Abstract

As part of its Green Deal, the European Union has advanced a ‘Carbon Border Adjustment Mechanism’ (CBAM). Reflective of a trend towards greater use of coercive trade measures to advance environmental and other policy objectives, the CBAM would extend carbon pricing to imported goods with the aim of limiting carbon leakage. Theoretical enquiry into this type of policy approach—known as border carbon adjustments (BCAs)—suggests economic and environmental benefits, but typically discounts the role of legal and practical constraints on BCA design and implementation. In this paper, we show why the BCA design commonly featured in past research—basing the adjustment level on default carbon intensities—runs counter to the economic logic of carbon pricing by distorting the incentives for emissions abatement. Requiring producers to demonstrate their actual carbon intensity captures additional economic benefits of carbon pricing and improves the overall legal prospects of a BCA, but adds to its administrative complexity and creates risk of avoidance practices such as ‘resource shuffling’. What emerges is a more nuanced understanding of BCAs that highlights the challenges when transitioning from theory to practice.

I. Introduction

As part of its European Green Deal, the European Union (EU) has proposed a ‘Carbon Border Adjustment Mechanism’ (CBAM), more generically also referred to as a ‘border carbon adjustment’ (BCA). The CBAM is meant to extend the geographic reach of the EU’s carbon price by applying it to goods imported from non-EU countries. Products covered by it would include basic materials—notably iron and steel, aluminium, cement, and fertilizers—and electricity, eventually expanding to additional product categories and more complex semi-manufactured goods (European Commission, 2021). Its application is meant to ensure that the price of imports more accurately reflects their carbon content, thereby helping to mitigate long-standing concerns about carbon leakage (the relocation of emissions from the EU to non-EU countries without a reduction in overall emissions).

The introduction of BCAs may prove critical to the international political economy of carbon pricing. First, a BCA by design extends an existing carbon price signal such as that of the EU Emissions Trading System (EU ETS) beyond national borders, broadening its scope. Second, it offers an alternative to the free allocation of emissions allowances as a leakage safeguard—which is fiscally costly and subject to industry lobbying. Third, the introduction of a BCA by progressive jurisdictions incentivizes laggards to begin pricing carbon if such efforts are credited towards compliance (Helm et al., 2012). Overall, BCAs thus offer the prospect of greater adherence to the ‘polluter pays’ principle at a global level.

So far, most economic analyses of BCAs have relied on data from Multi-region Input Output (MRIO) databases that provide sector- or country-level information on the carbon intensity of commodities, instead of disaggregated data on the carbon intensity of individual producers (Böhringer et al., 2012; Branger and Quirion, 2014). In its legislative proposal, however, the European Commission (EC) has proposed basing its CBAM on the carbon intensity of each shipment of imported goods, thus taking into account the individual producer’s decarbonization efforts.1 In this article, we show that a BCA design based on the carbon intensity of individual imports—which we label an ‘individual adjustment mechanism’ (IAM)—rather than a sectoral average or other default carbon intensity value offers important economic and legal benefits.

From an economic perspective, a BCA based solely on default intensities is a ‘one size fits all’ policy that runs counter to the economic logic underlying the use of carbon pricing to combat climate change. It has two main economic drawbacks. First, relatively clean producers get overcharged compared with high-carbon rivals. Second, it provides no incentives for abatement; the only way for foreign producers to reduce their carbon costs is to reduce their sales to the jurisdiction applying the BCA. Taken together, this means that key benefits of carbon pricing are lost—in a way that distorts abatement incentives and favours less climate-efficient foreign producers.

Which approach is chosen also has legal ramifications. First, because domestic producers have to report their actual emissions, the use of default intensities for imported goods treats domestic and foreign products differently, and therefore risks being perceived as discriminatory. Second, by sacrificing the incentivizing effect of carbon pricing, a default intensity is less likely to be considered justified on environmental grounds. Both factors thus increase the risk of a violation of international trade law.

Our key message in this paper is that an IAM—along the lines of the EC’s proposal—can at least partially address these economic and legal drawbacks. Relatively clean producers are now no longer disadvantaged, and efficient abatement incentives are at least partially restored in that reductions in actual carbon intensities can pay off. The inclusion of an IAM also lowers the burden of information on the implementing jurisdiction regarding the carbon intensities of foreign producers, and improves the prospects that a BCA will be found in alignment with World Trade Organization (WTO) rules. An IAM can help ensure greater symmetry in the treatment of domestic and foreign goods by allowing foreign producers to undergo the same process of monitoring, verification, and reporting (MRV) of emissions that domestic producers face, for instance under the EU ETS. Past case law, specifically the affirmation by a General Agreement on Tariffs and Trade (GATT) panel of a border tax adjustment by the United States on imports related to feedstock chemicals, supports our legal assessment.

Despite these economic and legal benefits, a BCA based on the actual carbon intensity of goods rather than on default values still comes at the expense of increased administrative complexity and cost, and also creates the possibility of avoidance strategies such as ‘resource shuffling’. Mandating importers to disclose the carbon intensity of all shipped products also gives rise to potential knock-on risks under general international law. Overall, thus, the analysis highlights some of the complexities encountered as BCAs progress from a theoretical concept to practical implementation, offering a cautionary tale for any jurisdiction weighing the costs and benefits of deploying coercive trade measures to advance wider policy objectives.

The article is structured as follows. Section II sets out a simple economic framework to understand the potential advantages of an IAM over the sole use of default carbon intensities. It also discusses concerns about resource shuffling as well as accommodating continued free allocation to energy-intensive and trade-exposed (EITE) sectors and foreign climate policy efforts in the BCA design. Section III discusses legal aspects with a focus on how an IAM improves the legal feasibility of a BCA in terms of WTO law. Section IV addresses practical considerations around the implementation of an IAM, including emissions verification. Section V concludes.

II. Economic considerations

(i) BCAs and principles of carbon pricing

From an economic perspective, the ideal policy is a uniform global carbon price that covers all countries and sectors. Following the logic of Pigou (1920) and Montgomery (1972), this price should be set at the social cost of carbon (SCC).2 Such a policy provides the correct incentives to internalize the climate externality, in line with the ‘polluter pays’ principle. Stern and Stiglitz (2017) estimate that the dynamic trajectory of a target-consistent global carbon price that is in line with the ambition of the Paris Agreement rises up to $50–100/tCO2 by 2030.3 As a market-based measure, its core appeal lies in achieving emissions abatement in a globally cost-effective manner. The use of carbon pricing is gradually spreading across jurisdictions (World Bank, 2021) but still falls well short of an efficient global policy benchmark.

The EU is now seeking to extend the geographic reach of its carbon price signal by introducing a CBAM that applies to imports into the EU. Its idea is summarized as follows:

Carbon leakage occurs when production is transferred from the EU to other countries with lower ambition for emission reduction, or when EU products are replaced by more carbon-intensive imports... a carbon border adjustment mechanism would ensure that the price of imports reflects more accurately their carbon content. (European Commission, 2020a)

In short, the CBAM is intended to level the playing field in carbon costs between domestic production and imports, and therefore mitigate the risk of carbon leakage.4

Because of a lack of available data, economic analyses of BCAs have typically relied on ‘default’ values when determining the carbon intensity of imports, instead of attempting to reflect the actual carbon intensity of individual product shipments. Use of default values also reduces the complexity and cost of BCA implementation in terms of the regulatory, administrative, and technical structures needed to collect, process, and store relevant data.

The use of a BCA based on default carbon-intensities runs counter to the economic logic of carbon pricing, however. This logic revolves around the carbon price providing incentives that lead to the marginal cost of abatement being equalized across producers—therefore minimizing the overall cost of emissions abatement. A crucial feature is that polluters pay the carbon price according to their actual carbon intensity. Instead, relying on a default intensity becomes more akin to a ‘one size fits all’ policy which inevitably raises the overall abatement cost (Newell and Stavins, 2003). In practice, carbon intensities can vary widely even within industrial sectors (Lyubich et al., 2018), so market-based flexibility becomes key to cost-effective decarbonization.

There is, thus, a good economic case for going beyond the use of default intensities in a BCA. In its legislative proposal of July 2021, the EC has indeed opted to require information on the actual carbon intensity of imported goods, allowing use of default values only as a fallback when actual emissions ‘cannot be adequately determined’ (European Commission, 2021).5

(ii) A framework for understanding BCA design options

A simple economic framework is helpful to understand different BCA design options. Suppose that the carbon price of the implementing jurisdiction is given by t (measured in €/tCO2). Consider a product i that is produced by a company j based in a country k outside the implementing jurisdiction and suppose that its actual carbon intensity (i.e. emissions per unit of output) is given by zijk. Suppose, for now, that this company faces a zero (or very low) domestic carbon price and that the introduction of a BCA leads to the discontinuation of free allowance allocation to domestic producers in the implementing jurisdiction.

A BCA based solely on a default intensity treats each foreign firm in the sector that sells product i as having carbon intensity Zi, regardless of its identity j and location k. So the default BCA involves a carbon cost of t x Zi being applied at the border to each unit of imported product from company j. This framework illustrates how a default CBAM comes with two economic drawbacks. First, there is a static inefficiency: any firm that is cleaner than the default intensity (zijk < Zi) gets overcharged relative to its actual carbon intensity (and relative to rivals with above-default intensities); this runs counter to the cost-effectiveness property of carbon pricing. Second, there is a dynamic inefficiency: given that the BCA is based on a default intensity beyond its control, the only way for a firm to reduce its carbon costs is to reduce its sales to the implementing jurisdiction; put differently, there is no incentive to engage in abatement that reduces its carbon intensity. Taken together, this means that key benefits of carbon pricing are lost—in a way that favours high-carbon companies.

Following the economic logic of carbon pricing, the ideal way to correct these static and dynamic drawbacks would be for the BCA to instead be based on firms’ actual carbon intensities. This would yield a per-unit carbon cost of t x zijk being applied at the border so the resulting carbon price faced by company j is identical to that if it were instead located within the implementing jurisdiction. Hence this would restore cost-effectiveness and other desirable properties of carbon pricing. However, as noted in the introduction (and explained further below), this type of mandatory product-by-product CBAM can give rise to concerns under general international law.

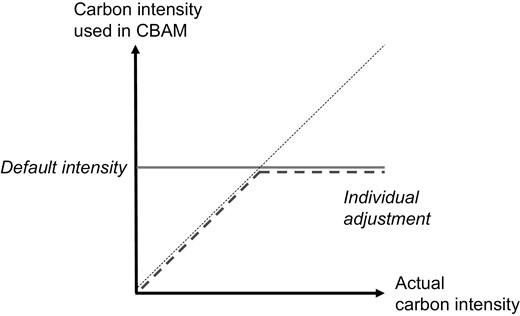

This leads us to the idea, supported by the legal analysis in the next section, of designing a BCA with a voluntary individual adjustment mechanism (IAM). This design retains a default intensity but gives the option to companies exporting to the implementing jurisdiction to demonstrate that their actual carbon intensity lies below the default value. This yields a carbon cost of t x min{zijk,Zi} at the border, reflecting that company j can choose the lower of its actual and the default intensity. Such a voluntary IAM partially addresses the two economic drawbacks identified: (i) relatively clean producers are now no longer disadvantaged, and (ii) efficient abatement incentives are partially restored in that reductions in actual carbon intensities can pay off. So, while this design still falls short of a Pigouvian ideal, it can be a significant improvement on the default BCA design; Figure 1 illustrates. The additional complexity of an IAM comes with increased implementation costs, which we discuss further in the following sections; at the same time, however, a voluntary IAM helps shift the informational burden concerning carbon performance from the regulator to the firms themselves. The remainder of this section discusses other concerns and design features of an IAM as part of BCA design.

Comparison of default BCA and individual adjustment mechanism.

(iii) Resource shuffling and carbon leakage

Resource shuffling (or ‘reshuffling’) has been an important concern for California’s BCA on electricity imports from other US states. The California Air Resources Board defines reshuffling as ‘any plan, scheme, or artifice by a First Deliverer of Electricity to substitute electricity deliveries from sources with relatively lower emissions for electricity deliveries from sources with relatively higher emissions to reduce its emissions compliance obligation’ (CARB, 2011). For example, a Californian utility that previously imported coal-fired power might, in response to a border carbon price, seek to replace this contract with gas-fired power—with the coal-fired power instead being sold in another state. California’s regulation employs an IAM for ‘specified sources’—while reverting to a default value for ‘unspecified sources’; it has nominally prohibited such reshuffling, but this prohibition has been difficult to enforce in practice (Fowlie and Cullenward, 2018; Pauer, 2018). Reshuffling is distinct from a policy’s market-based impacts in the form of carbon leakage that arise from firms’ profit-maximizing behaviour across multiple export markets; for example, carbon leakage can already arise even if all of a firm’s production has the same carbon intensity so there is no scope for reshuffling.

Hence resource shuffling is essentially a form of gaming the system: holding fixed existing trade flows, production from cleaner installations that would have otherwise gone to a third jurisdiction is used to contractually substitute for dirtier production so as to reduce exposure to the BCA, with zero effect on overall emissions. With a BCA based solely on a default carbon intensity, there is no incentive to engage in reshuffling—but such concerns do arise under an IAM. Reshuffling concerns are perhaps most acute for electricity markets due to the large heterogeneity in carbon intensities between different generation technologies combined with the flexibility of trading arrangements in wholesale power markets. By contrast, industrial sectors have different contractual arrangements between buyers and sellers, and the flow of goods they produce can be better tracked than the flow of electrons in power systems. Thus, reshuffling may be less pronounced under an IAM for industrial sectors than it has been for California’s BCA on electricity imports.

While prior economic analysis of BCAs has modelled its impacts on carbon leakage, it has typically not captured the potential for resource shuffling. One reason is that general-equilibrium simulation models often rely on Multi-region Input Output databases (such as GTAP-MRIO) presented at the country level; that is, each country is, in effect, a single player with a single (average) carbon intensity. This can detect carbon leakage at the market level, but lacks the granularity to capture the incentive to reshuffle production at the firm level, where a firm can redirect production between different facilities with different carbon intensities. Granular modelling of reshuffling at the firm level seems an important priority for future research.6

We return to the question of how policy can further mitigate resource shuffling in our discussion below of practical considerations around the implementation of an IAM.

(iv) Other CBAM design features

To complete our economic analysis, we now incorporate two other features of BCA design: the continued presence of free allocation within the implementing jurisdiction and foreign climate policy efforts. Both apply to BCA design in general, and are not specific to an IAM.

Free allocation to EITE sectors.

The above analysis assumes that the introduction of a BCA leads to free allocation to EITE sectors being discontinued. In practice, this process may be phased such that free allocation co-exists with a BCA over a transition period.7 In its legislative proposal for a CBAM, the EC envisions a gradual reduction of free allocation over the course of the decade from 2026 to 2035 (European Commission, 2021).

This approach necessitates adjustments to our formulae for carbon-price equalization. A simplified application to the EU ETS goes as follows. Suppose that yi* is the carbon intensity of the best 10% percentile EU producer in an EITE sector. Under current allocation rules, this company receives just enough free allocation to cover its compliance obligation; EU producers with a higher carbon intensity are left with a (post-allocation) compliance gap. Consider, again for product i, an EU producer j with a carbon intensity of yij> yi*, receiving free allocation covering a fraction fij = yi*/yij ∈ (0,1) of its emissions (per unit of output). Therefore, we can conceptualize an average degree of free allocation fi = average(fij) ∈ (0,1) across EU companies selling product i, with an average carbon intensity yi = average(yij). This leads to an allocation-adjusted carbon cost under the IAM of t x max{0, min{zijk,Zi} – fi x yi}, reflecting the watering down of the EU carbon price for EITE sectors from its headline level t.8 To illustrate, a non-EU producer cleaner than the default intensity, zijk< Zi, would face an IAM carbon cost of t x [zijk – fi x yi], unless its actual intensity is so low in that zijk < fi x yi, in which case its carbon cost is zero. For another example, suppose that the CBAM’s default intensity were set at the average EU carbon intensity and that the non-EU producer is less clean, Zi = yi < zijk; the formula for the carbon cost simplifies to t x Zi(1 – fi), reflecting the ‘dilution’ of the EU carbon price due to free allocation.

Climate policy efforts outside the implementing jurisdiction.

The above analysis assumes that the jurisdictions of origin have a zero carbon price. While this assumption is currently applicable in a wide range of cases, carbon constraints including carbon pricing have been picking up in the rest of the world. Suppose instead that producer j’s product i faces a domestic carbon price tijk in its country k so that ∆tijk = max{t–tijk,0} is the shortfall in its carbon price relative to the implementing jurisdiction. This adjusted carbon-price differential could then be used for the calculation of the BCA. For example, under an IAM, the ‘top up’ carbon price at the border would become ∆tijk x min{zijk,Zi}, and therefore vary by country of import.9 From an economic viewpoint, this top-up feature has the attractive property of ensuring carbon-price equalization over time by adjusting to enhanced carbon pricing in foreign jurisdictions—thus incentivizing them to adopt a carbon price.

The above adjustment has been exemplified through consideration of ‘explicit’ carbon prices that are determined within a cap-and-trade system like the EU ETS or by a carbon tax. It does not attempt to incorporate ‘effective’ carbon prices due to non-price policies that implicitly place a price on carbon; this includes taxes on road fuels, renewable support schemes, fossil fuel subsidies, and compensation schemes for indirect carbon costs due to increased power prices. The plethora of such policies makes estimating effective carbon prices very challenging, and there is currently no standard methodology. That explains why the legislative proposal for the CBAM only allows crediting of explicit carbon prices (European Commission, 2021). What is more, any estimates of effective carbon prices would also vary by EU member state, creating additional complexity in the calculation of a BCA.10

Finally, in the case of the EU, we can thus extend the formula to account for both carbon pricing outside the EU and free allocation within the EU ETS. This leads to a carbon cost under the IAM of ∆tijk x max{0, min{zijk,Zi} – fi x yi}. For simplicity, this assumes that the carbon price in the non-EU country itself is either a carbon tax or an auctioned ETS, i.e. it does not have any free allowance allocation. In general, the appropriate adjustment of a CBAM for carbon pricing outside the EU would need to take into account the specific design of free allocation (and potentially of other support policies).

III. Legal considerations

(i) International trade law

While the introduction of a BCA raises legal questions in more areas than one, international trade law is particularly relevant because of how the measure will be applied to goods traded across national borders. From the earliest announcement of the CBAM in Ursula von der Leyen’s political guidelines to various subsequent statements and documents, the European Commission and its President have consistently emphasized the need to ensure that it be ‘fully compliant with World Trade Organization rules’ (von der Leyen, 2019; similarly European Commission, 2019, 2020a). As is shown in this section, the proposed inclusion of an IAM improves the prospects that the CBAM will be found in alignment with World Trade Organization (WTO) rules.

At the heart of the WTO regime lies the General Agreement on Tariffs and Trade (GATT), which dates back to 1947 and is a legally binding international treaty with broad membership. According to its preamble, the GATT aims at a ‘substantial reduction of tariffs and other barriers to trade’ and at ‘the elimination of discriminatory treatment in international commerce’. A central tenet of the GATT—and a cornerstone of the multilateral trading system—is the principle of non-discrimination in international trade. For trade in goods, it consists of two elements: the most-favoured-nation (MFN) treatment obligation, set out in Article I of the GATT, and the national treatment (NT) obligation, set out in Article III of the GATT.

Article I:1 of the GATT prohibits parties from discriminating between ‘like’ products originating in, or destined for, any other party, whereas Article III of the GATT prohibits discrimination between domestic products and ‘like’ imported products. What constitutes ‘likeness’ of domestic and imported products is not defined in the GATT, but has been determined in relevant case law based on whether they share common physical characteristics and properties, end uses, and tariff classifications; whether they compete in the marketplace; and relevant consumer preferences.11

Importantly, differences in the processes and production methods (PPMs) that do not leave a physical trace in the final product—such as the source of energy used during production—are not generally considered to affect the likeness of products.12 Although the jurisprudence on ‘like’ products remains inconclusive and has seen some evolution in recent case law,13 there is a high probability that goods produced with low-carbon PPMs and carbon-intensive goods would be considered ‘like’ products, despite their different carbon footprints. Any differentiation between such products that leads to a competitive disadvantage could thus be considered discriminatory (Pauwelyn, 2013).

Under international trade law, treating domestic and imported goods differently based on the carbon intensity of their production therefore incurs a risk of judicial challenge (Mehling et al., 2019). A BCA that imposes a greater compliance burden on carbon-intensive imports than that faced by less carbon-intensive domestic products, for instance, could be considered discriminatory. Because such differentiation on the basis of (actual or assumed) carbon intensity is intrinsic to the notion of a BCA, however, and because—as shown in the preceding section—differentiation is critical to its environmental effectiveness, it is difficult to envision how the implementing jurisdiction can altogether avoid risking a violation of the principle of non-discrimination set out in the GATT.

For the same reason, the literature on border carbon adjustments has routinely highlighted the importance of Article XX of the GATT, which can provisionally justify measures that would otherwise be considered discriminatory (Condon and Ignaciuk, 2013). Two such general exceptions relate to measures ‘necessary to protect human, animal or plant life or health’ (Article XX(b)) or ‘relating to the conservation of exhaustible natural resources if such measures are made effective in conjunction with restrictions on domestic production or consumption’ (Article XX(g)). Both the wording of these provisions and their broad interpretation in past case law suggest that measures aimed at reducing greenhouse gas emissions can fall under either exception (UNEP and WTO, 2009).

Several conditions need to be met for Article XX(b) and (g) to be successfully invoked, however, including two that have a bearing on the legal implications of an IAM: the need for a sufficient connection between the BCA and its environmental objective, which is inferred from the wording ‘necessary to’ and ‘relating to’; and a requirement that the measure not be applied in a manner which would constitute ‘a means of arbitrary or unjustifiable discrimination between countries where the same conditions prevail’, which is derived from the introductory paragraph—or ‘chapeau’—of Article XX.

When applied to the concept of an IAM, the foregoing considerations imply the following two takeaways: first, an IAM can help ensure greater symmetry in the treatment of domestic and foreign goods by allowing foreign producers to undergo the same process of monitoring, reporting, and verification (MRV) that domestic producers face. In the case of a voluntary IAM, it is safe to assume that only foreign producers who are less carbon-intensive than the default intensity applied by the implementing jurisdiction would avail themselves of the IAM, whereas those who are more carbon-intensive will be treated as if they were as carbon-efficient as the default intensity. All else being equal, this would mean that foreign goods will be treated as or more favourably than domestic goods with the same carbon intensity, lowering the likelihood that such a BCA violates Article III of the GATT.

Second, if products with different carbon intensities are considered ‘like’ products despite their different carbon footprints, the BCA still risks being considered discriminatory because relatively less carbon-intensive domestic products will typically face a lower compliance burden than relatively more carbon-intensive foreign products. In that case, the admissibility of the BCA depends on whether it can be provisionally justified by one or more of the general exceptions under Article XX of the GATT. As mentioned earlier, Article XX(b) and (g) are the exceptions of greatest relevance in this context, and both require a sufficient connection between the measure and its environmental objective. The previous section already highlighted how an IAM improves the environmental effectiveness of a BCA by providing a stronger incentive for foreign producers to reduce their carbon intensity. Additionally, by ensuring greater symmetry in the treatment of domestic and foreign products, the IAM also helps meet the requirements of the chapeau of Article XX.

Past case law supports this assessment: in the United States—Superfund case, a GATT panel affirmed a border tax adjustment imposed by the United States under the Superfund Amendments and Reauthorization Act of 1986 (SARA) on certain imported substances produced from feedstock chemicals subject to a domestic excise tax.14 Importers were required to furnish the information necessary to determine the amount of feedstock chemicals and thus of tax to be imposed, but if they failed to do so, the United States was authorized to apply a default—or baseline—rate equal to the predominant method of production in the United States. According to the panel, this approach was sufficient to demonstrate equivalence under Article III of the GATT between the domestic excise tax and the border measure applied to imports.15

In a more recent case, United States—Reformulated Gasoline, the Appellate Body conversely held that a rule under the Clean Air Act regulating the composition and emission effects of gasoline to prevent air pollution was discriminatory by setting out different calculation methods for domestic and foreign gasoline.16 In particular, the Appellate Body objected to the fact that importers were subject to a default ‘statutory baseline’ that had no connection to the particular gasoline imported, while refiners of domestic gasoline were assessed against an individual baseline representing the quality of gasoline produced by each refiner. This, according to the Appellate Body, constituted an ‘unjustifiable discrimination’ and a ‘disguised restriction on international trade’ in the context of Article XX(g) of the GATT.17 It also rejected practical arguments that verification on foreign soil, and subsequent enforcement actions, would be so difficult as to rule out individual baselines. Here, the Appellate Body pointed to the possibility of relying on documentary evidence provided by the foreign refiners themselves—citing, inter alia, the option of third-party verification—and also highlighted the importance of cooperation on such administrative arrangements.18

To conclude, thus, the analysis of relevant legal provisions and case law suggests that an IAM improves the prospects of a BCA being found in compliance with WTO rules.

(ii) International environmental law

Under the Paris Agreement, an international climate treaty adopted in 2015 with nearly universal participation, parties agreed that the pace and ambition of domestic climate efforts is to be decided at the national level. According to Article 4(2) of the Paris Agreement, it is up to each party to ‘prepare, communicate and maintain successive nationally determined contributions that it intends to achieve’; Article 4(3) goes on to state that successive contributions should reflect each party’s ‘common but differentiated responsibilities and respective capabilities, in the light of different national circumstances’.

A BCA could be held to contravene this fundamental principle if it were considered a unilateral measure that coerces other countries to increase their domestic climate efforts in order to avoid or limit compliance obligations for products entering the implementing jurisdiction (Quick, 2020). Whether the Paris Agreement, whose overarching objective is to ‘strengthen the global response to the threat of climate change’ (Article 2(1)), can be interpreted to limit unilateral action if such action is primarily aimed at increasing climate ambition, is debatable; be that as it may, an IAM would arguably alleviate such concerns because, relative to a default intensity, it affords foreign producers greater flexibility. The ability to demonstrate actual carbon intensities of foreign products may, in turn, reduce pressure on the respective countries to change existing or adopt new policies mandating lower carbon intensities across the board in order to satisfy the relevant default threshold of the implementing country.

(iii) General international law

Finally, by seeking to influence policy choices in foreign jurisdictions and basing its calculation on physical processes taking place on foreign territory, a BCA could be considered an extraterritorial measure that infringes on the territorial sovereignty of affected trade partners. Territorial sovereignty comprises the right of states to exercise state authority within their territory, and manifests itself in the principle of non-intervention in the internal affairs of other states.19 Unilateral measures that take into account circumstances within foreign territory risk being considered a violation of that principle and of the domaine réservé of affected states. More generally, coercive action taken by one state to secure a change in the policies of another is likely to constitute an intervention in the internal affairs of the latter (Jamnejad and Wood, 2009), underscoring the risk associated with any mandatory policies.

A voluntary IAM can mitigate any residual risk under general international law and the principle of territoriality. It obviates the need for the implementing jurisdiction to collect emissions and production data from foreign entities, or to mandate the disclosure of such data. Aside from being difficult to enforce in foreign territory, such mandatory requirements would be more likely to face challenge as an intervention in the internal affairs of affected states. Instead, the combination of a default intensity with a voluntary IAM ensures that any consideration of activities on foreign territory, and any related action taken by foreign entities, occur on a purely voluntary basis. Consequently, the voluntary IAM lowers the risk of the BCA being considered a violation of the sovereignty of affected trade partners.

IV. Practical considerations

(i) General considerations

Functionally, an IAM provision would enable importers to avoid the compliance obligation that otherwise results from application of the default carbon intensity values specified for different products under the BCA. Such default carbon intensities can be set at very different levels, ranging from the assumption that foreign producers are highly carbon intensive and emit as if they had implemented the ‘worst available technology’ to a sectoral average carbon intensity in a particular geographic context, all the way to different ‘best available technology’ or ‘best performer’ benchmarks.20 Given the need to ensure equal treatment of ‘like’ domestic and imported products under Article III of the GATT and the prohibition of arbitrary or unjustifiable discrimination under the chapeau of Article XX, the default carbon intensity applied to imports should be at least as favourable as the average carbon intensity of domestic producers. Which default intensity is ultimately chosen has no bearing on the design and expedience of an IAM, however.

As proposed, the CBAM will be implemented through an extension of the EU ETS, with importers of covered products who are unable to, or refuse to, document actual emissions required to purchase and surrender CBAM certificates for the amount of emissions corresponding to the weight of imported product multiplied by the default value, adjusted for the remaining share of free allocation to domestic producers (European Commission, 2021). Importers with a carbon intensity that is lower than the default value who can provide the required documentation, however, would reduce their compliance obligation under the CBAM.

To do so, importers have to furnish verified information documenting the actual emissions associated with production. An important question, thus, relates to the methodologies and process used to determine and report the carbon intensity of imported products. Ideally, the rules applicable to imports should follow the same modalities used for domestic products to minimize differentiation and thus potential discrimination. Domestic producers whose installations are covered by the EU ETS, for instance, are required to comply with an elaborate compliance cycle setting out an annual procedure of monitoring, reporting, and verification (MRV) based on detailed rules, principles, and guidance documents; similarly, under the proposed CBAM, importers will be required to declare the emissions embedded in imported goods, and have the declared emissions verified by an accredited verifier to ensure the integrity of reported data (European Commission, 2021).

In essence, importers of covered products will thus have to comply with similar monitoring and reporting provisions as European producers. An EU CBAM is also likely to create new opportunities for ‘learning by doing’ by policy-makers. Already in the run-up to its introduction, affected producers located outside the EU have an increased incentive to quantify and report their carbon intensity of production. This effect would be magnified to the extent that the EU CBAM prompts further jurisdictions to introduce their own BCAs and price carbon at the border. Once the CBAM is in place, European policy-makers can proceed to fine-tune its operation—including the implementing acts on MRV procedures and methodologies. Such improvements may, in turn, help inform best practices and benefit other jurisdictions designing BCAs.

(ii) Specific challenges

Generally, the legal imperative to avoid discrimination between domestic and imported products favours applying the same rules and procedures to importers subject to an IAM. In some matters, however, differentiation may be justified, for instance to avoid undue cost and hardship, or to support the environmental objectives of the BCA. One such matter relates to the verifiers that are eligible to perform the independent verification of emission certificates compiled by importers. In its proposed rulemaking to define individual baselines for the US reformulated gasoline programme, for instance, the EPA would have required the verification process to be carried out by entities accredited in the United States. Limiting eligible verifiers to those located and accredited in the domestic jurisdiction could impose an undue cost on importers, however: the audit cost to importers should be comparable to the cost borne by domestic producers in order to avoid discrimination. Under the EU ETS, verifiers are entities certified by the national accreditation bodies of each member state. Hence, it appears reasonable to allow verification by entities accredited in the country from which imported products originate, provided the accreditation conditions are comparable in stringency.

A similar departure from the rules applicable to domestic producers could be justified when it comes to the point of regulation. In the EU, for instance, stationary emitters are regulated at the level of individual installations, defined by Article 3(e) of the EU ETS Directive as technical units where one or more covered activities are carried out. Installations operated by the same company at different sites are, thus, regulated separately, each reporting emissions and complying with EU ETS obligations independently. As mentioned earlier, however, determination of carbon intensity at the installation level for the purposes of an IAM can raise concerns about reshuffling between different installations owned by the same company.

Since such reshuffling can jeopardize the environmental objectives of the BCA—and thus also its justification under Article XX of the GATT—it could be justifiable to set the point of regulation for importers at the company level, meaning that an importer would have to comply with the BCA based on the average carbon intensity of all production facilities operated by the same producer in foreign jurisdictions. Importers would then no longer be able to lower their compliance burden by focusing abatement efforts on select installations designated for production for the market of the jurisdiction implementing the BCA. Still, such an approach would require further study, for instance on the additional administrative burden and economic cost it would impose on foreign producers by requiring MRV of emissions for multiple installations.

Also, alternative definitions of ‘company’ and their respective implications would need to be evaluated, especially with regard to large corporations with complex, vertically and horizontally layered decision-making structures, as well as state-owned enterprises where centralized decisions can affect several companies at once and are often reached on political grounds. One option to disincentivize resource shuffling could also be to retain some degree of discretion with regard to the IAM, and reserve the option of returning to a default carbon intensity for imported products if there are objective factors suggesting that the importer may be engaged in resource shuffling practices. At worst, thus, importers would fall back to the default intensity.

Finally, the process through which importers declare embedded emissions should be as straightforward as possible and aligned with existing processes to the extent possible. In the case of the CBAM, such data collected by the customs authorities would enable precise and automatic determination of the number of certificates to be surrendered by each importer, based on import volumes multiplied either by the default carbon intensity applied to that product or, where an emissions declaration has been submitted, the specific emissions associated with the imported product. Because all products covered by the CBAM would bear a customs tariff nomenclature reference corresponding to an EU ETS product code, production and emissions data as well as the average share of free allocation for the corresponding domestic products would be readily available.

V. Concluding remarks

As suggested by Helm et al. (2012), opposition to BCAs due to concerns about implementation costs is to see ‘the perfect as the enemy of the good’. In this paper, we have explored how far the good can be pushed in terms of policy design for a BCA on imports. We have proposed a BCA design with a voluntary individual adjustment that allows producers to demonstrate that their actual carbon intensity lies below a default value. Relative to a BCA based solely on the default value, an IAM captures additional economic benefits of carbon pricing—notably rewarding producers’ decarbonization efforts—and improves the overall prospects of the BCA being found to comply with international law and WTO rules.

In its proposed design for the CBAM, the EC has opted for an IAM by requiring importers of covered goods to declare actual embedded emissions (European Commission, 2021, Article 7). Doing so provides economic and environmental benefits, as shown in this article, and also improves the prospects of the CBAM under international trade law. It increases the administrative burden on EU customs authorities and foreign producers, however, and incurs a risk of resource shuffling. The legislative proposal of the CBAM contains a provision meant to tackle circumvention (European Commission, 2021, Article 27), but does not expressly address resource shuffling concerns. Whether and to what extent resource shuffling will prove a challenge once the CBAM is implemented is therefore difficult to predict. In any event, what the foregoing analysis of a specific BCA design feature—the determination of emissions embedded in traded goods—has shown is the important role that legal, political, and administrative considerations play in the practical implementation as well as the functioning of BCAs. Such considerations should inform our understanding and assessment of BCAs as a tool to address emissions leakage.

Another consideration is the ability of a BCA to raise additional fiscal revenue. Initial estimates by the European Commission, in a discussion of the recovery from COVID-19 and its reinforced financial framework for 2021–7, noted that ‘a carbon border adjustment mechanism could bring additional revenues ranging from about €5 billion to €14 billion, depending on the scope and design’ (European Commission, 2020b). Thereby, a BCA design based solely on default intensity arguably has the benefit of bringing relatively greater certainty about the likely size of the tax take.

The use of an IAM creates an additional layer of budgetary uncertainty and, all else remaining equal, also reduces the revenue raised (i) by eliminating the ‘overcharge’ on clean producers, and (ii) by inducing additional emissions abatement. This reduction in fiscal revenue would need to be weighed up against other economic, environmental, and legal benefits of the IAM. Commentators have, for instance, suggested that targeted expenditure of BCA revenue in developing countries could substantially soften diplomatic and legal resistance while addressing negative welfare impacts (Grubb, 2011; Springmann, 2013). More generally, this is a feature that is ‘baked into’ carbon pricing: policies that are more successful at driving decarbonization may also yield less government revenue as they shrink the future tax base.

This article builds on Michael A. Mehling and Robert A. Ritz, ‘Going Beyond Default Intensities in an EU Carbon Border Adjustment Mechanism’, MIT CEEPR Working Paper 2020-019, October 2020. The authors are grateful to several reviewers for their feedback and constructive suggestions.

References

— (

— (

— (

Footnotes

See European Commission (2021), Article 7 and Annex III.

Rubin (1996) extends this logic to dynamic emissions trading in an intertemporal context.

Stern and Stiglitz (2017) emphasize that complementary policies would be in place alongside carbon pricing; without these, the required carbon-price trajectory may be significantly higher.

Cosbey et al. (2019) provide a valuable overview of the core findings from the economics literature on BCAs before the EU’s CBAM policy proposals materialized.

As stated in Annex III of the proposed regulation, the default values ‘shall be set at the average emission intensity of each exporting country and for each of the goods . . . increased by a mark-up . . . . When reliable data for the exporting country cannot be applied for a type of goods, the default values shall be based on the average emission intensity of the 10 per cent worst performing EU installations for that type of goods’ (European Commission, 2021).

A full comparison of carbon leakage and resource shuffling under a default BCA with those under an IAM would require an economic model of multimarket competition that explicitly features how individual firms may have production facilities with different carbon intensities and may choose to sell their products across multiple markets. The answer may hinge on the finer details of the competitive environment, much of which is lost by modelling competition only at the country level.

A related point is that a CBAM will likely apply only to imports and therefore cannot level the playing field in terms of the carbon competitiveness of EU exports to foreign markets, which creates a rationale for the continued use of free allocation for exports (Evans et al., 2021) or another form of export subsidy or rebate (Garicano, 2021).

A caveat is that this simple calculation adjusts the carbon price purely based on accounting of free allocation, without incorporating the impact on economic incentives (e.g. on a firm’s marginal cost of production). Current EU allocation rules are a complex hybrid with elements of grandfathering, output-based allocation, and an emissions performance standard (due to benchmarking); working out its impact on economic incentives would require more detailed analysis.

A producer based in a country with a carbon price above the EU level would then be exempt from CBAM-related payments (and its country could apply a BCA on its imports from the EU).

Because the CBAM, as currently proposed, will only adjust for the explicit carbon price paid by EU producers under the EU ETS—and not other climate-related policies, such as energy taxes—it can also be argued that such non-price policies do not need to be taken into account to ensure symmetry between EU and foreign producers (unless perhaps the foreign jurisdiction relies solely on non-price policies to curb emissions from the same activities as those covered by the EU ETS, but this would raise significant methodological and likely also political—e.g. lobbying—challenges).

Appellate Body Report, Japan—Taxes on Alcoholic Beverages, WT/DS8/AB/R, WT/DS10/AB/R, WT/DS11/AB/R, adopted 1 November 1996, pp. 20–1; Appellate Body Report, EC—Measures Affecting Asbestos and Asbestos-containing Products, WT/DS135/AB/R, adopted 5 April 2001, para. 99.

Going back to, notably, Panel Report, United States—Restrictions on Imports of Tuna, DS21/R, DS21/R, 3 September 1991, unadopted.

See, for instance, Panel Report, United States—Measures Concerning the Importation, Marketing and Sale of Tuna and Tuna Products, WT/DS381/R, adopted 13 June 2012, para. 7.78; more generally, see also Potts (2008).

Panel Report, United States—Taxes on Petroleum and Certain Imported Substances, L/6175—34S/136, adopted 17 June 1987. In assessing whether this border adjustment complied with the national treatment obligation, the panel cited Article III of the GATT, stating that it ‘permits the imposition of an internal tax on imported products provided the like domestic products are taxed, directly or indirectly, at the same or a higher rate’, see ibid., para. 5.2.7.

Ibid., para. 5.2.9.

Appellate Body Report, United States—Standards for Reformulated and Conventional Gasoline, WT/DS2/AB/R, adopted 20 May 1996.

Ibid., p. 29.

An exception could only apply for cases where ‘the source of imported gasoline could not be determined or a baseline could not be established because of an absence of data’, see ibid., p. 27.

Deriving it from the principle of sovereign equality of states enshrined in Article 2(1) of the Charter of the United Nations: International Court of Justice, Military and Paramilitary Activities in and against Nicaragua (Nicaragua v. US), Merits, Judgment of 27 June 1986, [1986] ICJ Rep. 14, para. 202.

An example of such a ‘best performer’ benchmark are the product benchmarks used for purposes of free allocation to energy-intensive and trade-exposed industries under the EU ETS, representing the average carbon intensity of the 10 per cent most efficient installations in terms of metric tons of CO2 emitted per ton of product produced during a specified period.

{kind=link}