Abstract

This paper explores the impact of product market competition on the positive relation between labor mobility (LM) and future returns. We develop a production-based model and formalize the intuition that low exposure to systematic risk in a concentrated industry limits LM’s amplifying effect on operating leverage. Therefore, the model predicts a stronger positive relation between LM and expected returns for firms in competitive industries. Consistent with the model’s prediction, we empirically find that LM predicts returns only among firms in competitive industries. This evidence suggests that the intensity of competition in firms’ product market potentially drives the positive LM-return relation. (JEL G12, G14, J69)

Authors have furnished an Internet Appendix, which is available on the Oxford University Press Web site next to the link to the final published paper online.

Labor mobility (LM) is the flexibility of workers to enter and exit an industry in response to better opportunities. Recently, this has attracted much attention in the finance literature as Donangelo (2014) shows that firms in industries employing workers whose labor skills are more portable to other industries earn higher average stock returns than those in industries where workers have less portable skills. When the performance of an industry is relatively good, it tends to attract more mobile workers. But in times of adverse productivity shocks, mobile workers tend to leave this industry. The degree of dependency on mobile labor amplifies firms’ existing exposure to productivity shocks, as outflows of mobile workers in bad times reduce cash flows. This is precisely the source of the LM premium shown in Donangelo (2014) and closely related to the risk amplification effect of labor leverage in Donangelo et al. (2019). This line of analysis, however, assumes optimistically a perfectly competitive product market environment.

Congruently, product market competition is the other well-known industrial characteristic that affects firms’ exposure to productivity shocks, but in an opposite way to the LM. For example, Dou, Ji, and Wu (2021), Hou and Robinson (2006), and Peress (2010) show that market power shields firms from nondiversifiable aggregate shocks. In other words, the operating profits of firms in more concentrated (i.e., less competitive) industries are less sensitive to the productivity shocks thanks to the benefits brought by the market power (stemming from tougher barriers to entry, low elasticity of substitution, etc.). In light of their connection with the productivity shocks, it is particularly interesting to study the juxtaposition of product market competition and LM as well as their joint asset pricing effect on the cross-section of stock returns.1 More concretely, in view of the market power to insulate firms from the productivity shocks, it is no longer clear whether the risk amplification from LM is still significant for firms in less competitive industries. In a concentrated industry, where the performance is less correlated with nondiversifiable productivity shocks, from investors’ point of view, the risk induced by inflow and outflow of mobile labor is more idiosyncratic and hedgeable. Therefore, it remains unanswered that whether LM in a concentrated industry still carries a premium in equilibrium. To the best of our knowledge, despite the first-order importance of these questions, no prior studies have attempted to answer them. These questions motivate our research in this paper and are answered in our theoretical and empirical analyses.

Guided by the work of Peress (2010), our model generalizes the mobility-production economy of Donangelo (2014) and allows for a variable measure of the product market competition. This competition measure plays a key role in quantifying the combined sensitivity to the systematic productivity shocks from the interplay between LM and product market competition. Specifically, the imperfect elasticity of substitution combined with the market concentration, which measures (the inverse of) the degree of product market competition, propagates to the demand for mobile labor, which further determines the operating profits, in the initial production stage through the price of the intermediate goods in the final product market. By construction, the mobility-production model of Donangelo (2014) is nested as a special case assuming perfect competition within our model. The solution of our model allows to study the joint effect of LM and market competition on operating leverage, which acts as a systematic risk multiplier in the firm risk. Importantly, we show that when market power within an industry is large enough, LM can barely have any effect on firms’ systematic risk. This means that the insulation induced by the market power can quickly overshadow the LM’s amplification on systematic productivity shocks. These results from our model indicate that the LM premium is more significant or exists only for firms in highly competitive industries. To verify this novel theoretical prediction, we develop a testable hypothesis that the positive LM-return relation strengthens with the intensity of product market competition.

We test our hypothesis both by independently double sorting stocks on LM and product market competition and by Fama and MacBeth (1973) cross-sectional regressions. The results from the portfolio analyses show that the positive LM-return relation exists only in competitive industries. For example, the high-minus-low LM portfolio in competitive industries delivers an economically significant value-weighted average monthly return of 0.83% (t-statistic = 3.05). The value-weighted characteristic-adjusted return of 0.79% per month on this hedge portfolio is also statistically significant, with a t-statistic of 3.76. The LM premium in competitive industries persists even after adjusting for risk using premier asset pricing models. In particular, the value-weighted average monthly abnormal returns on the hedge portfolio relative to the (unconditional) capital asset pricing model of Sharpe (1964) and Lintner (1965), the Ferson and Schadt (1996) conditional capital asset pricing model, the Fama and French (1993) three-factor model, the Fama and French (1993) and Carhart (1997) four-factor model, the Fama and French (2015) five-factor model, and the Hou, Xue, and Zhang (2015)q-factor model are 0.82%, 0.84%, 0.92%, 0.69%, 0.83%, and 0.69%, with t-statistics of 3.07, 2.96, 3.23, 2.44, 2.53, and 2.08, respectively. In contrast, the high-minus-low LM portfolio in concentrated industries generates a monthly return of –0.15% (t-statistic = –0.91). The value-weighted characteristic-adjusted return of –0.23% per month on the portfolio is also statistically insignificant (t-statistic = –1.30). Furthermore, the average monthly abnormal returns on the portfolio relative to the asset pricing models are all negative and statistically indistinguishable from zero at conventional levels. Specifically, the capital asset pricing, the conditional capital asset pricing, the three-factor, the four-factor, the five-factor, and the q-factor model alphas are, respectively, –0.09% (t-statistic = –0.58), –0.14% (t-statistic = –0.87), –0.02% (t-statistic = –0.12), –0.02% (t-statistic = –0.13), –0.02% (t-statistic = –0.14), and –0.08 (t-statistic = –0.42). We also empirically verify the key mechanism of our model, in which the market power overshadows LM’s risk amplifying effect, by showing the cross-sectional variation of factor loadings on the LM-based productivity risk factor is larger (smaller) in more (less) competitive industries.

The empirical results, supporting our hypothesis, remain robust to using: the all-but-microcaps sample, which excludes stocks with a market value of equity below the 20th percentile of the NYSE market capitalization distribution; an extended sample period; unlevered returns; industry-level returns; independent double-sorted quartile or quintile portfolios; and a wide range of product market competition measures suggested in the recent literature. For example, we employ competition measures based on the data from the U.S. Census of Manufacturers (as in Bustamante and Donangelo, 2017), both private and public firms (as in Hoberg and Phillips, 2010), firm’s product market fluidity (as in Hoberg, Phillips, and Prabhala, 2014), total assets instead of net sales (as in Hou and Robinson, 2006), and price-cost margin (as in Peress, 2010).

The model’s prediction is also supported by the results from the cross-sectional regressions. After controlling for the potential effects of size, book-to-market equity, short-term reversal, momentum, and leverage, the results confirm that a significantly positive LM-return relation prevails only for firms in competitive industries. For example, the average slope estimates of returns on LM are 0.46 (t-statistic = 4.74) and 0.09 (t-statistic = 1.39), respectively, in competitive and concentrated industries. Importantly, the average spread between the slope estimates of returns on LM in competitive and concentrated industries is 0.37, which is statistically significant with a t-statistic of 3.01. The results remain qualitatively similar, when we conduct cross-sectional regression analyses using: the all-but-microcaps sample; an extended sample period; and different measures of product market competition. In a separate cross-sectional regression analysis, we also create interaction terms involving market competition dummy variables. After controlling for firm-level attributes, such as size, book-to-market equity, short-term reversal, momentum, and leverage, the results remain robust and support our theoretical model’s prediction of a stronger LM-return relation among firms in competitive industries. For example, we find that, all else being equal, a one-standard deviation increase in LM is associated with 24 basis points higher future returns per month for firms in competitive industries relative to all other firms. A qualitatively similar finding emerges when we run panel data regressions.

Our paper contributes to two strands of literature. First, our model belongs to the burgeoning literature discussing economic mechanisms that generate labor-induced operating leverage. The general equilibrium model by Danthine and Donaldson (2002) is one of the first to articulate a mechanism in which operating leverage induced by the priority status of wage claims magnifies the risk properties of the residual payments to firm owners and justifies a substantial risk premium. Favilukis and Lin (2016) develop a general equilibrium model to examine the quantitative effect of sticky wages and labor leverage on the equity premium and the value premium. Along this line of research, Donangelo et al. (2019) provide theoretical support and empirical validation that firm-level labor share acts as a proxy for firm-level labor leverage. Our model is most close to Donangelo (2014), who shows that labor flows make bad times worse for shareholders through the LM-induced operating leverage. But different from Donangelo (2014), we focus on the more plausible case of imperfect competition.

Second, our paper is related to the theoretical studies linking industrial organization to financial markets. Aguerrevere (2009) explores the opposing effects of market competition and industry growth on expected returns. Opp, Parlour, and Walden (2014) emphasize that market competition is linked with market efficiency in a very complex way. Bustamante and Donangelo (2017) study the impact of market competition on systematic risk through the operating leverage, the entry threat, and the risk feedback channels with opposing effects. Our model is also closely related to Peress (2010), who investigates the interplay between competition in the product market and information asymmetries in the equity market. We adopt the two-sector (a final and an intermediate goods sector) economy setup of Peress (2010) in our model. Other recent studies that are broadly related to our paper include Corhay, Kung, and Schmid (2020) and Loualiche (Forthcoming). By building general equilibrium models with endogenous firm entry, both these papers examine the interaction between product market competition and asset prices. Our paper is also related more generally to Chen et al. (2021) and Dou, Ji, and Wu (2021). Chen et al. (2021) study the dynamic interactions between endogenous strategic competition and financial distress. Dou, Ji, and Wu (2021) develop an industry-equilibrium model with dynamic strategic competition to examine the joint fluctuations in aggregate discount rates, profitability, market competition intensity, and asset prices.

The uniqueness of our contribution is from the fact that we contribute to the joint venue of these two important strands of literature. The novelty of our continuous-time model lies in the analytical resolution of asset pricing implications from the interplay between LM and product market competition. To the best of our knowledge, we are the first to show, both theoretically and empirically, that market competition has a nontrivial effect on risk and return profiles of firms in high-mobility industries. In other words, the intensity of competition in firms’ product market drives a significant portion of the positive LM-return relation. This novel finding contributes to the growing subset of the asset pricing literature that investigates the interaction effect of firm characteristics on expected stock returns. Specifically, some recent papers documenting the important role that product market competition plays in explaining other cross-sectional asset pricing anomalies include Deng (2019, profitability), Dou, Ji, and Wu (2021, 2022, profitability), Giroud and Mueller (2011, corporate governance), and Gu (2016, research and development investment). In this context, we provide robust evidence of another important role that competition plays in the riskiness among firms in low- and high-mobility industries. Our study also contributes to the strand of production-based asset pricing literature that links firm characteristics to expected stock returns (see, among others, Belo, Lin, and Bazdresch, 2014; Belo et al., 2017; Cochrane, 1991; Croce, 2014; Zhang, 2019, and the references therein). Taken together, our theoretical model and strong supporting evidence improve the understanding of the joint issues across the industrial organization, and the labor and financial markets.

1. The Model

In this section, we derive a partial equilibrium model characterizing the role of product market competition in the positive relation between LM and expected stock returns. Building on the work of Peress (2010), the model introduces the more plausible case of imperfect competition to the mobility-production model developed by Donangelo (2014), which in fact assumes a perfectly competitive product market environment. Below, we outline the environment of our dynamic model and present the mechanism underlying the model’s testable prediction.

1.1 Output integrating labor and competition

We integrate LM and market competition by extending the mobility-production economy setup of Donangelo (2014) with the risk-less technology of final good production in Peress (2010).2 Specifically, we assume N firms produce intermediate goods at time t, and the final good is produced by a competitive representative final good producer (see, e.g., Corhay, Kung, and Schmid, 2020) according to a risk-less technology where is the intermediate output from ith firm and is the final output of the economy at time t, and .3 The lower , the less the elasticity of substitution between any two goods and a less competitive input market (Peress, 2010). Therefore, it measures the degree of competition in the intermediate goods sector.

Following the mobility-production economy of Donangelo (2014), we model each intermediate good output as where is the industry-specific labor skills employed by ith firm, is the output elasticity of labor, and denotes total factor productivity (TFP), which follows the diffusion process

1.2 Operating profits

Similar to Peress (2010), we use the price of the final good as the numeraire in what follows. It is worth mentioning that introducing an intermediate goods market with imperfect competition into the model economy is a convenient way to embrace imperfect competition at the whole industry level. When considering the operating profits for an average firm in the industry, we focus on the profits of each intermediate good producer.

1.2.1 Profits of the intermediate goods market

Total profits of the final good producer are given by where is the price of the ith intermediate good. The final good producers set their demand for inputs to maximize profits, . The resultant demand for each intermediate good input is . This means that when the intermediate goods market clears, the price of the intermediate good is simply

Given Equations (1) and (4), total revenue for each intermediate good producer is

We follow Donangelo (2014) and assume the only cost for the intermediate good producers is wage.4 Therefore, the profit of each intermediate good producer is given by where is the hourly wage of the labor with specific skills (see Donangelo, 2014). Each intermediate good producer sets her demand for labor to maximize profits, taking the wage, , as given. The first-order condition yields the following:

From Equation (7), we can see that because of the identical technology and constant elasticity of substitution, the labor demand, , is identical for all firms, that is, for , in equilibrium. This further implies that we have and in equilibrium. Therefore, the equilibrium final output can be simplified as

Substituting (7) for into Equation (6) yields

1.2.2 Wages and labor supply

Considering N intermediate good producers with identical labor demand , the total demand for labor is . Therefore, the profit of each intermediate good producer is connected to and N as

Hourly wages per unit of general skills are exogenously given by the diffusion process

Following Donangelo (2014), we derive the equilibrium supply of the labor with specific skills. Specially, labor markets are composed of a continuum of workers with permanent occupations based on their endowed composition of labor skills. The occupations, labeled by the index in decreasing order of labor skill specialty, are modeled as

The parameter determines the level of generality of labor skills required by the production technology. Thus, represents the level of LM in the industry (see Donangelo, 2014). Same as , we treat as another exogenous parameter. Insignificant correlations between empirical measures of these two parameters justify this exogeniety setting. We present the empirical observations in Appendix A. At time t, given an indifference marginal occupation , labor markets are in equilibrium when all workers in occupations strictly prefer to remain inside the industry, and all workers in occupations strictly prefer to remain outside the industry; therefore, the equilibrium level of employable labor skills useful inside the industry is given by:

The equilibrium indifference marginal occupation and the resultant equilibrium level of employable labor skills are derived and summarized in the following proposition.

Given the general skill wage, , the TFP, , the average level of competition, , and the number of intermediate good producers, N, the supply of labor with specific skills in equilibrium iswhere and .

Proof. See Appendix A. ▪

Now, the equilibrium operating profit of each intermediate good producer,5, can be expressed formally as

Several comments are in order before we move on. The market competition is captured primarily by . A simple inspection of Equation (14) shows that together with , LM partially controls operating profits’ sensitivity to , which Donangelo (2014) defines as the relative productivity of the industry. Indeed, conditional on , increases operating profits’ sensitivity to systematic shocks. However, from Equation (14), we also see that more extensively than the LM, controls ’s direct connection with . This is consistent with Peress (2010), who finds that market power makes profits less sensitive to systematic shocks. More concretely, affects through three channels: (1) reflecting the source of uncertainty when there is no LM, the general productivity level is now scaled to be ; (2) reflecting the relative productivity; and (3) c reflecting ’s loading on the relative productivity due to LM. Our results show that imperfect competition (small ) not only reduces the systematic risk in both absolute (channel 1) and relative (channel 2) productivity but also limits the loading on the systematic risk in the relative productivity due to the LM (channel 3). In sum, we generalize the Donangelo (2014) model to allow for imperfect market competition, and show that the influence of LM on firms’ systematic risk is much weakened when the product market is not perfectly competitive. These effects are more directly quantified via operating leverage in Section 1.3. The following proposition formalizes the dynamics of .

Given the dynamics of and , has the following dynamicswhere and .

Proof. See Appendix A. ▪

1.3 Operating leverage as a systematic risk multiplier

Donangelo (2014) derives , which the author denotes as operating leverage, to quantify the systematic risk amplification. Note that in Donangelo (2014), is always larger than one and therefore one is subtracted from the quantity to have representing the systematic risk amplification. In our case, can be less than one (but always positive, which is shown in Proposition 3 and proven in Appendix A), we therefore define the operating leverage directly as . Note that measures the sensitivity of cash flow growth to the fundamental source of risk in a multiplier sense as opposed to the Donangelo (2014) amplification sense. Given Equation (15), the equilibrium operating leverage is expressed as

It is also important to note that Equation (13) in Donangelo (2014) is a special case of Equation (16) when , which corresponds to a perfectly competitive intermediate goods market. is increasing in when , which is generally true as wages for general skills are typically smoother than TFP (see Donangelo, 2014). This result is also consistent with Bustamante and Donangelo (2017, Proposition 1), where the authors show that the operating leverage is decreasing in concentration (which measures the inverse of market competition).6 However, different from Donangelo (2014), with the relation between and is no longer always positive and depends on the value of . We formalize these results in Proposition 3 below.

Given the dynamics of and , the definition of , and assuming , the following expressions are true:

;

; and

.

Proof. See Appendix A. ▪

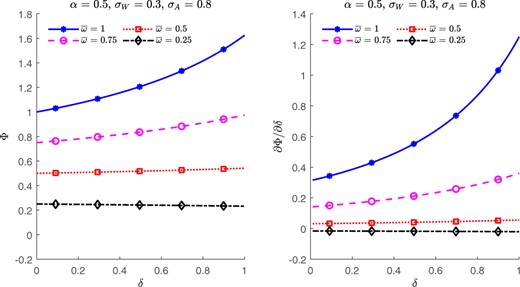

Proposition 3 quantifies the effects of LM and market competition on the systematic risk multiplier. Figure 1 illustrates the results. When , we reproduce the results of Donangelo (2014). The effect of LM on the systematic risk multiplier decreases mostly with the gradual decreasing of .7 More importantly, when is small enough, can barely have any effect on the firms’ systematic risk. In other words, firms’ market power can shield their profits from systematic shocks, and this insulation quickly overshadows LM’s amplification on systematic risk. These results of the systematic risk multiplier indicate that the asset pricing implications of LM (see, e.g., Donangelo, 2014) are likely to be strong or only exist in more competitive industries. Indeed, we find empirically that, in the cross-sectional dimension, in competitive industries, shocks are amplified by LM, but in concentrated industries, they are not (see Table A1 in the Appendix). In the time-series dimension, using large tariff cuts (LTC) as a proxy of increasing market competition (see Chen et al., 2021), we find that the sensitivity of firms’ profits and stock returns to a TFP factor becomes higher after the LTC and is only positively correlated with LM conditional on LTC (see Table IA3 in the Internet Appendix).8 We show in the next section that the results in Proposition 3 are directly linked to the asset pricing implications.

Φ versus δ

The left panel plots as a function of , and the right panel plots the first-order partial derivatives of w.r.t. . Four lines for , and 0.25 are plotted. The numerical values for the plots are shown in the subtitles.

1.4 Asset pricing implications

To explore asset pricing implications, we derive the value of a representative unlevered firm whose operating profits are given by . Consistent with the literature (see, among others, Berk, Green, and Naik, 1999, 2004; Donangelo, 2014), we take the pricing kernel as exogenous.9 The dynamics of the pricing kernel, denoted by , are given by where is a standard Wiener process representing the single source of systematic risk in the model, is the instantaneous risk-free rate, and is the market price of risk in the economy. Then, the value of the firm is the sum of all expected future operating profits (discounted properly):

Given , the firm’s instantaneous expected excess return is . The asset pricing implications of the interplay between LM and market competition can be revealed from , which is linearly linked to . The proposition below formalizes the results.

Given the dynamics of and , and assuming , the following expressions are true:

;

; and

.

Proof. See Appendix A. ▪

Part (3) of Proposition 4 combined with Part (1) of Proposition 3 indicates that LM has a positive effect on the firm’s expected excess return only when , and the degree of the effect is positively related to since . The asset pricing implication of LM diminishes when is close to zero. Therefore, we develop a testable hypothesis that the positive relation between LM and expected stock returns for firms strengthens with the degree of product market competition. In other words, the LM premium is more significant or prevails only for firms in highly competitive industries. In the following sections, we test our hypothesis and show robust evidence consistent with our theoretical model’s prediction. Although in the model we derive above we treat and N as independent parameters, we argue that can be correlated with N which captures the market concentration, for example, Herfindahl-Hirschman Index (HHI), in a more general setting. Indeed, in Appendix A, we show that in an extended version of the current model HHI is endogenously and negatively related to . This result justifies the various competition measures we use in our empirical analyses.

2. Data and Summary Statistics

This section describes the data used in the empirical analyses and the construction of product market competition and LM measures, and presents the summary statistics of relevant variables.

2.1 Data and measures of product market competition and LM

In this paper, we resort to a variety of data sources to conduct the empirical analyses. Firms’ monthly stock returns and all accounting information are sourced from the Center for Research in Security Prices (CRSP) and the Compustat Annual Industrial Files, respectively. Our preliminary sample includes all NYSE-, AMEX-, and NASDAQ-listed ordinary common stocks (CRSP share code SHRCD = 10 or 11). We filter the preliminary sample by excluding firms whose four-digit primary standard industrial classification (SIC) code is between 4900 and 4999 (regulated firms) or between 6000 and 6999 (financial firms), and firms with a nonpositive book value of equity. To account for delisting bias, we follow the approach of Shumway (1997) by imputing a return of –30% if the delisting return is missing and the delisting is performance related; however, this adjustment has no material effect on our empirical findings. The data on delisting returns are sourced from the CRSP. Our sample is restricted to the period from January 1990 to December 2016. This is due to the unavailability of data on LM for a longer sample period in the public domain, described below, which are a key ingredient of our analyses.

We focus on two samples constructed from the filtered preliminary sample, namely, the full sample and the all-but-microcaps sample. The full sample includes all NYSE-, AMEX-, and NASDAQ-listed nonfinancial and nonregulated ordinary common stocks for which both nonmissing product market competition and LM estimates in a given year are obtainable. Conversely, the all-but-microcaps sample excludes stocks, from the full sample, with an end-of-June market value of equity below the 20th percentile of the NYSE market capitalization cross-sectional distribution. Excluding microcaps (i.e., very small stocks) helps mitigating their possible undue influence on the empirical results obtained from the full sample. In an average month, the full sample comprises 2,891 firms, whereas 1,233 firms in the all-but-microcaps sample. We employ all accounting variables at the end of June of calendar year t by using accounting information available for the fiscal year ending in the calendar year 1 from the Compustat annual database. This adjustment, suggested in Fama and French (1992), provides time long enough for accounting information to be incorporated into firms’ stock prices.

Consistent with the literature (see, e.g., Giroud and Mueller, 2011; Hoberg and Phillips, 2010; Hou and Robinson, 2006), product market competition (also known as market concentration) for an industry is measured by the HHI.10 Formally, the index is defined as where is the market share of firm i in industry j in year t, is the number of firms operating in industry j in year t, and is the Herfindahl-Hirschman Index of industry j in year t.11 For each industry, we first aggregate the squared market shares of all firms in that industry in a given year t and then average the HHI values over the past 3 years. This adjustment prevents undue influence of potential data errors in the estimation of market concentration. To further improve the accuracy of the product market competition measure, we follow Hou, Xue, and Zhang (2020) and exclude an industry if the market share data are available for fewer than five firms or 80% of all firms in that industry. Throughout the main body of this paper, we compute the HHI using the market shares based on net sales (Compustat item SALE) and denote the resultant measure of product market competition by HSALE.

We also resort to six alternative measures of market competition in order to establish the robustness of the empirical findings. The first of them, denoted by , is measured per Hou and Robinson (2006), where we abstain from excluding an industry for which the market share data are available for fewer than five firms or 80% of all firms in that industry. The second of them, denoted by HAT, is the product market competition measured analogous to HSALE but using total assets (Compustat item AT) instead of net sales (Compustat item SALE). The third of them, denoted by , is obtained from Hoberg and Phillips (2010), which considers both privately held and public firms operating in a given industry by combining Compustat data with Herfindahl data from the U.S. Census Bureau and uses the fitted HHI to capture competitiveness. The fourth of them, denoted by PMF, is obtained from Hoberg, Phillips, and Prabhala (2014), which is a firm-specific competitive pressure measure (also known as firm’s product market fluidity) based on information from product descriptions contained in a firm’s 10-Ks.12 This measure captures changes in rival firms’ products relative to the firm’s products, so a higher value implies greater competitive threats faced by a firm in its product market. The fifth of them, denoted by , is obtained from the U.S. Census of Manufacturers, per Bustamante and Donangelo (2017).13 The last of them, denoted by PCM, is the firm-level price-cost margin as in Peress (2010).14 With the exception of PMF, we multiply the estimates of HSALE, , HAT, , , and PCM by minus one to simplify interpretation of the results. Hence, a higher value of these indexes/measures indicates a higher level of market competition. That is, the product market is shared by many competing firms. All competition measures are estimated and/or employed at the end of June of each year t.

The measure of LM is based on Donangelo (2014), who captures the level of interindustry dispersion of workers across occupations. Specifically, LM is constructed in two stages. In the first stage, the interindustry concentration of workers assigned to each occupation is estimated. This serves as a proxy for (the inverse of) workers’ intrinsic flexibility to switch industries. The second stage involves aggregating the occupation-level concentration measure by industry, weighted by the average annual wage expenditure corresponding to each occupation. Further details of estimating LM are provided in Donangelo (2014) and the standardized data (i.e., demeaned and rescaled to have standard deviation of one in each year) are sourced from Andrés Donangelo’s website.15 Consistent with Donangelo (2014), LM is lagged 18 months in our empirical analyses.

In the portfolio analyses, we utilize six prominent asset pricing models to compute average abnormal returns. These are the (unconditional) capital asset pricing model (CAPM) of Sharpe (1964) and Lintner (1965), the Ferson and Schadt (1996) conditional capital asset pricing (FS) model, the Fama and French (1993) three-factor (FF3) model, the Fama and French (1993) and Carhart (1997) four-factor (FFC) model, the Fama and French (2015) five-factor (FF5) model, and the Hou, Xue, and Zhang (2015)q-factor (HXZ) model. Our motivation for using the FS model is to account for possible time variation in model betas and risk premiums. The time-series data on the pricing factors (i.e., market, size, value, momentum, profitability, and investment) of the CAPM, FF3, FFC, and FF5 models, and monthly risk-free security returns are sourced from the Data Library maintained by Kenneth French.16 The time-series data on the HXZ model factors are sourced from Lu Zhang’s website.17 To compute monthly average abnormal returns on portfolios relative to the FS model, we obtain data of a set of instruments comprising the dividend yield of the Standard and Poor’s 500 Index from Robert Shiller’s website18, and the term spread between 10-year and 3-month Treasury constant-maturity yields, the Treasury-bill rate, and the default spread between BAA and AAA-rated corporate bond yields from Amit Goyal’s website.19 All of these instruments are demeaned before applying them in the time-series regressions for computing average abnormal returns on portfolios.

We use several control variables in our cross-sectional regressions. These variables include firm-level attributes, such as past 1-month return, past 1-year return skipping the last month, book-to-market equity, size, and leverage ratio. Following Fama and French (1992, 1993), we compute the book-to-market ratio, denoted by BM, at the end of June of year t as the ratio of the book value of equity at the end of the fiscal year ending in the calendar year 1 to the market value of equity at the end of December of the calendar year 1.20 In the event of a missing book value of equity, we resort to the Davis, Fama, and French (2000) book value of equity from the Data Library maintained by Kenneth French. The market value of equity, denoted by ME, is computed as absolute price per share times number of equity shares outstanding at the end of June of each year t. We obtain data on stock prices and shares outstanding from the CRSP. As in Bustamante and Donangelo (2017) and Donangelo (2014), the leverage ratio, denoted by LEV, is computed as the ratio of the book value of debt to the book value of assets minus the book value of equity plus the market value of equity at the end of June of year t.

2.2 Summary statistics

The empirical analyses begin by investigating financial and accounting characteristics across LM-sorted portfolios to help understand the data. In doing so, we allocate stocks in the full sample into three portfolios at the end of June of each year t based on the NYSE breakpoints for the bottom 30% (Low), middle 40% (Medium), and top 30% (High) of the ranked values of LM.21 The portfolios are rebalanced annually at the end of June. Panel A of Table 1 reports the time-series averages of the cross-sectional means of characteristics including HSALE, ME, BM, past 1-month return (), past 1-year return () skipping the most recent month’s return, and LEV. We see that the Low LM-sorted portfolio comprises stocks from the least competitive (or, equivalently, the most concentrated) industries, whereas the Medium LM-sorted portfolio comprises stocks from the most competitive (or, equivalently, the least concentrated) industries. Consistent with Donangelo (2014), we also find that the High LM portfolio contains stocks smaller than those comprising the other portfolios. The average market capitalization of such stocks amounts to $2,740.02 million. It is worth mentioning that both HSALE and ME exhibit a nearly inverted U-shaped relation with LM. On the contrary, average BM ratios show a monotonically decreasing relation with LM. That is, stocks in the High LM portfolio tend to be a growth stock, while stocks in the Low LM portfolio tend to be a value stock. Furthermore, past 1-month and 1-year returns increase monotonically with LM, whereas LEV displays a nearly decreasing pattern for LM-sorted portfolios.

Summary statistics

| A. Characteristics of portfolios sorted on LM | ||||||

|---|---|---|---|---|---|---|

| Portfolio | HSALE | ME | BM | LEV | ||

| Low | –0.213 | 2,946.152 | 1.059 | 1.014 | 11.301 | 0.411 |

| Medium | –0.178 | 3,421.161 | 0.746 | 1.225 | 12.150 | 0.313 |

| High | –0.206 | 2,740.021 | 0.739 | 1.411 | 16.102 | 0.320 |

| A. Characteristics of portfolios sorted on LM | ||||||

|---|---|---|---|---|---|---|

| Portfolio | HSALE | ME | BM | LEV | ||

| Low | –0.213 | 2,946.152 | 1.059 | 1.014 | 11.301 | 0.411 |

| Medium | –0.178 | 3,421.161 | 0.746 | 1.225 | 12.150 | 0.313 |

| High | –0.206 | 2,740.021 | 0.739 | 1.411 | 16.102 | 0.320 |

| B. Portfolio excess returns | |||||

|---|---|---|---|---|---|

| Low | Medium | High | H–L | ||

| LM | VW | 0.61 | 0.66 | 0.88 | 0.27 |

| (1.77) | (2.28) | (3.02) | (1.59) | ||

| EW | 0.73 | 0.95 | 1.14 | 0.41 | |

| (1.75) | (2.20) | (2.71) | (2.33) | ||

| B. Portfolio excess returns | |||||

|---|---|---|---|---|---|

| Low | Medium | High | H–L | ||

| LM | VW | 0.61 | 0.66 | 0.88 | 0.27 |

| (1.77) | (2.28) | (3.02) | (1.59) | ||

| EW | 0.73 | 0.95 | 1.14 | 0.41 | |

| (1.75) | (2.20) | (2.71) | (2.33) | ||

| C. Excess returns of quintile portfolios | |||||||

|---|---|---|---|---|---|---|---|

| Low | 2 | 3 | 4 | High | H–L | ||

| LM | VW | 0.73 | 0.54 | 0.66 | 0.68 | 1.00 | 0.27 |

| (2.01) | (1.55) | (2.19) | (2.56) | (3.46) | (1.60) | ||

| EW | 0.72 | 0.68 | 1.11 | 0.92 | 1.19 | 0.47 | |

| (1.74) | (1.58) | (2.53) | (2.28) | (2.73) | (2.37) | ||

| C. Excess returns of quintile portfolios | |||||||

|---|---|---|---|---|---|---|---|

| Low | 2 | 3 | 4 | High | H–L | ||

| LM | VW | 0.73 | 0.54 | 0.66 | 0.68 | 1.00 | 0.27 |

| (2.01) | (1.55) | (2.19) | (2.56) | (3.46) | (1.60) | ||

| EW | 0.72 | 0.68 | 1.11 | 0.92 | 1.19 | 0.47 | |

| (1.74) | (1.58) | (2.53) | (2.28) | (2.73) | (2.37) | ||

The sample includes all NYSE-, AMEX-, and NASDAQ-listed nonfinancial and nonregulated ordinary common stocks for which both nonmissing product market competition and labor mobility estimates in a given year t are available. There are 2,891 firms in an average month. HSALE is the product market competition measured by the Herfindahl-Hirschman Index (HHI), where for each industry, we first aggregate the squared net sales-based market shares of all firms in that industry in a given year and then average the HHI values over the past 3 years. We multiply HSALE by minus one so that a higher value indicates a higher level of product market competition. LM is the measure of labor mobility, which is computed in two stages, first at the occupation-level and then at the industry level. ME is the market value of equity (in million $) which is computed as the number of shares outstanding times the absolute price of one share at the end of June of each year . BM is the book-to-market ratio, which is computed in June of each year as the ratio of the book value of equity at the end of the fiscal year ending in the calendar year 1 to the market value of equity at the end of December of the calendar year 1. is the past 1-month return (in %). is the past 1-year return (in %) skipping the most recent month. LEV is the leverage ratio calculated as the ratio of the book value of debt to the book value of assets minus the book value of equity plus the market value of equity at the end of June of year t. At the end of June of each year t, stocks are sorted into three portfolios based on the NYSE breakpoints for the bottom 30% (Low), middle 40% (Medium), and top 30% (High) of the ranked values of LM, which is lagged 18 months, at the end of June of year t. Panel A reports the time-series averages of the cross-sectional mean characteristics of the portfolios of firms sorted by LM. Panel B (panel C) reports both the value-weighted (VW) and the equal-weighted (EW) average monthly excess returns (in %) for portfolios (quintile portfolios) sorted on LM. All portfolios are rebalanced annually at the end of June. H–L denotes the high-minus-low portfolio, that is, long stocks in the High portfolio and short stocks in the Low portfolio. Numbers in parentheses are t-statistics adjusted following Newey and West (1987). The sample period is from January 1990 to December 2016.

Summary statistics

| A. Characteristics of portfolios sorted on LM | ||||||

|---|---|---|---|---|---|---|

| Portfolio | HSALE | ME | BM | LEV | ||

| Low | –0.213 | 2,946.152 | 1.059 | 1.014 | 11.301 | 0.411 |

| Medium | –0.178 | 3,421.161 | 0.746 | 1.225 | 12.150 | 0.313 |

| High | –0.206 | 2,740.021 | 0.739 | 1.411 | 16.102 | 0.320 |

| A. Characteristics of portfolios sorted on LM | ||||||

|---|---|---|---|---|---|---|

| Portfolio | HSALE | ME | BM | LEV | ||

| Low | –0.213 | 2,946.152 | 1.059 | 1.014 | 11.301 | 0.411 |

| Medium | –0.178 | 3,421.161 | 0.746 | 1.225 | 12.150 | 0.313 |

| High | –0.206 | 2,740.021 | 0.739 | 1.411 | 16.102 | 0.320 |

| B. Portfolio excess returns | |||||

|---|---|---|---|---|---|

| Low | Medium | High | H–L | ||

| LM | VW | 0.61 | 0.66 | 0.88 | 0.27 |

| (1.77) | (2.28) | (3.02) | (1.59) | ||

| EW | 0.73 | 0.95 | 1.14 | 0.41 | |

| (1.75) | (2.20) | (2.71) | (2.33) | ||

| B. Portfolio excess returns | |||||

|---|---|---|---|---|---|

| Low | Medium | High | H–L | ||

| LM | VW | 0.61 | 0.66 | 0.88 | 0.27 |

| (1.77) | (2.28) | (3.02) | (1.59) | ||

| EW | 0.73 | 0.95 | 1.14 | 0.41 | |

| (1.75) | (2.20) | (2.71) | (2.33) | ||

| C. Excess returns of quintile portfolios | |||||||

|---|---|---|---|---|---|---|---|

| Low | 2 | 3 | 4 | High | H–L | ||

| LM | VW | 0.73 | 0.54 | 0.66 | 0.68 | 1.00 | 0.27 |

| (2.01) | (1.55) | (2.19) | (2.56) | (3.46) | (1.60) | ||

| EW | 0.72 | 0.68 | 1.11 | 0.92 | 1.19 | 0.47 | |

| (1.74) | (1.58) | (2.53) | (2.28) | (2.73) | (2.37) | ||

| C. Excess returns of quintile portfolios | |||||||

|---|---|---|---|---|---|---|---|

| Low | 2 | 3 | 4 | High | H–L | ||

| LM | VW | 0.73 | 0.54 | 0.66 | 0.68 | 1.00 | 0.27 |

| (2.01) | (1.55) | (2.19) | (2.56) | (3.46) | (1.60) | ||

| EW | 0.72 | 0.68 | 1.11 | 0.92 | 1.19 | 0.47 | |

| (1.74) | (1.58) | (2.53) | (2.28) | (2.73) | (2.37) | ||

The sample includes all NYSE-, AMEX-, and NASDAQ-listed nonfinancial and nonregulated ordinary common stocks for which both nonmissing product market competition and labor mobility estimates in a given year t are available. There are 2,891 firms in an average month. HSALE is the product market competition measured by the Herfindahl-Hirschman Index (HHI), where for each industry, we first aggregate the squared net sales-based market shares of all firms in that industry in a given year and then average the HHI values over the past 3 years. We multiply HSALE by minus one so that a higher value indicates a higher level of product market competition. LM is the measure of labor mobility, which is computed in two stages, first at the occupation-level and then at the industry level. ME is the market value of equity (in million $) which is computed as the number of shares outstanding times the absolute price of one share at the end of June of each year . BM is the book-to-market ratio, which is computed in June of each year as the ratio of the book value of equity at the end of the fiscal year ending in the calendar year 1 to the market value of equity at the end of December of the calendar year 1. is the past 1-month return (in %). is the past 1-year return (in %) skipping the most recent month. LEV is the leverage ratio calculated as the ratio of the book value of debt to the book value of assets minus the book value of equity plus the market value of equity at the end of June of year t. At the end of June of each year t, stocks are sorted into three portfolios based on the NYSE breakpoints for the bottom 30% (Low), middle 40% (Medium), and top 30% (High) of the ranked values of LM, which is lagged 18 months, at the end of June of year t. Panel A reports the time-series averages of the cross-sectional mean characteristics of the portfolios of firms sorted by LM. Panel B (panel C) reports both the value-weighted (VW) and the equal-weighted (EW) average monthly excess returns (in %) for portfolios (quintile portfolios) sorted on LM. All portfolios are rebalanced annually at the end of June. H–L denotes the high-minus-low portfolio, that is, long stocks in the High portfolio and short stocks in the Low portfolio. Numbers in parentheses are t-statistics adjusted following Newey and West (1987). The sample period is from January 1990 to December 2016.

We then proceed to examine whether one-way sorting on LM alone generates a pattern in average excess returns over the risk-free rate. Panel B of Table 1 reports the results from such an investigation where we construct three portfolios based on the NYSE breakpoints set to the bottom 30%, middle 40%, and top 30% of the ranked values of LM at the end of June of each year t. We find that the value-weighted (equal-weighted) average monthly excess portfolio returns increase monotonically, from 0.61% (0.73%) for the Low LM portfolio to 0.88% (1.14%) for the High LM portfolio. The value-weighted (equal-weighted) average return of 0.27% (0.41%) per month for the high-minus-low LM is statistically indistinguishable (distinguishable) from zero, with a t-statistic of 1.59 (2.33). Although the value-weighted average monthly return on the high-minus-low portfolio appears to be statistically insignificant at conventional levels, the portfolio generates an economically large and statistically significant average return of 0.83% (t-statistic = 3.05) per month for stocks in competitive industries (see Table 3).

Double sorts on product market competition and labor mobility

| Low competition | High competition | |||||||

|---|---|---|---|---|---|---|---|---|

| H–L | H–L | |||||||

A. Full sample | ||||||||

| Excess return | 0.95 | 0.76 | 0.80 | –0.15 | 0.19 | 0.77 | 1.02 | 0.83 |

| (3.15) | (2.66) | (3.10) | (–0.91) | (0.50) | (2.34) | (3.02) | (3.05) | |

| Char-adj return | 0.06 | –0.21 | –0.17 | –0.23 | –0.68 | –0.12 | 0.11 | 0.79 |

| (0.38) | (–2.18) | (–1.53) | (–1.30) | (–3.97) | (–1.02) | (0.96) | (3.76) | |

| CAPM | 0.33 | 0.14 | 0.24 | –0.09 | –0.54 | 0.06 | 0.28 | 0.82 |

| (2.10) | (1.12) | (2.20) | (–0.58) | (–2.35) | (0.27) | (1.66) | (3.07) | |

| FS | 0.29 | 0.13 | 0.14 | –0.14 | –0.54 | 0.18 | 0.30 | 0.84 |

| (2.01) | (0.97) | (1.29) | (–0.87) | (–2.32) | (1.05) | (1.85) | (2.96) | |

| FF3 | 0.22 | 0.09 | 0.20 | –0.02 | –0.54 | 0.26 | 0.38 | 0.92 |

| (1.67) | (0.77) | (1.91) | (–0.12) | (–2.18) | (1.76) | (2.47) | (3.23) | |

| FFC | 0.27 | 0.15 | 0.25 | –0.02 | –0.36 | 0.44 | 0.33 | 0.69 |

| (1.91) | (1.20) | (2.53) | (–0.13) | (–1.48) | (2.31) | (2.07) | (2.44) | |

| FF5 | 0.05 | 0.00 | 0.03 | –0.02 | –0.46 | 0.43 | 0.37 | 0.83 |

| (0.37) | (0.00) | (0.25) | (–0.14) | (–1.79) | (2.25) | (2.15) | (2.53) | |

| HXZ | 0.17 | 0.07 | 0.09 | –0.08 | –0.30 | 0.58 | 0.39 | 0.69 |

| (1.08) | (0.50) | (0.81) | (–0.42) | (–1.00) | (2.88) | (1.99) | (2.08) | |

B. All-but-microcaps sample | ||||||||

| Excess return | 0.77 | 0.87 | 0.93 | 0.16 | 0.49 | 0.93 | 1.33 | 0.84 |

| (2.21) | (2.86) | (2.74) | (1.31) | (1.07) | (2.19) | (3.33) | (2.60) | |

| Char-adj return | –0.29 | –0.27 | –0.16 | 0.13 | –0.54 | –0.07 | 0.26 | 0.79 |

| (–2.84) | (–2.45) | (–1.80) | (1.08) | (–3.25) | (–0.49) | (1.67) | (3.11) | |

| CAPM | 0.03 | 0.17 | 0.17 | 0.14 | –0.47 | 0.03 | 0.45 | 0.93 |

| (0.14) | (0.92) | (1.17) | (1.18) | (–2.17) | (0.12) | (1.77) | (3.06) | |

| FS | 0.04 | 0.12 | 0.15 | 0.11 | –0.28 | 0.21 | 0.51 | 0.79 |

| (0.23) | (0.61) | (0.97) | (0.90) | (–1.12) | (0.86) | (1.80) | (2.23) | |

| FF3 | –0.15 | 0.01 | 0.03 | 0.18 | –0.46 | 0.15 | 0.53 | 0.99 |

| (–1.06) | (0.07) | (0.28) | (1.57) | (–2.17) | (0.88) | (3.16) | (3.35) | |

| FFC | 0.10 | 0.19 | 0.22 | 0.12 | –0.15 | 0.37 | 0.49 | 0.64 |

| (0.78) | (1.33) | (2.15) | (0.96) | (–0.65) | (1.86) | (3.01) | (2.17) | |

| FF5 | –0.22 | –0.15 | –0.03 | 0.19 | –0.33 | 0.50 | 0.62 | 0.95 |

| (–1.37) | (–0.95) | (–0.22) | (1.46) | (–1.18) | (2.45) | (3.78) | (2.68) | |

| HXZ | 0.03 | 0.05 | 0.11 | 0.08 | –0.03 | 0.64 | 0.68 | 0.70 |

| (0.13) | (0.24) | (0.73) | (0.56) | (–0.09) | (3.25) | (3.05) | (2.07) | |

| Low competition | High competition | |||||||

|---|---|---|---|---|---|---|---|---|

| H–L | H–L | |||||||

A. Full sample | ||||||||

| Excess return | 0.95 | 0.76 | 0.80 | –0.15 | 0.19 | 0.77 | 1.02 | 0.83 |

| (3.15) | (2.66) | (3.10) | (–0.91) | (0.50) | (2.34) | (3.02) | (3.05) | |

| Char-adj return | 0.06 | –0.21 | –0.17 | –0.23 | –0.68 | –0.12 | 0.11 | 0.79 |

| (0.38) | (–2.18) | (–1.53) | (–1.30) | (–3.97) | (–1.02) | (0.96) | (3.76) | |

| CAPM | 0.33 | 0.14 | 0.24 | –0.09 | –0.54 | 0.06 | 0.28 | 0.82 |

| (2.10) | (1.12) | (2.20) | (–0.58) | (–2.35) | (0.27) | (1.66) | (3.07) | |

| FS | 0.29 | 0.13 | 0.14 | –0.14 | –0.54 | 0.18 | 0.30 | 0.84 |

| (2.01) | (0.97) | (1.29) | (–0.87) | (–2.32) | (1.05) | (1.85) | (2.96) | |

| FF3 | 0.22 | 0.09 | 0.20 | –0.02 | –0.54 | 0.26 | 0.38 | 0.92 |

| (1.67) | (0.77) | (1.91) | (–0.12) | (–2.18) | (1.76) | (2.47) | (3.23) | |

| FFC | 0.27 | 0.15 | 0.25 | –0.02 | –0.36 | 0.44 | 0.33 | 0.69 |

| (1.91) | (1.20) | (2.53) | (–0.13) | (–1.48) | (2.31) | (2.07) | (2.44) | |

| FF5 | 0.05 | 0.00 | 0.03 | –0.02 | –0.46 | 0.43 | 0.37 | 0.83 |

| (0.37) | (0.00) | (0.25) | (–0.14) | (–1.79) | (2.25) | (2.15) | (2.53) | |

| HXZ | 0.17 | 0.07 | 0.09 | –0.08 | –0.30 | 0.58 | 0.39 | 0.69 |

| (1.08) | (0.50) | (0.81) | (–0.42) | (–1.00) | (2.88) | (1.99) | (2.08) | |

B. All-but-microcaps sample | ||||||||

| Excess return | 0.77 | 0.87 | 0.93 | 0.16 | 0.49 | 0.93 | 1.33 | 0.84 |

| (2.21) | (2.86) | (2.74) | (1.31) | (1.07) | (2.19) | (3.33) | (2.60) | |

| Char-adj return | –0.29 | –0.27 | –0.16 | 0.13 | –0.54 | –0.07 | 0.26 | 0.79 |

| (–2.84) | (–2.45) | (–1.80) | (1.08) | (–3.25) | (–0.49) | (1.67) | (3.11) | |

| CAPM | 0.03 | 0.17 | 0.17 | 0.14 | –0.47 | 0.03 | 0.45 | 0.93 |

| (0.14) | (0.92) | (1.17) | (1.18) | (–2.17) | (0.12) | (1.77) | (3.06) | |

| FS | 0.04 | 0.12 | 0.15 | 0.11 | –0.28 | 0.21 | 0.51 | 0.79 |

| (0.23) | (0.61) | (0.97) | (0.90) | (–1.12) | (0.86) | (1.80) | (2.23) | |

| FF3 | –0.15 | 0.01 | 0.03 | 0.18 | –0.46 | 0.15 | 0.53 | 0.99 |

| (–1.06) | (0.07) | (0.28) | (1.57) | (–2.17) | (0.88) | (3.16) | (3.35) | |

| FFC | 0.10 | 0.19 | 0.22 | 0.12 | –0.15 | 0.37 | 0.49 | 0.64 |

| (0.78) | (1.33) | (2.15) | (0.96) | (–0.65) | (1.86) | (3.01) | (2.17) | |

| FF5 | –0.22 | –0.15 | –0.03 | 0.19 | –0.33 | 0.50 | 0.62 | 0.95 |

| (–1.37) | (–0.95) | (–0.22) | (1.46) | (–1.18) | (2.45) | (3.78) | (2.68) | |

| HXZ | 0.03 | 0.05 | 0.11 | 0.08 | –0.03 | 0.64 | 0.68 | 0.70 |

| (0.13) | (0.24) | (0.73) | (0.56) | (–0.09) | (3.25) | (3.05) | (2.07) | |

The table reports monthly returns of portfolios sorted on product market competition and labor mobility, LM. At the end of June of each year t, stocks are sorted into three groups based on the NYSE breakpoints for the bottom 30% (Low (L)), middle 40% (Medium (M)), and top 30% (High (H)) of the ranked values of product market competition at the end of June of year t. Product market competition for an industry is measured using net sales-based market shares of all firms in that industry. Independently, stocks are sorted into three groups based on the NYSE breakpoints for the bottom 30% (L), middle 40% (M), and top 30% (H) of the ranked values of labor mobility, which is lagged 18 months, at the end of June of year t. The intersections of the product market competition and labor mobility groups result in nine portfolios. All portfolios are rebalanced annually at the end of June. The full sample includes all NYSE-, AMEX-, and NASDAQ-listed nonfinancial and nonregulated ordinary common stocks for which both nonmissing product market competition and labor mobility estimates in a given year t are available. The all-but-microcaps sample excludes stocks, from the full sample, with an end-of-June market value of equity below the 20th percentile of the NYSE market capitalization distribution and the remaining stocks are used to compute the breakpoints for product market competition and labor mobility separately. Panel A (panel B) reports the value-weighted (equal-weighted) average monthly returns (in %) on portfolios. Excess return is the portfolio return in excess of the 1-month Treasury-bill rate. Characteristic-adjusted (Char-adj) returns are computed by adjusting returns using 125 () size/book-to-market/momentum benchmark portfolios (as in Daniel et al., 1997). The alphas (in %) are estimated from the time-series regressions of portfolio excess returns on various factor models including the capital asset pricing model (CAPM) of Sharpe (1964) and Lintner (1965), the Ferson and Schadt (1996) conditional capital asset pricing (FS) model, the Fama and French (1993) three-factor (FF3) model, the Fama and French (1993) and Carhart (1997) four-factor (FFC) model, the Fama and French (2015) five-factor (FF5) model, and the Hou, Xue, and Zhang (2015),q-factor (HXZ) model. H–L is the high-minus-low portfolio. Numbers in parentheses are t-statistics adjusted following Newey and West (1987). The sample period is from January 1990 to December 2016. See also the legend to Table 1.

Double sorts on product market competition and labor mobility

| Low competition | High competition | |||||||

|---|---|---|---|---|---|---|---|---|

| H–L | H–L | |||||||

A. Full sample | ||||||||

| Excess return | 0.95 | 0.76 | 0.80 | –0.15 | 0.19 | 0.77 | 1.02 | 0.83 |

| (3.15) | (2.66) | (3.10) | (–0.91) | (0.50) | (2.34) | (3.02) | (3.05) | |

| Char-adj return | 0.06 | –0.21 | –0.17 | –0.23 | –0.68 | –0.12 | 0.11 | 0.79 |

| (0.38) | (–2.18) | (–1.53) | (–1.30) | (–3.97) | (–1.02) | (0.96) | (3.76) | |

| CAPM | 0.33 | 0.14 | 0.24 | –0.09 | –0.54 | 0.06 | 0.28 | 0.82 |

| (2.10) | (1.12) | (2.20) | (–0.58) | (–2.35) | (0.27) | (1.66) | (3.07) | |

| FS | 0.29 | 0.13 | 0.14 | –0.14 | –0.54 | 0.18 | 0.30 | 0.84 |

| (2.01) | (0.97) | (1.29) | (–0.87) | (–2.32) | (1.05) | (1.85) | (2.96) | |

| FF3 | 0.22 | 0.09 | 0.20 | –0.02 | –0.54 | 0.26 | 0.38 | 0.92 |

| (1.67) | (0.77) | (1.91) | (–0.12) | (–2.18) | (1.76) | (2.47) | (3.23) | |

| FFC | 0.27 | 0.15 | 0.25 | –0.02 | –0.36 | 0.44 | 0.33 | 0.69 |

| (1.91) | (1.20) | (2.53) | (–0.13) | (–1.48) | (2.31) | (2.07) | (2.44) | |

| FF5 | 0.05 | 0.00 | 0.03 | –0.02 | –0.46 | 0.43 | 0.37 | 0.83 |

| (0.37) | (0.00) | (0.25) | (–0.14) | (–1.79) | (2.25) | (2.15) | (2.53) | |

| HXZ | 0.17 | 0.07 | 0.09 | –0.08 | –0.30 | 0.58 | 0.39 | 0.69 |

| (1.08) | (0.50) | (0.81) | (–0.42) | (–1.00) | (2.88) | (1.99) | (2.08) | |

B. All-but-microcaps sample | ||||||||

| Excess return | 0.77 | 0.87 | 0.93 | 0.16 | 0.49 | 0.93 | 1.33 | 0.84 |

| (2.21) | (2.86) | (2.74) | (1.31) | (1.07) | (2.19) | (3.33) | (2.60) | |

| Char-adj return | –0.29 | –0.27 | –0.16 | 0.13 | –0.54 | –0.07 | 0.26 | 0.79 |

| (–2.84) | (–2.45) | (–1.80) | (1.08) | (–3.25) | (–0.49) | (1.67) | (3.11) | |

| CAPM | 0.03 | 0.17 | 0.17 | 0.14 | –0.47 | 0.03 | 0.45 | 0.93 |

| (0.14) | (0.92) | (1.17) | (1.18) | (–2.17) | (0.12) | (1.77) | (3.06) | |

| FS | 0.04 | 0.12 | 0.15 | 0.11 | –0.28 | 0.21 | 0.51 | 0.79 |

| (0.23) | (0.61) | (0.97) | (0.90) | (–1.12) | (0.86) | (1.80) | (2.23) | |

| FF3 | –0.15 | 0.01 | 0.03 | 0.18 | –0.46 | 0.15 | 0.53 | 0.99 |

| (–1.06) | (0.07) | (0.28) | (1.57) | (–2.17) | (0.88) | (3.16) | (3.35) | |

| FFC | 0.10 | 0.19 | 0.22 | 0.12 | –0.15 | 0.37 | 0.49 | 0.64 |

| (0.78) | (1.33) | (2.15) | (0.96) | (–0.65) | (1.86) | (3.01) | (2.17) | |

| FF5 | –0.22 | –0.15 | –0.03 | 0.19 | –0.33 | 0.50 | 0.62 | 0.95 |

| (–1.37) | (–0.95) | (–0.22) | (1.46) | (–1.18) | (2.45) | (3.78) | (2.68) | |

| HXZ | 0.03 | 0.05 | 0.11 | 0.08 | –0.03 | 0.64 | 0.68 | 0.70 |

| (0.13) | (0.24) | (0.73) | (0.56) | (–0.09) | (3.25) | (3.05) | (2.07) | |

| Low competition | High competition | |||||||

|---|---|---|---|---|---|---|---|---|

| H–L | H–L | |||||||

A. Full sample | ||||||||

| Excess return | 0.95 | 0.76 | 0.80 | –0.15 | 0.19 | 0.77 | 1.02 | 0.83 |

| (3.15) | (2.66) | (3.10) | (–0.91) | (0.50) | (2.34) | (3.02) | (3.05) | |

| Char-adj return | 0.06 | –0.21 | –0.17 | –0.23 | –0.68 | –0.12 | 0.11 | 0.79 |

| (0.38) | (–2.18) | (–1.53) | (–1.30) | (–3.97) | (–1.02) | (0.96) | (3.76) | |

| CAPM | 0.33 | 0.14 | 0.24 | –0.09 | –0.54 | 0.06 | 0.28 | 0.82 |

| (2.10) | (1.12) | (2.20) | (–0.58) | (–2.35) | (0.27) | (1.66) | (3.07) | |

| FS | 0.29 | 0.13 | 0.14 | –0.14 | –0.54 | 0.18 | 0.30 | 0.84 |

| (2.01) | (0.97) | (1.29) | (–0.87) | (–2.32) | (1.05) | (1.85) | (2.96) | |

| FF3 | 0.22 | 0.09 | 0.20 | –0.02 | –0.54 | 0.26 | 0.38 | 0.92 |

| (1.67) | (0.77) | (1.91) | (–0.12) | (–2.18) | (1.76) | (2.47) | (3.23) | |

| FFC | 0.27 | 0.15 | 0.25 | –0.02 | –0.36 | 0.44 | 0.33 | 0.69 |

| (1.91) | (1.20) | (2.53) | (–0.13) | (–1.48) | (2.31) | (2.07) | (2.44) | |

| FF5 | 0.05 | 0.00 | 0.03 | –0.02 | –0.46 | 0.43 | 0.37 | 0.83 |

| (0.37) | (0.00) | (0.25) | (–0.14) | (–1.79) | (2.25) | (2.15) | (2.53) | |

| HXZ | 0.17 | 0.07 | 0.09 | –0.08 | –0.30 | 0.58 | 0.39 | 0.69 |

| (1.08) | (0.50) | (0.81) | (–0.42) | (–1.00) | (2.88) | (1.99) | (2.08) | |

B. All-but-microcaps sample | ||||||||

| Excess return | 0.77 | 0.87 | 0.93 | 0.16 | 0.49 | 0.93 | 1.33 | 0.84 |

| (2.21) | (2.86) | (2.74) | (1.31) | (1.07) | (2.19) | (3.33) | (2.60) | |

| Char-adj return | –0.29 | –0.27 | –0.16 | 0.13 | –0.54 | –0.07 | 0.26 | 0.79 |

| (–2.84) | (–2.45) | (–1.80) | (1.08) | (–3.25) | (–0.49) | (1.67) | (3.11) | |

| CAPM | 0.03 | 0.17 | 0.17 | 0.14 | –0.47 | 0.03 | 0.45 | 0.93 |

| (0.14) | (0.92) | (1.17) | (1.18) | (–2.17) | (0.12) | (1.77) | (3.06) | |

| FS | 0.04 | 0.12 | 0.15 | 0.11 | –0.28 | 0.21 | 0.51 | 0.79 |

| (0.23) | (0.61) | (0.97) | (0.90) | (–1.12) | (0.86) | (1.80) | (2.23) | |

| FF3 | –0.15 | 0.01 | 0.03 | 0.18 | –0.46 | 0.15 | 0.53 | 0.99 |

| (–1.06) | (0.07) | (0.28) | (1.57) | (–2.17) | (0.88) | (3.16) | (3.35) | |

| FFC | 0.10 | 0.19 | 0.22 | 0.12 | –0.15 | 0.37 | 0.49 | 0.64 |

| (0.78) | (1.33) | (2.15) | (0.96) | (–0.65) | (1.86) | (3.01) | (2.17) | |

| FF5 | –0.22 | –0.15 | –0.03 | 0.19 | –0.33 | 0.50 | 0.62 | 0.95 |

| (–1.37) | (–0.95) | (–0.22) | (1.46) | (–1.18) | (2.45) | (3.78) | (2.68) | |

| HXZ | 0.03 | 0.05 | 0.11 | 0.08 | –0.03 | 0.64 | 0.68 | 0.70 |

| (0.13) | (0.24) | (0.73) | (0.56) | (–0.09) | (3.25) | (3.05) | (2.07) | |

The table reports monthly returns of portfolios sorted on product market competition and labor mobility, LM. At the end of June of each year t, stocks are sorted into three groups based on the NYSE breakpoints for the bottom 30% (Low (L)), middle 40% (Medium (M)), and top 30% (High (H)) of the ranked values of product market competition at the end of June of year t. Product market competition for an industry is measured using net sales-based market shares of all firms in that industry. Independently, stocks are sorted into three groups based on the NYSE breakpoints for the bottom 30% (L), middle 40% (M), and top 30% (H) of the ranked values of labor mobility, which is lagged 18 months, at the end of June of year t. The intersections of the product market competition and labor mobility groups result in nine portfolios. All portfolios are rebalanced annually at the end of June. The full sample includes all NYSE-, AMEX-, and NASDAQ-listed nonfinancial and nonregulated ordinary common stocks for which both nonmissing product market competition and labor mobility estimates in a given year t are available. The all-but-microcaps sample excludes stocks, from the full sample, with an end-of-June market value of equity below the 20th percentile of the NYSE market capitalization distribution and the remaining stocks are used to compute the breakpoints for product market competition and labor mobility separately. Panel A (panel B) reports the value-weighted (equal-weighted) average monthly returns (in %) on portfolios. Excess return is the portfolio return in excess of the 1-month Treasury-bill rate. Characteristic-adjusted (Char-adj) returns are computed by adjusting returns using 125 () size/book-to-market/momentum benchmark portfolios (as in Daniel et al., 1997). The alphas (in %) are estimated from the time-series regressions of portfolio excess returns on various factor models including the capital asset pricing model (CAPM) of Sharpe (1964) and Lintner (1965), the Ferson and Schadt (1996) conditional capital asset pricing (FS) model, the Fama and French (1993) three-factor (FF3) model, the Fama and French (1993) and Carhart (1997) four-factor (FFC) model, the Fama and French (2015) five-factor (FF5) model, and the Hou, Xue, and Zhang (2015),q-factor (HXZ) model. H–L is the high-minus-low portfolio. Numbers in parentheses are t-statistics adjusted following Newey and West (1987). The sample period is from January 1990 to December 2016. See also the legend to Table 1.

Panel C of Table 1 presents the results from the univariate portfolio analyses where stocks are sorted into quintile portfolios. By construction, the Low LM portfolio contains stocks below the 20th percentile of the NYSE cross-sectional distribution of LM, while the High LM portfolio contains stocks above the 80th percentile of the NYSE cross-sectional distribution of LM. We see that both the value-weighted and the equal-weighted average excess returns on portfolios generate neither a monotonically increasing nor a monotonically decreasing pattern. The high-minus-low LM portfolio delivers a value-weighted average return of 0.27% per month (t-statistic = 1.60).22 The corresponding equal-weighted average return amounts to 0.47% per month (t-statistic = 2.37). Note that the high-minus-low portfolio generates a value-weighted average return of 0.90% per month (t-statistic = 2.90) for stocks in competitive industries (see Table IA5).

3. Empirical Results

This section tests our theoretical model, which predicts that the positive LM-return relation is stronger for firms in competitive industries.23 We follow two complementary methodologies: an independent double-sorted portfolio approach and a cross-sectional regression approach.

3.1 Portfolio-level analysis

At the end of June of each year t, we assign stocks to three groups using the breakpoints for the bottom 30% (Low), middle 40% (Medium), and top 30% (High) of the ranked values of HSALE in end-of-June. Independently, we also divide stocks into three groups according to the breakpoints for the bottom 30% (Low), middle 40% (Medium), and top 30% (High) of the ranked values of LM, which is lagged 18 months, at the end of June of year t. The intersections of the three market competition and three LM groups result in nine portfolios, which are rebalanced annually at the end of June.24 Consequently, the transaction costs associated with implementing the trading strategy are expected to be low. Standard in the empirical asset pricing literature, we then obtain the value-weighted average excess returns for portfolios based on the full sample, while the equal-weighted average excess returns for portfolios based on the all-but-microcaps sample. These average excess returns allow us to provide a comprehensive picture of the relation between LM and future stock returns for firms in concentrated and competitive industries. To ensure that our results from both the full sample and the all-but-microcaps sample are robust to firm characteristics, we further compute characteristic-adjusted returns of portfolios. Specifically, following the exact procedure in Daniel et al. (1997), characteristic-adjusted returns are computed as the difference between individual stocks’ returns and 125 () size/book-to-market/momentum benchmark portfolio returns.

Table 2 summarizes the time-series averages of the cross-sectional mean characteristics of the independent double-sorted portfolios. The first two rows in panels A and B show the sorting variables LM and HSALE. As expected, LM increases monotonically when moving from the Low LM portfolio, denoted by , to the High LM portfolio, denoted by , and this pattern is similar for both the Low competition and the High competition industries. It is also observable that firms in the High competition industries tend to have lower ME, lower BM, higher past returns, and lower LEV than firms in the Low competition industries. We report the main results from the bivariate independent-sort portfolio analyses in Table 3. In panel A, which makes use of the full sample and the NYSE breakpoints to sort variables, we find that the value-weighted average monthly excess returns of LM-sorted portfolios in the High competition industries increase monotonically when moving from the Low LM portfolio, , to the High LM portfolio, . Importantly, the high-minus-low LM portfolio generates an economically large value-weighted average monthly return of 0.83%, which is highly statistically significant, with a Newey and West (1987)-adjusted t-statistic of 3.05. A monotonically increasing pattern also can be seen for the characteristic-adjusted returns when moving from the Low LM portfolio, , to the High LM portfolio, . The value-weighted characteristic-adjusted return of the high-minus-low LM portfolio is 0.79% per month, with a corresponding t-statistic of 3.76. The monthly average abnormal returns on this spread portfolio relative to the CAPM, FS, FF3, FFC, FF5, and HXZ models are also economically large and statistically distinguishable from zero; they are 0.82% (t-statistic = 3.07), 0.84% (t-statistic = 2.96), 0.92% (t-statistic = 3.23), 0.69% (t-statistic = 2.44), 0.83% (t-statistic = 2.53), and 0.69% (t-statistic = 2.08), respectively. Note that the economic magnitude of the conditional alpha (i.e., the FS model alpha) is similar to unconditional ones (i.e., the FF3, FFC, FF5, and HXZ model alphas). This suggests somewhat of a negligible time variation in the pricing model betas.

Characteristics of portfolios double-sorted on product market competition

| Low competition | High competition | |||||||

|---|---|---|---|---|---|---|---|---|

| H–L | H–L | |||||||

A. Full sample | ||||||||

| LM | –0.92 | 0.15 | 1.25 | 2.17 | –0.93 | 0.17 | 1.13 | 2.07 |

| HSALE | –0.40 | –0.40 | –0.41 | 0.00 | –0.10 | –0.09 | –0.08 | 0.02 |

| ME | 3,577.30 | 2959.38 | 3284.64 | –292.66 | 2,983.62 | 2,941.98 | 2,238.16 | –745.46 |

| BM | 0.82 | 0.91 | 0.78 | –0.04 | 0.86 | 0.61 | 0.69 | –0.17 |

| 1.01 | 0.99 | 1.14 | 0.13 | 0.81 | 1.35 | 1.53 | 0.72 | |

| 11.72 | 11.93 | 13.89 | 2.17 | 9.71 | 14.90 | 17.70 | 7.99 | |

| LEV | 0.38 | 0.39 | 0.37 | –0.01 | 0.37 | 0.23 | 0.26 | –0.10 |

B. All-but-microcaps sample | ||||||||

| LM | –0.86 | 0.29 | 1.24 | 2.10 | –0.74 | 0.23 | 1.06 | 1.80 |

| HSALE | –0.36 | –0.35 | –0.36 | 0.00 | –0.08 | –0.09 | –0.07 | 0.01 |

| ME | 6,299.22 | 6,491.35 | 6,374.82 | 75.60 | 4,864.52 | 7,285.73 | 6,202.86 | 1,338.34 |

| BM | 0.61 | 0.55 | 0.49 | –0.12 | 0.51 | 0.36 | 0.34 | –0.17 |

| 0.96 | 1.08 | 1.18 | 0.22 | 0.78 | 1.25 | 1.65 | 0.87 | |

| 11.13 | 12.40 | 13.37 | 2.24 | 8.69 | 15.09 | 19.29 | 10.61 | |

| LEV | 0.36 | 0.35 | 0.33 | –0.04 | 0.27 | 0.19 | 0.18 | –0.09 |

| Low competition | High competition | |||||||

|---|---|---|---|---|---|---|---|---|

| H–L | H–L | |||||||

A. Full sample | ||||||||

| LM | –0.92 | 0.15 | 1.25 | 2.17 | –0.93 | 0.17 | 1.13 | 2.07 |

| HSALE | –0.40 | –0.40 | –0.41 | 0.00 | –0.10 | –0.09 | –0.08 | 0.02 |

| ME | 3,577.30 | 2959.38 | 3284.64 | –292.66 | 2,983.62 | 2,941.98 | 2,238.16 | –745.46 |

| BM | 0.82 | 0.91 | 0.78 | –0.04 | 0.86 | 0.61 | 0.69 | –0.17 |

| 1.01 | 0.99 | 1.14 | 0.13 | 0.81 | 1.35 | 1.53 | 0.72 | |

| 11.72 | 11.93 | 13.89 | 2.17 | 9.71 | 14.90 | 17.70 | 7.99 | |

| LEV | 0.38 | 0.39 | 0.37 | –0.01 | 0.37 | 0.23 | 0.26 | –0.10 |

B. All-but-microcaps sample | ||||||||

| LM | –0.86 | 0.29 | 1.24 | 2.10 | –0.74 | 0.23 | 1.06 | 1.80 |

| HSALE | –0.36 | –0.35 | –0.36 | 0.00 | –0.08 | –0.09 | –0.07 | 0.01 |

| ME | 6,299.22 | 6,491.35 | 6,374.82 | 75.60 | 4,864.52 | 7,285.73 | 6,202.86 | 1,338.34 |

| BM | 0.61 | 0.55 | 0.49 | –0.12 | 0.51 | 0.36 | 0.34 | –0.17 |

| 0.96 | 1.08 | 1.18 | 0.22 | 0.78 | 1.25 | 1.65 | 0.87 | |

| 11.13 | 12.40 | 13.37 | 2.24 | 8.69 | 15.09 | 19.29 | 10.61 | |

| LEV | 0.36 | 0.35 | 0.33 | –0.04 | 0.27 | 0.19 | 0.18 | –0.09 |

The table reports the time-series averages of the cross-sectional mean characteristics of the portfolios of firms sorted on product market competition and labor mobility, LM. At the end of June of each year t, stocks are sorted into three groups based on the NYSE breakpoints for the bottom 30% (Low (L)), middle 40% (Medium (M)), and top 30% (High (H)) of the ranked values of product market competition at the end of June of year t. Product market competition for an industry is measured using net sales-based market shares of all firms in that industry. Independently, stocks are sorted into three groups based on the NYSE breakpoints for the bottom 30% (L), middle 40% (M), and top 30% (H) of the ranked values of labor mobility, which is lagged 18 months, at the end of June of year t. The intersections of the product market competition and labor mobility groups result in nine portfolios. All portfolios are rebalanced annually at the end of June. The full sample in panel A includes all NYSE-, AMEX-, and NASDAQ-listed nonfinancial and nonregulated ordinary common stocks for which both nonmissing product market competition and labor mobility estimates in a given year t are available. The all-but-microcaps sample in panel B excludes stocks, from the full sample, with an end-of-June market value of equity below the 20th percentile of the NYSE market capitalization distribution and the remaining stocks are used to compute the breakpoints for product market competition and labor mobility separately. H–L is the high-minus-low portfolio. The sample period is from January 1990 to December 2016. See also the legend to Table 1.

Characteristics of portfolios double-sorted on product market competition

| Low competition | High competition | |||||||

|---|---|---|---|---|---|---|---|---|

| H–L | H–L | |||||||

A. Full sample | ||||||||

| LM | –0.92 | 0.15 | 1.25 | 2.17 | –0.93 | 0.17 | 1.13 | 2.07 |

| HSALE | –0.40 | –0.40 | –0.41 | 0.00 | –0.10 | –0.09 | –0.08 | 0.02 |

| ME | 3,577.30 | 2959.38 | 3284.64 | –292.66 | 2,983.62 | 2,941.98 | 2,238.16 | –745.46 |

| BM | 0.82 | 0.91 | 0.78 | –0.04 | 0.86 | 0.61 | 0.69 | –0.17 |

| 1.01 | 0.99 | 1.14 | 0.13 | 0.81 | 1.35 | 1.53 | 0.72 | |

| 11.72 | 11.93 | 13.89 | 2.17 | 9.71 | 14.90 | 17.70 | 7.99 | |

| LEV | 0.38 | 0.39 | 0.37 | –0.01 | 0.37 | 0.23 | 0.26 | –0.10 |

B. All-but-microcaps sample | ||||||||

| LM | –0.86 | 0.29 | 1.24 | 2.10 | –0.74 | 0.23 | 1.06 | 1.80 |

| HSALE | –0.36 | –0.35 | –0.36 | 0.00 | –0.08 | –0.09 | –0.07 | 0.01 |

| ME | 6,299.22 | 6,491.35 | 6,374.82 | 75.60 | 4,864.52 | 7,285.73 | 6,202.86 | 1,338.34 |

| BM | 0.61 | 0.55 | 0.49 | –0.12 | 0.51 | 0.36 | 0.34 | –0.17 |

| 0.96 | 1.08 | 1.18 | 0.22 | 0.78 | 1.25 | 1.65 | 0.87 | |

| 11.13 | 12.40 | 13.37 | 2.24 | 8.69 | 15.09 | 19.29 | 10.61 | |

| LEV | 0.36 | 0.35 | 0.33 | –0.04 | 0.27 | 0.19 | 0.18 | –0.09 |

| Low competition | High competition | |||||||

|---|---|---|---|---|---|---|---|---|

| H–L | H–L | |||||||

A. Full sample | ||||||||

| LM | –0.92 | 0.15 | 1.25 | 2.17 | –0.93 | 0.17 | 1.13 | 2.07 |

| HSALE | –0.40 | –0.40 | –0.41 | 0.00 | –0.10 | –0.09 | –0.08 | 0.02 |

| ME | 3,577.30 | 2959.38 | 3284.64 | –292.66 | 2,983.62 | 2,941.98 | 2,238.16 | –745.46 |

| BM | 0.82 | 0.91 | 0.78 | –0.04 | 0.86 | 0.61 | 0.69 | –0.17 |

| 1.01 | 0.99 | 1.14 | 0.13 | 0.81 | 1.35 | 1.53 | 0.72 | |

| 11.72 | 11.93 | 13.89 | 2.17 | 9.71 | 14.90 | 17.70 | 7.99 | |

| LEV | 0.38 | 0.39 | 0.37 | –0.01 | 0.37 | 0.23 | 0.26 | –0.10 |

B. All-but-microcaps sample | ||||||||

| LM | –0.86 | 0.29 | 1.24 | 2.10 | –0.74 | 0.23 | 1.06 | 1.80 |

| HSALE | –0.36 | –0.35 | –0.36 | 0.00 | –0.08 | –0.09 | –0.07 | 0.01 |

| ME | 6,299.22 | 6,491.35 | 6,374.82 | 75.60 | 4,864.52 | 7,285.73 | 6,202.86 | 1,338.34 |

| BM | 0.61 | 0.55 | 0.49 | –0.12 | 0.51 | 0.36 | 0.34 | –0.17 |

| 0.96 | 1.08 | 1.18 | 0.22 | 0.78 | 1.25 | 1.65 | 0.87 | |

| 11.13 | 12.40 | 13.37 | 2.24 | 8.69 | 15.09 | 19.29 | 10.61 | |

| LEV | 0.36 | 0.35 | 0.33 | –0.04 | 0.27 | 0.19 | 0.18 | –0.09 |

The table reports the time-series averages of the cross-sectional mean characteristics of the portfolios of firms sorted on product market competition and labor mobility, LM. At the end of June of each year t, stocks are sorted into three groups based on the NYSE breakpoints for the bottom 30% (Low (L)), middle 40% (Medium (M)), and top 30% (High (H)) of the ranked values of product market competition at the end of June of year t. Product market competition for an industry is measured using net sales-based market shares of all firms in that industry. Independently, stocks are sorted into three groups based on the NYSE breakpoints for the bottom 30% (L), middle 40% (M), and top 30% (H) of the ranked values of labor mobility, which is lagged 18 months, at the end of June of year t. The intersections of the product market competition and labor mobility groups result in nine portfolios. All portfolios are rebalanced annually at the end of June. The full sample in panel A includes all NYSE-, AMEX-, and NASDAQ-listed nonfinancial and nonregulated ordinary common stocks for which both nonmissing product market competition and labor mobility estimates in a given year t are available. The all-but-microcaps sample in panel B excludes stocks, from the full sample, with an end-of-June market value of equity below the 20th percentile of the NYSE market capitalization distribution and the remaining stocks are used to compute the breakpoints for product market competition and labor mobility separately. H–L is the high-minus-low portfolio. The sample period is from January 1990 to December 2016. See also the legend to Table 1.

However, we observe a completely different picture for LM-sorted portfolios in the Low competition industries (i.e., concentrated industries). For example, the value-weighted average monthly return of –0.15% on the high-minus-low LM portfolio is statistically insignificant at conventional levels (t-statistic = –0.91). The value-weighted characteristic-adjusted return of –0.23% per month on this hedge portfolio is also statistically insignificant (t-statistic = –1.30). Neither the average excess returns nor the average abnormal returns on portfolios displays a monotonically increasing pattern. For the high-minus-low LM portfolio, we also see that the value-weighted average abnormal returns relative to the six workhorse asset pricing models are all negative and statistically insignificant at conventional levels. Specifically, the CAPM, FS, FF3, FFC, FF5, and HXZ model alphas are –0.09%, –0.14%, –0.02%, –0.02%, –0.02%, and –0.08%, respectively, with t-statistics of –0.58, –0.87, –0.12, –0.13, –0.14, and –0.42. All these empirical results suggest that the positive LM-return relation exists only among firms in competitive industries. It is important to mention that the higher and statistically significant return of the high-minus-low LM portfolio of stocks in competitive industries indicates a stronger LM-return relation rather than a larger variation in the LM estimates. In fact, the spread in the LM estimates among firms with a high HSALE value in the average cross-section is 2.07, whereas it is higher at 2.17 among low HSALE firms (see Table 2).