Abstract

This article considers a stationary economy populated with overlapping generations that reproduce identically in continuous time. Each dynasty has a productivity and an opportunity cost of going to work that vary with age. Labor supply is extensive. At each date, the typical agent can either work full time or not work at all. The decision to work is based on a comparison between after tax income and the privately known opportunity cost of work. We assume that the utilitarian government, which aims at redistributing lifetime utility across dynasties, has a single policy instrument, a stationary income tax schedule function of current income. The article develops a method to study the government problem. This technique is applied to derive the properties of the optimal income tax schedule in a number of examples.

1. Introduction

We study income taxation in a dynamic stationary economy with overlapping generations, made of dynasties with fixed lifetime that reproduce identically. Time is continuous. Labor supply is extensive. At each date, one can either work full time or not work at all. The typical agent is characterized by an invariant instantaneous utility function for consumption and deterministic profiles of productivity, that is, production when working full time, and pecuniary cost of going to work. For simplicity, we assume that these profiles are deterministic. The government aims at redistributing lifetime welfare across dynasties, using the income tax. We put a number of restrictions on the government instrument, based on casual observation of developed economies: we suppose that the tax schedule is invariant over time and that tax depends only on current labor income. It cannot depend on the pecuniary cost of going to work, which is implicitly not verifiable by the tax authority. All non-workers are identically treated (they pay the same amount or receive the absolute value of the transfer if tax is negative). This transfer is independent of the (potential) productivity, supposed not to be verifiable for non-working individuals. We derive the properties of the optimal tax system in this setup.

Its dynamic structure makes the article unlike the bulk of the optimal taxation literature that takes place in a static model; see, for example, the survey of Piketty and Saez (2013). Also, it is different from the intensive labor supply models that follow Mirrlees, where the agents only differ by their productivities along a single dimension of heterogeneity. It shares features of the extensive model, notably the heterogeneity in the cost of going to work, which may generate an optimal subsidy of the labor supply of the low-skilled agents as in Choné and Laroque (2005).

The dynamic setup is similar (overlapping generations, deterministic trajectories,…) to that used by a number of recent works, Rogerson (2011), Shourideh and Troshkin (2012), or Weinzierl (2011). Our contribution with respect to these studies is in our focus on the extensive margin and the treatment of the two-dimensional heterogeneity on productivity and the cost of going to work.

To be able to derive the properties of the optimal tax system, we rule out tax schemes that depend on the history of earnings, an assumption which we feel justified by casual observation. This makes our analysis very different from that of Brito et al. (1991) and more recently the dynamic public finance literature; see, for example, Kocherlakota (2005, 2010). These works are interested in the dynamic revelation of information. We stick to a simpler redistributive problem where the nonlinear tax is constrained to be a function of current income. We also do not allow income tax to depend on age, contrary to Weinzierl (2011). Again our justification is casual observation. A natural way to have transfers conditional on age would be to introduce pensions. This is outside the scope of the current article and should be the subject of future work.

The main contribution of the article is our characterization of the optimal tax scheme in this dynamic extensive labor supply environment. Indeed, the optimal tax can be described as the result of a balance between two forces: a redistributive force, holding labor supply constant, and an efficiency force, which comes from changes in labor supply and production. This generalizes the first-order conditions from Laroque (2011). There is a lot of bunching at the optimum: the tax scheme often is piecewise constant, and there are regions where the marginal tax rate is 100%. This is due to the extensive character of labor supply: what is important is whether to work or not to work, the average and not the marginal tax rate. Otherwise the model is too general to lead by itself to definite policy implications. Given the trajectories of the productivity and opportunity cost of work of the dynasties in the economy, given also the tastes for redistribution of the government, our analysis allows to compute the optimal tax schedule. Without further restrictions on the parameters of the economy, the tax schedule however is largely unconstrained. An interesting feature, for policy purposes, is the treatment of low-skilled agents whose labor supply may be distorted downward as in the traditional Mirrleesian intensive models or distorted upward, justifying the American Earned Income Tax Credit (EITC) and the introduction of negative taxes.

We have investigated in more depth, economies with two types of agents. We show that the optimal allocation dramatically changes depending on the source of the heterogeneity. When the agents primarily differ by their opportunity costs of work, the income tax schedule solves a standard equity/redistribution trade-off with each of the two types of agents having their labor supply distorted downward. By contrast, when the agents primarily differ through their productivity, the tax schedule is used to subsidize low-skilled work, and hence generates upward labor supply distortions. The logic at work is reminiscent of Choné and Laroque (2011). Here, however, the mechanism comes from the low-skilled agent being the only one working at low productivities, due to the form of her life cycle trajectory, rather than to the shape of the distribution of the social weights in the population.

The article is organized as follows. Section 2 presents the model. Section 3 deals with optimal taxation, introducing the efficiency and redistributive forces. Finally, Section 4 studies in detail the properties of optimal tax in the case where there are two types of agents in the economy.

2. Model

The type of an agent is thus characterized by a couple of exogenous, nonnegative functions defined on and by the instantaneous utility index . The pair as the age a varies determines a curve in the space, which we call a ‘trajectory’. We assume that the functions , and are differentiable. The economy potentially exhibits a lot of heterogeneity.

At each date t, for each i in I, the economy contains a continuum of agents of type i of all ages a in ; overtime the older agents die and are replaced by newborns of the same type. Cohort i has size , with normalized to 1, and the economy is stationary. An ‘allocation’ specifies the nonnegative consumption and the labor supply in {0, 1} of all types i along their lives.

Furthermore, we assume that there are perfect financial markets for transferring wealth across time, with a zero interest rate. The agents use these markets to smooth their consumption overtime, independent of age. From now on, we restrict our attention to allocations where consumption is constant and equal to its aggregate value over the lifetime .

2.1 Feasibility

2.2 Utilitarian optimum (first best)

2.3 Laissez-faire

‘In all of the article we suppose that the utilitarian government observes the employment status of the agents and, when they work, their productivity w. It never observes the pecuniary cost δ, which is private information.’

2.4 Income tax

We study redistributive taxation in a setup where the tax schedule is assumed to be age independent and time invariant. The tax schedule is made of a function R(w), the after-tax income of a worker with before tax wage w, and of a scalar s equal to the subsistence income of the non-workers.

2.5 Second-best program

3. Optimal Income Tax

When an agent has productivity w at some date, her financial incentive to work is equal to , which is to be compared with the opportunity cost of work δ. It is useful to represent the financial incentive to work in the same plan as the individual trajectories . Hereafter, the ‘incentive schedule’ is the curve as productivity varies. An agent works in regions where her trajectory is located below the incentive schedule, that is, her opportunity cost of work δ is smaller than the financial incentive to work . Her work status changes at points where her trajectory crosses the incentive schedule.

The Lagrangian depends on the tax schedule through two channels: consumption levels and labor supplies . Hereafter, we label ‘redistribution force’ and ‘efficiency force’ the effect of R through these respective channels. The first force is present at all productivity levels, while the second is active only at points w where an agent is indifferent between working and not working. Formally, we compute the Fréchet derivatives of the Lagrangian of the government problem, seen as a functional that maps the set of functions R into . To this aim, we evaluate the Lagrangian at a slightly perturbed function , compute the ratio , and let tend to zero. A mathematical derivation of the limit can be found in Appendix A. Here we present a heuristic approach of the differentiation.

3.1 The redistribution force

By construction, is a nondecreasing function of w. The limit of as w goes to infinity is the total time agent i works over her life cycle, hereafter denoted .

The derivative of with respect to w, , is a positive measure which is almost everywhere continuous, possibly having mass points at productivity levels where agent i spends non-infinitesimal periods of time. If we think of agent i’s productivity when she works as a random variable, the probability measure can be thought of as the distribution of that random variable. Suppose agent i’s trajectory crosses the incentive schedule from below at w0, that is, the agent works for and does not work for along the trajectory. Then has a downward discontinuity at w0, and has a concave kink at w0. If the trajectory crosses the schedule from above, then the kink of is convex.

Lemma 1. The net social marginal utility of income of workers with productivity below w, , has the same sign as the correlation between marginal utilities and working times .

3.2 Labor supply elasticity

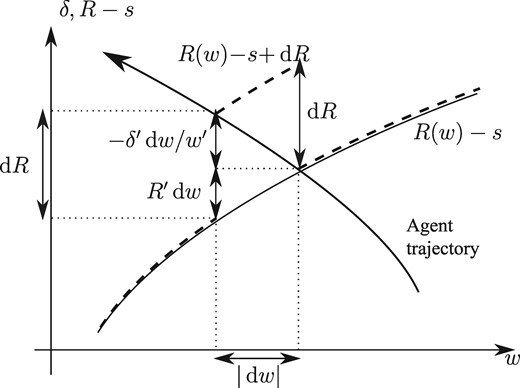

Labor supply elasticity. Original (perturbed) schedule: solid (dashed) line.

3.3 The efficiency force

Raising R at an indifference point increases labor supply, which alleviates the government budget constraint if and makes it more stringent if . Hence, income maximizing pushes the government to raise (lower) after-tax income in regions where (). This force translates into mass points in the derivative of the Lagrangian or even into discontinuity points in the Lagrangian function.

On the other hand, the redistributive force, expressed in the term (7), is absolutely continuous (except at productivity levels where some workers spend a finite time): the redistributive effect of an increase in the after-tax income on an interval of productivities is the integral on the interval of the net social marginal utility of income .

3.4 Finite number of types

The above analysis allows to concentrate attention on a particular class of tax schedules when I is finite:

The proof is in Appendix B. When the tax schedule coincides with an increasing trajectory, the government faces a particularly strong efficiency force.2 Otherwise, the monotonicity constraint binds. Putting the signs of and on the diagram of trajectories allows to qualitatively separate intervals of productivities where the redistribution and efficiency forces tend to push R up from those where these forces are downward.‘When the number of types is finite, the second-best optimum may be implemented with an incentive schedule that is piecewise either constant or coincident with an increasing trajectory.’

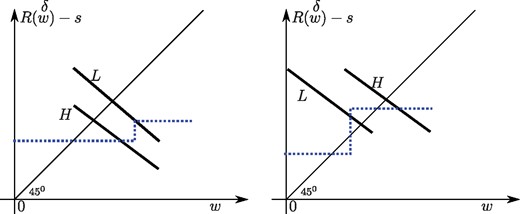

4. An Example: Two Types and Decreasing Trajectories

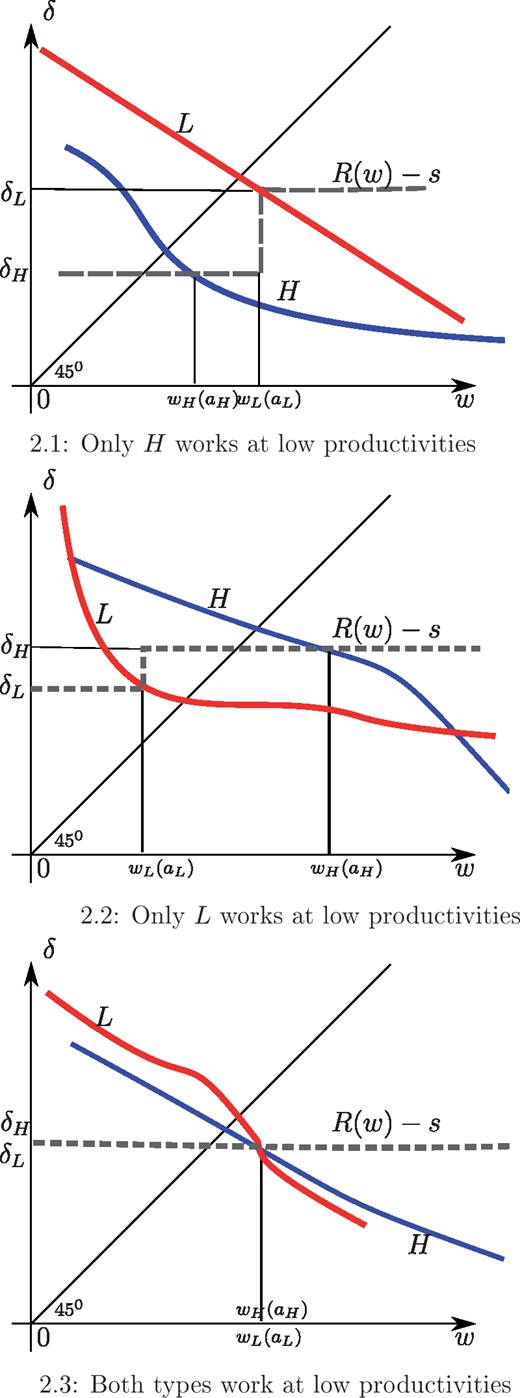

The three cases of Proposition 2.

Assumption 4.1 (Decreasing trajectories). The two agents have the same utility functions u. Their productivities, , decrease with age and their pecuniary costs of work, , increase with age. There exist ages and in (0, 1) such that and .

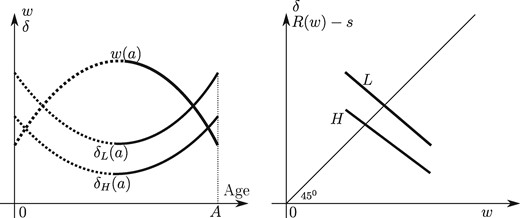

Two types, same productivities.

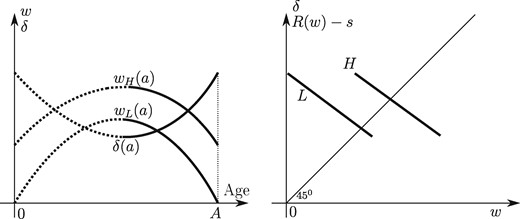

Two types, same opportunity costs of work.

Proposition 2. Under Assumption 4.1, the following properties hold:

There exists an optimal tax schedule with at most two values;

Agent H has her labor supply distorted downward;

Agent L labor supply can be distorted in any direction or undistorted;

Agent H retires later and enjoys higher lifetime consumption than agent L:

Example 1 (Same productivities, different opportunity costs of work). In addition to Assumption 4.1, suppose that the agents are equally productive, for all a, while agent H has a lower pecuniary cost of work: for all a. Then at the optimum, both agents have their labor supply distorted downward.

Example 2 (Different productivities, same opportunity costs of work). In addition to Assumption 4.1, suppose that the agents have the same pecuniary costs of work, for all a, while agent H is more productive: . Then at the optimum, agent L has her labor supply distorted upward.

The optima with same productivities (left), same opportunity costs of work (right).

In Example 2, we must be in case (2) of the proof of Proposition 2. Moreover, the configuration where the tax schedule is flat is not possible here. Indeed, the equality would imply aL = aH, meaning that the two agents would have the same total working time: a uniform increase of R − s would thus have no redistributive effect and a positive efficiency effect at —a contradiction. The optimal schedule is therefore discontinuous at as shown on the right panel of Figure 5.

In Example 1, the heterogeneity primarily comes from the opportunity cost of work, while in Example 2, it comes from the productivity. In both cases, the government cannot implement the first best in these two-type economies. The direction of the distortions, however, is sensitive to the source of the heterogeneity.

1 Suppose that is a disutility cost instead of a pecuniary one, i.e. agent i, when working, produces and has instantaneous utility , while she has instantaneous utility when not working. Then agent i works at age a under laissez-faire if and only if , where is her constant, instantaneous consumption level. Hence, this specification entails an ‘income effect’ in labor supply: participation decreases with . Using Pareto-optimality conditions, it can be checked that laissez-faire is efficient. The pecuniary model adopted in this article avoids these complications.

2 See the last paragraph of Appendix B.

3 A referee has asked us to what extent the results below can be generalized. We certainly can have more than two types. But the monotony and ranking of the dynasties are an essential element of the argument.

4 In other words, the Lagrangian is locally discontinuous in productivity regions where the tax schedule is locally tangent to a trajectory, see Appendix A.2.

5 The first-order conditions imply that the net social marginal utility of income, , is identically zero on and that at any switch point in this region.

Appendix

A. Proof of Proposition 1

A.1 Derivative of lifetime consumption and redistribution force

A.2 Labor supply elasticity and efficiency force

Labor supply is changed under the perturbed schedule only if the support of h contains switching points. For ease of exposition, we assume that the support contains only one switching point, that we denote by . We denote by i the switching agent and by the age at which agent i switches at . We have: and . To fix ideas, we suppose that both and are positive and that the slope of the indifferent agent’s trajectory is larger than the slope of the schedule: .

We use the same method to compute the Fréchet derivative of the term . The only difference with the above analysis is the presence of the multiplicative term , which, at , is equal to , given that is a switch point. This yields (12) and (13).

Discontinuous Lagrangian

Consider an indifference point w such that the incentive schedule is locally tangent to the indifferent agent’s trajectory. (In other words, we have: .) Then the Lagrangian is discontinuous at w, as an infinitesimally small increase in R implies a non-infinitesimal change in the Lagrangian. In other words, the efficiency force is particularly strong, creating a discontinuity in the Lagrangian, whose sign is the same as that of . This is in particular the case where the tax schedule locally coincides with an agent trajectory.

B. From Increasing to Piecewise Constant Schedules

Lemma B.1 Let R be any nondecreasing tax schedule. Let be such that none of the agents’ trajectories , , intersects the rectangle . Assume that the functions have at most finitely many discontinuity points.

Properties of the optimum when there is a finite number of types Consider an interval where the schedule is increasing. The schedule can locally coincide with an increasing trajectory, in which case efficiency and redistribution play in opposite directions: the schedule is slightly below the trajectory if and , slightly above if and . For instance, in the former case, lowering (raising) R entails an infinitesimal (a non-infinitesimal) fall in the Lagrangian through the redistribution (efficiency) effect.4

Now consider an interval where the schedule is increasing and does not coincide with an increasing trajectory.5 By compactness of , there exists a finite sequence such that no trajectory crosses the rectangles . On each interval , we apply Lemma B.1 and replace R with a piecewise constant schedule that takes its values in and leaves the government revenue and the agents’ lifetime consumption and labor supply unchanged.□

C. Proof of Proposition 2

Proof. The inequality aH > aL follows from the ordering and the monotonicity of the functions . This inequality, in turn, implies cH > cL and .

We now consider three cases in turn:

Agent H is the only one working at low productivities, ;

Agent L is the only one working at low productivities, ;

Both agents work at low productivities, .

To examine agent L’s labor supply, we suppose first the tax schedule is continuous at , that is, . In this case, the after-tax schedule takes only one value for , namely the common value of , and agent L’s labor supply is distorted downward because is larger than . We consider now the case where the schedule is discontinuous at . We know that R − s is flat and equal to above that point. We can therefore consider a transformation that pushes R − s down from to just above . The redistribution and efficiency effects of the transformation respectively bear on type H and type L. The former is positive and of the sign of since it takes from type H while leaving L’s lifetime consumption level unaffected. The latter is of the sign of . For them to sum up to zero, we must have : agent L’s labor supply, again, is distorted downward.

In case (2), we have . We deal separately with the situation where the two agents have the same opportunity costs when they stop working, and when that of H is larger than that of L. Suppose first that . Then the financial incentive to work is equal to that common opportunity cost for all . The efficiency force cannot be downward at as this would violate the first-order condition on the bunching interval starting at (in practice, the government would slightly decrease the after-tax income at ), hence : agent H’s labor supply is distorted downward.

Suppose now that . Since and only agent L works at productivities lying between and , the redistribution force pushes upward and the financial incentive to work R − s equals in that interval. The tax schedule, therefore, is discontinuous at and equal to above that point. Consider the perturbation that moves the discontinuity point in the tax schedule slightly to the left while maintaining . This perturbation, which does not affect agent H, increases agent L’s labor supply and consumption. Consumption is increased by a first-order quantity because the agent receives positive extra income during a small time interval, hence a positive redistributive effect. The efficiency part of the perturbation is a change in the Lagrangian of the sign of . Expressing that the latter must outweigh the former, the first-order condition on R in the bunching interval yields , an upward distortion in L’s labor supply.

Finally, we consider case (3), denoting by the common value of and . We first show that the tax schedule necessarily intersects the two trajectories at the same point: and must be equal. Suppose for instance that . A small increase in after-tax income below would put agent H to work on a small time interval of length . Similarly, a small decrease in after-tax income above would put agent L out of work on a small time interval of length . These transformations have redistribution effects that are of the second order. Choosing and such that , we find by (12) that the associated changes in the Lagrangian would be respectively and . The sum of these two quantities would be of the sign of , therefore positive, implying that one of the above changes would increase the Lagrangian through the efficiency force—a contradiction. A similar contradiction is found if , hence the announced equality.

The tax schedule is flat above . A slight decrease of its constant level has a positive redistribution effect, and must therefore have a negative efficiency effect, implying that both agents have their labor supply distorted downward.

Acknowledgements

This work has benefited from the financial support of the European Research Council under grant WSCWTBDS. It has been presented at numerous conferences, in Amsterdam, Koln, London, Lugano, Marseille, Munich, Nashville, and Uppsala. We are most grateful for the comments of Felix Bierbrauer, Sören Blomquist, Monika Buetler, Mikhail Golosov, Jean-Baptiste Michau, Panu Poutvaara, Nicola Pavoni, Richard Rogerson, Tom Sargent, Laurent Simula, and Eytan Sheshinski.

{kind=link}

{kind=link}

{kind=link}

{kind=link}