Abstract

Using a structural life-cycle model, we quantify the heterogeneous impact of school closures during the corona crisis on children affected at different ages and coming from households with different parental characteristics. In the model, public investment through schooling is combined with parental time and resource investments in the production of child human capital at different stages in the children’s development process. We quantitatively characterise the long-term consequences from a COVID-19-induced loss of schooling, and find average losses in the present discounted value of lifetime earnings of the affected children of |$2.1\%$|, as well as welfare losses equivalent to about |$1.2\%$| of permanent consumption. Because of self-productivity in the human capital production function, younger children are hurt more by the school closures than older children. The negative impact of the crisis on children’s welfare is especially severe for those with parents with low educational attainment and low assets.

Governments worldwide have reacted to the COVID-19 pandemic by closing schools and child care centres. In many countries, including the United States, these closures started in mid March 2020 and extended well into 2021. Whereas the economic consequences of temporary business closures are immediate and drew significant policy and media attention, the economic consequences of school and child care closures emerge in the longer run and are not always easily measured. Given the importance of human capital for individual prosperity and long-term macroeconomic growth, they are however likely substantial (see, e.g., Krueger and Lindahl, 2001; Manuelli and Seshadri, 2014).

In this paper, we analyse the long-term income, welfare and distributional consequences of the school and child care closures on the affected children. To do so, we build a heterogeneous agent partial equilibrium model with a human capital production function at its core that takes time and monetary inputs by parents and governmental investment into schooling as inputs. Parents also leave inter vivos transfers (IVT) to their children, which can be used to finance college and consumption. The key dimensions of heterogeneity we focus on are the age of a child in 2020 (when the school closures first occurred), as well as parental socio-economic characteristics, namely financial resources, marital status and education. We model school and child care closures as a reduction in the governmental investment in children corresponding to one year less schooling, the average time of school closures in the United States until summer of 2021. We also show results based on six months of school closures, assuming partial effectiveness of online teaching. In the model, parents endogenously adjust their investment into children and inter vivos transfers in response to the drop in governmental inputs, thereby potentially mitigating the adverse consequences of COVID-19-induced school closures. We use our model as a quantitative laboratory to analyse the long-term aggregate and distributional consequences of the COVID school shock on children’s acquired human capital, their high-school graduation and college choice, their labour market earnings and, ultimately, their welfare.

The key ingredients for the quantitative analysis are the parameters characterising the human capital production function, which we either take from the literature or calibrate to data moments on parental investments into children from US household micro data. Once the model is parameterised, we subject children and parents to a one-time unexpected COVID-19 school closure shock and document the short- and long-run economic consequences. On average (across children aged four to fourteen when the shock occurs), the model implies that the school closures alone lead to an increase in the future share of children without a high-school degree of |$16\%$| and a reduction of the share of children with a college degree of |$-7\%$|. On average, the present discounted earnings losses at labour market entry induced by reduced human capital accumulation and lower educational attainment amount to |$-2.1\%$|. To put these losses into a macroeconomic perspective, if we discount these losses to the beginning of 2020 and aggregate them across all school children impacted by the COVID-19 school closures, they amount to ca. |$3\%$| of 2019 US GDP. These effects materialise despite a significant endogenous adjustment of parental investments into their children: time inputs rise by |$16.6\%$| and monetary inputs by |$35.4\%$| on impact. Measured as consumption-equivalent variation, the average welfare loss of children from the COVID-induced school closures amounts to |$-1.21\%$|. Given the temporary nature of the shock, assumed to last one year in the baseline results, we view these numbers as quite large.

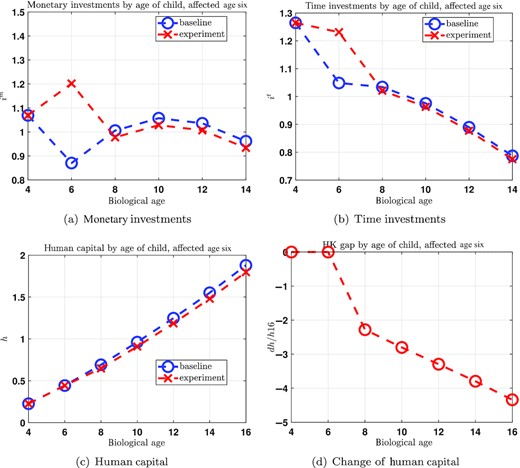

These average welfare losses mask substantial heterogeneity by the age and parental socio-economic characteristics of the children at the time of the crisis. Turning first to the age of the child, the adverse impact is most pronounced for younger children of school age (i.e., children of ages 6–10). The welfare losses of children aged six at the time of the crisis amount to |$-1.57\%$| in terms of consumption-equivalent variation. Even though parents respond strongly to the closure of schools by increasing their time and resource inputs into the child human capital production function, they do not quite fully offset the reduction in public inputs due to schooling. This implies that children arrive at older ages with less human capital due to the COVID crisis, and due to the self-productivity of human capital the effect is stronger for younger children. Additionally, since the human capital production function features dynamic complementarities, the marginal productivity of private investments at future ages is also reduced. Optimising parents respond to this by investing less into their children at older ages (relative to the pre-COVID scenario). Combined, these effects lead to lower human capital at age sixteen, adverse outcomes on high-school completion and college attendance, future wages and, consequently, welfare. Older children at the time of the COVID crisis, instead, have already accumulated most of their human capital, and therefore the adverse future effects due to self-productivity and lower incentives for parental human capital investment due to COVID school closures are less severe.

Apart from the age of the child, parental background matters for the negative impact of the COVID shock on human capital accumulation, wages and welfare. Broadly speaking, children with poorer parents suffer more. There are two reasons for this. First, even without any parental adjustments in investments, children from lower income households suffer more from the school closures, since for them, a larger part of educational investment comes from the government. Second, as a reaction to the school closures, rich parents increase their investment into children by more than poor parents. They have more financial resources to do so, and their children have on average higher human capital. Given that the human capital production function features dynamic complementarity, rich parents thus have higher incentives to compensate the reduction in government investment than poor parents. Focusing on each parental characteristic alone, we find that children from single parents, parents from the lowest asset quintile or high-school dropout parents have around 50% higher welfare losses than children from married parents, parents from the highest asset quintile or college-educated parents. However, these three parental characteristics are positively correlated, and thus losses along a single characteristic compound each other. Children from the most disadvantaged households then have four times larger welfare losses than children from the most privileged households.

This paper ties into the literature on schooling and human capital formation. Our human capital production function relies on Cunha et al. (2006), Cunha and Heckman (2007) and Cunha et al. (2010), especially on the feature of self-productivity, i.e., higher human capital in one period leads to higher human capital in the next period, and dynamic complementarity, i.e., human capital investment pays out more the higher the human capital.1 This feature implies that early childhood education is a crucial determinant of future income (Cunha and Heckman, 2007; and Caucutt and Lochner, 2020). Consequently, public schooling is a driver of intergenerational mobility. Relying on quantitative models, Kotera and Seshadri (2017) showed that differences in intergenerational mobility across US states can be explained by differences in public school finances. Related, Lee and Seshadri (2019) found that education subsidies can significantly increase intergenerational mobility.2 Agostinelli et al. (2020) also used a structural model of human capital formation to evaluate the consequences of COVID-19-related school closure, but focused on the high-school years of teenagers, and emphasised the loss of peer interactions as an important driver of losses in educational attainment. Jang and Yum (2021) built a general equilibrium model and focused on the effects of the school closures on aggregate outcomes and intergenerational mobility.

Whereas the quantitative literature focuses on the effects of public schooling investment on children’s outcomes and intergenerational mobility, there exists an empirical literature that analyses specifically the link between school instruction time and outcomes of children. Lavy (2015) exploited international differences in school instruction time, caused by differences in the length of an average school day and usual school weeks, and found that school instruction time in core subjects significantly affects testing outcomes of children. Similarly, Carlsson et al. (2015) exploited exogenous variation in testing dates in Sweden and reported that an extra ten days of school instruction raised scores on intelligence tests by 1% of a standard deviation.3 There are few studies investigating longer-term outcomes of school instruction time on children. Cortes et al. (2015) found a positive effect of math instruction time on the probability of attending college for low-performing students. Pischke (2007) exploited short school years associated with a shift in the school starting date in Germany in the 1960s, and found no significant effects on employment and earnings of affected children. Jaume and Willén (2019) found that half a year less instruction time during primary school caused by school strikes in Argentina lowers the long-term earnings by 3.2% for men and 1.9% for women.

The remainder of this paper unfolds as follows. Section 1 presents the model, and Section 2 its calibration. Sections 3 and 4 then discuss the results, first in terms of aggregate effects, then in terms of its distribution. Section 5 discusses the sensitivity of the results with respect to one crucial parameter, namely the elasticity of substitution between governmental and parental inputs. Last, Section 6 concludes, and the Online Appendix contains further details of the model, the data and calibration, as well as additional quantitative results.

1. A Quantitative Model of Education During the Epidemic

We now describe the structural life cycle model used to quantify the long-run consequences of school closures during the COVID-19 pandemic. After setting out the fundamentals of the economy (demographics, time, risk, endowments, preferences and government policy) we immediately focus on the recursive formulation of the model, since this is the representation we compute.

1.1. Individual State Variables, Risk and Economic Decisions

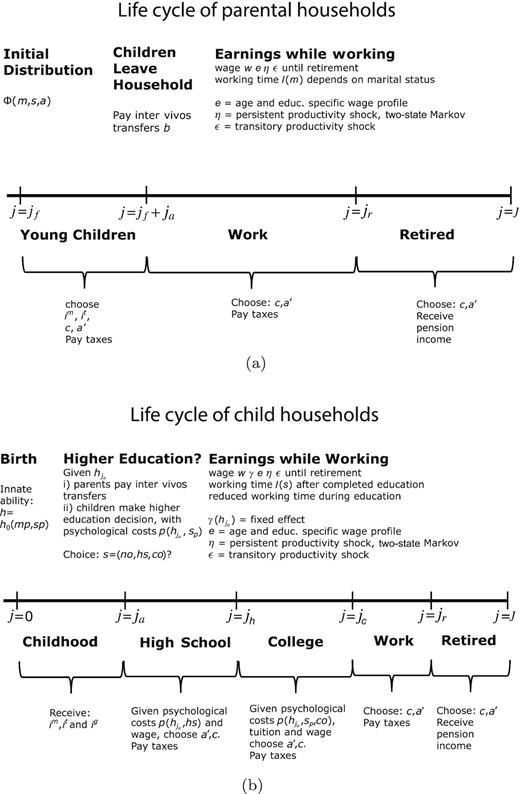

Time in the model is discrete and the current period is denoted by |$t.$| We model the life cycle of one adult and one children generation in partial equilibrium. The timing and events of this life cycle are summarised in Figure 1.

Life Cycle of Child and Parental Households.

Agents are heterogeneous with respect to the generation they belong to, |$k \in \lbrace ch,pa\rbrace ,$| either being part of the child (|$ch$|) or parental (|$pa$|) generation, and they differ by their marital status |$m \in \lbrace si,ma\rbrace$| for single (|$si$|) and married (|$ma$|), their age |$j \in \lbrace 0,\ldots ,J\lt \infty \rbrace$|, their asset position |$a$|, their current human capital |$h$|, their education level |$s \in \lbrace { {no}, {hs}, {co}}\rbrace$| for no (|${ {no}}$|) higher education (no high-school completion), high-school (|$hs$|) attendance and completion, college (|${ {co}}$|) attendance and completion, and idiosyncratic productivity risk modelled as a two-state Markov process with state vector |$\eta \in \lbrace \eta _l,\eta _h\rbrace$|, where |$\eta _l$| is low and |$\eta _h$| is high labour productivity, and transition matrix |$\pi (\eta ^\prime \mid \eta )$| and a transitory shock |$\varepsilon \in \lbrace \varepsilon _1,\ldots ,\varepsilon _n\rbrace$|. The individual state variables and the range of values they can take are summarised in Table 1.

State Variables.

| State variable | Values | Interpretation |

|---|---|---|

| |$k$| | |$k\in \lbrace ch,pa\rbrace$| | Generation |

| |$m$| | |$m\in \lbrace si,ma\rbrace$| | Marital status |

| |$j$| | |$j\in \lbrace 0,1,\ldots ,J\rbrace$| | Model age |

| |$a$| | |$a\ge -\underline{a}(j,s,k)$| | Assets |

| |$h$| | |$h\gt 0$| | Human capital |

| |$s$| | |$s \in \lbrace no,hs,co\rbrace $| | Education |

| |$\eta$| | |$\eta \in \lbrace \eta _l,\eta _h\rbrace $| | Persistent productivity shock |

| |$\varepsilon$| | |$\varepsilon \in \lbrace \varepsilon _1,\ldots ,\varepsilon _n\rbrace $| | Transitory productivity shock |

| State variable | Values | Interpretation |

|---|---|---|

| |$k$| | |$k\in \lbrace ch,pa\rbrace$| | Generation |

| |$m$| | |$m\in \lbrace si,ma\rbrace$| | Marital status |

| |$j$| | |$j\in \lbrace 0,1,\ldots ,J\rbrace$| | Model age |

| |$a$| | |$a\ge -\underline{a}(j,s,k)$| | Assets |

| |$h$| | |$h\gt 0$| | Human capital |

| |$s$| | |$s \in \lbrace no,hs,co\rbrace $| | Education |

| |$\eta$| | |$\eta \in \lbrace \eta _l,\eta _h\rbrace $| | Persistent productivity shock |

| |$\varepsilon$| | |$\varepsilon \in \lbrace \varepsilon _1,\ldots ,\varepsilon _n\rbrace $| | Transitory productivity shock |

Notes: List of state variables of the economic model.

State Variables.

| State variable | Values | Interpretation |

|---|---|---|

| |$k$| | |$k\in \lbrace ch,pa\rbrace$| | Generation |

| |$m$| | |$m\in \lbrace si,ma\rbrace$| | Marital status |

| |$j$| | |$j\in \lbrace 0,1,\ldots ,J\rbrace$| | Model age |

| |$a$| | |$a\ge -\underline{a}(j,s,k)$| | Assets |

| |$h$| | |$h\gt 0$| | Human capital |

| |$s$| | |$s \in \lbrace no,hs,co\rbrace $| | Education |

| |$\eta$| | |$\eta \in \lbrace \eta _l,\eta _h\rbrace $| | Persistent productivity shock |

| |$\varepsilon$| | |$\varepsilon \in \lbrace \varepsilon _1,\ldots ,\varepsilon _n\rbrace $| | Transitory productivity shock |

| State variable | Values | Interpretation |

|---|---|---|

| |$k$| | |$k\in \lbrace ch,pa\rbrace$| | Generation |

| |$m$| | |$m\in \lbrace si,ma\rbrace$| | Marital status |

| |$j$| | |$j\in \lbrace 0,1,\ldots ,J\rbrace$| | Model age |

| |$a$| | |$a\ge -\underline{a}(j,s,k)$| | Assets |

| |$h$| | |$h\gt 0$| | Human capital |

| |$s$| | |$s \in \lbrace no,hs,co\rbrace $| | Education |

| |$\eta$| | |$\eta \in \lbrace \eta _l,\eta _h\rbrace $| | Persistent productivity shock |

| |$\varepsilon$| | |$\varepsilon \in \lbrace \varepsilon _1,\ldots ,\varepsilon _n\rbrace $| | Transitory productivity shock |

Notes: List of state variables of the economic model.

We assume that parents give birth to children at the age of |$j_{f}$| and denote the fertility rate of households by |$\xi (m,s)$|, which differs by marital status and education groups. Note that |$\xi (m,s)$| is also the number of children per household. There is no survival risk and all households live until age |$J$| and thus the cohort size within each generation is constant (and normalised to 1). We now describe in detail how life unfolds for parents, and then for children, as summarised in Figure 1.

1.1.1. Life of the parental generation

Parental households become economically active at age |$j_f$| just before their children are born. They start their economic life in marital status |$m$| and with education level |$s$|, initial idiosyncratic productivity states |$\eta$| and |$\varepsilon$| and initial assets |$a$|. These initial states are exogenously given to the household, and drawn from the population distribution |$\Phi (s,m,\eta ,\varepsilon ,a)$| that will be informed directly by the data.

Parents then observe the innate ability (initial human capital) |$h=h_{0}(s,m)$| of their children that depends on parental education |$s$| and marital status |$m$|. Children live with their parents until age |$j_a$| (parental age |$(j_{f}+j_{a})$|), at which point they leave the parental household to form their own household.

When children leave the household at parental age |$j_f+j_a$|, parents may transfer additional monetary resources as inter vivos transfers |$b$| to their children. After this transfer parents and children separate and there are no further interactions between the two generations.

Parents work until retirement at age |$j_r$|, when they receive earnings-history-dependent per-period retirement benefits |$b^p \gt 0$| and live until age |$J$|. In addition to making human capital investment decisions for their children when these are present in the household, parents in each period make a standard consumption-saving choice, where household asset choices are subject to a potentially binding borrowing constraint |$a^\prime \ge -\underline{a}(j,s,m,pa)$|, which will be parameterised such that the model replicates well household debt at the age at which households have children |$j_f.$| The borrowing limit is assumed to decline linearly to zero over the life cycle towards the last period of work at age |$j_r-1$|. Table 2 summarises the choices of parents (and children, as described in the next subsection).

Per-Period Decision Variables.

| State variable | Values | Decision period | Interpretation |

|---|---|---|---|

| |$c$| | |$c \gt 0$| | |$j\ge j_a$| | Consumption |

| |$a^{\prime }$| | |$a^\prime \ge -\underline{a}(j,s,k)$| | |$j\ge j_a$| | Asset accumulation |

| |$i^t$| | |$i^t \ge 0$| | |$j \in \lbrace j_f,\ldots ,j_f+j_a\rbrace$| | Time investments |

| |$i^m$| | |$i^m \ge 0$| | |$j \in \lbrace j_f,\ldots ,j_f+j_a\rbrace$| | Monetary investments |

| |$b$| | |$b \ge 0$| | |$j =j_f+j_a$| | Monetary inter vivos transfer |

| |$s$| | |$s \in \lbrace no,hi,co\rbrace $| | |$j=j_a$| | (Higher) education |

| State variable | Values | Decision period | Interpretation |

|---|---|---|---|

| |$c$| | |$c \gt 0$| | |$j\ge j_a$| | Consumption |

| |$a^{\prime }$| | |$a^\prime \ge -\underline{a}(j,s,k)$| | |$j\ge j_a$| | Asset accumulation |

| |$i^t$| | |$i^t \ge 0$| | |$j \in \lbrace j_f,\ldots ,j_f+j_a\rbrace$| | Time investments |

| |$i^m$| | |$i^m \ge 0$| | |$j \in \lbrace j_f,\ldots ,j_f+j_a\rbrace$| | Monetary investments |

| |$b$| | |$b \ge 0$| | |$j =j_f+j_a$| | Monetary inter vivos transfer |

| |$s$| | |$s \in \lbrace no,hi,co\rbrace $| | |$j=j_a$| | (Higher) education |

Notes: List of decision variables of the economic model.

Per-Period Decision Variables.

| State variable | Values | Decision period | Interpretation |

|---|---|---|---|

| |$c$| | |$c \gt 0$| | |$j\ge j_a$| | Consumption |

| |$a^{\prime }$| | |$a^\prime \ge -\underline{a}(j,s,k)$| | |$j\ge j_a$| | Asset accumulation |

| |$i^t$| | |$i^t \ge 0$| | |$j \in \lbrace j_f,\ldots ,j_f+j_a\rbrace$| | Time investments |

| |$i^m$| | |$i^m \ge 0$| | |$j \in \lbrace j_f,\ldots ,j_f+j_a\rbrace$| | Monetary investments |

| |$b$| | |$b \ge 0$| | |$j =j_f+j_a$| | Monetary inter vivos transfer |

| |$s$| | |$s \in \lbrace no,hi,co\rbrace $| | |$j=j_a$| | (Higher) education |

| State variable | Values | Decision period | Interpretation |

|---|---|---|---|

| |$c$| | |$c \gt 0$| | |$j\ge j_a$| | Consumption |

| |$a^{\prime }$| | |$a^\prime \ge -\underline{a}(j,s,k)$| | |$j\ge j_a$| | Asset accumulation |

| |$i^t$| | |$i^t \ge 0$| | |$j \in \lbrace j_f,\ldots ,j_f+j_a\rbrace$| | Time investments |

| |$i^m$| | |$i^m \ge 0$| | |$j \in \lbrace j_f,\ldots ,j_f+j_a\rbrace$| | Monetary investments |

| |$b$| | |$b \ge 0$| | |$j =j_f+j_a$| | Monetary inter vivos transfer |

| |$s$| | |$s \in \lbrace no,hi,co\rbrace $| | |$j=j_a$| | (Higher) education |

Notes: List of decision variables of the economic model.

1.1.2. Life of the children generation

Children are born at age |$j=0$|, but for the first |$j_{a}-1$| periods of their life do not make economic decisions. Their human capital during these periods evolves as the outcome of parental investment decisions |$(i^m,i^t)$| described above and governmental schooling input |$(i^g)$|. At the beginning of age |$j_{a},$| and based on both the level of human capital as well as the financial transfer |$b$| from their parents (which determines their initial wealth |$a$|), children make a discrete higher education decision |$s \in \lbrace { {no}, {hs}, {co}}\rbrace$|, where |$s={ {no}}$| stands in for the choice not to complete high school, |$hs$| for high-school completion and |${ {co}}$| for college completion. For simplicity, children are stand-in bachelor households through their entire life cycle.

Acquiring a high-school or college degree comes at a utility (or psychological) cost |$p(s,s_p,h)$|, which is decreasing in the child’s acquired human capital |$h$| and also depends on parental education |$s_p$|. In addition, college (|${ {co}}$|) education requires a monetary cost |$\iota \ge 0$|. Children may finance some of their college expenses by borrowing, subject to a credit limit given by |$-\underline{a}(j,s,ch)$|, which is zero for |$s \in \lbrace no,hs\rbrace ,$| i.e., for individuals not going to college. As was the case for parents, this limit decreases linearly with age and converges to zero at the age of retirement |$j_r,$| requiring the children generation to pay off their student loans prior to their retirement.

Youngsters who decide not to complete high school, |$s =no,$| enter the labour market immediately at age |$j_w(s={ {no}})=j_{a}$|. Those who decide to complete high school, but not to attend college, do so at age |$j_w(s=hs)=j_h\gt j_a$|. While at high school, |$\lbrace j_a,\ldots ,j_h-1\rbrace$|, they work part time at wages of education group |$s={ {no}}$|. Youngsters who decide to attend college enter the labour market at |$j_w(s=co)=j_{c}$| and also work part time at wages of education group |$s={ {no}}$| during their high-school and college years |$\lbrace j_a,j_c-1\rbrace .$|

1.2. Decision Problems

Since we focus on a single parent and children generation, we can solve the model backward, starting from the dynamic programming problem of the children.

1.2.1. Children

The first meaningful economic decision in the children generation takes place at age |$j_a$|, when children leave the parental household with the receipt of inter vivos transfers, which constitute initial assets |$a,$| as well as with human capital |$h$|.

The retirement phase. During retirement, at ages |$\lbrace j_r,\ldots ,J\rbrace$|, all three education groups of the children generation solve a standard consumption-saving problem given in Online Appendix A.1.

1.2.2. Parents

1.3. Government

The government runs a pension system with a balanced budget. It also finances exogenous government spending, expressed as a share of aggregate output |$G/Y$|, and aggregate education subsidies (of pre-tertiary and tertiary education) through consumption taxes, capital income taxes and a progressive labour income tax code. In the initial scenario without the COVID-19 shock, the government budget clears by adjustment of the average labour income tax rate. In the thought experiments we hold all tax parameters constant, therefore implicitly assuming that the shortfalls or surpluses generated by a change in the environment are absorbed by government debt serviced by future generations.

1.4. Thought Experiment

We compute an initial stationary partial equilibrium with exogenous wages and returns prior to model period |$t=0$|. In period |$t=0$|, the COVID-19 shock unexpectedly occurs, and from that point on unfolds deterministically. That is, factor prices and fiscal policies are fixed, and households get surprised once by the shock, after which they have perfect foresight with respect to aggregate economic conditions. The COVID-19 school closures are represented in the model by a temporary (one year) reduction in public investment |$i^g$| into child human capital production.

We then trace out the impact of this temporary shock on parental human capital inputs (both time and money) and intergenerational transfer decisions, as well as on the education choices, future labour market outcomes and welfare of the children generation, both in terms of its aggregates as well as in terms of its distribution. Since children differ by age at the time of the shock (as well as in terms of parental characteristics), so will the long-run impact on educational attainment, future wages and welfare. We place special emphasis on this heterogeneity.

2. Calibration

A subset of parameters is calibrated exogenously outside the model, summarised in Table 3. The subset of second-stage parameters, summarised in Table 4, is calibrated endogenously by matching moments in the data. In the calibration, we use data from the PSID, including its Child Development Supplement (CDS),6 and the NLSY79.7 We now describe in detail our choice of first-stage parameters and the moments we match to calibrate the second-stage parameters.

First-Stage Calibration Parameters.

| Parameter | Interpretation | Value | Source (data/literature) |

|---|---|---|---|

| Population | |||

| |$j=0$| | Age at economic birth (age four) | 0 | |

| |$j_{a}$| | Age at beginning of economic life (age sixteen) | 6 | |

| |$j_{h}$| | Age at finishing HS (age eighteen) | 7 | |

| |$j_{c}$| | Age at finishing CL (age twenty-two) | 9 | |

| |$j_{f}$| | Fertility age (age thirty-two) | 14 | |

| |$j_{r}$| | Retirement age (age sixty-six) | 31 | |

| |$J$| | Max. lifetime (age eighty) | 38 | |

| |$\xi (m,s)$| | Fertility rates | See main text | PSID 2011–17 |

| |$\Phi (j_f,m,s)$| | Distribution of parents by martial status and education, age |$j_f$| | See main text | PSID 2011–17 |

| Preferences | |||

| |$\theta$| | Relative risk aversion parameter | 1 | |

| |$\varphi$| | Curvature of labour disutility | 0.5 | |

| Labour productivity | |||

| |$\lbrace \epsilon (j,s,m)\rbrace$| | Age profile | See main text | PSID 1968–2012 |

| |$[\varepsilon _l,\varepsilon _h]$| | Realisations of transitory shock | |$[0.881, 1.119]$| | PSID 1968–2012 |

| |$[\eta _l,\eta _h]$| | States of Markov process | [0.8226, 1.1774] | PSID 1968–2012 |

| |$\pi _{hl}$| | Transition probability of Markov process | 0.0431 | PSID 1968–2012 |

| |$\pi ^{r}_{hl}(s)$| | Transition probability of Markov process after lockdown | [0.0493,0.0486,0.0456] | See main text |

| |$\pi ^{r}_{ll}(s)$| | Transition probability of Markov process after lockdown | [0.9630,0.9624,0.9594] | See main text |

| |$\chi ^s$| | Hours worked for students, as a fraction of full time (HS and CL) | |$\lbrace 0.2,0.5 \rbrace $| | See main text |

| |$\gamma (s,h)$| | Ability gradient of earnings | See main text | NLSY79 |

| Endowments | |||

| |$r$| | (Annual) interest rate | 4.0% | Siegel (2002) |

| |$l(m)$| | Average hours worked by marital status (annual) | |$\lbrace 1868, 3810\rbrace $| | PSID 2011–17 |

| |$\Phi (a|j_f,m,s)$| | Asset distribution of parents by martial status and education, age |$j_f$| | See main text | PSID 2011–17 |

| |$\underline {a}(j_f,m, s,pa)$| | Borrowing limit for parents at age |$j_f$| | See main text | PSID 2011–17 |

| |$rp(m=si, s, pa)$| | Education-specific repayment amount for parents: singles | See Subsection 2.4 | |$\lbrace 0.006, 0.083, 0.151 \rbrace$| |

| |$rp(m=ma, s, pa)$| | Education-specific repayment amount for parents: couples | See Subsection 2.4 | |$\lbrace 0.048, 0.129, 0.110 \rbrace$| |

| Ability/human capital and education | |||

| |$\iota$| | College tuition costs (annual, net of grants and subsidies) | $14,756 | Krueger and Ludwig (2016) |

| |$\underline {a}(j \in [j_h,j_c-1],{ {co}},ch)$| | College borrowing limit | $45,000 | Krueger and Ludwig (2016) |

| |$rp(ch)$| | Repayment amount for children who choose college | 0.049 | See Subsection 2.7 |

| |$\sigma ^{h}$| | Elasticity of subst. between human capital and CES invest. aggregate | 1 | Cunha et al. (2010) |

| |$\sigma ^{g}$| | Elasticity of subst. between public invest. and CES aggregate of private invest. | 2.43 | Kotera and Seshadri (2017) |

| |$\sigma ^{m}$| | Elasticity of subst. between monetary and time investments | 1 | Lee and Seshadri (2019) |

| |$\kappa ^m_3$| | CES share parameter of monetary and time investments (age bin 6–8) | 0.5 | Normalisation |

| |$\kappa ^g_j=\bar{\kappa }^g,j\gt 0$| | Share of government input for ages six and older | 0.676 | Kotera and Seshadri (2017) |

| |$\Phi (h(j=0)|s_p,y_p,a_p)$| | Innate ability distribution of children by parental characteristics | See main text | PSID CDS I |

| |$\underline{h}_0$| | Normalisation parameter of initial distribution of initial ability | 0.1248 | PSID CDS I–III |

| Government policy | |||

| |$\xi$| | Public CL education subsidy | 38.8% | Krueger and Ludwig (2016) |

| |$i^g_j$| | Public early education spending by age | |$\approx \$\text{5,000}$| | UNESCO (1999–2005) |

| |$\tau _c$| | Consumption tax rate | 5.0% | Legislation |

| |$\tilde{\tau }_k$| | Capital income tax rate | 20% | Legislation |

| |$\tau ^p$| | Social security payroll tax | 12.4% | Legislation |

| |$G/Y$| | Government consumption to GDP | 13.8% | Current value |

| Parameter | Interpretation | Value | Source (data/literature) |

|---|---|---|---|

| Population | |||

| |$j=0$| | Age at economic birth (age four) | 0 | |

| |$j_{a}$| | Age at beginning of economic life (age sixteen) | 6 | |

| |$j_{h}$| | Age at finishing HS (age eighteen) | 7 | |

| |$j_{c}$| | Age at finishing CL (age twenty-two) | 9 | |

| |$j_{f}$| | Fertility age (age thirty-two) | 14 | |

| |$j_{r}$| | Retirement age (age sixty-six) | 31 | |

| |$J$| | Max. lifetime (age eighty) | 38 | |

| |$\xi (m,s)$| | Fertility rates | See main text | PSID 2011–17 |

| |$\Phi (j_f,m,s)$| | Distribution of parents by martial status and education, age |$j_f$| | See main text | PSID 2011–17 |

| Preferences | |||

| |$\theta$| | Relative risk aversion parameter | 1 | |

| |$\varphi$| | Curvature of labour disutility | 0.5 | |

| Labour productivity | |||

| |$\lbrace \epsilon (j,s,m)\rbrace$| | Age profile | See main text | PSID 1968–2012 |

| |$[\varepsilon _l,\varepsilon _h]$| | Realisations of transitory shock | |$[0.881, 1.119]$| | PSID 1968–2012 |

| |$[\eta _l,\eta _h]$| | States of Markov process | [0.8226, 1.1774] | PSID 1968–2012 |

| |$\pi _{hl}$| | Transition probability of Markov process | 0.0431 | PSID 1968–2012 |

| |$\pi ^{r}_{hl}(s)$| | Transition probability of Markov process after lockdown | [0.0493,0.0486,0.0456] | See main text |

| |$\pi ^{r}_{ll}(s)$| | Transition probability of Markov process after lockdown | [0.9630,0.9624,0.9594] | See main text |

| |$\chi ^s$| | Hours worked for students, as a fraction of full time (HS and CL) | |$\lbrace 0.2,0.5 \rbrace $| | See main text |

| |$\gamma (s,h)$| | Ability gradient of earnings | See main text | NLSY79 |

| Endowments | |||

| |$r$| | (Annual) interest rate | 4.0% | Siegel (2002) |

| |$l(m)$| | Average hours worked by marital status (annual) | |$\lbrace 1868, 3810\rbrace $| | PSID 2011–17 |

| |$\Phi (a|j_f,m,s)$| | Asset distribution of parents by martial status and education, age |$j_f$| | See main text | PSID 2011–17 |

| |$\underline {a}(j_f,m, s,pa)$| | Borrowing limit for parents at age |$j_f$| | See main text | PSID 2011–17 |

| |$rp(m=si, s, pa)$| | Education-specific repayment amount for parents: singles | See Subsection 2.4 | |$\lbrace 0.006, 0.083, 0.151 \rbrace$| |

| |$rp(m=ma, s, pa)$| | Education-specific repayment amount for parents: couples | See Subsection 2.4 | |$\lbrace 0.048, 0.129, 0.110 \rbrace$| |

| Ability/human capital and education | |||

| |$\iota$| | College tuition costs (annual, net of grants and subsidies) | $14,756 | Krueger and Ludwig (2016) |

| |$\underline {a}(j \in [j_h,j_c-1],{ {co}},ch)$| | College borrowing limit | $45,000 | Krueger and Ludwig (2016) |

| |$rp(ch)$| | Repayment amount for children who choose college | 0.049 | See Subsection 2.7 |

| |$\sigma ^{h}$| | Elasticity of subst. between human capital and CES invest. aggregate | 1 | Cunha et al. (2010) |

| |$\sigma ^{g}$| | Elasticity of subst. between public invest. and CES aggregate of private invest. | 2.43 | Kotera and Seshadri (2017) |

| |$\sigma ^{m}$| | Elasticity of subst. between monetary and time investments | 1 | Lee and Seshadri (2019) |

| |$\kappa ^m_3$| | CES share parameter of monetary and time investments (age bin 6–8) | 0.5 | Normalisation |

| |$\kappa ^g_j=\bar{\kappa }^g,j\gt 0$| | Share of government input for ages six and older | 0.676 | Kotera and Seshadri (2017) |

| |$\Phi (h(j=0)|s_p,y_p,a_p)$| | Innate ability distribution of children by parental characteristics | See main text | PSID CDS I |

| |$\underline{h}_0$| | Normalisation parameter of initial distribution of initial ability | 0.1248 | PSID CDS I–III |

| Government policy | |||

| |$\xi$| | Public CL education subsidy | 38.8% | Krueger and Ludwig (2016) |

| |$i^g_j$| | Public early education spending by age | |$\approx \$\text{5,000}$| | UNESCO (1999–2005) |

| |$\tau _c$| | Consumption tax rate | 5.0% | Legislation |

| |$\tilde{\tau }_k$| | Capital income tax rate | 20% | Legislation |

| |$\tau ^p$| | Social security payroll tax | 12.4% | Legislation |

| |$G/Y$| | Government consumption to GDP | 13.8% | Current value |

Notes: First-stage parameters calibrated exogenously by reference to other studies and data.

First-Stage Calibration Parameters.

| Parameter | Interpretation | Value | Source (data/literature) |

|---|---|---|---|

| Population | |||

| |$j=0$| | Age at economic birth (age four) | 0 | |

| |$j_{a}$| | Age at beginning of economic life (age sixteen) | 6 | |

| |$j_{h}$| | Age at finishing HS (age eighteen) | 7 | |

| |$j_{c}$| | Age at finishing CL (age twenty-two) | 9 | |

| |$j_{f}$| | Fertility age (age thirty-two) | 14 | |

| |$j_{r}$| | Retirement age (age sixty-six) | 31 | |

| |$J$| | Max. lifetime (age eighty) | 38 | |

| |$\xi (m,s)$| | Fertility rates | See main text | PSID 2011–17 |

| |$\Phi (j_f,m,s)$| | Distribution of parents by martial status and education, age |$j_f$| | See main text | PSID 2011–17 |

| Preferences | |||

| |$\theta$| | Relative risk aversion parameter | 1 | |

| |$\varphi$| | Curvature of labour disutility | 0.5 | |

| Labour productivity | |||

| |$\lbrace \epsilon (j,s,m)\rbrace$| | Age profile | See main text | PSID 1968–2012 |

| |$[\varepsilon _l,\varepsilon _h]$| | Realisations of transitory shock | |$[0.881, 1.119]$| | PSID 1968–2012 |

| |$[\eta _l,\eta _h]$| | States of Markov process | [0.8226, 1.1774] | PSID 1968–2012 |

| |$\pi _{hl}$| | Transition probability of Markov process | 0.0431 | PSID 1968–2012 |

| |$\pi ^{r}_{hl}(s)$| | Transition probability of Markov process after lockdown | [0.0493,0.0486,0.0456] | See main text |

| |$\pi ^{r}_{ll}(s)$| | Transition probability of Markov process after lockdown | [0.9630,0.9624,0.9594] | See main text |

| |$\chi ^s$| | Hours worked for students, as a fraction of full time (HS and CL) | |$\lbrace 0.2,0.5 \rbrace $| | See main text |

| |$\gamma (s,h)$| | Ability gradient of earnings | See main text | NLSY79 |

| Endowments | |||

| |$r$| | (Annual) interest rate | 4.0% | Siegel (2002) |

| |$l(m)$| | Average hours worked by marital status (annual) | |$\lbrace 1868, 3810\rbrace $| | PSID 2011–17 |

| |$\Phi (a|j_f,m,s)$| | Asset distribution of parents by martial status and education, age |$j_f$| | See main text | PSID 2011–17 |

| |$\underline {a}(j_f,m, s,pa)$| | Borrowing limit for parents at age |$j_f$| | See main text | PSID 2011–17 |

| |$rp(m=si, s, pa)$| | Education-specific repayment amount for parents: singles | See Subsection 2.4 | |$\lbrace 0.006, 0.083, 0.151 \rbrace$| |

| |$rp(m=ma, s, pa)$| | Education-specific repayment amount for parents: couples | See Subsection 2.4 | |$\lbrace 0.048, 0.129, 0.110 \rbrace$| |

| Ability/human capital and education | |||

| |$\iota$| | College tuition costs (annual, net of grants and subsidies) | $14,756 | Krueger and Ludwig (2016) |

| |$\underline {a}(j \in [j_h,j_c-1],{ {co}},ch)$| | College borrowing limit | $45,000 | Krueger and Ludwig (2016) |

| |$rp(ch)$| | Repayment amount for children who choose college | 0.049 | See Subsection 2.7 |

| |$\sigma ^{h}$| | Elasticity of subst. between human capital and CES invest. aggregate | 1 | Cunha et al. (2010) |

| |$\sigma ^{g}$| | Elasticity of subst. between public invest. and CES aggregate of private invest. | 2.43 | Kotera and Seshadri (2017) |

| |$\sigma ^{m}$| | Elasticity of subst. between monetary and time investments | 1 | Lee and Seshadri (2019) |

| |$\kappa ^m_3$| | CES share parameter of monetary and time investments (age bin 6–8) | 0.5 | Normalisation |

| |$\kappa ^g_j=\bar{\kappa }^g,j\gt 0$| | Share of government input for ages six and older | 0.676 | Kotera and Seshadri (2017) |

| |$\Phi (h(j=0)|s_p,y_p,a_p)$| | Innate ability distribution of children by parental characteristics | See main text | PSID CDS I |

| |$\underline{h}_0$| | Normalisation parameter of initial distribution of initial ability | 0.1248 | PSID CDS I–III |

| Government policy | |||

| |$\xi$| | Public CL education subsidy | 38.8% | Krueger and Ludwig (2016) |

| |$i^g_j$| | Public early education spending by age | |$\approx \$\text{5,000}$| | UNESCO (1999–2005) |

| |$\tau _c$| | Consumption tax rate | 5.0% | Legislation |

| |$\tilde{\tau }_k$| | Capital income tax rate | 20% | Legislation |

| |$\tau ^p$| | Social security payroll tax | 12.4% | Legislation |

| |$G/Y$| | Government consumption to GDP | 13.8% | Current value |

| Parameter | Interpretation | Value | Source (data/literature) |

|---|---|---|---|

| Population | |||

| |$j=0$| | Age at economic birth (age four) | 0 | |

| |$j_{a}$| | Age at beginning of economic life (age sixteen) | 6 | |

| |$j_{h}$| | Age at finishing HS (age eighteen) | 7 | |

| |$j_{c}$| | Age at finishing CL (age twenty-two) | 9 | |

| |$j_{f}$| | Fertility age (age thirty-two) | 14 | |

| |$j_{r}$| | Retirement age (age sixty-six) | 31 | |

| |$J$| | Max. lifetime (age eighty) | 38 | |

| |$\xi (m,s)$| | Fertility rates | See main text | PSID 2011–17 |

| |$\Phi (j_f,m,s)$| | Distribution of parents by martial status and education, age |$j_f$| | See main text | PSID 2011–17 |

| Preferences | |||

| |$\theta$| | Relative risk aversion parameter | 1 | |

| |$\varphi$| | Curvature of labour disutility | 0.5 | |

| Labour productivity | |||

| |$\lbrace \epsilon (j,s,m)\rbrace$| | Age profile | See main text | PSID 1968–2012 |

| |$[\varepsilon _l,\varepsilon _h]$| | Realisations of transitory shock | |$[0.881, 1.119]$| | PSID 1968–2012 |

| |$[\eta _l,\eta _h]$| | States of Markov process | [0.8226, 1.1774] | PSID 1968–2012 |

| |$\pi _{hl}$| | Transition probability of Markov process | 0.0431 | PSID 1968–2012 |

| |$\pi ^{r}_{hl}(s)$| | Transition probability of Markov process after lockdown | [0.0493,0.0486,0.0456] | See main text |

| |$\pi ^{r}_{ll}(s)$| | Transition probability of Markov process after lockdown | [0.9630,0.9624,0.9594] | See main text |

| |$\chi ^s$| | Hours worked for students, as a fraction of full time (HS and CL) | |$\lbrace 0.2,0.5 \rbrace $| | See main text |

| |$\gamma (s,h)$| | Ability gradient of earnings | See main text | NLSY79 |

| Endowments | |||

| |$r$| | (Annual) interest rate | 4.0% | Siegel (2002) |

| |$l(m)$| | Average hours worked by marital status (annual) | |$\lbrace 1868, 3810\rbrace $| | PSID 2011–17 |

| |$\Phi (a|j_f,m,s)$| | Asset distribution of parents by martial status and education, age |$j_f$| | See main text | PSID 2011–17 |

| |$\underline {a}(j_f,m, s,pa)$| | Borrowing limit for parents at age |$j_f$| | See main text | PSID 2011–17 |

| |$rp(m=si, s, pa)$| | Education-specific repayment amount for parents: singles | See Subsection 2.4 | |$\lbrace 0.006, 0.083, 0.151 \rbrace$| |

| |$rp(m=ma, s, pa)$| | Education-specific repayment amount for parents: couples | See Subsection 2.4 | |$\lbrace 0.048, 0.129, 0.110 \rbrace$| |

| Ability/human capital and education | |||

| |$\iota$| | College tuition costs (annual, net of grants and subsidies) | $14,756 | Krueger and Ludwig (2016) |

| |$\underline {a}(j \in [j_h,j_c-1],{ {co}},ch)$| | College borrowing limit | $45,000 | Krueger and Ludwig (2016) |

| |$rp(ch)$| | Repayment amount for children who choose college | 0.049 | See Subsection 2.7 |

| |$\sigma ^{h}$| | Elasticity of subst. between human capital and CES invest. aggregate | 1 | Cunha et al. (2010) |

| |$\sigma ^{g}$| | Elasticity of subst. between public invest. and CES aggregate of private invest. | 2.43 | Kotera and Seshadri (2017) |

| |$\sigma ^{m}$| | Elasticity of subst. between monetary and time investments | 1 | Lee and Seshadri (2019) |

| |$\kappa ^m_3$| | CES share parameter of monetary and time investments (age bin 6–8) | 0.5 | Normalisation |

| |$\kappa ^g_j=\bar{\kappa }^g,j\gt 0$| | Share of government input for ages six and older | 0.676 | Kotera and Seshadri (2017) |

| |$\Phi (h(j=0)|s_p,y_p,a_p)$| | Innate ability distribution of children by parental characteristics | See main text | PSID CDS I |

| |$\underline{h}_0$| | Normalisation parameter of initial distribution of initial ability | 0.1248 | PSID CDS I–III |

| Government policy | |||

| |$\xi$| | Public CL education subsidy | 38.8% | Krueger and Ludwig (2016) |

| |$i^g_j$| | Public early education spending by age | |$\approx \$\text{5,000}$| | UNESCO (1999–2005) |

| |$\tau _c$| | Consumption tax rate | 5.0% | Legislation |

| |$\tilde{\tau }_k$| | Capital income tax rate | 20% | Legislation |

| |$\tau ^p$| | Social security payroll tax | 12.4% | Legislation |

| |$G/Y$| | Government consumption to GDP | 13.8% | Current value |

Notes: First-stage parameters calibrated exogenously by reference to other studies and data.

Second-Stage Calibration Parameters.

| Parameter | Interpretation | Value |

|---|---|---|

| Preferences | ||

| |$\beta$| | Time discount rate (target: asset to income ratio, ages 25–60) | 0.9808 |

| |$\nu$| | Altruism parameter (target: average IVT per child) | 0.8380 |

| Labour productivity | ||

| |$\rho _0(s)$| | Normalisation parameter (target: |$ \mathbb {E} \gamma (s,h)=1$|) | |$[0.1890, 0.0034, -0.2015]$| |

| Human capital and education | ||

| |$\kappa$| | Utility weight on time invest. (target: average time invest.) | 0.7310 |

| |$\kappa ^h_j$| | Share of human capital (target: average monetary & slope of time investments) | cf. Online Appendix Figure B1 |

| |$\kappa ^m_j$| | Share of monetary input (target: slope of monetary invest.) | cf. Online Appendix Figure B1 |

| |$\kappa ^g_0$| | Share of government input for age bin 4–6 (target: average time invest. age bin 4–6) | 0.4437 |

| |$\bar{A}$| | Investment scale parameter (target: average HK at age |$j_a$|) | 1.1989 |

| |$\tilde{A}$| | Investment scale parameter in HS (target: average HK at age |$j_{a+1}$|) | 1.0739 |

| |$\phi$| | Utility costs |$s=hs$| (target: fraction of group |$s=hs$|) | 0.0561 |

| |$\tilde{\varrho }(s^p=no)=\tilde{\varrho }(s^p=hs)$| | Utility costs |$s={ {co}}, s^p=no \wedge s^p=hs$| (target: fraction of group |$s=co$|) | 1.2120 |

| |$\tilde{\varrho }(s^p=co)$| | Utility costs |$s={ {co}}, s^p=co$| (target: conditional fraction of group |$s=co$|) | 0.1707 |

| Government policy | ||

| |$\lambda$| | Level parameter of HSV tax function (balance government budget) | 0.8880 |

| |$\rho ^p$| | Pension replacement rate (balance social security budget) | 0.1893 |

| Parameter | Interpretation | Value |

|---|---|---|

| Preferences | ||

| |$\beta$| | Time discount rate (target: asset to income ratio, ages 25–60) | 0.9808 |

| |$\nu$| | Altruism parameter (target: average IVT per child) | 0.8380 |

| Labour productivity | ||

| |$\rho _0(s)$| | Normalisation parameter (target: |$ \mathbb {E} \gamma (s,h)=1$|) | |$[0.1890, 0.0034, -0.2015]$| |

| Human capital and education | ||

| |$\kappa$| | Utility weight on time invest. (target: average time invest.) | 0.7310 |

| |$\kappa ^h_j$| | Share of human capital (target: average monetary & slope of time investments) | cf. Online Appendix Figure B1 |

| |$\kappa ^m_j$| | Share of monetary input (target: slope of monetary invest.) | cf. Online Appendix Figure B1 |

| |$\kappa ^g_0$| | Share of government input for age bin 4–6 (target: average time invest. age bin 4–6) | 0.4437 |

| |$\bar{A}$| | Investment scale parameter (target: average HK at age |$j_a$|) | 1.1989 |

| |$\tilde{A}$| | Investment scale parameter in HS (target: average HK at age |$j_{a+1}$|) | 1.0739 |

| |$\phi$| | Utility costs |$s=hs$| (target: fraction of group |$s=hs$|) | 0.0561 |

| |$\tilde{\varrho }(s^p=no)=\tilde{\varrho }(s^p=hs)$| | Utility costs |$s={ {co}}, s^p=no \wedge s^p=hs$| (target: fraction of group |$s=co$|) | 1.2120 |

| |$\tilde{\varrho }(s^p=co)$| | Utility costs |$s={ {co}}, s^p=co$| (target: conditional fraction of group |$s=co$|) | 0.1707 |

| Government policy | ||

| |$\lambda$| | Level parameter of HSV tax function (balance government budget) | 0.8880 |

| |$\rho ^p$| | Pension replacement rate (balance social security budget) | 0.1893 |

Notes: Second-stage parameters calibrated endogenously by targeting selected data moments.

Second-Stage Calibration Parameters.

| Parameter | Interpretation | Value |

|---|---|---|

| Preferences | ||

| |$\beta$| | Time discount rate (target: asset to income ratio, ages 25–60) | 0.9808 |

| |$\nu$| | Altruism parameter (target: average IVT per child) | 0.8380 |

| Labour productivity | ||

| |$\rho _0(s)$| | Normalisation parameter (target: |$ \mathbb {E} \gamma (s,h)=1$|) | |$[0.1890, 0.0034, -0.2015]$| |

| Human capital and education | ||

| |$\kappa$| | Utility weight on time invest. (target: average time invest.) | 0.7310 |

| |$\kappa ^h_j$| | Share of human capital (target: average monetary & slope of time investments) | cf. Online Appendix Figure B1 |

| |$\kappa ^m_j$| | Share of monetary input (target: slope of monetary invest.) | cf. Online Appendix Figure B1 |

| |$\kappa ^g_0$| | Share of government input for age bin 4–6 (target: average time invest. age bin 4–6) | 0.4437 |

| |$\bar{A}$| | Investment scale parameter (target: average HK at age |$j_a$|) | 1.1989 |

| |$\tilde{A}$| | Investment scale parameter in HS (target: average HK at age |$j_{a+1}$|) | 1.0739 |

| |$\phi$| | Utility costs |$s=hs$| (target: fraction of group |$s=hs$|) | 0.0561 |

| |$\tilde{\varrho }(s^p=no)=\tilde{\varrho }(s^p=hs)$| | Utility costs |$s={ {co}}, s^p=no \wedge s^p=hs$| (target: fraction of group |$s=co$|) | 1.2120 |

| |$\tilde{\varrho }(s^p=co)$| | Utility costs |$s={ {co}}, s^p=co$| (target: conditional fraction of group |$s=co$|) | 0.1707 |

| Government policy | ||

| |$\lambda$| | Level parameter of HSV tax function (balance government budget) | 0.8880 |

| |$\rho ^p$| | Pension replacement rate (balance social security budget) | 0.1893 |

| Parameter | Interpretation | Value |

|---|---|---|

| Preferences | ||

| |$\beta$| | Time discount rate (target: asset to income ratio, ages 25–60) | 0.9808 |

| |$\nu$| | Altruism parameter (target: average IVT per child) | 0.8380 |

| Labour productivity | ||

| |$\rho _0(s)$| | Normalisation parameter (target: |$ \mathbb {E} \gamma (s,h)=1$|) | |$[0.1890, 0.0034, -0.2015]$| |

| Human capital and education | ||

| |$\kappa$| | Utility weight on time invest. (target: average time invest.) | 0.7310 |

| |$\kappa ^h_j$| | Share of human capital (target: average monetary & slope of time investments) | cf. Online Appendix Figure B1 |

| |$\kappa ^m_j$| | Share of monetary input (target: slope of monetary invest.) | cf. Online Appendix Figure B1 |

| |$\kappa ^g_0$| | Share of government input for age bin 4–6 (target: average time invest. age bin 4–6) | 0.4437 |

| |$\bar{A}$| | Investment scale parameter (target: average HK at age |$j_a$|) | 1.1989 |

| |$\tilde{A}$| | Investment scale parameter in HS (target: average HK at age |$j_{a+1}$|) | 1.0739 |

| |$\phi$| | Utility costs |$s=hs$| (target: fraction of group |$s=hs$|) | 0.0561 |

| |$\tilde{\varrho }(s^p=no)=\tilde{\varrho }(s^p=hs)$| | Utility costs |$s={ {co}}, s^p=no \wedge s^p=hs$| (target: fraction of group |$s=co$|) | 1.2120 |

| |$\tilde{\varrho }(s^p=co)$| | Utility costs |$s={ {co}}, s^p=co$| (target: conditional fraction of group |$s=co$|) | 0.1707 |

| Government policy | ||

| |$\lambda$| | Level parameter of HSV tax function (balance government budget) | 0.8880 |

| |$\rho ^p$| | Pension replacement rate (balance social security budget) | 0.1893 |

Notes: Second-stage parameters calibrated endogenously by targeting selected data moments.

2.1. Age Brackets

The model is calibrated at a biannual frequency. We initialise the parental economic life cycle when their children are of age four, model age |$j=0$|. The reason for this initialisation age is the calibration of the initial human capital endowment |$h(j=0)$|, which is informed by data on test score measures at child biological ages three to five. Thus, children are irrelevant to the economic model for the first three years of their biological lives. Parental age at the economic ‘birth’ of children is |$j_f=14$|, which we also refer to as ‘fertility’ age. This corresponds to a biological age of thirty-two, when children are of biological age four.8 Children make the higher eduction decisions at biological age sixteen, model age |$j_a=6$|. Children who complete high school stay in school for one additional model period; thus, high school is completed at |$j_h=7$|. Children who attend college stay in college for two model periods; thus, college is completed at |$j_c=9$|. Retirement is at exogenous age |$j_r=31$|, corresponding to biological age sixty-six. Households live at most with certainty until age |$J=38$|, biological age eighty.

2.2. Prices and Income Process

We normalise wages to |$w=1$| and set the interest rate to an annual rate of |$4\%$| based on Siegel (2002). The calibration of the stochastic wage process based on PSID data involves a standard calibration of the temporary and permanent shock distributions based on GMM estimates, described in detail in Online Appendix Section B.2.

2.3. Preferences

When children live in the parental household, we have |$x={[\ell (m)+ \kappa \cdot \xi (m,s) \cdot i^t ]}/{(1+\mathbf {1}_{m=ma} )}$|. Here |$\ell (m)$| is the hours worked by marital status, which we estimate from the data, giving annual hours of |$\ell ({ {si}})=1868$| and |$\ell (ma)=3810$|. The time cost parameter |$\kappa$| is calibrated to match average time investments by parents into the education of children, giving |$\kappa =0.74$|.

We calibrate the parameters of the cost function to match education shares in the data for the three groups |$s \in \lbrace { {no}, {hs}, {co}}\rbrace$|. We measure these shares for adults older than age twenty-two—which is the labour market entry age of all education groups in the model—and younger than age thirty-eight based on the PSID waves 2011, 2013, 2015 and 2017.9 Parameter |$\phi$| is calibrated to match the fraction of children without a high-school degree of 12.16%, giving |$\phi =0.06$|. With regard to the additional utility costs during the college period we restrict |$\tilde{\varrho }(no)=\tilde{\varrho }(hs)$| and calibrate it to match the fraction of children with a college degree of 33.21%, giving |$\tilde{\varrho }(no)=\tilde{\varrho }(hs)=1.21$|. Finally, parameter |$\tilde{\varrho }(s^p=co)$| is calibrated to match the fraction of children in college conditional on parents having a college degree of 63.3%, cf. Krueger and Ludwig (2016), giving |$\tilde{\varrho }(co)=0.17$|.

Households discount utility at rate |$\beta$|. We follow Busch and Ludwig (2020) and calibrate it to match the assets to income ratio in the PSID for ages twenty-five to sixty, giving |$\beta =0.98$| annually.

Utility of future generations is additionally discounted at rate |$\nu$|, chosen so that the average per-child inter vivos transfer is $61,200, as implied by the Rosters and Transfers supplement to the PSID,10 giving |$\nu =0.84$|.

2.4. Initial Distribution of Parents

For the initial distributions of parents at the fertility age, we restrict the sample to parents aged 25–35, leaving us with 3,024 observations.11

Marital status. Marital status is measured by the legal status of parents. This gives a share of singles of |$52\%$| and a share of married households of |$48\%$|.

Education categories. We group the data by years of education of household heads older than age twenty-two. Less than high school, |$s={ {no}}$|, is for less than twelve years of formal education. High-school completion (but no college) is for more than twelve but less than sixteen years of education. College is at least sixteen years of education. The population shares of parents in the three education categories by their marital status are summarised in columns 2 and 3 of Table 5.12

Household Shares and Characteristics by Education and Marital Status.

| % fraction of households | No. of children | Lower asset limit | ||||

|---|---|---|---|---|---|---|

| Education |$s$|/marital status |$m$| | |$si$| | |$ma$| | |$si$| | |$ma$| | |$si$| | |$ma$| |

| |${ {no}}$| | 0.2194 | 0.1621 | 2.36 | 2.33 | −2,380 | −18,931 |

| |$hs$| | 0.6064 | 0.5577 | 1.86 | 2.15 | −33,065 | −51,332 |

| |${ {co}}$| | 0.1742 | 0.2802 | 1.77 | 1.96 | −60,037 | −43,629 |

| % fraction of households | No. of children | Lower asset limit | ||||

|---|---|---|---|---|---|---|

| Education |$s$|/marital status |$m$| | |$si$| | |$ma$| | |$si$| | |$ma$| | |$si$| | |$ma$| |

| |${ {no}}$| | 0.2194 | 0.1621 | 2.36 | 2.33 | −2,380 | −18,931 |

| |$hs$| | 0.6064 | 0.5577 | 1.86 | 2.15 | −33,065 | −51,332 |

| |${ {co}}$| | 0.1742 | 0.2802 | 1.77 | 1.96 | −60,037 | −43,629 |

Notes: Columns 2 and 3 show fractions with education |$s \in \lbrace { {no}, {hs}, {co}}\rbrace$| by marital status. Columns 4 and 5 show numbers of children, and columns 6 and 7 lower asset limits for parents at model age |$j_f$|, expressed in 2010 dollars, by marital status and education.

Household Shares and Characteristics by Education and Marital Status.

| % fraction of households | No. of children | Lower asset limit | ||||

|---|---|---|---|---|---|---|

| Education |$s$|/marital status |$m$| | |$si$| | |$ma$| | |$si$| | |$ma$| | |$si$| | |$ma$| |

| |${ {no}}$| | 0.2194 | 0.1621 | 2.36 | 2.33 | −2,380 | −18,931 |

| |$hs$| | 0.6064 | 0.5577 | 1.86 | 2.15 | −33,065 | −51,332 |

| |${ {co}}$| | 0.1742 | 0.2802 | 1.77 | 1.96 | −60,037 | −43,629 |

| % fraction of households | No. of children | Lower asset limit | ||||

|---|---|---|---|---|---|---|

| Education |$s$|/marital status |$m$| | |$si$| | |$ma$| | |$si$| | |$ma$| | |$si$| | |$ma$| |

| |${ {no}}$| | 0.2194 | 0.1621 | 2.36 | 2.33 | −2,380 | −18,931 |

| |$hs$| | 0.6064 | 0.5577 | 1.86 | 2.15 | −33,065 | −51,332 |

| |${ {co}}$| | 0.1742 | 0.2802 | 1.77 | 1.96 | −60,037 | −43,629 |

Notes: Columns 2 and 3 show fractions with education |$s \in \lbrace { {no}, {hs}, {co}}\rbrace$| by marital status. Columns 4 and 5 show numbers of children, and columns 6 and 7 lower asset limits for parents at model age |$j_f$|, expressed in 2010 dollars, by marital status and education.

Demographics. The number of children by marital status and education of parents |$\xi (m,s)$| is computed as the average number of children living in households with household heads aged 25–35; cf. columns 4 and 5 of Table 5.

2.5. Acquired Human Capital and Earnings

2.6. Human Capital Production Function

Initial human capital. For calibration of the distribution of initial human capital |$h_0(s_p,m_p)$|, we recur to the Letter Word test score distribution in the PSID CDS surveys I–III, and match it to parental characteristics by merging the survey waves with the PSID.

Online Appendix Table B3 reports the joint distribution of average test scores of the children by parental education and marital status. We base the calibration of the initial ability distribution of children on this data by drawing six different types of children depending on the combination of marital status and parental education.15 Children’s initial human capital is normalised as the test score of that |$m^p,s^p$|-group relative to the average test score. We further scale the resulting number by the calibration parameter |$\bar{h}_0$| and, thus, initial human capital of the children is a multiple of |$\bar{h}_0$|. Parameter |$\bar{h}_0$| is calibrated exogenously to match the ratio of mean test scores at ages 3–5 to mean test scores at ages 16–17, which gives |$\bar{h}_0=0.125$|. Initial abilities relative to average abilities and the corresponding multiples of |$\bar{h}_0$| for the six types are contained in Table B3 of Online Appendix B.

In the second nest, we set the substitution elasticity |$\sigma ^g$| between private and government investments to |$\sigma ^g = 2.43$|, estimated by Kotera and Seshadri (2017)—who estimated the parameters of a CES nesting of private and public education investments similar to ours based on US data. Thus, parental and government investments are gross substitutes, but substitution across these education inputs is far from perfect. Since this elasticity of substitution is a crucial parameter, we show sensitivity of the results with respect to it in Section 5. We restrict |$\kappa ^g_j=\bar{\kappa }^g$| for |$j \gt 0$| and calibrate it exogenously again according to the estimates by Kotera and Seshadri (2017), giving |$\bar{\kappa }^g=0.676$|. At biological age four of the child, children are still in kindergarten, and we separately calibrate |$\kappa ^g_{0}$| to match the average time investments by parents into their children at that age. This gives |$\kappa ^g_0 = 0.44$|. By |$\bar{A}$| we denote a computational normalisation parameter that we choose such that average acquired human capital is equal to 1, sufficiently below the maximum human capital gridpoint, giving |$\bar{A}=1.20$|.

2.7. College Tuition Costs and Borrowing Constraint of Children

2.8. Government

The government side features the budget of the general tax and transfer system and a separate budget of the pension system, all set to mimic the US system. In the general budget the revenue side is represented by consumption, capital income and progressive labour income taxes. Details of the calibration are given in Online Appendix Section B.5.

Exogenous government spending (net of spending on education) is set to |$G/Y \%= 13.8\%$|. In addition, the government spends on schooling for children and pays the college subsidy for college students. The former we approximate as $5,000 per pupil based on UNESCO (1999–2005) data, as for example in Holter (2015). The latter is set to |$38.8\%$| of average gross tuition costs, as in Krueger and Ludwig (2016). Assuming, as in Krueger and Ludwig (2016), that the difference between net and gross tuition costs is due to both a public and a private subsidy with the latter not being explicitly modelled in our setup19 gives an average public subsidy of |$\$ 6,119$| per student.

2.9. Evaluating Non-Targeted Predictions of the Model

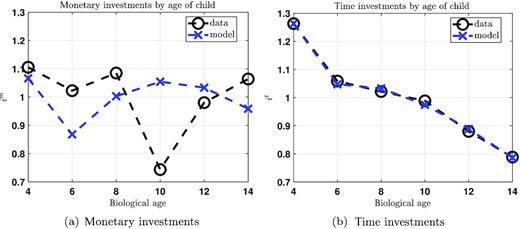

2.9.1. Time and resource investments

Figure 2 shows average time and monetary investments in the model and the data by child age. The good match of the model of time investments in panel (b) is a consequence of calibration since this is a targeted profile through age-dependent parameter |$\kappa ^h_j$| and parameter |$\kappa ^g_0$|. Monetary investments in panel (a) are slightly downward sloping in the data, and we match the lower slope of monetary investments compared to time investments through the age dependency of |$\kappa ^m_j$|.

Monetary and Time Investments by Age of Child.

Notes: Average monetary and time investments by children’s biological age in the data (black circles) and model (blue crosses).

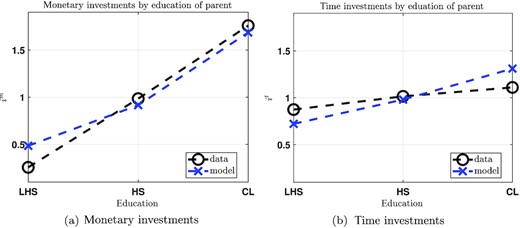

Figure 3 shows the analogous output by parental education levels, all of which are not targeted in the calibration. The model matches well the positive slope of both types of investment in parental education. Since income and initial wealth of a household is increasing in the household’s education, it is perhaps not surprising that more highly educated parents invest significantly more resources in each child, especially since these households have fewer children. The same observation (number of children decreasing in household education) is also responsible for the mildly increasing per-child time investment by parental education (see Figure 3(b)).

Monetary and Time Investments by Education of Parents.

Notes: Average monetary and time investments by parents’ education in the data (black circles) and model (blue crosses). LHS, less than high school (|$s={ {no}}$|); HS, high school (|$s=hs$|); CL, college (|$s=co$|).

2.9.2. Intergenerational persistence in education

In our calibration we also do not target directly any measure of intergenerational persistence in education. We measure this persistence by the regression coefficient |$\beta _1$| in a regression of the education of a child on parental education, |$s = \beta _0 + \beta _1 s^p + \epsilon$|. In this regression we form two groups, non-college for |$s \in \lbrace no,hs\rbrace$| and |$s^p \in \lbrace no,hs\rbrace$|, and college for |$s=co$| and |$s^p=co$|. Standard estimates of intergenerational education persistence according to this metric range from 0.4 to 0.5 and our (non-targeted) coefficient estimate of |$\beta _1=0.47$| is in that range.20

2.9.3. Evidence on the long-run earnings impact of school closures

Our model implies a significant decline of incomes for children affected by the closure of schools. We are not aware of any empirical evidence on the effects of school closures on long-run outcomes of children in the United States and therefore resort to the reduced-form evidence of Jaume and Willén (2019) on the effects of teacher strikes in Argentina between 1983 and 2014 on long-run economic outcomes of the affected children. Their main estimates refer to the closing of primary schools by half a year, and they report that this leads to a reduction of wages at ages 30–40 by about |$2\%\!{-}\!3\%$|. In our model, we consider for our main experiment an exogenous reduction of investments by the government corresponding to a school closure by a year, but in a sensitivity analysis also report results for half year school closures. In that experiment our model predicts an average wage loss at biological ages 30–40 for children who were of biological age six in the period of the lockdown of −1.21%, which is around one-half the size of the estimates from Jaume and Willén (2019), for a different country in a different time period.

2.9.4. Time investment into children during the COVID-19 crisis

Finally, our calibration implies that the time investment response of parents in our full experiment—where government education investments |$i^g$| are reduced and where parental households are both subject to a negative productivity shock and a negative hours worked shock calibrated as described above—translates to 1.17 hours per day of increased time investments into children during the period of the lockdown of schools.21 This lies well in the range of estimates provided on the basis of real-time surveys by Adams-Prassl et al. (2020).

3. Aggregate Consequences of the School Closures

In this section, we start out analysing the average consequences of the school closures for human capital accumulation, educational attainment, earnings and ultimately welfare of children. We then describe the optimal parental reactions, analyse their importance in counteracting the negative effects of the school closures and their welfare effects for the parents.

3.1. Human Capital Losses, Educational Attainment and Earnings

The lockdown of schools leads to a decline in educational attainment when the children affected by the COVID crisis today make their tertiary education decisions at age sixteen. As Table 6 (second column) shows, across all age cohorts the share of children that will end up dropping out of high school (i.e., choosing |$s={ {no}}$|) increases by 1.92 percentage points, and the share of college-educated children will decline by |$-2.34$| percentage points. While these shifts do not appear to be dramatic, they correspond to a |$16\%$| increase in the share of children without high-school degrees, and a |$-7\%$| decrease in the share of college-educated children.

Aggregate Outcomes for Main Experiments.

| Baseline | Change for children of biological age | |||||||

|---|---|---|---|---|---|---|---|---|

| Average | 4 | 6 | 8 | 10 | 12 | 14 | ||

| Change in percentage points | ||||||||

| Share |$s={ {no}}$| | 12.07 | 1.92 | 1.66 | 3.08 | 2.40 | 1.85 | 1.44 | 1.12 |

| Share |$s=hs$| | 54.64 | 0.41 | 0.10 | −0.13 | 0.35 | 0.63 | 0.76 | 0.78 |

| Share |$s=co$| | 33.30 | −2.34 | −1.75 | −2.95 | −2.74 | −2.49 | −2.20 | −1.89 |

| Change in percentages | ||||||||

| Average HK | 1.00 | −3.32 | −2.92 | −4.34 | −3.85 | −3.38 | −2.92 | −2.48 |

| PDV gross earn | $846,473 | −2.10 | −1.82 | −2.73 | −2.44 | −2.15 | −1.87 | −1.59 |

| PDV net earn | $696,076 | −1.68 | −1.45 | −2.20 | −1.96 | −1.72 | −1.49 | −1.26 |

| Child CEV | 0.00 | −1.21% | −1.09% | −1.57% | −1.40% | −1.23% | −1.07% | −0.91% |

| Baseline | Change for children of biological age | |||||||

|---|---|---|---|---|---|---|---|---|

| Average | 4 | 6 | 8 | 10 | 12 | 14 | ||

| Change in percentage points | ||||||||

| Share |$s={ {no}}$| | 12.07 | 1.92 | 1.66 | 3.08 | 2.40 | 1.85 | 1.44 | 1.12 |

| Share |$s=hs$| | 54.64 | 0.41 | 0.10 | −0.13 | 0.35 | 0.63 | 0.76 | 0.78 |

| Share |$s=co$| | 33.30 | −2.34 | −1.75 | −2.95 | −2.74 | −2.49 | −2.20 | −1.89 |

| Change in percentages | ||||||||

| Average HK | 1.00 | −3.32 | −2.92 | −4.34 | −3.85 | −3.38 | −2.92 | −2.48 |

| PDV gross earn | $846,473 | −2.10 | −1.82 | −2.73 | −2.44 | −2.15 | −1.87 | −1.59 |

| PDV net earn | $696,076 | −1.68 | −1.45 | −2.20 | −1.96 | −1.72 | −1.49 | −1.26 |

| Child CEV | 0.00 | −1.21% | −1.09% | −1.57% | −1.40% | −1.23% | −1.07% | −0.91% |

Notes: Share |$s \in \lbrace { {no}, {hs}, {co}}\rbrace$|, the education share in each respective education category where |$s={ {no}}$| denotes less than high school, |$s=hs$| denotes high school and |$s=co$| denotes college. Average HK, the average acquired human capital at age sixteen; PDV gross earn, the present discounted value of gross earnings assuming labour market entry at age twenty-two and retirement at age sixty-six; PDV net earn, present discounted value of net earnings; CEV, consumption equivalent variation. Columns for biological ages 4–14 show the respective percentage point changes of education shares, the percentage changes of acquired human capital and average earnings, and the CEV expressed as a percentage change, for children at various ages at the time of the school closures. Column ‘Average’ gives the respective average response. The CEV is the consumption equivalent variation of welfare measure (5).

Aggregate Outcomes for Main Experiments.

| Baseline | Change for children of biological age | |||||||

|---|---|---|---|---|---|---|---|---|

| Average | 4 | 6 | 8 | 10 | 12 | 14 | ||

| Change in percentage points | ||||||||

| Share |$s={ {no}}$| | 12.07 | 1.92 | 1.66 | 3.08 | 2.40 | 1.85 | 1.44 | 1.12 |

| Share |$s=hs$| | 54.64 | 0.41 | 0.10 | −0.13 | 0.35 | 0.63 | 0.76 | 0.78 |

| Share |$s=co$| | 33.30 | −2.34 | −1.75 | −2.95 | −2.74 | −2.49 | −2.20 | −1.89 |

| Change in percentages | ||||||||

| Average HK | 1.00 | −3.32 | −2.92 | −4.34 | −3.85 | −3.38 | −2.92 | −2.48 |

| PDV gross earn | $846,473 | −2.10 | −1.82 | −2.73 | −2.44 | −2.15 | −1.87 | −1.59 |

| PDV net earn | $696,076 | −1.68 | −1.45 | −2.20 | −1.96 | −1.72 | −1.49 | −1.26 |

| Child CEV | 0.00 | −1.21% | −1.09% | −1.57% | −1.40% | −1.23% | −1.07% | −0.91% |

| Baseline | Change for children of biological age | |||||||

|---|---|---|---|---|---|---|---|---|

| Average | 4 | 6 | 8 | 10 | 12 | 14 | ||

| Change in percentage points | ||||||||

| Share |$s={ {no}}$| | 12.07 | 1.92 | 1.66 | 3.08 | 2.40 | 1.85 | 1.44 | 1.12 |

| Share |$s=hs$| | 54.64 | 0.41 | 0.10 | −0.13 | 0.35 | 0.63 | 0.76 | 0.78 |

| Share |$s=co$| | 33.30 | −2.34 | −1.75 | −2.95 | −2.74 | −2.49 | −2.20 | −1.89 |

| Change in percentages | ||||||||

| Average HK | 1.00 | −3.32 | −2.92 | −4.34 | −3.85 | −3.38 | −2.92 | −2.48 |

| PDV gross earn | $846,473 | −2.10 | −1.82 | −2.73 | −2.44 | −2.15 | −1.87 | −1.59 |

| PDV net earn | $696,076 | −1.68 | −1.45 | −2.20 | −1.96 | −1.72 | −1.49 | −1.26 |

| Child CEV | 0.00 | −1.21% | −1.09% | −1.57% | −1.40% | −1.23% | −1.07% | −0.91% |

Notes: Share |$s \in \lbrace { {no}, {hs}, {co}}\rbrace$|, the education share in each respective education category where |$s={ {no}}$| denotes less than high school, |$s=hs$| denotes high school and |$s=co$| denotes college. Average HK, the average acquired human capital at age sixteen; PDV gross earn, the present discounted value of gross earnings assuming labour market entry at age twenty-two and retirement at age sixty-six; PDV net earn, present discounted value of net earnings; CEV, consumption equivalent variation. Columns for biological ages 4–14 show the respective percentage point changes of education shares, the percentage changes of acquired human capital and average earnings, and the CEV expressed as a percentage change, for children at various ages at the time of the school closures. Column ‘Average’ gives the respective average response. The CEV is the consumption equivalent variation of welfare measure (5).

The reason for the reallocation towards lower final educational attainment is the reduction in the amount of human capital the average child arrives with at age sixteen, which falls by |$-3.3\%$|. As Table 7, first column, demonstrates, in response to the COVID-19 school closures, parents increase their private investments into children, both in terms of resources as well as in terms of time. However, as discussed in greater detail below, this reaction is not sufficient to fully compensate the loss of government inputs into human capital production in the form of schooling. Consequently, average human capital at age sixteen is lower than without the COVID-19 school closure shock, and the children affected by the shock choose on average lower educational attainment. The lower educational attainment together with the lower human capital in turn imply losses in the average discounted value of gross lifetime earnings by |$-2.1\%$|; see the fifth row of Table 6. Thus, a transitory shock of closed schools for one year alone leads to a permanent reduction in long-term earnings by more than 2% for the affected children, on average, even after taking optimal parental adjustments into account. In terms of present discounted dollars, this corresponds to an average per-person loss of $17,776 dollars in year 2019 prices.

Parental Decisions.

| Baseline | % change for children of biological age | |||||||

|---|---|---|---|---|---|---|---|---|

| Average | 4 | 6 | 8 | 10 | 12 | 14 | ||

| Panel A: in the period of school closures | ||||||||

| Average monetary invest. | $1,385 | 35.44 | 23.73 | 38.08 | 36.72 | 36.77 | 37.82 | 39.51 |

| Average time invest. | 25.17 | 16.62 | 10.78 | 17.40 | 16.90 | 17.17 | 18.04 | 19.44 |

| Panel B: averages over remaining childhood | ||||||||

| Average monetary invest. | $1,381 | 14.06 | 2.90 | 5.37 | 7.49 | 11.01 | 18.08 | 39.51 |

| Average time invest. | 22.56 | 6.73 | 1.31 | 2.37 | 3.44 | 5.16 | 8.64 | 19.44 |

| Average IVT | $61,255 | 0.73 | 0.43 | 1.79 | 1.11 | 0.64 | 0.31 | 0.11 |

| Baseline | % change for children of biological age | |||||||

|---|---|---|---|---|---|---|---|---|

| Average | 4 | 6 | 8 | 10 | 12 | 14 | ||

| Panel A: in the period of school closures | ||||||||

| Average monetary invest. | $1,385 | 35.44 | 23.73 | 38.08 | 36.72 | 36.77 | 37.82 | 39.51 |

| Average time invest. | 25.17 | 16.62 | 10.78 | 17.40 | 16.90 | 17.17 | 18.04 | 19.44 |

| Panel B: averages over remaining childhood | ||||||||

| Average monetary invest. | $1,381 | 14.06 | 2.90 | 5.37 | 7.49 | 11.01 | 18.08 | 39.51 |

| Average time invest. | 22.56 | 6.73 | 1.31 | 2.37 | 3.44 | 5.16 | 8.64 | 19.44 |

| Average IVT | $61,255 | 0.73 | 0.43 | 1.79 | 1.11 | 0.64 | 0.31 | 0.11 |

Notes: In panel A we present columns for biological ages 4–14 that show the percentage changes in monetary investments and time investments in the period of the school closures. In panel B we present columns for biological ages 4–14 that show the percentage changes in monetary investments, time investments and inter vivos transfers for children at various ages at the time of the school closures. For monetary and time investments, these are averages of the percentage changes of the respective investment over the remaining life cycle, so, e.g., for a child of age six, the percentage change is the average of the percentage changes of investments at ages 6–14 for this child. Column ‘Average’ is the raw average across the biological ages of children.

Parental Decisions.

| Baseline | % change for children of biological age | |||||||

|---|---|---|---|---|---|---|---|---|

| Average | 4 | 6 | 8 | 10 | 12 | 14 | ||

| Panel A: in the period of school closures | ||||||||

| Average monetary invest. | $1,385 | 35.44 | 23.73 | 38.08 | 36.72 | 36.77 | 37.82 | 39.51 |

| Average time invest. | 25.17 | 16.62 | 10.78 | 17.40 | 16.90 | 17.17 | 18.04 | 19.44 |

| Panel B: averages over remaining childhood | ||||||||

| Average monetary invest. | $1,381 | 14.06 | 2.90 | 5.37 | 7.49 | 11.01 | 18.08 | 39.51 |

| Average time invest. | 22.56 | 6.73 | 1.31 | 2.37 | 3.44 | 5.16 | 8.64 | 19.44 |

| Average IVT | $61,255 | 0.73 | 0.43 | 1.79 | 1.11 | 0.64 | 0.31 | 0.11 |

| Baseline | % change for children of biological age | |||||||

|---|---|---|---|---|---|---|---|---|

| Average | 4 | 6 | 8 | 10 | 12 | 14 | ||

| Panel A: in the period of school closures | ||||||||

| Average monetary invest. | $1,385 | 35.44 | 23.73 | 38.08 | 36.72 | 36.77 | 37.82 | 39.51 |

| Average time invest. | 25.17 | 16.62 | 10.78 | 17.40 | 16.90 | 17.17 | 18.04 | 19.44 |

| Panel B: averages over remaining childhood | ||||||||

| Average monetary invest. | $1,381 | 14.06 | 2.90 | 5.37 | 7.49 | 11.01 | 18.08 | 39.51 |

| Average time invest. | 22.56 | 6.73 | 1.31 | 2.37 | 3.44 | 5.16 | 8.64 | 19.44 |

| Average IVT | $61,255 | 0.73 | 0.43 | 1.79 | 1.11 | 0.64 | 0.31 | 0.11 |

Notes: In panel A we present columns for biological ages 4–14 that show the percentage changes in monetary investments and time investments in the period of the school closures. In panel B we present columns for biological ages 4–14 that show the percentage changes in monetary investments, time investments and inter vivos transfers for children at various ages at the time of the school closures. For monetary and time investments, these are averages of the percentage changes of the respective investment over the remaining life cycle, so, e.g., for a child of age six, the percentage change is the average of the percentage changes of investments at ages 6–14 for this child. Column ‘Average’ is the raw average across the biological ages of children.