Abstract

This article analyses the effects of financialisation on non-financial companies’ (NFCs) investment and explores the interactions between financialisation and the structural and institutional features of developing and emerging economies (DEEs). We estimate the effects of financialisation on physical investment for a sample of DEEs using panel data based on the balance sheets of publicly listed NFCs. Our main contribution is to assess the interactions between the financialisation of the NFCs and country-level financial development, financial reform, capital account openness and global value chain participation. We find that the effects of the financialisation of the NFCs in DEEs are highly context specific. Stock market development, financial reforms for liberalisation, capital account openness and participation in the global value chains are associated with more pronounced negative effects of financialisation on investment. Our analysis provides novel empirical evidence regarding the sources of variation in the financialisation of corporations in DEEs.

1. Introduction

The last decades have witnessed ‘financialisation’ as a central phenomenon in the evolution of economies. Financialisation has been summarised as an ongoing and self-reinforcing economic and social process that manifests itself in the growing prominence and influence of behaviours derived from the financial sector (Epstein, 2005). Van der Zwan (2014) highlights three main features of this process: (i) a new regime of accumulation largely shaped around financial motives, (ii) the consolidation of the ‘shareholder value’ as the key principle in corporate governance and (iii) rising influence of finance within everyday life (pension schemes, mortgages, healthcare etc.). This article aims at analysing the impact of financialisation on investment in the context of developing and emerging economies (DEEs) with a focus on the first two aspects.

Despite a growing theoretical literature on the effects of financialisation on physical investment, the empirical analysis is mainly focused on developed countries. However, ‘the growing influence of financial markets and institutions, known as “financialization”, affects how wealth is produced and distributed’ (UNCTAD, 2015, p. 27) also in the context of DEEs. Demir (2007, 2009) analyse the negative impacts of financialisation on investment taking into account financial liberalisation for a set of emerging countries, while Seo et al. (2012) provide similar evidence about Korean non-financial corporations’ (NFCs) Research and Development (R&D) investments. Hecht (2014) presents a comparative analysis of the effects of financialisation on the NFCs in advanced and large developing economies, also testing competing heterodox theories on the effects of financialisation on investment.

In the development literature, the effect of financialisation on uneven international development has been highlighted (Becker et al., 2010; Bonizzi, 2013). Karwowski and Stockhammer (2016) compare macroeconomic aspects of financialisation (e.g. financial deregulation, financial inflows, business and household debt levels) in emerging economies and find a considerable degree of variability in the intensity of financialisation, in line with the ‘varieties of financialisation’ observed across the developed countries (Lapavitsas and Powell, 2013; Karwowski et al., 2019). Bonizzi et al. (2020, 2022) highlight the subordinate position of DEEs within the global hierarchy of financial and production relations, which shapes and consolidate different forms of financialisation in DEEs, ultimately benefiting the top of the pyramid in which developed country multinationals can consolidate their dominant position.

This paper contributes to the literature on the financialisation of the DEEs’ NFCs by shedding light on the under-analysed specific forms of financialisation in the emerging capitalist countries, considering the key aspects of financial liberalisation and the hierarchical nature of international production relations. The aim is to provide an empirical substantiation to the claims of the variegated/subordinate financialisation literature with a focus on the financialisation of the NFCs, in particular by analysing the relations between financial and productive subordination.

Our analysis builds on and integrates these two strands of literature in two aspects by providing (i) micro-econometric evidence on the effects of financialisation on investment using firm-level data for a fairly comprehensive sample of DEEs and (ii) a variegated analysis of the interaction of the structural and institutional features of the country and the process of financialisation.

We confirm the negative effects of financialisation on investment for a comprehensive sample of DEEs, and we identify the key dimensions along which this relationship differs across countries. Our results suggest a significant interaction between country-level structural and institutional features and firm-level financialisation. Although at the aggregate level the negative effects of financialisation on investment in DEEs are similar to what has been found for developed countries (although with some differences), our disaggregated analyses point to novel findings. We find that both higher degrees of financial liberalisation and stronger stock market development are associated with significant negative effects of financialisation. Similarly, a higher degree of capital account openness is associated with stronger negative effects of financialisation on the NFCs’ investment. In addition, the investment of NFCs in countries that are relatively more integrated within the Global Value Chain (GVC) suffers more from an overall negative effect of firm-level financialisation. Our results provide useful insights for policy debates regarding the role and capacity of the DEEs’ governments to mitigate the effects of national and regional processes of financialisation on investment.

The rest of the article is organised as follows. Section 2 reviews the literature on the financialisation of investment with a focus on DEEs. Section 3 presents our econometric model. Section 4 introduces the data, key stylised facts, and the estimation methodology. Section 5 discusses the estimation results. Section 6 concludes.

2. Investment, financialisation and development

From a mainstream perspective, the liberalisation and growth of financial markets are expected to facilitate the financing and efficient allocation of investment (Beck et al., 2000; Beck and Levine, 2004; Love, 2003; Levine, 2005).

However, post-Keynesian research highlight the negative impacts of an expanding financial sector on income distribution and demand (Onaran et al., 2010; Hein, 2015), and in particular on investment, providing evidence that increasing engagement of the NFCs with financial markets in the developed countries has decreased their investment (Stockhammer, 2004; Orhangazi, 2008; Cordonnier and Van de Velde, 2015; Davis, 2018; Tori and Onaran, 2018, 2020, among others).

The financialisation of the NFCs is a phenomenon that became evident also in the context of developing countries. In the last decades, there has been a general decline in investment as a ratio to profits, and an increase in dividends as a ratio to profits, financial assets as a ratio to total assets and debt ratios (UNCTAD, 2016). Regarding DEEs, Demir (2007, 2009) finds that financial liberalisation in Argentina, Mexico and Turkey channelled savings from the productive sector towards financial speculation, thus reducing the availability of funds for long-term physical investment and increasing returns on financial assets relative to fixed assets, significantly reduced investment in these emerging market NFCs.

The literature suggests the effects of financialisation depend on the specific institutional context. In this work, we consider various potential institutional factors mediating the effects of financialisation on investment in the context of DEEs following Akkemik and Ozen (2014).

Even though the available evidence depicts financialisation as a phenomenon common to both advanced and developing economies, the different institutional settings at the country and/or regional level reveal the presence of ‘varieties of financialisation’ (see Dore, 2008; Pike and Pollard, 2010; Lapavitsas and Powell, 2013). Moreover, some recent contributions put forward an interpretation of the financialisation process at the global level showing that emerging economies are in a subordinate position with respect to advanced countries, with the latter dominating both the production and financial spheres (Bortz and Kaltenbrunner, 2018; Bonizzi et al., 2020, 2022).

In this paper, we analyse three channels of interaction between the macroeconomic institutional features of DEEs and the financialisation of the NFCs. Our main interest is to explore the associations between country-level macroeconomic institutional features and firm-level investment behaviour in the context of financialisation.

First, we test whether a more developed financial sector reinforces the impact of financialisation on investment in the context of DEEs. The mainstream literature argues that firms with higher financing obstacles experience slower growth, but this relationship is weaker in countries with relatively more developed financial systems, and financial development is more effective in alleviating financing constraints, especially for smaller firms (Beck et al., 2005). However, while some studies find a significant and positive effect of financial development on economic growth and investment (Love, 2003; Hermes and Lensink, 2003; Levine, 2005), both the statistical significance and size of the estimates vary widely due to methodological heterogeneity (Valickova et al., 2015). Alternatively, Tori and Onaran (2020), focusing on European countries, find that the negative effect of financialisation on NFCs’ investment is stronger in countries with a relatively high level of financial development. We assess whether higher levels of activities in the financial markets and intermediaries delinked from the financing requirements incentivise NFCs to engage heavily in non-operating activities, ultimately affecting their investment.

Second, we test whether the effects of financialisation on NFCs’ investment are related to the degree of openness of DEEs. Even though financial ‘development’ and ‘liberalisation’ can be seen as two very interrelated phenomena (Chinn and Ito, 2008), the latter refers to the process of removal of barriers to the international movement of capital flows, while the former identifies changes in different dimensions of financial transactions (e.g. efficiency, depth, stability). Financial liberalisation has a relatively more international feature than financial development. The evidence regarding the effect of financial liberalisation on economic growth has been mixed (see Yanikkaya, 2003). While most of the mainstream contributions argue that capital account liberalisation fosters growth in developing countries (Levine, 2001; Hermes and Lensink, 2003; Wacziarg and Welch, 2008), post-Keynesians highlight the negative effects of international capital flows as the international dimension of financialisation (Stockhammer, 2010; Tyson and McKinley, 2014). Increased access to international markets provides NFCs in DEEs with more financial investment opportunities, e.g. thanks to the ability to exploit interest rate differentials (Bruno and Shin, 2017). However, Demir (2009) shows this had a detrimental effect on NFCs’ investment in Argentina, Mexico and Turkey. Moreover, it has been shown that large shares of capital inflows to DEEs are short-term and speculative (Bortz and Kaltenbrunner, 2018). A relatively more open macroeconomic environment can induce higher volatility, hence opportunities to profit from financial investment. Moreover, more cross-border capital flows can increase the competitive and financial pressures on the NFCs, hence pressure from shareholders. We explore whether a higher degree of openness to capital flows is associated with a stronger effect of financialisation on investment.

Third, we test whether a higher degree of participation in Global Value Chains moderates the effects of financialisation on NFCs’ investment. This hypothesis relates to an important issue raised within the financialisation literature with respect to the relationship between investment and offshoring. Milberg and Winkler (2009) show how the relocation of production outside the domestic boundaries has been one of the main causes of the slowdown in investment in the USA. Recently, Auvray and Rabinovich (2019) provide additional empirical evidence for the US non-energy sectors showing how offshoring and financialisation are intertwined phenomena. The decline in investment in companies based in developed countries is explained by the global nature of production, which is fostering the substitution of tangible capital with intangible capital by companies in developed countries. According to this view, the decline in investment in developed countries should be mirrored by an increase in NFCs’ investment in the DEEs, i.e. a transfer of productive capacity. Do companies operating in the DEEs follow such a similar pattern within a financialised context? We try to shed light on the relationship between GVC participation in DEEs and NFCs’ investment, to provide a fuller picture.

Table 1 summarises the three hypotheses identified above, which we econometrically test in Section 5.

Hypotheses

| H1 | The more developed and liberalised the financial sector of a DEE, the stronger the negative effects of financialisation on NFCs’ investment |

| H2 | The higher the degree of openness to capital flows of a DEE, the stronger the negative effects of financialisation on NFCs’ investment |

| H3 | The higher the degree of participation of a DEE to global value chains, the weaker the negative effects of financialisation on NFCs’ investment |

| H1 | The more developed and liberalised the financial sector of a DEE, the stronger the negative effects of financialisation on NFCs’ investment |

| H2 | The higher the degree of openness to capital flows of a DEE, the stronger the negative effects of financialisation on NFCs’ investment |

| H3 | The higher the degree of participation of a DEE to global value chains, the weaker the negative effects of financialisation on NFCs’ investment |

Hypotheses

| H1 | The more developed and liberalised the financial sector of a DEE, the stronger the negative effects of financialisation on NFCs’ investment |

| H2 | The higher the degree of openness to capital flows of a DEE, the stronger the negative effects of financialisation on NFCs’ investment |

| H3 | The higher the degree of participation of a DEE to global value chains, the weaker the negative effects of financialisation on NFCs’ investment |

| H1 | The more developed and liberalised the financial sector of a DEE, the stronger the negative effects of financialisation on NFCs’ investment |

| H2 | The higher the degree of openness to capital flows of a DEE, the stronger the negative effects of financialisation on NFCs’ investment |

| H3 | The higher the degree of participation of a DEE to global value chains, the weaker the negative effects of financialisation on NFCs’ investment |

While the first hypothesis aims at exploring variegation in financialisation at the firm level, the second refers to degrees of financial subordination and vulnerability. The third hypothesis contextualises financialisation at the firm level within productive subordination. We argue that these three hypotheses summarise the three key aspects (i.e. financial development, capital flows and global productive integration) against which the DEEs’ firm-level investment behaviour should be analysed.

3. The model

This section presents a model of investment building on the post-Keynesian theory of the firm and the alternative specifications, which form the basis of our econometric analysis. According to the Post-Keynesian theory, capital accumulation is an intrinsically dynamic process (Kalecki, 1954; Lopez and Mott, 1999). Physical investment is an irreversible phenomenon. There is a path dependency connecting past and future levels of accumulation, as confirmed by the previous empirical literature (Ford and Poret, 1991; Orhangazi, 2008, Arestis et al., 2012). Therefore, in all the models to be estimated, we include the lagged investment. Also, all other explanatory variables are lagged to depict the adjustment processes.1

To analyse the potential effects of financialisation, we use a basic model of investment building on Orhangazi (2008), which has been further amended by Tori and Onaran (2018, 2020).2 Equation (1) presents the specification of ‘financialised investment’, where the rate of accumulation, I/K, is:

where I is the addition to fixed assets, K is the net capital stock, S is net sales, π operating profit F is the sum of cash dividends and interest paid on debt, while πF is the total non-operating (financial) income as the sum of interest and dividends received by the company, TD is total debt, and TA is total assets. i is the firm index, identifies a set of time dummies to control for unobservable time-specific effects common to all firms in the different estimations, whilst the standard disturbance term εit captures firm-specific fixed effects and idiosyncratic shocks. All variables are introduced in the first lag to reflect the time consideration in the investment plans. Firm-specific dummy variables are not considered since this specification is estimated in first differences. The operating income/fixed assets ratio is a measure of internal funds availability, the sales/fixed assets ratio is a proxy reflecting capacity utilisation, financial payments/fixed assets and non-operating income/fixed assets are the two measures of the impact of financialisation.

Investment behaviour is influenced by expectations about future profitability. However, in an environment characterised by ‘uncertainty’ (Kregel, 1976), companies use past performances (in terms of profitability and demand levels) to inform their current and future investment spending. For this reason, we expect a positive effect of the variables measuring demand (sales), internal funds (operating income) and the lagged level of investment on current investment.

The discussion is more complex for the expected signs of financial payments and profits, and total debt. The composite measure for outward financialisation, F, which is the sum of interest and dividend payments (as a ratio to K), captures: (i) the liquidity effect of interest payments and (ii) the effect of the Shareholder Value Orientation (SVO).3 Unfortunately, the Worldscope database does not provide a sufficient number of observations about another central phenomenon within the financialisation of NFCs, namely ‘share buybacks’ (see Krippner, 2005). Although this is a limitation of our analysis, it is worth noting that the practice of share buybacks (or share repurchases) remained a legal peculiarity of the US market and developed in the European context only relatively recently, and there is still little evidence about the importance of this practice in DEEs.

According to the Post-Keynesian theory (and empirical evidence, provided among others by Orhangazi, 2008; Tori and Onaran, 2020), financial payments are likely to harm investment since they represent both a reduction in internal funds and prominence of short-term focuses on firms’ management. Furthermore, not only do NFCs use part of their funds to pay interest and dividends, but they can also pursue non-operating financial investments themselves, thus receiving financial income. We include the sum of interests and dividends received by the NFCs (πF) as a ratio to K as a variable to capture this aspect of financialisation.4 Theoretically, the expected sign of the effect of financial income on investment is ambiguous. On the one hand, these incomes may have a positive impact on the accumulation of fixed assets by easing the liquidity constraint faced by firms. On the other hand, financial activities can also be detrimental to physical investment, since the NFCs could be attracted by short-term, reversible financial investment, instead of engaging in long-term, irreversible physical investment. A counterargument might be that if the shift in investment spending from real to financial assets is only in the short run, this can add to the firm’s funds in the long run, and hence could potentially have a positive long-term impact on investment. If the firms are investing in financial assets when real investments are less profitable, earnings from financial investments could be used to fund real investments in the long run. The expectation of a negative coefficient for the financial profit variable developed above is potentially contentious. For one thing, this expectation is in contrast with the financing constraint hypothesis, according to which any income, whether from financial or real sources, would contribute to the internal funds of the firm, and hence its effect on investment should be positive. If in the future, the profit rate on financial assets falls below the profit rate on real assets, firms may use their income from current financial operations to finance their future real investment projects. In this case, past financial income can be positively correlated with the level of current capital expenditures. Second, even though financial income could be treated like any other income, there is no guarantee that it would be used to finance real investment. Financial income might be recycled back to financial markets or stockpiled as cash. The available evidence also suggests that the impact of financial income is non-linear to company size (Davis, 2018; Tori and Onaran, 2020). On the one hand, relatively small companies may use this additional source of income to partially ease liquidity constraints. On the other hand, larger and more flexible companies may see short-term and reversible financial investment as an attractive alternative to physical investment.5

We explore this possible dual, non-linear effect, by including an interaction dummy variable to account for the potentially different effects of financial income with respect to the size of the company (in terms of total assets). This alternative specification is described in equation (2)

where the dummy variable takes the value 1 if the average total assets of a company i lie in the lower n percentile of the distribution and take the value 0 otherwise. The place of a firm within size distribution is country specific, as size cohorts are not equally represented among the countries in the sample. The estimated coefficient shows the relative effect for the companies at the top of the distribution. The elasticity for the remaining companies is the sum of the coefficients and . A test for the joint statistical significance of the new variable is performed using a Wald test.

This second specification is used to capture the interactions between financialisation and the institutional structure of the DEEs discussed in Section 2. The model will be estimated using two sub-samples identified according to the median of the specific country-level indicator. The first panel will comprise NFCs operating in countries with an average of the indicator below the median, whilst the second panel will feature NFCs from countries above the median. The country-specific variables are discussed in more detail in Section 4.

We use this comprehensive but parsimonious model to test our hypotheses in the context of different institutional settings, based on the associations between variables reflecting the effects of financialisation and the country-specific variables.

4. Data, stylised facts and estimation methodology

We extract our data from the Worldscope database of publicly listed firms’ balance sheets, which contains standardised accounting information about not only investment, sales, profits, interest and dividend payments but also financial incomes. Standardised data on financial payments and, in particular, financial incomes are difficult to find; our database allows us to have comprehensive variables for our estimations. The Worldscope database has been acknowledged as a valuable source in the literature on firm-level investment analysis (e.g. Love, 2003; Love and Zicchino, 2006).

The selection of the sample has been informed by data availability, in particular for the financialisation variables. Using the Worldscope Database Guide, we identify the countries in the ‘advanced emerging, emerging and frontier markets’ category, excluding eastern European countries. We extract data for all active, publicly listed companies. First, we follow Love and Zicchino (2006) and include all countries with at least 30 firms and 100 firm-year observations between 1995 and 2015. Financial firms, identified by the primary SIC codes 6000-6799, are excluded.6 This results in an initial sample of 25 countries (Argentina, Bangladesh, Brazil, Chile, China, Colombia, Egypt, India, Indonesia, Malaysia, Mexico, Morocco, Nigeria, Pakistan, Peru, Philippines, Russian Federation, Saudi Arabia, Singapore, South Africa, South Korea, Sri Lanka, Thailand, Turkey and Vietnam).7

Next, we check for outliers and errors that usually characterise firm-level data. We exclude observations where fixed capital, capital expenditure, sales and total assets are negative or equal to zero. Also, companies with a negative mean operating income for the whole period are excluded.8 To avoid including episodes of mergers or acquisitions, companies with a rate of accumulation (I/K) higher than 2.5 or an increase in sales higher than 200 percent are excluded as recommended by Love (2003) and Bloom et al. (2004). We followed the standard procedure to exclude observations (not the company) in the upper and lower 1% of each variable’s distribution. Finally, it is recommended that firms should have at least five consecutive observations for the dependent variable (I/K), a condition also required for econometric purposes when employing a dynamic estimator (Roodman, 2009).

The result of this cleaning procedure is a sample of 3,720 NFCs from 21 DEEs (Argentina, Brazil, Chile, China, Colombia, Egypt, India, Indonesia, Malaysia, Mexico, Nigeria, Pakistan, Peru, Philippines, Russian Federation, Singapore, South Africa, South Korea, Sri Lanka, Thailand and Turkey). Supplementary Table 2A shows the list of countries in our sample with the number of observations and firms by country, while Supplementary Table 3A provides the descriptive statistics for the sample. As expected, the number of observations and firms included in the sample varies widely across the countries. The two countries with the largest number of observations in the sample are India and South Korea, while the ones with the lowest number are Nigeria and Colombia. Overall, our sample provides a comprehensive picture of the major DEEs.9

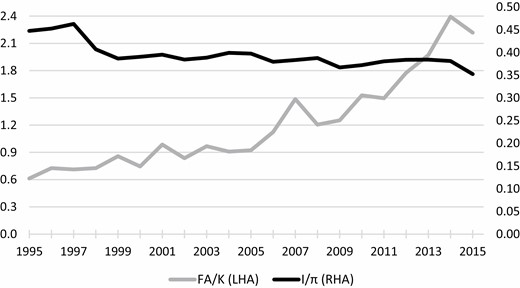

As can be seen in Figure 1 physical investment as a ratio to operating income, i.e. the re-investment of operating income by the NFCs, has decreased by 25% on average from 1995 to 2015 (15% by 2008 compared with its peak in 1997). At the same time, the ratio of financial assets to fixed assets increased significantly, reaching 2.2 in 2015 (an increase of about 260%).

Additions to fixed assets/operating income (I/π) and financial assets/fixed assets (FA/K), full sample, 1995–2015.

Source: Authors’ elaboration based on Worldscope data.

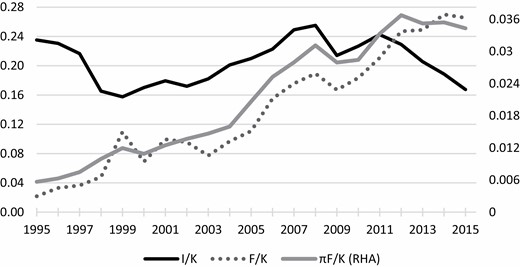

Figure 2 shows that, on average, the rate of capital accumulation (I/K) of NFCs in DEEs experienced a decrease during 1995–1999, recovered in the run-up to the 2008 crisis, and decreased again after the crisis. At the same time, both financial payments (dividends plus interest as a ratio to fixed assets) and financial incomes have been increasing significantly. The 2007–2008 crisis has led to a slight reversal in the NFCs’ financial payments and incomes, although the increasing trends re-emerged thereafter.10

Rate of accumulation (I/K), financial payments/fixed assets (F/K) and financial incomes/fixed assets (πF/K), full sample, 1995–2015.

Source: Authors’ elaboration based on Worldscope data

Supplementary Table 4A provides the data description and sources for country-level variables. All these variables are constructed by calculating the average value from 1995 to 2007, to avoid taking into consideration the years of the financial crisis.11

The de facto index of financial development is the average of the stock market and financial intermediaries’ development in the country, including domestic credit to the private sector, stock market capitalisation, stock market total value traded and the stock market turnover ratio (all as a percent to GDP). This is a widely used index in the literature on the effect of financial development on growth or investment (e.g. see Love, 2003). The financial reform index (Abiad et al., 2010) is a de jure index normalised between 0 and 1 aiming at summarising indicators regarding legislation about controls on credit, interest rates, pro-competition measures, banking supervision, privatisation, international capital flows and the security markets.

The ratio of total financial liabilities to GDP is used as a proxy for the level of openness to foreign investors and captures the de facto capital account openness. Data are from the Lane and Milesi-Ferretti (2007) database. This measure includes all foreign liabilities in the form of portfolio and FDI investments. The widely used Chinn-Ito index (KaOpen) is employed to measure de jure capital account openness.

To capture the internationalisation of production we use the Global Value Chain (GVC) Participation Index provided by the UNCTAD-Eora GVC Database (UNCTAD, 2022). This index is better suited to capture the multi-faceted aspects of the integration of DEEs into GVCs compared to the simple offshoring measures (Milberg, 2008; Aslam et al., 2017). The index is equal to the sum of the share of foreign value-added in the country i’s exports and the share of country i’s value-added in foreign countries’ exports (indirect value-added), divided by the total value-added of exports.

Table 2 summarises the country-level variables.

Country-specific variables, average 1995–2008a

| Country | Financial development index | Financial reform index | Financial liabilities to GDP | Capital account openness index (Chinn-Ito) | Global Value Chain Participation Index |

|---|---|---|---|---|---|

| Argentina | −0.662 | 0.749 | 0.915 | 0.413 | 0.359 |

| Brazil | −0.242 | 0.515 | 0.546 | −0.768 | 0.405 |

| Chile | −0.040 | 0.835 | 0.975 | 0.485 | 0.488 |

| Colombia | 1.271 | 0.334 | 0.513 | −1.195 | 0.390 |

| China | −0.684 | 0.680 | 0.353 | −0.922 | 0.332 |

| Egypt, Arab Rep. | 0.082 | 0.675 | 0.623 | 1.574 | 0.443 |

| India | 0.120 | 0.506 | 0.346 | −1.195 | 0.399 |

| Indonesia | −0.330 | 0.606 | 0.879 | 1.326 | 0.463 |

| Korea, Rep. | 1.032 | 0.719 | 0.520 | −0.458 | 0.520 |

| Malaysia | 1.521 | 0.714 | 1.037 | 0.168 | 0.643 |

| Mexico | −0.645 | 0.866 | 0.574 | 0.919 | 0.420 |

| Nigeria | −0.842 | 0.729 | 0.981 | −0.999 | 0.408 |

| Pakistan | 0.376 | 0.511 | 0.504 | −1.249 | 0.316 |

| Peru | −0.645 | 0.896 | 0.723 | 2.233 | 0.453 |

| Philippines | −0.201 | 0.760 | 0.810 | 0.100 | 0.644 |

| Russian Federation | −0.564 | 0.744 | 0.692 | −0.544 | 0.574 |

| Singapore | 1.609 | 0.900 | 6.228 | 2.211 | 0.782 |

| South Africa | 0.955 | 0.847 | 0.676 | −1.113 | 0.531 |

| Sri Lanka | −0.582 | 0.629 | 0.663 | 0.100 | 0.380 |

| Thailand | 1.009 | 0.643 | 0.891 | −0.212 | 0.514 |

| Turkey | −0.096 | 0.703 | 0.552 | −1.113 | 0.505 |

| Median | −0.096 | 0.714 | 0.676 | −0.212 | 0.453 |

| Average | 0.116 | 0.693 | 0.952 | −0.011 | 0.475 |

| Min | −0.842 | 0.334 | 0.346 | −1.249 | 0.316 |

| Max | 1.609 | 0.900 | 6.228 | 2.233 | 0.782 |

| Country | Financial development index | Financial reform index | Financial liabilities to GDP | Capital account openness index (Chinn-Ito) | Global Value Chain Participation Index |

|---|---|---|---|---|---|

| Argentina | −0.662 | 0.749 | 0.915 | 0.413 | 0.359 |

| Brazil | −0.242 | 0.515 | 0.546 | −0.768 | 0.405 |

| Chile | −0.040 | 0.835 | 0.975 | 0.485 | 0.488 |

| Colombia | 1.271 | 0.334 | 0.513 | −1.195 | 0.390 |

| China | −0.684 | 0.680 | 0.353 | −0.922 | 0.332 |

| Egypt, Arab Rep. | 0.082 | 0.675 | 0.623 | 1.574 | 0.443 |

| India | 0.120 | 0.506 | 0.346 | −1.195 | 0.399 |

| Indonesia | −0.330 | 0.606 | 0.879 | 1.326 | 0.463 |

| Korea, Rep. | 1.032 | 0.719 | 0.520 | −0.458 | 0.520 |

| Malaysia | 1.521 | 0.714 | 1.037 | 0.168 | 0.643 |

| Mexico | −0.645 | 0.866 | 0.574 | 0.919 | 0.420 |

| Nigeria | −0.842 | 0.729 | 0.981 | −0.999 | 0.408 |

| Pakistan | 0.376 | 0.511 | 0.504 | −1.249 | 0.316 |

| Peru | −0.645 | 0.896 | 0.723 | 2.233 | 0.453 |

| Philippines | −0.201 | 0.760 | 0.810 | 0.100 | 0.644 |

| Russian Federation | −0.564 | 0.744 | 0.692 | −0.544 | 0.574 |

| Singapore | 1.609 | 0.900 | 6.228 | 2.211 | 0.782 |

| South Africa | 0.955 | 0.847 | 0.676 | −1.113 | 0.531 |

| Sri Lanka | −0.582 | 0.629 | 0.663 | 0.100 | 0.380 |

| Thailand | 1.009 | 0.643 | 0.891 | −0.212 | 0.514 |

| Turkey | −0.096 | 0.703 | 0.552 | −1.113 | 0.505 |

| Median | −0.096 | 0.714 | 0.676 | −0.212 | 0.453 |

| Average | 0.116 | 0.693 | 0.952 | −0.011 | 0.475 |

| Min | −0.842 | 0.334 | 0.346 | −1.249 | 0.316 |

| Max | 1.609 | 0.900 | 6.228 | 2.233 | 0.782 |

Notes:

The light grey colour indicates that the respective country is above the median for a particular indicator. All the institutional variables used in our estimations are averaged for the period 1995–2007, to avoid considering turbulent years around the great financial crisis.

Sources: Authors’ elaboration based on World Bank, IMF, Chinn and Ito (2008), Lane and Milesi-Ferretti (2007) and UNCTAD. See Supplementary Table 4A for more information.

Country-specific variables, average 1995–2008a

| Country | Financial development index | Financial reform index | Financial liabilities to GDP | Capital account openness index (Chinn-Ito) | Global Value Chain Participation Index |

|---|---|---|---|---|---|

| Argentina | −0.662 | 0.749 | 0.915 | 0.413 | 0.359 |

| Brazil | −0.242 | 0.515 | 0.546 | −0.768 | 0.405 |

| Chile | −0.040 | 0.835 | 0.975 | 0.485 | 0.488 |

| Colombia | 1.271 | 0.334 | 0.513 | −1.195 | 0.390 |

| China | −0.684 | 0.680 | 0.353 | −0.922 | 0.332 |

| Egypt, Arab Rep. | 0.082 | 0.675 | 0.623 | 1.574 | 0.443 |

| India | 0.120 | 0.506 | 0.346 | −1.195 | 0.399 |

| Indonesia | −0.330 | 0.606 | 0.879 | 1.326 | 0.463 |

| Korea, Rep. | 1.032 | 0.719 | 0.520 | −0.458 | 0.520 |

| Malaysia | 1.521 | 0.714 | 1.037 | 0.168 | 0.643 |

| Mexico | −0.645 | 0.866 | 0.574 | 0.919 | 0.420 |

| Nigeria | −0.842 | 0.729 | 0.981 | −0.999 | 0.408 |

| Pakistan | 0.376 | 0.511 | 0.504 | −1.249 | 0.316 |

| Peru | −0.645 | 0.896 | 0.723 | 2.233 | 0.453 |

| Philippines | −0.201 | 0.760 | 0.810 | 0.100 | 0.644 |

| Russian Federation | −0.564 | 0.744 | 0.692 | −0.544 | 0.574 |

| Singapore | 1.609 | 0.900 | 6.228 | 2.211 | 0.782 |

| South Africa | 0.955 | 0.847 | 0.676 | −1.113 | 0.531 |

| Sri Lanka | −0.582 | 0.629 | 0.663 | 0.100 | 0.380 |

| Thailand | 1.009 | 0.643 | 0.891 | −0.212 | 0.514 |

| Turkey | −0.096 | 0.703 | 0.552 | −1.113 | 0.505 |

| Median | −0.096 | 0.714 | 0.676 | −0.212 | 0.453 |

| Average | 0.116 | 0.693 | 0.952 | −0.011 | 0.475 |

| Min | −0.842 | 0.334 | 0.346 | −1.249 | 0.316 |

| Max | 1.609 | 0.900 | 6.228 | 2.233 | 0.782 |

| Country | Financial development index | Financial reform index | Financial liabilities to GDP | Capital account openness index (Chinn-Ito) | Global Value Chain Participation Index |

|---|---|---|---|---|---|

| Argentina | −0.662 | 0.749 | 0.915 | 0.413 | 0.359 |

| Brazil | −0.242 | 0.515 | 0.546 | −0.768 | 0.405 |

| Chile | −0.040 | 0.835 | 0.975 | 0.485 | 0.488 |

| Colombia | 1.271 | 0.334 | 0.513 | −1.195 | 0.390 |

| China | −0.684 | 0.680 | 0.353 | −0.922 | 0.332 |

| Egypt, Arab Rep. | 0.082 | 0.675 | 0.623 | 1.574 | 0.443 |

| India | 0.120 | 0.506 | 0.346 | −1.195 | 0.399 |

| Indonesia | −0.330 | 0.606 | 0.879 | 1.326 | 0.463 |

| Korea, Rep. | 1.032 | 0.719 | 0.520 | −0.458 | 0.520 |

| Malaysia | 1.521 | 0.714 | 1.037 | 0.168 | 0.643 |

| Mexico | −0.645 | 0.866 | 0.574 | 0.919 | 0.420 |

| Nigeria | −0.842 | 0.729 | 0.981 | −0.999 | 0.408 |

| Pakistan | 0.376 | 0.511 | 0.504 | −1.249 | 0.316 |

| Peru | −0.645 | 0.896 | 0.723 | 2.233 | 0.453 |

| Philippines | −0.201 | 0.760 | 0.810 | 0.100 | 0.644 |

| Russian Federation | −0.564 | 0.744 | 0.692 | −0.544 | 0.574 |

| Singapore | 1.609 | 0.900 | 6.228 | 2.211 | 0.782 |

| South Africa | 0.955 | 0.847 | 0.676 | −1.113 | 0.531 |

| Sri Lanka | −0.582 | 0.629 | 0.663 | 0.100 | 0.380 |

| Thailand | 1.009 | 0.643 | 0.891 | −0.212 | 0.514 |

| Turkey | −0.096 | 0.703 | 0.552 | −1.113 | 0.505 |

| Median | −0.096 | 0.714 | 0.676 | −0.212 | 0.453 |

| Average | 0.116 | 0.693 | 0.952 | −0.011 | 0.475 |

| Min | −0.842 | 0.334 | 0.346 | −1.249 | 0.316 |

| Max | 1.609 | 0.900 | 6.228 | 2.233 | 0.782 |

Notes:

The light grey colour indicates that the respective country is above the median for a particular indicator. All the institutional variables used in our estimations are averaged for the period 1995–2007, to avoid considering turbulent years around the great financial crisis.

Sources: Authors’ elaboration based on World Bank, IMF, Chinn and Ito (2008), Lane and Milesi-Ferretti (2007) and UNCTAD. See Supplementary Table 4A for more information.

Although the rankings of the different indicators show some overlaps, the median splits based on different country-specific dimensions produce a rich and diverse categorisation.12 The various clusters constitute the sub-panels for the estimations.

4.1 Estimation methodology

In dynamic panel data models, the unobserved panel-level effects are correlated with the lagged dependent variables, and standard estimators (e.g. ordinary or generalised least squares) are inconsistent. Therefore, we estimate our model using a difference-Generalised Methods of Moments (GMM) estimator (Arellano and Bond, 1991). This methodology is suitable for analyses based on a ‘small-time/large observations’ sample. GMM is a powerful estimator for analyses based on firm-level data mainly for three reasons (Roodman, 2009). First, GMM is one of the best techniques to control for all sources of endogeneity between the dependent and explanatory variables, by using internal instruments, namely the lagged levels of the explanatory variables, which allows us to address dual causality if rising financial payments and incomes are also consequences of the slowdown in accumulation. The instrument set consists of instruments not correlated with the first difference of the error term but correlated with the dependent variable. Second, by first-differencing, this estimator eliminates companies’ unobservable fixed effects. Third, GMM can efficiently address auto-correlation problems. We apply two tests to assess the appropriateness of the instrument sets and lag structures. First, we check for second-order serial correlation with the Arellano-Bond test (Arellano and Bond, 1991). Second, we verify the validity of the instruments through the Hansen test.13 In all models, both the lagged dependent variable and all the explanatory variables enter the instrument set as endogenous regressors. Consistent with the structure of the GMM estimator, all the variables in the different specifications are instrumented using the second and third lags of the specific variables, while the year dummies are included in the exogenous set of instruments. We test the joint significance of the time dummies and the significance of the interaction dummies on financial income using a Wald test.

All the variables are in logarithmic form. We employ a log–log specification for five reasons: (i) to allow for non-linear relationships between the dependent and the explanatory variables; (ii) to control for heteroskedasticity; (iii) to allow for more meaningful interpretation of effects as elasticities (in percentage changes); (iv) to allow for direct comparison with previous micro-level studies about financialisation and in particular with Orhangazi (2008) and Tori and Onaran (2018, 2020); and (v) this form has proven to be more robust (in terms of auto-correlation and Hansen tests) when testing microeconomic relationship along with macroeconomic (institutional) variables (see e.g. Tori and Onaran, 2020). Robust standard errors are calculated through a two-step procedure, after a finite-sample correction (Windmeijer, 2005).

The country groupings are defined by computing the average of each indicator during the pre-crisis period 1995–2007, and by applying a median split between countries. All the estimations for the country groups come from weighted regressions, with the weights equal to 1 divided by the number of available observations in that country. This procedure mitigates the bias due to the high number of observations in some countries and allows considering country-specific time-invariant characteristics in a dynamic estimation (see Love, 2003).

5. Estimation results

This section presents the estimation results for alternative specifications of the investment model presented in Section 3. Table 3 presents the estimation results for the baseline model in equations (1) and (2) for the sample period of 1995–2015. The estimation results for specification (I) show both lagged accumulation and sales (i.e. demand) having a positive and highly significant effect on NFCs’ rate of accumulation. Also, operating profit has a positive effect on investment, although both its magnitude and significance level are relatively lower than the two previous variables. These results are in line with the evidence for NFCs in developed countries. In particular, the effect of profitability on capital accumulation is weak, and this could be directly due to the interaction between profits and the two financialisation channels described in Section 2.

Estimation results, full sample, dependent variable (I/K)t

| (I) | (II) | (III) | (IV) | (V) | (VI) | |

|---|---|---|---|---|---|---|

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.374*** | 0.372*** | 0.375*** | 0.378*** | 0.374*** | 0.369*** | |

| (0.025) | (0.025) | (0.024) | (0.024) | (0.026) | (0.025 | |

| 0.379*** | 0.375*** | 0.364*** | 0.344*** | 0.345*** | 0.365*** | |

| (0.051) | (0.053) | (0.053) | (0.054) | (0.051) | (0.049) | |

| 0.022* | 0.023* | 0.024* | 0.028** | 0.027** | 0.026** | |

| (0.013) | (0.013) | (0.013) | (0.013) | (0.013) | (0.013) | |

| −0.068** | −0.070** | −0.072*** | −0.084*** | −0.068*** | −0.071*** | |

| (0.028) | (0.028) | (0.028) | (0.027) | (0.026) | (0.025) | |

| −0.024 | −0.019 | 0.012 | 0.187*** | 0.346*** | 0.750** | |

| (0.022) | (0.024) | (0.035) | (0.058) | (0.120) | (0.352) | |

| −0.029 | −0.109 | −0.350*** | −0.455*** | −0.827** | ||

| (0.167) | (0.085) | (0.092) | (0.144) | (0.375) | ||

| −0.058*** | −0.058*** | −0.061*** | −0.062*** | −0.061*** | −0.057*** | |

| (0.017) | (0.016) | (0.017) | (0.015) | (0.014) | (0.017) | |

| Number of observations | 27885 | 27885 | 27885 | 27885 | 27885 | 27885 |

| Number of firms | 3720 | 3720 | 3720 | 3720 | 3720 | 3720 |

| Average number of observations | 7.5 | 7.5 | 7.5 | 7.5 | 7.5 | 7.5 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.199 | 0.265 | 0.301 | 0.233 | 0.206 | 0.323 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.423 | 0.419 | 0.479 | 0.813 | 0.772 | 0.803 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes |

| p-value Wald test for time effects | 0.008 | 0.002 | 0.001 | 0.000 | 0.005 | 0.002 |

| p-value | 0.210 | 0.130 | 0.001 | 0.002 | 0.019 |

| (I) | (II) | (III) | (IV) | (V) | (VI) | |

|---|---|---|---|---|---|---|

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.374*** | 0.372*** | 0.375*** | 0.378*** | 0.374*** | 0.369*** | |

| (0.025) | (0.025) | (0.024) | (0.024) | (0.026) | (0.025 | |

| 0.379*** | 0.375*** | 0.364*** | 0.344*** | 0.345*** | 0.365*** | |

| (0.051) | (0.053) | (0.053) | (0.054) | (0.051) | (0.049) | |

| 0.022* | 0.023* | 0.024* | 0.028** | 0.027** | 0.026** | |

| (0.013) | (0.013) | (0.013) | (0.013) | (0.013) | (0.013) | |

| −0.068** | −0.070** | −0.072*** | −0.084*** | −0.068*** | −0.071*** | |

| (0.028) | (0.028) | (0.028) | (0.027) | (0.026) | (0.025) | |

| −0.024 | −0.019 | 0.012 | 0.187*** | 0.346*** | 0.750** | |

| (0.022) | (0.024) | (0.035) | (0.058) | (0.120) | (0.352) | |

| −0.029 | −0.109 | −0.350*** | −0.455*** | −0.827** | ||

| (0.167) | (0.085) | (0.092) | (0.144) | (0.375) | ||

| −0.058*** | −0.058*** | −0.061*** | −0.062*** | −0.061*** | −0.057*** | |

| (0.017) | (0.016) | (0.017) | (0.015) | (0.014) | (0.017) | |

| Number of observations | 27885 | 27885 | 27885 | 27885 | 27885 | 27885 |

| Number of firms | 3720 | 3720 | 3720 | 3720 | 3720 | 3720 |

| Average number of observations | 7.5 | 7.5 | 7.5 | 7.5 | 7.5 | 7.5 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.199 | 0.265 | 0.301 | 0.233 | 0.206 | 0.323 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.423 | 0.419 | 0.479 | 0.813 | 0.772 | 0.803 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes |

| p-value Wald test for time effects | 0.008 | 0.002 | 0.001 | 0.000 | 0.005 | 0.002 |

| p-value | 0.210 | 0.130 | 0.001 | 0.002 | 0.019 |

Notes: Weighted regressions (w=1/total country obs.), two-step difference-GMM estimations. Specification I is based on equation (1) and specifications II–VI based on equation (2). Coefficients for the year dummies are not reported. Robust corrected standard error in parenthesis.

Significant at 10%.

Significant at 5%.

Significant at 1.

Source: authors’ computations based on Worldscope data.

Estimation results, full sample, dependent variable (I/K)t

| (I) | (II) | (III) | (IV) | (V) | (VI) | |

|---|---|---|---|---|---|---|

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.374*** | 0.372*** | 0.375*** | 0.378*** | 0.374*** | 0.369*** | |

| (0.025) | (0.025) | (0.024) | (0.024) | (0.026) | (0.025 | |

| 0.379*** | 0.375*** | 0.364*** | 0.344*** | 0.345*** | 0.365*** | |

| (0.051) | (0.053) | (0.053) | (0.054) | (0.051) | (0.049) | |

| 0.022* | 0.023* | 0.024* | 0.028** | 0.027** | 0.026** | |

| (0.013) | (0.013) | (0.013) | (0.013) | (0.013) | (0.013) | |

| −0.068** | −0.070** | −0.072*** | −0.084*** | −0.068*** | −0.071*** | |

| (0.028) | (0.028) | (0.028) | (0.027) | (0.026) | (0.025) | |

| −0.024 | −0.019 | 0.012 | 0.187*** | 0.346*** | 0.750** | |

| (0.022) | (0.024) | (0.035) | (0.058) | (0.120) | (0.352) | |

| −0.029 | −0.109 | −0.350*** | −0.455*** | −0.827** | ||

| (0.167) | (0.085) | (0.092) | (0.144) | (0.375) | ||

| −0.058*** | −0.058*** | −0.061*** | −0.062*** | −0.061*** | −0.057*** | |

| (0.017) | (0.016) | (0.017) | (0.015) | (0.014) | (0.017) | |

| Number of observations | 27885 | 27885 | 27885 | 27885 | 27885 | 27885 |

| Number of firms | 3720 | 3720 | 3720 | 3720 | 3720 | 3720 |

| Average number of observations | 7.5 | 7.5 | 7.5 | 7.5 | 7.5 | 7.5 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.199 | 0.265 | 0.301 | 0.233 | 0.206 | 0.323 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.423 | 0.419 | 0.479 | 0.813 | 0.772 | 0.803 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes |

| p-value Wald test for time effects | 0.008 | 0.002 | 0.001 | 0.000 | 0.005 | 0.002 |

| p-value | 0.210 | 0.130 | 0.001 | 0.002 | 0.019 |

| (I) | (II) | (III) | (IV) | (V) | (VI) | |

|---|---|---|---|---|---|---|

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.374*** | 0.372*** | 0.375*** | 0.378*** | 0.374*** | 0.369*** | |

| (0.025) | (0.025) | (0.024) | (0.024) | (0.026) | (0.025 | |

| 0.379*** | 0.375*** | 0.364*** | 0.344*** | 0.345*** | 0.365*** | |

| (0.051) | (0.053) | (0.053) | (0.054) | (0.051) | (0.049) | |

| 0.022* | 0.023* | 0.024* | 0.028** | 0.027** | 0.026** | |

| (0.013) | (0.013) | (0.013) | (0.013) | (0.013) | (0.013) | |

| −0.068** | −0.070** | −0.072*** | −0.084*** | −0.068*** | −0.071*** | |

| (0.028) | (0.028) | (0.028) | (0.027) | (0.026) | (0.025) | |

| −0.024 | −0.019 | 0.012 | 0.187*** | 0.346*** | 0.750** | |

| (0.022) | (0.024) | (0.035) | (0.058) | (0.120) | (0.352) | |

| −0.029 | −0.109 | −0.350*** | −0.455*** | −0.827** | ||

| (0.167) | (0.085) | (0.092) | (0.144) | (0.375) | ||

| −0.058*** | −0.058*** | −0.061*** | −0.062*** | −0.061*** | −0.057*** | |

| (0.017) | (0.016) | (0.017) | (0.015) | (0.014) | (0.017) | |

| Number of observations | 27885 | 27885 | 27885 | 27885 | 27885 | 27885 |

| Number of firms | 3720 | 3720 | 3720 | 3720 | 3720 | 3720 |

| Average number of observations | 7.5 | 7.5 | 7.5 | 7.5 | 7.5 | 7.5 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.199 | 0.265 | 0.301 | 0.233 | 0.206 | 0.323 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.423 | 0.419 | 0.479 | 0.813 | 0.772 | 0.803 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes |

| p-value Wald test for time effects | 0.008 | 0.002 | 0.001 | 0.000 | 0.005 | 0.002 |

| p-value | 0.210 | 0.130 | 0.001 | 0.002 | 0.019 |

Notes: Weighted regressions (w=1/total country obs.), two-step difference-GMM estimations. Specification I is based on equation (1) and specifications II–VI based on equation (2). Coefficients for the year dummies are not reported. Robust corrected standard error in parenthesis.

Significant at 10%.

Significant at 5%.

Significant at 1.

Source: authors’ computations based on Worldscope data.

The average effect of financial payments (interest plus dividends) is negative and significant, while financial income is insignificant. Also, the ratio of debt to total assets has a significantly negative effect on capital accumulation, indicating that debt has constrained investment in the DEEs.

Columns II–IV of Table 3 shows the estimation results for equation (2), in which the effect of financial income interacts with the firm sizes measured by total assets. In specification II, the dummy variable is equal to 1 for companies in the bottom 10% in terms of size distribution, while in specification VI, = 1 for companies in the bottom 90% in terms of size distribution. The other thresholds in terms of size are the first, second and third quartiles (i.e. 25, 50 and 75%). An interesting finding is that larger NFCs from the top 50% to the top 10% experienced a positive effect of financial income on investment (columns IV–VI). The elasticity for financial income across these percentiles is equal to +0.43 on average for the relatively larger companies, while for the smaller firms, this is between −0.16 and −0.77.14 This result stands in stark contrast to the ones so far proposed by the literature on developed economies (e.g. see Orhangazi, 2008; Tori and Onaran, 2018, 2020), where cash-constrained smaller companies experience generally positive effects of financial incomes on their investment. This result can be explained from a ‘catching-up’ perspective, where larger companies in DEEs aim at improving their productive basis to compete with competitors operating in developed countries, also utilising income from financial investments, whereas smaller companies seem to favour (reversible) financial investment over (irreversible) fixed capital expenditures.15 The effects of both financial payments and debt on investment are consistently negative and significant in all estimations.

Next, we present the results of the tests of the three hypotheses presented in Section 2 regarding the effect of country-specific features on the effects of financialisation at the firm level. The sub-panel including NFCs in countries with indicators below the median is named ‘panel 0’, while ‘panel 1’ is used to indicate NFCs in countries above the median.

The first set of estimations tests the variation in the effects of financialisation on NFCs with respect to the financial development and reform of the country, testing hypothesis 1. Tables 4 and 7 present the estimation results from the median split based on the composite index of financial development and the financial reform index, respectively.

Estimation results, full sample, 1995–2015, financial development index median split, dependent variable (I/K)t

| Financial development index below the median | Financial development index above the median | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | (IX) | (X) | (XI) | (XII) | |

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.295*** | 0.283*** | 0.294*** | 0.310*** | 0.307*** | 0.301*** | 0.440*** | 0.432*** | 0.437*** | 0.443*** | 0.430*** | 0.420*** | |

| (0.042) | (0.041) | (0.039) | (0.040) | (0.042) | (0.041) | (0.028) | (0.029) | (0.029) | (0.029) | (0.034) | (0.040) | |

| 0.282*** | 0.291*** | 0.244*** | 0.229** | 0.281*** | 0.268*** | 0.411*** | 0.421*** | 0.427*** | 0.404*** | 0.378*** | 0.396*** | |

| (0.084) | (0.085) | (0.089) | (0.091) | (0.082) | (0.080) | (0.053) | (0.053) | (0.055) | (0.056) | (0.058) | (0.065) | |

| 0.021 | 0.024 | 0.025 | 0.026 | 0.020 | 0.023 | 0.021 | 0.018 | 0.021 | 0.020 | 0.023 | 0.029 | |

| (0.022) | (0.022) | (0.021) | (0.021) | (0.021) | (0.022) | (0.016) | (0.016) | (0.016) | (0.016) | (0.015) | (0.019) | |

| −0.069 | −0.078 | −0.078 | −0.094** | −0.067 | −0.069* | −0.067*** | −0.061** | −0.069*** | −0.068*** | −0.068*** | −0.073** | |

| (0.047) | (0.049) | (0.049) | (0.048) | (0.044) | (0.042) | (0.025) | (0.027) | (0.026) | (0.025) | (0.026) | (0.032) | |

| −0.034 | −0.023 | 0.034 | 0.219** | 0.350** | 0.645** | −0.005 | −0.024 | −0.026 | 0.085 | 0.328*** | 1.262 | |

| (0.035) | (0.042) | (0.052) | (0.086) | (0.160) | (0.277) | (0.022) | (0.030) | (0.049) | (0.059) | (0.124) | (0.907) | |

| −0.022 | −0.184* | −0.398*** | −0.467** | −0.724** | 0.765 | 0.108 | −0.188 | −0.437*** | −1.373 | |||

| (0.089) | (0.105) | (0.124) | (0.190) | (0.295) | (0.740) | (0.224) | (0.122) | (0.161) | (0.975) | |||

| −0.027 | −0.030 | −0.032 | −0.035 | −0.043* | −0.028 | −0.070*** | −0.067*** | −0.068*** | −0.074*** | −0.065*** | −0.066*** | |

| (0.029) | (0.029) | (0.030) | (0.027) | (0.026) | (0.030) | (0.014) | (0.014) | (0.014) | (0.014) | (0.013) | (0.014) | |

| Number of observations | 6,436 | 6,436 | 6,436 | 6,436 | 6,436 | 6,436 | 21,449 | 21,449 | 21,449 | 21,449 | 21,449 | 21,449 |

| Number of firms | 767 | 767 | 767 | 767 | 767 | 767 | 2,953 | 2,953 | 2,953 | 2,953 | 2,953 | 2,953 |

| Average number of observations | 8.4 | 8.4 | 8.4 | 8.4 | 8.4 | 8.4 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.514 | 0.531 | 0.618 | 0.476 | 0.545 | 0.638 | 0.044 | 0.123 | 0.036 | 0.019 | 0.112 | 0.222 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.838 | 0.837 | 0.918 | 0.729 | 0.744 | 0.855 | 0.426 | 0.682 | 0.502 | 0.421 | 0.485 | 0.918 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald test for time effects (p-value) | 0.002 | 0.001 | 0.000 | 0.005 | 0.001 | 0.000 | 0.010 | 0.008 | 0.009 | 0.012 | 0.004 | 0.003 |

| p-value | 0.514 | 0.058 | 0.005 | 0.022 | 0.057 | 0.304 | 0.650 | 0.026 | 0.144 | |||

| Financial development index below the median | Financial development index above the median | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | (IX) | (X) | (XI) | (XII) | |

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.295*** | 0.283*** | 0.294*** | 0.310*** | 0.307*** | 0.301*** | 0.440*** | 0.432*** | 0.437*** | 0.443*** | 0.430*** | 0.420*** | |

| (0.042) | (0.041) | (0.039) | (0.040) | (0.042) | (0.041) | (0.028) | (0.029) | (0.029) | (0.029) | (0.034) | (0.040) | |

| 0.282*** | 0.291*** | 0.244*** | 0.229** | 0.281*** | 0.268*** | 0.411*** | 0.421*** | 0.427*** | 0.404*** | 0.378*** | 0.396*** | |

| (0.084) | (0.085) | (0.089) | (0.091) | (0.082) | (0.080) | (0.053) | (0.053) | (0.055) | (0.056) | (0.058) | (0.065) | |

| 0.021 | 0.024 | 0.025 | 0.026 | 0.020 | 0.023 | 0.021 | 0.018 | 0.021 | 0.020 | 0.023 | 0.029 | |

| (0.022) | (0.022) | (0.021) | (0.021) | (0.021) | (0.022) | (0.016) | (0.016) | (0.016) | (0.016) | (0.015) | (0.019) | |

| −0.069 | −0.078 | −0.078 | −0.094** | −0.067 | −0.069* | −0.067*** | −0.061** | −0.069*** | −0.068*** | −0.068*** | −0.073** | |

| (0.047) | (0.049) | (0.049) | (0.048) | (0.044) | (0.042) | (0.025) | (0.027) | (0.026) | (0.025) | (0.026) | (0.032) | |

| −0.034 | −0.023 | 0.034 | 0.219** | 0.350** | 0.645** | −0.005 | −0.024 | −0.026 | 0.085 | 0.328*** | 1.262 | |

| (0.035) | (0.042) | (0.052) | (0.086) | (0.160) | (0.277) | (0.022) | (0.030) | (0.049) | (0.059) | (0.124) | (0.907) | |

| −0.022 | −0.184* | −0.398*** | −0.467** | −0.724** | 0.765 | 0.108 | −0.188 | −0.437*** | −1.373 | |||

| (0.089) | (0.105) | (0.124) | (0.190) | (0.295) | (0.740) | (0.224) | (0.122) | (0.161) | (0.975) | |||

| −0.027 | −0.030 | −0.032 | −0.035 | −0.043* | −0.028 | −0.070*** | −0.067*** | −0.068*** | −0.074*** | −0.065*** | −0.066*** | |

| (0.029) | (0.029) | (0.030) | (0.027) | (0.026) | (0.030) | (0.014) | (0.014) | (0.014) | (0.014) | (0.013) | (0.014) | |

| Number of observations | 6,436 | 6,436 | 6,436 | 6,436 | 6,436 | 6,436 | 21,449 | 21,449 | 21,449 | 21,449 | 21,449 | 21,449 |

| Number of firms | 767 | 767 | 767 | 767 | 767 | 767 | 2,953 | 2,953 | 2,953 | 2,953 | 2,953 | 2,953 |

| Average number of observations | 8.4 | 8.4 | 8.4 | 8.4 | 8.4 | 8.4 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.514 | 0.531 | 0.618 | 0.476 | 0.545 | 0.638 | 0.044 | 0.123 | 0.036 | 0.019 | 0.112 | 0.222 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.838 | 0.837 | 0.918 | 0.729 | 0.744 | 0.855 | 0.426 | 0.682 | 0.502 | 0.421 | 0.485 | 0.918 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald test for time effects (p-value) | 0.002 | 0.001 | 0.000 | 0.005 | 0.001 | 0.000 | 0.010 | 0.008 | 0.009 | 0.012 | 0.004 | 0.003 |

| p-value | 0.514 | 0.058 | 0.005 | 0.022 | 0.057 | 0.304 | 0.650 | 0.026 | 0.144 | |||

Notes: Weighted regressions (w=1/total country obs.), two-step difference-GMM estimations. Specifications I and VII are based on equation (1) and specifications II–VI and VIII–XII based on equation (2). Coefficients for the year dummies are not reported. Robust corrected standard error in parenthesis.

Significant at 10%.

Significant at 5%.

Significant at 1%.

Source: Authors’ computations based on Worldscope data.

Estimation results, full sample, 1995–2015, financial development index median split, dependent variable (I/K)t

| Financial development index below the median | Financial development index above the median | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | (IX) | (X) | (XI) | (XII) | |

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.295*** | 0.283*** | 0.294*** | 0.310*** | 0.307*** | 0.301*** | 0.440*** | 0.432*** | 0.437*** | 0.443*** | 0.430*** | 0.420*** | |

| (0.042) | (0.041) | (0.039) | (0.040) | (0.042) | (0.041) | (0.028) | (0.029) | (0.029) | (0.029) | (0.034) | (0.040) | |

| 0.282*** | 0.291*** | 0.244*** | 0.229** | 0.281*** | 0.268*** | 0.411*** | 0.421*** | 0.427*** | 0.404*** | 0.378*** | 0.396*** | |

| (0.084) | (0.085) | (0.089) | (0.091) | (0.082) | (0.080) | (0.053) | (0.053) | (0.055) | (0.056) | (0.058) | (0.065) | |

| 0.021 | 0.024 | 0.025 | 0.026 | 0.020 | 0.023 | 0.021 | 0.018 | 0.021 | 0.020 | 0.023 | 0.029 | |

| (0.022) | (0.022) | (0.021) | (0.021) | (0.021) | (0.022) | (0.016) | (0.016) | (0.016) | (0.016) | (0.015) | (0.019) | |

| −0.069 | −0.078 | −0.078 | −0.094** | −0.067 | −0.069* | −0.067*** | −0.061** | −0.069*** | −0.068*** | −0.068*** | −0.073** | |

| (0.047) | (0.049) | (0.049) | (0.048) | (0.044) | (0.042) | (0.025) | (0.027) | (0.026) | (0.025) | (0.026) | (0.032) | |

| −0.034 | −0.023 | 0.034 | 0.219** | 0.350** | 0.645** | −0.005 | −0.024 | −0.026 | 0.085 | 0.328*** | 1.262 | |

| (0.035) | (0.042) | (0.052) | (0.086) | (0.160) | (0.277) | (0.022) | (0.030) | (0.049) | (0.059) | (0.124) | (0.907) | |

| −0.022 | −0.184* | −0.398*** | −0.467** | −0.724** | 0.765 | 0.108 | −0.188 | −0.437*** | −1.373 | |||

| (0.089) | (0.105) | (0.124) | (0.190) | (0.295) | (0.740) | (0.224) | (0.122) | (0.161) | (0.975) | |||

| −0.027 | −0.030 | −0.032 | −0.035 | −0.043* | −0.028 | −0.070*** | −0.067*** | −0.068*** | −0.074*** | −0.065*** | −0.066*** | |

| (0.029) | (0.029) | (0.030) | (0.027) | (0.026) | (0.030) | (0.014) | (0.014) | (0.014) | (0.014) | (0.013) | (0.014) | |

| Number of observations | 6,436 | 6,436 | 6,436 | 6,436 | 6,436 | 6,436 | 21,449 | 21,449 | 21,449 | 21,449 | 21,449 | 21,449 |

| Number of firms | 767 | 767 | 767 | 767 | 767 | 767 | 2,953 | 2,953 | 2,953 | 2,953 | 2,953 | 2,953 |

| Average number of observations | 8.4 | 8.4 | 8.4 | 8.4 | 8.4 | 8.4 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.514 | 0.531 | 0.618 | 0.476 | 0.545 | 0.638 | 0.044 | 0.123 | 0.036 | 0.019 | 0.112 | 0.222 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.838 | 0.837 | 0.918 | 0.729 | 0.744 | 0.855 | 0.426 | 0.682 | 0.502 | 0.421 | 0.485 | 0.918 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald test for time effects (p-value) | 0.002 | 0.001 | 0.000 | 0.005 | 0.001 | 0.000 | 0.010 | 0.008 | 0.009 | 0.012 | 0.004 | 0.003 |

| p-value | 0.514 | 0.058 | 0.005 | 0.022 | 0.057 | 0.304 | 0.650 | 0.026 | 0.144 | |||

| Financial development index below the median | Financial development index above the median | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | (IX) | (X) | (XI) | (XII) | |

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.295*** | 0.283*** | 0.294*** | 0.310*** | 0.307*** | 0.301*** | 0.440*** | 0.432*** | 0.437*** | 0.443*** | 0.430*** | 0.420*** | |

| (0.042) | (0.041) | (0.039) | (0.040) | (0.042) | (0.041) | (0.028) | (0.029) | (0.029) | (0.029) | (0.034) | (0.040) | |

| 0.282*** | 0.291*** | 0.244*** | 0.229** | 0.281*** | 0.268*** | 0.411*** | 0.421*** | 0.427*** | 0.404*** | 0.378*** | 0.396*** | |

| (0.084) | (0.085) | (0.089) | (0.091) | (0.082) | (0.080) | (0.053) | (0.053) | (0.055) | (0.056) | (0.058) | (0.065) | |

| 0.021 | 0.024 | 0.025 | 0.026 | 0.020 | 0.023 | 0.021 | 0.018 | 0.021 | 0.020 | 0.023 | 0.029 | |

| (0.022) | (0.022) | (0.021) | (0.021) | (0.021) | (0.022) | (0.016) | (0.016) | (0.016) | (0.016) | (0.015) | (0.019) | |

| −0.069 | −0.078 | −0.078 | −0.094** | −0.067 | −0.069* | −0.067*** | −0.061** | −0.069*** | −0.068*** | −0.068*** | −0.073** | |

| (0.047) | (0.049) | (0.049) | (0.048) | (0.044) | (0.042) | (0.025) | (0.027) | (0.026) | (0.025) | (0.026) | (0.032) | |

| −0.034 | −0.023 | 0.034 | 0.219** | 0.350** | 0.645** | −0.005 | −0.024 | −0.026 | 0.085 | 0.328*** | 1.262 | |

| (0.035) | (0.042) | (0.052) | (0.086) | (0.160) | (0.277) | (0.022) | (0.030) | (0.049) | (0.059) | (0.124) | (0.907) | |

| −0.022 | −0.184* | −0.398*** | −0.467** | −0.724** | 0.765 | 0.108 | −0.188 | −0.437*** | −1.373 | |||

| (0.089) | (0.105) | (0.124) | (0.190) | (0.295) | (0.740) | (0.224) | (0.122) | (0.161) | (0.975) | |||

| −0.027 | −0.030 | −0.032 | −0.035 | −0.043* | −0.028 | −0.070*** | −0.067*** | −0.068*** | −0.074*** | −0.065*** | −0.066*** | |

| (0.029) | (0.029) | (0.030) | (0.027) | (0.026) | (0.030) | (0.014) | (0.014) | (0.014) | (0.014) | (0.013) | (0.014) | |

| Number of observations | 6,436 | 6,436 | 6,436 | 6,436 | 6,436 | 6,436 | 21,449 | 21,449 | 21,449 | 21,449 | 21,449 | 21,449 |

| Number of firms | 767 | 767 | 767 | 767 | 767 | 767 | 2,953 | 2,953 | 2,953 | 2,953 | 2,953 | 2,953 |

| Average number of observations | 8.4 | 8.4 | 8.4 | 8.4 | 8.4 | 8.4 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.514 | 0.531 | 0.618 | 0.476 | 0.545 | 0.638 | 0.044 | 0.123 | 0.036 | 0.019 | 0.112 | 0.222 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.838 | 0.837 | 0.918 | 0.729 | 0.744 | 0.855 | 0.426 | 0.682 | 0.502 | 0.421 | 0.485 | 0.918 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald test for time effects (p-value) | 0.002 | 0.001 | 0.000 | 0.005 | 0.001 | 0.000 | 0.010 | 0.008 | 0.009 | 0.012 | 0.004 | 0.003 |

| p-value | 0.514 | 0.058 | 0.005 | 0.022 | 0.057 | 0.304 | 0.650 | 0.026 | 0.144 | |||

Notes: Weighted regressions (w=1/total country obs.), two-step difference-GMM estimations. Specifications I and VII are based on equation (1) and specifications II–VI and VIII–XII based on equation (2). Coefficients for the year dummies are not reported. Robust corrected standard error in parenthesis.

Significant at 10%.

Significant at 5%.

Significant at 1%.

Source: Authors’ computations based on Worldscope data.

Estimation results, full sample, 1995–2015, financial reform index median split, dependent variable (I/K)t

| Financial reform index below the median | Financial reform index above the median | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | (IX) | (X) | (XI) | (XII) | |

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.408*** | 0.412*** | 0.404*** | 0.397*** | 0.397*** | 0.399*** | 0.324*** | 0.326*** | 0.325*** | 0.344*** | 0.345*** | 0.328*** | |

| (0.032) | (0.032) | (0.032) | (0.034) | (0.035) | (0.033) | (0.036) | (0.035) | (0.035) | (0.036) | (0.040) | (0.039) | |

| 0.457*** | 0.463*** | 0.415*** | 0.405*** | 0.413*** | 0.440*** | 0.345*** | 0.345*** | 0.364*** | 0.333*** | 0.345*** | 0.325*** | |

| (0.068) | (0.081) | (0.076) | (0.077) | (0.073) | (0.068) | (0.069) | (0.069) | (0.068) | (0.067) | (0.069) | (0.069) | |

| −0.008 | −0.008 | 0.004 | 0.005 | 0.006 | −0.005 | 0.057*** | 0.058*** | 0.058*** | 0.054*** | 0. 051*** | 0.054*** | |

| (0.020) | (0.022) | (0.019) | (0.020) | (0.020) | (0.020) | (0.014) | (0.014) | (0.014) | (0.015) | (0.015) | (0.015) | |

| −0.018 | −0.025 | −0.017 | −0.014 | −0.018 | −0.024 | −0.129*** | −0.128*** | −0.129*** | −0.159*** | −0.120*** | −0.111*** | |

| (0.034) | (0.034) | (0.033) | (0.032) | (0.033) | (0.033) | (0.036) | (0.036) | (0.036) | (0.038) | (0.037) | (0.038) | |

| −0.018 | −0.026 | 0.065 | 0.160** | 0.224** | 0.316* | −0.062** | −0.067* | −0.067* | 0.192 | 0.238 | 0.392 | |

| (0.027) | (0.037) | (0.059) | (0.075) | (0.103) | (0.184) | (0.028) | (0.036) | (0.038) | (0.191) | (0.237) | (0.585) | |

| 0.316 | −0.344 | −0.374** | −0.317** | −0.361* | 0.013 | 0.026 | −0.365*** | −0.351 | −0.478 | |||

| (0.506) | (0.231) | (0.154) | (0.130) | (0.193) | (0.074) | (0.085) | (0.129) | (0.272) | (0.625) | |||

| −0.109*** | −0.106*** | −0.130*** | −0.126*** | −0.115*** | −0.106*** | −0.027 | −0.028 | −0.029 | −0.028 | −0.026 | −0.027 | |

| (0.018) | (0.018) | (0.024) | (0.022) | (0.019) | (0.019) | (0.024) | (0.024) | (0.024) | (0.019) | (0.016) | (0.025) | |

| Number of observations | 15,029 | 15,029 | 15,029 | 15,029 | 15,029 | 15,029 | 12,856 | 12,856 | 12,856 | 12,856 | 12,856 | 12,856 |

| Number of firms | 2,054 | 2,054 | 2,054 | 2,054 | 2,054 | 2,054 | 1,666 | 1,666 | 1,666 | 1,666 | 1,666 | 1,666 |

| Average number of observations | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.7 | 7.7 | 7.7 | 7.7 | 7.7 | 7.7 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.324 | 0.426 | 0.569 | 0.268 | 0.138 | 0.198 | 0.199 | 0.276 | 0.233 | 0.182 | 0.308 | 0.140 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.744 | 0.807 | 0.663 | 0.995 | 0.870 | 0.821 | 0.591 | 0.601 | 0.530 | 0.840 | 0.735 | 0.755 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald test for time effects (p-value) | 0.002 | 0.000 | 0.009 | 0.000 | 0.003 | 0.002 | 0.001 | 0.000 | 0.005 | 0.006 | 0.002 | 0.000 |

| p-value | 0.550 | 0.130 | 0.020 | 0.028 | 0.124 | 0.312 | 0.517 | 0.000 | 0.025 | 0.093 | ||

| Financial reform index below the median | Financial reform index above the median | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | (IX) | (X) | (XI) | (XII) | |

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.408*** | 0.412*** | 0.404*** | 0.397*** | 0.397*** | 0.399*** | 0.324*** | 0.326*** | 0.325*** | 0.344*** | 0.345*** | 0.328*** | |

| (0.032) | (0.032) | (0.032) | (0.034) | (0.035) | (0.033) | (0.036) | (0.035) | (0.035) | (0.036) | (0.040) | (0.039) | |

| 0.457*** | 0.463*** | 0.415*** | 0.405*** | 0.413*** | 0.440*** | 0.345*** | 0.345*** | 0.364*** | 0.333*** | 0.345*** | 0.325*** | |

| (0.068) | (0.081) | (0.076) | (0.077) | (0.073) | (0.068) | (0.069) | (0.069) | (0.068) | (0.067) | (0.069) | (0.069) | |

| −0.008 | −0.008 | 0.004 | 0.005 | 0.006 | −0.005 | 0.057*** | 0.058*** | 0.058*** | 0.054*** | 0. 051*** | 0.054*** | |

| (0.020) | (0.022) | (0.019) | (0.020) | (0.020) | (0.020) | (0.014) | (0.014) | (0.014) | (0.015) | (0.015) | (0.015) | |

| −0.018 | −0.025 | −0.017 | −0.014 | −0.018 | −0.024 | −0.129*** | −0.128*** | −0.129*** | −0.159*** | −0.120*** | −0.111*** | |

| (0.034) | (0.034) | (0.033) | (0.032) | (0.033) | (0.033) | (0.036) | (0.036) | (0.036) | (0.038) | (0.037) | (0.038) | |

| −0.018 | −0.026 | 0.065 | 0.160** | 0.224** | 0.316* | −0.062** | −0.067* | −0.067* | 0.192 | 0.238 | 0.392 | |

| (0.027) | (0.037) | (0.059) | (0.075) | (0.103) | (0.184) | (0.028) | (0.036) | (0.038) | (0.191) | (0.237) | (0.585) | |

| 0.316 | −0.344 | −0.374** | −0.317** | −0.361* | 0.013 | 0.026 | −0.365*** | −0.351 | −0.478 | |||

| (0.506) | (0.231) | (0.154) | (0.130) | (0.193) | (0.074) | (0.085) | (0.129) | (0.272) | (0.625) | |||

| −0.109*** | −0.106*** | −0.130*** | −0.126*** | −0.115*** | −0.106*** | −0.027 | −0.028 | −0.029 | −0.028 | −0.026 | −0.027 | |

| (0.018) | (0.018) | (0.024) | (0.022) | (0.019) | (0.019) | (0.024) | (0.024) | (0.024) | (0.019) | (0.016) | (0.025) | |

| Number of observations | 15,029 | 15,029 | 15,029 | 15,029 | 15,029 | 15,029 | 12,856 | 12,856 | 12,856 | 12,856 | 12,856 | 12,856 |

| Number of firms | 2,054 | 2,054 | 2,054 | 2,054 | 2,054 | 2,054 | 1,666 | 1,666 | 1,666 | 1,666 | 1,666 | 1,666 |

| Average number of observations | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.7 | 7.7 | 7.7 | 7.7 | 7.7 | 7.7 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.324 | 0.426 | 0.569 | 0.268 | 0.138 | 0.198 | 0.199 | 0.276 | 0.233 | 0.182 | 0.308 | 0.140 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.744 | 0.807 | 0.663 | 0.995 | 0.870 | 0.821 | 0.591 | 0.601 | 0.530 | 0.840 | 0.735 | 0.755 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald test for time effects (p-value) | 0.002 | 0.000 | 0.009 | 0.000 | 0.003 | 0.002 | 0.001 | 0.000 | 0.005 | 0.006 | 0.002 | 0.000 |

| p-value | 0.550 | 0.130 | 0.020 | 0.028 | 0.124 | 0.312 | 0.517 | 0.000 | 0.025 | 0.093 | ||

Notes: Weighted regressions (w=1/total country obs.), two-step difference-GMM estimations. Specifications I and VII are based on equation (1) and specifications II–VI and VIII–XII based on equation (2). Coefficients for the year dummies are not reported. Robust corrected standard error in parenthesis.

Significant at 10%.

Significant at 5%.

Significant at 1%.

Source: Authors’ computations based on Worldscope data.

Estimation results, full sample, 1995–2015, financial reform index median split, dependent variable (I/K)t

| Financial reform index below the median | Financial reform index above the median | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | (IX) | (X) | (XI) | (XII) | |

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.408*** | 0.412*** | 0.404*** | 0.397*** | 0.397*** | 0.399*** | 0.324*** | 0.326*** | 0.325*** | 0.344*** | 0.345*** | 0.328*** | |

| (0.032) | (0.032) | (0.032) | (0.034) | (0.035) | (0.033) | (0.036) | (0.035) | (0.035) | (0.036) | (0.040) | (0.039) | |

| 0.457*** | 0.463*** | 0.415*** | 0.405*** | 0.413*** | 0.440*** | 0.345*** | 0.345*** | 0.364*** | 0.333*** | 0.345*** | 0.325*** | |

| (0.068) | (0.081) | (0.076) | (0.077) | (0.073) | (0.068) | (0.069) | (0.069) | (0.068) | (0.067) | (0.069) | (0.069) | |

| −0.008 | −0.008 | 0.004 | 0.005 | 0.006 | −0.005 | 0.057*** | 0.058*** | 0.058*** | 0.054*** | 0. 051*** | 0.054*** | |

| (0.020) | (0.022) | (0.019) | (0.020) | (0.020) | (0.020) | (0.014) | (0.014) | (0.014) | (0.015) | (0.015) | (0.015) | |

| −0.018 | −0.025 | −0.017 | −0.014 | −0.018 | −0.024 | −0.129*** | −0.128*** | −0.129*** | −0.159*** | −0.120*** | −0.111*** | |

| (0.034) | (0.034) | (0.033) | (0.032) | (0.033) | (0.033) | (0.036) | (0.036) | (0.036) | (0.038) | (0.037) | (0.038) | |

| −0.018 | −0.026 | 0.065 | 0.160** | 0.224** | 0.316* | −0.062** | −0.067* | −0.067* | 0.192 | 0.238 | 0.392 | |

| (0.027) | (0.037) | (0.059) | (0.075) | (0.103) | (0.184) | (0.028) | (0.036) | (0.038) | (0.191) | (0.237) | (0.585) | |

| 0.316 | −0.344 | −0.374** | −0.317** | −0.361* | 0.013 | 0.026 | −0.365*** | −0.351 | −0.478 | |||

| (0.506) | (0.231) | (0.154) | (0.130) | (0.193) | (0.074) | (0.085) | (0.129) | (0.272) | (0.625) | |||

| −0.109*** | −0.106*** | −0.130*** | −0.126*** | −0.115*** | −0.106*** | −0.027 | −0.028 | −0.029 | −0.028 | −0.026 | −0.027 | |

| (0.018) | (0.018) | (0.024) | (0.022) | (0.019) | (0.019) | (0.024) | (0.024) | (0.024) | (0.019) | (0.016) | (0.025) | |

| Number of observations | 15,029 | 15,029 | 15,029 | 15,029 | 15,029 | 15,029 | 12,856 | 12,856 | 12,856 | 12,856 | 12,856 | 12,856 |

| Number of firms | 2,054 | 2,054 | 2,054 | 2,054 | 2,054 | 2,054 | 1,666 | 1,666 | 1,666 | 1,666 | 1,666 | 1,666 |

| Average number of observations | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.3 | 7.7 | 7.7 | 7.7 | 7.7 | 7.7 | 7.7 |

| Number of instruments | 31 | 33 | 33 | 33 | 33 | 33 | 31 | 33 | 33 | 33 | 33 | 33 |

| p-value Hanses test | 0.324 | 0.426 | 0.569 | 0.268 | 0.138 | 0.198 | 0.199 | 0.276 | 0.233 | 0.182 | 0.308 | 0.140 |

| p-value A-B test (AR1) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| p-value A-B test (AR2) | 0.744 | 0.807 | 0.663 | 0.995 | 0.870 | 0.821 | 0.591 | 0.601 | 0.530 | 0.840 | 0.735 | 0.755 |

| Time effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald test for time effects (p-value) | 0.002 | 0.000 | 0.009 | 0.000 | 0.003 | 0.002 | 0.001 | 0.000 | 0.005 | 0.006 | 0.002 | 0.000 |

| p-value | 0.550 | 0.130 | 0.020 | 0.028 | 0.124 | 0.312 | 0.517 | 0.000 | 0.025 | 0.093 | ||

| Financial reform index below the median | Financial reform index above the median | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (I) | (II) | (III) | (IV) | (V) | (VI) | (VII) | (VIII) | (IX) | (X) | (XI) | (XII) | |

| TOT | TA10 | TA25 | TA50 | TA75 | TA90 | TOT | TA10 | TA25 | TA50 | TA75 | TA90 | |

| 0.408*** | 0.412*** | 0.404*** | 0.397*** | 0.397*** | 0.399*** | 0.324*** | 0.326*** | 0.325*** | 0.344*** | 0.345*** | 0.328*** | |