Abstract

We show that banks cross-sell future deposits and loans to existing household depositors. A bank is 20-percentage-points more likely to sell a loan to an existing depositor than to an otherwise comparable household. Existing depositors pay a premium when borrowing, and we find no indication that banks obtain an informational advantage on such borrowers, suggesting that the cross-selling is driven more by demand than by supply complementarities. These demand complementarities are in turn driven more by stickiness rather than by unobserved persistent preferences. Finally, banks internalize future cross-selling potential when setting deposit rates.

Authors have furnished an Internet Appendix, which is available on the Oxford University Press Web site next to the link to the final published paper online

The majority of existing empirical research on financial intermediation between households and banks, as well as between firms and banks, focuses on the sale of a single banking product, such as mortgages, corporate loans, credit cards, or deposits. This narrow focus results typically from data limitations rather than from a lack of interesting economic questions regarding the behavior of banks as multiproduct firms. In this paper, we utilize unique data encompassing both loans and deposits for all household-bank relationships in Norway to investigate how different bank products interact across both sides of bank balance sheets. Specifically, we document, analyze, and explore the implications of cross-selling. In our setting, cross-selling refers to the case when existing depositors are more likely, relative to otherwise comparable households, to purchase other bank services in the future, such as future deposit services or loans. Through cross-selling, the value of a depositor to a bank consists of the current deposit spread between policy and deposit rates, as well as the expected future profits generated from cross-selling activities. Cross-selling is well-known in the marketing literature (e.g., Li, Sun, and Montgomery 2011 or Li, Sun, and Wilcox 2005), but because of the data limitations discussed above, it has been less explored in the context of banking.

We use administrative relationship-level data that cover every deposit and loan relationship in each year between 2004 and 2018 for all households and banks in Norway. We observe both deposit and loan volumes for each bank-household relationship, as well as the interest paid or received. We match this with detailed administrative panel data on household balance sheets, demographics, and bank-level information. We explore to what extent banks cross-sell services to existing depositors, which mechanisms are behind cross-selling, and whether the cross-selling potential of a given client based on that client’s observables matters for the ex ante pricing of deposits. We make three broad contributions to the literature.

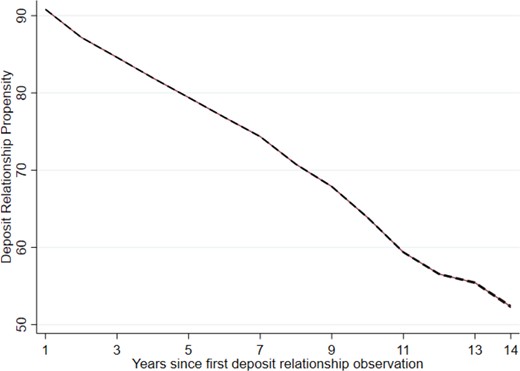

Our first main contribution is to document substantial cross-selling in banking to households, in terms of both future deposit accounts and future loans to existing depositors. On the deposit side, we show that one year after we first observe a household to have deposits with a bank, the household is about 90 percentage points (pp) more likely to still have deposits there compared to another household, even when we condition on the household’s outside options. The prevalence of this household inaction falls only slowly in the subsequent 14 years. It costs households up to 2 pp of deposit interest p.a.

On the loan side, we find that existing depositors are about 20 pp more likely to take out a loan from the same bank in the next 14 years, compared to a household in the same municipality, age, salary and education group but with deposits elsewhere. We refer to this as “depositor borrower conversion.” It occurs when households move within or even across municipalities, in the subsample of densely populated municipalities, or in municipalities where competition is high. This suggests that conversion is unlikely to be driven by location alone.

Our second main contribution to the literature is to explore the mechanisms behind cross-selling. We focus on the cross-selling of future loans and hypothesize that cross-selling can occur because either households want or must remain at their existing bank (“demand complementarities”) or banks obtain, through repeated interaction, better information about clients and therefore offer existing depositors better loan rates (“supply complementarities”). We thus investigate empirically whether existing depositors receive a discount on future loans, which would suggest that banks prefer them as borrowers over new clients or pay more as they prefer to stick with their relationship bank. We find existing depositors to pay a risk-adjusted loan premium of about 20 basis points (bp) on future loans. Consistent with that, we find that, while banks do charge higher loan prices to borrowers who later default, this is not more pronounced for existing depositors, suggesting that banks are not better at screening existing relative to new clients. This is in contrast with the literature on bank-firm relationships (e.g., Petersen and Rajan 1994 or Mester, Nakamura, and Renault 2007), as well as with recent evidence on the pricing of household credit card debt (Berger et al. forthcoming) where supply complementarities matter. It is consistent with household mortgage lending being more standardized and less affected by asymmetric information. In sum, our results support demand complementarities as key driver of depositor borrower conversion in our setup.

We then explore in turn the different channels through which such demand complementarities could arise. We distinguish between households’ unobserved persistent preferences for particular bank features and inaction caused by stickiness as in Andersen et al. (2020) or Handel (2013). We first adopt an instrumental variables approach where we restrict attention to households that change their municipality. We use the market share of a bank in a moving household’s old municipality as instrument for whether the household is an existing depositor at a bank in the household’s new municipality. This instrument focuses on variation in deposit relationship existence driven by availability rather than preferences. Focusing on this source of variation generates qualitatively similar and if anything larger estimates of depositor borrower conversion. This suggests that cross-selling in our setup is mostly driven by stickiness rather than by persistent preferences. We corroborate this latter conclusion further in two ways. First, we show that the extent of cross-selling correlates with household characteristics, some of which have been highlighted as determinants of switching costs due to psychological and information gathering costs (Andersen et al. 2020). Second, we hypothesize based on Klemperer (1995) that switching costs are increasing in the length of a bank household relationship, while unobserved preferences are not, and show that otherwise comparable borrowers with different tenure at their bank have different propensities to switch banks when taking up a new loan. Specifically, the likelihood of switching banks for a new loan decreases by 5 pp per year of bank tenure.1

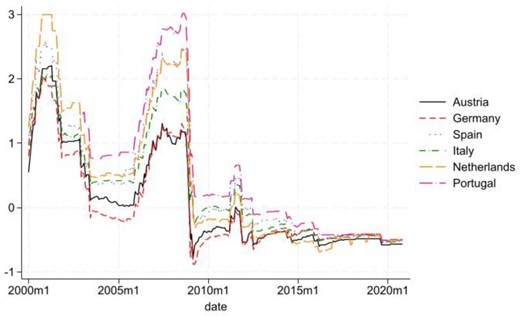

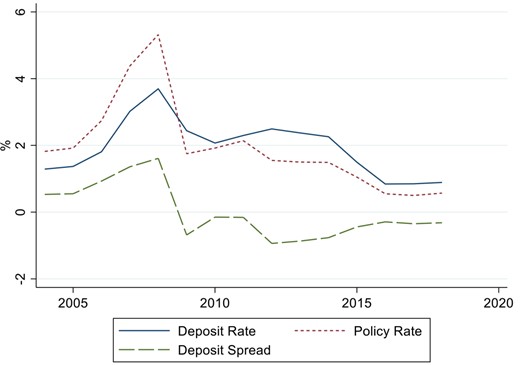

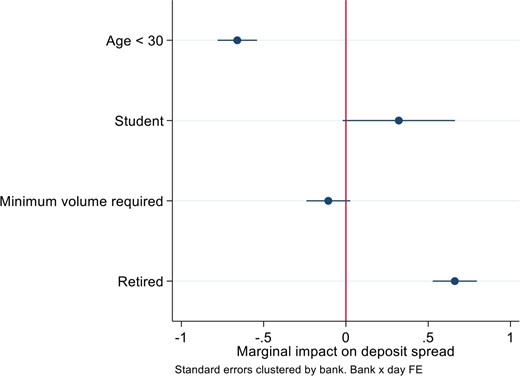

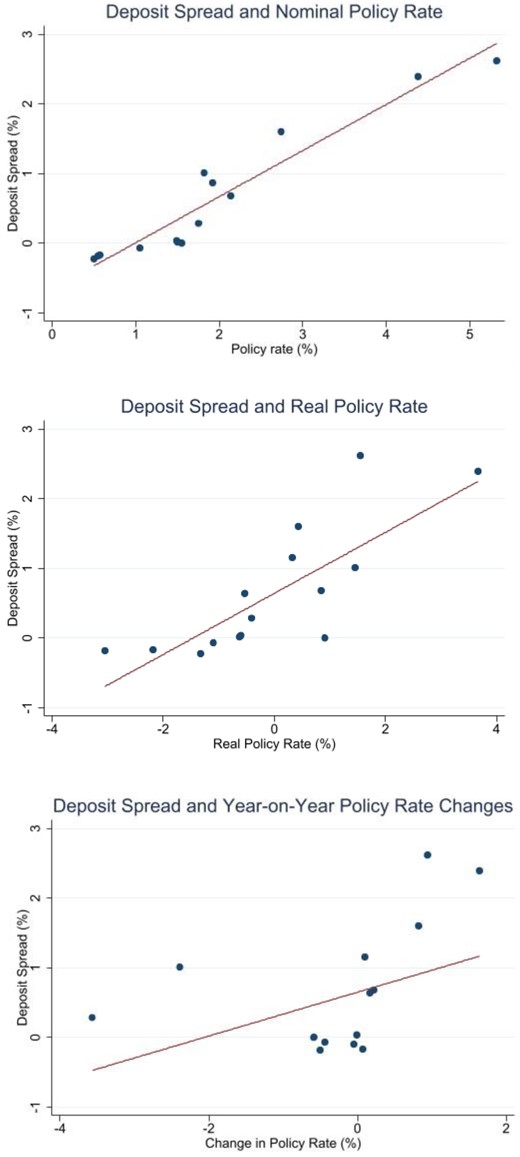

Our third main contribution is to document the implications of cross-selling for deposit pricing. We focus on whether cross-selling can explain cross-sectional, as well as time-series variation in deposit rates. We show that banks tend to offer more attractive deposit spreads to households who, in expectation, borrow more in the future. We find among others lower deposit spreads for those below 30 years old, parents, and those with more income. These are also households that in expectation will borrow more from their existing bank in the future. The effects are quantitatively important. For instance, on average, deposit accounts for households younger than 30 years old have a 28-bp lower deposit spread. This implies that banks, on average, lose and households earn money compared to interbank market rates on these accounts alone. At the same time, we notice that the cross-selling profits analyzed in our setup occur typically only several years after the initial onboarding of a new deposit client. Consequently, a bank’s optimal strategy would seem to involve offering a larger initial deposit spread discount when policy rates and discount rates are lower. Cross-selling can therefore help rationalize why banks have accepted negative deposit spreads in times of low policy rates as shown in Figure 1 and Figure 2. Negative deposit spreads also contrast monopolistic bank price-setting models with single goods like the Monti-Klein model (e.g., Freixas and Rochet 2008).

Deposit spreads from selected European countries

This figure plots the European Central Bank’s (ECB) Deposit Facility Rates (DFR; see https://www.ecb.europa.eu/ecb/educational/explainers/tell-me/html/what-is-the-deposit-facility-rate.en.html) less the average deposit rates for six selected euro area economies by month.

Source: ECB Statistical Data Warehouse (https://sdw.ecb.europa.eu/browse.do?node=9691394)

Average deposit spreads in Norway

This figure plots Norwegian policy rates (https://www.norges-bank.no/en/topics/Monetary-policy/Policy-rate/), average deposit rates taken from www.finansportalen.no/, and their difference by year.

1 Contributions to the Existing Literature

Our paper relates to at least three strands of the literature: (1) the benefits of issuing deposits for banks, (2) the role of switching costs and inaction in relationship banking, and (3) the broader literature on cross-selling.

First, a rich literature has emphasized the benefits of deposits for banks. Drechsler, Savov, and Schnabl (2017) emphasize that deposits are a cheap and stable financing source for lending. Berlin and Mester (1999) and Drechsler, Savov, and Schnabl (2021) stress that deposit interest rates have a low sensitivity to market interest rates and hence allow banks to take on less interest rate risk. Li, Loutskina, and Strahan (2023) in turn point out that deposits are associated with limited liquidity risk. Beyond these benefits of deposits as a source to refinance lending, Mester (1987), Kashyap, Rajan, and Stein (2002), Gatev, Schuermann, and Strahan (2009), or Robles-Garcia, Benetton, and Buchak (2022) emphasize different synergies from issuing deposits together with offering other bank services, such as lending, for instance, by using the same branches, staff, IT, or other resources. Our paper contributes to this literature by documenting and exploring a new channel of how deposits add value for banks via generating more scope for cross-selling of loans to the same household. Our paper therefore lends support to the view that the activities on the asset and the liability side of banks are related, in contrast to, for instance, the baseline version of the Monti-Klein model (Freixas and Rochet 2008).

Second, a large literature has documented switching costs in banking. One strand of the literature focuses on switching costs within the market for specific products, for instance, U.S. (Sharpe 1997), Finnish (Shy 2002), Spanish (Carbo-Valverde, Hannan, and Rodriguez-Fernandez 2011), or Dutch (Deuflhard 2018) deposit markets, or U.S. (Kim, Kliger, and Vale 2003) or European (Liaudinskas and Grigaite 2021) loan markets. Another strand of this literature focuses on the relationship aspect of switching costs and the role of asymmetric information. Petersen and Rajan (1994) and Mester, Nakamura, and Renault (2007) are seminal papers in this literature, both focusing on bank-firm relationships where much lending is uncollateralized and creditworthiness is often harder to evaluate than for the average household. These studies emphasize the value of a bank’s prior knowledge of the client in facilitating screening. Our paper contributes to this literature by documenting and exploring the drivers of switching costs in bank-household relationships.

Third, several studies explore the importance and determinants of cross-selling. Li, Sun, and Montgomery (2011) and Li, Sun, and Wilcox (2005) posit a theory of how institutions can improve profits from cross-selling. Gupta et al. (2006) compute customer lifetime value (CLV) as net present value from each customer and discuss different models to estimate for each client the optimal acquisition cost in order to optimize profits from the sum of acquisition, retention and cross-selling. They focus on acquisition via marketing, we focus on product pricing. Implications of client stickiness also have been explored in the industrial organization literature (see, e.g., Tirole 1988 or Klemperer 1995). An emerging literature focuses on cross-selling in banking. Hellmann, Lindsey, and Puri (2008), Laux and Walz (2009), Ivashina and Kovner (2011), Carbo-Valverde, Hannan, and Rodriguez-Fernandez (2011), Lepetit et al. (2008), Agarwal et al. (2018), Neuhann and Saidi (2018), Qi (2017), Norden and Weber (2010), and Santikian (2014) focus on either bank-level indications of cross-selling or the cross-selling of products by banks to firms. A common thread of many of these papers is the driving factor supply complementarities. We contribute to this literature with evidence on cross-selling to households. In contrast to the literature on bank-firm relationships, we show that demand complementarities are an important determinant of cross-selling to households, thus contributing to market power and bank franchise values.2

2 Data and Summary Statistics

In this section we describe the main data sources, the measurement of key variables and provide and discuss some summary statistics of the variables most relevant to our analysis.

2.1 Data sources

We use data from four sources in the analysis.

2.1.1 Deposit and loans accounts

The first data source is relationship-level data from the Norwegian tax register covering all outstanding loan and deposit relationships between Norwegian individuals and Norwegian banks.3 These data contain information on the amount deposited at or borrowed from a given bank, in addition to the observed interest paid or received over the year. The data are annual, reported at the end of the year and covers the period 2004–2018. The data are high-quality and third-party reported by banks and other institutions. These data—in addition to the data source discussed next—have been obtained by the Tax Authorities for tax purposes. Norway levies a wealth tax on households, and as such the Tax Authorities are enabled a detailed overview of the balance sheet of each Norwegian household, including deposit and loan information. Most of the loans in our data are mortgages, and most deposit accounts have either a short fixed term or an indefinite term. At an aggregate level, 85% of household credit in Norway are mortgages (Baltzersen 2020). More than 99% of outstanding deposits have a maturity of less than a year.

2.1.2 Other household information

The second data source is a comprehensive overview of individual-level information for all Norwegian taxpayers. This information includes a detailed breakdown of individuals’ balance sheets, containing information on (among other things) income sources, assets, and liabilities. It also contains information about demographics, including age, education, and location. These annual data are reported at the end of the year and cover the years 2004–2018.

2.1.3 Bank-level information

We add bank-level information from the supervisory database ORBOF, which covers all major balance sheet and income statement items for the universe of banks operating in Norway.

2.1.4 Finansportalen.no

The fourth and final data source is daily interest rates at the product level from the price comparison website Finansportalen.no. Since 2008, all banks have been obliged by law to report each day the interest rate on their outstanding deposit products, as well as different contractual terms, such as volume limits and age restrictions.

2.1.5 Combining the data

Our primary data for analysis consists of merged data from the three first data sources. The fourth data set is used for supplementary analysis. We aggregate our data to the bank-household-year level, as major financial decisions like mortgage borrowing are often decided at the household level. So the unit of observation in our data is a bank-household-year triplet.

When analyzing depositor borrower conversion, that is, the propensity for household h to take out a loan with bank b in year t conditional on having had deposits there in prior years, we do not count deposit accounts opened in the year in which the loan is initiated. By dropping those (small number of) cases, we may slightly underestimate the positive effect of a deposit relationship on starting another relationship with the same bank. Still, we wish to avoid artificial inflation of the importance of the relationship by counting deposit accounts opened as the bank required the household to do so in connection with a loan.

2.2 Variable definitions and summary statistics

Most of the variables we use in our analysis are relatively straightforward, that is, loan and deposit volumes. However, some key variables are constructed based on the raw data. Below, we will outline how we construct these variables.

2.2.1 Deposit and loan rates

To impute deposit (loan) rates, we divide the interest a household receives (pays) from (to) a bank in a given year by the deposits (debt) it holds there. We compute debt and deposits as the average between the outstanding balances in years t – 1 and t.4 We then compute loan spreads as the imputed loan rate less the policy rate, and deposit spreads as the policy rate less the imputed deposit rate.

2.2.2 Education characteristics

We bin households into different groups of different variables to ensure comparability between households. For most variables, for instance, labor income, we bin based on the household’s position in the distribution (i.e., first, second, third, and fourth quartiles). For education, however, we bin them into four groups based on absolute education levels: (1) those with at most elementary education, (2) those with elementary + high school, (3) those with a bachelor’s degree (undergraduate level), and (4) those with a master’s degree or higher (graduate level).

2.2.3 Market power metrics

As we observe the universe of Norwegian deposit and loan balances, we can also compute each bank’s market share for each of deposit and loan products in each municipality.5 We compute market shares, Herfindahl-Hirschmann indices (HHI) for both loans and deposits within each municipality, as well as banks’ weighted HHIs as the weighted average of the HHIs in the municipalities the banks operate in, weighted with their exposures to these areas.

2.2.4 Summary statistics

In Table 1, panel A, we provide summary statistics on the bank-household-year triplets underlying most of our analyses. To start with, we see that the policy rate varies between 0.50% and 5.32% and averaged 1.82% in our sample. Imputed deposit rates vary between 0.07% and 4.92%, which implies deposit spreads of between –2.84 and 4.76, with an average of 0.54 pp. Loan rates range between 1.23% and 9.01% and an average 3.59%, which results in raw loan spreads of between 3.12% and 7.19%, with an average of 1.54%. Average deposit volumes correspond to NOK 140,000, or roughly about US$14,000 or 14,000 euro, while loan volumes average NOK 160,000 and in the last observed relationship year NOK 1.1 million. Household debt to all banks used by that household across all years observed is on average NOK 970,000. Deposit interest lost from failing to switch banks averages 2.4 pp, or 320,000 NOK p.a., when comparing the interest households actually earn to the highest rate earned by anyone in the same municipality and year including accounts not everyone is eligible for. The duration of bank relationships we observe ranges from 1 to 15 years and averages close to 9 years.

Summary statistics

| Observations | Mean | SD | Min | Max | |

|---|---|---|---|---|---|

| A. Relationship characteristics | |||||

| Policy rate (pp) | 46,132,510 | 1.82 | 1.23 | 0.50 | 5.32 |

| Deposit rate (pp) | 46,132,510 | 1.29 | 1.18 | 0.07 | 4.92 |

| Deposit spread (pp) | 46,132,510 | 0.54 | 1.37 | –2.84 | 4.76 |

| Loan rate (pp) | 11,883,905 | 3.59 | 1.66 | 1.23 | 9.01 |

| Loan spread (pp) | 11,883,905 | 1.54 | 1.65 | –3.12 | 7.19 |

| Mean deposit volume (NOK) | 46,132,510 | 140,000 | 300,000 | 0 | 2,000,000 |

| Mean loan volume (NOK) | 46,132,510 | 160,000 | 510,000 | 0 | 4,000,000 |

| Final loan volume (NOK) | 46,132,510 | 1,100,000 | 1,500,000 | 0 | 6,900,000 |

| Mean household debt (NOK) | 46,132,510 | 970,000 | 1,300,000 | 0 | 6,900,000 |

| Deposit interest lost (pp) | 46,132,510 | 2.40 | 1.22 | –3.06 | 4.82 |

| Deposit money lost (NOK) | 46,132,510 | 320,000 | 480,000 | 0 | 1,800,000 |

| Relationship duration (years) | 46,132,510 | 8.91 | 4.26 | 1.00 | 15.00 |

| B. Household characteristics | |||||

| I(Age < 30) | 46,132,510 | .34 | .47 | .00 | 1.00 |

| I(Education group 1) | 45,754,686 | .15 | .35 | .00 | 1.00 |

| I(Education group 2) | 45,754,686 | .42 | .49 | .00 | 1.00 |

| I(Education group 3) | 45,754,686 | .30 | .46 | .00 | 1.00 |

| I(Education group 4) | 45,754,686 | .13 | .34 | .00 | 1.00 |

| I(Has real estate) | 46,132,510 | .53 | .50 | .00 | 1.00 |

| House value (NOK) | 46,132,510 | 1,200,000 | 1,900,000 | –5,000,000 | 440,000,000 |

| HH’s # of banks | 46,132,510 | 2.88 | 1.60 | 1.00 | 7.00 |

| Population density | 12,918,625 | 1.00 | 0.87 | 0.00 | 2.40 |

| C. Bank and market characteristics | |||||

| Conversion | 46,132,508 | 3.41 | 2.52 | 0.00 | 8.93 |

| Bank deposits (NOK mio) | 46,132,510 | 86,000 | 110,000 | 0 | 310,000 |

| HHI(D) | 46,132,510 | .30 | .12 | .11 | .86 |

| HHI(L) | 46,132,510 | .18 | .09 | .08 | .86 |

| WHHI(D) | 46,132,510 | .30 | .07 | .13 | .69 |

| WHHI(L) | 46,132,510 | .18 | .05 | .00 | .49 |

| WMS(D) | 46,132,510 | .31 | .16 | .00 | .69 |

| WMS(L) | 46,132,510 | .16 | .10 | .00 | .52 |

| Observations | Mean | SD | Min | Max | |

|---|---|---|---|---|---|

| A. Relationship characteristics | |||||

| Policy rate (pp) | 46,132,510 | 1.82 | 1.23 | 0.50 | 5.32 |

| Deposit rate (pp) | 46,132,510 | 1.29 | 1.18 | 0.07 | 4.92 |

| Deposit spread (pp) | 46,132,510 | 0.54 | 1.37 | –2.84 | 4.76 |

| Loan rate (pp) | 11,883,905 | 3.59 | 1.66 | 1.23 | 9.01 |

| Loan spread (pp) | 11,883,905 | 1.54 | 1.65 | –3.12 | 7.19 |

| Mean deposit volume (NOK) | 46,132,510 | 140,000 | 300,000 | 0 | 2,000,000 |

| Mean loan volume (NOK) | 46,132,510 | 160,000 | 510,000 | 0 | 4,000,000 |

| Final loan volume (NOK) | 46,132,510 | 1,100,000 | 1,500,000 | 0 | 6,900,000 |

| Mean household debt (NOK) | 46,132,510 | 970,000 | 1,300,000 | 0 | 6,900,000 |

| Deposit interest lost (pp) | 46,132,510 | 2.40 | 1.22 | –3.06 | 4.82 |

| Deposit money lost (NOK) | 46,132,510 | 320,000 | 480,000 | 0 | 1,800,000 |

| Relationship duration (years) | 46,132,510 | 8.91 | 4.26 | 1.00 | 15.00 |

| B. Household characteristics | |||||

| I(Age < 30) | 46,132,510 | .34 | .47 | .00 | 1.00 |

| I(Education group 1) | 45,754,686 | .15 | .35 | .00 | 1.00 |

| I(Education group 2) | 45,754,686 | .42 | .49 | .00 | 1.00 |

| I(Education group 3) | 45,754,686 | .30 | .46 | .00 | 1.00 |

| I(Education group 4) | 45,754,686 | .13 | .34 | .00 | 1.00 |

| I(Has real estate) | 46,132,510 | .53 | .50 | .00 | 1.00 |

| House value (NOK) | 46,132,510 | 1,200,000 | 1,900,000 | –5,000,000 | 440,000,000 |

| HH’s # of banks | 46,132,510 | 2.88 | 1.60 | 1.00 | 7.00 |

| Population density | 12,918,625 | 1.00 | 0.87 | 0.00 | 2.40 |

| C. Bank and market characteristics | |||||

| Conversion | 46,132,508 | 3.41 | 2.52 | 0.00 | 8.93 |

| Bank deposits (NOK mio) | 46,132,510 | 86,000 | 110,000 | 0 | 310,000 |

| HHI(D) | 46,132,510 | .30 | .12 | .11 | .86 |

| HHI(L) | 46,132,510 | .18 | .09 | .08 | .86 |

| WHHI(D) | 46,132,510 | .30 | .07 | .13 | .69 |

| WHHI(L) | 46,132,510 | .18 | .05 | .00 | .49 |

| WMS(D) | 46,132,510 | .31 | .16 | .00 | .69 |

| WMS(L) | 46,132,510 | .16 | .10 | .00 | .52 |

Panel A shows household bank relationship characteristics. Rates and spreads (against the policy rate) are expressed in percentage points (pp), volumes in Norwegian Kroners (NOK). Panel B shows household characteristics, mostly with indicators denoted as I. Panel C shows bank and municipal market characteristics. There HHI(D) and HHI(L) stand for the household municipality’s Herfindahl-Hirschmann index (HHI) for the deposit (D) and loan (L) market, respectively. WHHI(D) and WHHI(L) stand for the corresponding bank-level values, weighted by the bank’s portfolios across municipalities, while WMS stand for each bank’s weighted market share. The conversion variable summarizes the bank-level means of each relationship’s mean loan over mean deposit volume.

Summary statistics

| Observations | Mean | SD | Min | Max | |

|---|---|---|---|---|---|

| A. Relationship characteristics | |||||

| Policy rate (pp) | 46,132,510 | 1.82 | 1.23 | 0.50 | 5.32 |

| Deposit rate (pp) | 46,132,510 | 1.29 | 1.18 | 0.07 | 4.92 |

| Deposit spread (pp) | 46,132,510 | 0.54 | 1.37 | –2.84 | 4.76 |

| Loan rate (pp) | 11,883,905 | 3.59 | 1.66 | 1.23 | 9.01 |

| Loan spread (pp) | 11,883,905 | 1.54 | 1.65 | –3.12 | 7.19 |

| Mean deposit volume (NOK) | 46,132,510 | 140,000 | 300,000 | 0 | 2,000,000 |

| Mean loan volume (NOK) | 46,132,510 | 160,000 | 510,000 | 0 | 4,000,000 |

| Final loan volume (NOK) | 46,132,510 | 1,100,000 | 1,500,000 | 0 | 6,900,000 |

| Mean household debt (NOK) | 46,132,510 | 970,000 | 1,300,000 | 0 | 6,900,000 |

| Deposit interest lost (pp) | 46,132,510 | 2.40 | 1.22 | –3.06 | 4.82 |

| Deposit money lost (NOK) | 46,132,510 | 320,000 | 480,000 | 0 | 1,800,000 |

| Relationship duration (years) | 46,132,510 | 8.91 | 4.26 | 1.00 | 15.00 |

| B. Household characteristics | |||||

| I(Age < 30) | 46,132,510 | .34 | .47 | .00 | 1.00 |

| I(Education group 1) | 45,754,686 | .15 | .35 | .00 | 1.00 |

| I(Education group 2) | 45,754,686 | .42 | .49 | .00 | 1.00 |

| I(Education group 3) | 45,754,686 | .30 | .46 | .00 | 1.00 |

| I(Education group 4) | 45,754,686 | .13 | .34 | .00 | 1.00 |

| I(Has real estate) | 46,132,510 | .53 | .50 | .00 | 1.00 |

| House value (NOK) | 46,132,510 | 1,200,000 | 1,900,000 | –5,000,000 | 440,000,000 |

| HH’s # of banks | 46,132,510 | 2.88 | 1.60 | 1.00 | 7.00 |

| Population density | 12,918,625 | 1.00 | 0.87 | 0.00 | 2.40 |

| C. Bank and market characteristics | |||||

| Conversion | 46,132,508 | 3.41 | 2.52 | 0.00 | 8.93 |

| Bank deposits (NOK mio) | 46,132,510 | 86,000 | 110,000 | 0 | 310,000 |

| HHI(D) | 46,132,510 | .30 | .12 | .11 | .86 |

| HHI(L) | 46,132,510 | .18 | .09 | .08 | .86 |

| WHHI(D) | 46,132,510 | .30 | .07 | .13 | .69 |

| WHHI(L) | 46,132,510 | .18 | .05 | .00 | .49 |

| WMS(D) | 46,132,510 | .31 | .16 | .00 | .69 |

| WMS(L) | 46,132,510 | .16 | .10 | .00 | .52 |

| Observations | Mean | SD | Min | Max | |

|---|---|---|---|---|---|

| A. Relationship characteristics | |||||

| Policy rate (pp) | 46,132,510 | 1.82 | 1.23 | 0.50 | 5.32 |

| Deposit rate (pp) | 46,132,510 | 1.29 | 1.18 | 0.07 | 4.92 |

| Deposit spread (pp) | 46,132,510 | 0.54 | 1.37 | –2.84 | 4.76 |

| Loan rate (pp) | 11,883,905 | 3.59 | 1.66 | 1.23 | 9.01 |

| Loan spread (pp) | 11,883,905 | 1.54 | 1.65 | –3.12 | 7.19 |

| Mean deposit volume (NOK) | 46,132,510 | 140,000 | 300,000 | 0 | 2,000,000 |

| Mean loan volume (NOK) | 46,132,510 | 160,000 | 510,000 | 0 | 4,000,000 |

| Final loan volume (NOK) | 46,132,510 | 1,100,000 | 1,500,000 | 0 | 6,900,000 |

| Mean household debt (NOK) | 46,132,510 | 970,000 | 1,300,000 | 0 | 6,900,000 |

| Deposit interest lost (pp) | 46,132,510 | 2.40 | 1.22 | –3.06 | 4.82 |

| Deposit money lost (NOK) | 46,132,510 | 320,000 | 480,000 | 0 | 1,800,000 |

| Relationship duration (years) | 46,132,510 | 8.91 | 4.26 | 1.00 | 15.00 |

| B. Household characteristics | |||||

| I(Age < 30) | 46,132,510 | .34 | .47 | .00 | 1.00 |

| I(Education group 1) | 45,754,686 | .15 | .35 | .00 | 1.00 |

| I(Education group 2) | 45,754,686 | .42 | .49 | .00 | 1.00 |

| I(Education group 3) | 45,754,686 | .30 | .46 | .00 | 1.00 |

| I(Education group 4) | 45,754,686 | .13 | .34 | .00 | 1.00 |

| I(Has real estate) | 46,132,510 | .53 | .50 | .00 | 1.00 |

| House value (NOK) | 46,132,510 | 1,200,000 | 1,900,000 | –5,000,000 | 440,000,000 |

| HH’s # of banks | 46,132,510 | 2.88 | 1.60 | 1.00 | 7.00 |

| Population density | 12,918,625 | 1.00 | 0.87 | 0.00 | 2.40 |

| C. Bank and market characteristics | |||||

| Conversion | 46,132,508 | 3.41 | 2.52 | 0.00 | 8.93 |

| Bank deposits (NOK mio) | 46,132,510 | 86,000 | 110,000 | 0 | 310,000 |

| HHI(D) | 46,132,510 | .30 | .12 | .11 | .86 |

| HHI(L) | 46,132,510 | .18 | .09 | .08 | .86 |

| WHHI(D) | 46,132,510 | .30 | .07 | .13 | .69 |

| WHHI(L) | 46,132,510 | .18 | .05 | .00 | .49 |

| WMS(D) | 46,132,510 | .31 | .16 | .00 | .69 |

| WMS(L) | 46,132,510 | .16 | .10 | .00 | .52 |

Panel A shows household bank relationship characteristics. Rates and spreads (against the policy rate) are expressed in percentage points (pp), volumes in Norwegian Kroners (NOK). Panel B shows household characteristics, mostly with indicators denoted as I. Panel C shows bank and municipal market characteristics. There HHI(D) and HHI(L) stand for the household municipality’s Herfindahl-Hirschmann index (HHI) for the deposit (D) and loan (L) market, respectively. WHHI(D) and WHHI(L) stand for the corresponding bank-level values, weighted by the bank’s portfolios across municipalities, while WMS stand for each bank’s weighted market share. The conversion variable summarizes the bank-level means of each relationship’s mean loan over mean deposit volume.

In panel B, we report household characteristics independent of a particular bank relationship. We see that 34% of households have at least one member below 30 years old when we first observe their bank relationship.6 In addition, 15% fall into education group 1, 42% into group 2, 30% into group 3, and 13% into group 4, where the different education groups correspond as discussed above to elementary school, high school, undergraduate, or graduate level, respectively. In the relationship years when we observe them, about 53% of households have nonzero taxable real estate, which the tax authorities value on average (including zeros) at NOK 1.2 million. Households use between 1 and 7 banks and on average 3 banks. The mean population density is 1,000 capita per km2.

Finally, in panel C, we report key bank and municipal market characteristics. To start with, we find that the average bank converts in its average relationship each NOK of deposits into 3.4 NOK of loan volume. In terms of bank size, we see the average bank holding about NOK 86 billion deposits. Municipal deposit (loan) markets have Herfindahl-Hirschmann indices (HHI) of market concentration of, on average, 0.3 (0.18). Bank-level-weighted HHI values differ from bank to bank, but their averages are the same as the municipal ones. Finally, banks have average portfolio-weighted deposit (loan) market shares of 31% (16%).

3 Cross-Selling of Deposits and Loans

In this section, we explore whether banks cross-sell future deposit accounts or loans to existing depositors. We start by documenting substantial inaction in bank-household deposit relationships, which is also conditional on proxies for households’ outside options. We then document that existing depositors are substantially more likely to be converted to future borrowers, compared to other households with similar characteristics.

3.1 Cross-selling of deposits

3.1.1 Empirical strategy

The key coefficient is β, which captures the persistence in the bank-household deposit relationship. As almost all deposit accounts in Norway and hence in our data are either indefinite term contracts or fixed term for a very limited amount of time, this coefficient captures persistence in bank-household deposit relationships due to households choosing to stay with bank b.8

3.1.2 Empirical results on cross-selling of deposits

Figure 3 shows results related to the cross-selling of deposits. In the year after we first observe household h to hold deposits at bank b, the household is still a bit over 90-pp more likely to hold deposits at bank b than at any other randomly chosen bank that also offers deposit accounts in the same municipality, even after controlling for outside options.9 This persistence gradually declines each year after we first observe a deposit relationship, but even after the maximum observed time period of 14 years it still exceeds 50 pp.

Depositor stickiness

Estimates are obtained using a data set where for each household × year we fill in also all other banks present in that municipality and which the household could alternatively have been using. Then we control for municipality × year fixed effects to capture all outside options.

Table 2 reports results on the determinants of this inaction, where we measure the extent of inaction as the loss of income from continuing the existing bank relationship instead of switching to another bank available in that municipality. This variable, in a parsimonious way, captures the monetary costs of inaction. Columns 1 and 3 explore the determinants of the deposit rate lost, that is, in the difference between the approximated deposit rate earned in the observed relationship and the best one paid in any other relationship in that municipality and year. In columns 2 and 4 the outcome of interest is the log of deposit income lost. In columns 1 and 2 we regress the outcomes of interest only on household observables, whereas in columns 3 and 4 we condition also on municipality × salary quarter × education group fixed effects. Overall, the fixed effects turn out to make only a limited difference, so we focus on the latter two columns, which we deem more conservative.

Determinants of deposits lost by not switching banks

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Deposit rate lost | log deposit income lost | Deposit rate lost | log deposit income lost | |

| I(Parent) | –0.180*** | –0.143*** | –0.148*** | –0.216*** |

| (0.001) | (0.002) | (0.001) | (0.002) | |

| I(Retired) | –0.063*** | 0.724*** | –0.096*** | 0.704*** |

| (0.001) | (0.001) | (0.001) | (0.002) | |

| ln(Inc) | 0.018*** | –0.076*** | 0.022*** | –0.090*** |

| (0.000) | (0.001) | (0.000) | (0.001) | |

| ln(Wealth) | –0.047*** | 0.304*** | –0.041*** | 0.295*** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| ln(Deposits) | 0.004*** | 0.019*** | 0.005*** | 0.019*** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| I(Age <30) | –0.264*** | 0.142*** | –0.277*** | 0.188*** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Constant | 2.871*** | 7.908*** | 2.764*** | 8.188*** |

| (0.003) | (0.007) | (0.003) | (0.008) | |

| Observations | 46,134,493 | 44,257,652 | 45,756,649 | 43,888,934 |

| R 2 | .019 | .181 | .039 | .198 |

| Fixed effects | N | N | Y | Y |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Deposit rate lost | log deposit income lost | Deposit rate lost | log deposit income lost | |

| I(Parent) | –0.180*** | –0.143*** | –0.148*** | –0.216*** |

| (0.001) | (0.002) | (0.001) | (0.002) | |

| I(Retired) | –0.063*** | 0.724*** | –0.096*** | 0.704*** |

| (0.001) | (0.001) | (0.001) | (0.002) | |

| ln(Inc) | 0.018*** | –0.076*** | 0.022*** | –0.090*** |

| (0.000) | (0.001) | (0.000) | (0.001) | |

| ln(Wealth) | –0.047*** | 0.304*** | –0.041*** | 0.295*** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| ln(Deposits) | 0.004*** | 0.019*** | 0.005*** | 0.019*** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| I(Age <30) | –0.264*** | 0.142*** | –0.277*** | 0.188*** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Constant | 2.871*** | 7.908*** | 2.764*** | 8.188*** |

| (0.003) | (0.007) | (0.003) | (0.008) | |

| Observations | 46,134,493 | 44,257,652 | 45,756,649 | 43,888,934 |

| R 2 | .019 | .181 | .039 | .198 |

| Fixed effects | N | N | Y | Y |

The deposit rate lost for each relationship × year is the difference between the maximum rate paid by any bank in that year and municipality and the rate earned in that relationship and year. The deposit income lost is computed as the product of that rate loss and the deposit volume in each relationship and year. We then regress the rate lost and log income lost on client observables. Columns 3 and 4 include additionally fixed effects for each combination of municipality, salary quarter, and education group. Standard errors clustered by relationship are in parentheses.

p < .1;

p < .05;

p < .01.

Determinants of deposits lost by not switching banks

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Deposit rate lost | log deposit income lost | Deposit rate lost | log deposit income lost | |

| I(Parent) | –0.180*** | –0.143*** | –0.148*** | –0.216*** |

| (0.001) | (0.002) | (0.001) | (0.002) | |

| I(Retired) | –0.063*** | 0.724*** | –0.096*** | 0.704*** |

| (0.001) | (0.001) | (0.001) | (0.002) | |

| ln(Inc) | 0.018*** | –0.076*** | 0.022*** | –0.090*** |

| (0.000) | (0.001) | (0.000) | (0.001) | |

| ln(Wealth) | –0.047*** | 0.304*** | –0.041*** | 0.295*** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| ln(Deposits) | 0.004*** | 0.019*** | 0.005*** | 0.019*** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| I(Age <30) | –0.264*** | 0.142*** | –0.277*** | 0.188*** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Constant | 2.871*** | 7.908*** | 2.764*** | 8.188*** |

| (0.003) | (0.007) | (0.003) | (0.008) | |

| Observations | 46,134,493 | 44,257,652 | 45,756,649 | 43,888,934 |

| R 2 | .019 | .181 | .039 | .198 |

| Fixed effects | N | N | Y | Y |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Deposit rate lost | log deposit income lost | Deposit rate lost | log deposit income lost | |

| I(Parent) | –0.180*** | –0.143*** | –0.148*** | –0.216*** |

| (0.001) | (0.002) | (0.001) | (0.002) | |

| I(Retired) | –0.063*** | 0.724*** | –0.096*** | 0.704*** |

| (0.001) | (0.001) | (0.001) | (0.002) | |

| ln(Inc) | 0.018*** | –0.076*** | 0.022*** | –0.090*** |

| (0.000) | (0.001) | (0.000) | (0.001) | |

| ln(Wealth) | –0.047*** | 0.304*** | –0.041*** | 0.295*** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| ln(Deposits) | 0.004*** | 0.019*** | 0.005*** | 0.019*** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| I(Age <30) | –0.264*** | 0.142*** | –0.277*** | 0.188*** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Constant | 2.871*** | 7.908*** | 2.764*** | 8.188*** |

| (0.003) | (0.007) | (0.003) | (0.008) | |

| Observations | 46,134,493 | 44,257,652 | 45,756,649 | 43,888,934 |

| R 2 | .019 | .181 | .039 | .198 |

| Fixed effects | N | N | Y | Y |

The deposit rate lost for each relationship × year is the difference between the maximum rate paid by any bank in that year and municipality and the rate earned in that relationship and year. The deposit income lost is computed as the product of that rate loss and the deposit volume in each relationship and year. We then regress the rate lost and log income lost on client observables. Columns 3 and 4 include additionally fixed effects for each combination of municipality, salary quarter, and education group. Standard errors clustered by relationship are in parentheses.

p < .1;

p < .05;

p < .01.

The results indicate that deposit rate or income lost due to inaction varies with household characteristics. Households in which the household head is less than 30 years old lose 28-bp less deposit rate and 18% less deposit income, while parents lose 15 bp and 23% less, respectively. These two characteristics are plausibly correlated with both higher price sensitivity and lower switching costs, which are more likely to increase with age and bank relationship duration. Retiree status and wealth are associated with smaller losses in terms of the interest rate but bigger losses in terms of deposit income, presumably as these two groups are on average also reasonably price sensitive but have greater deposit volumes at stake. These results are largely consistent with those of Andersen et al. (2020), who document that wealth and age are important determinants of switching cost related to psychological and information gathering costs.

3.2 Cross-selling of loans

3.2.1 Empirical strategy

Practitioner accounts suggest that banks strive to sell different types of products to the same client over time.10 One reason for this to be attractive is that the same kind of switching costs that lead households to keep their deposits with the same bank may also lead them to apply for a loan to that same bank. In this case, we have demand complementarities. These complementarities can be due to efforts to align bank incentives as in Laux and Walz (2009), due to physical switching costs as in Sharpe (1997), administrative and cognitive costs (Handel 2013; Andersen et al. 2020) or due to loyalty as in Ongena, Paraschiv, and Reite (2021). Motivated by this literature, we investigate whether existing depositors have an elevated propensity to become a borrower at their relationship bank. We exploit the granularity of our data to ensure that we compare fairly similar households. To remove the concern of reverse causality, we focus on loan relationships that started at least 1 year after the client established the deposit account.11

Although is a binary outcome, our baseline analysis uses a linear probability model (LPM) to make it computationally feasible to include our highly granular fixed effects and so compare a household with deposits at bank b to one that has its deposits elsewhere but is otherwise as much as possible comparable to the former household.

3.2.2 Empirical results on cross-selling of loans

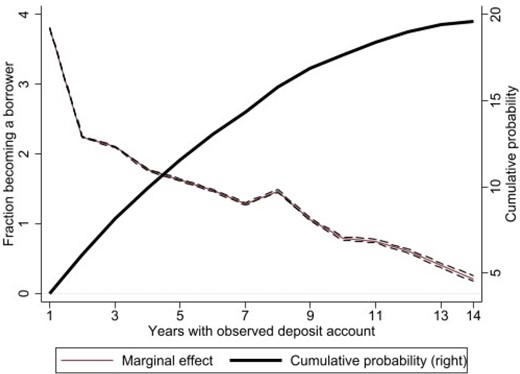

Figure 4 visually displays the results from estimating Equation (3). The existence of a deposit relationship in year t increases the likelihood of observing a new loan between the bank and that household with roughly 4 pp in . The marginal effect is still a bit over 2 pp after 2 years, and then gradually falls year by year but remains statistically significant and positive throughout the full sample up to 14 years for which we observe bank-household relationships. As an alternative reference, year-by-year estimates are displayed also Internet Appendix Table 1. Cumulatively these marginal effects make an existing depositor close to 20-pp more likely to borrow from its deposit-taking than an observationally similar household with no deposits at that bank.12 Overall, this suggests significant effects of an existing deposit relationship on the likelihood of a loan relationship which banks may want to consider also when onboarding and retaining depositors.

Existing depositors and subsequent borrowing

This figure plots our estimates of the marginal and cumulative effect of a household’s opening of a deposit account with a bank on the propensity for that household to borrow from that bank in each of the subsequent 14 years, along with 95% confidence intervals. The sample includes also hypothetical relations of each household with any other bank present in the municipality. Regressions control for municipality × salary group × education × age group fixed effects.

3.2.3 Robustness

In Internet Appendix Table 2, panel A we show further evidence on the impact of existing deposit relationships on the propensity to borrow. In the top panel, we compare the effects of using different estimation approaches to estimating the effect of a deposit relationship in any observed year on the propensity to start a loan one year later. Linear probability model (LPM) estimations without any fixed effects yield an effect of 2.2 pp, logit estimations yield marginal effects of 2.4, and probit estimations of 2.3 pp. Adding the full set of fixed effects reduces the estimate to 2.1 pp. This suggests that using a LPM with fixed effects is, if anything, slightly more conservative, but does not differ significantly from the discussed alternatives.

While panel A starts from actually observed bank-household relationships only, panel B fills in for each household also all potential relationships with all banks that have at least one relationship in the household’s municipality. Doing so increases the sample size by about 28%. The estimates increase from 2.1 to 2.3 pp when using fixed effects or from 2.2 to 2.7 pp when not using fixed effects. The difference is not large. This fits with the observation from Table 1 that the average household uses already close to 3 banks and a maximum of 7, reflecting that municipalities have a limited number of banks.

In both samples without and with hypothetical relationships of each household with each other bank active in that municipality, we find a strong link between deposit and loan relationships, and this is not significantly weakened by any of our fixed effects. This suggests that the results are not driven by unobservables. Yet one still may be concerned that both relationships are driven by the geographical distance between a household’s exact address and the address of its bank’s closest branch, neither of which we can observe beyond the postcode. We explore this in Internet Appendix Tables 3–7 and show that our results are robust to focusing on a subsample of movers (both within and across municipalities), markets with a high population density, and markets with low banking concentration. We will explain these tests in more detail in Section 5.1.1.

Loan pricing

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Loan rate | Loan spread | Loan rate | Loan spread | Loan rate | Loan spread | |

| I(Depositor) | 0.147*** | 0.146*** | 0.226*** | 0.223*** | 0.267*** | 0.265*** |

| (0.037) | (0.036) | (0.027) | (0.026) | (0.026) | (0.025) | |

| ln(Debt) | –0.124*** | –0.122*** | –0.124*** | –0.122*** | ||

| (0.004) | (0.004) | (0.005) | (0.004) | |||

| I(Owns real estate) | –0.320*** | –0.314*** | ||||

| (0.026) | (0.025) | |||||

| ln(Deposits) | 0.001** | 0.001** | 0.001*** | 0.001*** | ||

| (0.001) | (0.001) | (0.001) | (0.001) | |||

| Birth year | –0.005*** | –0.005*** | –0.005*** | –0.005*** | ||

| (0.000) | (0.000) | (0.000) | (0.000) | |||

| Has ever received UI | 0.053*** | 0.052*** | 0.045*** | 0.045*** | ||

| (0.002) | (0.002) | (0.002) | (0.002) | |||

| Number of banks used | –0.102*** | –0.100*** | –0.092*** | –0.090*** | ||

| (0.005) | (0.005) | (0.005) | (0.005) | |||

| ln(House value) | –0.098*** | –0.096*** | ||||

| (0.006) | (0.006) | |||||

| Constant | 3.377*** | 1.528*** | 15.212*** | 13.420*** | 16.345*** | 14.525*** |

| (0.021) | (0.020) | (0.530) | (0.524) | (0.597) | (0.591) | |

| Observations | 19,990,561 | 19,990,561 | 5,196,287 | 5,196,287 | 4,601,525 | 4,601,525 |

| R 2 | .158 | .222 | .237 | .297 | .279 | .304 |

| Bank × Year FE | Y | Y | Y | Y | Y | Y |

| Municipality × Education | ||||||

| × Year FE | N | N | Y | Y | Y | Y |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Loan rate | Loan spread | Loan rate | Loan spread | Loan rate | Loan spread | |

| I(Depositor) | 0.147*** | 0.146*** | 0.226*** | 0.223*** | 0.267*** | 0.265*** |

| (0.037) | (0.036) | (0.027) | (0.026) | (0.026) | (0.025) | |

| ln(Debt) | –0.124*** | –0.122*** | –0.124*** | –0.122*** | ||

| (0.004) | (0.004) | (0.005) | (0.004) | |||

| I(Owns real estate) | –0.320*** | –0.314*** | ||||

| (0.026) | (0.025) | |||||

| ln(Deposits) | 0.001** | 0.001** | 0.001*** | 0.001*** | ||

| (0.001) | (0.001) | (0.001) | (0.001) | |||

| Birth year | –0.005*** | –0.005*** | –0.005*** | –0.005*** | ||

| (0.000) | (0.000) | (0.000) | (0.000) | |||

| Has ever received UI | 0.053*** | 0.052*** | 0.045*** | 0.045*** | ||

| (0.002) | (0.002) | (0.002) | (0.002) | |||

| Number of banks used | –0.102*** | –0.100*** | –0.092*** | –0.090*** | ||

| (0.005) | (0.005) | (0.005) | (0.005) | |||

| ln(House value) | –0.098*** | –0.096*** | ||||

| (0.006) | (0.006) | |||||

| Constant | 3.377*** | 1.528*** | 15.212*** | 13.420*** | 16.345*** | 14.525*** |

| (0.021) | (0.020) | (0.530) | (0.524) | (0.597) | (0.591) | |

| Observations | 19,990,561 | 19,990,561 | 5,196,287 | 5,196,287 | 4,601,525 | 4,601,525 |

| R 2 | .158 | .222 | .237 | .297 | .279 | .304 |

| Bank × Year FE | Y | Y | Y | Y | Y | Y |

| Municipality × Education | ||||||

| × Year FE | N | N | Y | Y | Y | Y |

Columns 1, 3, and 5 use as outcome the loan rate. Columns 2, 4, and 6 the spread thereof over the policy rate. See the main text for the rationale. “I” stands for indicators; “ln” for natural logarithms; and “UI” for unemployment insurance benefits. Standard errors clustered by bank × year are in parentheses.

p < .1;

p < .05;

p < .01.

Loan pricing

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Loan rate | Loan spread | Loan rate | Loan spread | Loan rate | Loan spread | |

| I(Depositor) | 0.147*** | 0.146*** | 0.226*** | 0.223*** | 0.267*** | 0.265*** |

| (0.037) | (0.036) | (0.027) | (0.026) | (0.026) | (0.025) | |

| ln(Debt) | –0.124*** | –0.122*** | –0.124*** | –0.122*** | ||

| (0.004) | (0.004) | (0.005) | (0.004) | |||

| I(Owns real estate) | –0.320*** | –0.314*** | ||||

| (0.026) | (0.025) | |||||

| ln(Deposits) | 0.001** | 0.001** | 0.001*** | 0.001*** | ||

| (0.001) | (0.001) | (0.001) | (0.001) | |||

| Birth year | –0.005*** | –0.005*** | –0.005*** | –0.005*** | ||

| (0.000) | (0.000) | (0.000) | (0.000) | |||

| Has ever received UI | 0.053*** | 0.052*** | 0.045*** | 0.045*** | ||

| (0.002) | (0.002) | (0.002) | (0.002) | |||

| Number of banks used | –0.102*** | –0.100*** | –0.092*** | –0.090*** | ||

| (0.005) | (0.005) | (0.005) | (0.005) | |||

| ln(House value) | –0.098*** | –0.096*** | ||||

| (0.006) | (0.006) | |||||

| Constant | 3.377*** | 1.528*** | 15.212*** | 13.420*** | 16.345*** | 14.525*** |

| (0.021) | (0.020) | (0.530) | (0.524) | (0.597) | (0.591) | |

| Observations | 19,990,561 | 19,990,561 | 5,196,287 | 5,196,287 | 4,601,525 | 4,601,525 |

| R 2 | .158 | .222 | .237 | .297 | .279 | .304 |

| Bank × Year FE | Y | Y | Y | Y | Y | Y |

| Municipality × Education | ||||||

| × Year FE | N | N | Y | Y | Y | Y |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Loan rate | Loan spread | Loan rate | Loan spread | Loan rate | Loan spread | |

| I(Depositor) | 0.147*** | 0.146*** | 0.226*** | 0.223*** | 0.267*** | 0.265*** |

| (0.037) | (0.036) | (0.027) | (0.026) | (0.026) | (0.025) | |

| ln(Debt) | –0.124*** | –0.122*** | –0.124*** | –0.122*** | ||

| (0.004) | (0.004) | (0.005) | (0.004) | |||

| I(Owns real estate) | –0.320*** | –0.314*** | ||||

| (0.026) | (0.025) | |||||

| ln(Deposits) | 0.001** | 0.001** | 0.001*** | 0.001*** | ||

| (0.001) | (0.001) | (0.001) | (0.001) | |||

| Birth year | –0.005*** | –0.005*** | –0.005*** | –0.005*** | ||

| (0.000) | (0.000) | (0.000) | (0.000) | |||

| Has ever received UI | 0.053*** | 0.052*** | 0.045*** | 0.045*** | ||

| (0.002) | (0.002) | (0.002) | (0.002) | |||

| Number of banks used | –0.102*** | –0.100*** | –0.092*** | –0.090*** | ||

| (0.005) | (0.005) | (0.005) | (0.005) | |||

| ln(House value) | –0.098*** | –0.096*** | ||||

| (0.006) | (0.006) | |||||

| Constant | 3.377*** | 1.528*** | 15.212*** | 13.420*** | 16.345*** | 14.525*** |

| (0.021) | (0.020) | (0.530) | (0.524) | (0.597) | (0.591) | |

| Observations | 19,990,561 | 19,990,561 | 5,196,287 | 5,196,287 | 4,601,525 | 4,601,525 |

| R 2 | .158 | .222 | .237 | .297 | .279 | .304 |

| Bank × Year FE | Y | Y | Y | Y | Y | Y |

| Municipality × Education | ||||||

| × Year FE | N | N | Y | Y | Y | Y |

Columns 1, 3, and 5 use as outcome the loan rate. Columns 2, 4, and 6 the spread thereof over the policy rate. See the main text for the rationale. “I” stands for indicators; “ln” for natural logarithms; and “UI” for unemployment insurance benefits. Standard errors clustered by bank × year are in parentheses.

p < .1;

p < .05;

p < .01.

Screening of future defaulters

| (1) | (2) | |

|---|---|---|

| Loan rate | Loan spread | |

| Future default | 0.05*** | 0.05*** |

| (0.01) | (0.01) | |

| I(Depositor) | 0.27*** | 0.26*** |

| (0.02) | (0.02) | |

| Future default x I(Depositor) | –0.02 | –0.02 |

| (0.02) | (0.02) | |

| ln(Debt) | –0.12*** | –0.12*** |

| (0.00) | (0.00) | |

| ln(House value) | –0.09*** | –0.09*** |

| (0.01) | (0.01) | |

| ln(Deposits) | 0.00*** | 0.00*** |

| (0.00) | (0.00) | |

| Birth year | –0.01*** | –0.01*** |

| (0.00) | (0.00) | |

| Has ever received UI | 0.04*** | 0.04*** |

| (0.00) | (0.00) | |

| Number of banks used | –0.09*** | –0.09*** |

| (0.00) | (0.00) | |

| Constant | 17.37*** | 15.54*** |

| (0.66) | (0.66) | |

| Observations | 5,165,425 | 5,165,425 |

| R 2 | .27 | .30 |

| Bank × Year FE | Y | Y |

| Municipality × Education × Year FE | Y | Y |

| (1) | (2) | |

|---|---|---|

| Loan rate | Loan spread | |

| Future default | 0.05*** | 0.05*** |

| (0.01) | (0.01) | |

| I(Depositor) | 0.27*** | 0.26*** |

| (0.02) | (0.02) | |

| Future default x I(Depositor) | –0.02 | –0.02 |

| (0.02) | (0.02) | |

| ln(Debt) | –0.12*** | –0.12*** |

| (0.00) | (0.00) | |

| ln(House value) | –0.09*** | –0.09*** |

| (0.01) | (0.01) | |

| ln(Deposits) | 0.00*** | 0.00*** |

| (0.00) | (0.00) | |

| Birth year | –0.01*** | –0.01*** |

| (0.00) | (0.00) | |

| Has ever received UI | 0.04*** | 0.04*** |

| (0.00) | (0.00) | |

| Number of banks used | –0.09*** | –0.09*** |

| (0.00) | (0.00) | |

| Constant | 17.37*** | 15.54*** |

| (0.66) | (0.66) | |

| Observations | 5,165,425 | 5,165,425 |

| R 2 | .27 | .30 |

| Bank × Year FE | Y | Y |

| Municipality × Education × Year FE | Y | Y |

This table shows the results from regressing the loan rate and loan spread on a wide range of household characteristics, including a dummy for whether the household eventually defaults. Default is measured as an event where the outstanding debt is nonzero, but the bank has not received any interest payments. Standard errors clustered by bank × year are in parentheses.

p < .1;

p < .05;

p < .01.

Screening of future defaulters

| (1) | (2) | |

|---|---|---|

| Loan rate | Loan spread | |

| Future default | 0.05*** | 0.05*** |

| (0.01) | (0.01) | |

| I(Depositor) | 0.27*** | 0.26*** |

| (0.02) | (0.02) | |

| Future default x I(Depositor) | –0.02 | –0.02 |

| (0.02) | (0.02) | |

| ln(Debt) | –0.12*** | –0.12*** |

| (0.00) | (0.00) | |

| ln(House value) | –0.09*** | –0.09*** |

| (0.01) | (0.01) | |

| ln(Deposits) | 0.00*** | 0.00*** |

| (0.00) | (0.00) | |

| Birth year | –0.01*** | –0.01*** |

| (0.00) | (0.00) | |

| Has ever received UI | 0.04*** | 0.04*** |

| (0.00) | (0.00) | |

| Number of banks used | –0.09*** | –0.09*** |

| (0.00) | (0.00) | |

| Constant | 17.37*** | 15.54*** |

| (0.66) | (0.66) | |

| Observations | 5,165,425 | 5,165,425 |

| R 2 | .27 | .30 |

| Bank × Year FE | Y | Y |

| Municipality × Education × Year FE | Y | Y |

| (1) | (2) | |

|---|---|---|

| Loan rate | Loan spread | |

| Future default | 0.05*** | 0.05*** |

| (0.01) | (0.01) | |

| I(Depositor) | 0.27*** | 0.26*** |

| (0.02) | (0.02) | |

| Future default x I(Depositor) | –0.02 | –0.02 |

| (0.02) | (0.02) | |

| ln(Debt) | –0.12*** | –0.12*** |

| (0.00) | (0.00) | |

| ln(House value) | –0.09*** | –0.09*** |

| (0.01) | (0.01) | |

| ln(Deposits) | 0.00*** | 0.00*** |

| (0.00) | (0.00) | |

| Birth year | –0.01*** | –0.01*** |

| (0.00) | (0.00) | |

| Has ever received UI | 0.04*** | 0.04*** |

| (0.00) | (0.00) | |

| Number of banks used | –0.09*** | –0.09*** |

| (0.00) | (0.00) | |

| Constant | 17.37*** | 15.54*** |

| (0.66) | (0.66) | |

| Observations | 5,165,425 | 5,165,425 |

| R 2 | .27 | .30 |

| Bank × Year FE | Y | Y |

| Municipality × Education × Year FE | Y | Y |

This table shows the results from regressing the loan rate and loan spread on a wide range of household characteristics, including a dummy for whether the household eventually defaults. Default is measured as an event where the outstanding debt is nonzero, but the bank has not received any interest payments. Standard errors clustered by bank × year are in parentheses.

p < .1;

p < .05;

p < .01.

Instrumental variable regressions on depositor-borrower conversion

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| I(Future loan) | I(Future loan) | I(Depositor) | I(Future loan) | I(Future loan) | I(Future loan) | I(Depositor) | I(Future loan) | |

| I(Existing depositor) | 0.080*** | 0.205*** | 0.030*** | 0.110*** | ||||

| (0.000) | (0.000) | (0.000) | (0.001) | |||||

| Old dep market share | 0.244*** | 1.189*** | 0.019*** | 0.176*** | ||||

| (0.000) | (0.000) | (0.000) | (0.000) | |||||

| Current dep market share | 0.205*** | 0.226*** | 1.020*** | 0.114*** | ||||

| (0.000) | (0.000) | (0.000) | (0.001) | |||||

| Constant | 0.002*** | 0.001*** | 0.008*** | 0.001*** | 0.001*** | 0.006*** | ||

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |||

| Observations | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 |

| R 2 | .067 | .080 | .223 | –.052 | .102 | .099 | .294 | .047 |

| Regression | OLS | RF | FS | IV | OLS | RF | FS | IV |

| Cluster | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| I(Future loan) | I(Future loan) | I(Depositor) | I(Future loan) | I(Future loan) | I(Future loan) | I(Depositor) | I(Future loan) | |

| I(Existing depositor) | 0.080*** | 0.205*** | 0.030*** | 0.110*** | ||||

| (0.000) | (0.000) | (0.000) | (0.001) | |||||

| Old dep market share | 0.244*** | 1.189*** | 0.019*** | 0.176*** | ||||

| (0.000) | (0.000) | (0.000) | (0.000) | |||||

| Current dep market share | 0.205*** | 0.226*** | 1.020*** | 0.114*** | ||||

| (0.000) | (0.000) | (0.000) | (0.001) | |||||

| Constant | 0.002*** | 0.001*** | 0.008*** | 0.001*** | 0.001*** | 0.006*** | ||

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |||

| Observations | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 |

| R 2 | .067 | .080 | .223 | –.052 | .102 | .099 | .294 | .047 |

| Regression | OLS | RF | FS | IV | OLS | RF | FS | IV |

| Cluster | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E |

This table restricts attention to a subsample of movers and shows the results from an IV regression where I(Existing depositor) is instrumented using the market share of the bank in the old municipality. The sample is filled in to include for each household also potential relationships with all banks doing business in that household’s current municipality, as explained in the main text. “RF” corresponds to reduced form, that is, regressing the key dependent variable directly on the instrument, while “FS” corresponds to the first stage. All six columns control for municipality × age group × salary group × education group fixed effects. Columns 1–4 do not, while columns 5–8 do control for the bank’s market share in the household’s current municipality. Standard errors clustered by bank × year are in parentheses.

p < .1;

p < .05;

p < .01.

Instrumental variable regressions on depositor-borrower conversion

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| I(Future loan) | I(Future loan) | I(Depositor) | I(Future loan) | I(Future loan) | I(Future loan) | I(Depositor) | I(Future loan) | |

| I(Existing depositor) | 0.080*** | 0.205*** | 0.030*** | 0.110*** | ||||

| (0.000) | (0.000) | (0.000) | (0.001) | |||||

| Old dep market share | 0.244*** | 1.189*** | 0.019*** | 0.176*** | ||||

| (0.000) | (0.000) | (0.000) | (0.000) | |||||

| Current dep market share | 0.205*** | 0.226*** | 1.020*** | 0.114*** | ||||

| (0.000) | (0.000) | (0.000) | (0.001) | |||||

| Constant | 0.002*** | 0.001*** | 0.008*** | 0.001*** | 0.001*** | 0.006*** | ||

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |||

| Observations | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 |

| R 2 | .067 | .080 | .223 | –.052 | .102 | .099 | .294 | .047 |

| Regression | OLS | RF | FS | IV | OLS | RF | FS | IV |

| Cluster | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| I(Future loan) | I(Future loan) | I(Depositor) | I(Future loan) | I(Future loan) | I(Future loan) | I(Depositor) | I(Future loan) | |

| I(Existing depositor) | 0.080*** | 0.205*** | 0.030*** | 0.110*** | ||||

| (0.000) | (0.000) | (0.000) | (0.001) | |||||

| Old dep market share | 0.244*** | 1.189*** | 0.019*** | 0.176*** | ||||

| (0.000) | (0.000) | (0.000) | (0.000) | |||||

| Current dep market share | 0.205*** | 0.226*** | 1.020*** | 0.114*** | ||||

| (0.000) | (0.000) | (0.000) | (0.001) | |||||

| Constant | 0.002*** | 0.001*** | 0.008*** | 0.001*** | 0.001*** | 0.006*** | ||

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |||

| Observations | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 | 110,640,774 |

| R 2 | .067 | .080 | .223 | –.052 | .102 | .099 | .294 | .047 |

| Regression | OLS | RF | FS | IV | OLS | RF | FS | IV |

| Cluster | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E | M*A*S*E |

This table restricts attention to a subsample of movers and shows the results from an IV regression where I(Existing depositor) is instrumented using the market share of the bank in the old municipality. The sample is filled in to include for each household also potential relationships with all banks doing business in that household’s current municipality, as explained in the main text. “RF” corresponds to reduced form, that is, regressing the key dependent variable directly on the instrument, while “FS” corresponds to the first stage. All six columns control for municipality × age group × salary group × education group fixed effects. Columns 1–4 do not, while columns 5–8 do control for the bank’s market share in the household’s current municipality. Standard errors clustered by bank × year are in parentheses.

p < .1;

p < .05;

p < .01.

Switching as a function of bank tenure

| (1) | (2) | |

|---|---|---|

| Switcher | Switcher | |

| I(Age < 30) | 0.069*** | |

| (0.000) | ||

| I(Wealth <P50) | 0.116*** | 0.052*** |

| (0.000) | (0.002) | |

| I(University) | 0.021*** | |

| (0.000) | ||

| Bank tenure | –0.055*** | –0.050*** |

| (0.000) | (0.001) | |

| Constant | 0.395*** | 0.449*** |

| (0.001) | (0.003) | |

| Observations | 3,307,023 | 3,258,934 |

| R 2 | .298 | .357 |

| Municipality × Age × | N | Y |

| Salary × Education FE |

| (1) | (2) | |

|---|---|---|

| Switcher | Switcher | |

| I(Age < 30) | 0.069*** | |

| (0.000) | ||

| I(Wealth <P50) | 0.116*** | 0.052*** |

| (0.000) | (0.002) | |

| I(University) | 0.021*** | |

| (0.000) | ||

| Bank tenure | –0.055*** | –0.050*** |

| (0.000) | (0.001) | |

| Constant | 0.395*** | 0.449*** |

| (0.001) | (0.003) | |

| Observations | 3,307,023 | 3,258,934 |

| R 2 | .298 | .357 |

| Municipality × Age × | N | Y |

| Salary × Education FE |

The sample investigates for all household × year combinations in which a new loan is taken out whether the household did already hold deposits at that bank before (Switcher ; about 75% of cases) or not (Switcher ; about 25% of cases). Standard errors are in parentheses.

p < .1;

p < .05;

p < .01.

Switching as a function of bank tenure

| (1) | (2) | |

|---|---|---|

| Switcher | Switcher | |

| I(Age < 30) | 0.069*** | |

| (0.000) | ||

| I(Wealth <P50) | 0.116*** | 0.052*** |

| (0.000) | (0.002) | |

| I(University) | 0.021*** | |

| (0.000) | ||

| Bank tenure | –0.055*** | –0.050*** |

| (0.000) | (0.001) | |

| Constant | 0.395*** | 0.449*** |

| (0.001) | (0.003) | |

| Observations | 3,307,023 | 3,258,934 |

| R 2 | .298 | .357 |

| Municipality × Age × | N | Y |

| Salary × Education FE |

| (1) | (2) | |

|---|---|---|

| Switcher | Switcher | |

| I(Age < 30) | 0.069*** | |

| (0.000) | ||

| I(Wealth <P50) | 0.116*** | 0.052*** |

| (0.000) | (0.002) | |

| I(University) | 0.021*** | |

| (0.000) | ||

| Bank tenure | –0.055*** | –0.050*** |

| (0.000) | (0.001) | |

| Constant | 0.395*** | 0.449*** |

| (0.001) | (0.003) | |

| Observations | 3,307,023 | 3,258,934 |

| R 2 | .298 | .357 |

| Municipality × Age × | N | Y |

| Salary × Education FE |

The sample investigates for all household × year combinations in which a new loan is taken out whether the household did already hold deposits at that bank before (Switcher ; about 75% of cases) or not (Switcher ; about 25% of cases). Standard errors are in parentheses.

p < .1;

p < .05;

p < .01.

Household and bank determinants of loan probability, loan amount, and deposit pricing

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| I(Loan) | ln(FinalDebt) | Dspread | I(Loan) | ln(FinalDebt) | Dspread | |

| I(Parent) | –0.022*** | 0.635*** | –0.156*** | –0.023*** | 0.446*** | –0.135*** |

| (0.000) | (0.005) | (0.003) | (0.000) | (0.005) | (0.009) | |

| I(Retired) | 0.013*** | –2.797*** | –0.040*** | 0.029*** | –1.235*** | –0.029*** |

| (0.000) | (0.003) | (0.001) | (0.000) | (0.004) | (0.004) | |

| ln(Inc) | 0.008*** | 0.932*** | –0.011*** | 0.003*** | 0.590*** | –0.016*** |

| (0.000) | (0.002) | (0.000) | (0.000) | (0.002) | (0.002) | |

| ln(Wealth) | 0.001*** | 0.142*** | –0.027*** | 0.001*** | 0.086*** | –0.027*** |

| (0.000) | (0.001) | (0.000) | (0.000) | (0.001) | (0.002) | |

| ln(Deposits) | 0.003*** | –0.062*** | –0.005*** | 0.003*** | –0.059*** | –0.005*** |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | |

| I(Age <30) | 0.075*** | 0.999*** | –0.258*** | 0.074*** | 0.827*** | –0.281*** |

| (0.000) | (0.003) | (0.001) | (0.000) | (0.003) | (0.007) | |

| HH’s # of banks | –0.013*** | 0.582*** | –0.086*** | –0.014*** | 0.478*** | –0.078*** |

| (0.000) | (0.001) | (0.000) | (0.000) | (0.001) | (0.002) | |

| Multiproduct HH | 0.086*** | 0.082*** | ||||

| (0.001) | (0.010) | |||||

| Constant | –0.027*** | –3.759*** | 1.608*** | –0.007*** | 1.229*** | 1.644*** |

| (0.001) | (0.020) | (0.003) | (0.001) | (0.025) | (0.013) | |

| Observations | 17,090,102 | 17,090,102 | 7,806,169 | 16,860,604 | 16,860,604 | 7,684,772 |

| R 2 | .047 | .199 | .027 | .058 | .229 | .041 |

| M*S*E FE | N | N | N | Y | Y | Y |

| Cluster | Rel | Rel | Rel | M*S*E | M*S*E | M*S*E |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| I(Loan) | ln(FinalDebt) | Dspread | I(Loan) | ln(FinalDebt) | Dspread | |

| I(Parent) | –0.022*** | 0.635*** | –0.156*** | –0.023*** | 0.446*** | –0.135*** |

| (0.000) | (0.005) | (0.003) | (0.000) | (0.005) | (0.009) | |

| I(Retired) | 0.013*** | –2.797*** | –0.040*** | 0.029*** | –1.235*** | –0.029*** |

| (0.000) | (0.003) | (0.001) | (0.000) | (0.004) | (0.004) | |

| ln(Inc) | 0.008*** | 0.932*** | –0.011*** | 0.003*** | 0.590*** | –0.016*** |

| (0.000) | (0.002) | (0.000) | (0.000) | (0.002) | (0.002) | |

| ln(Wealth) | 0.001*** | 0.142*** | –0.027*** | 0.001*** | 0.086*** | –0.027*** |

| (0.000) | (0.001) | (0.000) | (0.000) | (0.001) | (0.002) | |

| ln(Deposits) | 0.003*** | –0.062*** | –0.005*** | 0.003*** | –0.059*** | –0.005*** |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | |

| I(Age <30) | 0.075*** | 0.999*** | –0.258*** | 0.074*** | 0.827*** | –0.281*** |

| (0.000) | (0.003) | (0.001) | (0.000) | (0.003) | (0.007) | |

| HH’s # of banks | –0.013*** | 0.582*** | –0.086*** | –0.014*** | 0.478*** | –0.078*** |

| (0.000) | (0.001) | (0.000) | (0.000) | (0.001) | (0.002) | |

| Multiproduct HH | 0.086*** | 0.082*** | ||||

| (0.001) | (0.010) | |||||

| Constant | –0.027*** | –3.759*** | 1.608*** | –0.007*** | 1.229*** | 1.644*** |

| (0.001) | (0.020) | (0.003) | (0.001) | (0.025) | (0.013) | |

| Observations | 17,090,102 | 17,090,102 | 7,806,169 | 16,860,604 | 16,860,604 | 7,684,772 |

| R 2 | .047 | .199 | .027 | .058 | .229 | .041 |

| M*S*E FE | N | N | N | Y | Y | Y |

| Cluster | Rel | Rel | Rel | M*S*E | M*S*E | M*S*E |

Household characteristics until the indicator for age below 30 as above. HH’s # of banks is the number of banks with which the household entertains a relationship in that year. Multiproduct HH is an indicator for households that have both deposits and a loan in that bank relationship. Columns 1–3 without fixed effects and with standard errors clustered by bank relationship. Columns 4–6 include municipality × salary × education fixed effects and cluster standard errors by these same categories.

p < .1;

p < .05;

p < .01.

Household and bank determinants of loan probability, loan amount, and deposit pricing

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| I(Loan) | ln(FinalDebt) | Dspread | I(Loan) | ln(FinalDebt) | Dspread | |

| I(Parent) | –0.022*** | 0.635*** | –0.156*** | –0.023*** | 0.446*** | –0.135*** |

| (0.000) | (0.005) | (0.003) | (0.000) | (0.005) | (0.009) | |

| I(Retired) | 0.013*** | –2.797*** | –0.040*** | 0.029*** | –1.235*** | –0.029*** |

| (0.000) | (0.003) | (0.001) | (0.000) | (0.004) | (0.004) | |

| ln(Inc) | 0.008*** | 0.932*** | –0.011*** | 0.003*** | 0.590*** | –0.016*** |

| (0.000) | (0.002) | (0.000) | (0.000) | (0.002) | (0.002) | |

| ln(Wealth) | 0.001*** | 0.142*** | –0.027*** | 0.001*** | 0.086*** | –0.027*** |

| (0.000) | (0.001) | (0.000) | (0.000) | (0.001) | (0.002) | |

| ln(Deposits) | 0.003*** | –0.062*** | –0.005*** | 0.003*** | –0.059*** | –0.005*** |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | |

| I(Age <30) | 0.075*** | 0.999*** | –0.258*** | 0.074*** | 0.827*** | –0.281*** |

| (0.000) | (0.003) | (0.001) | (0.000) | (0.003) | (0.007) | |

| HH’s # of banks | –0.013*** | 0.582*** | –0.086*** | –0.014*** | 0.478*** | –0.078*** |

| (0.000) | (0.001) | (0.000) | (0.000) | (0.001) | (0.002) | |

| Multiproduct HH | 0.086*** | 0.082*** | ||||

| (0.001) | (0.010) | |||||

| Constant | –0.027*** | –3.759*** | 1.608*** | –0.007*** | 1.229*** | 1.644*** |

| (0.001) | (0.020) | (0.003) | (0.001) | (0.025) | (0.013) | |

| Observations | 17,090,102 | 17,090,102 | 7,806,169 | 16,860,604 | 16,860,604 | 7,684,772 |

| R 2 | .047 | .199 | .027 | .058 | .229 | .041 |

| M*S*E FE | N | N | N | Y | Y | Y |

| Cluster | Rel | Rel | Rel | M*S*E | M*S*E | M*S*E |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| I(Loan) | ln(FinalDebt) | Dspread | I(Loan) | ln(FinalDebt) | Dspread | |

| I(Parent) | –0.022*** | 0.635*** | –0.156*** | –0.023*** | 0.446*** | –0.135*** |

| (0.000) | (0.005) | (0.003) | (0.000) | (0.005) | (0.009) | |

| I(Retired) | 0.013*** | –2.797*** | –0.040*** | 0.029*** | –1.235*** | –0.029*** |

| (0.000) | (0.003) | (0.001) | (0.000) | (0.004) | (0.004) | |

| ln(Inc) | 0.008*** | 0.932*** | –0.011*** | 0.003*** | 0.590*** | –0.016*** |

| (0.000) | (0.002) | (0.000) | (0.000) | (0.002) | (0.002) | |

| ln(Wealth) | 0.001*** | 0.142*** | –0.027*** | 0.001*** | 0.086*** | –0.027*** |

| (0.000) | (0.001) | (0.000) | (0.000) | (0.001) | (0.002) | |

| ln(Deposits) | 0.003*** | –0.062*** | –0.005*** | 0.003*** | –0.059*** | –0.005*** |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | |

| I(Age <30) | 0.075*** | 0.999*** | –0.258*** | 0.074*** | 0.827*** | –0.281*** |

| (0.000) | (0.003) | (0.001) | (0.000) | (0.003) | (0.007) | |

| HH’s # of banks | –0.013*** | 0.582*** | –0.086*** | –0.014*** | 0.478*** | –0.078*** |

| (0.000) | (0.001) | (0.000) | (0.000) | (0.001) | (0.002) | |

| Multiproduct HH | 0.086*** | 0.082*** | ||||

| (0.001) | (0.010) | |||||

| Constant | –0.027*** | –3.759*** | 1.608*** | –0.007*** | 1.229*** | 1.644*** |

| (0.001) | (0.020) | (0.003) | (0.001) | (0.025) | (0.013) | |

| Observations | 17,090,102 | 17,090,102 | 7,806,169 | 16,860,604 | 16,860,604 | 7,684,772 |

| R 2 | .047 | .199 | .027 | .058 | .229 | .041 |

| M*S*E FE | N | N | N | Y | Y | Y |

| Cluster | Rel | Rel | Rel | M*S*E | M*S*E | M*S*E |

Household characteristics until the indicator for age below 30 as above. HH’s # of banks is the number of banks with which the household entertains a relationship in that year. Multiproduct HH is an indicator for households that have both deposits and a loan in that bank relationship. Columns 1–3 without fixed effects and with standard errors clustered by bank relationship. Columns 4–6 include municipality × salary × education fixed effects and cluster standard errors by these same categories.

p < .1;

p < .05;

p < .01.

4 Understanding the Mechanisms behind Cross-Selling

The results above indicate that banks are able to cross-sell loans to existing depositors. However, the underlying mechanism is unclear. On the one hand, there could be supply complementarities from selling different products to the same client because of, for example, more reliable borrower screening, as emphasized by Petersen and Rajan (1994) or Mester, Nakamura, and Renault (2007). As discussed in the introduction, these forms of complementarities have been documented in the literature on firm-bank relationships. On the other hand, demand complementarities could give rise to household inaction (Andersen et al. 2020; Handel 2013). Such inaction could arise from persistent preferences for particular financial institutions, or from stickiness based on search costs (Abel, Eberly, and Panageas 2007) and/or switching costs. Either way, from the economics of multiproduct pricing,13 (e.g., Tirole 1988), it is clear that both demand and supply complementarities can motivate firms to price the initial product below marginal cost for future profits.

The purpose of this section is to shed further light on the underlying mechanism through which cross-selling arises. We start by documenting that cross-selling in our setup seems more likely to be demand driven, and then we explore the drivers of these demand factors.

4.1 Supply versus demand complementarities

4.1.1 Empirical strategy on supply versus demand complementarities

To explore whether supply or demand complementarities dominate on average, we test two hypotheses. First, we investigate whether existing depositors get a discount on their loan rate relative to otherwise comparable households with no deposits at that bank.

Observing such a discount () is consistent with supply complementarities being the dominant driver of cross-selling, as banks that prefer lending to existing clients due to cheaper or more reliable screening should pass a fraction of these benefits on to those clients.

We interpret as evidence for screening benefits, that is, that banks are better equipped to price future defaults for borrowers that have a preexisting relationship with the bank. We interpret as suggesting no screening benefits.

4.1.2 Empirical results on supply versus demand complementarities