay a premium to the insurer based on the loss risk. Pooled funds are used to compensate for realized losses. In contrast to traditional insurance, which indemnifies against actual loss, parametric insurance covers the probability of a predefined event triggered by an index or metric. Parametric insurance has a basis risk, which is the risk that the triggered index does not represent the underlying risk exposure. Negative basis risk results when a loss is incurred without the contract being triggered, while a positive basis risk results in a payout without a financial loss. |

| Sensitivity describes the intrinsic properties of the focal element (e.g. a community of fishers) in its ability to withstand a shock. For example, sensitivity to marine heatwaves is increased for fishers dependent on one species that dies during marine heatwaves. Reducing the sensitivity is traditionally through diversification (e.g. change target species for a fisher, change the prey species for a predator, and change the diet for an aquaculture operation). | Reinsurance is a practice in the insurance industry where an insurance company reduces its risk of paying large claims by purchasing insurance policies from other insurers, known as reinsurers. In other words, it is a form of insurance for insurers. Reinsurance allows insurance companies to remain solvent by mitigating the risk associated with underwritten policies. In the event of a significant claim, the insurance company would not bear the entire financial burden but would share it with the reinsurer. This helps ensure that the insurance company has sufficient reserves to pay out claims, especially in times of high-claim events like natural disasters. In a reinsurance contract, the company that purchases the reinsurance pays a premium to the reinsurer, who would then pay a portion of the claims based on the agreement. The original insurer is the ceding company, and the risk passed to the reinsurer is called the ceded risk. Reinsurance can be divided into two types: facultative reinsurance and treaty reinsurance. Facultative reinsurance provides coverage for an individual or a specified risk or contract, while treaty reinsurance covers all or a portion of the risks that an insurance company might encounter. |

| Adaptive capacity describes the ability to cope with a stressor as a result of the extrinsic properties of the system in which the focal element lies. Increasing the adaptive capacity increases the coping range. For example, quite simply, the greater the capital reserves (i.e. money in the bank) that a fisher of aquaculturalist has access to, the better able they are to buy gear and technology and invest in their teams and knowledge, with which to minimize the negative impacts of a shock. | Moral hazard and adverse selection are two key concepts in the field of insurance and economics that refer to situations where the behaviour of one party changes to the detriment of another after a transaction has been completed. Moral hazard term refers to the change in behaviour of insured parties once they are covered by an insurance policy. Essentially, it is the idea that individuals might take on more risk because they know they are insured and that potential losses will be covered by the insurer. For instance, a fisherman with a comprehensive insurance policy might choose to sail during a severe storm or fish in unsustainable ways because they know any damage or loss incurred will be compensated by their insurance company. The problem with moral hazard is that it can lead to an increase in the frequency and severity of claims, which in turn can cause insurance premiums to rise for everyone. |

| Resilience—a broadly used term in both qualitative and quantitative ways. For example, the term resilience has been used to describe a system’s general ability to cope with shocks/change, but it also describes the width of a basin of attraction of an equilibrium point in a dynamical system. The term resilience is often used in conjunction with vulnerability to describe the general ability for a community to withstand a shock (or not). | Adverse selection refers to a situation where an individual’s demand for insurance (the quantity of insurance purchased and the probability of a claim) is positively correlated with the individual’s risk of loss (the insurer is more likely to issue a policy to one who needs it most). In other words, those who are most likely to file a claim are often the ones most likely to seek out and purchase insurance. This happens when the insurer does not have as much information about the risk associated with a potential client as the client does. For instance, in the fisheries context, a fisherman who knows they will be fishing in more risky areas or using more hazardous methods might be more likely to seek comprehensive insurance. Adverse selection can distort the insurance market because insurers might set premiums based on average risk, which might not be sufficient to cover the higher-risk individuals. If not managed, it can lead to a situation where insurance becomes too expensive for low-risk members, driving them out of the insurance pool and leading to what is known as a “death spiral” of increasing premiums. |

| Climate adaptation terminology | Financial risk management terminology |

|---|---|

| Vulnerability is a term broadly used to describe how a certain community might be negatively impacted by climate change. There is an equation that defines vulnerability as exposure multiplied by sensitivity divided by adaptive capacity. These additional terms are described below. In this way, the vulnerability of a given actor, group, or community is increased by sensitivity and exposure but reduced by adaptive capacity. | Risk avoidance is simply when people/communities move away from the area exposed to the threat. In the case of fisheries, this could be in terms of geography, when fishers move away from areas affected by marine heatwaves to different fishing grounds, or economically, when fishers change their target species to those not affected by the risk. Risk transfer is when the negative impacts of a shock are transferred to someone else (e.g. an insurance company). This is essentially what insurance facilitates. |

| Exposure to a stressor (e.g. a climate event or trend) can be thought of as being directly analogous to risk, the probability of a stressor/threat/hazard being realized. The greater the risk, the more frequently the community is exposed to the stressor. For example, certain coastal communities are periodically exposed to marine heatwaves, and this directly impacts their vulnerability. Reducing the exposure to a stressor (or reducing the probability of being hit by a shock) is achieved through three means: risk avoidance and transfer. | Insurance is a form of risk management represented by a contractual arrangement called a policy, in which one party is indemnified against financial losses by an insurer. The insurer pools funds across similarly insured parties, who pay a premium to the insurer based on the loss risk. Pooled funds are used to compensate for realized losses. In contrast to traditional insurance, which indemnifies against actual loss, parametric insurance covers the probability of a predefined event triggered by an index or metric. Parametric insurance has a basis risk, which is the risk that the triggered index does not represent the underlying risk exposure. Negative basis risk results when a loss is incurred without the contract being triggered, while a positive basis risk results in a payout without a financial loss. |

| Sensitivity describes the intrinsic properties of the focal element (e.g. a community of fishers) in its ability to withstand a shock. For example, sensitivity to marine heatwaves is increased for fishers dependent on one species that dies during marine heatwaves. Reducing the sensitivity is traditionally through diversification (e.g. change target species for a fisher, change the prey species for a predator, and change the diet for an aquaculture operation). | Reinsurance is a practice in the insurance industry where an insurance company reduces its risk of paying large claims by purchasing insurance policies from other insurers, known as reinsurers. In other words, it is a form of insurance for insurers. Reinsurance allows insurance companies to remain solvent by mitigating the risk associated with underwritten policies. In the event of a significant claim, the insurance company would not bear the entire financial burden but would share it with the reinsurer. This helps ensure that the insurance company has sufficient reserves to pay out claims, especially in times of high-claim events like natural disasters. In a reinsurance contract, the company that purchases the reinsurance pays a premium to the reinsurer, who would then pay a portion of the claims based on the agreement. The original insurer is the ceding company, and the risk passed to the reinsurer is called the ceded risk. Reinsurance can be divided into two types: facultative reinsurance and treaty reinsurance. Facultative reinsurance provides coverage for an individual or a specified risk or contract, while treaty reinsurance covers all or a portion of the risks that an insurance company might encounter. |

| Adaptive capacity describes the ability to cope with a stressor as a result of the extrinsic properties of the system in which the focal element lies. Increasing the adaptive capacity increases the coping range. For example, quite simply, the greater the capital reserves (i.e. money in the bank) that a fisher of aquaculturalist has access to, the better able they are to buy gear and technology and invest in their teams and knowledge, with which to minimize the negative impacts of a shock. | Moral hazard and adverse selection are two key concepts in the field of insurance and economics that refer to situations where the behaviour of one party changes to the detriment of another after a transaction has been completed. Moral hazard term refers to the change in behaviour of insured parties once they are covered by an insurance policy. Essentially, it is the idea that individuals might take on more risk because they know they are insured and that potential losses will be covered by the insurer. For instance, a fisherman with a comprehensive insurance policy might choose to sail during a severe storm or fish in unsustainable ways because they know any damage or loss incurred will be compensated by their insurance company. The problem with moral hazard is that it can lead to an increase in the frequency and severity of claims, which in turn can cause insurance premiums to rise for everyone. |

| Resilience—a broadly used term in both qualitative and quantitative ways. For example, the term resilience has been used to describe a system’s general ability to cope with shocks/change, but it also describes the width of a basin of attraction of an equilibrium point in a dynamical system. The term resilience is often used in conjunction with vulnerability to describe the general ability for a community to withstand a shock (or not). | Adverse selection refers to a situation where an individual’s demand for insurance (the quantity of insurance purchased and the probability of a claim) is positively correlated with the individual’s risk of loss (the insurer is more likely to issue a policy to one who needs it most). In other words, those who are most likely to file a claim are often the ones most likely to seek out and purchase insurance. This happens when the insurer does not have as much information about the risk associated with a potential client as the client does. For instance, in the fisheries context, a fisherman who knows they will be fishing in more risky areas or using more hazardous methods might be more likely to seek comprehensive insurance. Adverse selection can distort the insurance market because insurers might set premiums based on average risk, which might not be sufficient to cover the higher-risk individuals. If not managed, it can lead to a situation where insurance becomes too expensive for low-risk members, driving them out of the insurance pool and leading to what is known as a “death spiral” of increasing premiums. |

Glossary of climate adaptation and financial risk management terms.

| Climate adaptation terminology | Financial risk management terminology |

|---|---|

| Vulnerability is a term broadly used to describe how a certain community might be negatively impacted by climate change. There is an equation that defines vulnerability as exposure multiplied by sensitivity divided by adaptive capacity. These additional terms are described below. In this way, the vulnerability of a given actor, group, or community is increased by sensitivity and exposure but reduced by adaptive capacity. | Risk avoidance is simply when people/communities move away from the area exposed to the threat. In the case of fisheries, this could be in terms of geography, when fishers move away from areas affected by marine heatwaves to different fishing grounds, or economically, when fishers change their target species to those not affected by the risk. Risk transfer is when the negative impacts of a shock are transferred to someone else (e.g. an insurance company). This is essentially what insurance facilitates. |

| Exposure to a stressor (e.g. a climate event or trend) can be thought of as being directly analogous to risk, the probability of a stressor/threat/hazard being realized. The greater the risk, the more frequently the community is exposed to the stressor. For example, certain coastal communities are periodically exposed to marine heatwaves, and this directly impacts their vulnerability. Reducing the exposure to a stressor (or reducing the probability of being hit by a shock) is achieved through three means: risk avoidance and transfer. | Insurance is a form of risk management represented by a contractual arrangement called a policy, in which one party is indemnified against financial losses by an insurer. The insurer pools funds across similarly insured parties, who pay a premium to the insurer based on the loss risk. Pooled funds are used to compensate for realized losses. In contrast to traditional insurance, which indemnifies against actual loss, parametric insurance covers the probability of a predefined event triggered by an index or metric. Parametric insurance has a basis risk, which is the risk that the triggered index does not represent the underlying risk exposure. Negative basis risk results when a loss is incurred without the contract being triggered, while a positive basis risk results in a payout without a financial loss. |

| Sensitivity describes the intrinsic properties of the focal element (e.g. a community of fishers) in its ability to withstand a shock. For example, sensitivity to marine heatwaves is increased for fishers dependent on one species that dies during marine heatwaves. Reducing the sensitivity is traditionally through diversification (e.g. change target species for a fisher, change the prey species for a predator, and change the diet for an aquaculture operation). | Reinsurance is a practice in the insurance industry where an insurance company reduces its risk of paying large claims by purchasing insurance policies from other insurers, known as reinsurers. In other words, it is a form of insurance for insurers. Reinsurance allows insurance companies to remain solvent by mitigating the risk associated with underwritten policies. In the event of a significant claim, the insurance company would not bear the entire financial burden but would share it with the reinsurer. This helps ensure that the insurance company has sufficient reserves to pay out claims, especially in times of high-claim events like natural disasters. In a reinsurance contract, the company that purchases the reinsurance pays a premium to the reinsurer, who would then pay a portion of the claims based on the agreement. The original insurer is the ceding company, and the risk passed to the reinsurer is called the ceded risk. Reinsurance can be divided into two types: facultative reinsurance and treaty reinsurance. Facultative reinsurance provides coverage for an individual or a specified risk or contract, while treaty reinsurance covers all or a portion of the risks that an insurance company might encounter. |

| Adaptive capacity describes the ability to cope with a stressor as a result of the extrinsic properties of the system in which the focal element lies. Increasing the adaptive capacity increases the coping range. For example, quite simply, the greater the capital reserves (i.e. money in the bank) that a fisher of aquaculturalist has access to, the better able they are to buy gear and technology and invest in their teams and knowledge, with which to minimize the negative impacts of a shock. | Moral hazard and adverse selection are two key concepts in the field of insurance and economics that refer to situations where the behaviour of one party changes to the detriment of another after a transaction has been completed. Moral hazard term refers to the change in behaviour of insured parties once they are covered by an insurance policy. Essentially, it is the idea that individuals might take on more risk because they know they are insured and that potential losses will be covered by the insurer. For instance, a fisherman with a comprehensive insurance policy might choose to sail during a severe storm or fish in unsustainable ways because they know any damage or loss incurred will be compensated by their insurance company. The problem with moral hazard is that it can lead to an increase in the frequency and severity of claims, which in turn can cause insurance premiums to rise for everyone. |

| Resilience—a broadly used term in both qualitative and quantitative ways. For example, the term resilience has been used to describe a system’s general ability to cope with shocks/change, but it also describes the width of a basin of attraction of an equilibrium point in a dynamical system. The term resilience is often used in conjunction with vulnerability to describe the general ability for a community to withstand a shock (or not). | Adverse selection refers to a situation where an individual’s demand for insurance (the quantity of insurance purchased and the probability of a claim) is positively correlated with the individual’s risk of loss (the insurer is more likely to issue a policy to one who needs it most). In other words, those who are most likely to file a claim are often the ones most likely to seek out and purchase insurance. This happens when the insurer does not have as much information about the risk associated with a potential client as the client does. For instance, in the fisheries context, a fisherman who knows they will be fishing in more risky areas or using more hazardous methods might be more likely to seek comprehensive insurance. Adverse selection can distort the insurance market because insurers might set premiums based on average risk, which might not be sufficient to cover the higher-risk individuals. If not managed, it can lead to a situation where insurance becomes too expensive for low-risk members, driving them out of the insurance pool and leading to what is known as a “death spiral” of increasing premiums. |

| Climate adaptation terminology | Financial risk management terminology |

|---|---|

| Vulnerability is a term broadly used to describe how a certain community might be negatively impacted by climate change. There is an equation that defines vulnerability as exposure multiplied by sensitivity divided by adaptive capacity. These additional terms are described below. In this way, the vulnerability of a given actor, group, or community is increased by sensitivity and exposure but reduced by adaptive capacity. | Risk avoidance is simply when people/communities move away from the area exposed to the threat. In the case of fisheries, this could be in terms of geography, when fishers move away from areas affected by marine heatwaves to different fishing grounds, or economically, when fishers change their target species to those not affected by the risk. Risk transfer is when the negative impacts of a shock are transferred to someone else (e.g. an insurance company). This is essentially what insurance facilitates. |

| Exposure to a stressor (e.g. a climate event or trend) can be thought of as being directly analogous to risk, the probability of a stressor/threat/hazard being realized. The greater the risk, the more frequently the community is exposed to the stressor. For example, certain coastal communities are periodically exposed to marine heatwaves, and this directly impacts their vulnerability. Reducing the exposure to a stressor (or reducing the probability of being hit by a shock) is achieved through three means: risk avoidance and transfer. | Insurance is a form of risk management represented by a contractual arrangement called a policy, in which one party is indemnified against financial losses by an insurer. The insurer pools funds across similarly insured parties, who pay a premium to the insurer based on the loss risk. Pooled funds are used to compensate for realized losses. In contrast to traditional insurance, which indemnifies against actual loss, parametric insurance covers the probability of a predefined event triggered by an index or metric. Parametric insurance has a basis risk, which is the risk that the triggered index does not represent the underlying risk exposure. Negative basis risk results when a loss is incurred without the contract being triggered, while a positive basis risk results in a payout without a financial loss. |

| Sensitivity describes the intrinsic properties of the focal element (e.g. a community of fishers) in its ability to withstand a shock. For example, sensitivity to marine heatwaves is increased for fishers dependent on one species that dies during marine heatwaves. Reducing the sensitivity is traditionally through diversification (e.g. change target species for a fisher, change the prey species for a predator, and change the diet for an aquaculture operation). | Reinsurance is a practice in the insurance industry where an insurance company reduces its risk of paying large claims by purchasing insurance policies from other insurers, known as reinsurers. In other words, it is a form of insurance for insurers. Reinsurance allows insurance companies to remain solvent by mitigating the risk associated with underwritten policies. In the event of a significant claim, the insurance company would not bear the entire financial burden but would share it with the reinsurer. This helps ensure that the insurance company has sufficient reserves to pay out claims, especially in times of high-claim events like natural disasters. In a reinsurance contract, the company that purchases the reinsurance pays a premium to the reinsurer, who would then pay a portion of the claims based on the agreement. The original insurer is the ceding company, and the risk passed to the reinsurer is called the ceded risk. Reinsurance can be divided into two types: facultative reinsurance and treaty reinsurance. Facultative reinsurance provides coverage for an individual or a specified risk or contract, while treaty reinsurance covers all or a portion of the risks that an insurance company might encounter. |

| Adaptive capacity describes the ability to cope with a stressor as a result of the extrinsic properties of the system in which the focal element lies. Increasing the adaptive capacity increases the coping range. For example, quite simply, the greater the capital reserves (i.e. money in the bank) that a fisher of aquaculturalist has access to, the better able they are to buy gear and technology and invest in their teams and knowledge, with which to minimize the negative impacts of a shock. | Moral hazard and adverse selection are two key concepts in the field of insurance and economics that refer to situations where the behaviour of one party changes to the detriment of another after a transaction has been completed. Moral hazard term refers to the change in behaviour of insured parties once they are covered by an insurance policy. Essentially, it is the idea that individuals might take on more risk because they know they are insured and that potential losses will be covered by the insurer. For instance, a fisherman with a comprehensive insurance policy might choose to sail during a severe storm or fish in unsustainable ways because they know any damage or loss incurred will be compensated by their insurance company. The problem with moral hazard is that it can lead to an increase in the frequency and severity of claims, which in turn can cause insurance premiums to rise for everyone. |

| Resilience—a broadly used term in both qualitative and quantitative ways. For example, the term resilience has been used to describe a system’s general ability to cope with shocks/change, but it also describes the width of a basin of attraction of an equilibrium point in a dynamical system. The term resilience is often used in conjunction with vulnerability to describe the general ability for a community to withstand a shock (or not). | Adverse selection refers to a situation where an individual’s demand for insurance (the quantity of insurance purchased and the probability of a claim) is positively correlated with the individual’s risk of loss (the insurer is more likely to issue a policy to one who needs it most). In other words, those who are most likely to file a claim are often the ones most likely to seek out and purchase insurance. This happens when the insurer does not have as much information about the risk associated with a potential client as the client does. For instance, in the fisheries context, a fisherman who knows they will be fishing in more risky areas or using more hazardous methods might be more likely to seek comprehensive insurance. Adverse selection can distort the insurance market because insurers might set premiums based on average risk, which might not be sufficient to cover the higher-risk individuals. If not managed, it can lead to a situation where insurance becomes too expensive for low-risk members, driving them out of the insurance pool and leading to what is known as a “death spiral” of increasing premiums. |

In the absence of insurance and thus the ability to transfer risk, climate shocks have greater impacts on production and profit margins, and the overall adaptive capacity of actors is reduced and their sensitivity to climate shocks increased (Mills, 2005; Falco et al., 2014). These economic losses engendered by marine climate shocks result in less capital to pay for key necessities, including the means to adapt to future shocks. This is particularly important for actors who have limited or no access to credit. Capital reserves are a vital part of an actor’s overall ability to adapt to climate change, for example, by facilitating a transition to new fishing grounds or buying new equipment and targeting different species. As risk exposure increases due to climate change, historical methods of risk management through avoidance and absorption by blue-food actors (Sethi, 2010) will be less effective, as the accrued negative impacts of multiple (and more extreme) climate shocks over time will seriously hamper adaptive capacity. Additionally, government disaster relief is now used regularly to help mitigate the economic impacts of marine climate shocks. However, payments are made many years after the event and cover only a fraction of the costs. In the United States, there is a fear that the current approach to government disaster relief for marine climate shocks will not work in the future (Bellquist et al., 2021). The development and uptake of effective insurance tools that overcome issues relating to moral hazard, adverse selection, and risk pricing to transfer risk and increase adaptive capacity in blue-food sectors is thus a critical challenge and could offer a necessary improvement to government disaster relief for mitigating the impacts of marine climate shocks (Barange et al., 2018; Sainsbury et al., 2019; Turner et al., 2020).

Differences in blue-food sectors

Blue-food sectors cope with climate shocks in a variety of ways (Sethi et al., 2010), depending on the operational nature of the business (e.g. aquaculture vs. wild fisheries), scale of the industry (e.g. commercial fisheries vs. artisan fisheries), the agility of the sector to make changes, value and location of the activity (e.g. proximity to highly productive fishing grounds). The frequency and severity of climate shocks also determines the vulnerability of sectors (Barange et al., 2018). Certainly, the public vs. private nature of many wild-capture and aquaculture stocks respectively is a key determinant of how actors from the two sectors manage the risks they face (which they often share) and how they engage with financial risk management organizations like insurance firms (Fischer et al., 2017). Related is the difference in the (in)ability for risk management organizations (e.g. insurance firms) to confirm stock sizes and losses. These many differences determine which kinds of financial risk management tools can be of use to each sector (or shared across them), and indeed their viability as a tool for mitigating the impacts of climate shocks at all. Below we discuss the major differences between commercial fisheries and aquaculture and the potential usefulness of marine climate shock insurance.

Why is there not more production insurance for fisheries?

Commercial fisheries in the Global North (including those from Australia) have been affected by numerous climate shocks in recent decades (Bellquist et al., 2021; Smith et al., 2021). Over the period 1989–2020, 71 large-scale climate shocks have impacted fisheries in the United States and been classified as federal disasters, amounting to ∼$3.2 billion (2019 USD) in direct revenue losses. For example, in 2015/2016, the highly important Dungeness crab fishery on the United States west coast was closed due to a harmful algal bloom, driven by a multi-year marine heatwave known as the “Blob” (Cheung and Frölicher, 2020). The Dungeness crab fishery accounts for 26% of all annual fishery revenue and supports >25% of all commercial fishing vessels in California alone. California Dungeness crab landings for the 2015–16 season reached only 52% of the average catch of the previous 5 years, with a total value lost estimated at US|${\$}$|97.5 million (Jardine et al., 2020; Frankowicz, 2021). The event attracted $27.3 million in federal disaster relief funding; however, this assistance has been criticized for being ad hoc and unfair in terms of benefit allocation. Critically, financial assistance was only available to fishing communities several years after the climate shock occurred (Bellquist et al., 2021).

In addition to heavily industrialized commercial fisheries in the Global North, smaller-scale fisheries in the Global South have also been heavily impacted by climate and weather extremes (e.g. Sainsbury et al., 2018; Turner et al., 2020). For example, fisheries in Puerto Rico were devastated by Hurricane Maria in September 2017 (Agar et al., 2020; Villegas et al., 2021): the hurricane caused commercial landings to fall by 20% due to the loss of productive assets and power for extended periods and reduced demand; economic losses have been estimated at US|${\$}$|17.8 million; damaged fishing capital (i.e. vessel, engine, and gear) and shoreside infrastructure accounted for 51% of the losses and forgone fishing revenue the remaining 49%. It was not until three years later (2021) that the US Federal Emergency Management Agency (FEMA) announced that it would provide US|${\$}$|1.8 million in grants to fishers in Puerto Rico to help cope with the impacts of the hurricane. Prior to Hurricane Maria, there were >44 fishing villages on the island, whereas by 2021, only around 20 villages operating full- or part-time remained (Agar et al., 2020). The inefficiency and delay in federal emergency funding to support the local fishing industry have failed to reduce the vulnerability of these small communities to climate shocks such as hurricanes, the most intense of which are projected to increase in frequency under climate change (Knutson et al., 2013; Mudd et al. 2014). Marine insurance potentially provides an alternative mechanism (to federal disaster relief) to reduce the vulnerability of these small fisheries to these shocks.

Marine disasters, such as those seen in Chile, Puerto Rico, and the Northeastern Pacific, could be prepared for proactively through insurance rather than reactively through government disaster relief. Disaster relief is usually funded by taxpayers and provides financial support to fishers and seafood farmers who have lost revenue due to a marine disaster. Similarly, but with obvious differences, customers pay premiums to an insurance company, which then provides payouts to those who have suffered a loss. The key differences between the two approaches are the scale at which financial support is maintained and the efficiency of the two programmes. While government relief is a vital component of a country’s resilience to a broad range of environmental disasters, it can take a long time to materialize (Bellquist et al., 2021). This delay in financial support can be detrimental to fishers and fish-farmers, whose financial solvency hinges upon small margins and seasonal timescales. In contrast, financial payouts from private insurance sources have the potential to be much timelier.

A primary challenge in developing insurance solutions for production losses for fishers specifically is the economic uncertainty associated with the harvest of wild fish stocks. Depending on the management institution in place, fisheries are generally considered common pool resources where access is often non-exclusive and competitive, meaning the actions of one fisher can diminish the returns of another (Ostrom, 2008). These properties mean that fish stocks cannot be treated as private goods. The challenge is that insurance policies are generally developed for private goods, where ownership is clear, distinct, and non-rivalrous. In general, it is a challenge to create insurance policies for public goods and/or common pool resources (Quaas and Baumgärtner, 2008). There are examples of wild-capture fisheries production insurance that have overcome this challenge. For example, in Japan, there exists a Fishery Mutual Insurance Scheme whereby fishers make payments into a mutual fund that covers production costs and thus allows fishermen to stay in business in the face of major losses (Hotta, 1999). The programme is essentially a form of a fishery cooperative. Similar “mutual clubs” are found in Norwegian fisheries, and in China, there is a government-backed fishery mutual insurance programme to help fishers pool their risk (Jiang and Faure, 2020). Insurance and risk management organizations, together with fishing communities, are slowly exploring new ways to overcome these challenges and to provide insurance to fisheries operators. For example, a parametric storm insurance programme was recently started by the Caribbean Catastrophe Risk Insurance Facility (CCRIFF SPC, 2023) to help protect fishers from losses associated with hurricanes. These early examples of new insurance offerings presented to fisheries are being supported through umbrella organizations such as the Ocean Risk and Resilience Action Alliance (OSRAA, 2023) and through collaborative programmes between fishers, academics, non-profit organizations, and certain insurance companies.

Production insurance for aquaculture

In contrast to wild-capture fisheries, aquaculture more closely resembles a private good, that is, coastal marine areas that are privately owned or leased to grow seafood. As such, the aquaculture sector has seen growth in the offering and use of insurance to protect against various perils, including adverse environmental effects on productivity and infrastructure, as well as disease outbreaks (see the Global Aquaculture Insurance Consortium; GAIC, 2023). However, the use of insurance by aquaculture operators is still small relative to agriculturalists, and it is a financial risk management tool used primarily by large operators, with most small to medium-sized aquaculture operations are uninsured, leaving them exposed to numerous risks (Secetan, 2008). Even with present insurance policies, marine climate shocks can be detrimental to aquaculture operations. For example, in recent years, harmful algal blooms driven by anomalously warm ocean conditions have led to large negative impacts on several large-scale aquaculture operations (Díaz et al., 2019; Brown et al., 2020). For example, in 2016, the convergence of extensive blooms of two harmful algae species in Chile led to the most catastrophic event in Chilean aquaculture to date. The event, known as the “Godzilla-Red tide”, was linked to strong El Niño conditions and the positive phase of the Southern Annular Mode and caused the largest fish farm mortality ever recorded worldwide (Trainer et al., 2020). This resulted in an export loss of ∼US|${\$}$|800 million, which, when combined with shellfish toxicity, led to major social unrest and rioting in coastal communities. Even with insurance, the large international salmon aquaculture firms that operate in Chile were exposed to heavy economic losses, with subsequent impacts on the global supply and price of salmon (Terazono and Mander, 2016).

The environmental risks that aquaculture operations are exposed to, including harmful algal blooms, disease outbreaks, changes in water quality, and extreme weather events, are difficult to predict and control, making the pricing of insurance coverage challenging. Furthermore, the relative novelty of commercial-scale aquaculture, compared to the various forms of agriculture, means there is less historical data available for insurers to use in risk assessments and pricing decisions. The lack of data can increase uncertainty, leading to higher premiums and, thus, lower take-up by aquaculture operators. Last, the uncertainty surrounding stocking levels adds another layer of complexity. It is often difficult to verify the number and health of product in an aquaculture operation accurately. If insurers cannot be certain of the volume and quality of the product being insured, this creates additional risk, which can drive up premiums or lead insurers to limit coverage. Addressing these constraints will require collaborative efforts by stakeholders in the aquaculture industry, including producers, researchers, government agencies, and insurers. Improved data collection, better biosecurity measures, and the development of more resilient strains of fish and shellfish could all help reduce risk and uncertainty, making it easier for insurers to provide affordable coverage. Importantly, the development of innovative insurance products, such as parametric insurance, which pays out when certain parameters are met rather than requiring proof of loss, could also play a role in expanding coverage options. While aquaculture is the fastest-growing food production sector globally, expanding rapidly in recent decades, most existing insurance solutions are still used only by the larger aquaculture firms that can afford the high premium rates. There remains a significant challenge for most aquaculture operations worldwide, which typically are small-scale operations in the Global South (Zheng et al., 2018).

General challenges associated with blue food production insurance

Any use of insurance faces several challenges. For blue foods specifically, the absence of quality data with which to quantify and price risk and methods to attribute a specified loss to a particular climate shock (Kaplan et al., 2016; Siedlecki et al., 2016; Malick et al., 2020; Norton et al., 2020) is one such challenge. Risk is a much-discussed quantity (Haimes, 2009), and “pricing risk” in the context of insurance refers to the process of determining the premium that an insurance company will charge for covering a specific risk. The premium is the price that the insured party—in this case, a blue-foods sector actor like a fisherman—pays for the insurance coverage. This process involves quantifying the potential financial loss that might result from the risk, along with the likelihood that the risk event will occur. Different types of insurance policies will have different methods of pricing risk. For example, in car insurance, the insurer might consider factors such as the driver’s age, driving history, the type of car, and the location where the car is typically driven. To price risk effectively, insurance companies rely heavily on statistical and actuarial analyses, where mathematical models and historical data are used to predict the likelihood of an insured event occurring, the potential cost if it does occur, and how many policyholders will make a claim. In the context of fisheries and, to some extent, aquaculture, there remains a challenge to accurately price the risk of specific climate shocks. One limitation is that observations of ocean properties such as temperature, oxygen levels, and nutrient availability, and importantly, the climate shock events themselves are simply not available for long enough periods and for all locations. Teleconnections between spatially distant parts of the ocean and the role of the atmosphere in driving these events are complex (Okamoto et al. 2020), and it remains an active area of research to make accurate forecasts of these events weeks to months ahead at spatial scales relevant to blue food production from fisheries and aquaculture (Hobday et al., 2018). At longer timescales, the impacts of climate change on the world’s oceans are difficult to quantify at these same scales. Similarly, attributing a drop in fishery or aquaculture production to a specific marine shock is challenging. Coastal systems have open ocean boundaries and so are exposed to both local risks and risks originating elsewhere. In the case of wild fisheries, animals can move and interact with other species or, more importantly, a multitude of stressors (McClanahan et al., 2014). Impacts on a particular marine system may not always be visible in the way that the effects of a hurricane or drought are obvious on land. These all complicate the attribution of direct revenue losses in marine systems to a given climate shock. However, the accuracy of ocean forecasts, understanding of causal pathways, and our ability to predict fish population dynamics and fisheries/aquaculture production are improving (e.g. Siedlecki et al., 2016; Tommasi et al., 2017; Malick et al., 2020), with great scope for use in future insurance applications.

Another factor playing a role in the viability of insurance in fisheries and aquaculture to date, is related to the health of marine ecosystems from which blue foods are extracted and the overcapitalization of these industries in some regions. Historically, there are numerous examples from around the world of poorly managed fisheries with unsustainable effort levels (Costello et al., 2010; Teh et al., 2013). In these cases, employing financial mechanisms to boost the economic resilience of seafood producers can lead to further degradation of marine ecosystems, and thus threaten the long-term economic viability of these industries. The reduction or cessation of fishing because of a climate shock may actually improve ecosystem health for a short period of time (perhaps similarly to the 2020 pandemic; Bennett et al., 2020), however the chronic issues of overcapitalization and poor management will persist. Government support is often necessary to initiate an insurance scheme (Mills, 2005), and it is possible that governments tasked with balancing both the economic productivity of coastal communities and ecosystem health, are reluctant to increase the resilience of these maladapted marine systems. Conversely, if a fishery is well managed, creating financial tools like insurance to keep fishers working is acceptable (Hodgkinson et al., 2014). We argue that it is only in marine regions where sustainable fisheries management exists that insurance can be deployed to effectively achieve both economic and environmental wins.

In and around these issues specific to marine systems, insurance itself has several core challenges, specifically moral hazard and adverse selection (Mills, 2005; Müller et al., 2017; see the Table 1 for a description of the major terms used in financial risk management). Moral hazard describes unintended risk-seeking and perverse behaviours that insurance can engender. For example, in the case of car insurance where a policyholder does not lock their car because they are covered if their car is stolen. To manage this moral hazard, the insurer will often stipulate that the car must be locked in order for the cover to be valid. In another example, pastoralists have traditionally employed a range of risk management techniques, notably farming a diverse portfolio of crops. However, when insurance is held, farmers will often start farming monocultures in the knowledge that should their crop fail, they will receive a payout (Müller et al., 2017). A similar attitude could potentially be adopted in fisheries if insurance were made available, where fishers who would typically rely on a diverse catch portfolio (Kasperski and Holland 2013; Fuller et al. 2017; Klein et al. 2017; Nomura et al. 2022) to minimize income risk end up targeting a single species, knowing that they have insurance to back them up should that one fishery fail. Another way in which moral hazard manifests is in terms untruthful claims. For example, if insured, a fisher could claim a loss of a specific line of revenue when no actual (environmentally created) loss occurred. Verifying truthful losses due to a specific risk can be highly costly for insurers (Miranda and Farrin, 2012).

Another major challenge with insurance is adverse selection, which describes a situation where an individual’s demand for insurance (either the propensity to buy insurance or the quantity purchased, or both) is positively correlated with the individual’s risk of loss. In simple terms, adverse selection occurs when people who believe they have a higher risk of needing insurance are more likely to buy it. For example, a person who knows they are in poor health may be more likely to buy life insurance. The insurer, on the other hand, may not have access to this information or may not be able to use it due to legal or ethical restrictions (Handel, 2013). This asymmetry of information between the insurer and the insured can lead to a higher-than-expected claim rate, as the pool of insured individuals is riskier than originally presumed. In turn, this can force insurers to raise premiums, which can result in a situation where only those who expect to claim insurance are the ones buying it. Adverse selection can lead to a form of market failure known as a “death spiral.” As insurance becomes more expensive, only those who are most likely to need it will buy it, which in turn forces the price up even further. Eventually, the price may become so high that no one can afford the insurance, leading to market collapse.

Cooperative and parametric insurance as potential solutions

Insurance solutions for fisheries and aquaculture that minimize the risk posed by marine climate shocks could take many forms, including indemnity insurance and parametric insurance. Indemnity insurance is the most common form of insurance, where the insured (e.g. a fisher) pays a premium to the insurer (i.e. the insurance company) for the policy, and in return, the insurer pledges to pay the insured a certain sum of money should a loss occur (i.e. similarly to everyday-type insurance, such as car or home insurance). In this case, the nature of the loss must be specified and verified. Specifically, where a fisher has suffered a loss in revenue, this loss must be attributable to a climate shock (such as a marine heatwave) for indemnity insurance to be viable. As we have discussed, this can be very difficult for wild fisheries, as many factors, in addition to the climate shock can contribute to the loss of revenue. In aquaculture, it is easier to assess the direct impact of a climate shock on production, and consequently, various forms of indemnity insurance are presently available to the sector in certain parts of the world (Beach and Viator, 2008; Barange et al., 2018). The verification that a loss has occurred is however contentious and expensive, with a large fraction of the costs of operationalizing an insurance product arising from monitoring and verification. The contentious nature of loss verification and the costs of monitoring are the main challenges that limit the take-up of indemnity insurance programmes in economically vulnerable communities (Miranda and Farrin, 2012).

Another form of insurance is parametric insurance (otherwise known as index insurance; Maltby et al., 2022). Parametric insurance policies provide a payout from the insurer, triggered by an objective measure of a correlate of losses (i.e. an environmental index). For example, a parametric insurance policy would include an automated payout of some amount to an insured party (i.e. a fisher or aquaculture operator) when some critical environmental threshold is exceeded (e.g. prolonged sea surface temperatures above some level). Very recently, new parametric insurance policies have been offered to blue food producers; for example, the Caribbean Catastrophic Risk Insurance Facility (CCRIF) uses parametric insurance to protect fishing communities from storms. The advantages of parametric insurance over traditional indemnity insurance are greatly reduced costs, as verification is not required, and more timely payouts, as actual losses are not required to be verified post-event. However, the main challenges with parametric insurance relate to the dimensionality of the environmental index and its error with losses—this is called basis risk. Fisheries and aquaculture production is influenced by many factors (e.g. ocean temperature, oxygen levels, and disease risk), and as a result, so is revenue. This multidimensionality means a simple environmental trigger (e.g. high ocean temperatures) will often not be adequate, which can be confusing for both insurers and the insured. While there are several approaches for accounting for multiple environmental factors (e.g. sophisticated statistical and machine learning methods), marine parametric insurance is likely to be complicated, which makes it difficult for the insured to understand the product, which can again lead to contention over claims (Maltby et al., 2022). However, while this is most probable at the individual level, if the policyholder is at the sovereign/national level, this is less likely to be an issue.

Basis risk can lead to inefficiencies in the parametric insurance policy that can greatly diminish its uptake by potential customers. Errors in the index-loss relationship can lead to situations where a payout is made because the environmental index was triggered but no losses occurred. The converse problem occurs when losses are experienced but no payout is made. A solution to this is to verify losses, but this leads to the same cost issues that limit the scope of traditional indemnity insurance. Basis risk is the main constraint limiting the applicability of parametric insurance to the blue-food sectors. However, as fisheries and aquaculture productivity datasets and ocean observations grow, coupled with technology advances such as machine learning in environmental prediction (e.g. Lee and Lee, 2018; Fleming et al. 2021), these index-loss relationships can be refined to better model the economic impacts of marine climate shocks on these sectors.

Insurance is typically thought of a contract between an individual and an insurance company, but it can also involve a collective/cooperative or risk-pool more generally (Tilman et al., 2018; Santos et al., 2021). A risk-pool cooperative is where a group of insured (e.g. fishers) form a group, which then engages as a collective with insurers. The cooperative can take the role of the insurer, paying for small losses, for example, with the insurance company acting as the reinsurance company, funding the cooperative should a large risk be realized that affects all members of the cooperative. In essence, the cooperative forms a mutual insurance association, where members pay premiums into a mutual fund, and in the event of a loss, compensation is paid out from this fund. Any surplus at the end of the year may be returned to the members in the form of dividends or retained for future claims. For instance, this is how, in the United States, the Nationwide Mutual Insurance Company began as a mutual insurer for farmers from the state of Ohio in 1926. Cooperative parametric insurance schemes also exist, and these are innovative risk-sharing mechanisms are increasingly used in smallholder agriculture systems in developing countries. They involve insurance payouts being triggered not by individual loss assessments but when an environmental index for the region in which the cooperative exists passes a threshold (Trærup, 2012). The R4 Rural Resilience Initiative, for example, uses this model to provide insurance to smallholder farmers in Ethiopia, Senegal, Malawi, and Zambia. Insurance cooperatives and mutual fund associations have several attractive aspects. First, as a cooperative, social norms can help manage issues relating to moral hazard and adverse selection. Second, marrying an insurance policy to existing social capital greatly increases the chance of uptake of the insurance policy. Third, as a cooperative, groups of insured (i.e. fishing communities) have more leverage with insurance companies and can secure lower costs for their insurance. However, a question remains over the necessary size of an insurance cooperative. Small local mutual fund associations can consist of a small set of individuals, perhaps a few dozen members. In contrast, the R4 Rural Resilience Initiative includes thousands of farmers over several countries. The exact number will likely be determined by those individuals who are willing to pool their risks and resources and to trust each other to manage those resources effectively and fairly.

Various management regimes are specifically designed to nurture cooperative behaviour among fishers. These frameworks facilitate effective risk pooling and contribute to promoting sustainable resource management. Key among these are Community-Based Fisheries Management (CBFM), co-management approaches, Individual Transferable Quotas (ITQs), and Territorial Use Rights for Fisheries (TURFs). CBFM promotes the involvement of local communities in managing and conserving their fisheries resources, thereby fostering cooperation among fishers. Co-management approaches share the responsibility of managing fisheries between local fishing communities, governments, and other key stakeholders. ITQs and TURFs provide exclusive rights to fish, which can stimulate cooperation and responsible resource management (Costell et al. 2008). The success of cooperative self-insurance relies heavily on the existence of certain enabling conditions that smooth the way for the establishment, management, and long-term viability of these risk-sharing initiatives. Foremost among these conditions are trust and social capital among fishers, which form the backbone of cooperative self-insurance. A robust organizational structure is required to manage the collective resources, distribute payouts, and enforce rules. Basic financial literacy and risk management principles are crucial for fishers to make informed decisions and manage their pooled resources effectively. A conducive legal and regulatory framework is also key to enabling these cooperatives form and persist.

Governments have a substantial role to play in promoting cooperative self-insurance among fishers and creating an environment conducive to private solutions for managing marine climate shocks. This is how the Japanese, Norwegian, and Chinese fisheries have organized mutual insurance programmes to help their fishers manage environmentally driven losses (Hotta, 1999; Jiang and Faure, 2020). By crafting supportive policies and legislation, governments can pave the way for these initiatives. They can offer technical assistance and capacity-building programmes to equip fishers with the knowledge and skills needed to establish and manage cooperative self-insurance initiatives effectively. Governments can also facilitate access to pertinent data and cutting-edge technology. Encouraging collaboration between various stakeholders, such as insurance companies, research institutions, and non-governmental organizations, can lead to innovative private solutions to marine climate shocks. By setting the stage for cooperative self-insurance, governments can empower fishers to assume greater control over their risk management, fostering sustainable resource management and long-term climate change adaptation.

Another role that the government can play is in the provision of subsidies (Müller et al., 2017). Premium prices for indemnity or parametric insurance can be beyond what a potential purchaser could afford, and who may lack the extra income required to pay the recurring costs of an insurance premium. This is the case for many sectors across many of the most vulnerable communities around the world. For example, this challenge is present in insurance designed for small-holder farms in sub-Saharan Africa and India (Miranda and Farrin, 2012). How then do these communities (who are in most need) afford insurance? Government subsidy can support communities proactively by paying for (some fraction of) premiums or offering tax credits, for example, rather than through retrospective disaster relief say. The increasing engagement of NGOs through financial instruments (Shiiba et al., 2021) is another potential funding source that can potentially initiate a climate-shock insurance programme. Crowdsourced and micro-lending platforms are also popular methods of aggregating public support for commercial activities in developing nations (Clarke and Grenham, 2013) and could offer another route by which new insurance policies are made affordable to fishers and aquaculturalists.

Looking to the future

Equitable resilience

The complex nature of income landscapes for coastal communities is also important in the design of insurance tools that provide resilience to climate shocks across the spectrum of actors that work in the blue foods industries. Low-income workers such as deckhands and fish-process factory workers tend to work several jobs, many of a seasonal nature (Mishra et al., 2013; Wiederkehr et al., 2019). This is a key example of adaptive capacity, that is, should income from one job cease, there are other jobs to maintain a living. Insurance must be carefully designed to not reduce this natural form of adaptive capacity and, thus, the diversity of employment in coastal communities. Just like small-holder farmers who move from cultivating a diverse set of crops to harvesting monocultures once insurance was available (Müller et al., 2017), insurance deployed for marine climate shocks could engender similar behaviours. Broadly applicable and scalable insurance programmes for coastal communities could also promote the collapse in income diversity across sectors. It is important to ensure that insurance can provide economic resilience not only to the individuals that buy insurance policies but also to the sectors that they work in. This may otherwise lead to inter-sector issues. For example, if insurance against marine climate shocks were only to be made available to the aquaculture sector, a migration of labour from wild-capture fisheries to the aquaculture sector may occur simply because the jobs are more stable (as a direct outcome of the insurance). Reducing the diversity of industries supporting coastal communities can lead to lower resilience overall to climate shocks. In general, it is important to recognize the connectivity of supply chains: risks at the base of a supply chain (i.e. in terms of the supply of blue foods) will propagate up through the fish-processing plants, the distributors, the retailers, and ultimately the consumer (Davis et al., 2021). Protecting the base of blue food supply chains using insurance designed for climate shocks will help increase the resilience of entire blue food supply chains, and hence the coastal communities more broadly defined, to climate change.

It is important to acknowledge that the diversity of the blue food industries that coastal communities engage in is much greater than just commercial fisheries and aquaculture (Fisher et al., 2021). Marine tourism and recreational fisheries are also important alternative or main livelihoods for people in coastal communities, and they also rely on access to healthy and abundant marine species and habitats. Disruption of tourist activities such as diving, fishing, whale watching, and visits to seabird and marine mammal colonies can occur because of marine extreme events. Coral bleaching because of marine heatwaves disrupted national (e.g. the Seychelles) and regional (e.g. the Great Barrier Reef) economies, with individual operators idle as tourist visitation was reduced. Cyclones damage both habitats and infrastructure and disrupt tourism businesses for some time after the event. For example, the Tropical Cyclone Winston led to nearly F|${\$}$|600 million in losses in Fiji due to changes in the economic flows of the production of goods and services, with F|${\$}$|120 million from lost tourism alone (Mansur et al., 2017). Traditional insurance products may cover losses to infrastructure (e.g. damage to boats), but not to loss of amenity due to environmental damage. Furthermore, federal disaster relief payments rarely cover the period of lost income following an extreme event for marine tourism operators (Bellquist et al., 2021).

Climate change, disaster relief, and reinsurance

Another important challenge in designing financial risk management tools like insurance, for protecting blue-foods actors from climate shocks is long-term climate change. The non-stationarity in the earth system means that the frequency and intensity of marine climate shocks are going to change over time, in many cases increasing in both ways, and so any insurance policies must adapt and change accordingly through risk adjustments (O'Neill et al., 2017). Risk adjustments are when insurers modifying insurance premiums or coverage based on the level of risk associated with the insured individual or entity, and it is commonplace in most applications of insurance; however, it is yet to be determined how frequently a marine insurance policy, designed for today's conditions, would need to be updated in the future. In addition, the magnitude and frequency of certain climate shocks (e.g. marine heatwaves) are likely to increase nonlinearly under climate change (Hobday et al., 2018; Hobday and Pecl, 2014). For example, there may be step-changes in the frequency of harmful algal blooms driven by marine heatwaves. Additionally, marine food webs are known to exhibit non-linear dynamics such as regime shifts, and a slight increase in the frequency or intensity of a marine climate shock can lead to large changes in the productivity of fisheries or aquaculture. These non-linear changes in productivity resulting from climate change and shocks will likely mean that insurance premiums will need to be adjusted regularly.

This is not necessarily bad; the rising cost of insurance is often used as an indicator that alternative risk management measures should be taken. In many cases of climate shocks, the long-term alternative might be to take relatively drastic action, for example, moving to locations where risks are lower (Sethi, 2010; Selden et al., 2020). This may or may not be an option for some actors. Insurance can help actors conserve capital reserves as they are hit by climate shocks, which can then bolster their adaptive capacity, ultimately helping them transition to new locations or sources of income should climate change be detrimental to a particular way of life.

A related concern is that in the face of long-term climate change, insurance may serve to prop up failing industries. Many marine species ranges are shifting spatially (Pinsky et al., 2020), and at some point, certain species will no longer be found in areas that have been historically fished (Seldon et al., 2020). For some communities, the extra fuel costs for tracking these shifting distributions mean that this fishery will not be a viable option in the future. In this case, insurance may encourage fishers to continue working in this fishery rather than incentivizing a gradual shift away to a more viable alternative such a different local fishery. Delaying a move to another source of income could be more harmful than if fishers were left to be exposed to income shocks early in the absence of insurance. The key here is to implement insurance mechanisms that provide economic resilience in the near term, combined with support mechanisms for long-term planning. Migration of populations from coastal zones that are at high risk of impacts from sea level rise is termed “managed retreat” (Hauer et al., 2020). In terms of the production of blue foods and marine climate shocks, we can imagine a similar process to managed retreat, but in terms of income landscapes, where insurance helps people move to other sources of income or move into other fisheries.

This challenge will be confronted by insurers too. As the risk profiles of blue food producers change, the viability of certain insurance contracts may reduce to such a point that the insurer, for example, a private insurance company, will cease offering the insurance product. Government subsidies and support from non-traditional sources such as NGOs could play a role here. Indeed, the insurer could be the government itself, and as we have discussed, (parametric) insurance could take the role of disaster relief for mitigating the impacts of climate change. However, there remain several questions over whether blue foods operators would accept a switch from disaster relief, which is free, to an insurance policy, which would have a cost in its premium. Economic research is required to better understand whether a higher frequency and lower delay in payments from insurance, which comes at a cost, would be more attractive than infrequent and very delayed disaster relief that is free. One benefit of the government being the insurer is its scale. Marine climate shocks are correlated over large spatial scales, and as such whole regions may be impacted at the same time. This challenge can deplete the capital reserves of the insurer unless there is reinsurance. Reinsurance is insurance for the insurer, and just like in agricultural insurance around the world, reinsurance will have to play a central role in the development and implementation of marine climate shock insurance.

Implementation: from concept to creation