Abstract

Since the creation of the euro, capital flows among member countries have been large and volatile. Motivated by this fact, I provide a theory connecting the exchange rate regime to financial integration. The key feature of the model is that monetary policy affects the value of collateral that creditors seize upon default. Under flexible exchange rates, national governments can expropriate foreign creditors by depreciating the exchange rate, which induces investors to impose tight constraints on international borrowing. Creating a monetary union, by eliminating this source of currency risk, increases financial integration among member countries. This process, however, does not necessarily lead to higher welfare. The reason is that a high degree of capital mobility can generate multiple equilibria, with bad equilibria characterized by inefficient capital flights. Capital controls or fiscal transfers can eliminate bad equilibria, but their implementation requires international cooperation.

1. Introduction

What are the benefits and costs from adopting a common currency? This question has been at the centre of a long-standing debate in international macroeconomics. In a seminal paper, Friedman (1953) claimed that flexible exchange rates act as shock absorbers, so that fixing exchange rates will generate welfare losses by increasing macroeconomic volatility. Instead, while writing about the European monetary integration, Ingram (1973) provided a more positive view of currency unions. He argued that forming a currency union will foster financial integration among member countries, leading to a more efficient international allocation of capital and higher welfare.

Ingram’s view resonates well with some aspects of the euro area experience. Indeed, the introduction of the euro has been accompanied by a sharp increase in financial flows among member countries (Lane, 2006). Moreover, existing empirical evidence suggests that the elimination of currency risk has been the main driver behind the euro’s positive impact on financial integration (Kalemli-Ozcan et al., 2010). But some crucial questions are open. First, why should the exchange rate regime matter for financial integration and capital flows? And does higher capital mobility necessarily lead to higher welfare, especially in light of the fact that several euro area countries suffered crisis periods characterized by financial instability and capital flights?1

In this article, I tackle these questions by providing a theory connecting the exchange rate regime to international financial integration. There are three frictions at the heart of the model. The first one is the presence of nominal wage rigidities, a classic friction in monetary economics, which implies that monetary policy has real effects on output. The second friction, typical of the macro-finance literature, is that output is used as collateral to perform financial transactions. As we will see, the combination of these two frictions creates a link between monetary—and exchange rate—policy and financial flows. The third friction is that monetary authorities lack the ability to commit.

The first result of the article is that, in accordance with Ingram’s view, forming a currency union increases financial integration among member countries. The reason is simple. In the model, an exchange rate depreciation reduces the value of the collateral that foreign investors repossess when domestic agents default. National governments thus face a time-consistency problem. Once the external debt of a country exceeds a threshold, it is optimal for the government to engineer a depreciation to expropriate foreign creditors. To escape expropriation, international investors respond by imposing ex ante tight constraints on international borrowing. Under flexible exchange rates, therefore, international capital mobility is limited.

It is often claimed that investors can escape currency risk by denominating debt contracts in a foreign currency or in real terms. This is not the case here, since expropriation occurs because the exchange rate affects the value of collateral backing financial contracts. This feature sets the model apart from the literature on nominal debt and limited commitment over monetary policy (Bohn, 1990), in which the central bank’s time-consistency problem can be solved by issuing debt contracts denominated in a foreign currency or in real terms. In contrast, addressing the time-consistency problem studied by this article requires more fundamental changes in the monetary framework, such as forming a currency union.2

In a monetary union national governments delegate monetary policy to a supranational authority, the union’s central bank, which acts in the interest of all member countries. Unlike national governments, the union’s central bank does not have a strong incentive to expropriate creditors, as long as they belong to the union. Joining a currency union thus imposes a vincolo esterno—that is an external constraint—on national governments, preventing them from using monetary policy to expropriate foreign creditors.3 Hence, in a currency union countries can sustain a higher stock of foreign debt toward other members without defaulting. Adopting a common currency thus increases international capital mobility within the monetary union.4

Does this process lead to efficient capital flows and higher welfare? I first show that forming a monetary union might increase welfare by fostering capital flows toward countries in which capital is most productive. For this to happen, two conditions have to be met. First, there must be some asymmetry in terms of investment opportunities among member countries. This result contrasts with the traditional optimal currency area literature, in which giving up exchange rate flexibility is costly precisely when countries are asymmetric (Mundell, 1961). Second, financial frictions need to be severe enough to prevent an efficient international allocation of capital under flexible exchange rates. Hence, adopting a common currency is optimal only if financial markets are not too developed to start with.

But this benign view does not square well with the recent experience of the euro area, characterized by financial instability and volatile capital flows. As argued by a vast literature, financial instability might be the result of complementarities in investment decisions (Akerlof, 2019). Building on this insight, I introduce investment complementarities by considering an economy in which governments finance some fixed expenditure with taxes on capital income. This opens the door to fluctuations in capital flows purely driven by animal spirits.5 Expectations of high taxes on capital, the logic is, can trigger a capital flight and a fall in domestic investment. The associated fall in the tax base forces the government to raise taxes, inducing another round of capital flights. This feedback loop can make pessimistic expectations self-fulfilling and give rise to capital flights out of high-productivity countries.

Importantly, episodes of inefficient capital flights can take place only if financial integration is sufficiently high. Therefore monetary unions, with their inherent high degree of capital mobility, are particularly prone to experience expectations-driven fluctuations in capital flows.6 Forming a monetary union might thus lower welfare, by inducing volatility in international financial flows and capital misallocation. Furthermore, inefficient capital flights are more likely to happen when a monetary union is hit by large shocks requiring a fiscal response, such as large financial crises or pandemics. In this respect, the model suggests that participating in a common currency might hamper national governments’ ability to react to shocks through fiscal policy, due to high capital mobility and the risk of capital flights driven by pessimistic animal spirits.

A natural question to ask is what policy interventions can prevent self-fulfilling capital flights from taking place. One possibility is to impose controls on capital flows. Another option is to set up a system of countercyclical fiscal transfers among the countries of the union, in the spirit of Kenen (1969) and Farhi et al. (2014). If credible, the presence of a countercyclical transfers scheme anchors agents’ expectations on the good equilibrium, in which capital flows toward high-productivity countries. Volatility in capital flows driven by animal spirits is thus ruled out, without the need to actually transfer resources among countries in equilibrium.

While these policies are beneficial from a global perspective, however, they might lower welfare for some countries in the union. In fact, during episodes of inefficient capital flights some member countries act as safe havens, and so benefit from inflows of cheap foreign capital. Implementing policies that rule out capital flights driven by pessimistic expectations might then lower welfare in safe-haven countries. Successfully managing financial integration in a monetary union is therefore possible, but requires close international cooperation.

Related literature. This article contributes to the optimal currency area literature, which studies the costs and benefits associated with forming a monetary union. Friedman (1953) argues that joining a monetary union is costly, because the loss of independent monetary policy leads to higher output volatility in response to asymmetric shocks. Benigno (2004) and Fornaro (2018) provide modern formulations of this argument using New Keynesian open-economy models. A large literature has considered factors that mitigate the impact on welfare of asymmetric shocks in monetary unions. To cite a few examples, Mundell (1961) and Farhi and Werning (2014) stress the role of labour mobility, Kenen (1969), Gali and Monacelli (2008), and Farhi et al. (2014) focus on fiscal transfers, Farhi and Werning (2017) consider fiscal devaluations, Farhi et al. (2014), Schmitt-Grohé and Uribe (2016), and Sergeyev (2016) study macroprudential policies, while Aguiar et al. (2015) and Bianchi and Mondragon (2021) focus on public debt and rollover crises. A smaller body of work has studied the benefits derived from creating a monetary union. For instance, in Giavazzi and Pagano (1988) and Alesina and Barro (2002) countries might wish to join a currency union in order to reduce inflation. In Rey (2001) and Alesina and Barro (2002), sharing a common currency reduces the cost of performing international transactions and facilitates trade. Nurkse (1944), Jeanne and Rose (2002), and Gabaix and Maggiori (2015) argue that flexible exchange rates, rather than acting as shock absorbers, can be a source of volatility by triggering speculative flows. None of these papers study the impact of the exchange rate regime on financial integration.

The notion that creating a monetary union will lead to higher financial integration has a long history (Keynes, 1930; Ingram, 1973), and was very much present in the debate paving the way to the euro adoption (Giavazzi, 1989), but few attempts have been made at formalizing this insight. To the best of my knowledge, in fact, Doepke and Schneider (2017) provide the only other framework in which forming a monetary union increases financial integration among member countries. The key friction in Doepke and Schneider (2017) is that financial contracts are non-contingent and defaulting generates social losses. Sharing a common currency leads to higher international financial integration because it limits the probability that agents default in response to exogenous shocks. The channel emphasized by this article is very different. In fact, my argument does not rest on the inability to write contingent contracts, but rather on the combination of nominal wage rigidities and collateral constraints. Moreover, in Doepke and Schneider (2017) monetary policy is exogenous, while in this article the endogenous response of monetary policy to capital flows plays a crucial role.7 Finally, in Doepke and Schneider (2017) increasing financial integration is welfare improving. Here, instead, higher financial integration may generate financial instability and welfare losses.

A small literature has studied the interplay between the exchange rate regime and access to foreign credit in small open economies settings. In Arellano and Heathcote (2010) governments finance their expenditure through seignorage or foreign borrowing, and they are punished with exclusion from credit markets in case of default. Fixing the exchange rate—and so giving up seignorage—exacerbates the cost of being excluded from the credit markets and thus increases the government’s debt limit. Closer to this article, Fornaro (2015), Ottonello (2021), and Coulibaly (2018) study economies in which monetary policy affects collateral value because of the presence of nominal wage rigidities. These works, however, abstract from the time-consistency problem which is at the heart of this article, by assuming that national governments can commit not to use monetary policy to expropriate foreign investors. Furthermore, in Fornaro (2015), Ottonello (2021), and Coulibaly (2018) fixing the exchange rate triggers a process of reduction in foreign debt, which seems inconsistent with the experience of peripheral countries during the first ten years of the euro. Another important difference is that all these works focus on single small open economies, while this article studies a multi-country economy, in which global credit markets clear. This allows me to model how the exchange rate regime affects the potential for capital outflows by domestic agents, a dimension which is absent in Arellano and Heathcote (2010), Fornaro (2015), Ottonello (2021), and Coulibaly (2018). This aspect is crucial to understand why currency unions might be particularly exposed to capital flows volatility and episodes of inefficient capital flights.

The paper is also related to Tirole (2003) and Jeanne (2009), who study settings in which placing constraints on government policy facilitates international borrowing, because it limits the government’s ability to expropriate foreign investors. Compared to these papers, I focus on an alternative channel through which expropriation can occur, given by the interplay between monetary policy and collateral value. Moreover, both Tirole (2003) and Jeanne (2009) consider a single country. Instead, a key element of this article is its multi-country dimension, and in particular the fact that forming a currency union facilitates financial flows both in and out of member countries. Because of this reason, the impact of higher financial integration on welfare is ambiguous in my model, while it is positive in Tirole (2003) and Jeanne (2009).

Finally, this article is connected to the literature emphasizing how increasing international financial integration can have an ambiguous impact on welfare. Two examples are Martin and Rey (2006) and Broner and Ventura (2016). In both papers, a high degree of financial integration may open the door to pessimistic equilibria characterized by inefficient capital flights. However, these papers take the level of international financial integration as determined by exogenous forces. Here financial integration is endogenously determined, and depends on the exchange rate regime.

The rest of the article is composed of five sections. Section 2 presents the baseline model. Section 3 describes the connection between the exchange rate regime and financial integration. Section 4 derives the implications for capital flows and welfare. Section 5 discusses some policy implications for monetary unions. Section 6 concludes. The Appendix contains all the proofs and derivations not included in the main text.

2. Model

Consider a world composed of two countries, home and foreign. There are two periods: 0 and 1. In period 0 agents sign financial contracts and make their investment decisions. In period 1 production takes place, financial contracts are settled and agents consume. Agents are rational and there is perfect foresight.

To simplify the exposition, while presenting the model I will focus on the home economy. The foreign country is, however, characterized by exactly the same equilibrium conditions. When needed, I will denote variables pertaining to the foreign country with |$*$| superscripts.

2.1. Households

In this expression, |$C_T$| and |$C_N$| denote respectively consumption of a tradable and a non-tradable good, while |$L$| denotes labour effort.8

In period 0 households are endowed with |$N$| units of the tradable good. There are two assets in which households can invest to transfer tradable goods to period 1. First, households can invest in a domestic technology, call it capital, that transforms one unit of the tradable good in period 0 into |$A$| units of the tradable good in period 1. Let |$I$| denote investment in home-country capital. In addition, households have access to a real bond denominated in units of the tradable good. Denote by |$D$| the level of debt assumed by domestic households in period 0 and due in period 1, and |$R$| the gross interest rate between the two periods. The bond is traded internationally, and |$R$| is common across the two countries.

Intuitively, if |$A>R$| households maximize investment in domestic capital by borrowing up to their limit. Instead, if |$A<R$| investment in domestic capital is unprofitable, and households lend all their net worth on the international credit markets. Finally, if |$A=R$| households are indifferent between investing in domestic capital and lending on the credit markets.

The left-hand side of this expression represents the households’ expenditure. |$P_T$| and |$P_N$| denote respectively the price of a unit of tradable and non-tradable good in terms of the home currency. Hence, |$P_T C_T + P_N C_N$| is the total nominal expenditure in consumption. Since period 1 is the terminal date of the economy, households hold no assets at the end of the period.

|$\mathcal{R}$| is the amount of loan repayment that households make in period 1. |$W$| denotes the nominal wage, and hence |$W L$| is the households’ labour income.

In words, the payment that households make to their creditors cannot exceed a fraction |$\kappa$| of their income. The assumption that defaulting triggers a fall in the borrower’s income follows a vast literature in macroeconomics. It is, indeed, commonly made in the sovereign default literature (Eaton and Gersovitz, 1981). It is also close in spirit to the friction considered by Kiyotaki and Moore (1997), but with the household’s income instead of capital as collateral.9

Demand for non-tradables is thus decreasing in their relative price |$P_N/P_T$|.

2.2. Nominal wage rigidities

To allow for real effects from monetary policy, I introduce a simple friction in the adjustment of nominal wages. In particular, nominal wages are fixed and equal to |$W$|. To clear the labour market, I then assume that households satisfy firms’ labour demand.

To be clear, the results that follow do not rely at all on this extreme form of wage rigidity, and would extend to a setting in which partial adjustment of nominal wages is possible. But considering an economy with fixed wages is convenient, because it simplifies the analysis and allows for a transparent characterization of the economic forces at the heart of the model.

2.3. Non-tradable production and the real exchange rate

Non-traded output |$Y_N$| is produced by a large number of competitive firms. Labour is the only factor of production, and the production function is |$Y_N = L$|. Profits are given by |$P_N Y_N - W L$|. The zero profit condition implies that in equilibrium |$P_N = W$|.

Notice that, since the nominal wage is rigid, changes in the nominal price of the tradable good affect the real exchange rate. In fact, as I will explain later on, this is the channel through which monetary policy affects the real economy.

2.4. Market clearing and equilibrium

Hence the real exchange rate, through its impact on demand, effectively determines production of non-tradable goods.

As highlighted by this equation, collateral is thus equal to a fraction |$\kappa$| of the value of the country’s output in terms of the tradable good. This happens because foreign creditors cannot consume non-traded goods produced by the home country. Hence, when foreigners repossess non-tradable goods from defaulting debtors they need to sell them at price |$p$| in exchange for tradable goods.

In principle, the relationship between the real exchange rate and collateral value is ambiguous and depends on |$\eta$|. The results that follow only require that movements in the real exchange rate affect collateral value, and so that |$\eta \neq 1$|. But, purely to simplify the exposition, from now on I will assume that |$\eta > 1$|.10 In this case, a real exchange rate depreciation reduces the value of collateral. Analogous market clearing conditions hold for the foreign economy.

Equation (9) ensures that global investment in capital is equal to the world endowment of the tradable good in period 0. Equation (10) implies that period 1 global consumption of tradable goods is equal to global production.

We are now ready to define a competitive equilibrium.

A competitive equilibrium is a set of real allocations  ,

,  and world interest rate |$R$|, satisfying (1), (2), (3), (6), (7), (8)—plus their counterparts for the foreign country—and (10), given policy-determined values for the real exchange rates |$\{p, p^*\}$| and for the debt limits |$\{\bar{D}, \bar{D}^*\}$|.

and world interest rate |$R$|, satisfying (1), (2), (3), (6), (7), (8)—plus their counterparts for the foreign country—and (10), given policy-determined values for the real exchange rates |$\{p, p^*\}$| and for the debt limits |$\{\bar{D}, \bar{D}^*\}$|.

2.5. Discussion of assumptions

The key feature of the model is that monetary policy can influence the payment that foreign creditors receive from domestic agents. This happens because monetary policy affects the real exchange rate, and so the value in terms of tradables of the domestic production of non-traded goods. However, several other assumptions would give rise to similar results. For instance, in the spirit of Kiyotaki and Moore (1997), one could consider a setting in which collateral is given by some long-lived asset, such as capital, land, or housing. As long as monetary policy has an impact on the foreign currency value of this asset, as for instance in Fornaro (2015), the main results of the article go through.

Another possibility is to consider debt contracts denominated in domestic currency. Also in this case, in fact, monetary policy would affect the payment received by foreign creditors. However, as documented empirically by Maggiori et al. (2020), foreign creditors rarely accept to sign debt contracts denominated in domestic currency. This is the reason why the model considers debt contracts denominated in real terms, which cannot be directly affected by monetary policy. In fact, one could even assume that agents sign equity—rather than debt—contracts. As long as their payment is backed up by collateral, all the main results would still apply.

Finally, let me clarify that all the results that follow would go through if one were to assume that |$\eta < 1$|. The only difference is that in this case monetary authorities would need to appreciate the exchange rate in order to expropriate foreign investors. The same consideration applies to the model studied by Fornaro (2015), in which exchange rate depreciations increase land price and collateral value. In this case, the expropriation of foreign investors would take place through an appreciation of the exchange rate, leading to a drop in land price and collateral value.

3. Exchange Rate Regime and Financial Integration

What is the relationship between monetary policy, the exchange rate regime and financial integration? To answer this question, I solve the model backward and start by characterizing the equilibrium in period 1. Throughout I will contrast two different policy regimes. First, I will consider the case of flexible exchange rates. I will then turn to the case of a monetary union.

3.1. Flexible exchange rates

Closing the model requires specifying how monetary policy is conducted. I consider governments that implement the optimal non-cooperative monetary policy. Therefore, each government seeks to maximize the welfare of its country’s citizens, without any concern for welfare in the rest of the world. Moreover, each government operates under discretion. This means that governments set monetary policy in period 1, without being restricted by any promise that they might have made in period 0.

Hence, by setting |$p$| the government affects two margins. First, |$p$| determines the quantity of non-tradable goods produced and consumed by domestic households. Second, if the home country is in a default state, the real exchange rate affects the value of the collateral that foreign creditors repossess from domestic agents.

To understand this condition, consider that |$Y_N = 1$| is the natural level of non-tradable output, that is the amount of non-tradable goods that the economy would produce in absence of nominal rigidities.13 Hence, conditional on no default, the optimal monetary policy offsets the impact of nominal rigidities on production.

In case of default the government has thus an additional incentive to depreciate the exchange rate. An exchange rate depreciation, in fact, reduces the value of collateral and thus the amount of tradable goods that foreign creditors can extract from domestic households. The counterpart of this exchange rate depreciation is the overheating of the domestic economy, in the sense that output of non-tradable goods ends up being above its natural level (|$Y_N > 1$|). So, conditional on defaulting, the home government trades off the gains from depreciating the exchange rate to expropriate foreign creditors, with the costs associated with an inefficiently high production of the non-tradable good.

In words, the home country defaults whenever its foreign debt is higher than the threshold |$\bar{D}_{flex}$|. The following proposition summarizes these results.14

Under flexible exchange rates, the home country does not default if and only if |$D \leq \bar{D}_\textit{flex}$|. Moreover, in absence of default monetary policy sets |$p = Y_N = 1$|. Analogous expressions hold for the foreign country.

A couple of remarks are in order. First, since agents are rational, ex-ante investors will never lend to the home country more than |$\bar{D}_\textit{flex}/R$|. Otherwise, the home country would default and creditors would make a loss. It follows that the debt ceiling imposed by foreign investors under flexible exchange rates is |$\bar{D} = \bar{D}_\textit{flex}$|.15 This also means that countries never accumulate enough debt to trigger a default, and so in equilibrium monetary policy sets |$p = Y_N = 1$| to replicate the allocation under flexible wages.

This happens because foreign investors anticipate that, if they were to lend to the home country slightly more than |$\bar{D}_\textit{flex}$|, the government would engineer a discrete depreciation of the real exchange rate. In turn, the depreciation would trigger a discrete fall in the value of collateral. Hence, under flexible exchange rates, a naive observer would conclude that borrowers never borrow enough to exhaust the value of their collateral.16

To end this section, notice that national governments are subject to a time-consistency problem. In period 0, in fact, the government would like to commit not to depreciate the exchange rate in period 1. This would relax the borrowing limit imposed by investors on domestic agents. However, when period 1 comes the government has an incentive to forget its past promises and to expropriate foreign creditors through a depreciation. In absence of commitment, the period 0 promise not to devalue the exchange rate ex post is thus not credible. This commitment problem is precisely the reason why the debt ceiling imposed by foreign investors is lower than the amount of collateral observed in equilibrium.17

Interestingly, this time-consistency problem is present even though debt is denominated in real terms, rather than in terms of the domestic currency. This feature sets the model apart from the literature on nominal debt and limited commitment over monetary policy (Bohn, 1990; Araujo et al., 2013; Engel and Park, 2018; Ottonello and Perez, 2019), in which the central bank’s time-consistency problem can be avoided by signing debt contracts in real terms or in terms of a foreign currency. The limited commitment problem at the heart of this model, instead, cannot be solved by changing the currency denomination of debt, or even by signing equity—rather than debt—contracts. As we will see, addressing it requires more fundamental changes in the monetary framework, such as forming a currency union.

3.2. Monetary union

I now turn to the case of a monetary union.18 In a monetary union, the two countries share the same currency and so |$S=1$|. The law of one price for the tradable good then implies that |$P_T = P^*_T$|, so that differences in the nominal price of tradables across countries cannot arise.

Moreover, monetary policy is no longer controlled by national governments. It is instead set by a supranational authority, the union’s central bank. To parallel the case of flexible exchange rates, I consider a benevolent central bank that operates under discretion. The key difference is that the central bank of the union seeks to maximize the welfare of the union as a whole. More concretely, I assume that the central bank attaches equal weight to the welfare of every citizen of the union.

In principle, the home and foreign country could have different pre-set nominal wages. To keep the analysis transparent, it is however convenient to assume that |$W = W^*$|. Under this condition, both countries feature the same real exchange rate and the same production of non-traded goods (|$p = p^*$|, |$Y_N = Y_N^*$|).

To understand this result, consider that from the point of view of the union’s central bank it does not matter how tradable consumption is distributed across the two countries. Hence, the central bank of the union has no incentives to use monetary policy to redistribute resources across home and foreign agents.19 The optimal policy then purely focuses on offsetting the impact of nominal rigidities on output, so that production of non-traded goods in both countries is equal to its natural level.20

The debt ceiling imposed by foreign investors is thus exactly equal to the value of collateral observed in equilibrium |$(\bar{D} = \bar{D}_{mu})$|.

In a monetary union, the home country does not default if and only if |$D \leq \bar{D}_{mu}$|. Moreover, assuming |$W=W^*$|, monetary policy sets |$p = Y_N = 1$|. Analogous expressions hold for the foreign country.

Intuitively, forming a monetary union mitigates the time-consistency problem faced by national central banks. This happens because the union’s central bank, which attaches equal weight to the welfare of both debtors and creditors, has no incentives to use the exchange rate to decrease collateral value and expropriate investors.21

3.3. Impact of forming a monetary union on financial integration

This means that the stock of assets that home agents can hold abroad without triggering a default by the foreign country increases when a monetary union is formed.

Hence, compared to the case of flexible exchange rates, countries in a monetary union can both absorb higher amounts of foreign debt and lend larger sums abroad. Adopting a single currency thus fosters financial integration across member countries, by increasing international capital mobility. This happens because joining a currency union imposes a vincolo esterno—i.e. an external constraint—on national policymakers, preventing them from using monetary policy to expropriate foreign creditors.

A peculiar feature of this framework is that forming a monetary union increases financial integration, without having any impact on real exchange rates or collateral value in equilibrium. The reason is that adopting a common currency mitigates the time-consistency problem faced by national governments, and eliminates the off-equilibrium threat faced by foreign investors of being expropriated through a depreciation. Empirically, this result implies that forming a monetary union might have a very big impact on capital mobility, even if it does not affect much real exchange rates, collateral value, and asset prices.22

3.4. Redistribution within the union, outside investors, and financial reforms

Before moving to the analysis of capital flows and welfare, it is useful to pause for a moment and consider a few extensions to the baseline model. This will help to further clarify the channels through which adopting a common currency fosters financial integration.

3.4.1. Redistribution within the union

In the baseline model, the union’s central bank has no incentives to redistribute wealth among member countries. But what if a redistributive motive exists? Here, I show that the presence of a redistributive motive might weaken the positive impact of forming a currency union on financial integration. This happens if the union’s central bank wishes to redistribute wealth out of creditor and toward debtor countries. However, even in this case, the key result that forming a monetary union fosters financial integration holds.

Notice that, as in the baseline model, I have assumed |$W=W^*$| so that |$p=p^*$| and |$Y_N = Y_N^*$|. I have also assumed that the home country is a debtor and the foreign one a creditor (|$D>0$|). Hence, a higher |$\xi$| is associated with a larger weight assigned to the consumption of tradable goods in the debtor country, compared to the creditor one.

Following the steps outlined in Section 3.1 one finds that, if the home country does not default, it is optimal for the central bank to replicate the natural allocation by setting |$p=Y_N=1$|. In fact, if the central bank attaches the same weight to both countries |$(\xi = 1/2)$|, setting |$p=1$| is optimal even in case of default by home agents. If |$\xi=1/2$|, the debt ceiling that creditors impose on the home country is then equal to |$\bar{D}_{mu}$|. This corresponds to the case studied in the baseline model, in which the union’s central bank has no incentives to use monetary policy to redistribute wealth among member countries.

This expression embeds two insights. First, notice that the debt ceiling is lower than |$\bar{D}_{mu}$|, and it is decreasing in |$\xi$|.24 Intuitively, the use of monetary policy to expropriate creditors ex-post induces investors to tighten the debt limit ex-ante. This effect is stronger the larger the weight attached to the debtor country by the union’s central bank, explaining why the debt ceiling is decreasing in |$\xi$|.

Moreover, the debt ceiling implied by expression (11) is higher than |$\bar{D}_\textit{flex}$|.25 Therefore, even if |$\xi>1/2$|, moving from flexible exchange rates to a monetary union increases financial integration. The reason is that adopting a common currency reduces the incentives to use monetary policy to expropriate creditors. On the one hand, this happens because the union’s central bank attaches some value to the consumption of tradable goods by agents in the creditor country (as long as |$\xi<1$|). But there is another, more subtle, reason. Deviating from the natural allocation (i.e. from setting |$p=1$|) is particularly costly in a monetary union, because it induces production distortions both in creditor and debtor countries. This second effect explains why, perhaps surprisingly, forming a monetary union increases financial integration even in the extreme case |$\xi=1$|, that is when the union’s central bank attaches no value at all to the consumption of tradable goods by agents in the creditor country.

Expression (11) also defines the debt ceiling when |$\xi<1/2$|, that is when the union’s central bank wishes to redistribute wealth from debtors to creditors. In fact, in this case the debt ceiling faced by the home country is higher than |$\bar{D}_{mu}$|. This means that a larger weight on creditors’ consumption in the objective function of the central bank amplifies the positive impact of forming a monetary union on financial integration.

Before ending this section, let me briefly mention what happens if the union’s central bank has an incentive to redistribute wealth from the richer to the poorer member countries of the union. As discussed in Appendix D, this effect arises if the utility that agents derive from consuming tradable goods is subject to diminishing returns. In this case, the temptation to use monetary policy to expropriate creditors is stronger if the debtor countries are relatively poor compared to the rest of the union. Conversely, if capital flows from the poorer to the richer member countries of the union, the central bank has an incentive sustain collateral value in order to prevent default. The implication is that forming a monetary union now has an asymmetric impact on financial integration. While forming a currency union increases foreign borrowing capacity for all member countries, this effect is stronger for the wealthier countries of the union, and it is weaker for the poorer ones.

3.4.2. Outside investors

The baseline model abstracts from financial flows between the monetary union and the rest of the world. Appendix C considers an extension of the model in which such flows are allowed. The key result is that even in this case forming a monetary union relaxes international borrowing constraints within the union, but it does not affect financial integration between the union and the rest of the world.

The intuition behind this result is quite simple. Just like national governments, the central bank of the union has an incentive to use monetary policy to expropriate outside investors. Hence, forming a monetary union does not change the maximal external debt that the union as a whole can sustain without defaulting. But, even in presence of outside investors, the central bank of the union has no incentives to use monetary policy to redistribute wealth among member countries. Therefore, as in the baseline model, adopting a common currency increases capital mobility within the union.

An interesting corollary of this result is that forming a monetary union creates an endogenous segmentation in the international credit markets. To make this point, let’s take the perspective of the home country. Moving from flexible exchange rates to a monetary union increases the maximal external debt that the home country can sustain without defaulting, from |$\bar{D}_\textit{flex}$| to |$\bar{D}_{mu} > \bar{D}_\textit{flex}$|. But, as shown in Appendix C, the debt ceiling that investors from outside the union need to impose on the home country to avoid expropriation is strictly lower than |$\bar{D}_{mu}$|. Therefore, any external debt in excess of the ceiling imposed by outside investors has to be obtained from investors within the monetary union. The reason why loans from investors outside and within the union are not perfect substitutes, of course, is that the central bank of the union has an incentive to use monetary policy to expropriate outside investors, but not investors within the union.

These insights might help explain why euro area countries receive the majority of their capital inflows from within the union (Gros, 2017). Through the lens of the model, adopting the euro should have increased capital mobility within the union, while leaving essentially unaffected financial integration between the union and the rest of the world.

3.4.3. Financial reforms

Besides altering their exchange rate regime, countries can foster financial integration by undertaking legal reforms that remove barriers on international capital flows. For instance, as discussed by Kalemli-Ozcan et al. (2010), the introduction of the euro has been accompanied by reforms aiming at harmonizing financial regulation among member countries. Their empirical analysis also suggests that these reforms had a positive impact on financial integration, which complemented the direct effect due to the disappearance of currency risk.

In the model, a financial reform can be captured by an increase in the fraction of output that foreign creditors can repossess upon default, i.e., by a rise in |$\kappa$|. Independently of the exchange rate regime, the result is a rise in the amount of foreign debt that a country can sustain without defaulting. So, there are some similarities between financial reforms and adopting a common currency, in that they both lead to higher financial integration and more capital mobility.

In words, the impact of a rise in |$\kappa$| on the stock of foreign debt that a country can sustain without defaulting is larger in a currency union. The reason is that the higher |$\kappa$| the bigger the effect of an exchange rate depreciation on collateral value. This means that, under flexible exchange rates, the central bank’s incentive to use monetary policy to expropriate foreign creditors is increasing in |$\kappa$|. This effect reduces the positive impact of a rise in |$\kappa$| on financial integration. In a currency union, this effect is not present, and so a rise in |$\kappa$| has a larger impact on the country’s debt ceiling. This observation might help to explain why, as noted by Kalemli-Ozcan et al. (2010), the adoption of the euro was accompanied by financial reforms. The interpretation offered by the model is that the adoption of the euro might have increased the payoff of these reforms in terms of higher financial integration.

Turning to the differences, financial reforms act at the microeconomic level, that is by lifting the debt ceiling that foreign creditors impose on each individual borrower. Instead, changes in the exchange rate regime act at the macroeconomic level, that is by affecting the aggregate stock of foreign debt that a country can sustain without defaulting. The implication is that after a financial reform we should observe a rise in the value of collateral that each individual borrower can offer to foreign creditors. This need not be the case if higher financial integration is achieved by forming a common currency.

To see this point, consider the home country under flexible exchange rates. As we have seen, in equilibrium the aggregate stock of foreign debt cannot exceed |$\bar{D}_\textit{flex}$|, the central bank sets |$p=1$|, and the amount of collateral observed is equal to |$\kappa (Y_T + 1)$|. This means that some home agents may very well borrow up to |$\kappa (Y_T +1)$| from foreign investors, as long as the aggregate stock of foreign debt is smaller than |$\bar{D}_\textit{flex}$|.26 Forming a currency union relaxes the ceiling on the aggregate stock of foreign debt, but it does not alter the value of collateral observed in equilibrium, which is still equal to |$\kappa ( Y_T +1 )$|. Adopting a common currency therefore does not relax the credit friction at the microeconomic level, since it does not affect the maximal debt that each individual borrower can take. In contrast, a financial reform, captured by a rise in |$\kappa$|, leads precisely to an increase in the amount of collateral observed in equilibrium. It thus acts by relaxing the credit constraint faced by each individual borrower.

A second difference is that forming a currency union causes an increase in financial integration within the union, while not affecting significantly financial integration between the union and the rest of the world (see Section 3.4.2). Financial reforms, instead, are likely to lead to a better enforcement of the rights of all foreign creditors.27 It is thus plausible to expect that financial reforms will end up lifting the borrowing limit toward all foreign creditors, and not just toward investors within the union. Achieving higher financial integration by forming a currency union, as opposed to undertaking financial reforms, should therefore have a disproportionately large impact on capital flows within the union.

4. Capital flows and welfare

We have just seen that forming a monetary union increases financial integration. But does this process lead to efficient capital flows and higher welfare? To answer this question, we need to fully characterize the equilibrium of the model. It turns out that the answer is not clear cut. To make this point, I will start by describing a scenario in which forming a monetary union unambiguously increases welfare. I will then turn to a scenario in which adopting a common currency might generate welfare losses by inducing financial instability and capital misallocation.

4.1. The benign view

To interpret this condition, consider that there are two possible cases. First, it might be that home agents’ debt ceiling is large enough so that all the savings are channelled toward the home country (|$I = N+ N^*$|). Instead, if home agents’ debt ceiling is tight enough the home country is not be able to absorb the entire stock of global savings. In this case, the interest rate must be such that foreign agents are indifferent between investing in foreign capital or lending to home agents |$(R = A^*)$| and home investment is equal to |$I = N + \bar{D}/A^*$|. Hence, due to the presence of financial frictions, in the competitive equilibrium the allocation of capital might be inefficient.

Let us now focus on a scenario in which under flexible exchange rates only part of global savings are invested in the home country. This is the case if the following assumption holds.

These inequalities ensure that credit constraints are tight enough so that home agents are not able to absorb all foreign savings. The second inequality implies that the credit multiplier |$\kappa A/A^*$| is smaller than 1, so that an increase in investment by one unit generates less than a unit increase in collateral value.

Now consider what happens if the two countries form a monetary union. As discussed above, the borrowing limit |$\bar{D}$| increases. Once a monetary union is created, therefore, more capital ends up flowing toward the high-return home country. The international allocation of capital thus becomes more efficient, and global production of tradable goods increases. Since equilibrium production of non-traded goods does not depend on the exchange rate regime, higher output of tradables leads to higher welfare.29

Suppose that |$A > A^*$| and that assumption 1 holds. Then moving from flexible exchange rates to a monetary union leads to an increase in global output of tradable goods and welfare.

There are two points worth mentioning. First, in this model forming a monetary union increases welfare only if member countries are asymmetric in terms of their investment opportunities. Indeed, if |$A=A^*$|, there are no welfare gains from sharing a common currency. This contrasts with the traditional optimal currency area literature, in which giving up exchange rate flexibility is costly precisely when countries are hit by asymmetric shocks. Second, forming a monetary union has a positive impact on welfare only if under flexible exchange rates credit frictions prevent capital from being allocated efficiently across countries. Hence, it is optimal to form a currency union only if financial markets are not too developed to start with.30

The results presented so far are in line with Ingram’s view. Forming a monetary union boosts financial integration and leads to a more efficient allocation of capital across member countries. But, as I will show next, such a benign view is not the only possibility.

4.2. The not-so-benign view

Compared with the recent experience of the euro area, the benign view of the previous section seems to be at best incomplete. The euro area crisis, in fact, was characterized by high volatility in financial markets and sharp reversals in capital flows. Summarizing the existing literature, Akerlof (2019) argues that episodes of financial instability can be rationalized with the existence of complementarities in investment decisions among agents. This section builds on this notion and shows that, in presence of investment complementarities, forming a monetary union might lead to coordination failures among agents, capital misallocation, and welfare losses. The key insight is that high financial integration facilitates large and swift movements of capital across countries. In turn, a high degree of capital mobility may open the door to episodes of inefficient capital flights driven by pessimistic expectations.

Complementarities in investment decisions arise when the private return to investing is increasing in aggregate investment. Though several options are possible, I will focus on increasing returns arising from a fiscal externality. In a nutshell, capital taxation influences the private return from investing. But, since the tax base depends on the capital stock, investment affects the level of taxation. As shown by Eaton (1987) and Velasco (1996), this complementarity can give rise to episodes of inefficient capital flights driven by animal spirits. Intuitively, expectations of high taxes on capital depress investment, and therefore the tax base. A low tax base forces the government to impose a high tax rate to finance its expenditures, validating agents’ initial expectations. This story is reminiscent of some aspects of the recent euro area crisis, during which capital flights from peripheral to core countries coincided with fiscal stress.31 I will now show that, under certain conditions, monetary unions can be particularly prone to experience these episodes of inefficient capital flights.32

Suppose that the government in the home country has to finance an exogenous spending in period 1, equal to |$G$| units of the tradable good. This fiscal expenditure could represent the cost of solving a domestic banking crisis, result from the kick in of automatic stabilizers during a deep recession, or be the consequence of the spread of a pandemic. This assumption could also capture a public debt overhang scenario, in which high public expenditure derives from interest payments on a large stock of inherited public debt.33 It does not matter too much how government expenditure affects households’ utility. In fact, the results that follow hold regardless of whether government expenditure is a pure waste, it is rebated to domestic households through lump-sum transfers or it enters directly households’ utility function, as long as utility is separable in government expenditure.

When choosing their investment strategy, agents compare the after-tax return from investing in domestic capital to the interest rate. In turn, the interest rate depends on the relative return from investment in the home and foreign country. To simplify the exposition, I will restrict attention to interior equilibria in which investment is positive in both countries. This happens if agents’ borrowing capacity is low enough compared to the supply of savings. To ensure that this is the case, I will make the following parametric assumptions.

We now have three possible cases to consider. First imagine that the after-tax return from investing in the home country is high enough so that |$\tilde{A} > A^*$|. Then home agents maximize investment in domestic capital, by borrowing as much as possible from abroad. The equilibrium interest rate is then equal to |$A^*$|, to ensure that foreign agents are indifferent between investing domestically and lending on the international credit markets. Now suppose that the after-tax return to home investment is low, so that |$\tilde{A} < A^*$|. Then home agents maximize lending on the international credit markets. The equilibrium interest rate is equal to |$\tilde{A}$|, so that home agents are indifferent between investing in domestic capital and lending to foreign agents. Finally, if |$\tilde{A} = A^*$| agents are indifferent between investing at home or in the foreign country, and the equilibrium interest rate is |$A^*$|.

There are two observations to make. First, as it is natural, a lower tax rate on home investment induces a (weakly) higher production of tradable goods in the home country. Second, the impact of changes in taxes on investment depends on the ease with which capital can be moved across the two countries, as captured by the debt ceilings |$\bar{D}$| and |$\bar{D}^*$|. Higher debt limits correspond to a stronger sensitivity of investment and production to changes in taxes.

The schedules |$\tilde{A}$| and |$I$| describe two increasing relationships between the tax rate on capital and production of tradable goods. As stated by the following proposition, the feedback loop between these two variables can be strong enough to generate multiple equilibria.

Suppose that the parameters satisfy the conditions stated by assumption 2. If |$G < (A-A^*) (N + \bar{D}/A^*)$| there exists a unique stable capital inflows equilibrium in which home agents borrow up to the limit and maximize investment in domestic capital. If |$G > (A-A^*) (N - \bar{D}^*/A^*)$| there exists at least one stable capital flight equilibrium in which home agents maximize lending to foreign agents. Therefore, if |$(A-A^*) (N - \bar{D}^*/A^*)< G < (A-A^*) (N + \bar{D}/A^*)$| there are multiple stable equilibria. If multiple equilibria are possible, global output and welfare are higher in the capital inflow equilibrium compared to the capital flight equilibria.

Proposition 4 implies that if |$G$| is sufficiently small there is a capital inflows equilibrium, in which the after-tax return from investing at home is higher than the interest rate and capital flows toward the home country. If |$G$| is large enough, instead, capital flight equilibria are possible. In these equilibria the after-tax return from investing at home is lower than the return from investing in the foreign country. Therefore capital flies toward the foreign country. Fiscal externalities can thus distort the international allocation of capital, by inducing capital flows toward the country in which investment is least productive. Moreover, for intermediate values of |$G$| both type of equilibria coexist. In this case, agents’ expectations determine which equilibrium materializes. These results essentially extend the findings of Eaton (1987) and Velasco (1996) to this setting.

Proposition 4 also establishes a novel link between the exchange rate regime and the international allocation of capital. Notice that according to Proposition 4 the degree of international financial integration, as captured by the debt ceilings |$\bar{D}$| and |$\bar{D}^*$|, is a key determinant of whether capital flows into or flies from the home country. The exchange rate regime, through its impact on financial integration, can therefore affect the direction of capital flows.

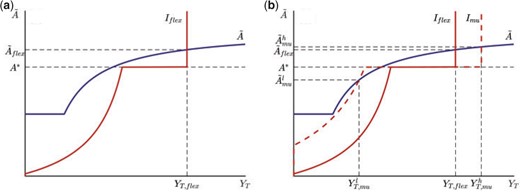

It is not hard to construct a scenario under which forming a monetary union can worsen the international allocation of capital. This point can be seen most clearly by looking at Figure 1, which visually represents the |$\tilde{A}$| and |$I$| schedules in the |$Y_T - \tilde{A}$| space. An equilibrium corresponds to a point in which the two curves intersect.

Exchange rate regime and capital flows.

Notes: Left panel: Unique equilibrium with flexible exchange rates. Right panel: Multiple equilibria in a monetary union.

Imagine that under flexible exchange rates there is a unique equilibrium characterized by capital inflows toward the home country. This case is shown by Figure 1(a). As highlighted by Proposition 4, a capital inflow equilibrium exists under flexible exchange rates if |$G < (A-A^*) (N + \bar{D}_{flex}/A^*)$|. Intuitively, this condition ensures that with capital inflows the tax base in the home country is large enough to guarantee that the after-tax return from investing at home is higher than the interest rate.

It is useful to pause for a second and consider why the capital flight equilibria are instead ruled out. Imagine that agents anticipate that the after-tax return from investing at home will be lower than |$A^*$|. In this case, the home country will experience a capital flight. However, if foreign agents’ debt limit is tight, the capital flight will be small, and so it will have a small impact on investment, on the tax base and so on the tax rate. But then the return from investing at home will not fall below |$A^*$|, contradicting the initial pessimistic expectations.36 In this scenario, therefore, under flexible exchange rates expectations-driven capital flights cannot take place because international capital mobility is too low.

What might happen if the two countries adopt a common currency? A possible outcome is displayed by Figure 1(b). Once a currency union is formed financial integration increases, leading to a rise in the borrowing limits |$\bar{D}$| and |$\bar{D}^*$|. Domestic agents can now sustain a higher amount of foreign debt. Hence, if |$\tilde{A} > A^*$|, home agents increase their foreign borrowing and more capital is installed in the home country. Graphically, this is captured by the rightward shift in the |$I$| schedule. This implies that, if expectations coordinate on the capital inflow equilibrium, forming a monetary union leads to a more efficient international allocation of capital and to higher global production of tradable goods.

But forming a monetary union also increases the borrowing capacity of foreign agents, as captured by the leftward shift of the |$I$| schedule for |$\tilde{A} < A^*$|. Now consider what happens if expectations coordinate on a capital flight equilibrium. Since the borrowing capacity of foreign agents is now higher, more capital flies out of the home country. If |$G > (A-A^*) (N - \bar{D}^*_{mu}/A^*)$|, the capital flight is large enough to push the after-tax return on home investment below |$A^*$|. Pessimistic expectations thus become self-fulfilling, and the capital flight indeed occurs. Forming a monetary union therefore creates the possibility of coordination failures in investment decisions. The following corollary to Proposition 4 collects these results.

Suppose that assumption 2 holds and that |$(A-A^*)(N - \bar{D}_{mu}^*/A^*)< G < (A-A^*)(N - \bar{D}_{flex}^*/A^*)$|. Then under flexible exchange rates the equilibrium is unique and features capital inflows. Instead, in a monetary union there is a stable capital inflows equilibrium and at least one stable capital flight equilibrium.

In this example, the case in favour of forming a monetary union is not clear cut, and depends on expectations and animal spirits. If agents are optimistic, giving up exchange rate flexibility to join a monetary union leads to an increase in welfare, by fostering a more efficient allocation of capital across countries. However, in a monetary union self-fulfilling episodes of inefficient capital flights are possible. In particular, a wave of pessimism can induce capital flows toward the country characterized by the lowest productivity. When this happens, global production and welfare drop.

This example illustrates one of the potential dangers of forming a monetary union. The easiness with which capital can flow across countries in a monetary union, in fact, can generate financial instability and capital misallocation. Moreover, inefficient capital flights are more likely to happen when a monetary union is hit by large shocks requiring a fiscal response, such as during the ongoing Covid-19 pandemic. In this respect, the model suggests that participating in a common currency might hamper national governments’ ability to react to shocks through fiscal policy. This is the case because, due to high capital mobility, a large increase in government expenditure creates the conditions for capital flights driven by pessimistic animal spirits.37

5. Policy Implications

A natural question to ask is whether there exist policy interventions that can rule out capital flight equilibria, so as to ensure that increasing financial integration by forming a monetary union leads to a rise in the union’s welfare. I will now show that several policies can accomplish this objective. But I also argue that implementing them, due to their distributive implications, might require a high degree of international cooperation.

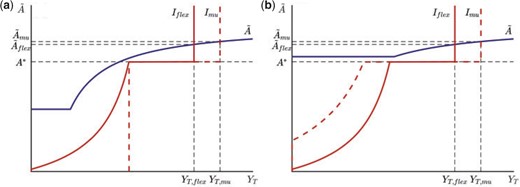

5.1. Capital controls and fiscal transfers

Managing capital flows in a monetary union.

Notes: Left panel: Capital controls. Right panel: Fiscal transfers.

In practice, however, imposing controls on capital outflows might be challenging. The reason is that private agents have strong incentives to elude them. Ultimately, whether a government can successfully implement controls on outflows is an empirical question. While the jury is still out, existing evidence suggests that controlling capital outflows is a complicated task. For instance, Edwards (1999) summarizes the experience of emerging markets with controls on outflows, and concludes that they had a very limited impact on actual flows. Moreover, due to the complexity of their financial systems, successfully implementing controls on outflows in advanced economies might represent an even bigger challenge. In fact, Ilzetzki et al. (2019) document that controls on capital outflows have essentially been absent in advanced economies since the early 1990s.39

Let us also assume that the transfer is indexed to home production of tradable goods, according to the function |$T=\max\left(G-\tilde{\tau} Y_T, 0\right)$|. This policy effectively imposes an upper bound on the capital tax equal to |$\tilde{\tau}$|. As long as |$A(1-\tilde{\tau}) > A^*$|, capital flight equilibria are ruled out. The reason is that, as shown by Figure 2(b), with this policy in place the return to investment at home never falls below the foreign one.

So a system of sufficiently strong countercyclical transfers eliminates inefficient capital flights, by anchoring expectations on the good equilibrium in which capital flows toward high-productivity countries. Notice that, as long as the transfer scheme is credible, inefficient capital flights are ruled out without the need to actually transfer resources across countries in equilibrium. Aside from the benefits already highlighted by the literature, complementing a monetary union with a system of fiscal transfers has thus the additional advantage of preventing episodes of capital flights driven by pessimistic animal spirits.

5.2. The importance of international cooperation

There is, however, a fundamental problem with the policies proposed above. The foreign government, in fact, has an incentive to oppose them. The reason is that capital flights out of the home country increase foreign citizens’ welfare. This happens because capital flights depress the interest rate, allowing foreign agents to profit from the spread between the interest rate and the return to investment. More formally, under Assumption 2, in a capital inflows equilibrium foreign agents’ consumption of tradable goods is equal to |$A^* N^*$|. Instead, in a capital flight equilibrium foreign households tradable consumption is |$A^* N^* + (A^*/\tilde{A} - 1)\bar{D}^* > A^* N^*$|, since in a capital flight equilibrium |$\tilde{A} < A^*$|. Hence, from a global perspective implementing policies that rule out capital flight equilibria makes sense. But these policies have important redistributive implications, and so not all countries might support them.40

The general lesson here is that there are several policies that can eliminate episodes of self-fulfilling capital flights. Implementing them, however, might be difficult due to their distributive implications. Indeed, during episodes of inefficient capital flights, some countries—which can be thought of as safe-haven countries—benefit from inflows of cheap foreign capital. Safe-haven countries might then end up loosing from policies that anchor expectations on the equilibrium that maximizes global welfare. This result suggests that successfully managing the high degree of capital mobility characterizing monetary unions requires close cooperation among member countries.

6. Conclusion

We have thus seen that forming a monetary union is likely to lead to an increase financial integration across member countries. With a single currency, the reason is, national governments cannot use monetary policy to expropriate foreign investors. However, boosting financial integration by forming a monetary union might have an ambiguous impact on welfare. This happens because high capital mobility opens the door to episodes of expectation-driven inefficient capital flights, especially during periods of large asymmetric fiscal shocks. While there are several policies that can eliminate pessimistic equilibria, most notably countercyclical fiscal transfers, their implementation requires international cooperation because of their redistributive implications.

This article represents a first step of a larger research program connecting the exchange rate regime to financial integration. To conclude, let me mention three questions that could be addressed in future research. The first one is about boom-bust cycles in capital flows. The model suggests that countries with low net worth positions are particularly vulnerable to episodes of capital flights driven by animal spirits. According to Proposition 4, in fact, capital flights out of the home country can materialize only if |$N$| is low enough. The interesting point here is that a low |$N$| might be the result of legacy external debt. In this case, a period of large capital inflows—if it leads to a deterioration of national net worth—might create the conditions for future financial instability. This reasoning hints at the possibility that monetary unions might be particularly vulnerable to boom–bust cycles in capital flows driven by animal spirits. To investigate this hypothesis, one would need to extend the model to a fully dynamic setting, which is a very exciting topic for future research.

The second one is motivated by the fact that, in the run up to the 2008 global financial crisis, capital flows toward peripheral euro area countries were associated with a slowdown in productivity growth. Several explanations have been advanced by the literature. Benigno and Fornaro (2014) show that capital inflows might lead to lower productivity growth by discouraging innovation activities by firms in the tradable sector.41 In Gopinath et al. (2017) and Reis (2013), instead, capital inflows depress productivity by inducing misallocation of capital across firms. This literature thus suggests that capital inflows might be detrimental to productivity growth. It would be interesting to revisit the benefits and costs from forming a currency union in light of this insight.

Third, in this article, I have focused on the impact of financial integration on net capital flows and on the international allocation of capital. International financial integration, however, also affects risk sharing across countries. In this respect, the model in this paper suggests that forming a currency union might facilitate international risk sharing, by increasing the potential for gross capital flows across member countries. Investigating the relationship between the exchange rate regime, gross capital flows and international risk sharing is a promising area for future research.

The editor in charge of this paper was Veronica Guerrieri.

APPENDIX

A. Proofs

A.1. Proof of Proposition 1

Under flexible exchange rates, default does not occur if and only if |$D \leq \bar{D}_{flex}$|. Moreover, in absence of default monetary policy sets |$p = Y_N = 1$|. Analogous expressions hold for the foreign country.

A necessary condition for this to be an equilibrium is |$D \leq \kappa \left(Y_T + 1\right)$|.

A necessary condition for this to be an equilibrium is |$D > \kappa \left(Y_T + \left(1 + \kappa (\eta - 1)\right)^{\frac{1}{\eta}-1} \right)$|.

One can show that |$\kappa \left(Y_T + \left(1 + \kappa (\eta - 1)\right)^{\frac{1}{\eta}-1} \right) < \bar{D}_{flex} < \kappa \left(Y_T + 1\right)$|.42 It follows that default is avoided if and only if |$D \leq \bar{D}_{flex}$|. The problem of the government in the foreign country is symmetric. □

A.2. Proof of Proposition 2

In a monetary union, the home country does not default if and only if |$D \leq \bar{D}_{mu}$|. Moreover, monetary policy sets |$p = Y_N = 1$|. Analogous expressions hold for the foreign country.

Analogous expressions hold for the foreign country. □

A.3. Proof of Proposition 3

Suppose that |$A > A^*$| and that assumption 1 holds. Then moving from flexible exchange rates to a monetary union produces an increase in global output of tradable goods and welfare.

So output of tradable goods is higher in a monetary union compared to flexible exchange rates. Since production of non-traded goods does not depend on the exchange rate regime, welfare is higher in a monetary union compared to the case of flexible exchange rates.

A.4. Proof of Proposition 4

Suppose that the parameters satisfy the conditions stated by assumption 2. If |$G < (A-A^*) (N + \bar{D}/A^*)$| there exists a unique stable capital inflows equilibrium in which home agents borrow up to the limit and maximize investment in domestic capital. If |$G > (A-A^*) (N - \bar{D}^*/A^*)$| there exists at least one stable capital flight equilibrium in which home agents maximize lending to foreign agents. Therefore, if |$(A-A^*) (N - \bar{D}^*/A^*)< G < (A-A^*) (N + \bar{D}/A^*)$| there are multiple stable equilibria. If multiple equilibria are possible, global output and welfare are higher in the capital inflow equilibrium compared to the capital flight equilibria.

Condition |$G < (A-A^*) (N + \bar{D}/A^*)$| ensures that |$\tilde{A} > A^*$|. This proves that a capital inflow equilibrium exists. To see why this equilibrium is stable, imagine that there was a slight fall in aggregate investment in domestic capital. The after-tax return to investing at home would still be higher than the interest rate, meaning that home agents would have an incentive to increase investment until the initial equilibrium is restored. We do not need to consider upward movements in aggregate investment, since the borrowing constraint rules them out.

Condition |$G > (A-A^*) (N - \bar{D}^*/A^*)$| then ensures that |$\tilde{A} < A^*$|. This proves that a capital flight equilibrium exists. To prove that this equilibrium is stable, consider a slight fall in aggregate investment at home. This triggers an increase in taxes and a drop in the interest rate. In turn, the drop in the interest rate increases borrowing from foreign agents leading to an increase in capital flights and a fall in home investment. The equilibrium is stable if the fall in investment drive by capital flight is smaller than the initial deviation. A symmetric argument holds for upward deviations. Therefore, an equilibrium is stable if around the equilibrium point the |$A(1-\tau)$| schedule is flatter than the |$I$| schedule. Looking at Figure 1 one can see that if a capital flight equilibrium exists, there is always going to be a capital flight equilibrium that satisfies this property.

The third part of the proposition follows from the fact that |$(A-A^*) (N - \bar{D}^*/A^*)< (A-A^*) (N + \bar{D}/A^*)$|. Finally, If multiple equilibria are possible the capital inflow equilibrium will feature the highest investment in home capital. Then the capital inflow equilibrium will also be the one with the highest global production of tradable goods. Since global production of non-tradables is the same across all the equilibria, the capital inflow equilibrium will also be the one with the highest global welfare. □

B. Multiple Equilibria with Technological Spillovers

In this Appendix, I consider a scenario in which coordination failures can happen due to the presence of technological spillovers. This is the case in the classic contributions by Bryant (1987) and Murphy et al. (1989). In these frameworks, agents can invest in two technologies, one of which is characterized by a higher return. However, investing in the high-return technology is profitable only if enough agents do so. Agents can thus coordinate on an optimistic equilibrium, in which everybody ends up adopting the high-return technology. But expectations can also coordinate on a pessimistic equilibrium, in which every agent remains stuck with the low-return inefficient technology.

In words, the return to investing in domestic capital experiences an upward jump once the threshold level of aggregate investment (|$\bar{I}$|) is reached. This is the case if switching from a low-return to a high-return technology entails positive spillovers across agents, so that the high-return technology is profitable only if it is adopted on a large-enough scale. For simplicity, assume that the return from investing in foreign capital is constant and equal to |$A^*$|. Moreover, to make things interesting, consider the case |$A_l < A^* < A_h$|. Hence, investing in the home economy is efficient only if the threshold level of investment |$\bar{I}$| is reached.

Individual investment decisions now depend on expectations of aggregate investment. In particular, if agents expect that |$I \geq \bar{I}$| they anticipate that capital will yield a higher return in the home country compared to the foreign one. It will then be optimal for home households to maximize investment in domestic capital by borrowing up to the limit. Conversely, if agents expect that |$I < \bar{I}$| it will be optimal for home agents to minimize investment in domestic capital by shipping as much capital as possible abroad.

Rather than fully characterizing all the possible equilibria of this version of the model, let me provide an example in which forming a monetary union reduces welfare. Again, restrict attention to equilibria in which the borrowing limit is always binding.43 Now consider a case in which the equilibrium under flexible exchange rates is as depicted in the left panel of Figure B.1.

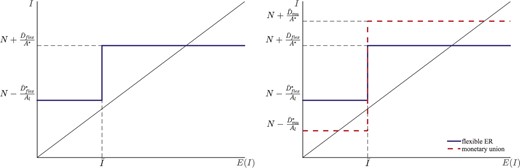

Equilibrium with aggregate increasing returns from investment.

Notes: left panel refers to flexible exchange rates, right panel shows impact of creating a monetary union.

Figure B.1 plots actual investment |$I$| as a function of expected investment |$E(I)$|. If |$E(I) \geq \bar{I}$| then it is more profitable to invest in home rather than in foreign capital. In this case, home agents borrow up to the limit to maximize investment in domestic capital. The equilibrium interest rate is |$R=A^*$|, so that foreign agents are indifferent between investing in foreign capital or lending to home agents. If instead |$E(I) < \bar{I}$|, it is foreigners who will maximize borrowing from domestic agents to invest in foreign capital. The borrowing capacity of foreign agents, however, is not large enough to fully absorb savings from home households, and so there is positive investment in home capital. The equilibrium interest rate is then |$R= A_l$|, so that home agents are indifferent between investing in capital or on the credit market.

In the case shown in the figure, the only possible equilibrium is one in which investment in home-country capital is large enough so that the high-return technology is adopted. It is useful to pause for a second and consider why the pessimistic equilibrium, in which the low-return technology is adopted, is ruled out. Imagine that agents anticipate that the low-return technology will be adopted. In this case, home agents will ship capital abroad until the borrowing constraint of foreign households ends up binding. But, in the case shown in the figure, the borrowing limit of foreign agents is so tight that investment in home capital exceeds the threshold |$\bar{I}$| even if expectations coordinate on the pessimistic equilibrium. For this reason, under flexible exchange rates the pessimistic equilibrium cannot materialize.

The right panel illustrates what may happen once a monetary union is formed. Domestic agents can now sustain a higher amount of foreign debt. Hence, if the high-return technology is adopted home agents increase their foreign borrowing and more capital is be installed in the home country. Graphically, this is captured by the upward shift in the investment curve for the range |$E(I) \geq \bar{I}$|. Therefore, if expectations coordinate on the optimistic equilibrium the efficiency in the international allocation of capital is higher in a monetary union compared to the case of flexible exchange rates.

But now consider what happens if agents expect that the low-return technology is adopted. Since the borrowing capacity of foreign agents is now higher, more capital flies out of the home country compared to the case of flexible exchange rates. In the case shown in the figure, this capital flight is large enough so that investment in home capital is lower than the threshold |$\bar{I}$|. Hence, the low-return technology ends up being adopted, validating agents’ initial pessimistic expectations. Forming a monetary union thus creates the possibility of coordination failures in investment decisions.44

C. Outside Investors

The model in the main text abstracts from financial flows between the monetary union and the rest of the world. This appendix revisits the analysis in Section 3, allowing agents in the monetary union to trade in financial assets with outside investors.

Imagine that there exists a third country, called rest of the world. This country does not join the monetary union, in case one is formed, but it is otherwise symmetric to the home and foreign countries considered in the main text. Denote by |$\mathcal{D}$| and |$\mathcal{D}^*$| the debt to be repaid in period 1 to investors in the rest of the world, respectively by the home and foreign country. We are interested in understanding how the presence of this external debt affects the impact of forming a monetary union on financial integration.

C.1. Flexible exchange rates