Abstract

Compensation of mutual fund managers is paramount to understanding agency frictions in asset delegation. We collect a unique registry-based dataset on the compensation of Swedish mutual fund managers. We find a concave relationship between pay and revenue, in contrast to how investors compensate the fund company (firm). We also find a surprisingly weak sensitivity of pay to performance, even after accounting for the indirect effects of performance on revenue. Firm-level fixed effects, revenues, and profits add substantial explanatory power for compensation.

Received April 25, 2017; editorial decision August 21, 2017 by Editor Matthew Spiegel. Authors have furnished supplementary code, which is available on the Oxford University Press Web site next to the link to the final published paper online.

Mutual fund research has long taken a prominent role in finance, not only because a large and growing number of investors delegate their investments in risky assets to fund companies, but also because they offer a unique laboratory in which to test theories of incentive provision, performance evaluation, and information acquisition. Indeed, few areas of the financial sector have better quality data on prices (fund returns) and quantities (portfolio holdings and investor fund flows) to test such theories. One major piece of evidence has been missing, however: data on manager compensation. In its absence, empirical analysis has focused on the relationship between mutual fund investors and funds. It has analyzed how investors pay for the services of a fund—the management fee is typically a fraction of assets under management—and how sensitive investor flows are to fund performance. But fund companies delegate the actual management of the funds to employees, fund managers.

Little is known about the nature of the compensation contract between owners (firms) and managers, and even less is known about the actual compensation managers earn. The implicit assumption in the literature has been that there are no frictions in this second layer of delegation. This paper collects a unique data set on mutual fund manager compensation to shed light on the determinants of manager compensation. The goal is a better understanding of the economic relationship between the firm and the managers it employs. This relationship, in turn, is important for investors delegating their assets to such funds.

We find a lower sensitivity of pay to manager-level assets under management (AUM), compared with the fixed fraction of AUM typically charged by funds. Second, we find weak sensitivity of pay to performance. Third, we show that firm-level characteristics, which are typically ignored in the literature, add substantial explanatory power for manager compensation.

We start from Morningstar data on the universe of mutual funds sold in Sweden, an economy with a highly developed mutual fund industry. We link the names and tenure of the individuals managing funds to tax records. The tax records provide annual labor income (which includes bonus payments) and other forms of compensation, but also give access to their demographics, education, and financial income. For each manager and year, we connect compensation to the assets under management and to the return on that manager’s portfolio of funds. This novel data set provides a unique vantage point from which to study the determinants of manager compensation and the interplay between the fund manager and the firm that employs her.1

In the mutual fund industry, the predominant contract between investors and funds is one where fees are proportional to assets under management.2 The first result shows that while there is a strong relationship between the labor income of the manager and the size of the funds under management, the relationship is concave. Our main specification estimates a regression of log manager pay on log manager revenue, a natural measure of size. We find an elasticity of compensation to revenues of 0.15. A 1% increase in revenues generated by this manager increases her compensation by 0.15%, implying there is far from complete pass-through of fund revenues to managerial compensation. The 0.15 point estimate implies that a 1% increase in revenue lowers the manager’s share of revenue by 0.85%. The differential impact of changes in AUM on fund revenues and managerial pay provides evidence on how surplus is shared, and highlights the importance of better understanding the agency conflicts between fund managers and owners, and their relative bargaining power (Das and Sundaram 2002).

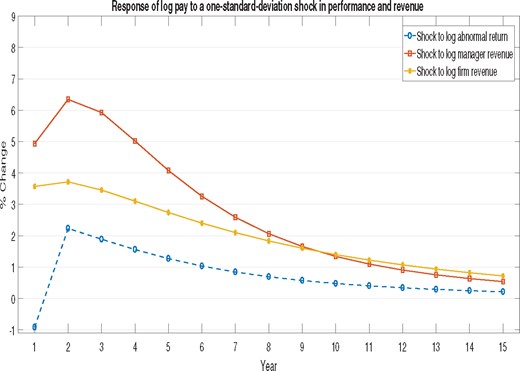

Theory suggests that a component of a fund manager’s pay should be directly tied to return performance, especially when there is uncertainty regarding managers’ ability.3 Our second result indicates that the relationship between pay and performance is quite weak. We define the abnormal return on a fund as the gross (before fees) return in excess of the benchmark as stated in the fund’s prospectus. A one cross-sectional standard-deviation increase in abnormal return performance increases compensation by 3.0%, nearly 10 times less than a one-standard-deviation increase in revenue. This modest relation is mostly driven by talented managers on average generating higher returns and earning higher labor income rather than time-series variation for a given manager. Considering longer evaluation periods and dynamics increases the strength of the link between performance and subsequent pay.4 However, the economic magnitudes remain modest. The pay-performance sensitivity (PPS) increases once the components of revenue that are correlated with current and past abnormal returns, such as fund flows, are accounted for. Even then, the PPS remains economically small. The component of revenue that is unrelated to past fund performance remains the dominant driver of pay. Managerial fundraising skill, advertising, and broker-intermediated flows could all be related to this non-performance-driven revenue component.5 The modest magnitude of the PPS is instructive for theory going forward, as models of delegation evolve toward predicting quantities as well.

Mutual fund companies manage multiple funds. This raises the possibility that manager pay depends not only on the revenue and performance of the funds she is responsible for but also on the revenue and performance generated by other funds in the same fund family (firm). Our analysis uncovers, first, that there are systematic pay differences across firms. Second, the sensitivity of manager compensation to firm revenue is comparable to that of manager revenue. Third, firms with higher profits pay significantly more. At the same time, profitability lowers the sensitivity of compensation to manager revenues and increases that to performance. This evidence is consistent with a compensation package that contains one component that depends on manager-level revenues and another component that comes out of a firm-wide bonus pool. This bonus pool only exists when the firm makes a profit. Pay-for-performance is only present in profitable firms, but even there plays a small role in determining compensation. By emphasizing the impact of fund family revenues and profits on managers’ pay, we contribute to the literature on the role of the fund family.6

Our results are robust across investment categories and hold for a variety of other measures of performance employed in the literature. They hold when we extend our definition of pay to include dividend income as well as partnership income of the fund managers. When we allow for nonlinearities in the pay-for-performance relationship, we find some evidence that superior performance increases pay, but the higher impact on pay remains economically modest. Finally, our results are similar whether or not we include transitions out of the mutual fund industry, across firms in the industry, and across funds in the same firm.

The newly gained evidence can help direct and better tailor research striving to understand the role of fund families in portfolio delegation and the intricate interplay between the firm, the managers it employs, and the fund investors. Our evidence highlights the limitations of considering managers in isolation from the fund family they work for. Managers are an integral part of a fund family, and their incentives will be shaped not only by how well they manage their own fund, but also by how they integrate within the rest of the family and the corporate culture. Consequently, intra-fund family incentive frictions will influence managers’ allocation decisions. A careful evaluation of managerial skill should account for such externalities. Our evidence should be valuable not only for theories of mutual fund management but labor economics more broadly.

1. Data and Measurement

1.1. Sweden: A good laboratory

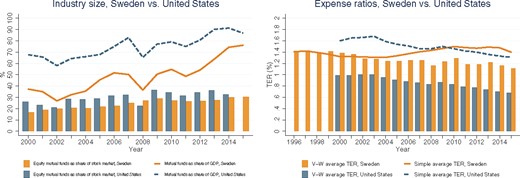

In addition to having unique data on compensation of mutual fund managers, the Swedish setting constitutes a good laboratory to investigate the mutual fund industry. Sweden has one of the deepest and competitive mutual fund sectors in the world. The size of the total mutual fund industry’s AUM relative to gross domestic product (GDP) is one of the highest in the cross-section of countries. Khorana, Servaes, and Tufano (2005) surveyed 58 countries in 2001. According to their data, Sweden’s mutual fund industry represents 31.1% of GDP, ranking 8th out of 58 countries. Moreover, since 2001, the Swedish mutual fund industry has grown tremendously. By 2015, Sweden had almost caught up with the United States in terms of AUM/GDP, as shown in Figure 1. Khorana, Servaes, and Tufano (2005) also calculate the ratio of the AUM in equity funds to the stock market capitalization. For Sweden, this ratio is 23.1% in 2001, ranking it 12th out of 58 countries. The bars in Figure 1 show the evolution of the equity mutual funds’ AUM to stock market capitalization ratio over the previous decade in Sweden and the United States. According to this metric, the Swedish fund industry has also grown tremendously, and is similar in size to that of the United States.

Size and fees of the Swedish mutual fund industry

Data for the United States are from the 2014 Investment Company Factbook and the National Income and Products Accounts. Data for Sweden are from the Swedish Mutual Fund Industry Association and Statistics Sweden.

Sweden also is representative in terms of fund return performances and fees charged in the cross-section of developed countries. Ferreira et al. (2012) study 28 countries from 2001 to 2007. They show that fund performance, measured by quarterly raw returns (1.93%), one-factor alpha (|$-0.80%$|), or four-factor alpha (|$-0.83%$|), in Sweden is close to the cross-country averages (2.07%, |$-0.47%$|, |$-0.60%$|). Flam and Vestman (2017) confirm that Swedish fund alphas are close to their U.S. counterparts. Percentage annual fees of 1.38% are also close to the cross-country average of 1.29%. Figure 1 plots the time series for the total expense ratio (TER) over a longer and more recent sample, again comparing the United States to Sweden. The lines plot equally weighted averages across funds, while the bars plot AUM-weighted averages. Sweden has comparable fees to the United States, especially on an equally weighted basis. The evidence is consistent with Sweden having a competitive mutual fund sector in the international context.

A third piece of international evidence comes from the flow-performance relationship. We confirm in our data (see Appendix C) the strong flow-performance relationship found for Sweden by Ferreira et al. (2012). These authors show a stronger flow-performance relationship in eight countries, including Sweden, than the one for the United States first established by Sirri and Tufano (1998). The convexity of this relationship can result from misspecification of the fractional flow model Spiegel and Zhang, 2013. Our work does not rely on the nature of the flow-performance relationship.

A final piece of evidence speaks to the competitiveness of the market for skilled labor in Sweden. Adams, Keloharju, and Knupfer (2016) study CEO pay in Sweden. Their Figure 2, panel B, shows an elasticity of CEO pay to firm assets of 0.27. They note that this estimate is quite close to the 0.3 estimate reported for U.S. firms. The pay specification they use is the same we employ below, and follows from the assignment model of Gabaix and Landier (2008). This is evidence that the pay culture for skilled labor in Sweden may not be very different from that in the United States. As we show below, Swedish mutual fund managers have an elasticity of pay to revenue that is only half as high as that of Swedish CEOs.

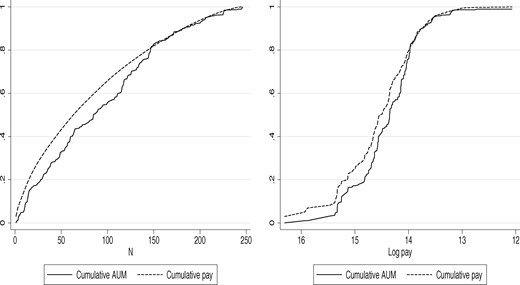

Cumulative labor income and assets under management by income

Both panels plot the cumulative fraction of labor income expressed as a fraction of total labor income paid (dashed line), and cumulative assets under management, expressed as a fraction of total AUM (solid line) for all managers in the last year of our sample, 2015. Managers are ordered from highest to lowest pay on the horizontal axis. The left panel plots the number of managers on the x-axis, while the right panel plots the log pay.

1.2. Three hierarchical levels of data

Our data set has three hierarchical levels: mutual fund companies, which we refer to as firms, mutual funds, and fund managers. This section describes how we measure returns, revenues, and compensation at these various levels of aggregation.

From Morningstar Direct, we obtain the universe of open-ended mutual funds that are available for sale in Sweden or in the Nordic countries. The sample period is from January 1994 until December 2015. The sample includes both active and no longer active funds. The mutual funds have inception dates between 1975 and 2014. We eliminate all funds that have Region of Sale equal to Global Cross-Border or European Cross-Border because those are funds that do not have local operations in Sweden. The sample contains 1,744 funds that belong to 182 fund companies, identified by Morningstar’s variable Firm Name. Some fund companies are subsidiaries of a larger unit, the fund complex, identified by the Morningstar variable Branding Name. Often, the various fund companies in a fund complex operate in different Nordic companies.7 The 182 fund companies form 126 complexes.

Morningstar Direct provides the manager history for each fund. The history contains the first and last names of each manager with a start date and end date. This generates 10,123 non-missing fund manager-year observations for 1,600 funds.8

What makes our data set unique is that we match the managers to their social security numbers, using publicly available sources. This is what allows the match to the tax records that contain the manager income data. We describe the matching procedure in detail in Appendix A.1. For 670 fund managers’ names, we do not find a (reliable) match with a social security number. Many of these names are Finnish, Danish, or Norwegian and likely stem from the inclusion of Nordic cross-border funds. These fund managers are not Swedish taxpayers and do not have a Swedish social security number. For common manager names, we obtain several candidate social security numbers. Based on age, industry, and occupation, we are often able to identify the correct individual. In some cases, too many candidates remain, and we drop such many-to-one matches. Our final estimation sample contains 2,898 fund manager-year observations pertaining to 945 funds and 531 fund managers.

1.2.1 Fund level.

We denote by |$R^{\it gross}_{\it it}$| mutual fund |$i$|’s gross return in month |$t$|. The net return |$R^{net}_{\it it}$| is the gross return minus the total expense ratio, denoted by |${\it TER}_{\it it}$|. |$R^B_{\it it}$| is the fund’s benchmark return. This can be either the return on the benchmark stated in the prospectus or the return from a factor model. We denote by |$R^{\it abn}_{\it it}$| the abnormal return, defined as the return of the fund over the benchmark return before expenses. The fund earns fee revenue (|${\it REV}_{\it it}$|) equal to the product of assets under management at the end of last month times the total expense ratio (annual TER/12). The value added (|$V_{\it it}$|) is defined as in Berk and van Binsbergen (2015) as the product of the AUM of the fund at the end of last month (|${\it AUM}_{it-1}$|) times the difference between the gross return and the benchmark return. Net value-added takes out fund revenue from (gross) value added.

Following the literature, we eliminate money market mutual funds as well as index funds, identified as such by Morningstar or by the word “index” in their name. We also eliminate the four government pension funds that invest public pension money. We believe they are fundamentally different from privately owned mutual funds. The remaining funds belong to one of five categories based on the Morningstar GlobalBroadCategoryGroup variable: Equity, Allocation (mix of stocks and bonds), Fixed Income, Alternatives, and a Rest category, which combines commodity funds, miscellaneous funds, and funds where the category variable is missing. The Alternatives category contains Currency, Long/Short Equity, Market Neutral, Multi-Alternative, and Other Alternative funds. This category mainly consists of hedge funds which in Sweden are allowed to market themselves directly toward the general public. Many of the Equities and Fixed Income funds specialize in specific investment regions or in specific industries.9 Most of the miscellaneous funds in the Rest category are either capital protected or guaranteed, a common type of structured product in Europe.

We retrieve monthly time series of AUM from Morningstar, calculate monthly revenue, and form annual counterparts by summing the monthly values.10 Several funds have multiple share classes. AUM is available per share class. We aggregate those share classes into a single fund (identified by Morningstar’s variable FundId). We convert AUM values in other currencies than SEK into SEK when necessary. Similarly, we obtain total expense ratios per share class and aggregate them across share classes using AUM weights. We complement the annual AUM and TER time series from Morningstar Direct with two additional sources, Bloomberg and some hand-collected data obtained from AMF Fonder.11 Our final data set has 5,668 fund-year observations. In 1994, the aggregate AUM among the sample funds is 2.6 billion SEK. Aggregate AUM increases to 1,772.9 billion SEK by 2015. All SEK amounts are expressed in 2012 real SEK. The average SEK/USD exchange rate over the 1994–2015 period is 7.5.

Summary statistics for the funds employed in our main regression analysis are reported in Table 1. Panel A shows that the average fund has AUM of 2,300 million SEK, or about

Summary statistics at the fund level

| 10% | 25% | 50% | 75% | 90% | Mean | Sd | N | |

|---|---|---|---|---|---|---|---|---|

| A. Fund AUM and TER | ||||||||

| |${\it AUM}_{i}$| (mio. SEK) | 63.3 | 199.9 | 698.3 | 2,424.8 | 6,600.3 | 2,305.7 | 3,976.9 | 5,545 |

| |${\it TER}_{i}$| (%) | 0.50 | 0.77 | 1.42 | 1.70 | 2.21 | 1.36 | 0.68 | 5,609 |

| |${\it REV}_i$| (mio. SEK) | 0.7 | 2.4 | 7.9 | 28.5 | 80.4 | 27.6 | 47.7 | 5,518 |

| |$\log({\it REV}_{i})$| | 13.5 | 14.7 | 15.9 | 17.2 | 18.2 | 15.8 | 1.8 | 5,518 |

| B. Fund performance (%) | ||||||||

| |$\log (1+R_{i}^{\it exc})$| | –20.2 | –2.2 | 6.9 | 18.1 | 27.9 | 5.2 | 21.6 | 4,484 |

| |$\log (1+R_{i}^{\it abn})$| | –8.6 | –2.9 | 0.5 | 4.1 | 9.8 | 0.6 | 8.5 | 4,467 |

| |$\log (1+R_{i}^{\it abn,CAPM})$| | –10.0 | –3.9 | 0.3 | 4.0 | 10.1 | 0.1 | 9.3 | 4,460 |

| |$\log (1+R_{i}^{\it abn,FF3})$| | –9.3 | –3.3 | 0.7 | 4.4 | 9.6 | 0.4 | 8.8 | 4,460 |

| |$\log (1+R_{i}^{\it abn,GF5})$| | –8.4 | –3.8 | 0.1 | 3.7 | 9.7 | 0.2 | 8.1 | 4,393 |

| |$ValueAdded_{i}$| (mio. SEK) | –90.2 | –15.0 | 1.3 | 27.9 | 142.6 | 26.9 | 225.5 | 4,416 |

| C. Manager characteristics | ||||||||

| |${\it Age}_m$| | 33 | 37 | 42 | 48 | 52 | 42 | 7.5 | 2,898 |

| |${\it Exper}_m$| | 1.0 | 2.4 | 4.8 | 8.1 | 12.2 | 5.9 | 4.7 | 2,898 |

| |${\it Edu}_m$| | 12 | 15 | 15 | 16 | 16 | 15 | 2 | 2,898 |

| |${\it Coman}_m$| | 0.00 | 0.00 | 0.12 | 1.00 | 1.00 | 0.45 | 0.48 | 2,898 |

| |$ {\it Teams}_m$| | 0.00 | 0.00 | 0.92 | 1.00 | 3.00 | 1.21 | 2.26 | 2,898 |

| |${\it TeamSize}_m$| | 0.00 | 0.00 | 0.14 | 1.00 | 2.00 | 0.72 | 1.03 | 2,898 |

| |${\it NumCat}_m$| | 1.0 | 1.0 | 1.0 | 1.0 | 2.0 | 1.2 | 0.5 | 2,898 |

| D. Manager income (1000s of SEK) | ||||||||

| |$L_m$| | 510.6 | 788.3 | 1,206.5 | 1,806.7 | 2,739.8 | 1,559.3 | 1,522.5 | 2,898 |

| |$D_m$| | 0.0 | 0.0 | 4.2 | 41.8 | 450.6 | 813.0 | 8,730.1 | 2,898 |

| |$Y_m$| | 548.1 | 856.4 | 1,341.5 | 2,042.8 | 3,427.1 | 2,372.3 | 8,864.5 | 2,898 |

| E. Firm level | ||||||||

| |${\it AUM}_{f}$| (bio. SEK) | 0.1 | 0.7 | 3.7 | 17.7 | 65.6 | 24.5 | 61.2 | 929 |

| |${\it TER}_{f}$| (%) | 0.69 | 1.00 | 1.26 | 1.64 | 2.40 | 1.40 | 0.66 | 928 |

| |${\it REV}_f$| (mio. SEK) | 2.0 | 9.9 | 48.0 | 208.4 | 693.1 | 278.0 | 670.2 | 928 |

| |$\log({\it REV}_f)$| | 14.5 | 16.1 | 17.7 | 19.2 | 20.4 | 17.6 | 2.2 | 928 |

| |${\it Profit}_f$| (mio. SEK) | –1.9 | 0.3 | 10.1 | 48.3 | 152.1 | 57.5 | 152.1 | 646 |

| |${\it Profit}_f^{+}$| (mio. SEK) | 1.1 | 4.5 | 22.7 | 68.5 | 217.3 | 76.0 | 168.5 | 498 |

| No. of funds / year | 1.0 | 2.0 | 5.0 | 11.0 | 31.0 | 11.2 | 17.7 | 929 |

| No. of managers / year | 1.0 | 2.0 | 3.0 | 9.0 | 20.0 | 7.6 | 10.5 | 929 |

| 10% | 25% | 50% | 75% | 90% | Mean | Sd | N | |

|---|---|---|---|---|---|---|---|---|

| A. Fund AUM and TER | ||||||||

| |${\it AUM}_{i}$| (mio. SEK) | 63.3 | 199.9 | 698.3 | 2,424.8 | 6,600.3 | 2,305.7 | 3,976.9 | 5,545 |

| |${\it TER}_{i}$| (%) | 0.50 | 0.77 | 1.42 | 1.70 | 2.21 | 1.36 | 0.68 | 5,609 |

| |${\it REV}_i$| (mio. SEK) | 0.7 | 2.4 | 7.9 | 28.5 | 80.4 | 27.6 | 47.7 | 5,518 |

| |$\log({\it REV}_{i})$| | 13.5 | 14.7 | 15.9 | 17.2 | 18.2 | 15.8 | 1.8 | 5,518 |

| B. Fund performance (%) | ||||||||

| |$\log (1+R_{i}^{\it exc})$| | –20.2 | –2.2 | 6.9 | 18.1 | 27.9 | 5.2 | 21.6 | 4,484 |

| |$\log (1+R_{i}^{\it abn})$| | –8.6 | –2.9 | 0.5 | 4.1 | 9.8 | 0.6 | 8.5 | 4,467 |

| |$\log (1+R_{i}^{\it abn,CAPM})$| | –10.0 | –3.9 | 0.3 | 4.0 | 10.1 | 0.1 | 9.3 | 4,460 |

| |$\log (1+R_{i}^{\it abn,FF3})$| | –9.3 | –3.3 | 0.7 | 4.4 | 9.6 | 0.4 | 8.8 | 4,460 |

| |$\log (1+R_{i}^{\it abn,GF5})$| | –8.4 | –3.8 | 0.1 | 3.7 | 9.7 | 0.2 | 8.1 | 4,393 |

| |$ValueAdded_{i}$| (mio. SEK) | –90.2 | –15.0 | 1.3 | 27.9 | 142.6 | 26.9 | 225.5 | 4,416 |

| C. Manager characteristics | ||||||||

| |${\it Age}_m$| | 33 | 37 | 42 | 48 | 52 | 42 | 7.5 | 2,898 |

| |${\it Exper}_m$| | 1.0 | 2.4 | 4.8 | 8.1 | 12.2 | 5.9 | 4.7 | 2,898 |

| |${\it Edu}_m$| | 12 | 15 | 15 | 16 | 16 | 15 | 2 | 2,898 |

| |${\it Coman}_m$| | 0.00 | 0.00 | 0.12 | 1.00 | 1.00 | 0.45 | 0.48 | 2,898 |

| |$ {\it Teams}_m$| | 0.00 | 0.00 | 0.92 | 1.00 | 3.00 | 1.21 | 2.26 | 2,898 |

| |${\it TeamSize}_m$| | 0.00 | 0.00 | 0.14 | 1.00 | 2.00 | 0.72 | 1.03 | 2,898 |

| |${\it NumCat}_m$| | 1.0 | 1.0 | 1.0 | 1.0 | 2.0 | 1.2 | 0.5 | 2,898 |

| D. Manager income (1000s of SEK) | ||||||||

| |$L_m$| | 510.6 | 788.3 | 1,206.5 | 1,806.7 | 2,739.8 | 1,559.3 | 1,522.5 | 2,898 |

| |$D_m$| | 0.0 | 0.0 | 4.2 | 41.8 | 450.6 | 813.0 | 8,730.1 | 2,898 |

| |$Y_m$| | 548.1 | 856.4 | 1,341.5 | 2,042.8 | 3,427.1 | 2,372.3 | 8,864.5 | 2,898 |

| E. Firm level | ||||||||

| |${\it AUM}_{f}$| (bio. SEK) | 0.1 | 0.7 | 3.7 | 17.7 | 65.6 | 24.5 | 61.2 | 929 |

| |${\it TER}_{f}$| (%) | 0.69 | 1.00 | 1.26 | 1.64 | 2.40 | 1.40 | 0.66 | 928 |

| |${\it REV}_f$| (mio. SEK) | 2.0 | 9.9 | 48.0 | 208.4 | 693.1 | 278.0 | 670.2 | 928 |

| |$\log({\it REV}_f)$| | 14.5 | 16.1 | 17.7 | 19.2 | 20.4 | 17.6 | 2.2 | 928 |

| |${\it Profit}_f$| (mio. SEK) | –1.9 | 0.3 | 10.1 | 48.3 | 152.1 | 57.5 | 152.1 | 646 |

| |${\it Profit}_f^{+}$| (mio. SEK) | 1.1 | 4.5 | 22.7 | 68.5 | 217.3 | 76.0 | 168.5 | 498 |

| No. of funds / year | 1.0 | 2.0 | 5.0 | 11.0 | 31.0 | 11.2 | 17.7 | 929 |

| No. of managers / year | 1.0 | 2.0 | 3.0 | 9.0 | 20.0 | 7.6 | 10.5 | 929 |

The sample contains all fund-year observations that are used in our main analysis (Table 2). Panels A and B provide summary statistics at the fund level. A fund-year observation is included if it is managed by a manager in our sample in that year. We winsorize the performance variables, AUM, TER, and REV, at the 1% and 99% levels. Panels C and D contain summary statistics at the manager level. We do not winsorize income or characteristics variables. Panel E aggregates the fund-year observations into firm-year observations.

Summary statistics at the fund level

| 10% | 25% | 50% | 75% | 90% | Mean | Sd | N | |

|---|---|---|---|---|---|---|---|---|

| A. Fund AUM and TER | ||||||||

| |${\it AUM}_{i}$| (mio. SEK) | 63.3 | 199.9 | 698.3 | 2,424.8 | 6,600.3 | 2,305.7 | 3,976.9 | 5,545 |

| |${\it TER}_{i}$| (%) | 0.50 | 0.77 | 1.42 | 1.70 | 2.21 | 1.36 | 0.68 | 5,609 |

| |${\it REV}_i$| (mio. SEK) | 0.7 | 2.4 | 7.9 | 28.5 | 80.4 | 27.6 | 47.7 | 5,518 |

| |$\log({\it REV}_{i})$| | 13.5 | 14.7 | 15.9 | 17.2 | 18.2 | 15.8 | 1.8 | 5,518 |

| B. Fund performance (%) | ||||||||

| |$\log (1+R_{i}^{\it exc})$| | –20.2 | –2.2 | 6.9 | 18.1 | 27.9 | 5.2 | 21.6 | 4,484 |

| |$\log (1+R_{i}^{\it abn})$| | –8.6 | –2.9 | 0.5 | 4.1 | 9.8 | 0.6 | 8.5 | 4,467 |

| |$\log (1+R_{i}^{\it abn,CAPM})$| | –10.0 | –3.9 | 0.3 | 4.0 | 10.1 | 0.1 | 9.3 | 4,460 |

| |$\log (1+R_{i}^{\it abn,FF3})$| | –9.3 | –3.3 | 0.7 | 4.4 | 9.6 | 0.4 | 8.8 | 4,460 |

| |$\log (1+R_{i}^{\it abn,GF5})$| | –8.4 | –3.8 | 0.1 | 3.7 | 9.7 | 0.2 | 8.1 | 4,393 |

| |$ValueAdded_{i}$| (mio. SEK) | –90.2 | –15.0 | 1.3 | 27.9 | 142.6 | 26.9 | 225.5 | 4,416 |

| C. Manager characteristics | ||||||||

| |${\it Age}_m$| | 33 | 37 | 42 | 48 | 52 | 42 | 7.5 | 2,898 |

| |${\it Exper}_m$| | 1.0 | 2.4 | 4.8 | 8.1 | 12.2 | 5.9 | 4.7 | 2,898 |

| |${\it Edu}_m$| | 12 | 15 | 15 | 16 | 16 | 15 | 2 | 2,898 |

| |${\it Coman}_m$| | 0.00 | 0.00 | 0.12 | 1.00 | 1.00 | 0.45 | 0.48 | 2,898 |

| |$ {\it Teams}_m$| | 0.00 | 0.00 | 0.92 | 1.00 | 3.00 | 1.21 | 2.26 | 2,898 |

| |${\it TeamSize}_m$| | 0.00 | 0.00 | 0.14 | 1.00 | 2.00 | 0.72 | 1.03 | 2,898 |

| |${\it NumCat}_m$| | 1.0 | 1.0 | 1.0 | 1.0 | 2.0 | 1.2 | 0.5 | 2,898 |

| D. Manager income (1000s of SEK) | ||||||||

| |$L_m$| | 510.6 | 788.3 | 1,206.5 | 1,806.7 | 2,739.8 | 1,559.3 | 1,522.5 | 2,898 |

| |$D_m$| | 0.0 | 0.0 | 4.2 | 41.8 | 450.6 | 813.0 | 8,730.1 | 2,898 |

| |$Y_m$| | 548.1 | 856.4 | 1,341.5 | 2,042.8 | 3,427.1 | 2,372.3 | 8,864.5 | 2,898 |

| E. Firm level | ||||||||

| |${\it AUM}_{f}$| (bio. SEK) | 0.1 | 0.7 | 3.7 | 17.7 | 65.6 | 24.5 | 61.2 | 929 |

| |${\it TER}_{f}$| (%) | 0.69 | 1.00 | 1.26 | 1.64 | 2.40 | 1.40 | 0.66 | 928 |

| |${\it REV}_f$| (mio. SEK) | 2.0 | 9.9 | 48.0 | 208.4 | 693.1 | 278.0 | 670.2 | 928 |

| |$\log({\it REV}_f)$| | 14.5 | 16.1 | 17.7 | 19.2 | 20.4 | 17.6 | 2.2 | 928 |

| |${\it Profit}_f$| (mio. SEK) | –1.9 | 0.3 | 10.1 | 48.3 | 152.1 | 57.5 | 152.1 | 646 |

| |${\it Profit}_f^{+}$| (mio. SEK) | 1.1 | 4.5 | 22.7 | 68.5 | 217.3 | 76.0 | 168.5 | 498 |

| No. of funds / year | 1.0 | 2.0 | 5.0 | 11.0 | 31.0 | 11.2 | 17.7 | 929 |

| No. of managers / year | 1.0 | 2.0 | 3.0 | 9.0 | 20.0 | 7.6 | 10.5 | 929 |

| 10% | 25% | 50% | 75% | 90% | Mean | Sd | N | |

|---|---|---|---|---|---|---|---|---|

| A. Fund AUM and TER | ||||||||

| |${\it AUM}_{i}$| (mio. SEK) | 63.3 | 199.9 | 698.3 | 2,424.8 | 6,600.3 | 2,305.7 | 3,976.9 | 5,545 |

| |${\it TER}_{i}$| (%) | 0.50 | 0.77 | 1.42 | 1.70 | 2.21 | 1.36 | 0.68 | 5,609 |

| |${\it REV}_i$| (mio. SEK) | 0.7 | 2.4 | 7.9 | 28.5 | 80.4 | 27.6 | 47.7 | 5,518 |

| |$\log({\it REV}_{i})$| | 13.5 | 14.7 | 15.9 | 17.2 | 18.2 | 15.8 | 1.8 | 5,518 |

| B. Fund performance (%) | ||||||||

| |$\log (1+R_{i}^{\it exc})$| | –20.2 | –2.2 | 6.9 | 18.1 | 27.9 | 5.2 | 21.6 | 4,484 |

| |$\log (1+R_{i}^{\it abn})$| | –8.6 | –2.9 | 0.5 | 4.1 | 9.8 | 0.6 | 8.5 | 4,467 |

| |$\log (1+R_{i}^{\it abn,CAPM})$| | –10.0 | –3.9 | 0.3 | 4.0 | 10.1 | 0.1 | 9.3 | 4,460 |

| |$\log (1+R_{i}^{\it abn,FF3})$| | –9.3 | –3.3 | 0.7 | 4.4 | 9.6 | 0.4 | 8.8 | 4,460 |

| |$\log (1+R_{i}^{\it abn,GF5})$| | –8.4 | –3.8 | 0.1 | 3.7 | 9.7 | 0.2 | 8.1 | 4,393 |

| |$ValueAdded_{i}$| (mio. SEK) | –90.2 | –15.0 | 1.3 | 27.9 | 142.6 | 26.9 | 225.5 | 4,416 |

| C. Manager characteristics | ||||||||

| |${\it Age}_m$| | 33 | 37 | 42 | 48 | 52 | 42 | 7.5 | 2,898 |

| |${\it Exper}_m$| | 1.0 | 2.4 | 4.8 | 8.1 | 12.2 | 5.9 | 4.7 | 2,898 |

| |${\it Edu}_m$| | 12 | 15 | 15 | 16 | 16 | 15 | 2 | 2,898 |

| |${\it Coman}_m$| | 0.00 | 0.00 | 0.12 | 1.00 | 1.00 | 0.45 | 0.48 | 2,898 |

| |$ {\it Teams}_m$| | 0.00 | 0.00 | 0.92 | 1.00 | 3.00 | 1.21 | 2.26 | 2,898 |

| |${\it TeamSize}_m$| | 0.00 | 0.00 | 0.14 | 1.00 | 2.00 | 0.72 | 1.03 | 2,898 |

| |${\it NumCat}_m$| | 1.0 | 1.0 | 1.0 | 1.0 | 2.0 | 1.2 | 0.5 | 2,898 |

| D. Manager income (1000s of SEK) | ||||||||

| |$L_m$| | 510.6 | 788.3 | 1,206.5 | 1,806.7 | 2,739.8 | 1,559.3 | 1,522.5 | 2,898 |

| |$D_m$| | 0.0 | 0.0 | 4.2 | 41.8 | 450.6 | 813.0 | 8,730.1 | 2,898 |

| |$Y_m$| | 548.1 | 856.4 | 1,341.5 | 2,042.8 | 3,427.1 | 2,372.3 | 8,864.5 | 2,898 |

| E. Firm level | ||||||||

| |${\it AUM}_{f}$| (bio. SEK) | 0.1 | 0.7 | 3.7 | 17.7 | 65.6 | 24.5 | 61.2 | 929 |

| |${\it TER}_{f}$| (%) | 0.69 | 1.00 | 1.26 | 1.64 | 2.40 | 1.40 | 0.66 | 928 |

| |${\it REV}_f$| (mio. SEK) | 2.0 | 9.9 | 48.0 | 208.4 | 693.1 | 278.0 | 670.2 | 928 |

| |$\log({\it REV}_f)$| | 14.5 | 16.1 | 17.7 | 19.2 | 20.4 | 17.6 | 2.2 | 928 |

| |${\it Profit}_f$| (mio. SEK) | –1.9 | 0.3 | 10.1 | 48.3 | 152.1 | 57.5 | 152.1 | 646 |

| |${\it Profit}_f^{+}$| (mio. SEK) | 1.1 | 4.5 | 22.7 | 68.5 | 217.3 | 76.0 | 168.5 | 498 |

| No. of funds / year | 1.0 | 2.0 | 5.0 | 11.0 | 31.0 | 11.2 | 17.7 | 929 |

| No. of managers / year | 1.0 | 2.0 | 3.0 | 9.0 | 20.0 | 7.6 | 10.5 | 929 |

The sample contains all fund-year observations that are used in our main analysis (Table 2). Panels A and B provide summary statistics at the fund level. A fund-year observation is included if it is managed by a manager in our sample in that year. We winsorize the performance variables, AUM, TER, and REV, at the 1% and 99% levels. Panels C and D contain summary statistics at the manager level. We do not winsorize income or characteristics variables. Panel E aggregates the fund-year observations into firm-year observations.

Sensitivity of pay to size and performance

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$\log ( {\it REV}_{\it m,t} )$| | 0.153*** | 0.141*** | 0.123*** | |||

| (0.0184) | (0.0194) | (0.0239) | ||||

| |$\log (1+R^{\it abn}_{\it m,t-1})$| | 0.340* | 0.407** | 0.0913 | |||

| (0.206) | (0.189) | (0.143) | ||||

| |${\it Exper}_{\it m,t-1}$| | 0.0323*** | 0.0961** | 0.0570*** | 0.121** | ||

| (0.0118) | (0.0482) | (0.0123) | (0.0569) | |||

| |${\it Exper}^2_{\it m,t-1}$| | –0.000533 | –0.0000195 | –0.00119*** | –0.000731 | ||

| (0.000408) | (0.000755) | (0.000446) | (0.000721) | |||

| |${\it Age}_{\it m,t-1} $| | 0.177*** | 0.0942 | 0.175*** | 0.0994 | ||

| (0.0292) | (0.0676) | (0.0278) | (0.0751) | |||

| |${\it Age}^2_{\it m,t-1}$| | –0.00191*** | –0.00153*** | –0.00193*** | –0.00156*** | ||

| (0.000351) | (0.000544) | (0.000327) | (0.000584) | |||

| |${\it Edu}_{\it m,t-1} $| | 0.00938 | –0.0264 | 0.0164 | –0.00132 | ||

| (0.0145) | (0.0493) | (0.0150) | (0.0500) | |||

| |$ {\it Finance}_{\it m,t-1}$| | 0.259** | 0.255*** | 0.335*** | 0.280*** | ||

| (0.106) | (0.0572) | (0.0892) | (0.0654) | |||

| |${\it Coman}_{\it m,t-1}$| | –0.223*** | 0.0626 | –0.310*** | 0.00874 | ||

| (0.0830) | (0.106) | (0.0830) | (0.113) | |||

| |$ {\it Teams}_{\it m,t-1}$| | –0.0261** | 0.00121 | 0.00781 | 0.0166* | ||

| (0.0103) | (0.00855) | (0.0104) | (0.00915) | |||

| |$ {\it TeamSize}_{\it m,t-1}$| | 0.114*** | –0.0110 | 0.0952** | –0.0346 | ||

| (0.0384) | (0.0466) | (0.0391) | (0.0504) | |||

| |$ {\it NumCat}_{\it m,t-1}$| | 0.0988 | 0.0934* | 0.118* | 0.151*** | ||

| (0.0691) | (0.0511) | (0.0694) | (0.0553) | |||

| Constant | 10.96*** | 7.173*** | 10.35*** | 13.59*** | 9.450*** | 11.64*** |

| (0.321) | (0.595) | (1.834) | (0.155) | (0.632) | (2.192) | |

| Manager FE | No | No | Yes | No | No | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | No | Yes | Yes | No | Yes | Yes |

| |$N$| | 2,898 | 2,898 | 2,898 | 2,898 | 2,898 | 2,898 |

| Adjusted \(R^{2}\) | 0.139 | 0.229 | 0.614 | 0.023 | 0.146 | 0.594 |

| Standardized Revenue and Performance | ||||||

| |$ \log ( {\it REV}_{\it m,t} )_{\it std}$| | 0.281*** | 0.253*** | 0.187*** | |||

| (0.0365) | (0.0362) | (0.0468) | ||||

| |$ \log (1+R^{\it abn}_{\it m,t-1} )_{\it std}$| | 0.0298 | 0.0290 | –0.00328 | |||

| (0.0198) | (0.0193) | (0.0154) | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$\log ( {\it REV}_{\it m,t} )$| | 0.153*** | 0.141*** | 0.123*** | |||

| (0.0184) | (0.0194) | (0.0239) | ||||

| |$\log (1+R^{\it abn}_{\it m,t-1})$| | 0.340* | 0.407** | 0.0913 | |||

| (0.206) | (0.189) | (0.143) | ||||

| |${\it Exper}_{\it m,t-1}$| | 0.0323*** | 0.0961** | 0.0570*** | 0.121** | ||

| (0.0118) | (0.0482) | (0.0123) | (0.0569) | |||

| |${\it Exper}^2_{\it m,t-1}$| | –0.000533 | –0.0000195 | –0.00119*** | –0.000731 | ||

| (0.000408) | (0.000755) | (0.000446) | (0.000721) | |||

| |${\it Age}_{\it m,t-1} $| | 0.177*** | 0.0942 | 0.175*** | 0.0994 | ||

| (0.0292) | (0.0676) | (0.0278) | (0.0751) | |||

| |${\it Age}^2_{\it m,t-1}$| | –0.00191*** | –0.00153*** | –0.00193*** | –0.00156*** | ||

| (0.000351) | (0.000544) | (0.000327) | (0.000584) | |||

| |${\it Edu}_{\it m,t-1} $| | 0.00938 | –0.0264 | 0.0164 | –0.00132 | ||

| (0.0145) | (0.0493) | (0.0150) | (0.0500) | |||

| |$ {\it Finance}_{\it m,t-1}$| | 0.259** | 0.255*** | 0.335*** | 0.280*** | ||

| (0.106) | (0.0572) | (0.0892) | (0.0654) | |||

| |${\it Coman}_{\it m,t-1}$| | –0.223*** | 0.0626 | –0.310*** | 0.00874 | ||

| (0.0830) | (0.106) | (0.0830) | (0.113) | |||

| |$ {\it Teams}_{\it m,t-1}$| | –0.0261** | 0.00121 | 0.00781 | 0.0166* | ||

| (0.0103) | (0.00855) | (0.0104) | (0.00915) | |||

| |$ {\it TeamSize}_{\it m,t-1}$| | 0.114*** | –0.0110 | 0.0952** | –0.0346 | ||

| (0.0384) | (0.0466) | (0.0391) | (0.0504) | |||

| |$ {\it NumCat}_{\it m,t-1}$| | 0.0988 | 0.0934* | 0.118* | 0.151*** | ||

| (0.0691) | (0.0511) | (0.0694) | (0.0553) | |||

| Constant | 10.96*** | 7.173*** | 10.35*** | 13.59*** | 9.450*** | 11.64*** |

| (0.321) | (0.595) | (1.834) | (0.155) | (0.632) | (2.192) | |

| Manager FE | No | No | Yes | No | No | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | No | Yes | Yes | No | Yes | Yes |

| |$N$| | 2,898 | 2,898 | 2,898 | 2,898 | 2,898 | 2,898 |

| Adjusted \(R^{2}\) | 0.139 | 0.229 | 0.614 | 0.023 | 0.146 | 0.594 |

| Standardized Revenue and Performance | ||||||

| |$ \log ( {\it REV}_{\it m,t} )_{\it std}$| | 0.281*** | 0.253*** | 0.187*** | |||

| (0.0365) | (0.0362) | (0.0468) | ||||

| |$ \log (1+R^{\it abn}_{\it m,t-1} )_{\it std}$| | 0.0298 | 0.0290 | –0.00328 | |||

| (0.0198) | (0.0193) | (0.0154) | ||||

The dependent variable is annual log labor income of the fund manager. The independent variables are a constant, log revenue generated by the manager in that same year, log annual fund returns at the manager level over the past year, manager experience in years working as a fund manager, experience squared, manager age, manager age squared, years of education, indicator variable for finance or economics degree, the fraction of funds that are co-managed with other managers, the number of management teams the manager serves on, the size of management teams, and the number of different investment categories that the manager’s funds belong to. All specifications include year fixed effects. Some specifications additionally include investment category fixed effects and manager fixed effects. When category fixed effects are included, the Equity category is omitted. The bottom panel estimates a separate set of regressions, which replaces the variables in the first two rows by standardized versions of those same variables (denoted by the subscript “std”). The scaling is done by investment category and results in a variable that is mean zero and has standard deviation of one. All standard errors are clustered at the manager level.

Sensitivity of pay to size and performance

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$\log ( {\it REV}_{\it m,t} )$| | 0.153*** | 0.141*** | 0.123*** | |||

| (0.0184) | (0.0194) | (0.0239) | ||||

| |$\log (1+R^{\it abn}_{\it m,t-1})$| | 0.340* | 0.407** | 0.0913 | |||

| (0.206) | (0.189) | (0.143) | ||||

| |${\it Exper}_{\it m,t-1}$| | 0.0323*** | 0.0961** | 0.0570*** | 0.121** | ||

| (0.0118) | (0.0482) | (0.0123) | (0.0569) | |||

| |${\it Exper}^2_{\it m,t-1}$| | –0.000533 | –0.0000195 | –0.00119*** | –0.000731 | ||

| (0.000408) | (0.000755) | (0.000446) | (0.000721) | |||

| |${\it Age}_{\it m,t-1} $| | 0.177*** | 0.0942 | 0.175*** | 0.0994 | ||

| (0.0292) | (0.0676) | (0.0278) | (0.0751) | |||

| |${\it Age}^2_{\it m,t-1}$| | –0.00191*** | –0.00153*** | –0.00193*** | –0.00156*** | ||

| (0.000351) | (0.000544) | (0.000327) | (0.000584) | |||

| |${\it Edu}_{\it m,t-1} $| | 0.00938 | –0.0264 | 0.0164 | –0.00132 | ||

| (0.0145) | (0.0493) | (0.0150) | (0.0500) | |||

| |$ {\it Finance}_{\it m,t-1}$| | 0.259** | 0.255*** | 0.335*** | 0.280*** | ||

| (0.106) | (0.0572) | (0.0892) | (0.0654) | |||

| |${\it Coman}_{\it m,t-1}$| | –0.223*** | 0.0626 | –0.310*** | 0.00874 | ||

| (0.0830) | (0.106) | (0.0830) | (0.113) | |||

| |$ {\it Teams}_{\it m,t-1}$| | –0.0261** | 0.00121 | 0.00781 | 0.0166* | ||

| (0.0103) | (0.00855) | (0.0104) | (0.00915) | |||

| |$ {\it TeamSize}_{\it m,t-1}$| | 0.114*** | –0.0110 | 0.0952** | –0.0346 | ||

| (0.0384) | (0.0466) | (0.0391) | (0.0504) | |||

| |$ {\it NumCat}_{\it m,t-1}$| | 0.0988 | 0.0934* | 0.118* | 0.151*** | ||

| (0.0691) | (0.0511) | (0.0694) | (0.0553) | |||

| Constant | 10.96*** | 7.173*** | 10.35*** | 13.59*** | 9.450*** | 11.64*** |

| (0.321) | (0.595) | (1.834) | (0.155) | (0.632) | (2.192) | |

| Manager FE | No | No | Yes | No | No | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | No | Yes | Yes | No | Yes | Yes |

| |$N$| | 2,898 | 2,898 | 2,898 | 2,898 | 2,898 | 2,898 |

| Adjusted \(R^{2}\) | 0.139 | 0.229 | 0.614 | 0.023 | 0.146 | 0.594 |

| Standardized Revenue and Performance | ||||||

| |$ \log ( {\it REV}_{\it m,t} )_{\it std}$| | 0.281*** | 0.253*** | 0.187*** | |||

| (0.0365) | (0.0362) | (0.0468) | ||||

| |$ \log (1+R^{\it abn}_{\it m,t-1} )_{\it std}$| | 0.0298 | 0.0290 | –0.00328 | |||

| (0.0198) | (0.0193) | (0.0154) | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$\log ( {\it REV}_{\it m,t} )$| | 0.153*** | 0.141*** | 0.123*** | |||

| (0.0184) | (0.0194) | (0.0239) | ||||

| |$\log (1+R^{\it abn}_{\it m,t-1})$| | 0.340* | 0.407** | 0.0913 | |||

| (0.206) | (0.189) | (0.143) | ||||

| |${\it Exper}_{\it m,t-1}$| | 0.0323*** | 0.0961** | 0.0570*** | 0.121** | ||

| (0.0118) | (0.0482) | (0.0123) | (0.0569) | |||

| |${\it Exper}^2_{\it m,t-1}$| | –0.000533 | –0.0000195 | –0.00119*** | –0.000731 | ||

| (0.000408) | (0.000755) | (0.000446) | (0.000721) | |||

| |${\it Age}_{\it m,t-1} $| | 0.177*** | 0.0942 | 0.175*** | 0.0994 | ||

| (0.0292) | (0.0676) | (0.0278) | (0.0751) | |||

| |${\it Age}^2_{\it m,t-1}$| | –0.00191*** | –0.00153*** | –0.00193*** | –0.00156*** | ||

| (0.000351) | (0.000544) | (0.000327) | (0.000584) | |||

| |${\it Edu}_{\it m,t-1} $| | 0.00938 | –0.0264 | 0.0164 | –0.00132 | ||

| (0.0145) | (0.0493) | (0.0150) | (0.0500) | |||

| |$ {\it Finance}_{\it m,t-1}$| | 0.259** | 0.255*** | 0.335*** | 0.280*** | ||

| (0.106) | (0.0572) | (0.0892) | (0.0654) | |||

| |${\it Coman}_{\it m,t-1}$| | –0.223*** | 0.0626 | –0.310*** | 0.00874 | ||

| (0.0830) | (0.106) | (0.0830) | (0.113) | |||

| |$ {\it Teams}_{\it m,t-1}$| | –0.0261** | 0.00121 | 0.00781 | 0.0166* | ||

| (0.0103) | (0.00855) | (0.0104) | (0.00915) | |||

| |$ {\it TeamSize}_{\it m,t-1}$| | 0.114*** | –0.0110 | 0.0952** | –0.0346 | ||

| (0.0384) | (0.0466) | (0.0391) | (0.0504) | |||

| |$ {\it NumCat}_{\it m,t-1}$| | 0.0988 | 0.0934* | 0.118* | 0.151*** | ||

| (0.0691) | (0.0511) | (0.0694) | (0.0553) | |||

| Constant | 10.96*** | 7.173*** | 10.35*** | 13.59*** | 9.450*** | 11.64*** |

| (0.321) | (0.595) | (1.834) | (0.155) | (0.632) | (2.192) | |

| Manager FE | No | No | Yes | No | No | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | No | Yes | Yes | No | Yes | Yes |

| |$N$| | 2,898 | 2,898 | 2,898 | 2,898 | 2,898 | 2,898 |

| Adjusted \(R^{2}\) | 0.139 | 0.229 | 0.614 | 0.023 | 0.146 | 0.594 |

| Standardized Revenue and Performance | ||||||

| |$ \log ( {\it REV}_{\it m,t} )_{\it std}$| | 0.281*** | 0.253*** | 0.187*** | |||

| (0.0365) | (0.0362) | (0.0468) | ||||

| |$ \log (1+R^{\it abn}_{\it m,t-1} )_{\it std}$| | 0.0298 | 0.0290 | –0.00328 | |||

| (0.0198) | (0.0193) | (0.0154) | ||||

The dependent variable is annual log labor income of the fund manager. The independent variables are a constant, log revenue generated by the manager in that same year, log annual fund returns at the manager level over the past year, manager experience in years working as a fund manager, experience squared, manager age, manager age squared, years of education, indicator variable for finance or economics degree, the fraction of funds that are co-managed with other managers, the number of management teams the manager serves on, the size of management teams, and the number of different investment categories that the manager’s funds belong to. All specifications include year fixed effects. Some specifications additionally include investment category fixed effects and manager fixed effects. When category fixed effects are included, the Equity category is omitted. The bottom panel estimates a separate set of regressions, which replaces the variables in the first two rows by standardized versions of those same variables (denoted by the subscript “std”). The scaling is done by investment category and results in a variable that is mean zero and has standard deviation of one. All standard errors are clustered at the manager level.

We obtain monthly net fund returns from Morningstar. To calculate gross monthly returns, we add TER/12. All returns are converted into SEK. Excess returns are calculated by subtracting the one-month STIBOR (Stockholm Interbank Offered Rate) rate. We calculate annual log returns by summing log monthly returns. Panel B of Table 1 shows that the average fund has a log excess annual return of 5.2%; the median is 6.9%. The interquartile range is large, ranging from –2.2% to 18.1%.

As our main measure of performance, we use the gross abnormal return or “alpha” relative to the stated benchmark return in logs, |$\log(1+R^{\it abn}_i)$|. This is a simple measure of gross alpha. Gross returns rather than net returns are what matter in the relationship between owners and managers. In order to construct it, we require a benchmark for each fund in our sample.

Morningstar reports a Primary Prospectus Benchmark for 74% of our funds. Some funds have linear combinations of indices as their benchmark. There are more than 300 different benchmark indices present in our sample. We find monthly return information for most of them on Morningstar, Bloomberg, and Datastream. For funds with no assigned benchmark or irretrievable benchmark, we assign a benchmark by hand.12 We express all benchmark returns in SEK. The median annual log (gross) abnormal return is 0.5%. The distribution has a large 8.5% standard deviation. The interquartile range is |$-2.9%$| to 4.1%. Net abnormal returns (after expenses, not reported) are slightly negative on average, consistent with the evidence for the United States.

We explore four alternative measures of abnormal returns. They are the CAPM alpha, the Fama-French three-factor alpha, the global five-factor alpha, and gross value added. For the Equity, Alternative, and Allocation categories we use the Swedish stock market index return (SIXPRX) in excess of the one-month STIBOR rate as the CAPM market factor. For the Fixed Income and Other categories, we use the Swedish government bond index return (OMRX) in excess of the one-month STIBOR rate as the CAPM market factor.13 The three-factor Fama-French model has the stock market factor, the size factor (SMB), and the value factor (HML), constructed from all Swedish stocks. We also consider a global five-factor model. For the Equity, Alternative, and Allocation categories, the five factors are five excess returns on different international equity baskets.14 For the Fixed Income and Other categories, the five factors are five international bond factor excess returns.15 Gross value added, defined in Equation (4), uses the stated benchmark and is expressed in millions of SEK. The last four rows of panel B of Table 1 show the distribution of these alternative performance measures across funds. The average gross CAPM alpha is 0.1% and has an even wider dispersion than the main abnormal return measure. Average three- and five-factor alphas are also close to zero with similar dispersion. Median gross value added is 1.3 million SEK. It is negative for slightly less than half the fund-year observations, and has a right tail of 143 million SEK at the 90th percentile.

1.2.2 Manager level.

Panel C of Table 1 reports manager characteristics for the final sample of manager-year observations.17 The average and median age is 42 years. Their average years of experience managing mutual funds is 5.9, with a standard deviation of 4.7 years. They have 15 years of formal education on average, which reflects having obtained a college degree. The manager at the 10th percentile has only completed high-school whereas the top 25% have completed at least one additional one-year degree. We calculate the fraction of manager |$m$|’s funds that are co-managed (|${\it Coman}$|), the average number of teams manager that |$m$| is on in a given year (|${\it Teams}$|), and the average team size, excluding the manager herself, for the funds managed by manager |$m$| (|${\it TeamSize}$|). The median manager co-manages 12% of her AUM, is on 0.92 teams, and has 0.14 teammates. There is nontrivial dispersion in all of these variables. Managers mostly manage funds within a single investment category: the average number of investment categories in manager |$m$|’s portfolio of funds (|${\it NumCat}$|), in a given year, is typically 1, with less than 20% managing assets in more than one category.

Our main outcome variable is the labor income (|$L_{\it mt}$|) of a mutual fund manager |$m$| in year |$t$|. Labor income is defined as regular salary and benefits plus business income, before taxes. Including business income is useful for cases where the manager is running a fund for a fund family as a self-employed consultant. From the perspective of Swedish tax legislation, any bonus pay from the employer is considered as labor income and included in our measure. Panel D reports income measures in thousands of Swedish kronor (SEK). The median fund manager earns 1.2 million SEK in labor income (about

While there is substantial inequality in labor income in our sample, it is not the case that a handful of managers account for most of the labor income or the assets under management. To see this, Figure 2 plots the cumulative fraction of labor income and assets under management for all managers in the last year of our sample, 2015. Managers are ordered from highest to lowest pay on the horizontal axis. The left panel plots the number of managers on the x-axis, while the right panel plots the log pay. The middle one hundred managers out of 246 managers, whose log labor income lies between 13.8 and 14.4, account for one-third of the income paid and over 40% of AUM. These managers manage a significant amount of assets.

As a second measure of pay, we add dividend income (|$D_{\it m,t}$|) to labor income to obtain total income (|$Y_{\it m,t}$|). The advantage of including dividend income is that we obtain a more comprehensive measure of pay. Some mutual fund managers may be compensated with stock or may have personal companies that are shareholders in the mutual fund family. That personal company then pays dividends to the individual. These payments reflect, at least in part, the efforts and talents of the manager. Payments through dividends may also be a more tax-efficient way of providing compensation.18 There are two disadvantages. We only have data on total dividend income, so that dividend income includes dividends from all other equity positions the manager has, including many that have no relationship to his or her employment. Second, the timing of the dividend payments from the personal company to the individual is arbitrary and may break the link between performance in year |$t-1$| and total pay in year |$t$|. The median fund manager has very little dividend income. But the distribution is extremely right-skewed.19 Dividend income is 0.5 million at the 90th percentile and 0.8 million on average. The standard deviation is 8.7 million. In other words, we have some extremely high-earning individuals in our data set, even by U.S. standards. Total income averages 2.4 million SEK or

1.2.3 Firm level.

Each fund company or firm offers multiple funds and employs many managers. Panel E of Table 1 aggregates up from the fund to the firm level. Our sample contains about 930 unique firm-year observations. The average AUM at the firm level is 25 billion SEK, the median is 4 billion. The average TER at the firm level remains around 1.4%. Firm revenue averages 280 million SEK. From the Serrano accounting data base, we obtain net firm profits. Median firm profits are 11 million SEK, mean profits 58 million SEK. We define |${\it Profit}^+$| as the positive part of profits.20 It is only defined for firm-year observations with positive profits. The average firm has 11.2 funds and employs 7.6 managers in a given year in our data set, while 10% percent of firm-year observations have more than 31 funds and more than 20 fund managers.

2. Manager-level Determinants of Compensation

This section investigates the manager-level determinants of labor income in the cross-section of mutual fund managers. The next section argues that firm-level characteristics co-determine fund manager compensation.

2.1. Pay-revenue sensitivity

2.1.1 Empirical specification.

In our first set of results, we ask whether managerial pay depends on the size of the fund(s) managed and the performance of the fund(s). As our main measure of size we use the fee revenue of the funds managed by a given manager. Fee revenue is easily measurable, and therefore contractible, and it is a measure of the sales revenue directly associated with the activities of the manager. As indicated above, manager-level revenue is the assets under management times total expense ratio, calculated for each month, and then added up across months. Since AUM and revenue change throughout the year, we want to allow for revenue to affect pay contemporaneously.21 Fund performance is lagged because the bonus received in year |$t$| typically reflects performance in the previous calendar year.

2.1.2 Sensitivity of pay to revenue.

To estimate the pay-revenue sensitivity (PRS) coefficient |$\beta$|, we set |$\gamma=0$| in Equation (11). In Column (1) of Table 2, we only include a constant and log revenue. We find an elasticity of pay to size of 0.153, which is measured precisely (standard error of 0.018). A 1% increase in the revenues from the funds a manager operates increases her pay by about 0.15 %. This specification rejects the null hypothesis of a compensation that is independent of fund size. Log revenue accounts for a substantial 13.9% of the overall variation in pay.

On the one hand, this result suggests that the owners and the managers of mutual funds have incentives that are aligned, in that both of their payoffs increase in fund revenue. It also shows that the manager-specific fund revenue matters for compensation.

On the other hand, large variation in fund revenue is associated with only modest variation in manager pay. A doubling of revenue from funds under management (increase by 100% or 1 log unit) increases pay by 15%. Fund managers capture only a small share of the additional fund revenues. To illustrate, consider a simple example with amounts converted to U.S. dollars. Average manager-level revenue is about

To further gauge the economic magnitude of the effect, we standardize log revenue by dividing by the cross-sectional standard deviation. Because fixed income and equity mutual funds may have different revenue distributions, we standardize investment category by category.23 We then reestimate the same regression specification but with standardized log revenue as independent variable. The main coefficients of interest are reported in the bottom panel of Table 2. A one-standard-deviation increase in log revenue is associated with a 28.1% increase in pay. This represents a 0.4-standard-deviation change in log labor income.

In Column (2), we add control variables |$X_{\it m,t-1}$|. These are measured annually and include: the manager’s experience in years worked as a fund manager (|${\it Exper}$|), experience squared (|${\it Exper}^2$|), age of the manager (|${\it Age}$|), age squared (|${\it Age}^2$|), years of education (|${\it Edu}$|), an indicator variable for a degree with a finance specialization (|${\it Finance}$|),24 the fraction of manager |$m$|’s funds that are co-managed (|${\it Coman}$|), the average number of teams manager |$m$| is on in a given year (|${\it Teams}$|), the average team size excluding the manager herself for the funds managed by manager |$m$| (|${\it TeamSize}$|), the average number of categories manager |$m$| runs (|${\it NumCat}$|), and investment category fixed effects. The equity funds category is the omitted category.

The control variables enter with the expected sign, and several are statistically significant. One year of additional experience as a fund manager increases pay by 3.2%. The returns to experience are concave. Older managers make more, and the returns to age are strongly concave, after controlling for experience. On average, a 45-year-old manager makes 7.3% more than a 40-year-old manager, using both linear and quadratic terms. An extra year of education increases pay by 1%. This effect is not significant because we have too little variation in years of education. Having a specialized finance education boosts pay by an economically and statistically significant 25.9%. A manager who co-manages all her funds has 22.3% lower pay than a manager who manages all funds by herself. Each additional team subtracts 2.6% from pay. Larger teams are associated with higher pay; each team member adds 11.4% to pay. Finally, a manager active in more than one investment category makes 9.9% per additional category, but this effect is imprecisely estimated. The specification includes investment category (asset class) fixed effects. The controls increase the |$R^2$| of this regression to 22.9%, a gain of 9.1 percentage points.

Taking into account controls does not change the sensitivity of pay to revenue by much. The elasticity point estimate is 0.141 and remains precisely estimated. The bottom panel of the table shows that a one-standard-deviation increase in revenue (relative to the other funds in the same category) increases pay by 25.3% once controls are included.

In Column (3) we add manager fixed effects. The sensitivity of pay to revenue is now identified from time-series variation for a given manager. Years in which the manager’s funds generate more fee revenue are years of higher managerial pay. The elasticity estimate drops only modestly to 0.123 and remains precisely estimated. A one-standard-deviation increase in revenue increases pay by 18.7%. Comparing the point estimates on size in Columns (2) and (3), we conclude that most of the variation in pay related to fund revenue is not driven by cross-sectional variation in constant skill levels.25

2.1.3 Log-log specification.

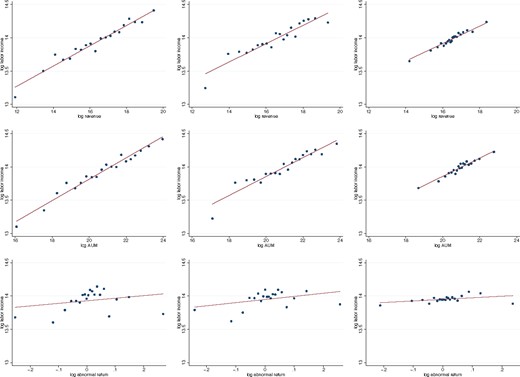

The top row of Figure 3 shows the relationship between log fund revenue (one the horizontal axis) and log pay (on the vertical axis). Each of the 20 points represents 5% of the observations. The best-fitting line through the points is also shown; its slope is the elasticity of pay to size. The left picture corresponds to Column (1) of Table 2, the middle picture shows the slope after including the controls and corresponds to Column (2), while the right panel controls for manager fixed effects in addition. The graphs make clear that a log-log specification for revenue and compensation fits the data very well.26 This log-log specification comes out of the matching framework of Gabaix and Landier (2008) and is also used for Swedish CEO pay by Adams, Keloharju, and Knupfer (2016).

Elasticity of pay to revenue, assets under management, and performance

Each dot pertains to 5% of all observations. The top row plots log revenue |$\log\left({\it REV}_{\it mt}\right)$| against log compensation |$\log\left(L_{\it mt}\right)$|, the middle row plots log AUM |$\log\left({\it AUM}_{\it mt}\right)$| against log compensation and the bottom row plots log abnormal return |$\log\left(1+R^{\it abn}_{\it mt}\right)$| against log compensation. The left panels are the raw data. The middle panel removes the effect of the control variables, year fixed effects, and category fixed effects. The right panels additionally remove manager fixed effects.

The middle panels in Figure 3 replace log revenue by log of assets under management. This alternative size measure of size displays a very similar linear-in-logs relationship to managerial pay. Given the similarity, we proceed with revenue as our preferred measure of size.

2.1.4 Comparison to Berk and Green.

To contextualize the pay-revenue sensitivity estimate of 0.15, it is useful to compare it with the PRS in a benchmark model. The frictionless delegation model of Berk and Green (2004) is a natural benchmark. In that model, each firm runs one fund. The fund manager has unknown ability to the owner and investors, and realizations of abnormal returns are combined with priors to form posterior beliefs on the skill (alpha) of the manager. The model assumes that there are no frictions in the second layer of delegation between the firm owner and the firm manager.27 Equivalently, managerial pay is proportional to firm revenue. Trivially, a regression of log labor income on log revenue delivers a PRS of 1 and an |$R^2$| of 100%. Moreover, controlling for manager fixed effects should capture the manager’s alpha quite well, especially for more experienced managers for whom the posterior precision of beliefs about alpha is high. Our results indicate a much lower PRS than 1, a much lower |$R^2$| than 100%, and a PRS estimate that is little affected by the inclusion of manager fixed effects. The model comparison provides further support for the claim that the estimated PRS is small.

2.2. Pay-performance sensitivity

A second natural manager-level candidate determinant of pay is the return performance of the manager. We define performance as the abnormal return, the manager’s gross return over the stated benchmark, and expressed in logs. We lag the abnormal return under the hypothesis that the return from the past year is what determines the bonus in the current year.

We estimate |$\gamma$| in Equation (11), and set |$\beta=0$|. Column (4) of Table 2 contains the simplest specification without controls or manager fixed effects. We find a baseline PPS of 0.34. The point estimate is significant at the 10% level. Variation in abnormal returns explains only 2.3% of variation in pay. The bottom panel indicates that a one-standard-deviation increase in abnormal return, relative to the other funds in the investment category, increases pay by 2.98%.

A one-percentage-point increase in the log annual abnormal return of a manager increases pay by 0.34%. This is a very small effect. Log pay increases from 13.59 when the net abnormal return is zero to 13.5934 (|$13.59 + 0.01 \times 0.34$|) when the annual abnormal return is 1%. At 7.5 SEK per USD, the (nontrivial) increase of 1% point in abnormal return represents an annual pay increase of a paltry

Column (5) adds the control variables. The performance sensitivity coefficient increases in magnitude to 0.407 as well as in significance (5% level). There is some evidence that managerial pay is linked to the abnormal returns, after controlling for experience, age, education, and so on. But the economic magnitude of the pay-for-performance sensitivity remains small. Even though performance-based pay may be prevalent, as suggested by Ma, Tang, and Gomez (2016), the importance of the performance-based component of compensation appears modest at best. One possibility we explore is that pay is tied to additional lags of abnormal returns.

Column (6) adds manager fixed effects. The semielasticity drops to 0.093 and loses significance. Whatever PPS we find is largely driven by cross-sectional variation rather than time-series variation for a given manager.

2.2.1 Log-log specification.

The bottom row of Figure 3 visually confirms the weak relationship between performance (log gross abnormal return on the horizontal axis) and log pay (on the vertical axis). The slope of the best-fitting line through the points is the semi-elasticity of pay to performance. The left picture corresponds to Column (4) of Table 2, the middle picture shows the slope after including the controls and corresponds to Column (5), while the right panel controls for manager fixed effects in addition (Column 6). The graphs make clear that a linear-in-logs specification for abnormal return, and pay does not fit the data that well.28 We explore different nonlinear specifications in Section 4.1.

2.2.2 Comparison to Berk and Green.

To gauge how small the estimated PPS is, we return to the Berk and Green model. We simulate their benchmark calibration and estimate a panel regression of log compensation on the lagged log abnormal return in simulated data. We find a PPS estimate of 1.61 without and 0.75 with fixed effects. The estimates are a factor four to six times larger than the estimates in the data. In a world with uncertainty about managerial skill, abnormal returns are informative to investors and managers alike. Investors reward high-performance fund managers with flows and fee revenues. The data suggest much weaker responses than in the model. Simulation and calibration details are in Appendix B.

2.3. Revenue as measure of skill

In this section, we investigate the relationship between pay and fee revenue further. Specifically, we address the possibility that pay is sensitive to fee revenue because revenue contains performance-related components that are associated with pay. Managers with higher abnormal returns mechanically grow their AUM, and hence their fee revenue; they may attract more investor flows (Sirri and Tufano 1998); may be able to charge higher expense ratios (Warner and Wu 2011); and may be promoted by firm owners to run more or larger funds (Berk, van Binsbergen, and Liu 2017). However, revenue could also differ across funds and over time for reasons unrelated to the manager’s investment skill. Firm-level variables, such as advertising/marketing, distribution network, or common research infrastructure, could affect fund revenue. So could managerial talents unrelated to investment skill, such as fundraising ability or people management skills. Finally, fund flows could result from portfolio rebalancing or from investors responding to benchmark returns (Del Guercio and Reuter 2014).

To remove the performance-related component of revenue, we regress log revenue on log abnormal return. The residual of this regression is the component of log revenue that is orthogonal to performance, |$\log({\it REVorth}_{\it m,t})$|. Column (2) of Table 3 orthogonalizes log revenue in year |$t$| to both the current year’s abnormal return, |$\log(1+R^{\it abn}_{\it m,t})$|, and the previous year’s, |$\log(1+R^{\it abn}_{\it m,t-1})$|. It shows that the sensitivity of pay to revenue is essentially unaffected. Compared with our benchmark specification, repeated for convenience in Column (1), the PRS mildly increases from 0.141 to 0.144. In Column (3), log revenue is orthogonalized to two additional lags of abnormal return, |$\log(1+R^{\it abn}_{\it m,t-2})$| and |$\log(1+R^{\it abn}_{\it m,t-3})$|. The PRS remains stable at 0.134.29 In sum, the PRS is barely affected even after the effect of manager-level abnormal returns is purged from revenue.

Decomposing the effect of revenue on pay

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$ \log ( {\it REV}_{\it m,t} )$| | 0.141*** | 0.140*** | |||||

| (0.0194) | (0.0195) | ||||||

| |$ \log ({\it REVorth}_{\it m,t})$| | 0.144*** | 0.134*** | 0.144*** | 0.144*** | 0.130*** | ||

| (0.0194) | (0.0257) | (0.0193) | (0.0193) | (0.0255) | |||

| |$ \log (1+R^{\it abn}_{\it m,t})$| | 0.0646 | 0.253 | |||||

| (0.151) | (0.194) | ||||||

| |$ \log (1+R^{\it abn}_{{\it m,t-}1})$| | 0.148 | 0.327* | 0.325* | 0.586** | |||

| (0.176) | (0.174) | (0.170) | (0.236) | ||||

| |$ \log (1+R^{\it abn}_{{\it m,t-}2})$| | 0.583*** | ||||||

| (0.200) | |||||||

| |$ \log(1+R^{\it abn}_{{\it m,t-}3})$| | 0.274* | ||||||

| (0.158) | |||||||

| Constant | 7.173*** | 9.509*** | 9.074*** | 7.212*** | 9.563*** | 9.561*** | 9.141*** |

| (0.595) | (0.639) | (0.894) | (0.602) | (0.646) | (0.645) | (0.904) | |

| Manager FE | No | No | No | No | No | No | No |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Firm FE | No | No | No | No | No | No | No |

| |$N$| | 2,898 | 2,883 | 1,932 | 2,898 | 2,883 | 2,883 | 1,932 |

| Adjusted |$R^{2}$| | 0.229 | 0.233 | 0.182 | 0.229 | 0.234 | 0.234 | 0.190 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$ \log ( {\it REV}_{\it m,t} )$| | 0.141*** | 0.140*** | |||||

| (0.0194) | (0.0195) | ||||||

| |$ \log ({\it REVorth}_{\it m,t})$| | 0.144*** | 0.134*** | 0.144*** | 0.144*** | 0.130*** | ||

| (0.0194) | (0.0257) | (0.0193) | (0.0193) | (0.0255) | |||

| |$ \log (1+R^{\it abn}_{\it m,t})$| | 0.0646 | 0.253 | |||||

| (0.151) | (0.194) | ||||||

| |$ \log (1+R^{\it abn}_{{\it m,t-}1})$| | 0.148 | 0.327* | 0.325* | 0.586** | |||

| (0.176) | (0.174) | (0.170) | (0.236) | ||||

| |$ \log (1+R^{\it abn}_{{\it m,t-}2})$| | 0.583*** | ||||||

| (0.200) | |||||||

| |$ \log(1+R^{\it abn}_{{\it m,t-}3})$| | 0.274* | ||||||

| (0.158) | |||||||

| Constant | 7.173*** | 9.509*** | 9.074*** | 7.212*** | 9.563*** | 9.561*** | 9.141*** |

| (0.595) | (0.639) | (0.894) | (0.602) | (0.646) | (0.645) | (0.904) | |

| Manager FE | No | No | No | No | No | No | No |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Firm FE | No | No | No | No | No | No | No |

| |$N$| | 2,898 | 2,883 | 1,932 | 2,898 | 2,883 | 2,883 | 1,932 |

| Adjusted |$R^{2}$| | 0.229 | 0.233 | 0.182 | 0.229 | 0.234 | 0.234 | 0.190 |

See Table 2. The second, fifth, and sixth columns use as the independent variable the part of log revenue that is orthogonal to abnormal returns at time |$t$| and |$t-1$|. The third and seventh columns additionally orthogonalize revenue to abnormal returns at times |$t-2$| and |$t-3$|.

Decomposing the effect of revenue on pay

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$ \log ( {\it REV}_{\it m,t} )$| | 0.141*** | 0.140*** | |||||

| (0.0194) | (0.0195) | ||||||

| |$ \log ({\it REVorth}_{\it m,t})$| | 0.144*** | 0.134*** | 0.144*** | 0.144*** | 0.130*** | ||

| (0.0194) | (0.0257) | (0.0193) | (0.0193) | (0.0255) | |||

| |$ \log (1+R^{\it abn}_{\it m,t})$| | 0.0646 | 0.253 | |||||

| (0.151) | (0.194) | ||||||

| |$ \log (1+R^{\it abn}_{{\it m,t-}1})$| | 0.148 | 0.327* | 0.325* | 0.586** | |||

| (0.176) | (0.174) | (0.170) | (0.236) | ||||

| |$ \log (1+R^{\it abn}_{{\it m,t-}2})$| | 0.583*** | ||||||

| (0.200) | |||||||

| |$ \log(1+R^{\it abn}_{{\it m,t-}3})$| | 0.274* | ||||||

| (0.158) | |||||||

| Constant | 7.173*** | 9.509*** | 9.074*** | 7.212*** | 9.563*** | 9.561*** | 9.141*** |

| (0.595) | (0.639) | (0.894) | (0.602) | (0.646) | (0.645) | (0.904) | |

| Manager FE | No | No | No | No | No | No | No |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Firm FE | No | No | No | No | No | No | No |

| |$N$| | 2,898 | 2,883 | 1,932 | 2,898 | 2,883 | 2,883 | 1,932 |

| Adjusted |$R^{2}$| | 0.229 | 0.233 | 0.182 | 0.229 | 0.234 | 0.234 | 0.190 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$ \log ( {\it REV}_{\it m,t} )$| | 0.141*** | 0.140*** | |||||

| (0.0194) | (0.0195) | ||||||

| |$ \log ({\it REVorth}_{\it m,t})$| | 0.144*** | 0.134*** | 0.144*** | 0.144*** | 0.130*** | ||

| (0.0194) | (0.0257) | (0.0193) | (0.0193) | (0.0255) | |||

| |$ \log (1+R^{\it abn}_{\it m,t})$| | 0.0646 | 0.253 | |||||

| (0.151) | (0.194) | ||||||

| |$ \log (1+R^{\it abn}_{{\it m,t-}1})$| | 0.148 | 0.327* | 0.325* | 0.586** | |||

| (0.176) | (0.174) | (0.170) | (0.236) | ||||

| |$ \log (1+R^{\it abn}_{{\it m,t-}2})$| | 0.583*** | ||||||

| (0.200) | |||||||

| |$ \log(1+R^{\it abn}_{{\it m,t-}3})$| | 0.274* | ||||||

| (0.158) | |||||||

| Constant | 7.173*** | 9.509*** | 9.074*** | 7.212*** | 9.563*** | 9.561*** | 9.141*** |

| (0.595) | (0.639) | (0.894) | (0.602) | (0.646) | (0.645) | (0.904) | |

| Manager FE | No | No | No | No | No | No | No |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Firm FE | No | No | No | No | No | No | No |

| |$N$| | 2,898 | 2,883 | 1,932 | 2,898 | 2,883 | 2,883 | 1,932 |

| Adjusted |$R^{2}$| | 0.229 | 0.233 | 0.182 | 0.229 | 0.234 | 0.234 | 0.190 |

See Table 2. The second, fifth, and sixth columns use as the independent variable the part of log revenue that is orthogonal to abnormal returns at time |$t$| and |$t-1$|. The third and seventh columns additionally orthogonalize revenue to abnormal returns at times |$t-2$| and |$t-3$|.

Next, we ask how the pay-performance sensitivity is affected by the removal of the performance-related components of revenue. Columns (4)–(7) of Table 3 contain the results. Column (4) estimates Equation (11) as a reference point, and finds a PRS of 0.140 and a PPS of 0.148, similar to the estimates in Table 2. Column (5) shows that when revenue has been orthogonalized to current and lagged abnormal return, the PPS increases from 0.148 to 0.327 and turns marginally significant. Column (6) adds the contemporaneous abnormal return, which does not alter the estimates. In Column (7), we use the revenue measure that has been orthogonalized to current and three years’ worth of lagged abnormal returns instead, and include all abnormal return terms. The main PRS coefficient increases further to 0.586 and becomes significant at the 5% level. We discuss the effect of the additional lags of returns in Section 2.4. In sum, the sensitivity of pay to performance increases once the abnormal return term captures not only the direct effect of higher return on compensation (the bonus part of pay that is tied to performance), but also the indirect effects of higher abnormal return on revenue (part of the pay tied to revenue). Nevertheless, the economic effect remains very small, with a one-percentage-point increase in abnormal return resulting in a mere 0.586% increase in pay.

Appendix C explores which components of revenue are responsible for the undiminished sensitivity of pay to orthogonalized revenue. It finds nonzero elasticities of pay to several of these components, including lagged revenues, TER growth, benchmark returns, inflows unrelated to performance, and AUM from funds newly assigned to a manager, after these components have been orthogonalized to performance.

2.4. Longer performance evaluation periods

Since returns and abnormal returns are noisy measures of investment skill, performance-based pay may depend not only on last year’s compensation but on longer lags of abnormal returns. Two pieces of empirical evidence are consistent with this conjecture. U.S. mutual funds report mean and median performance evaluation periods of three years.30 Since 2009, new European-level regulation came into place stipulating that a fraction of variable pay must be postponed for three years. Theoretically, fund owners and investors who are learning about a fund manager’s investment skill would only gradually update their posterior about skill.

Table 4 extends our baseline specification for log labor income, reprised in Column (1), by including one or two additional lags of abnormal returns. This is done in Columns (4) and (6). Twice-lagged abnormal returns enter significantly with an estimated elasticity of 0.33. Thrice-lagged returns in Column (6) are imprecisely estimated at 0.19. The last column replaces revenue by revenue orthogonalized to current and three lags of abnormal returns. As explained above, this reallocates the performance-related components of revenue to the abnormal return terms. The PPS coefficients are 0.61, 0.57, and 0.29, all different from zero. While these coefficients are larger and more significant, the economic magnitude of the PPS remains modest at best. A one-percentage-point abnormal return in each of the past three years, which is a nontrivial feat in light of the weak evidence on performance persistence, increases pay by less than 2%.31 Simulations from the Berk and Green model with lagged abnormal returns confirm that our PPS coefficients are low; they are more than 50% larger in the model than in the data. Appendix B contains the details.

Longer evaluation periods

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |$\log (L_{\it m,t})$| | |

| |$\log ({\it REV}_{\it m,t})$| | 0.140*** | 0.143*** | 0.135*** | 0.141*** | 0.132*** | 0.131*** | |

| (0.0195) | (0.0220) | (0.0256) | (0.0222) | (0.0256) | (0.0255) | ||

| |$\log({\it REVorth}_{\it m,t})$| | 0.131*** | ||||||

| (0.0256) | |||||||

| |$\log (1+R^{\it abn}_{{\it m,t-}1})$| | 0.148 | 0.276 | 0.348 | 0.278 | 0.348 | 0.366 | 0.611** |

| (0.176) | (0.214) | (0.248) | (0.214) | (0.249) | (0.253) | (0.246) | |

| |$\log (1+R^{\it abn}_{{\it m,t-}2} )$| | 0.330** | 0.452** | 0.462** | 0.573*** | |||

| (0.163) | (0.193) | (0.197) | (0.196) | ||||

| |$\log (1+R^{\it abn}_{{\it m,t-}3})$| | 0.198 | 0.286* | |||||

| (0.157) | (0.160) | ||||||

| Constant | 7.212*** | 6.939*** | 6.871*** | 7.034*** | 6.904*** | 6.969*** | 9.136*** |

| (0.602) | (0.722) | (0.866) | (0.732) | (0.868) | (0.876) | (0.902) | |

| Manager FE | No | No | No | No | No | No | No |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Category FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Firm FE | No | No | No | No | No | No | No |

| |$N$| | 2,898 | 2,411 | 1,932 | 2,411 | 1,932 | 1,932 | 1,932 |